Merger & Acquisitions Corporate Restructuring. Sanjeev... · Tax advantages. 7 Agenda Background...

25

1 Merger & Acquisitions Corporate Restructuring Sanjeev Bafna April 2010

Transcript of Merger & Acquisitions Corporate Restructuring. Sanjeev... · Tax advantages. 7 Agenda Background...

1

Merger & Acquisitions

Corporate Restructuring

Sanjeev Bafna

April 2010

2

Agenda

Background

Aspects of a Deal

Cases

3

Agenda

Background

Aspects of a Deal

Cases

4

Economic Reforms: Journey 1991-2009

Period Pre 1991 1991-1997 1998-2003 2004-2009

Economic Indicators

GDP/ p.a. (USD Bn) 250 375 600 1,100

GDP Growth (%) 3-5% 4-7% 4-6% 7-9%

Country Rating BB+ / Ba1 BBB-/Ba3

Forex Reserves (USD Bn) 4 4-26 26-76 80-280

Balance of Payments (USD Bn) Crisis situation 2-7 (surplus) 8-10 (surplus) 16-55 (surplus)

Fiscal Deficit (% of GDP) 7.5% 5-7% 5-6% 3.5-7%

Tax collections (% of GDP) 10.5% 9.5% 8.5-9% 10-12%

Tax Rates 54% 52-46% 43-36.75% 33.60-33.99%

Exchange Rate INR/USD < 20 30-35 35-49 39-52

Sensex 700 1,000-3,500 3,500-4,500 5,000-22,000

Market Cap (Rs Crs) 65,000 5,00,000 6,00,000 50,00,000

M&A (USD Bn) 22

FDI Inbound (USD Bn) Negligible 2-3 4-5 6-42

Portfolio Investment (USD Bn) Negligible 2-3 2-3 10-20

5

India Story

Outward FDI

Developed country phenomenon till 1980s;

Developing economies’ share increased from 5% to 20% in two decades

Emerging to developed countries (E2D) on the rise

India

Cumulative outward FDI from USD 0.5 bn in 2005 to USD 62 bn in 2008

Outward FDI stands at half of the inbound FDI (USD 123 bn)

Bharti – Warid, Zain (USD 11 bn)

Scale/Market Presence

Tata- Chorus (EUR 8.5 bn)

Tata- JLR (USD 2.3 bn)

Brands/Technology/Assets

ONGC–Imperial (GBP 1.4 bn)

Essar - Trinity Coal (USD 600 Mn)

Raw Material

UB–Whyte & Mackay(GBP 600 Mn)

GMR- Intergen (USD 1.1 bn)Hindalco – Novelis (USD 6 bn)

Suzlon – REpower (EUR 1.3 Bn)

Renuka - Equipav (USD 300 Mn)

Reddy – Betapharm (EUR 480 Mn)

Recent Acquisitions

6

Why M&A – inorganic route

Forward & backward integration-value chain

Enlarging the geographical area/Size of operation – Economies of Scale

Product lifecycle quadrant

Consolidation in the market

Diversification

Emerging market opportunities

Brand Acquisition

Attractive valuations

Extent of leveraging

Operational leveraging

Financial leveraging

Tax leveraging

Business barriers

Knowledge base & technical know how

Tax advantages

7

Agenda

Background

Aspects of a Deal

Cases

Valuation methodologies

Structuring

Regulatory issues

Tax implications

Transaction costs

Post deal challenges

Due-diligence

8

Valuation Methodologies

DCF valuation

– for rigorous analysis, sensitivities

Multiples – EV/EBITDA, PE (EPS) etc

for quick and easy reference of pricing available in the market

Asset Based Valuation

cement, real estate or other capital intensive sectors

Sector specific multiples

Rs crs per MW, ton of cement production, hotel room, telecom tower etc.

Range of the valuation

optimistic and pessimistic, for negotiation purposes

Additional cash flow due to synergies arising in case of mergers

9

Structuring

Financing

Debt Equity ratio – bases on industry benchmarks, profitability, bankability

Bridge loan, Mezzanine/Subordinated Debt, Overseas– ECB, FCCBs etc

Share exchange, part cash and part share

Management Control

Shareholder Agreement – RoFR, Anti dilution, Drag along, Tag along rights,

deadlock provisions, Board representation (in JVs, PE investment)

Indemnities for known risks, brand transfer etc. in the Agreement

Forming an SPV

Tax implications in different jurisdictions on dividend, interest income, capital

gain, operating income, etc

o Mauritius (incorporation status GBC I & GBC II differ in tax benefits) , DTAA

o Singapore (DTAA & FTAs, tax incentives in shipping)

o British Virgin Islands (negligible taxes)

10

Regulatory Issues

Regulatory bodies

SEBI - listing requirements – duration of the whole process, open offer

RBI – debt financing, banking guidelines, ECB restrictions

Cross border related

FEMA – cross border transactions – RBI & SEBI both

FDI norms – sectoral limits

o Comes under Deptt of Industrial Policy & Promotion (DIPP) and Ministry of Commerce and Industry

Regulations of Target country in case of cross-border acquisition or listing

Sector specific

Concerned Department/Ministry – DoT, Ministry of Communications & IT etc.

