MEMA Financial Services Group, Inc. 2015 Educational Seminar … MFSG Educational... · MEMA...

175

MEMA Financial Services Group, Inc. 2015 Educational Seminar Sponsored By Kane, Russell, Coleman and Logan PC Commitment. Performance. Results

Transcript of MEMA Financial Services Group, Inc. 2015 Educational Seminar … MFSG Educational... · MEMA...

MEMA Financial Services Group, Inc.2015 Educational Seminar

Sponsored By

Kane, Russell, Coleman and Logan PCCommitment. Performance. Results

MFSG 2015 Educational SeminarAgenda

8:10 am – 9:15 am Tackling B2B Transaction Complexity-Dave Lindeen and Russell Bogan of Corcentric

9:15 am – 9:35 am Networking Break

9:35 am – 10:45 am State of the Motor Vehicle Industry–Dave Andrea of Original Equipment Suppliers Association (OESA)

10:45 am – 12:15 pm Customers that Go Dark and Credit Applications – Joe Coleman and John Kane of Kane, Russell, Coleman & Logan PC

MFSG 2015 Educational SeminarAgenda

12:15 pm – 1:15 pm Networking Lunch – In Cultivate Restaurant

1:15 pm – 2:30 pm Supply Chain Financing – Bob Scott of SunTrust Robinson Humphrey

2:30 pm – 2:50 pm Networking Break2:50 pm – 4:00 pm Ask the Attorneys – Joe Coleman and

John Kane of Kane, Russell, Coleman & Logan PC

4:00 pm – 4:10 pm Closing Comments

MFSG 2015 Educational SeminarRequests

• Please silence all cell phones• If you must make or take a call, please leave the room• Limit side conversations during presentations• Please ask questions to make the presentations interactive• Please complete the evaluation form after each speaker and at

the end of the day please leave it at your place and it will be picked up

• Spend the breaks and lunch to network and meet someone you don’t know, it can be exceptionally beneficial

• Have a great time

Tackling B2B Transaction Complexity

Dave Lindeenand

Russell Bogan

Corcentric

Tackling B2B Transaction Complexity

7

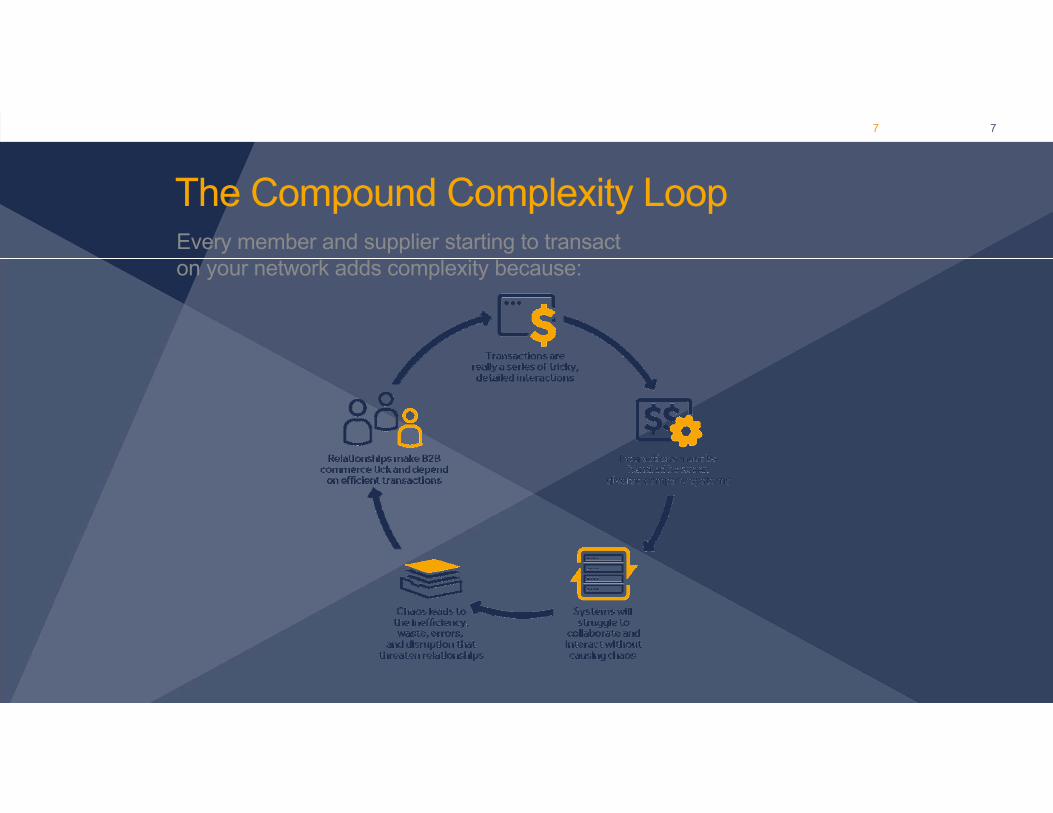

The Compound Complexity LoopEvery member and supplier starting to transact on your network adds complexity because:

7

8

Compound B2B transaction complexity

88

9

You need a transaction model

Our solution: CorConnect

CorConnect:

The Collaborative Transaction

The solution to Compound Complexity means: 1. Fast and easy transactions2. Many systems to one system3. Key shared resources4. Faster access to cash flow5. Win‐Win‐Win for all

12

1. Fast and Easy TransactionsKills errors, silos, and antagonism

13

2. Many Systems To One SystemNormalizes data and reduces complexity

14

3. Key Shared ResourcesWith technology, people, finance, and analytics

15

Managed Credit Risk

16

Transaction Experts: Dispute Management and Resolution

When a dispute halts the flow of business, you need it resolved – fast. Our transaction experts can investigate, communicate, resolve, and report back to you in full.

16

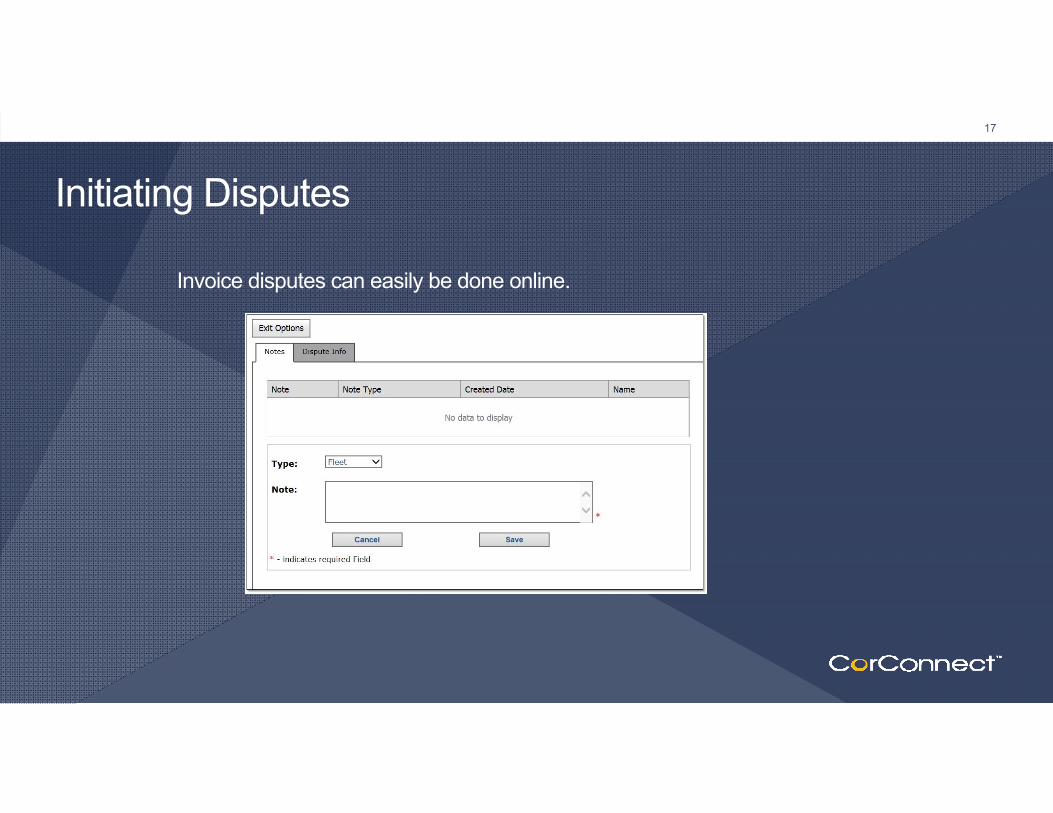

Initiating Disputes

Invoice disputes can easily be done online.

17

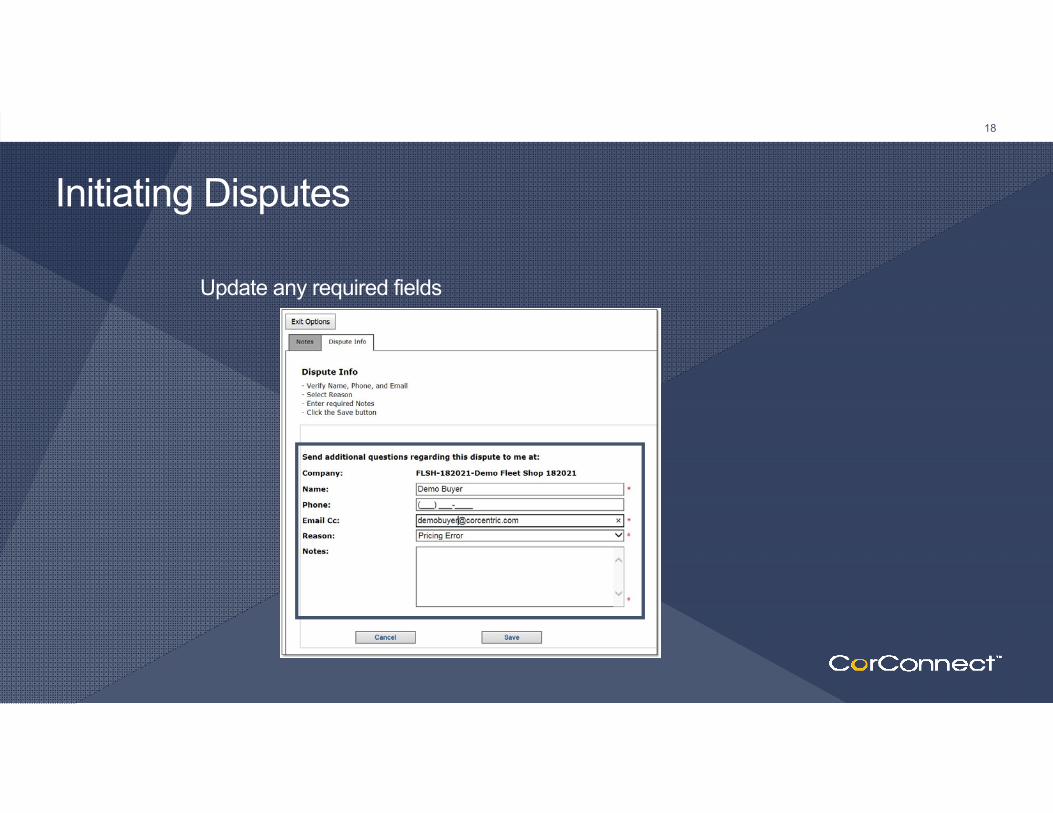

Initiating Disputes

Update any required fields

18

Initiating Disputes

Select the proper reason

19

Initiating DisputesSuccessfully saved dispute info message

20

Quick Tip: When a dispute is initiated an email notification will be sent to the initiator when the dispute is filed and when it is resolved. Even if the user is not setup for Dispute Notifications in their setup.

Dispute Information

Invoice will contain dispute information

21

Unresolved Dispute

22

Resolved Dispute

23

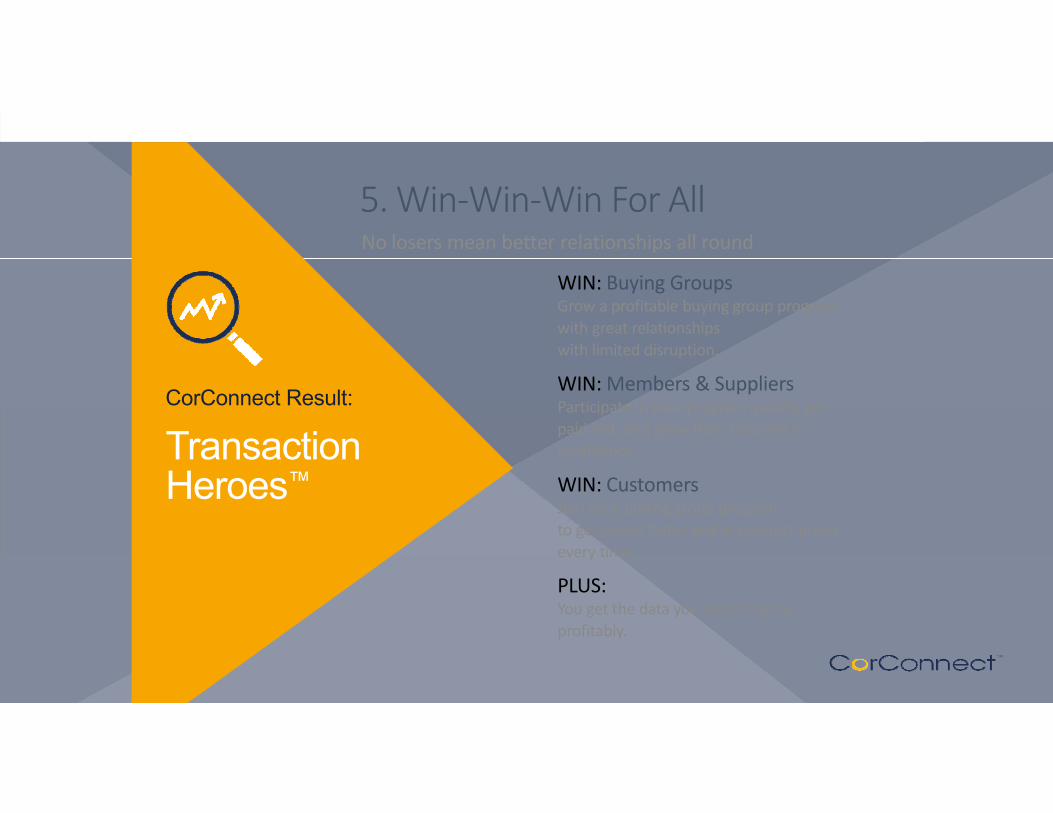

CorConnect Result:

Transaction Heroes™

5. Win‐Win‐Win For AllNo losers mean better relationships all round

WIN: Buying GroupsGrow a profitable buying group program with great relationships with limited disruption.

WIN: Members & SuppliersParticipate in your program quickly, get paid fast, and grow their business in confidence.

WIN: CustomersJoin your buying group program to get goods faster and at contract prices, every time.

PLUS: You get the data you need to grow profitably.

