Meezan Bank · PDF fileThe Premier Islamic Bank Meezan Bank Designed and Produced by...

74

The Premier Islamic Bank Meezan Bank Designed and Produced by Circuit/FCB ANNUAL REPORT 2003

Transcript of Meezan Bank · PDF fileThe Premier Islamic Bank Meezan Bank Designed and Produced by...

The Premier Islamic BankMeezan Bank

Designed and Produced by Circuit/FCB

A N N U A L R E P O R T 2 0 0 3

In the name of Allah, The most Beneficent, The most Merciful

The Premier Islamic BankMeezan Bank

ANNUAL REPORT

2003

Our Vision≈Establish Islamic banking as

banking of first choiceº∆

Establish Islamic banking as banking of first choice to facilitate implementation of an equitable economic system, providing a

strong foundation for establishing a fair and just society for mankind.

Our Mission≈To be a premier Islamic bankº∆

To be a premier Islamic bank offering a one-stop shop for innovative value-added products

and services to our customers within thebounds of Shariah, while optimizing the

stakeholders» value through an organizationalculture based on learning, fairness, respectfor individual enterprise and performance.

KEY FIGURES AT A GLANCE

Annu

al Re

port

200

3

Key Corporate Values 1

Corporate Information 2

History 5

Milestones & Achievements 7

Key Business Units 8

Chairman»s Review 14

President»s Message 16

Shareholders» Profile 18

Shariah Board»s Profile 19

Notice of Annual General Meeting 20

Directors» Report to the Shareholders 22

Shariah Advisor»s Report 30

Statement of Compliance 32

Review Report to the Members 34

Auditors» Report 35

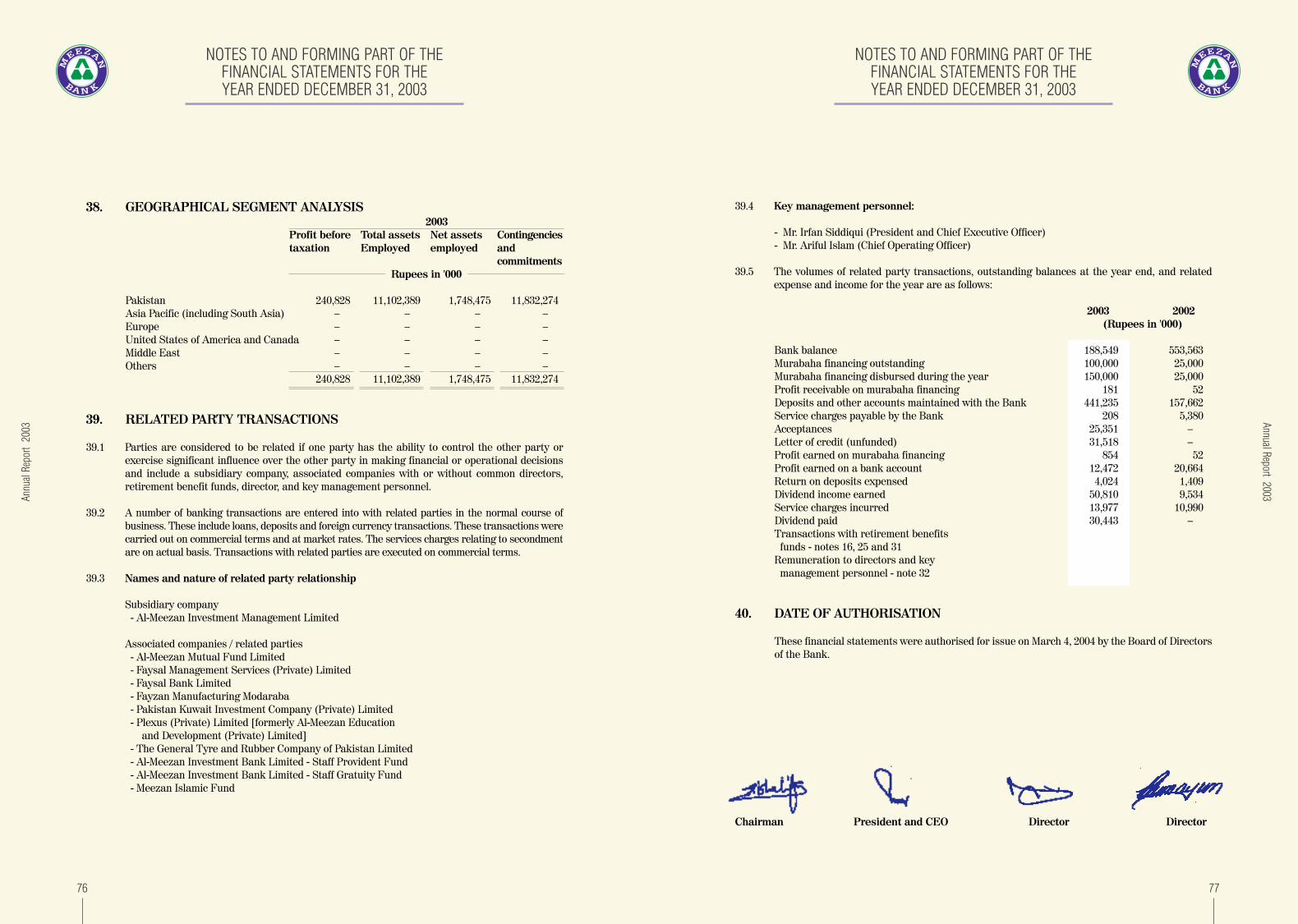

Balance Sheet 36

Profit & Loss Account 37

Cash Flow Statement 39

Statement of Changes in Equity 41

Notes to and Forming Part of the Accounts 42

Consolidated Financial Statements 79

Pattern of Shareholding 128

Correspondent Banking Network 131

Branch Network 134

Proxy Form

CONTENTS

Annual Report 2003

RRuuppeeeess iinn mmiilllliioonnss

DDeecc.. DDeecc.. DDeecc.. ** JJuunnee JJuunnee JJuunnee22000033 22000022 22000011 22000011 22000000 11999999

Paid-up Capital 1,064 1,001 901 901 721 721Shareholders» Equity 1,748 1,586 1,203 1,257 878 850Total Assets 11,102 6,971 2,053 2,179 1,314 1,180Financing 7,397 3,532 865 1,242 482 525Deposits 7,757 5,079 637 644 214 231Total Income 679 660 30 554 288 192Operating Expenses 255 195 36 101 64 13Profit/(Loss) Before Taxation 241 270 (35) 397 170 141Profit/(Loss) After Taxation 214 223 (54) 366 126 91

Earnings per share - pre tax (Rs.) 2.26 2.81 (0.38) 4.44 2.36 1.96Earnings per share - after tax (Rs.) 2.01 2.10 (0.58) 4.09 1.75 1.26Break-up Value (Rs.) 16.43 15.84 13.35 13.95 12.17 11.80Cash Dividend (%) 5.00 5.00 √~ 17.50 15.00 √~Stock Dividend (%) 10.00 10.00 √~ √~ √~ √~

* Represents figures for the six-month period ended December 31, 2001 due to change in year end from June to December.

2,000

1,500

1,000

500

0Dec2003

Dec2002

Dec2001

June2001

June2000

June1999

SHAREHOLDER’S EQUITY

7,500

0Dec2003

Dec2002

Dec2001

June2001

June2000

June1999

TOTAL FINANCING

7,0006,5006,0005,5005,0004,5004,0003,5003,0002,5002,0001,5001,000

500

12,000

10,000

8,000

4,000

0Dec

2003Dec

2002Dec

2001June2001

June2000

June1999

TOTAL ASSETS

6,000

2,000

8,000

6,000

2,000

0Dec

2003Dec

2002Dec

2001June2001

June2000

June1999

TOTAL DEPOSITS

4,000

1,000

3,000

5,000

7,000

Rs.

in m

illio

nsR

s. in

mill

ions

Rs.

in m

illio

nsR

s. in

mill

ions

Enlightenment comes intothe life of one who lets the

purity of light enter.The enrichment that followsis two fold: a comfortablelife fulfilling all your basicneeds in this world, anda conformity with the

Shariah laws that makes the Hereafter better.

1

Annual Report 2003

RelationshipsAre long term with Meezan Bank. We recognize and value our customers» needsabove all, and strive to ensure their fulfillment. All customers are treated withprofessionalism and in a friendly manner. It is our endeavor to ensure that theyreceive efficient & timely service. The Meezan Bank experience is a unique one.

Core ValuesShariah Compliance, Integrity, Professionalism,Service Excellence, Social Responsibility.

BrandPersonality

Staff Committed, motivated, and professionallytrained employees who are empathetic totheir customer»s needs.

A sober and established, strong, empathetic, professional person; who isan extremely loyal and dependable friend and business partner, and iscommitted to offering comprehensive value-based Shariah-compliantfinancial solutions.