Others

Accounting standards, Competition Act 2002

11

Tax Implications

Foreign multinationals merge, employee at Indian Subsidiary has ESOP (of

foreign parent company), TAX ?

Indian law provides exemptions for exchange of Assets in the event of merger. Is

this exemption available for shares held in such foreign companies?

Is exemption available if consideration is received in the form of;

o Shares and Cash; Shares and Bonds; Preference shares for Equity shares or vice versa

Implications under Sec 43B and 40(a)(i) when taxes are unpaid by the

amalgamating company and subsequently paid / deducted by amalgamated

company ?

Does the foreign merger have to comply with the conditions of Section 2(1B) ?

Whether MAT credit is allowable in the hands of Amalgamated or Resulting

Company?

Meaning of ‘undertaking’ under Section 2(19AA). Whether investments in various

group companies of an investment holding company would qualify as

‘undertaking’ for the purpose of Section 2(19AA)?

How is the taxation in case acquisition price is settled by way of share swaps?

12

Due- Diligence

Financial, Legal & Tax related, Technical

Potential liabilities

Warranty issues, Environmental, patent infringements, lawsuits, pending

regulatory issues

During interaction

Be Commercial

o Talk Financials only

o Allow business partners to take informed commercial decisions,

o Focus on big ticket items,

o Do not expect 100% clear data

Be prepared to know

o To know what to ask for, What to look for, What to deliver to whom and How to get there

13

Transaction costs

Fess of constituents Investment banker, Legal advisor,Foreign Lawyer, Valuers, due

diligence, Bankers charges,Technical consultants,

Stamp Duty As high as 15% in many states, Max cap in some states, The relevant

law differs from state to state.

Income Tax Carry forward of business losses/depreciation, determinants of block for

IT depreciation, Sec 14A disallowance, amortisation, Sec 80IA deduction

disallowance, Goodwill disallowed

Regulatory consents SEBI, RBI, Companies Act, concerned GoI Dept, Competition Act

Controlling Interest

Premium

Premium may differ upon the % of controlling to be acquired

- 51% for management control

- 76% for ability to carry through special resolution-useful in M& A /

transfer of - business or assets

- 90% for delisting the company

Estimated time for

completion of entire

transaction

Loss of interest, manpower cost, opportunity loss etc

Experienced advisors play a crucial role

14

Integration of Target company

- Business dynamics

- Growth Strategy

Increased Profitability - Effective cost

- Tangible results

Acquisition funding

Lag in gain realisation

BV-$50 pt

Replacement cost $75

MV of all assets $ 125

EV $ 150

The return has to be on EV + Other incidental costs

15

Post Deal Challenges

Operational

Integration of Operations, MIS

Performance uncertainty

Financial

Accounting issues –Amortization of goodwill

Settling hidden liabilities/losses

Managerial

HR & Cultural Integration

Effective communication with all stakeholders

Displacements of leadership teams and turnover

Collusion & Cartelization – Short Term Impact

16

Agenda

Background

Aspects of a Deal

Cases

17

Company XYZ

Size of deal Stakes were small High

Vendor settlement Difficult Complicated

Time lag Minimal Stretched

Valuations Due to depressed

market the eventual

cost has gone up

Attractive as per

current valuations

Rationale for

acquisition

Foot hold in state Consolidation of

operations

Acquirer Small Player Big Player

18

Arcelor - Mittal

Motivations for Mittal

Leadership position in premium segment in Europe with strong R&D capabilities

Low Cost slab-manufacturing in Brazil.

Distribution network in Europe

Flat products

Motivations for Arcelor

Leadership position in Premium segment in the US.

Access to Raw Materials & upstream integration

Low cost slab manufacturing in Ukraine.

Long Products

19

Arcelor - Mittal (contd..)

Jan 27, 2006

4 new company shares and cash of € 35.25 for every 5 shares in Arcelor

4 new company shares and cash of € 40 for every 5 convertible Bondholder in

Arcelor

Minimum 50% of Arcelor shares to be surrendered

75% of Commission to be in form of equity in new company & 25% in Cash

Option to Arcelor shareholders to accept 16 shares for every 15 shares of Arcelor

or receive cash € 28.21 per share fore very Arcelor Share.

Value of firm € 18.6 million

Divident to Arcelon shares holds @ € 1.85 - € 5 Million

Jun 11, 2006

Mittal revised bid value to € 25.8 billion with highs cash component

Deal closed at € 33.5 billion

Takeover Defiance - Setverstal, Russia

20

Arcelor - Mittal (contd..)