• Purchase Order Processing• Price Verification• Order Acknowledgements• Shipping Notices• Shipment Tracking• Invoicing• Emergency Order Processing‐Out of

Stock Items & Non Stock Items• Price Quotations• Stock Availabilities• Return & Warranty Management• Payments

252525

Transaction Engine: Order Management Finance teams waste time taking calls about when invoices will be paid. And buyers waste time chasing up delivery information.Suppliers and buyers can log in and track their invoices and orders.

Who’s using CorConnect today?

CorConnect today

27

Daimler uses CorConnect to transform billing and support services across dealers and customers.

Case Study #1:

Daimler Trucks North America

28

The system highlights include:

29

The efficiencies have driven major business results in under two years:1. Double-digit revenue increase

2. Increase in new customers signed

3. Increased customer retention

4. Better managed credit risk

5. Decreased operational expenses

6. Better decision making with end-to-end process visibility

30

In summary

Join the likes of Daimler Trucks in choosing CorConnect.

Replace friction, errors, and antagonism with efficiency, financial management, accuracy, and great relationships.

And do it with no disruption to your current business.

In SummaryWith CorConnect you can:

Sound good?

32

Questions & AnswersRuss [email protected]

MFSG 2015 Educational Seminar

• Please complete your speaker evaluation for Dave Lindeen and Russell Bogan and their presentation:

Tackling B2B Transaction Complexity

9:15 a.m. – 9:35 a.m. – Networking Break

State of the Motor Vehicle Industry

Dave Andrea

Original Equipment Manufacturers Association(OESA)

Dave Andrea

Senior Vice President and Chief Economist

OESA – Original Equipment Suppliers Association

MEMA Financial Services GroupEducational Seminar

September 17, 2015

Detroit – Washington D. C.

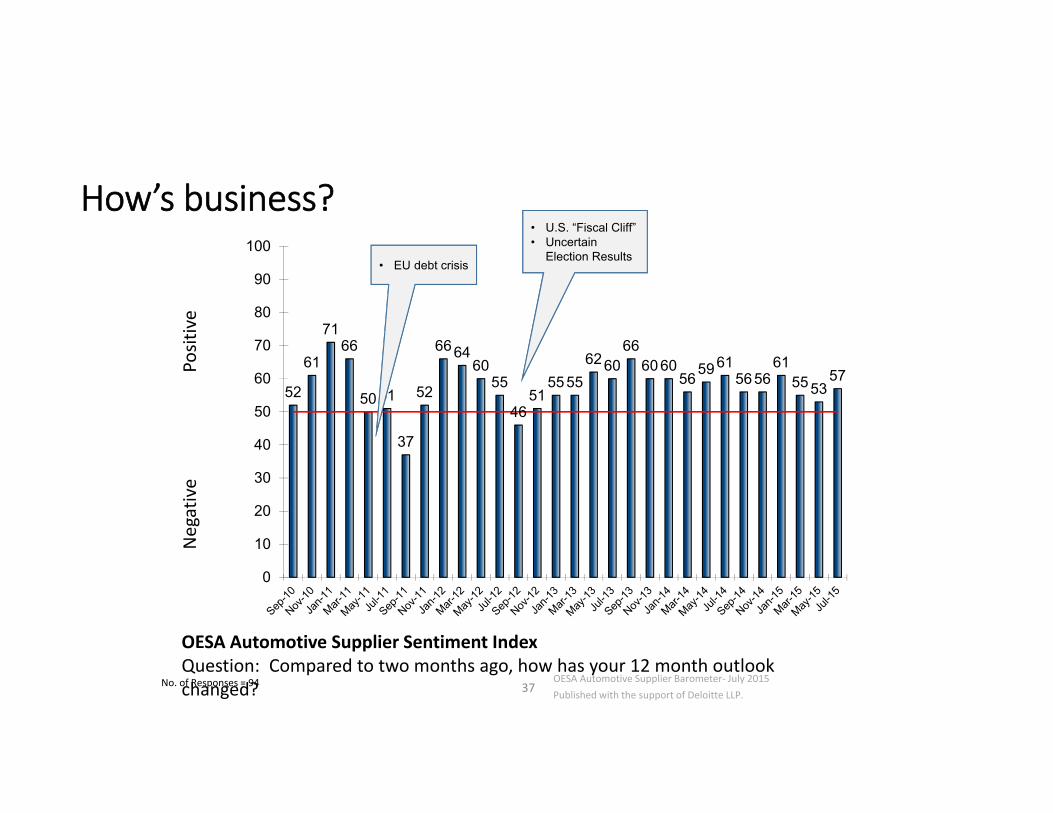

How’s business?Po

sitive

Negative

52

61

7166

50 51

37

52

666460

55

4651

55556260

6660 60

5659615656

615553

57

0

10

20

30

40

50

60

70

80

90

100

37No. of Responses = 94 OESA Automotive Supplier Barometer‐ July 2015Published with the support of Deloitte LLP.

• EU debt crisis

• U.S. “Fiscal Cliff”• Uncertain

Election Results

OESA Automotive Supplier Sentiment IndexQuestion: Compared to two months ago, how has your 12 month outlook changed?

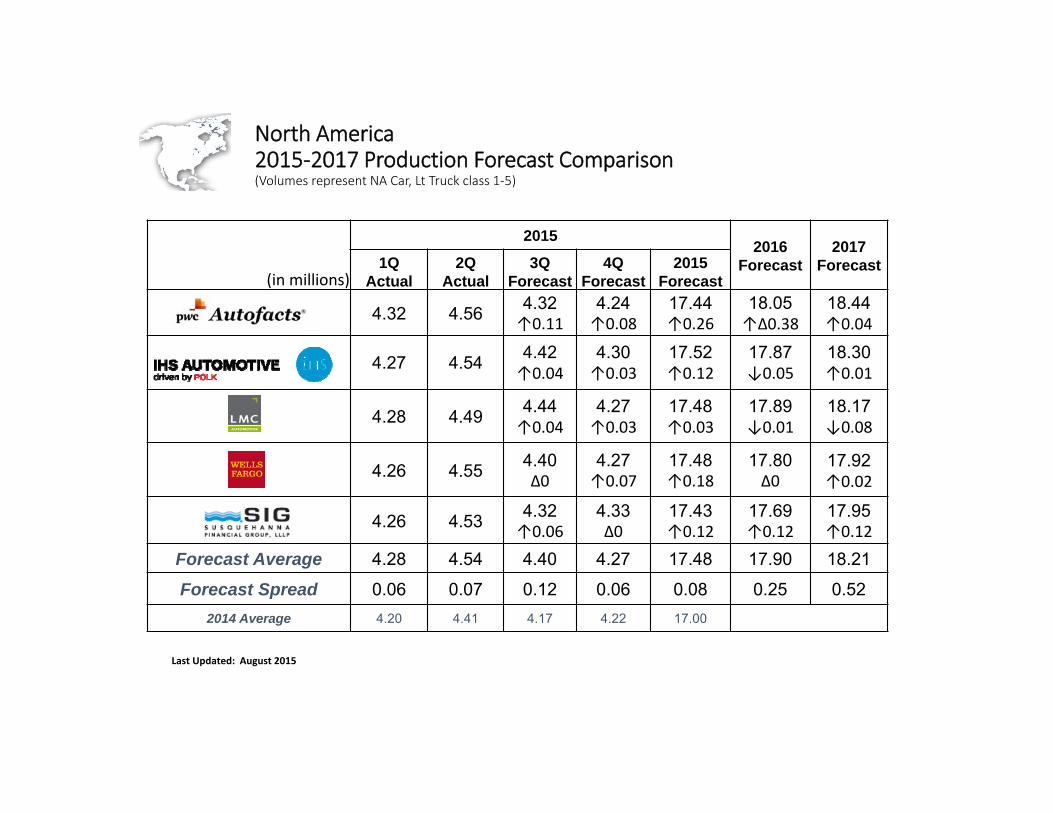

(in millions)

20152016

Forecast2017

Forecast1Q Actual

2QActual

3Q Forecast

4Q Forecast

2015Forecast

4.32 4.56 4.32↑0.11

4.24↑0.08

17.44↑0.26

18.05↑Δ0.38

18.44↑0.04

4.27 4.54 4.42↑0.04

4.30↑0.03

17.52↑0.12

17.87↓0.05

18.30↑0.01

4.28 4.49 4.44↑0.04

4.27↑0.03

17.48↑0.03

17.89↓0.01

18.17↓0.08

4.26 4.55 4.40Δ0

4.27↑0.07

17.48↑0.18

17.80Δ0

17.92↑0.02

4.26 4.53 4.32↑0.06

4.33Δ0

17.43↑0.12

17.69↑0.12

17.95↑0.12

Forecast Average 4.28 4.54 4.40 4.27 17.48 17.90 18.21

Forecast Spread 0.06 0.07 0.12 0.06 0.08 0.25 0.522014 Average 4.20 4.41 4.17 4.22 17.00

North America 2015‐2017 Production Forecast Comparison (Volumes represent NA Car, Lt Truck class 1‐5)

Last Updated: August 2015

39

Millions of Units

8.0

10.0

12.0

14.0

16.0

18.0

20.0

1980 1985 1990 1995 2000 2005 2010 2015 2020

17.3

10.4

16.0

12.3

Trend

Source: Ward’s Automotive and the Federal Reserve Bank of Chicago

Millions

When Do You Think the US Light Vehicle Sales Cycle Will Turn Down?

40Source: Bank of America Merrill Lynch, The Rate Cascade in Automotive, September 14, 2015

Rates Will Go Up . . . But Remember Where We are Coming From

41

L.V. SAAR / Nonfarm Employment

0.050

0.075

0.100

0.125

0.150

0.175

0.200

'67 '71 '75 '79 '83 '87 '91 '95 '99 '03 '07 '11

VPE 12 MMA

Units

Source: Ward’s Automotive and BEA and Federal Reserve Bank of Chicago

Real Fed Mandate: Don’t Kill Employment Expansion

Global Program Launches by Region

17 18 2516

34 2735 40 45 47

26

24 2023

26

3027

2529

28 29

27

2014

2116

1416

2120 19 15

17

21

16

33

31

32

26

32 19

4428

358

5

817

523

2123

33

36

13

0

20

40

60

80

100

120

140

160

180

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

# of Lau

nche

s

North America Europe Japan/Korea China Other

42© 2015 IHS

73

115

169

Increased industry pace places pressure on talent, resources and infrastructure.

Source: IHS Automotive - OESA Sales & Marketing Council | June 2015

43

How are your OEM customer relations?

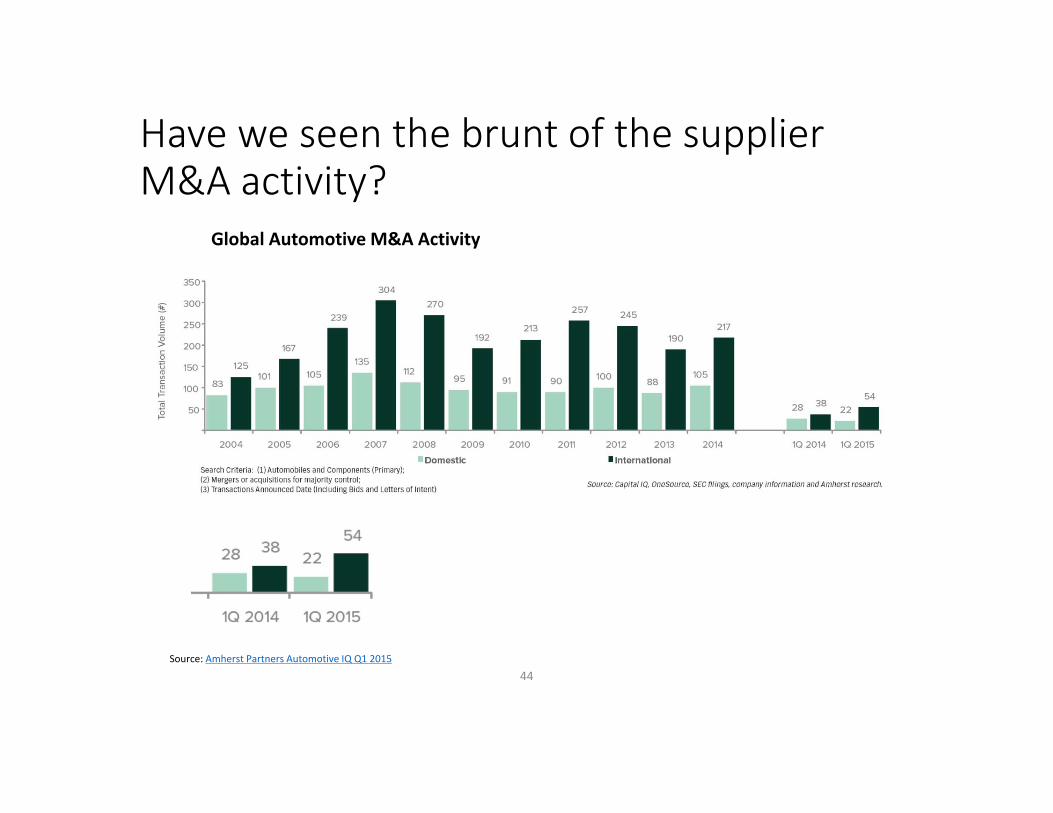

Have we seen the brunt of the supplier M&A activity?

44Source: Amherst Partners Automotive IQ Q1 2015

Global Automotive M&A Activity

Do you think all this connected vehicle talk is real this time?

45

Mcity is a 32‐acre simulated urban and suburban environment that includes a network of roads with intersections, traffic signs and signals, streetlights, building facades, sidewalks and construction obstacles. It is designed to support rigorous, repeatable testing of new technologies before they are tried out on public streets and highways.

The types of technologies that will be tested at the facility include connected technologies –vehicles talking to other vehicles or to the infrastructure, commonly known as V2V or V2I –and various levels of automation all the way up to fully autonomous, or driverless vehicles.

Mcity was designed and developed by U‐M’s interdisciplinary MTC, in partnership with the Michigan Department of Transportation (MDOT).

http://www.dykema.com/assets/htmldocuments/MdASurvey.10.2014.pdf

When are all these recalls are going to end?“Early Warning Reporting” requirements are at the core of the TREAD Act, enabling the NHTSA to collect data, notice trends, and warn consumers of potential defects in vehicles.

SOURCE: Automotive News (*edited by MEMA)

*

3/3/15 OESA Board of Directors

How do you think the Corporate Average Fuel Economy standards will play out?

• Goal: 54.5 mpg (163 grams per mile) for 2025

• LDV Mid‐Term Evaluation

• Joint Technical Assessment Report (TAR)

• EPA, NHTSA, CARB to collaborate and issue by Nov. 15, 2017

• May be moved forward

• EPA Clean Air decision no later than April 1, 2018

• 2015: Auto manufacturers seeking legislation to provide CAFE credits for new safety technology

NAS Light Vehicle Project http://www8.nationalacademies.org/cp/projectview.aspx?key=49432

March 2015 OESA Board of Directors

Where are the UAW – D3 Negotiations Going:Observations after 24 hours• FCA will be the lead company• Counter‐Intuitive Strategy: Pick the weakest company with the hardest negotiator• Consistent Strategy with public relations advertising push and silence on both sides• Biggest UAW question: how to close the $47 per hour average FCA hourly rate with the $55 per hour average GM rate and the $57 per hour Ford rate

• The answer lies in changes to the two‐tier rate of approximately $28.50/hour and $15.80 to $19.28/hour for entry workers . . . In second tier rates, faster grow‐in or lower/equal caps (FCA is at 45% second tier).