KEY CORPORATE VALUES

CORPORATE INFORMATION

3

Annual Report 2003

CORPORATE INFORMATION

MMAANNAAGGEEMMEENNTTIrfan Siddiqui President & CEOAriful Islam Chief Operating OfficerNajmul Hassan Corporate & Business DevelopmentGohar Iqbal Shaikh Finance & Human ResourcesAyaz Wasay Treasury & Financial InstitutionsAqeel Siddiqui Retail BankingArshad Majeed OperationsMohammad Haris Corporate FinanceSohail Khan SME & Auto LeasingEmad ul Hasan Internal Audit & ComplianceMehnaz Ikram Legal AdvisorFaiz-ur-Rehman Information TechnologyMunawar Rizvi General Services & AdministrationZafar Ali Khan Marketing & Housing Finance

LLEEGGAALL AADDVVIISSOORRRizvi, Isa, Afridi & Angell

AAUUDDIITTOORRSSA.F. Ferguson & Co.

RREEGGIISSTTEERREEDD OOFFFFIICCEE3rd Floor, PNSC Building, Moulvi Tamizuddin Khan Road, Karachi-74000, Pakistan.Ph: 9221-5610582 Fax: 9221-5610375Website: www.meezanbank.com Email: [email protected]

RREEGGIISSTTRRAARR && SSHHAARREE TTRRAANNSSFFEERR OOFFFFIICCEETHK Associates (Pvt.) LimitedGround Floor, Sheikh Sultan Trust Building No. 2, Beaumont Road, Karachi-75530, Pakistan.Ph: 9221-5689021 Fax: 9221-5655595

Annu

al Re

port

200

3

2

BBOOAARRDD OOFF DDIIRREECCTTOORRSSH.E. Sheikh Ebrahim bin Khalifa Al-Khalifa ChairmanNaser Abdul Mohsen Al Marri Vice ChairmanIrfan Siddiqui President & CEOZaigham Mahmood RizviMohamed Abdul-Rehman HussainTarik KivancMazen Khalid Al-BraikanAriful IslamRana Ahmad HumayunYousif Saleh Khalaf

SSHHAARRIIAAHH BBOOAARRDDJustice (Retd.) Muhammad Taqi Usmani ChairmanDr. Abdul Sattar Abu GhuddahSheikh Essam M. IshaqDr. Muhammad Imran Usmani

EEXXEECCUUTTIIVVEE CCOOMMMMIITTTTEEEENaser Abdul Mohsen Al MarriZaigham Mahmood RizviMohamed Abdul-Rehman HussainIrfan Siddiqui

AAUUDDIITT CCOOMMMMIITTTTEEEEZaigham Mahmood RizviMohamed Abdul-Rehman HussainIrfan Siddiqui

CCOOMMPPAANNYY SSEECCRREETTAARRYYGohar Iqbal Shaikh

AADDVVIISSOORRYYDr. Muhammad Imran Usmani Shariah AdvisorZafar Aziz Osmani Human Resource Advisor

HISTORY

1947 The inception of Pakistan as the first IslamicRepublic created in the name of Islam.

1949 The Objectives Resolution was adopted bythe first Constituent Assembly based onthe ideology of a sovereign Islamic state.This was the first step in the conceptiontowards Pakistan»s Constitution.

1956 The first Constitution defined Islam as theState Religion and all laws to be accordingto the injunctions of the Quran and Sunnah.

1962 The establishment of Council of IslamicIdeology (CII) was followed by the conceptionof the second constitution of Pakistan.

1973 The third constitution of Pakistan waspassed allowing comprehensive legislationon Islamic principles and establishment ofFederal Shariat Court.

1980 CII presents report on the elimination ofinterest genuinely considered to be the firstmajor comprehensive work in the worldundertaken on Islamic banking and finance.

1985 Commercial banks change their nomen-clature stating all Rupee saving accounts asinterest-free. However, foreign currencydeposits in Pakistan and on lending offoreign loans continued as before.

1991 Procedure adopted by banks in 1985 wasdeclared unIslamic by the Federal ShariatCourt (FSC). The Government and somebanks/DFIs made appeals to the ShariatAppellate Bench (SAB) of the SupremeCourt of Pakistan.

1997 Al-Meezan Investment Bank is establishedas an Islamic Investment Bank withDr. Imran Usmani appointed as resident Shariah Advisor.

1999 The Shariat Appellate Bench of the SupremeCourt of Pakistan rejects the appeals anddirects all laws on interest banking to cease. The government sets off a high levelcommission, task forces and committees toinstitute and promote Islamic banking onparallel basis with conventional system.

2001 The Shariah Supervisory Board isestablished at Al-Meezan InvestmentBank led by Justice (Retd.) MuhammadTaqi Usmani as Chairman. The StateBank sets criteria for establishment ofIslamic commercial banks in privatesector and subsidiaries and stand-alonebranches by existing commercial banks toconduct Islamic banking in the country.

2002 The first Islamic banking license is issued toMeezan Bank by the State Bank of Pakistan.Simultaneously, Meezan Bank acquires thePakistan operations of Societe Generale, aFrench commercial bank. President GeneralPervez Musharraf inaugurates the Bank.

2003 A Musharakah-based Export RefinanceProduct is designed by the State Bank inorder to provide export finance to eligibleexporters on the basis of Islamic modes offinancing. Efforts are underway to developIslamic money market instruments like IjarahSukuk to facilitate the banks in respect ofliquidity and SLR management. In addition, afull fledged Islamic Banking Department hasnow been created in the SBP.

5

Annual Report 2003

One tree gives rise to a forestof trees over a period of years.

Thisprinciple works withMeezanBank products

because of their convenienceand versatility. They are

customized toyour lifestyleand conform to the principlesof Shariah, thus multiplying

your returns quickly andefficiently.

The Story of Riba-freeBanking in Pakistan

Nature brings to us flowersthat spread their seeds farand wide to germinate andgrow. Following in Nature’s

footsteps, Meezan Bankgive its customers bankingsolutions through a branch

network that is spreadacross the country and

ever growing.

● Islamic Auto Leasing

● Islamic Housing Finance

● Islamic commercial banking license

7

● Acquisition of Societe Generale, Pakistan

● Fayzan Modaraba √ 1st Structured Off-Balance SheetProject Finance

● Development of Islamic banking software √ Islamic Banker

Annual Report 2003

● Expansion of branch network nationwide

Islamic Housing FinanceEasyHome

● Islamic Export Refinance Scheme

● Meezan Islamic Fund √ Pakistan»s 1stShariah-compliant open-end equity fund

MILESTONES & ACHIEVEMENTS

● Sitara Group Musharakah Term Finance Certificate

9

Annual Report 2003Annu

al Re

port

200

3

8

It is a very comprehensive product basedon the Diminishing Musharakah mode, that provides the market a long awaited totally Shariah-compliant mortgage facility that allows home purchase, building, renovation, and even replacement of an existing mortgage.

Bringing this facility to the market involvedan extensive process addressing various critical areas: ProductDevelopment and Shariah approval, internal risk management infrastructure encompassing credit processing, analysis & credit initiation, Systems for portfolio riskmanagement and processing control, CustomerSales & Service through our branch network andCall Center, and External Infrastructure coveringlegal, property appraisal, property search,verification, and real estate agencies.

Meezan Bank has committed itself to ensuringthat the nation»s critical need for Housing is notonly supported, but led by Islamic HousingFinance, with a comprehensive product, verycompetitive pricing, and an application processthat is smooth, fair and quick, ensuring access toall eligible applicants. As the pioneer, the Bank

has established a very thorough and customerfriendly experience for all applicants, whereby

risk is controlled, service is paramount, and dreams are turned into reality as soon

as possible, by the grace of Allah Almighty.

Highly trained mortgage specialists are

responding to the

overwhelming demand in the

market. Just in the first month of the launch, the

pipeline of approved applications stood at over PKR 100 million.

Over the past year and ahalf, Meezan Bank»s CarIjarah (Auto Leasing) product has gained overall market recognitionand has developedinto an important part of MBL»s overall product offering. The product has grown all over the country with a portfolio of Rs. 291 million as of 31st Dec 2003 with no non-performing contracts.

The product is now offered in Karachi, Lahore, Faisalabad,

Islamabad & Multan. The up-country marketshave also shown tremendous acceptability ofthe product.

Our focus over the coming year is to take Car Ijarah to the next level of success by significantly increasing our investment in this business line. The product will target employees of well-reputed local and multinational companies and self-employed professionals. Active marketing and sales efforts will be employed over the coming year to increase public awareness of the product. A comprehensive dealer network is alsobeing developed to establish a regular source of

business leads.

In view of our past experience, we expect a very positive response to our market-ing initiative and are in the process of

actively building the human andinfrastructural resources needed

to achieve the targets set for thisbusiness line. Our experience

with the product over the last year has given usthe confidence that with active marketing andresource allocation, Car Ijarah will very soondevelop into a major profit-center of the Bank.

Just in the first month ofthe launch, the pipelineof approved applicationsstood at over PKR 100million.