Financials(USD Mn)

Mittal Arcelor Total (pre merger) Arcelor Mittal

(post merger)

2005 2006 2005 2006 2005 2006 2007 2008

Revenue 28,132 58,870 38,747 43,493 66,879 102,363 124,936 105,216

EBIDTA 6,056 9,844 6,751 7,790 12,807 17,634 18,336 19,400

Net Profit 3,795 6,086 4,305 4,820 8,100 10,906 10,439 11,850

EPS 4.79 5.28 5.94 6.2 10.73 11.48 6.78 7.41

Net Worth 13,286 42,127 17,713 25,277 30,999 67,404 55,198 56,685

21

Siva Group

Background

USD 3 bn Group promoted by Mr C. Sivasankaran

o a first generation entrepreneur, known for his ability to identify business opportunities well ahead of

others

Diversified business interests

o in sectors like Telecommunications, Renewable energy, Shipping & Logistics, Hospitality & Realty,

Engineering, Food & Beverages

Early mover in broadband and mobile telephony

o Dishnet Wireless & Aircel in 1999

New Ventures

o S Tel (GSM based telecom services)

o WinWinD Oy, Finland (wind energy)

22

Aircel - built and divested

Growing telecom business

Acquired licenses in 1997 to operate in Rest of Tamil Nadu (RoTN) Circle

Launched services in RoTN at revolutionary rate of Rs 1 per 3 minutes in 1999

Became leading operator in Tamil Nadu within 18 months

Acquired RPG Cellular and entered Chennai circle and became leader in 2003

Applied for licenses for 10 B & C circles in Northern and Eastern India;

o Obtained 7 licenses and launched services in 3 circles by end of 2005

Divestment

Sold Aircel to Maxis Communications for a Enterprise value of USD 1.08 bn

Amount invested - ~ USD 110 Mn with weighted average period of ~ 4.2 years

Return on Investment – 60.4% p.a

23

Barista – bought and divested

Acquisition

Acquired 65% in Barista Coffee Company Ltd in April 2004

Balance 35% acquired during later part of 2004

Operated

Incurring losses when acquired due to high rentals, wastages etc

Post acquisition, systems and processes were refined to improve efficiencies

Clubbed with Fresh & Honest, an in-house coffee vending machine business

Divestment

Sold to Lavazza, an Italian Coffee major, in a packaged deal for EV of Rs 207

Crs in 2006

Amount invested - Rs 128 Crs for a weighted average of 1.6 years

Return on Investment – 27.0%

24

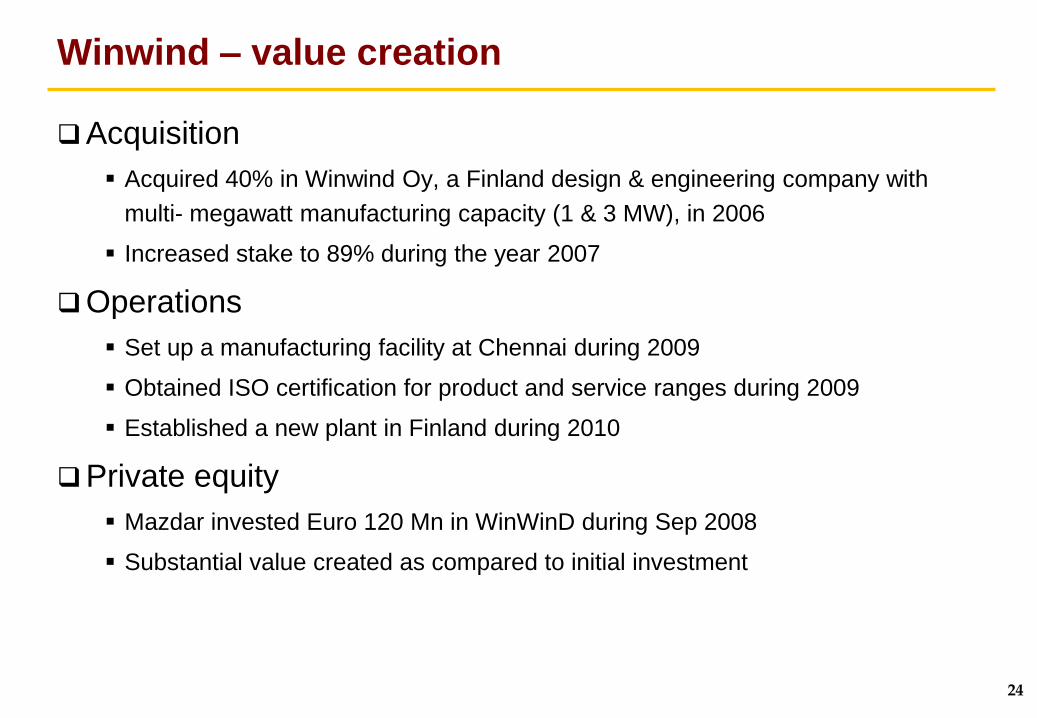

Winwind – value creation

Acquisition

Acquired 40% in Winwind Oy, a Finland design & engineering company with

multi- megawatt manufacturing capacity (1 & 3 MW), in 2006

Increased stake to 89% during the year 2007

Operations

Set up a manufacturing facility at Chennai during 2009

Obtained ISO certification for product and service ranges during 2009

Established a new plant in Finland during 2010

Private equity

Mazdar invested Euro 120 Mn in WinWinD during Sep 2008

Substantial value created as compared to initial investment

25

Q&A