• One of D3 top questions: health care consortium for active hourly employees and salaried• Pundits have said with FCA there is a threat of a strike – low risk, UAW has to keep its powder dry . . . if there is it will be a targeted and come up to the edge of Jeep and Ram production, but you don’t loose units when at full capacity; you don’t have any room to catch up and pay year‐end bonuses.

48

Market Growth – production cycles will continue; the US industry needs new capabilities to reach 20 million units

Resource Challenges– will force industry, government and educational to continuously improve productivity of people and capital

Innovation Leads – fuel efficiency, driver assist and connected vehicles will drive need for new personnel skills, production capacities, suppliers and regulations

Public Policy Dynamics– will drive product decisions and shape global manufacturing and engineering footprints

The Next 10 Years Will Make the Last 5 Look Calm

49

Thank You

50

Dave AndreaSenior Vice President and Chief Economist

OESA – Original Equipment Suppliers Association29525 Telegraph Rd.

Suite 350Southfield, MI 48033

248‐430‐[email protected]

Europe2015‐2017 Production Forecast Comparison (Volumes represent EU Car, Lt Truck class 1‐5)

(in millions)

2015 2016Forecast

2017Forecast1Q

Actual2Q

Actual3Q

Forecast4Q

Forecast2015

Forecast

5.36 5.25 4.26↓0.12

5.31↓0.07

20.18↓0.26

20.45↓0.09

21.47↓0.57

5.35 5.36 4.74↑0.19

4.92↑0.13

20.36↑0.60

20.63↑0.42

21.11↑0.28

5.33 5.29 4.72↑0.15

4.96Δ 0

20.31↑0.41

20.83↑0.59

21.67↓0.02

5.43 5.25 4.78↓0.02

5.00Δ 0

20.45↑0.05

20.76↑0.06

21.29↑0.09

5.30 5.23 4.60↑0.04

5.06↑0.04

20.19↑0.13

20.69↓0.04

21.23↓0.02

Forecast Average 5.37 5.29 4.63 5.05 20.33 20.67 21.39Forecast Spread 0.10 0.11 0.52 0.39 0.27 0.38 0.56

2014 Average 5.12 5.22 4.46 4.95 19.74

Countries included in the EU forecast: Austria, Belgium, Czech Republic, Finland, France, Germany, Hungary, Italy, Netherlands, Poland, Portugal, Romania, Russia, Slovakia, Slovenia, Spain, Sweden, Turkey, United Kingdom.

Last Updated: August 2015

MFSG 2015 Educational Seminar

• Please complete your speaker evaluation for Dave Andrea and his presentation:

The State of the Industry

Customers That Go Dark and

Credit Applications

Joe Colemanand

John Kane

Kane, Russell, Coleman & Logan, PC

CUSTOMERS THAT “GO DARK”

Joseph M. ColemanJohn J. Kane

Kane Russell Coleman & Logan PCSeptember 17, 2015

CUSTOMERS THAT “GO DARK”

OVERVIEW• Customers can go out of business without bankruptcy, ABC or other formal proceedings

• Legal Issues and Remedies• Cost‐Effective Strategies

What Causes a Customer to GoOut of Business?

•No Bankruptcy?

•No Assignment for the Benefit of Creditors?

•Maybe no notice?

•What is your experience with “Going Dark” Customers?

What Causes a Customer to GoOut of Business?

•What Causes a Customer to Go Out of Business without Bankruptcy, ABC, Notice, …? Wind Down Business Bank Foreclosure Sale Change Nature of Business

•Wind Down

What Causes a Customer to GoOut of Business?

•Wind Down Business loses key customer(s) Regulatory problems make continuing

business operations unfeasible Key officer disability Significant changes in the market or business Other?

What Causes a Customer to GoOut of Business?

•Bank Foreclosure Common problem with smaller troubled

businesses Owners cooperate? Why? Who receives notice? What happens to unsecured suppliers? How is a foreclosure sale accomplished?

oPublic SaleoPrivate Sale

What Causes a Customer to GoOut of Business?

• SaleWhy sell outside of Bankruptcy?

oAustin CompanyoBenefits of BankruptcyoCons of Bankruptcy:

1. Cost2. Oversight3. Destruction of Business, Customer

BaseBoard of Directors’ Responsibilities

What Causes a Customer to GoOut of Business?

•Change Business Model From purchase and sale of inventory to sales rep business Internet instead of “hard asset” model From manufacturing to outsource production and selling finished goods Shut down divisions/operating units

•Other?

What Causes a Customer to GoOut of Business?

•What Are Some Early Warning Signs?

What Causes a Customer to GoOut of Business?

Changes in upper management Layoffs at the company Customer has been put on hold by bank

and trade references Collection calls go unreturned Promises of payment don’t result in

payment Customer begins to dispute pricing

What Causes a Customer to GoOut of Business?

Customer request copies of all open invoices

Customer’s A/R over 90 days is increasing Customer’s financial statements are

inaccurate or constantly being adjusted Changes to corporate structure Dividends/repay loans to insiders

• Early Warning Signs

• Early Warning Signs

What Causes a Customer to GoOut of Business?

Balance of inter‐company accounts dramatically changing

Payables that are guarantied are being paid ahead of other payables

Change of product lines Efforts to raise capital (bonds, foreign S‐1,

bank debt with warrants, etc.)

LEGAL ISSUES AND REMEDIES • Due DiligenceContacting the customerSales repUCC and Secretary of State searchMEMANoticeOthers?

• Depending upon what your customer is doing directly impacts your rights and remediesForeclosure v. Sale: very different impact upon unsecured suppliersQuickly obtaining information and examining remedies important

LEGAL ISSUES AND REMEDIES • Immediate UCC Remedies for Suppliers: UCC 2‐705 Stop Goods in TransitUCC 2‐702 Reclamation

• Other Legal Strategies:Temporary Restraining OrderWrit of AttachmentUnderlying Lawsuit: Fraudulent Transfer, Corporate Denuding, Breach of Fiduciary Duty, Collection Action Involuntary Bankruptcy

LEGAL ISSUES AND REMEDIES

• Potential Remedies—depending upon the circumstances (due diligence is important)Bulk Transfer lawsFraudulent ConveyanceAttack Foreclosure SaleD&O ActionSuccessor LiabilityInvoluntary Bankruptcy

LEGAL ISSUES AND REMEDIES

•Bulk Transfer LawsThe Origin of Bulk Transfer Laws

o In the mid‐20th century, Fraudulent Transfer laws were too onerous in what they had to prove, i.e. bad faith and insufficient consideration.

oOwners could sell the majority of their inventory outside the ordinary course of business to defeat the claims of creditors who sought to seize goods to satisfy debts.

oBulk Transfer laws were enacted to protect suppliers from this abuse.

•Notice to Creditors of Bulk Transfer

LEGAL ISSUES AND REMEDIES

•Notice to Creditors of Bulk TransferSeller must notify (via local newspaper, county Recorder, and direct mail) creditors at least 12 days prior to the bulk saleCreditors are provided a right to commence litigation to challenge the proposed Bulk SaleReasons for Challenge:

oTechnical Bulk Sale Requirementso Insufficient Consideration

LEGAL ISSUES AND REMEDIES

•UCC Article 6A “bulk transfer”under UCC Article 6 takes place with the transfer “of a major part of the materials, supplies, merchandise or other inventory” outside the ordinary course of business. In 1989, Article 6 was revised (i.e. over half of inventory) due to difficulty in its application.

oDrafters recommended outright repeal. Meanwhile, Fraudulent Transfer law was evolving.

LEGAL ISSUES AND REMEDIES

•Remnants of the Bulk Transfer LawsArticle 6

o Maryland

Revised Article 6 (1989)o California*o District of Columbia

Repealedo Georgia (as of July 1, 2015)o All other states

Fraudulent Transfer law has made Bulk Transfer law largely obsolete.

LEGAL ISSUES AND REMEDIES

• Fraudulent ConveyancesTwo types of fraudulent conveyances

o Actual intent o Constructive fraud

Bankruptcy analog: avoidance action under § 548 of the Bankruptcy Code

o Creditors may avoid conveyances up to 2 years prior to filing a bankruptcy petition

o § 544 incorporates State Law Fraudulent Conveyance, therefore 4 year SOL

LEGAL ISSUES AND REMEDIES

• Fraudulent Conveyances – Actual Intent Actual Intent: intent to hinder, delay or defraud a creditor Fraudulent intent may be inferred from “Badges of Fraud:”

o A close relationship among parties to the transaction (family, friends, etc.)

o Secrecy/haste o Inadequate consideration (did not receive REV)o The transferor’s knowledge of the creditor’s claim and his own inability to pay it

LEGAL ISSUES AND REMEDIES

LEGAL ISSUES AND REMEDIES • Fraudulent Conveyance – Constructive FraudMisnomer: no fraudulent intent required

Two Requirements:oUnreasonably Equivalent Value; andoInsolvency

•UCC Art. 9 Foreclosure Sale–GenerallyUnder § 9‐610 of the UCC, upon Default, a secured creditor may dispose of collateral in a “commercially reasonable manner”

o Including public and private proceedings.o No judicial proceedings required.o All junior liens are extinguished.o Notice ONLY to other lienholders.

Unsecured Creditors get “Squat”

LEGAL ISSUES AND REMEDIES

•UCC Art. 9 Foreclosure Sale–Disposition Public Sale

oAuction‐type competitive sale complete with an auctioneer or investment banker

oStrict notice requirementsoNapa Valley Example

Private SaleoSecured party may not bid at private saleoPrivate sales are encouraged under the UCC (cmt. 2; 9‐610)

LEGAL ISSUES AND REMEDIES

LEGAL ISSUES AND REMEDIES • The D&O LawsuitDuties of Directors and Officers of an Insolvent company

o Duty of Careo Duty of Loyalty

Conflict of Interests Business Judgment Rule

To Whom Are D&O’s Duties Owedo Shareholderso Creditors

What is Involved

LEGAL ISSUES AND REMEDIES

• Successor LiabilityAs a general rule, a corporation which buys or acquires another corporate entity’s assets does not assume the seller’s liabilities.The Asset Purchase Agreement will always say: “Buyer does not assume any of Seller’s liabilities.”

LEGAL ISSUES AND REMEDIES

•Successor Liability: ExceptionsStandard exceptions to the general rule of no liability include:

o Express/implied assumption of liabilities in the purchase agreemento De facto mergers: Substance over Form, Statutory Merger Lawso Mere continuation of the seller’s business by the purchasero Fraudulent transactions to escape liability

LEGAL ISSUES AND REMEDIES • Successor Liability ExceptionsProduct line continued by Mfg purchaser

o Linked to products liability tort claimso Adopted: CA, MS, NJ, NM, NY, PA, WAo Rejected: OH, VA, MA, ME, CT, NH, IA, TX, GA, KS, MI, MO, NE, OK, WI, ND, SD, VT, FL, CO, IL, OR, DC

Other state and federal regulationso Environmental o Labor lawso Civil Rights

• Involuntary Bankruptcy

Infrequently used ‐ One‐half of one percent (.5%)

Automatic stay ‐ The most all encompassing injunction in all of jurisprudence

Easy to File ‐ No evidence, no hearing, just file a two page document

83

LEGAL ISSUES AND REMEDIES

LEGAL ISSUES AND REMEDIES •Commencing an Involuntary BankruptcyThree or more creditorsAggregate debt of $15,325Creditors debts cannot be (i) subject

to a bona fide dispute or (ii) contingent

Sign a two page petition

Commencing an Involuntary Bankruptcy

• Test: Debtor is not paying debts as they generally are due

a) Number of debtsb) Degree of delinquencyc) Materiality of non‐paymentd)Total debt compared to debtor’s annual incomee)Whether debtor is only not paying Petitioning Creditors

f)Whether debtor is still operating its business

Strategic Reasons To File Involuntary Bankruptcy• Debtor is only paying debts that the principal has guarantied

• Removal of property or sales outside the ordinary course of business

• Bank control

• Insider transfers

• Debtor’s selective payments to only certain creditors

• Trapping preferences

• Control location of the bankruptcy case

• Incompetent management ‐ Bankruptcy Trustee or Crisis Manager

• Debtor’s intention to over‐collateralize bank

• Judgment creditor is about to levy on unencumbered property86

Involuntary Bankruptcy

Involuntary Bankruptcy

Key To Victory

•Due diligence before filing involuntary petition is absolutely critical

•Once You File – You can’t “unfile” or dismiss involuntary petition

• DO DUE DILIGENCE – involuntary bankruptcies are very hard to dismiss• In re Maury Rosenberg• In re TPG Troy, LLC

• Consider what is to be gained, i.e. strategic reasons for filing

• Don’t hesitate to use this very powerful weapon• But don’t be wrong – not a substitute for collection

action(a) Liable for attorney fees(b) Punitive damages

88

Involuntary Bankruptcy

with Customer Going Dark

• Big Problem: $$$$$$• All Of Creditors’ Remedies Are Quite Expensive In Terms Of Legal Fees• That Is Why Due Diligence Is So Important• Different Remedies and Strategies, Depending upon Type of Transaction Sale Foreclosure Change of Business Model

• Things to Look For To Obtain Legal Traction: Sale to affiliateControl by bankUnperfected security interestsActions that solely benefit principal/guarantor without consideration of suppliersTransfers to affiliates, insiders, or related partiesSale to related party or affiliate

with Customer Going Dark

• Often Times, Customer’s Business Is Simply Becoming No Longer Feasible, i.e. Go Broke

• When The Business Is Simply Failing, Remedies Are Limited Due DiligencePre‐Suit DepositionInvoluntary BankruptcyCollection Suit—likely not much help

with Customer Going Dark

• Suggested MEMA Game Plan• Incremental Efforts Such That Creditors Remain In Control Of Costs

• Group Of Creditors To Significantly Reduce Costs• Three Phases, With Goal Of Enabling Creditors To Stop at any time; or Keep Going Based Upon Informed Business Decisions

with Customer Going Dark

MEMA GAME PLAN

MEMA GAME PLAN—Phase I• Begin Due Diligence• Cost to Suppliers: ZeroKRCL: Secretary of State, database and UCC searchCreditors: Marshall information and resources (i.e. sales reps and similar industry investigation)Dan Pike make initial contact, requesting information

• Goal: Obtain As Much Quality Information As Possible At Minimal, If Any, Cost

• Enable Suppliers to Begin Making Intelligent and Informed Decisions

MEMA GAME PLAN—Phase II• After a Conference Call Delivering Results of Phase IAdditional MEMA Due Diligence: Visit by Pike, Obtain Documents, Phone Interview with Principal, Discussions with Bank’s Counsel—Whatever the situation calls for and depends upon some reasonable cooperation by customer Counsel is Not Engaged, so consultation is on the MEMA RetainerSome reasonable charge by MEMA, depending upon involvement and expenses

MEMA GAME PLAN—Phase III• Examine Pros And Cons Of Alternative Legal Remedies• Retain Counsel• Key Is You Are Not Spending Money Without A Specific Reason And Game Plan—Provides information and strategy to discuss with management before counsel is engagedSuppliers have a specific game plan that is fully vetted—informed business decision before money is “invested”

Prevents The Proverbial Throwing Good Money After Bad

• Customers Going Dark—There Is A Reason—Through Due Diligence, you need to Understand the Reason

• Going On The Attack Without Good Due Diligence And A Game Plan Is Likely Wasteful

• Suppliers Do Have Remedies—Hope—But Most Require A Meaningful Investment

CREDIT APPLICATIONS—What You Need to Know—

‐Hopefully‐

ARE THEY NECESSARY?No. They Are Not Necessary.