Housing FinanceThe nation»s first Islamichousing facility, EasyHomewas officially launched in December.

Our focus over thecoming year is to takeCar Ijarah to the next levelof success by significantlyincreasing our investmentin this business line.

Car Ijarah

KEY BUSINESS UNITS KEY BUSINESS UNITS

11

Annual Report 2003

KEY BUSINESS UNITS

Water that is flowing is pureand sparklingly clean just

like the Riba-Free bankingsolutions that Meezan Bankgives its customers to helpmake your money grow

safely, securely andprofitably within the

parameters of Shariah.

The SME sector forms the backbone of anyeconomy and is generally regarded as a high-return sector for banks with its unique set ofrisks and return. In Pakistan, this sector isyet largely untapped by the bankingcommunity, although awareness about theopportunities offered in this sector is on therise. The government is also focusing onpromoting this sector and the State Bank hasrecently issued a separate set of PrudentialRegulations for SMEs, under which theregulatory compliance requirements for SMEcustomers have been structured keeping inview the set-up, constraints and dynamics ofSME business entities.

The SME business is a priority sector for MeezanBank because of its socio-economic importanceand the need to strengthen the building blocks ofthe nation. The sector is also important becauseof the huge business opportunity it offers andthe fact that a vast majority of entrepreneurs inthis sector have a very keen Shariah mindset,placing Meezan Bank in a unique advantageousposition as the preferred bank for this sector.

After starting our SME business operations inOctober 2002, the business portfolio grew to anasset size of Rs. 341 million spread over 35

clients by 31st December 2003, with no non-performing contracts. The initiative alsogenerated non-funded business of Rs. 520million over the year.

Our targets for the upcoming year aggressivelyfocus on increasing our SME portfolio. We areactively developing the human andinfrastructural resources necessary to managethis business and are keenly looking forwardtowards building this business line as a majorprofit center in the near future.

Our targets for the up-coming year aggressivelyfocus on increasing ourSME portfolio. We areactively developing thehuman and infrastructuralresources.

The SME sector formsthe backbone of anyeconomy and is generallyregarded as a high-returnsector for banksº

Small & MediumEnterprise (SME)

Business

KEY BUSINESS UNITS

Annu

al Re

port

200

3

12

KEY BUSINESS UNITS

13

Annual Report 2003

The Corporate & Investment Banking Unitcontinues to provide comprehensive andinnovative financial solutions to the Bank»s clientbase through a diverse product offering. Wenurture and develop long-term relationshipswith clients by understanding their uniquefinancing requirements and providing Shariah-compliant financing solutions.

The focus continues on tailoring solutions tomeet customer financing needs which arechanging in a fast changing global environment.These solutions include use of different modesof Islamic finance and/or their hybrids formeeting short & long-term financing and othertrade related requirements of our customers.Murabaha and Ijarah continue to be the mostactively used financing contracts, which enableMBL to meet the working capital needs of itscustomers and to finance purchase of plantand machinery. The Bank also undertook variousinnovative transactions during the year bydeveloping financial structures based on theconcepts of Diminishing Musharakah, ShirkatulWujooh and Musharakah.

Under Diminishing Musharakah, Meezan Bankstructured a financing arrangement for SitaraEnergy Limited (SEL). The asset purchased under this financing is divided into a number of notional

units and it is agreed that SEL will purchase theunits of the share of the Bank gradually, thusincreasing its own share until all the units of theBank are purchased by SEL so as to become thesole owner of the asset after a specified period.SEL pays rent for using the Bank»s share in theasset and thus the transaction ensures a Shariah-compliant solution for the Customer as well as forthe Bank.

MBL has entered into a Musharakaharrangement using the concept of ShirkatulWujooh with a reputable supplier of engineeringequipments. In Shirkatul Wujooh one or morepartners have no investment in the venture.They purchase commodities on deferred price,and sell them at spot. The profit earned isdistributed between them at an agreed ratio. Byusing this concept MBL has opened a UsanceLC for the import of certain engineeringequipments. After the arrival of equipment,MBL»s partner would sell the importedequipments in local market on cash and theprofit so earned would be shared between MBLand its partner according to the agreed ratios.Loss, if any, would also be shared between thepartners as per their investment ratio.

MBL during the year also structured alandmark Musharakah transaction withAssociated Constructors Limited (ACL) √ aleading contracting company, to participate inPhase 2 of Creek City project of DefenceHousing Authority (DHA). The Creek Cityhousing development is expected to be alandmark project for the city of Karachi.

These products are being used to further diversifythe Bank»s expanding financing portfolio and theydemonstrate the focus and expertise the Bankpossesses in developing new and innovativeproducts. With the help of existing and newproducts, we continue to aggressively expand our

The focus continues ontailoring solutions tomeet customer financingneeds which are changingin a fast changing globalenvironment.

Corporate & InvestmentBanking corporate portfolio by adding large multinationals

and prime local corporates/groups whichcurrently include names such as Al-Abid Silk, Al-Karam Textile, Alcatel, Crescent Textile,Crescent Steel, Dawood Group, Dewan Group,Engro Chemical, Fatima Group, Fazal Group,General Tyre, Gul Ahmed Textile, Ibrahim Fibres,ICI, MIMA Group, Nishat Group, PSO, PremierGroup, Rafhan Maize, Shafi Group, Siemens andSitara Group.

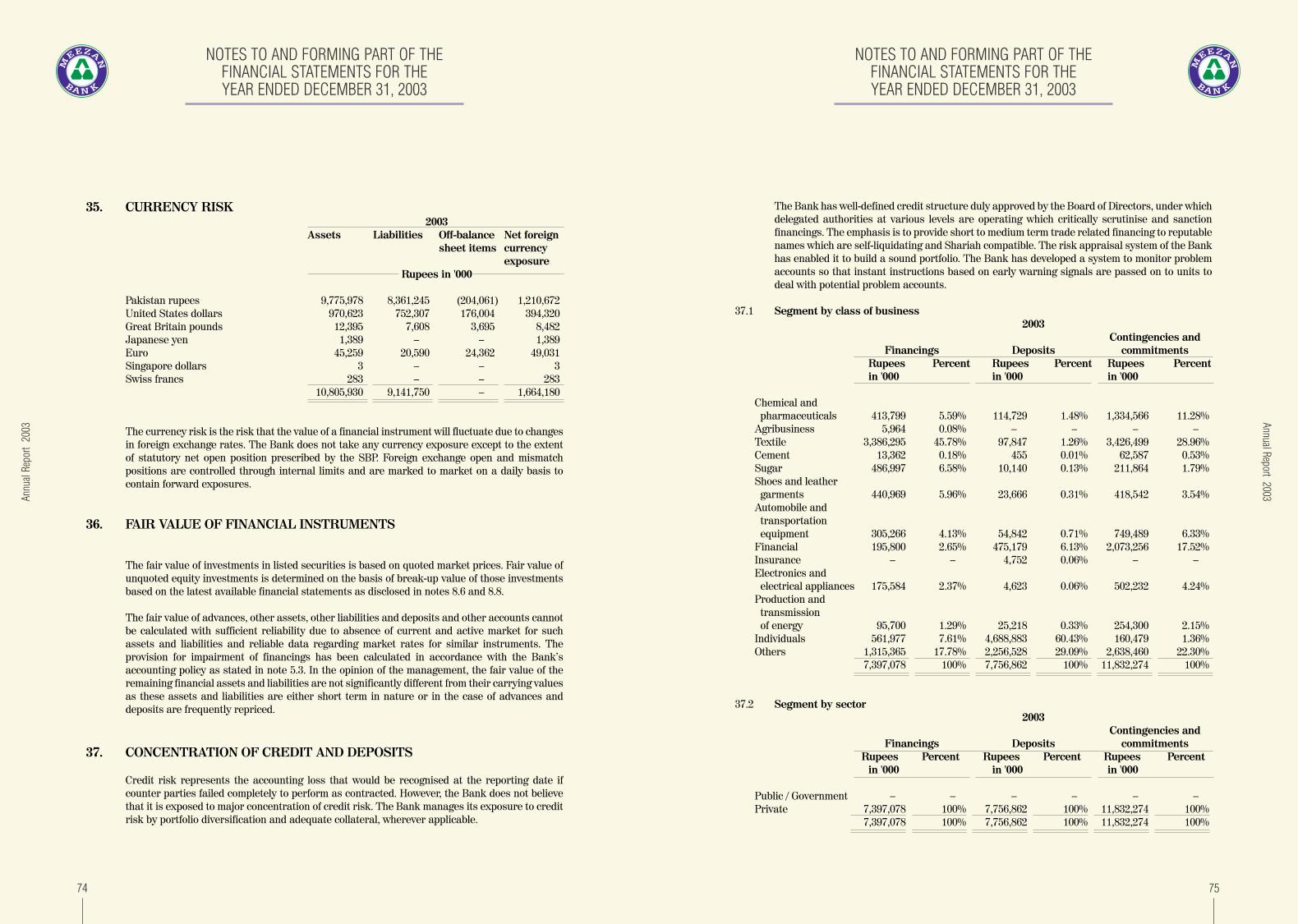

The total financing portfolio of the Bank as onDecember 31, 2003 amounted to Rs. 7.40billion as compared to Rs. 3.53 billion as onDecember 31, 2002, representing an increaseof 110%. The portfolio is well diversified withmajor concentration in the textile sector sincethat is the backbone of the Pakistan economy.Sector distribution of the financing portfolio isshown below:

Another major breakthrough for Meezan Bankduring the year was the launch of the IslamicExport Refinance Scheme Part II which wasdeveloped in close coordination with the StateBank of Pakistan. This has now enabled exportersto avail financing at concessional rates under bothPart I and Part II schemes of the SBP, IslamicExport Refinance Scheme. Meezan Bank hasalready disbursed funds to many customers underthis scheme some of whom are: Al-Karam Textile,

Fatima Group, Gul Ahmed Textile, MIMA Group,Nishat Group, Shafi Group and Sitara Group.

The Corporate & Investment Banking Unit alsoprovides a range of advisory services integratingindustry, product and regional specialization tohelp businesses address their strategic issues andformulate and execute dynamic businessstrategies. The Unit put together a PKR 910million Syndicated Short Term Islamic FinanceFacility to Saadullah Khan & Brothers, one of theleading construction firms of Pakistan. The Unitalso advised the Privatisation Commission,Government of Pakistan on the divestment ofshares of Sui Southern Gas Company Limited aspart of a consortium through the domestic stockexchanges. The offer represents a record settingissue as it was over-subscribed by fifteen times.

Textile Spinning15%

Textile Weaving1%

Textile Composite23%

Textile Others6%Sugar

7%

Leather6%

Auto4%

Financial3%

Electronics2%

Energy1%

Individuals8%

Others18%

Chemicals6%

SECTORAL BREAKUP OF FINANCING PORTFOLIO

The total financing port-folio of the Bank as onDecember 31, 2003amounted to Rs. 7.40billion as compared toRs. 3.53 billion as onDecember 31, 2002,representing an increaseof 110%.

CHAIRMAN»S REVIEW

Annu

al Re

port

200

3

14

CHAIRMAN»S REVIEW

15

Annual Report 2003

The ongoing success of Meezan Bank is not justan accomplishment for its employees andstakeholders, it is in fact a clear success forIslamic Banking, both in Pakistan as well asacross the globe. As more and more peoplerealize the benefits of the Islamic model offinance, what began as a little knownalternative system has grown into a full-fledgedglobal industry experiencing phenomenalgrowth in assets, market penetration, and newproducts. Meezan Bank, with its expandingproduct menu and branch network, is allowingpeople from all walks of life to undertake Riba-free financial transactions.

It is a privilege for me to present MeezanBank»s annual report for the year 2003. Asbefore, the Bank continues to carry forwardits mission at the forefront of Islamic bankingin Pakistan. As an institution dedicated solelyto offering Shariah-compliant avenues, itleads the market with innovative researchand development in providing a variety ofproducts and services that are in adherenceto the dictates of Shariah. Since the Bank»sinauguration in September 2002, it is alreadysuccessfully operating 10 branches acrossPakistan with more planned for this year aswell. Our goal is to provide the highest qualitycustomer service using innovative Shariahcompatible products, which cater to allmodern day customer needs.

In the banking industry, commercial bankswere initially reluctant in starting Islamicbanking on a wide scale, fearing uncertaintyin market potential. Today however, largebanks are beginning to flex their muscles asthey now see an enabling environment thatoffers Islamic banking the opportunity tocompete as well as a market that has clearly

shown its demand for such products. Keymarket players are opening Islamic windows in an effort to attain some of this lucrativemarket share. With this increased competition,the industry will only benefit, as all participantsstrive to offer effective value propositionscoupled with service efficiency.

Meezan Bank, while welcoming and supportingthis new strategic shift by conventional banks, isgearing up strategically for the increasedcompetition and is focused on maintaining alean and fit organization by controlling costs andmaximizing our depositors and share-holders»profits. The issue of excess liquidity and productdevelopment remain challenges for IslamicBanks. We welcome the establishment of IslamicBanking Division at the SBP which will enable itto regulate the Islamic Banks effectively.

In all, we remain very confident that MeezanBank is positioned to continue to lead theIslamic banking forum in Pakistan. We believeso because:

Meezan Bank, with its expanding product menu andbranch network, is allowing people from all walks oflife to undertake Riba-free financial transactions.

■ Meezan Bank has a team of experiencedbanking professionals who have shared valuestowards the development of Islamic banking.

■ The Bank has a very pro-active ShariahSupervisory Board comprising of leadinginternationally renowned scholars.

■ A Shariah scholar of sound standing andrepute supervises the day-to-day activities ofthe Bank.

■ The Bank remains committed inmaintaining a full range of internal controlsystems and procedures, which ensuresbest management practices.

■ The main shareholders of the Bank areleading financial institutions that addsignificant value to the Bank either directlythrough its Board representation, orindirectly by way of synergies throughregional cooperation and syndications.

The Government of Pakistan and the State Bankof Pakistan continue to give us support in allspheres to provide impetus to the growth ofIslamic banking. We express our gratitude for thecommitment shown by them towards theestablishment of an Islamic financial economy.The SBP now has an independent IslamicBanking Department that ensures effectiveregulation of all Islamic banks and is taking a

proactive role in meeting the various challengeswe face. The Government of Pakistan alsocontinues to facilitate the Islamic bankingindustry by introducing more and moreinvestment opportunities. We would like to thankthe President of Pakistan, General PervezMusharraf once again for his continued supportand for his landmark inauguration in 2002, to thefinance Minister Mr. Shaukat Aziz and GovernorSBP, Dr. Ishrat Husain, for their encouragementand great personal interest in promoting thecause of Islamic banking in Pakistan.

We congratulate the government insuccessfully reviving an economy that ispaving the way for Pakistan in becoming aregional and global economic player. I wouldlike to thank the State Bank of Pakistan for itscontinuous support in the regulatory frame-work and further development in IslamicBanking. I also thank our shareholders, fellowBoard members, members of the ShariahSupervisory Board and employees for theircommon unrelenting mission in makingMeezan Bank the premier and dedicatedIslamic bank of Pakistan.

HH..EE.. SSHHEEIIKKHH EEBBRRAAHHIIMM BBIINN KKHHAALLIIFFAA AALL--KKHHAALLIIFFAAChairman

Since the Bank»sinauguration in September2002, it is alreadysuccessfully operating 10branches across Pakistanwith more planned for thisyear as well.

PRESIDENT»S MESSAGE

Annu

al Re

port

200

3

16

clients. The essential feature of this instrumentis the requirement for an underlying asset thatis financed by the Bank on a deferred paymentbasis. This mode of finance provides a fixed rateof return to the Bank, which is acceptable fromthe Shariah perspective. Other financing modesinclude Ijarah, Mudaraba and Musharakah. Onemajor recent breakthrough for Meezan Bankwas the pioneering introduction of an IslamicExport Refinance Scheme, which enables us toprovide export refinance at concessional ratesunder Shariah-compliant instruments.

We are also implementing robust and aggressivestrategic initiatives on the consumer bankingside. The Bank has grown its branch network toten branches across all major cities nation-wideto date, and we envision growing this network tosome 15 branches in the very near future.Providing our customers accessibility andconvenience is a prime target, within anatmosphere and culture of dedicated service andrecognition of their needs. Our expandingproduct menu provides a range of depositoryproducts that ensure easy accessibility,unmatched stability, and strong return oninvestment. On the financing side, we provideIslamic auto finance with Car Ijarah, a productthat offers very competitive pricing and quickturn around time. We have also launched ourIslamic Home Finance proposition, Easy Home, avery comprehensive product that provides themarket a long awaited totally Shariah-compliantmortgage facility that allows home purchase,building, renovation, and even replacement of anexisting mortgage. In fact, the market responseto EasyHome has been phenomenal, as peoplehave been very desirous of a Halal facility withwhich to acquire their own homes.

Our Call Center is geared to attain the nextlevel in alternate distribution by ensuringdedicated convenience and personalizedcustomer attention, while nation-wide ATMaccess is also being put in place. We are hencevery excited and eager to provide the marketwith a broad range of consumer bankingproducts and services, ones that not only meet

our customers» needs, but do so in a veritablyconfirmed Shariah-compliant manner coupledwith dedicated service excellence.

We gratefully acknowledge the unwaveringcommitment and support demonstrated bythe State Bank of Pakistan to Meezan Bank,and in particular Governor Dr. Ishrat Husainas well as the Federal Minister for Finance,Mr. Shaukat Aziz, in setting the path forIslamic banking in Pakistan. We believe thatthe future of Islamic banking is bright andwith the support of the Government and ourcustomers, Meezan Bank will successfullyfulfill its responsibility to play a pioneeringrole in setting the true foundation of Islamicbanking in Pakistan, Inshallah.