Yes, Really.Article 2 of the Uniform Commercial Code

It’s The Boss.

Basic Structure of A Transaction

• Seller and Buyer discuss transaction• Buyer offers to purchase X goods for $Y• Seller accepts offer, proposes payment terms.• Buyer accepts payment terms.• Seller invoices buyer, ships goods.

That’s All You Need

Transaction Overview• Negotiation of Price• Negotiation of Terms• Unsecured Extension of Credit • Creation of Account Receivable• No Credit Application

But is that really a “best practice?”

What If Your New Customer Is Like This Guy?

What If Your Long‐Time Customer Is Like These Guys?

Reasons to Require Credit Applications• Examine credit worthiness• Establish binding credit terms• Determine necessity of guaranties• Integrate Security Agreements• Require financial reporting• Monitor risks of default and bankruptcy• Reclamation benefits

Pretty Long List of Benefits

But still not as long as the list of Cleveland Browns QBs since 1999‐Hooray Football Season!‐

‐GO COWBOYS‐

BEST PRACTICES

Yes, we’re talking about practices…

The Five Big Fundamentals

The Five Big Fundamentals

• Determine Credit Worthiness• Establish Terms of Sale• Monitor Customer’s Financial Condition• Protect The House• Take Advantage of Legal Conveniences

Determine Credit Worthiness

• Customer Financials• Audited financial statements• Bank Accounts/Records

• Credit References• Multiple similarly situated vendors

• Debtor’s customer list• Diverse or large single

• Necessity of Guaranty• Business or Personal

Establish Terms of Sale

• Sale Terms Controlling• Set binding terms affecting all invoices

• Late Charges• Late interest fee, accrual date

• Nature of Credit Relationship• Short term issuance of credit on invoice only• No executory contracts

Monitor Financial Condition• Monthly or Semi‐Annual Financials

• Keep tabs on your customers

• Mandatory Notice: Change of Condition• Notice of insolvency, change of ownership, loss of key customer, change in business structure

• Attestation of Solvency• Quarterly or monthly attestation of solvency• Reclamation benefits

Protect The House• Security Interests

• Continuing PMSI• Cooperation for perfection, no subordination

• Kill Switch• Unilateral right to terminate relationship, cease shipments, drop credit limit to zero

• Enforcement of Remedies• Right to costs of collection, including fees, costs• Marshalling and repossession

• Waivers of Warranties• Merchantability• Suitability for a particular purpose• Incidental and consequential damage waiver

Legal Conveniences

• Choice of Law• You choose which State’s law applies

• Venue and Jurisdiction• Bring suit in your back yard

• Waiver of Jury Trial• Reduce risk, expedite litigation

• Indemnification• Customer protects your interests in case of suit

• Integration Clause• All of the terms of the agreement

• Battle of the Forms• Ensure Credit Application controls parties’ relationship

So, What Do I Think About Them?

Two Thumbs Up

Quick Hits – Big BenefitsWe All Make Mistakes

A Well Drafted Credit ApplicationCan Ease the Pain Caused By A Bad Customer

Risk Mitigation• Monitor Financials• Reduce or Eliminate Credit• Amend Terms to COD

• Reduce Preference Exposure

• Terminate Relationship if Necessary

Credit Monitoring & Reclamation

• Repossessing goods sold on credit• Learn of insolvency, make reclamation demand

• 10 Day Limitation

• Quarterly Financials• Misrepresentation of solvency in writing

• 90 days!

That’s good news for these guys!

Purchase Money Security Interest• Purchase Money Security Interest

• Security Agreement• Built into terms of Application

• Agreement of Cooperation• Perfection within 20 Days of Delivery

• UCC‐1• Notice of holders of liens on inventory

GuarantiesYou Can Mitigate Risk With

Personal & Business Guaranties

“I Guarantee It”

Disclaimers of Warranties

• Goal – Limit Potential Exposure• Implied Warranties

• Merchantability• Fitness

• Disclaimers• Need to stand out and grab the reader’s attention• YOU NEED TO SEE THEM AND NOTICE THEM!

Disclaimers of Warranties

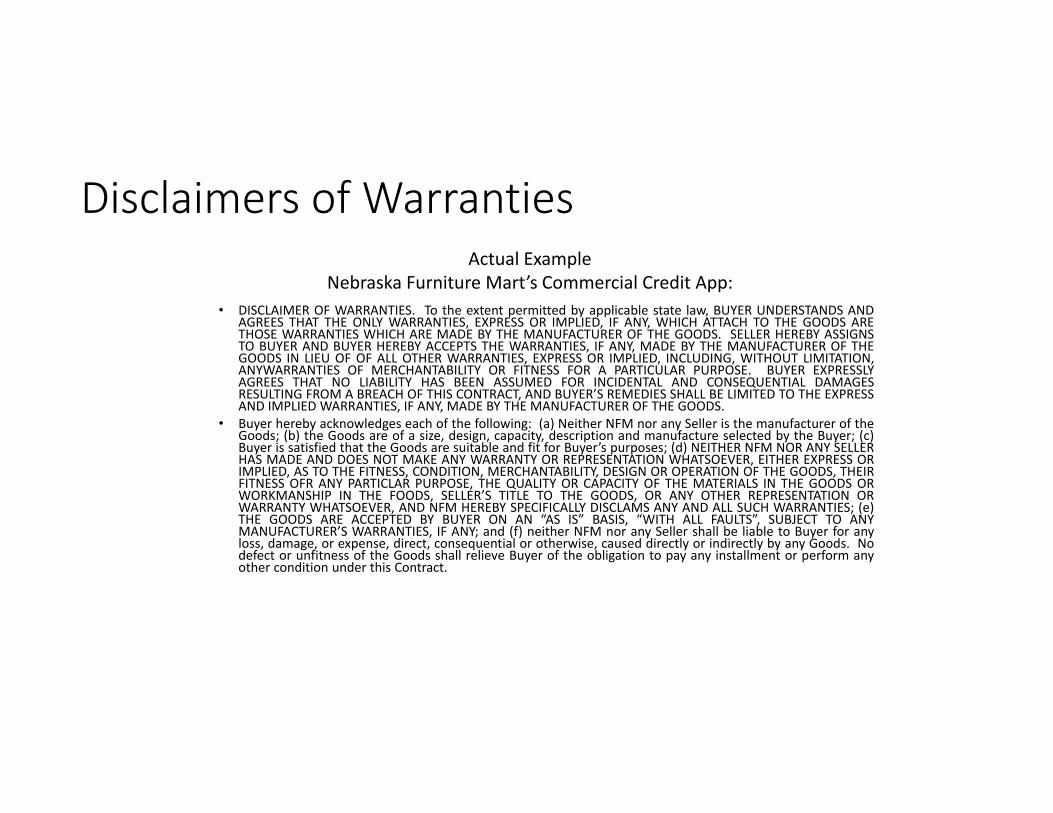

• DISCLAIMER OF WARRANTIES. To the extent permitted by applicable state law, BUYER UNDERSTANDS ANDAGREES THAT THE ONLY WARRANTIES, EXPRESS OR IMPLIED, IF ANY, WHICH ATTACH TO THE GOODS ARETHOSE WARRANTIES WHICH ARE MADE BY THE MANUFACTURER OF THE GOODS. SELLER HEREBY ASSIGNSTO BUYER AND BUYER HEREBY ACCEPTS THE WARRANTIES, IF ANY, MADE BY THE MANUFACTURER OF THEGOODS IN LIEU OF OF ALL OTHER WARRANTIES, EXPRESS OR IMPLIED, INCLUDING, WITHOUT LIMITATION,ANYWARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE. BUYER EXPRESSLYAGREES THAT NO LIABILITY HAS BEEN ASSUMED FOR INCIDENTAL AND CONSEQUENTIAL DAMAGESRESULTING FROM A BREACH OF THIS CONTRACT, AND BUYER’S REMEDIES SHALL BE LIMITED TO THE EXPRESSAND IMPLIED WARRANTIES, IF ANY, MADE BY THE MANUFACTURER OF THE GOODS.

• Buyer hereby acknowledges each of the following: (a) Neither NFM nor any Seller is the manufacturer of theGoods; (b) the Goods are of a size, design, capacity, description and manufacture selected by the Buyer; (c)Buyer is satisfied that the Goods are suitable and fit for Buyer’s purposes; (d) NEITHER NFM NOR ANY SELLERHAS MADE AND DOES NOT MAKE ANY WARRANTY OR REPRESENTATION WHATSOEVER, EITHER EXPRESS ORIMPLIED, AS TO THE FITNESS, CONDITION, MERCHANTABILITY, DESIGN OR OPERATION OF THE GOODS, THEIRFITNESS OFR ANY PARTICLAR PURPOSE, THE QUALITY OR CAPACITY OF THE MATERIALS IN THE GOODS ORWORKMANSHIP IN THE FOODS, SELLER’S TITLE TO THE GOODS, OR ANY OTHER REPRESENTATION ORWARRANTY WHATSOEVER, AND NFM HEREBY SPECIFICALLY DISCLAMS ANY AND ALL SUCH WARRANTIES; (e)THE GOODS ARE ACCEPTED BY BUYER ON AN “AS IS” BASIS, “WITH ALL FAULTS”, SUBJECT TO ANYMANUFACTURER’S WARRANTIES, IF ANY; and (f) neither NFM nor any Seller shall be liable to Buyer for anyloss, damage, or expense, direct, consequential or otherwise, caused directly or indirectly by any Goods. Nodefect or unfitness of the Goods shall relieve Buyer of the obligation to pay any installment or perform anyother condition under this Contract.

Actual Example Nebraska Furniture Mart’s Commercial Credit App:

Battle of the Forms

• Strong Controlling Contract Provision• Negates efforts to say other agreements should control the relationship between Buyer and Seller

• Integration Clause + Controlling and Binding• Unilateral amendments on notice to buyer• All others in writing, signed by both parties

Battle of the FormsExamples

• This Agreement, together with any application you submitted in connection with theAccount…constitutes the entire agreement between you and us relating to yourAccount and supersedes any other prior or contemporaneous agreement between youand us and/or our predecessors relating to your Account. We may amend thisAgreement, including to impose additional or different fees or to change the terms ofyour Account, by giving you 15 days advance notice thereof; provided, however, we maysuspend or terminate your Account or change your credit limit without any notice toyou (as described in more detail above). This Agreement may not otherwise beamended. [Northern Tool + Equipment]

• This agreement contains the entire and only understanding between Customer andRadioShack Credit Services relating to the subject matter hereof. No provision of thisAgreement can be waived, amended or modified, except by an instrument in writingsigned by a duly authorized representative of RadioShack Credit Services. Additionalterms or conditions that may or may not accompany Customer's preprinted PurchaseOrder forms expressly do not supersede any part of this agreement and Customeragrees that said terms and conditions of their preprinted Purchase Order forms are ofno force and effect as between RadioShack Credit Services and Customer. Customerswho are in the business of providing leased equipment to third parties are liable in fullfor all purchases made on their account regardless of the current relationship betweenCustomer and their lessee.

Other Goodies• Indemnification Agreements• Confidentiality Agreements• Attorneys’ Fees

Recoup the Costs of Collection Associated With These Guys

Other Means of Accomplishing Goals?Yes

Other Agreements with Similar Contractual Provisions

But As a Wise Man Once Said

Incorporating All Key Terms Into One Document May Be Preferable• Avoid the confusion of which documents control• Consolidate binding terms, rights, remedies

MFSG 2015 Educational Seminar

• Please complete your speaker evaluation for Joe Coleman and John Kane and their presentation:

Customers That Go Dark & Credit Applications

12:15 pm – 1:15 pm Networking lunch in hotel’srestaurant

Sponsored by Kane, Russell, Coleman & Logan

MEMA Financial Services Group, Inc.2015 Educational Seminar

Sponsored By

Kane, Russell, Coleman and Logan PCCommitment. Performance. Results

Introduction of Afternoon Topics

Dan Pike

MEMA Financial Services Group, Inc.

Supply Chain Financing

Bob ScottSunTrust Robinson Humphrey

Supply Chain Finance Discussion

MEMA Financial Services Group

September 17, 2015

Overview of SunTrust

Source: SNL Financial

Overview

Total assets of $189Bn

− TCE Ratio: 8.38%

− Leverage Ratio: 8.91%

− Total RBC Ratio: 13.45%

Senior LT Debt / Deposit Ratings:

− Moody’s: Baa1 / A1

− Standard & Poor’s: BBB+ / A-

− Fitch: BBB+ / A-

Market Cap over $15.3BN

Raised $1.04 billion of equity and $1 billion of senior notes to fully redeem $4.85 billion of TARP on 3/30/2011

5 million total client relationships and more than 27,000 employees

Headquartered in Atlanta with over 1,600 branches and 2,800+ ATMs across the east coast

Regional Corporate Banking Offices: New York City, Boston, Chicago, San Francisco, Los Angeles, Dallas, Charlotte, Tampa, Miami, Atlanta

Ranked Top 3 in Deposit Market Share

− Still one of the best footprints in banking

− Population growth of 6.2% (3.9% national average)

− Household growth of 14.0% (12.4% national average)

Atlanta

Branch Map

Top Ten U.S. Commercial Banks Ranked by Deposits

Rank Bank1 J.P. Morgan Chase & Company

2 Bank of America Corporation

3 Wells Fargo & Company

4 Citigroup Inc.

5 U.S. Bancorp6 PNC Financial Services Group, Inc.7 Capital One Financial Corporation

8 SunTrust Banks Inc.9 BB&T Corporation

10 Regions Financial Corporation

STRH – Nationally Focused, Full-Service Investment Banking Firm

Investment Banking

Fixed Income Research, S&T

Equity Research, S&T

~ 135 corporate coverage bankers, middle market relationship managers and product specialists

Over 900 employees

National client base

Industry sector driven

Middle market focus

Full line of investment banking services

Traditional/corporate banking capabilities professionals

2010 national winner of Greenwich Associates award for investment banking among businesses $10-$500 million in revenue

Consumer & Retail

Energy & Power

Industrials

Media & Comm.

Healthcare

Financial Sponsors

Fin. Services & Tech.