IIRRFFAANN SSIIDDDDIIQQUUIIPresident & CEO

PRESIDENT»S MESSAGE

Meezan Bank stands today, Alhamdolillah, at anoteworthy and critical juncture of its evolutionas the premier Islamic Bank in Pakistan. Thebanking sector is showing a significantparadigm shift away from traditional means ofbusiness and is catering to an increasinglyastute and demanding financial consumer whois also becoming keenly aware of IslamicBanking. Meezan Bank bears the criticalresponsibility of leading the way forward inestablishing a real, stable, and dynamic Islamicbanking system in Pakistan.

Meezan Bank was first established as aninvestment banking entity in October of 1997,and entered the market with the clear butformidable mandate of establishing andpromoting Islamic banking. Embedded within adeep-rooted conventional financial system andfaced with a somewhat skeptical publicviewpoint doubtful of the effective applicabilityand even veracity of the Islamic financialmodel, the Bank faced an uphill task enormousby any measure. But with the mercy of AllahAlmighty, Meezan Bank made fundamental andsignificant progress forwards, and in doing soestablished a strong and credible managementteam comprised of experienced professionals,which achieved a strong balance sheet withexcellent operating profitability, including acapital adequacy ratio that placed the Bank atthe top of the industry, a long-term entity ratingof A+, and a short-term entity rating of A1+,the highest short-term rating.

Meezan Bank, we strive to find commonalitieswith the conventional banking system withabsolutely no compromise on Shariah rulings.The Bank has developed an extraordinary

research and development capability bycombining investment bankers, commercialbankers, Shariah scholars and legal experts todevelop innovative, viable, and competitivevalue propositions that not only meet therequirements of today»s complex financialworld, but do so with the world-class serviceexcellence that our customer»s demand, allwithin the bounds of Shariah. Furthermore, theBank has built a strong Information Technologyand customer knowledge-based focus thatcontinues to use state-of-the-art technology and

systems. The Bank»s Corporate and InvestmentBanking business unit is geared towards nur-turing and developing a long-term relationshipwith clients by understanding their uniquefinancing requirements and providing Shariah-compliant financing solutions. On the asset side,the Murabaha product is the most actively usedfinancing contract which enables an Islamicbank to finance the acquisition of fixed capitalassets and meet the working capital needs of

17

Annual Report 2003

At Meezan Bank, we striveto find commonalities withthe conventional bankingsystem with absolutely nocompromise on Shariahrulings.

Meezan Bank:Shariah Compliant

Financial SolutionsMeezan Bank will success-fully fulfill its responsibilityto play a pioneering role insetting the true foundationof Islamic banking inPakistan, Inshallah.

SHARIAH BOARD»S PROFILE

19

Annual Report 2003

SHAREHOLDERS» PROFILE

Annu

al Re

port

200

3

18

Pakistan Kuwait Investment Company (Private)Limited (PKIC) is a 50:50 joint venture betweenthe Governments of Pakistan and Kuwait. With ashareholders» equity of Rs. 9.9 billion and an assetbase of approximately Rs. 16.5 billion (December2003), PKIC is one of the most profitable andrespected financial institutions in Pakistan. It iscommonly referred to as the epitomy of asuccessful sovereign joint venture. PKIC is thefirst financial institution in Pakistan, which hasbeen rated AAA (Triple A) for medium to longterm by JCR-VIS Credit Rating Company Limited,an affiliate of Japan Credit Rating Company.

Shamil Bank of Bahrain E.C. is a leadingfinancial institution and is a subsidiary of theglobally renowned Dar-Al-Maal-Al-Islami Group(DMI) based in Geneva. The Group has sizeableinvestments in Pakistan and has played adominant role in the economic development ofPakistan by arranging cross border funds.

Islamic Development Bank, Jeddah, (IDB) is aninternational financial institution establishedin 1975 in pursuance of a declaration of theconference of Finance Ministers of Muslimcountries, to foster economic development andsocial progress in Member (Islamic) countries.

The Bank participates in equity capital andgrants loans for productive projects andenterprises besides providing financialassistance in other forms for economic andsocial development. it accepts deposits andmobilizes financial resources through Shariahcompatible modes. IDB has a capital base ofapproximately US$5 billion and enjoys apresence in 53 member countries.

Kuwait Awqaf Public Foundation is attached tothe Ministry of Awqaf & Islamic Affairs,Government of Kuwait. The Foundation has aglobal investment portfolio and is strictlygoverned by Shariah principles.

Saudi Pak Industrial & Agricultural InvestmentCompany (Private) Limited is a joint venturebetween the Kingdom of Saudi Arabia and theGovernment of Pakistan to promote industrialdevelopment in Pakistan. It has a total balancesheet size of Rs. 10 billion with a shareholders»equity amounting to Rs. 3.5 billion.

SShhaarreehhoollddiinngg SSttrruuccttuurree RRss iinn mmiilllliioonnss

Pakistan Kuwait Investment Company (Pvt.) Limited 340

Shamil Bank of Bahrain E.C. 276

Islamic Development Bank, Jeddah 99

Kuwait Awqaf Public Foundation 88

Saudi Pak Ind. & Agricultural investment Company 49

General Public 212

Paid up Capital 1,064

Pak Kuwait

Pak-Kuwait

SSaauuddii PPaakk

SShhaammiill BBaannkk

The members of the Shariah Board of MeezanBank are internationally renowned scholarsserving on the boards of many Islamic banksoperating in different countries.

The members of the Shariah Board are:1. Justice (Retd.) Muhammad Taqi Usmani

(Chairman)2. Dr. Abdul Sattar Abu Ghuddah 3. Sheikh Essam M. Ishaq4. Dr. Muhammad Imran Usmani

JUSTICE (RETD.) MUHAMMAD TAQIUSMANI is a renowned figure in the field ofShariah, particularly Islamic Finance. Heholds the position of Deputy Chairman at theIslamic Fiqh Academy, Jeddah. He is also amember of Shariah advisory boards of anumber of financial institutions practicingIslamic Banking and Finance including SaudiAmerican Bank, Saudia Arabia; HSBC plc,Global Islamic Finance, London; Citi IslamicInvestment Bank, Bahrain and Dow JonesIslamic Market Index. Justice (Retd.)Muhammd Taqi Usmani has vast experiencein Islamic Shariah, he has been teachingvarious subjects on Islam for 39 years. He isalso serving as the Vice President of Darul-Uloom, Karachi. He also served as a Judge inthe Shariat Appellate Bench, Supreme Courtof Pakistan.

Born in Pakistan, Justice (Retd.) MuhammadTaqi Usmani holds an LLB from KarachiUniversity. He graduated from PunjabUniversity in 1970. Prior to that, hecompleted Takhassus course i.e. thespecialization course of Islamic Fiqh andFatwa (Islamic Jurisprudence) from JamiaDarul-Uloom, Karachi.

DR. ABDUL SATTAR ABU GHUDDAHholds positions of Shariah Advisor andDirector, Department of FinancialInstruments at Al-Baraka Investment Co. ofSaudia Arabia. He holds a Ph.D in Islamic

Law from Al Azhar University Cairo, Egypt.He is an active member of Islamic FiqhAcademy and the Accounting & AuditingStandards Board of Islamic FinancialInstitutions.

Dr. Abdul Sattar teaches Fiqh, IslamicStudies and Arabic in Riyadh and has done avaluable task of researching and compilinginformation for the Fiqh Encyclopedia in theMinistry of Awqaf and Islamic Affairs inKuwait. He was a member of the Fatwa Boardin the Ministry from 1982 to 1990.

SHEIKH ESSAM M. ISHAQ graduated inPolitical Science from McGill University,Montreal, Canada. Currently he is teachingFiqh and Aqeeda courses in UAE andBahrain at Umm Al-DarDa' Islamic Centre.He holds the position of Shariah Advisor atDiscover Islam, Bahrain.

DR. MUHAMMAD IMRAN USMANI isan M. Phil, Ph.D in Islamic Economics andgraduated as a scholar from Jamia Darul-Uloom, Karachi. He has done a specializationcourse in Islamic Jurisprudence as well. Heis also involved in conducting trainingsessions for Meezan Bank staff on IslamicFinance and Shariah issues. Dr. Usmani hasbeen teaching several branches of Islamiclearning since 1998 at Jamia Darul-Uloom,Karachi.

IIssllaammiicc DDeevveellooppmmeenntt BBaannkk

KKuuwwaaiitt AAwwqqaaff

NOTICE OF ANNUAL GENERAL MEETING

Proxies in order to be effective must bereceived at the registered office not less than48 hours before the holding of the Meeting.

iii) An individual beneficial owner of theCentral Depository Company, entitled tovote at this Meeting must bring his/herNational Identity Card with him/her toprove his/her identity, and in case of proxymust enclose an attested copy of his/herNational Identity Card. Representatives ofcorporate members should bring the usualdocuments required for such purposes.

SSttaatteemmeenntt UUnnddeerr SSeeccttiioonn 116600 ooff tthheeCCoommppaanniieess OOrrddiinnaannccee,, 11998844

This statement is annexed to the Notice of theEighth Annual General Meeting of Meezan BankLimited to be held on March 30, 2004 at whichcertain special business is to be transacted. Thepurpose of this statement is to set forth thematerial facts concerning such special business.

Item (4) of the AgendaThe Board of Directors recommend that takinginto account the financial position of theCompany the issued capital of the Company beincreased by capitalization of free reservesamounting to Rs. 106,404,514 (Rupees onehundred and six million four hundred and fourthousand five hundred and fourteen only) byway of issuing bonus shares in the ratio of 1:10i.e. 10%. The Directors of the Company areinterested in the business to the extent of theirshareholding in the Company.

Item (5) of the AgendaIn order to bring the Articles of Association ofthe Company in accordance with theCompanies Ordinance 1984, the followingamendments are proposed to be made:

i) Clause 27 to be amended to read as follows:Annual General Meeting

The Company shall hold a generalmeeting, designated as the annual generalmeeting, within three (3) months followingthe close of each financial year of theCompany, but so that an annual general

meeting is held in every calendar year(except that the first annual general meetingmay be held within eighteen (18) monthsfrom the date of incorporation) and not morethan fifteen (15) months elapse between anytwo (2) consecutive annual general meetings,and subject as aforesaid each such annualgeneral meeting shall be held at such time asmay be determined by the Directors.

ii) Clause 31 to be amended to read as follows:Quorum

No business shall be transacted at anygeneral meeting unless a quorum ofMembers is present at the time of thecommencement of proceedings. Ten (10)Members present personally who representnot less than twenty-five per cent (25%) ofthe total voting power, either on their ownaccount or as proxies shall be a quorum.

iii) Clause 49 to be amended to read as follows:

Qualification of DirectorsSave as provided in Section 187 of theOrdinance, no person shall be appointed as aDirector unless he is a Member and holdsqualification shares of Rs. 5000.00 (Rupeesfive thousand only). For the purposes of thisArticle, the Director may hold thequalification shares in his own namerelaxable in the case of a Directorrepresenting interest holding shares of therequisite value. Further, no person shall beappointed as a Director if he has beendeclared by a court of competent jurisdictionas defaulter in repayment of loan to afinancial institution, exceeding, such amountas may be notified by the Commission fromtime to time and is a member of a StockExchange engaged in the business ofbrokerage, or is a spouse of such member.

By Order of the Board

((GGoohhaarr IIqqbbaall SShhaaiikkhh))Company SecretaryDate: March 9, 2004

Karachi

21

Annual Report 2003

NOTICE OF ANNUAL GENERAL MEETING

Annu

al Re

port

200

3

20

Notice is hereby given that the 8th AnnualGeneral Meeting of the members of MeezanBank Limited will be held Inshallah on TuesdayMarch 30, 2004 at 11:00 a.m. at Beach LuxuryHotel, Moulvi Tamizuddin Khan Road, Karachito transact the following business:

ORDINARY BUSINESS1. To receive and adopt the Directors» and

Auditors» Reports and Audited Accountsfor the year ended December 31, 2003.

2. To consider and approve cash dividend @ 5% as recommended by the Directors.

3. To appoint the auditors for the year endingDecember 31, 2004 and fix their remu-neration. The present auditors M/s A.F.Ferguson & Co., Chartered Accountants,retire and being eligible, offer themselvesfor reappointment.

SPECIAL BUSINESS 4. To consider, and if thought fit, to pass the

following Resolution as an OrdinaryResolution:

""RReessoollvveedd tthhaatt::aa)) aa ssuumm ooff RRss.. 110066,,440044,,551144 ((RRuuppeeeess oonnee

hhuunnddrreedd aanndd ssiixx mmiilllliioonn ffoouurr hhuunnddrreedd aannddffoouurr tthhoouussaanndd ffiivvee hhuunnddrreedd aanndd ffoouurrtteeeennoonnllyy)) oouutt ooff tthhee ffrreeee rreesseerrvveess ooff tthheeCCoommppaannyy bbee ccaappiittaalliizzeedd aanndd aapppplliieeddttoowwaarrddss tthhee iissssuuee ooff 1100,,664400,,445511 oorrddiinnaarryysshhaarreess ooff RRss.. 1100//-- eeaacchh aass bboonnuuss sshhaarreess iinntthhee rraattiioo ooff 11::1100 ii..ee.. 1100%% oonn oorrddiinnaarryysshhaarreess hheelldd bbyy tthhee mmeemmbbeerrss wwhhoossee nnaammeessaappppeeaarr oonn tthhee MMeemmbbeerrss»» RReeggiisstteerr oonnMMaarrcchh 3300,, 22000044.. TThheessee bboonnuuss sshhaarreess sshhaallllrraannkk ppaarrii ppaassssuu iinn aallll rreessppeeccttss wwiitthh tthheeeexxiissttiinngg sshhaarreess..

bb)) MMeemmbbeerrss eennttiittlleedd ttoo ffrraaccttiioonnss ooff sshhaarreess aass aarreessuulltt ooff tthheeiirr hhoollddiinngg eeiitthheerr bbeeiinngg lleessss tthhaann1100 oorrddiinnaarryy sshhaarreess oorr iinn eexxcceessss ooff aann eexxaaccttmmuullttiippllee ooff 1100 oorrddiinnaarryy sshhaarreess sshhaallll bbee ggiivveenntthhee ssaallee pprroocceeeeddss ooff tthheeiirr ffrraaccttiioonnaalleennttiittlleemmeennttss ffoorr wwhhiicchh ppuurrppoosseess tthhee ffrraaccttiioonnsssshhaallll bbee ccoonnssoolliiddaatteedd iinnttoo wwhhoollee sshhaarreess aannddssoolldd oonn tthhee KKaarraacchhii SSttoocckk EExxcchhaannggee..

cc)) FFoorr tthhee ppuurrppoossee ooff ggiivviinngg eeffffeecctt ttoo tthheeffoorreeggooiinngg,, tthhee DDiirreeccttoorrss bbee aanndd aarree hheerreebbyyaauutthhoorriisseedd ttoo ggiivvee ssuucchh ddiirreeccttiioonnss aass tthheeyyddeeeemm ffiitt ttoo sseettttllee aannyy qquueessttiioonn oorr aannyyddiiffffiiccuullttiieess tthhaatt mmaayy aarriissee iinn tthhee ddiissttrriibbuuttiioonnooff tthhee ssaaiidd bboonnuuss sshhaarreess oorr iinn tthhee ppaayymmeennttooff tthhee ssaallee pprroocceeeeddss ooff tthhee ffrraaccttiioonnss..""

5. Amendment in the Articles of Association

To consider and approve the amendmentsin the Articles of Association of the Com-pany to bring it in accordance with require-ments of the Companies Ordinance 1984.

A statement under Section 160 of theCompanies Ordinance 1984 setting forth allmaterial facts concerning the Resolutionscontained in items (4) and (5) of the Noticewhich will be considered for adoption at theMeeting is annexed to this Notice of Meetingbeing sent to Members.

GENERAL BUSINESS6. To transact any other business that may

be placed before the Meeting with the permission of the chair.

By Order of the Board

((GGoohhaarr IIqqbbaall SShhaaiikkhh))Company SecretaryDate: March 9, 2004

Karachi

NOTES:i) The Members» Register will remain closed

from March 22, 2004 to March 30, 2004(both days inclusive). Transfer received inorder at the office of the Share Registrar ofthe Bank by the close of the business hourson March 21, 2004 will be treated in timefor the entitlement of dividend payment.

ii) A member eligible to attend and vote at thisMeeting may appoint another member asproxy to attend and vote in the Meeting.

Annual Report 2003

DIRECTORS» REPORT

23

DIRECTORS» REPORT

Annu

al Re

port

200

3

22

Meezan Bank was the first bank to be grantedthe license of a Scheduled Islamic CommercialBank in January 2002. Over the past two yearsMeezan Bank has played a key developmentalrole in promoting Islamic finance in Pakistanand Alhamdolillah today is recognized as anicon in the Islamic financial industry. Over thistwo-year period no other license for a dedicatedIslamic bank has been issued and we continueto be the only dedicated scheduled Islamic bankin Pakistan.

The Bank»s experience to date has, Alhamdolillahbeen very dynamic and growth oriented. Within ashort span of time the Bank has a well diversifiedfinancing portfolio which includes key blue chipmultinationals as well as strong local corporategroups. In addition, the Bank has establisheditself as a premium financial services provider forthe consumer sector with a Car Ijarah (leasing)

and house financing product. Now, a growingrange of financially savvy individuals across thesocio-economic spectrum are realizing the valueof Meezan Bank»s competitive, solid, and effectiveproducts and services, all coupled with ourunique advantage of Shariah compliance.