Equity Sales & Trading Over 50 Trading Professionals Over 500 Institutional Clients Extensive Domestic and International

Distribution Capabilities Make Markets in Over 800 Listed

StocksEquity Research 20 Equity Research Analysts 330+ Companies Under Coverage Growth-oriented Focus

SunTrust Robinson Humphrey continues to strategically expand our coverage and execution teams

SunTrust Robinson Humphrey ‐Supply Chain Finance Team

136

Michael MazaManaging Director, Asset Finance Group

David HartGroup Head, Supply Chain Finance

[email protected] | 404.926.5180

Supply Chain Finance

Emily CooperProduct Specialist, Operations

Marie TenagliaVice President, SCF

Implementation, On-boarding, Operations404.926.5484

Bob ScottDirector, SCF Originations, Strategy

Debra IrwinProduct Specialist, Operations

Sharon HarrisonAdministrative Assistant

Brennan BubpAssociate/ Onboarding

Trey ByrdAnalyst / Onboarding

Richard RoweDirector, Loan Structuring, On-boarding

Asset Securitization Program Lending & Supply Chain Finance Asset Based Lending Structured Real EstateEquipment Finance

Leasing

Asset Finance Group

Supply Chain Finance Market Dynamics

Buyer Perspective

Supply Chain Finance Market DynamicsAberdeen Group Study: Working Capital Initiatives(1)

Source: (1) Aberdeen Group, January 2011

SpendPer Invoice

Number of Invoices

Large $ Direct Spend

Small $ Indirect Spend

Supply Chain Finance Program

Corporate Card Program

Two complementary AP centric solutions that extend final payment terms while enabling early payment to suppliers

Transition

Two Complimentary Working Capital Solutions

18%

31%

31%

23%

30%

22%

29%

19%

17%

54%

18%

24%

24%

30%

64%

0% 10%20%30%40%50%60%70%

Support more favorable Pricing during initial transactions

Implement / increase usage of early payment discount

programs

Analyse spending patter to prioritize trading partner for

SCF initiatives

Invest in automation of financial processes to support SCF

Alter payment terms with partners

Percentage of Respondents, n = 145

Best-In-Class

Industry Average

SunTrust Robinson Humphrey has provides over $2.1 Billion in Supply Chain Finance program commitments as Sole Lead Arranger orFunding Partner to the corporations listed above.

Executive Supplier Risk Comments (10‐Ks) Risks associated with a vendors inability to obtain credit in a tightened credit market or remain solvent given disruptions in

the financial markets

Manufacturing process delays due to shortages, outages, or interruptions in the delivery of key components from direct and tier 2 suppliers

A supply shortage could increase our cost of goods sold due to higher prices for components in limited supply

Risk of our diminished product quality with alternate suppliers resulting in higher charge backs, warranty claims, replacement products, or service repairs

Customer just in time delivery (demand management) increases our inventory carrying costs and exposure to inventory obsolescence

Global operational risk associated with the impact of local economies, inflation, interest rates, regional recessions, commodity prices, & currency volatility

A supplier shortage could cause us to redesign or reconfigure our products to accommodate a substitute component

Supplier risks associated with compliance of U.S & international laws impacting global operations

Lost revenue if suppliers are not able to meet the forecasted demands of our rapid growth

What keeps senior sourcing and supply chain executives up at night?

Which new strategies are being considered to address supplier risk?

Supply Chain Finance Defined

Buyers: Want to delay disbursements, retain capital, extend DPO, improve CCC, vendor funded share of wallet

Suppliers: Want to accelerate receivables, increase cash, reduce DSO, improve CCC, off balance sheet financing

Payables Discounting Program ‐ SCF is a payables discounting program designed to provide your suppliers with alternative financing by permitting them to sell their approved receivables to SunTrust. In exchange for immediate liquidity, suppliers agree to a discount rate applied to the sold receivables.

Working Capital Tool – Supplier financing offers an early payment option that provides suppliers with immediate liquidity by facilitating the sale of Confirmed Receivables (CRs) to the bank for cash. Alternatively the supplier can elect to sell CRs at a future date or hold them until the due date to collect 100% of the value.

Attractive Pricing ‐ Regardless of size or credit rating, suppliers receive the pricing benefit of the Corporate Client’s credit profile. SCF provides suppliers access to less expensive working capital when compared to the costs of asset‐based lending, factoring and other traditional borrowing activities.

Extend Payment Terms – Given the working capital benefits of SCF to their suppliers, corporate buyers will have ample negotiating leverage to “push payment terms” with those suppliers.

Solidify Supplier Base ‐ A SCF program supports the corporate philosophy of building strong collaborative supplier relationships, by providing an alternative form of financing for suppliers who need to keep up with your corporate growth.

Supply Chain Finance is a collaborative approach to enhance the working capital position of both the corporate buyer and its suppliers

Working Capital Dilemma

SCF Program Defined

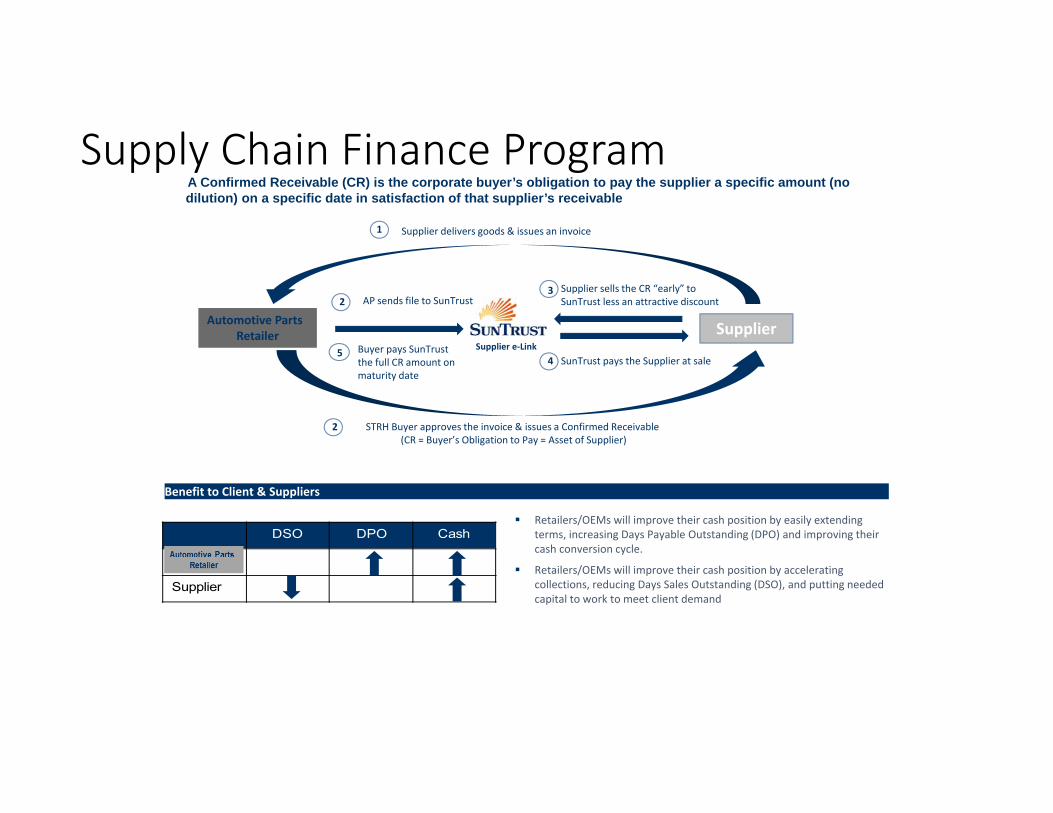

Supply Chain Finance Program

Supplier

Supplier delivers goods & issues an invoice1

STRH Buyer approves the invoice & issues a Confirmed Receivable (CR = Buyer’s Obligation to Pay = Asset of Supplier)

2

Buyer pays SunTrust the full CR amount on maturity date

5SunTrust pays the Supplier at sale4

Supplier sells the CR “early” to SunTrust less an attractive discount

3

Supplier e‐Link

A Confirmed Receivable (CR) is the corporate buyer’s obligation to pay the supplier a specific amount (no dilution) on a specific date in satisfaction of that supplier’s receivable

Benefit to Client & Suppliers

Retailers/OEMs will improve their cash position by easily extending terms, increasing Days Payable Outstanding (DPO) and improving their cash conversion cycle.

Retailers/OEMs will improve their cash position by accelerating collections, reducing Days Sales Outstanding (DSO), and putting needed capital to work to meet client demand

Automotive Parts Retailer

AP sends file to SunTrust2

DSO DPO Cash

Client

Supplier

Industry Comparison Working Capital Metrics

Aftermarket Autoparts Industry Comparable Analysis

Industry Comp Set

Company NameFY Avg.

Cash Conversion Cycle FY Avg.

Days Payable Out. FY Avg.

Days Inventory Out. FY Avg.

Days Sales Out. FY

Inventory Turnover FY

Cash And Equivalents FY

Annual Spend % Sales S&P Credit

RatingAdvance Auto Parts Inc. (NYSE:AAP) 60 220 273 7 1.3x $1,112.5 55.8% BBB-Genuine Parts Company (NYSE:GPC) 73 71 103 41 3.6x $196.9 83.1% N/APep Boys - Manny, Moe & Jack (NYSE:PBY) 101 60 156 4 2.4x $59.2 71.2% BO'Reilly Automotive Inc. (NasdaqGS:ORLY) 51 215 259 7 1.4x $231.3 52.4% BBBAutoZone, Inc. (NYSE:AZO) (11) 249 231 7 1.6x $142.2 51.6% BBB

Mean 55 163 204 13 2.1x $348.4 62.8%Median 60 215 231 7 1.6x $196.9 55.8%

All values in millions, except per share data and ratios.Values converted at today's spot rate.Source: S&P Capital IQ

Working Capital Impact of Extending Payment Terms Company: Leggett & Platt

Inputs (1) Supplier Adoption Tables Revenue $3,746.0 Assumptions Rates Annual SpendAnnual AP Spend $3,266.5 1 10.0% $327Annual Spend % of Revenue 87.2% 2 25.0% $817Accounts Receivable $467.4 3 50.0% $1,633Accounts Payable $339.3Average Inventory $495.9Days Sales Outstanding 41 DaysDays Inventory Outstanding 60 365Days Payable Outstanding 38Cash Conversion Cycle (CCC) 63Cash $272.7(1) $ in millions and 2013 Financials

Company: ABC Buyer Inc.

25% Supplier Adoption Table; Impact on Overall Working Capital Supplier Adoption Rate: Extend Terms in Days25% Current 30 60 90 120 150Overall DPO 38 8 45 15 53 23 60 30 68 38 75Overall DIO 60 0 60 0 60 0 60 0 60 0 60Overall DSO 41 0 41 0 41 0 41 0 41 0 41Overall CCC 63 (8) 56 (15) 48 (23) 41 (30) 33 (38) 26

Cash Flow Improvement(1)na na $67 na $134 na $201 na $268 na $336

(1) $ in millions

50% Supplier Adoption Table; Impact on Overall Working Capital Supplier Adoption Rate: Extend Terms in Days50% Current 30 60 90 120 150Overall DPO 38 15 53 30 68 45 83 60 98 75 113Overall DIO 60 0 60 0 60 0 60 0 60 0 60Overall DSO 41 0 41 0 41 0 41 0 41 0 41Overall CCC 63 (15) 48 (30) 33 (45) 18 (60) 3 (75) (12)

Cash Flow Improvement(1)na na $134 na $268 na $403 na $537 na $671

(1) $ in millions

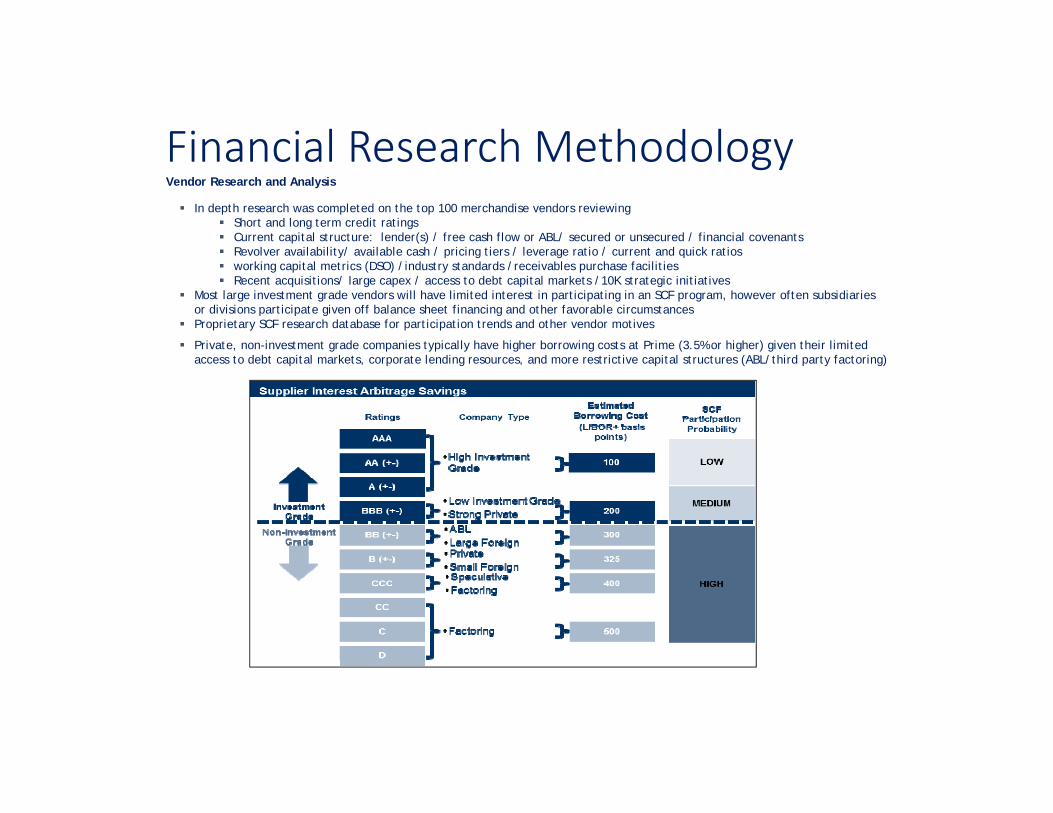

Financial Research MethodologyVendor Research and Analysis

In depth research was completed on the top 100 merchandise vendors reviewing Short and long term credit ratings Current capital structure: lender(s) / free cash flow or ABL/ secured or unsecured / financial covenants Revolver availability/ available cash / pricing tiers / leverage ratio / current and quick ratios working capital metrics (DSO) /industry standards /receivables purchase facilities Recent acquisitions/ large capex / access to debt capital markets /10K strategic initiatives

Most large investment grade vendors will have limited interest in participating in an SCF program, however often subsidiariesor divisions participate given off balance sheet financing and other favorable circumstances

Proprietary SCF research database for participation trends and other vendor motives

Private, non-investment grade companies typically have higher borrowing costs at Prime (3.5% or higher) given their limited access to debt capital markets, corporate lending resources, and more restrictive capital structures (ABL/third party factoring)

Supplier Working Capital Impact Central Bank Rates(1)