As a new commercial bank, we embarked on anaggressive program of expanding our branchnetwork and overall reach. This requiredextensive market presentation and dissemination

of information. Although this resulted in highexpenditure levels, by the Grace of Allah, ourprofitability remained robust with a net profitafter tax of Rs. 214 million on a balance sheetfooting of Rs. 11.1 billion, up from Rs. 7.0 billionfor the corresponding period last year. We arealso pleased to report that there are no baddebts in the portfolio.

The Directors of Meezan Bank Limited are pleased to presentthe seventh annual report and audited financial statementssetting out detailed financial results of the Bank along withconsolidated financial statements of the group includingAl-Meezan Investment Management Limited for the financialyear ended 31st December 2003.

FINANCIAL RESULTSAMOUNT

(Rs. in 000s)Authorised Share Capital 1,500,000Paid up Capital 1,064,045Capital Reserve 351,444Revenue Reserve 221,073Total Shareholders» Funds 1,748,475Profit before taxation 240,828Less: Taxation 27,015Net Profit for the year 213,813

EECCOONNOOMMIICC RREEVVIIEEWWThe Pakistan economy continues to postimpressive gains and the macro-economicindicators of the country all indicate apositive trend. A strong surge in aggregatedemand, sustained external account

improvement, the resilience endowed bysound macro-economic foundations, andgood fortune, contributed to a broad-basedacceleration in Pakistan»s economy during2003, raising real GDP growth to 5.1%. Adistinguishing characteristic of theperformance in the year 2003, relative to thatof 2002, is the scale and depth of theimprovement. The agricultural sector growthwas recorded at 4.1% as compared to anegative growth of 0.1% in 2002, industrialgrowth comfortably reached 5.4%, the sameas achieved in 2002, large scalemanufacturing grew by 8.7% in 2003 ascompared to 4.9% in 2002, exports increasedto a record US $ 11.1 billion, and the currentaccount surplus jumped to an all-time high ofUS $ 4 billion. Remittances also acceleratedto a new high of US $ 4.2 billion,underpinning a substantial improvement innational savings as well as supporting the

increase in the SBP forex reserves to arecord US $ 12 billion. The achievement oftax collection target that, together withdisciplined spending, pushed the fiscal deficitto a 27 year low. The confluence of lowgovernment borrowings and adroitmanagement of external inflows by the SBPalso pushed interest rates to historic lowswhile supporting exports through the relativestability of the exchange rate. Thegovernment has also been able to repay itsexpensive debts to multilateral organizationsand has also recently successfully launched aUS $ 500 million Eurobond issue which tapsthe international financial markets after alapse of many years.

MMOONNEEYY MMAARRKKEETTThe State Bank of Pakistan continued tomaintain easy monetary policy posture adoptedin June 2001 with the lowering of the discountrate to kick-start the process of economicrecovery and accelerate the pace of economicdevelopment. The lending rates, deposit rates

The State Bank of Pakistancontinued to maintain easymonetary policy postureadopted in June 2001 withthe lowering of discount rateto kick-start the process ofeconomic recovery andaccelerate the pace ofeconomic development.

The banking industry turnedin an exceptional perfor-mance for the secondsuccessive year leveragingon a spectacular growth indeposits, aggressivemarketing and investments,and increased efficiency, to counteract the impact of a sharp decline ininterest rates.

DIRECTORS» REPORT

The journey has continued in the currentyear as well and the index is trading wellabove the 4700 level. The increase in theindex is mainly attributable to expectationsof significant increase in profitability, burgeoningmarket liquidity and substantial decline ininterest rates, hopes for the early privatisationof state owned enterprises and the generalincrease in optimism based on hopes of abroader recovery in the economy. Banks havealso been able to realize substantial incomefrom capital market operations, howeversince the market is already trading at its alltime high levels, similar profits may not bebooked during the forthcoming year.

OOPPEERRAATTIINNGG RREESSUULLTTSS OOFF TTHHEE BBAANNKKThe year 2003 was the first full year of the bankas a Scheduled Islamic Commercial Bank. Thebalance sheet of the Bank grew from Rs. 7 billionto Rs. 11.1 billion reflecting an increase of 59%,with the financing and investment portfolioincreasing by 96% and deposits growing by 53%during the year. The Bank earned a profit aftertax of Rs. 214 million, 4% lower than thecorresponding figure reported in the previousyear. An analysis of the results shows thatalthough the bottom line is marginally lower,income from core banking business hasincreased by 62% which reflects a healthy trend

despite the shrinking spreads which have besetthe banking industry as a whole. Other income isalso in line with the previous year if one adjustsfor the one-time recovery made from bad debtsin 2002. It is also encouraging to note that the

Bank recorded very good capital gains from theequity markets despite the constraint faced bythe Bank in not being able to trade GovernmentSecurities which has been one of the mainfactors contributing to the impressive figuresreported by other banks for 2003.

The significant achievements during the yearmay be highlighted as follows:

● Opening of four new branches, two inKarachi, and one each in Multan andFaisalabad, and relocation of two branchesi.e. Lahore and Islamabad to moreconvenient and customer friendly locations.

● Approval of the Islamic Export RefinanceScheme Part II by the State Bank of Pakistan.

● Introduction of Islamic Housing Finance.

● Acquisition, implementation of new softwareto cater to the needs of retail banking.

● Acquisition of 40% shares of Al-MeezanInvestment Management Limited resultingin an aggregate holding of 70% and thusmaking it a subsidiary of the Bank,enabling it to launch an Islamic open endfund namely Meezan Islamic Fund.

● Providing training to the staff of Bank ofKhyber for undertaking Islamic banking.

FFUUTTUURREE OOUUTTLLOOOOKKWe welcome the entrance of other banks in thefield of Islamic banking since this would helpthe players in the market to work together toincrease the market share of Islamic banks.However, it is also critical that the newentrants ensure that they maintain a highdegree of credibility with regard to Shariahcompliance. We are confident that the StateBank of Pakistan would continue to provideeffective policy guidelines to ensure a levelplaying field for Islamic Banks. Meezan Bank,

25

Annual Report 2003

DIRECTORS» REPORT

Annu

al Re

port

200

3

24

and yields on T-bills and PIBs (GovernmentSecurities) of different maturities came downconsiderably. The weighted average lendingrates decreased by 229 basis points to 5.29%during July 2003 to November 2003. This was onthe back of 459 basis points reduction that tookplace between July 2002 and June 2003 makingthe total reduction to 688 basis points in 18months. Simultaneously the weighted averagedeposit rates also decreased by 45 basis pointsto 1.45% during the same period. During July toJune 2003 the deposit rates had already declinedby 212 basis points resulting in an overalldecrease of 257 basis points in 18 months. Thisresulted in the narrowing down of thedifferential between the average lending andborrowing rates by 184 basis points to 3.86percent by November 2003 down from 5.86percent in June 2003. The above reduction in theinterest rates scenario resulted in substantialgrowth of private sector credit off-take, howeveron the other hand resulted in reduced spreadsand reduction in income from core bankingactivities. Rates are now stable at the currentlevels and the Central Bank has re-affirmed thatthe rate scenario in the country is not unlikely tochange substantially.

TTHHEE BBAANNKKIINNGG SSEECCTTOORRThe banking industry turned in an exceptionalperformance for the second successive yearleveraging on a spectacular growth indeposits, substantial capital gains from thestock market and long-term governmentsecurities, and also in some cases increasedefficiency, to counteract the impact of a sharpdecline in interest rates. As a result, not onlydid the profitability of the sector increase, butselected industry indicators also depictedmajor improvements relative to the precedingyear. In addition, the industry took importantstrides in improving governance, thefurtherance of Islamic banking, and theprivatisation of government owned-banks. TheCentral Bank focus continued onstrengthening the supervisory and regulatory

framework, instilling a competitive businessenvironment both by promoting the role of theprivate sector and liberalizing the financialmarkets, and to improve financial health of thebanking sector. During the year the policy ofprivatizing government-owned bankscontinued and the government divested 51%shares of Habib Bank Limited and is in theprocess of further reducing its share in AlliedBank Limited. During the year the CentralBank granted licences to Muslim CommercialBank, Bank of Khyber and Bank Al Falah toopen dedicated branches that offer Islamicbanking products to customers. This wouldallow Islamic banks to increase their marketshare on the one hand which is a positivedevelopment for Meezan Bank. However, thepresence of these banks will inevitablyincrease competition and may lead to afurther drop in spreads.

The Central Bank has issued new PrudentialRegulations which are in effect from 1stJanuary 2004. These new regulations governnot only corporate but also consumer financingand provide an effective framework for thebanking sector as a whole.

CCAAPPIITTAALL MMAARRKKEETTSSThe capital markets of the country continuedtheir upward journey during 2003 and thebenchmark Karachi Stock Exchange Indexincreased by a phenomenal 66% to reach ahigh of 4471 points as at 31st December 2003.

The balance sheet of the Bankgrew from Rs. 7 billion toRs. 11.1 billion reflectingan increase of 59%, with thefinancing and investmentportfolio increasing by 96%. The Bank is putting in place

state-of-the-art IT systemsso as to enable it to providethe highest level of serviceto its customers.