GER 3.0%

CHI 5.0%

CAN 1.0%

KOREA 2.5%

UK 0.5%

USA 0.25%

AUS 2.75%

INDIA 7.25%

MEX 4.0%

RUS 8.25%

BRZ 8.0%

CHN 6.0%JAPAN 0.1%

Global suppliers feel regional interest rate pressures

Global suppliers may have limited access to cheap working capital

INDO 6.0%

SAF 5.0%

ECB 0.5%

NZE 2.5%

(1) Source: Triami Media BV/ Globalrates.com/ Central Bank Rate Monitor / July 1, 2013

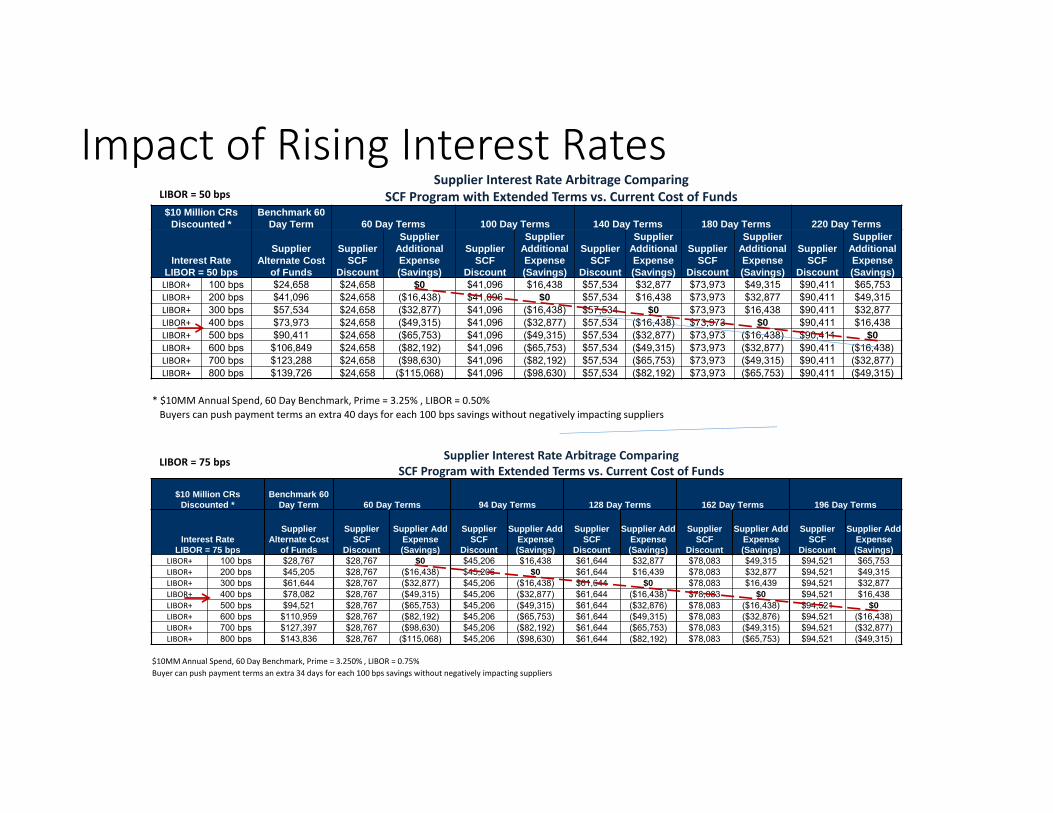

Supplier Interest Rate Arbitrage

New Invoice Due Date= CR Maturity Date

I1.50% ‐

5.25% ‐

Interest Rate

Day 1 Day 30 Day 60 Day 90 Day 120

SCF Program LIBOR + 100 bps

Supplier’s alternatesource of capital Prime + 200 bps

Original Invoice Due Date

I

Extend Payment Terms

“SCF Leverages Buyer’s Credit Profile”

Every 100 bps in Supplier savings suggests Buyer could push payment terms an additional 40 days

Breakeven line (red) suggests maximum number of days Buyer could extend terms before negatively impacting a Supplier

Supplier financing provides immediate liquidity not previously available

Source of off balance sheet financing for the Supplier at a less expensive rate.

Supplier Credit

Risk Catagory

SCF Program Interest

Expense L+100 bps **

Supplier A 100 bps $24,658 $24,658 $0 $16,438 $32,877 $49,315

Supplier B 200 bps $41,096 $24,658 ($16,438) $0 $16,438 $32,877

Supplier C (Prime) 300 bps $57,534 $24,658 ($32,877) ($16,438) $0 $16,438

Supplier D (Prime) 400 bps $73,973 $24,658 ($49,315) ($32,877) ($16,438) $0

Supplier E (Prime) 500 bps $90,411 $24,658 ($65,753) ($49,315) ($32,877) ($16,438)

Supplier F (Prime) 600 bps $106,849 $24,658 ($82,192) ($65,753) ($49,315) ($32,877)

* Table assumes $10MM Annual Spend @ 60 day terms / LIBOR = 0.50% / Prime = 3.25%

** Table assumes SunTrust SCF Program LIBOR+100 bps offered to all suppliers (illustration purposes only)

Summary Comment: Suppliers will accept extending terms up to 40 days for every 100 bps in interest savings.

Supplier Current Interest

Expense LIBOR +

60 Day

Terms

100 Day

Terms

140 Day

Terms

180 Day

Terms

Supplier (Savings) Expense with

SunTrust SCF Program$10 Million in Annual Spend @ Standard 60 day Terms*

Illustration: Impact of Extending Payment Terms on Suppliers

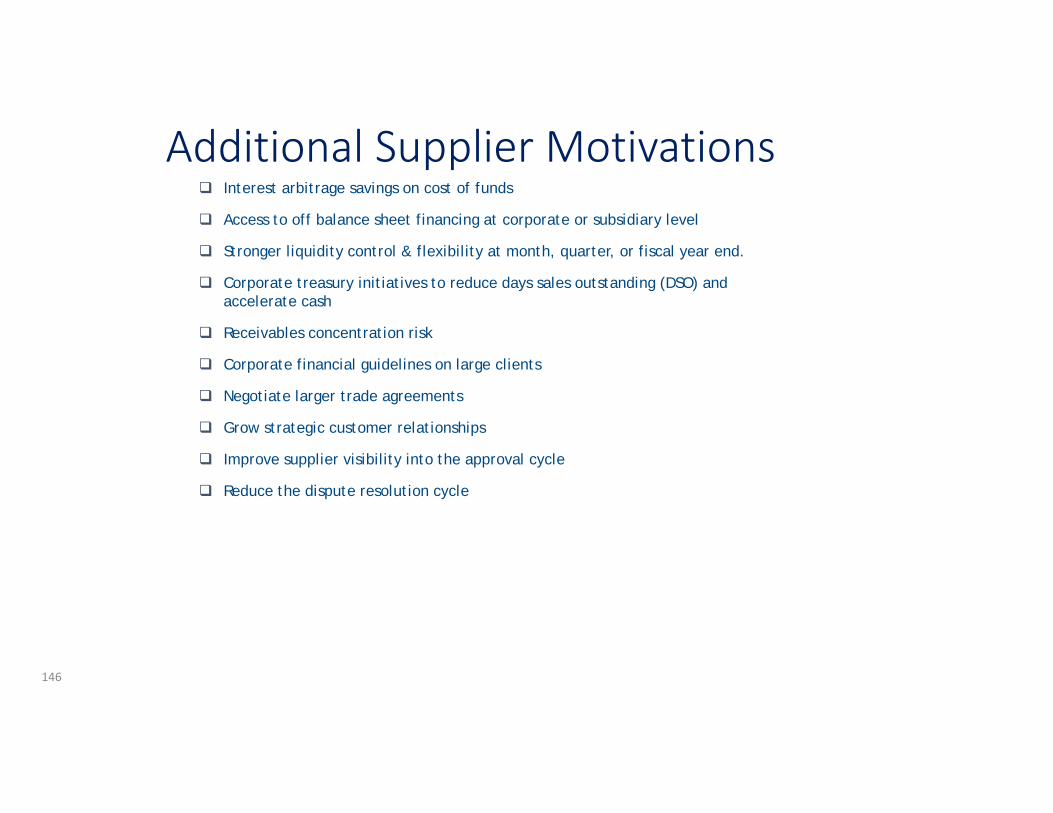

Additional Supplier Motivations

146

Interest arbitrage savings on cost of funds

Access to off balance sheet financing at corporate or subsidiary level

Stronger liquidity control & flexibility at month, quarter, or fiscal year end.

Corporate treasury initiatives to reduce days sales outstanding (DSO) and accelerate cash

Receivables concentration risk

Corporate financial guidelines on large clients

Negotiate larger trade agreements

Grow strategic customer relationships

Improve supplier visibility into the approval cycle

Reduce the dispute resolution cycle

SunTrust Supply Chain Finance Program Structure 100% supplier funded program (Split) Unsecured, uncommitted line (Secured) Utilization footnote to short term payables No underwriting, commitment, or syndication fees No implementation or file integration fees No supplier spend analysis or on‐boarding fees No supplier marketing or promotional fees No supplier payment transaction fees (Split/Rebate) Supplier adoption minimums Program start in 60 days

Client Spend Analysis Formal Strategic On‐Boarding Plan Client Procurement Team Engagement & Training Supplier On‐boarding Promotions

– Educational Seminars & Webinars– Vendor Day Presentations– Telemarketing Campaigns – Direct Supplier Meetings

Supplier Enrollment & User Training Procurement & AP Coordination Buyer & Supplier Reporting

SCF Program Key Characteristics Supplier On‐boarding Expertise

SunTrust’s SCF platform is well known

for its ease of use with participating

buyers and suppliers

Demos are available to review

capabilities and functionality

Decentralized Organization B2B Integration

SunTrust SCF Integration Team• File Monitoring• Protocol Mediation • Mapping Translation • Notifications / Exceptions

SunTrust SCF Operations Team• Strategic Rollout Plan• Procurement Spend Analysis• Supplier Engagement

• On‐boarding & Agreements• Portal Access & Training

•Ongoing Supplier & Client Support

Supplier Network

Supplier 1

Supplier 2

Supplier 3

Supplier 4

Supplier 5

Supplier 6

Decentralized Organization

Supply Chain e‐Link

Secure FTP orDirect Transmission

EDI 810

IDOC

XML

Excel File

CSV File

ProprietaryCorporate Client

Subsidiary 1

Division A

Division B

Subsidiary 2

Region C

Region D

Subsidiary 3

Business Line E

Business Line F

Sample AP Spend File

Company Name Vendor Type Product Type Credit Score* Annual Spend Payment Terms Discount Terms Average InvoiceCompany A Category 1 $1,000,000 Net 30 2/10, Net 30 $50,000Company B Category 1 $500,000 Net 60 2/10, Net 60 $5,000Company C Category 1 $5,000,000 Net 30 No Discount $250,000Company D Category 2 $3,000,000 Net 30 2/10, Net 30 $75,000Company E Category 2 $4,000,000 Net 60 2/10, Net 60 $150,000Company F Category 3 $2,000,000 Net 60 No Discount $40,000Total $15,500,000 $570,000*Either rating agency or internal credit scoring metric

SunTrust SCF team will request a copy of a standard AP spend file. The more detailed the file the more comprehensive our SCF recommendations Vendor credit scoring information (D&B scores or S&P ratings) Standard terms with the suppliers, product shelf life, inventory turn While all fields are optional the most important fields in order of importance are as follows:

Vendor Name/ HQ address / country Annual spend Current payment terms /discount terms Vendor parent company (if available) AP or ERP internal credit score, D&B, Moody’s, or S&P rating (if available) Product type, division, or business line Number of invoices or average number of invoices

Prefer Excel or CSV file while a standard AP or ERP system export format is also acceptable.

Sample Spend File

150

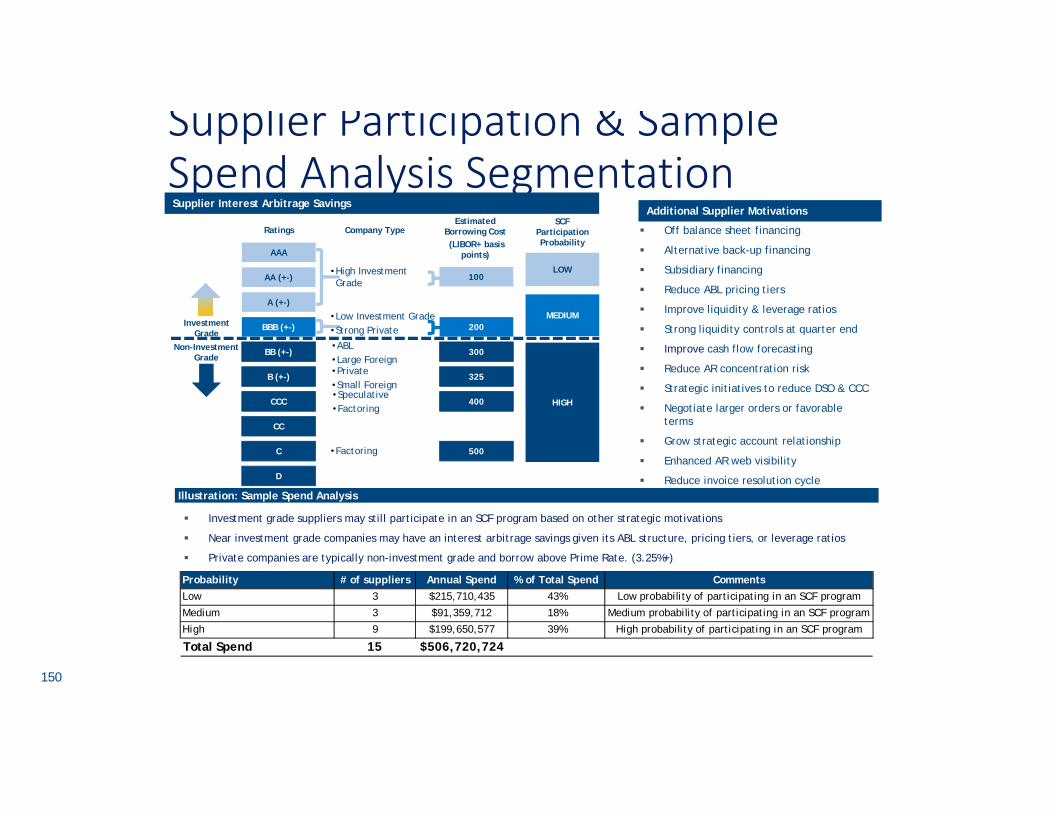

Supplier Participation & Sample Spend Analysis Segmentation

Investment grade suppliers may still participate in an SCF program based on other strategic motivations

Near investment grade companies may have an interest arbitrage savings given its ABL structure, pricing tiers, or leverage ratios

Private companies are typically non-investment grade and borrow above Prime Rate. (3.25%+)

AAA

Ratings

AA (+-)

A (+-)

BBB (+-)

BB (+-)

B (+-)

CCC

CC

C

D

Investment Grade

Non-Investment Grade

Company Type

• High Investment Grade

• Low Investment Grade• Strong Private

Estimated Borrowing Cost(LIBOR+ basis

points)

• ABL• Large Foreign• Private• Small Foreign• Speculative• Factoring

• Factoring

100

200

300

325

400

500

HIGH

SCF Participation Probability

MEDIUM

LOW

Supplier Interest Arbitrage Savings Additional Supplier Motivations

Off balance sheet financing

Alternative back-up financing

Subsidiary financing

Reduce ABL pricing tiers

Improve liquidity & leverage ratios

Strong liquidity controls at quarter end

Improve cash flow forecasting

Reduce AR concentration risk

Strategic initiatives to reduce DSO & CCC

Negotiate larger orders or favorable terms

Grow strategic account relationship

Enhanced AR web visibility

Reduce invoice resolution cycle Illustration: Sample Spend Analysis

Probability # of suppliers Annual Spend % of Total Spend CommentsLow 3 $215,710,435 43% Low probability of participating in an SCF program

Medium 3 $91,359,712 18% Medium probability of participating in an SCF program

High 9 $199,650,577 39% High probability of participating in an SCF program

Total Spend 15 $506,720,724

151

Sample Supplier Spend AnalysisVendor Name Annual Spend

Current Terms

Public or Private Rating

Estimated Borrowing

Cost

SCF Participation Probability

# Days to Push

Result Days Comments DSO Industry Classification

IBM Corporation $136,089,711 60 Public AA- L + 20 Low 30 90$10B Revolver pricing has five ranges from (10 - 75 bps) to

(30-112.25 bps), current range is 10 - 75 bps). 40

IT Consulting and Other

Services

Corrections Corporation of

America$106,818,082 30 Public BB+ L + 180 High 30 60

$900 MM Revolver pricing ranges from L + 150 to L + 240

bps, current pricing is L + 180 bpsN/A Correctional Facilities

Whirlpool National $82,144,934 15 Public BBB L + 125 Medium 30 45

Revolver pricing ranges from L + 100-225 bps depending

upon credit rating , currently at L + 125 bps. Offers early

payment static discount of 1.35% if paid in first 15 days.

Has own SCF program in place.

39 Household Appliances

Samsung Electronics America $78,467,865 30 Public A+ L + 100 Low 30 60 Operates as a subsidiary of Samsung Electronics Co. Ltd. 39Technology Hardware,

Storage and Peripherals

Tenet Health Systems $26,949,057 0 Public B L + 200 High 30 30$800MM Revolver pricing ranges from L + 200 to L + 250

bps, current pricing is L + 200 bps55 Healthcare Facilities

Dell USA LP $26,192,059 30 Private BB+ L + 350 High 30 60Term Loan B-1 priced at L + 400, Term Loan B-2 priced at L

+ 35042

Technology Hardware,

Storage and Peripherals

Hewlett-Packard Company $25,258,683 30 Public BBB+ L + 275 High 30 60Last floating rate note issuance at L + 2.75%, put on

negative credit watch by S&P in 10/201449

Technology Hardware,

Storage and Peripherals

SCANA Energy $8,056,847 30 Public BBB+ L + 150 Medium 30 60Parent - Multiple Revolvers pricing ranges from L +80 to L +

165 bps, current pricing is L + 127.5 bps64 Multi-Utilities

URS Corporation $5,059,095 0 Public BB- L + 200 High 30 30$17B Revolver pricing ranges from L + 112.5 to L + 200 bps,

current pricing is L + 200 bps97

Construction and

Engineering

Sharp Corporation $4,427,652 30 Public B+ L + 375 High 30 60

Operates as a subsidiary of Sharp Corporation. Publicly

traded Japanese company traded on the Toronto Stock

Exchange. 1 yr CDS trades at 125 bps.

53 Consumer Electronics

Momentive Specialty

Chemicals$2,073,445 30 Private CCC+ L + 500 High 30 60 $400MM revolver pricing from L +175 to L+225(+) 42 Diversified Chemicals

Nexeo Solutions LLC $1,497,023 45 Private B L + 425 High 30 75Private company based in The Woodlands, TX with public

debt profile.50 Distribution Service

Sulzer Mixpac USA Inc. $1,375,481 45 PrivateNot

RatedL + 300 High 30 75

Private sub. Based in Salem, NH; parent based in Zurich,

Switzerland.106 Specialty Chemicals

PRC Desoto International Inc. $1,157,931 30 Private A- L + 150 Medium 30 60Sub based in Glendale, CA; Parent PPG Industries based in

Pittsburgh, PA $1.2BN revolver pricing from L+100 to L+21061 Specialty Chemicals

Georgia Pacific LLC $1,152,859 30 Private A+ L + 75 Low 30 60Private company with public debt based in Atlanta, GA.

Revolver Pricing from L+32.5 to L+77.531 Paper Products

Total 15 $506,720,724

Sample Spend Analysis ResultsOnce the spend file is received our SCF team will complete a Sample Spend Analysis evaluating the working capital metrics of a limited number of suppliers which will demonstrate the potential financial impact on the client. Spend analysis results can be segmented by business line, division, credit score, country, or other requested parameters as provided.

A more comprehensive full spend analysis on all suppliers is available for clients as part of the new SCF program implementation, strategic planning, and on‐boarding process.

Sample research and spend analysis was completed on the largest 153 Suppliers or 75% of Total Annual Spend.

Largest 80 Various Suppliers representing over $80MM or 15% of Evaluated Spend

Largest 40 Freight Suppliers representing over $210MM or 43% of Evaluated Spend

Largest 33 Raw Material Suppliers representing over $200MM or 42% of Evaluated Spend

153

Supplier On‐boarding and Support Strategy

“SunTrust’s Supply Chain Finance programs are designed to maximize supplier adoption and participation”

Supplier Spend Analysis & Program Rollout – Identify and prioritize suppliers whose participation would contribute the greatest working capital impact. Work jointly with the Merchandising team to understand any supplier sensitivities and confirm the strategic approach for each supplier

Merchandising Team Training – Provide consultative sales tools, market intelligence, interest rate arbitrage tables, best practices, most popular questions, and suggest extended terms

Support terms negotiations – Participate in meetings between merchandising team and suppliers to provide SCF subject matter expertise

Direct Calling & Onsite Supplier Meetings – Conduct direct phone and onsite meetings to provide suppliers with a detailed understanding of the SCF program benefits and review onboarding packet

Telemarketing & Promotional Campaigns – Attend industry trade shows and onsite vendor work days, in addition to providing marketing support and supplier webinars

Supplier Enrollment & Training – SunTrust takes full ownership of supplier enrollment, documentation, granting user access, site navigation, user guides, best practices, and ongoing support

SCF Program Pilot StructureThe following is a basic SCF program implementation plan outlining potential resource needs, roles, responsibilities, and estimated timeline for a five week implementation project.

Tim

ing

Driv

en B

y C

lient

Goa

ls

Time Commentary Client Resource Type/Hours

Week 1

1) Review four page buyer agreement 2) Schedule future kickoff meeting 3) ID client point person to lead project 4) Introduction to technology, AP, and Sourcing key

contacts Phase I: Customize SCF materials & Kickoff meeting

1 point person x 20 hours x 1.0 months

Week 2

1) AP to provide vendor spend file 2) SunTrust performs spend analysis, segmentation, &

recommendation 3) ID client point person to lead project 4) Introduction to technology, AP, and Sourcing key

contacts

Week 3

1) Test AP output data file & confirm format 2) SunTrust to conduct training of sourcing key personal 3) Provide tools for engaging with suppliers

Phase II: Technology & AP Integration

1 Tech resource x 4 hours one time 1 AP resource x 4 hours one time

Week 4

1) AP to provide vendor spend file 2) SunTrust performs spend analysis, segmentation, &

recommendation 3) ID client point person to lead project 4) Introduction to technology, AP, and Sourcing key

contacts

Phase III: Vendor Enrollment

Sourcing Team Training 4 resources x 2 hours sessions one

time

Week 5

(Go Live)

1) Begin vendor terms negotiations 2) Begin vendor SCF enrollment

Phase V: Go Live Production

1 Sourcing resource 5 hours/week

1 AP resource x 1hour/week

Diagram Phased Approach

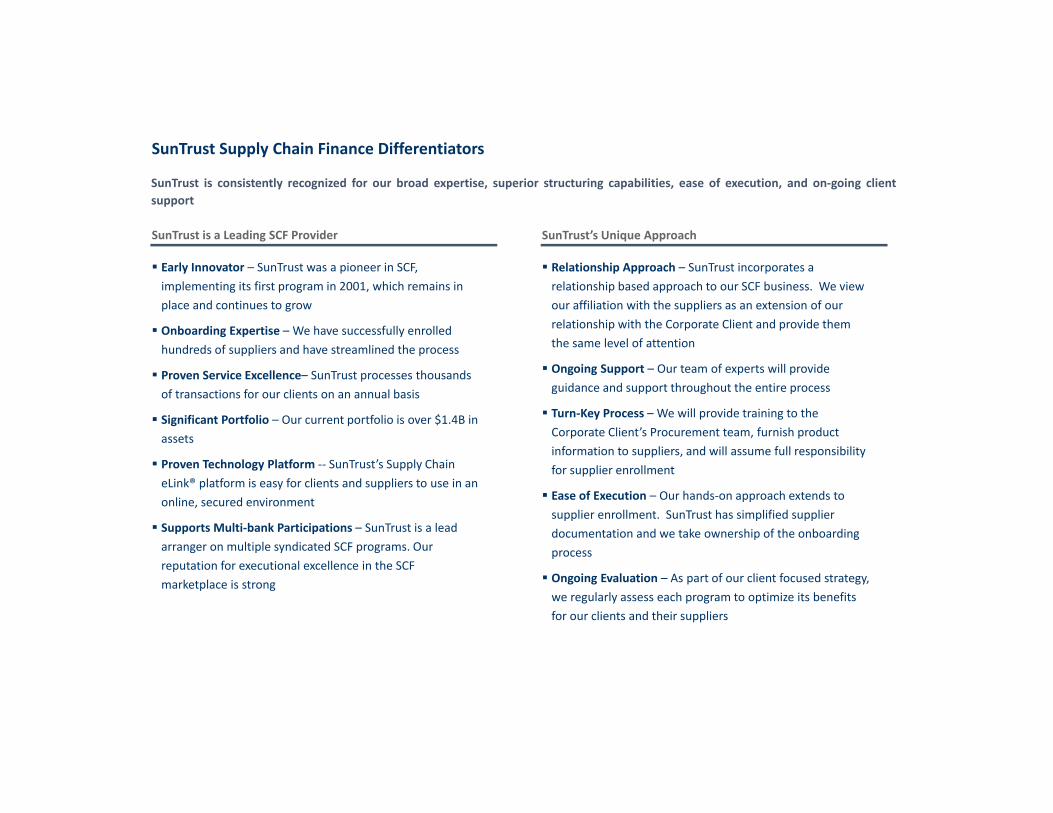

SunTrust Supply Chain Finance Differentiators

SunTrust is consistently recognized for our broad expertise, superior structuring capabilities, ease of execution, and on‐going clientsupport

SunTrust’s Unique Approach

Relationship Approach – SunTrust incorporates a relationship based approach to our SCF business. We view our affiliation with the suppliers as an extension of our relationship with the Corporate Client and provide them the same level of attention

Ongoing Support – Our team of experts will provide guidance and support throughout the entire process

Turn‐Key Process – We will provide training to the Corporate Client’s Procurement team, furnish product information to suppliers, and will assume full responsibility for supplier enrollment

Ease of Execution – Our hands‐on approach extends to supplier enrollment. SunTrust has simplified supplier documentation and we take ownership of the onboarding process

Ongoing Evaluation – As part of our client focused strategy, we regularly assess each program to optimize its benefits for our clients and their suppliers

SunTrust is a Leading SCF Provider

Early Innovator – SunTrust was a pioneer in SCF, implementing its first program in 2001, which remains in place and continues to grow

Onboarding Expertise – We have successfully enrolled hundreds of suppliers and have streamlined the process

Proven Service Excellence– SunTrust processes thousands of transactions for our clients on an annual basis

Significant Portfolio – Our current portfolio is over $1.4B in assets

Proven Technology Platform ‐‐ SunTrust’s Supply Chain eLink® platform is easy for clients and suppliers to use in an online, secured environment

Supports Multi‐bank Participations – SunTrust is a lead arranger on multiple syndicated SCF programs. Our reputation for executional excellence in the SCF marketplace is strong

“We’ve worked with the SunTrust Supply Chain Finance program for nearly 10 years. During this time, we have experienced the highest level of professionalism and courtesy from the SunTrust staff. The Confirmed Receivables funding process is simple and straight‐forward and we look forward to continuing our relationship with SunTrust in the future.”

Randy

SunTrust Bank Supply Chain Finance

Note: Individual surnames as well as company names have been omitted for confidentiality reasons

“We would absolutely recommend SunTrust , their service is excellent and the website, Supply Chain eLink is easy to use.”

Shannon

“Just a quick note to thank you and your team at SunTrust as we finish up our first year utilizing your SCF services for [Client]. The set up process was efficient and timely as we worked through the legal documents with our respective corporate lawyers. The help with working through the initial process and the training to utilize the new internet processing option was great. Kay and I have enjoyed working with the SunTrust team and look forward to our continued association.”

Shaun

“Everything that SunTrust hasdone with us has always met or exceeded our needs and the [Client] SCF Program is no exception, the program has worked flawlessly and has made my job much easier”.

Anthony

“I would recommend SunTrust to any suppliers selling receivables under [Client]’s Supply Chain Finance program. SunTrust has given us competitive rates and a flawless banking experience. We find web banking at SunTrust very user friendly and efficient”. Freddy

“We appreciate SunTrust’s competitive prices, their flexibility in scheduling payments and how easy they are to work with”.

Heather

“We have used a number of SCF websites and SunTrust’s eLink is absolutely the best. We get visibility into the entire transaction, we know exactly what the discount was and the amount we will be paid. Access to the invoice detail allows for reconcilement and the site is the easiest to use”.

Ron

SunTrust SCF Supplier Feedback

What Our Clients and Suppliers Have Been Saying About SunTrust:

Buyer Home Page Once you have signed on, the Supply Chain eLink home page will display the Buyer’s account summary

This page lists all active CRs and the corresponding invoice detail

Buyer Reports Page From this screen you can create reports based on your specified criteria

Reports may be viewed on the screen or exported into text, Excel or CSV format

Vendor Home Page Once a vendor signs on, the Supply Chain eLink home page displays an account summary under three tabs – Available for

sale, Pending Payments and Scheduled Payments

The first tab, Available for Sale, lists all outstanding CRs that may be offered to sell to SunTrust along with correspondinginvoice detail

The vendor can choose to sell specific CRs or sell all of them directly from this screen

Supplier Perspective & Industry Trends

Supply Chain Finance Best Practices • Maximize AP Automation & Approval Workflows

• Consider invoice scan, OCR, and scrub process• Automated business rules

• By invoice, supplier, PO range, tolerances• Accelerate average approval cycle to 3‐8 days• Streamline multi‐approver process

• Supplier Collaboration Portal • Invoice & supporting document submission • Direct supplier communications • Faster dispute turns and resolution• Minimize dispute resolution process

• Alternative Payment Methods • Take advantage of static discounts• Corporate card pull with indirect spend• Buyer initiated payments

• Standardize Payment Terms• Confirm the hundreds of different types of payment terms currently being utilized• Management should standardize terms across the vendor community or by business line• Simplifies contract management and A/P processes

• Procurement Incentives & Quantifiable Impacts • SCF programs are effectively marketed by procurement teams which own the vendor relationship• Incentives need to be in place to encourage team participation• Quantify the company benefit achieved through SCF program

• Extending DPO by an average of X days represents $XMM to finance a new store opening• Which means additional demand for Supplier’s products and services

• Business line challenges and competition

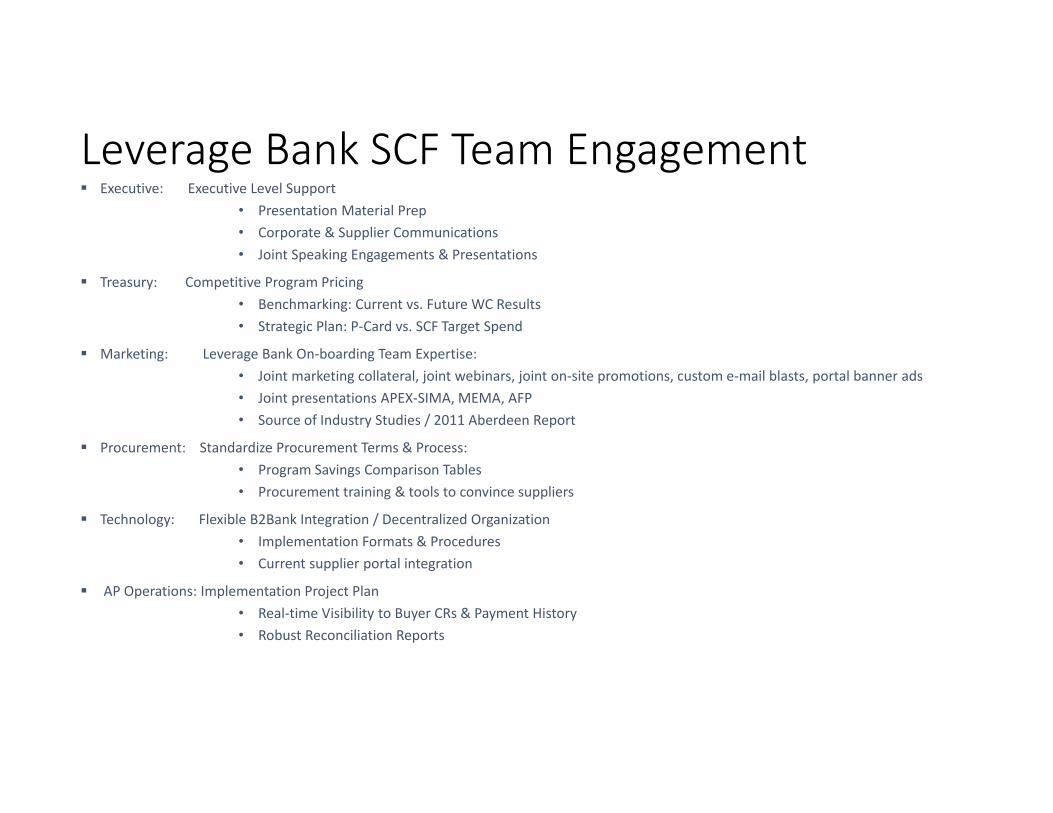

Leverage Bank SCF Team Engagement Executive: Executive Level Support

• Presentation Material Prep• Corporate & Supplier Communications • Joint Speaking Engagements & Presentations

Treasury: Competitive Program Pricing• Benchmarking: Current vs. Future WC Results• Strategic Plan: P‐Card vs. SCF Target Spend

Marketing: Leverage Bank On‐boarding Team Expertise: • Joint marketing collateral, joint webinars, joint on‐site promotions, custom e‐mail blasts, portal banner ads• Joint presentations APEX‐SIMA, MEMA, AFP • Source of Industry Studies / 2011 Aberdeen Report

Procurement: Standardize Procurement Terms & Process:• Program Savings Comparison Tables• Procurement training & tools to convince suppliers

Technology: Flexible B2Bank Integration / Decentralized Organization• Implementation Formats & Procedures • Current supplier portal integration

AP Operations: Implementation Project Plan• Real‐time Visibility to Buyer CRs & Payment History• Robust Reconciliation Reports

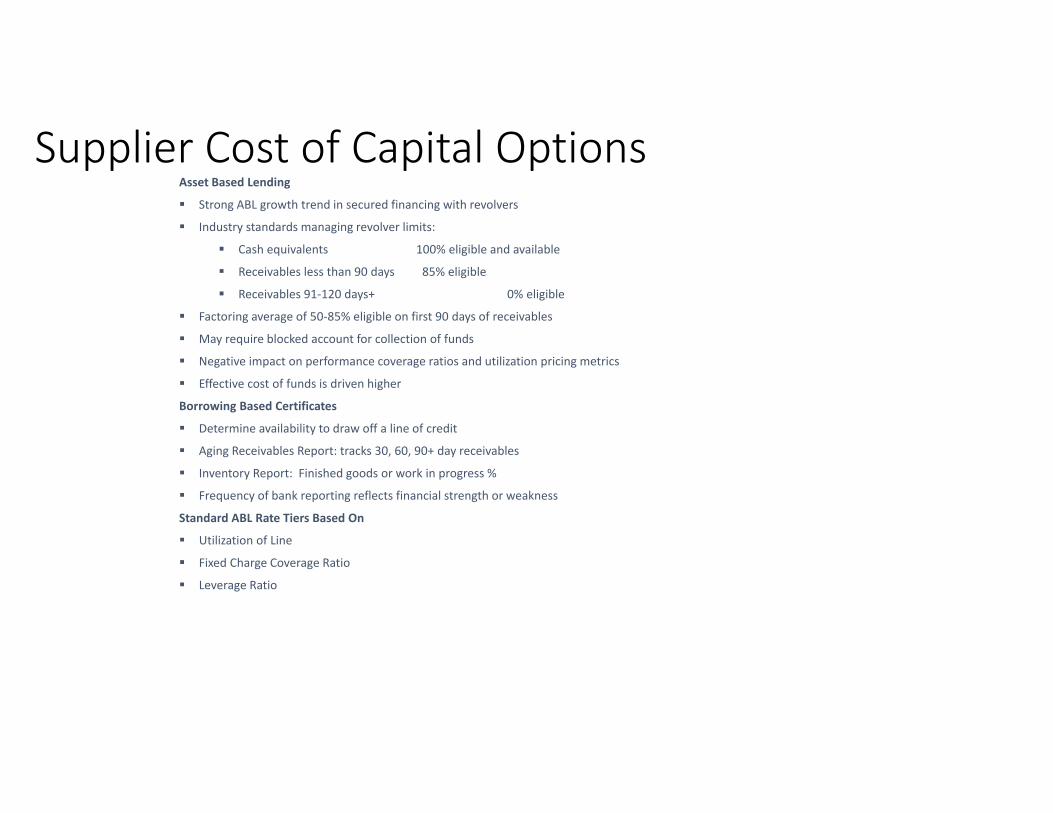

Supplier Cost of Capital Options Asset Based Lending

Strong ABL growth trend in secured financing with revolvers

Industry standards managing revolver limits:

Cash equivalents 100% eligible and available

Receivables less than 90 days 85% eligible

Receivables 91‐120 days+ 0% eligible

Factoring average of 50‐85% eligible on first 90 days of receivables

May require blocked account for collection of funds

Negative impact on performance coverage ratios and utilization pricing metrics

Effective cost of funds is driven higher

Borrowing Based Certificates

Determine availability to draw off a line of credit

Aging Receivables Report: tracks 30, 60, 90+ day receivables

Inventory Report: Finished goods or work in progress %

Frequency of bank reporting reflects financial strength or weakness

Standard ABL Rate Tiers Based On

Utilization of Line

Fixed Charge Coverage Ratio

Leverage Ratio

Impact on ABL Revolver Pricing Example: ABL Revolver of BB rated Supplier with average receivables of 90 days from BBB rated Buyer

Line Revolver SCF Discount

Utilization Rate Rate

Level 3: $50MM+ L+ 300 bps L+ 150 bps

Level 2: $25‐$50MM L+ 275 bps L+ 150 bps

Floor: $0‐$25MM L+ 250 bps L+ 150 bps

Must know current revolver price tier and performance pricing metrics.

Additional cash will improve fixed coverage ratio at month or quarter end.

If ABL pricing tiers are based on utilization with eligibility of only 85% of receivables less than 90 days, then the effective price tiers may actually be driven higher by 17.6% if eligibility is only $0.85 on the dollar ($1.00/$.85).

If SCF provides next day availability on receivables when discounting, then the effective rate of interest is the same as the published SCF program rate tied to the Buyer’s investment grade credit rating. (L+150 bps).

SCF Programs Offer Immediate Liquidity:

Strong source of off balance sheet financing for Suppliers

Reduce utilization of line to move to lower revolver pricing

Improve fixed charge coverage ratio to move to lower pricing tier

Additional bump in cash for monthly, quarterly, or fiscal year end reporting to improve credit rating

Improved credit rating can result in reductions in cost of capital

Supply Chain Finance Industry Trends• Corporate Clients

• AP Workflow Automation• Joint SCF and P‐Card Strategy• Average Payment Terms• Sourcing Coordination vs. Open Selection • Leverage Bank On‐boarding Team• Periodic Vendor Spend Analysis• Supplier Segmentation: Business Line, Division, Subsidiary, Region • Joint Marketing & Promotions • Multiple SCF programs• Technology partner programs• Dynamic Discounting• International Bank Payment Obligation (BPO) via SWIFT• New program actively growing across multiple industries

• Funding Banks• Market Pricing Compression Continues• Greater Awareness of SCF with Supplier Banks• Bank Integrated Approach to Working Capital Solutions• Insurance Funding Partners

• Strategic Suppliers• Single View Across Multiple Buyers • Request Favored Bank Programs• Single bank multi‐ program pricing • Push terms with tier 2 suppliers

Confirmed Receivables vs. Draft Acceptance • Instrument: Confirmed Receivable (aka Account Receivable)

• Instrument: Draft Acceptance (aka Confirmed Payable)

Governed by UCC Article 3 “Holder in Due Course” of negotiable

instruments No Perfection of Interest

No UCC filing No carve out consent

Bank Compliance State certificate of good standing Check OFAC‐SDN List

Supplier sells “rights” to future dated Time Draft

Supplier electronically endorses Time Draft over to bank

Bank becomes “holder in due course” of instrument

Supplier receives net proceeds at attractive discount

Buyer 3 way match completed Buyer issues Time Draft Treated like future dated check Buyer’s irrevocable obligation to pay Bank obligated to fund if purchased

from supplier

Supplier Buyer Bank

Governed by UCC Article 9 “Secured Transactions” Bank Perfection of Interest

Require UCC search UCC‐1 filing Carve out consent agreement

Bank Compliance State certificate of good standing Check OFAC‐SDN List

Buyer 3 way match completed Buyer issues a Confirmed Receivable

(CR) Buyer’s irrevocable obligation to pay Bank obligated to fund if purchased

from supplier

Confirmed Receivable (CR) is asset of supplier

Supplier sells CR to bank Supplier receives net proceeds at

attractive discount

Buyer Supplier Bank

CONFIRMED

ENDORSED

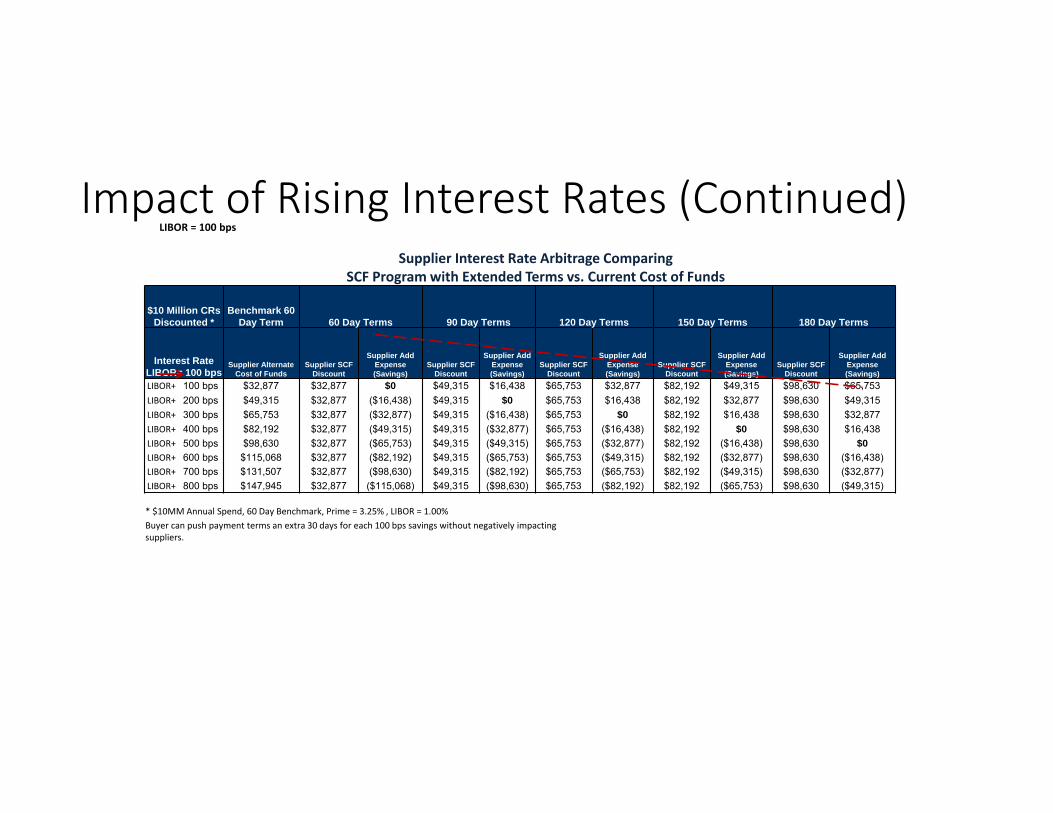

Impact of Rising Interest Rates Supplier Interest Rate Arbitrage Comparing

SCF Program with Extended Terms vs. Current Cost of Funds$10 Million CRs

Discounted *Benchmark 60

Day Term 60 Day Terms 100 Day Terms 140 Day Terms 180 Day Terms 220 Day Terms

Interest Rate LIBOR = 50 bps

Supplier Alternate Cost

of Funds

Supplier SCF

Discount

Supplier Additional Expense (Savings)

Supplier SCF

Discount

Supplier Additional Expense (Savings)

Supplier SCF

Discount

Supplier Additional Expense (Savings)

Supplier SCF

Discount

Supplier Additional Expense (Savings)

Supplier SCF

Discount

Supplier Additional Expense (Savings)