DIRECTORS» REPORT

5. The system of internal control is sound indesign and has been effectivelyimplemented and monitored.

6. There are no doubts upon the Bank»s abilityto continue as a going concern.

7. There has been no material departure fromthe best practices of Corporate Governanceas detailed in the listing regulations.

8. Key operating and financial data for the lastsix years in summarized form is annexed tothe report.

9. The Bank has fully complied with the bestpractices on Transfer Pricing and theprovisions of the Code of CorporateGovernance as contained in the listingregulations of the Karachi Stock Exchangethroughout the accounting period and theDirectors are satisfied that there is anongoing process of internal control foridentifying, evaluating and managing thesignificant risks faced by the Bank.

10. The value of investments of the Bank»srecognized Provident Fund based onaudited accounts as at June 30, 2002amounted to Rs. 4.7 million and based onun-audited accounts as at 31st December2003 amounted to Rs. 11.4 million. Thevalue of investments of Gratuity Fund

amounted to Rs. 1.93 million based on un-audited accounts.

11. The purchase and sale of shares by theDirectors, Chief Executive, CFO andCompany Secretary, the pattern of share-holding and record of Board meetingsduring the year is given in the enclosedannexure.

CCOOMMPPLLIIAANNCCEE SSTTAATTEEMMEENNTT OOFF EETTHHIICCSSAANNDD BBUUSSIINNEESSSS PPRRAACCTTIICCEESSThe Bank»s reputation and its actions as a legalentity depend on the conduct of its employees. Itis the policy of Meezan Bank to follow the highestbusiness ethics and standards of conduct. TheBank»s Code of Business Ethics and Standards ofConduct sets parameters for ethical behaviorand business practices for directors andemployees. The code is obligatory and enforcedat all levels fairly and without prejudice.

CCRREEDDIITT RRAATTIINNGGThe JCR-VIS Credit Rating Company Limited, anaffiliate of Japan Credit Rating Agency, Japanhas graded the Bank»s long-term entity rating atA+ with stable outlook, while the short-termrating has been graded at A1+, which is thehighest possible in this category.

AAUUDDIITTOORRSSThe present auditors M/s A.F. Ferguson & Co.,Chartered Accountants, retire and beingeligible, offer themselves for re-appointment.As required under the Code of CorporateGovernance, the Audit Committee hasrecommended the appointment of M/s A.F.Ferguson & Co., as auditors for the year ending31st December 2004.

HH..EE.. SSHHEEIIKKHH EEBBRRAAHHIIMM BBIINN KKHHAALLIIFFAA AALL--KKHHAALLIIFFAAChairman

27

Annual Report 2003

DIRECTORS» REPORT

Annu

al Re

port

200

3

26

realizing the cost of setting up a brick andmortar structure of branches would cautiouslyincrease its branch network enabling easyaccess to customers. The Bank is putting inplace state-of-the-art IT systems so as toenable it to provide the highest level of service

to its customers. The Bank is in the advancedstages of setting up its own ATM networkand will soon be connected to the 1 Linkswitch allowing its customers access to alarge nationwide network of ATMs. Extensiveresearch and development work would alsobe undertaken to ensure that the Bank isable to meet the requirements of its customersin all areas of operation.

The Bank expects that the State Bank ofPakistan would soon launch the Ijarah Sukuk,an alternate to government bonds which areeligible for the purpose of Statutory LiquidityRequirement. This would help the Bank inmanaging its excess liquidity therebyensuring better profitability.

DDIIVVIIDDEENNDDThe Board is pleased to recommend a 5 % CashDividend and a 10% Stock Dividend for the year2003 continuing its payout record since the dateof listing on the stock exchange.

CCOORRPPOORRAATTEE AANNDD FFIINNAANNCCIIAALLRREEPPOORRTTIINNGG FFRRAAMMEEWWOORRKKThe Board of Directors of Meezan Bank is fullycognizant of its responsibility as recognizedby the recently formulated Code of CorporateGovernance issued by the Securities andExchange Commission of Pakistan and theState Bank of Pakistan. The following statementsare a manifestation of its commitment towardshigh standards of Corporate Governance andcontinuous organizational improvement:

1. The financial statements prepared by themanagement of Meezan Bank present fairlyits state of affairs, the results of itsoperations, cash flow and changes in equity.

2. Proper books of account of Meezan Bankhave been maintained.

3. Appropriate accounting policies have beenconsistently applied in preparation offinancial statements.

4. International Accounting Standards asapplicable in Pakistan have been followedin preparation of financial statementsand any departure therefrom has beenadequately disclosed.

The Board of Directors ofMeezan Bank is fully cogni-zant of its responsibility asrecognized by the recentlyformulated Code of CorporateGovernance issued by theSecurities and ExchangeCommission of Pakistan.

The Bank has fully compliedwith best practices onTransfer Pricing and theprovisions of the Code ofCorporate Governance ascontained in the listingregulations of the KarachiStock Exchange.

The Bank»s reputation and itsactions as a legal entitydepend on the conduct of itsemployees. It is the policy ofMeezan Bank to follow thehighest business ethics andstandards of conduct.

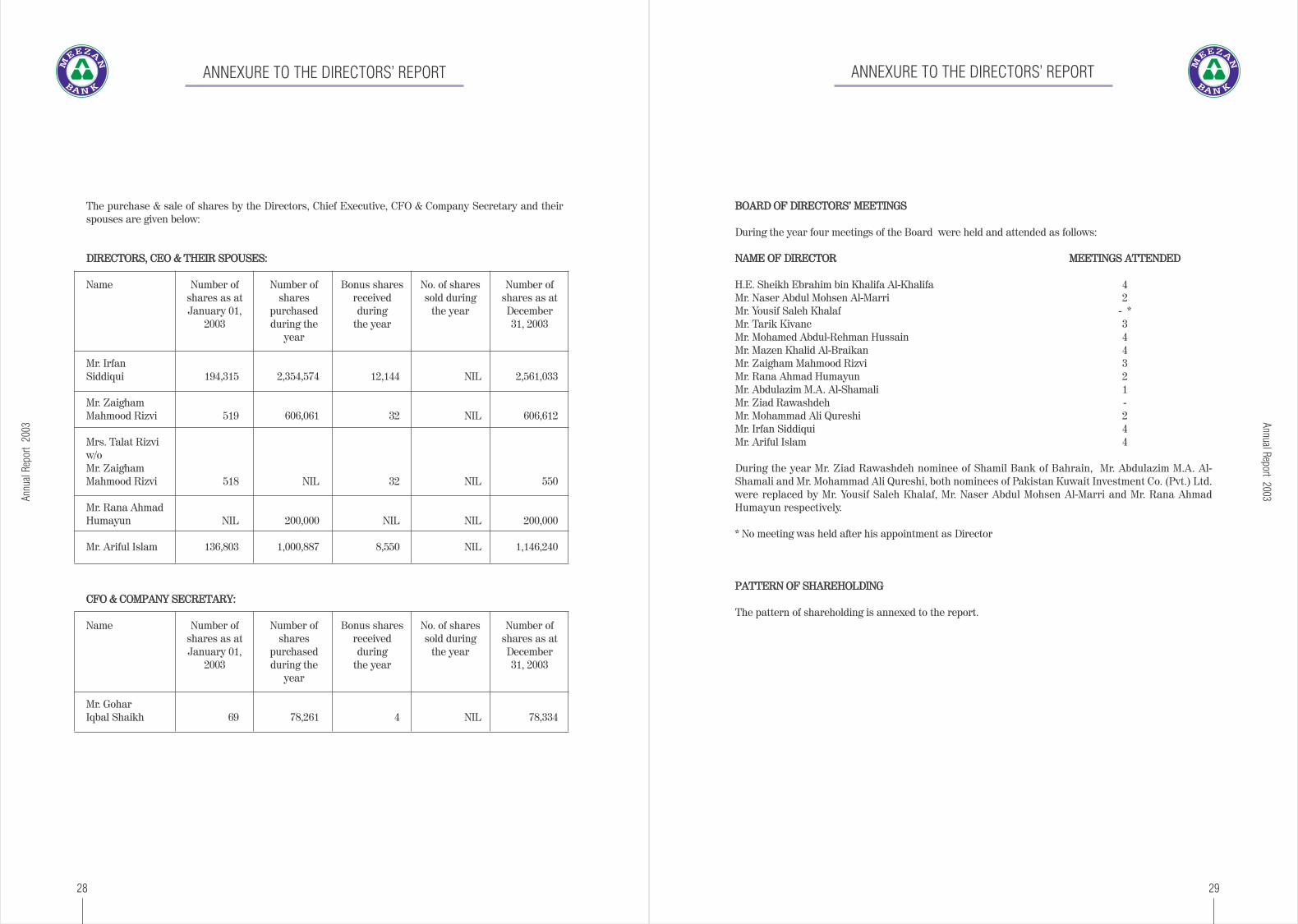

ANNEXURE TO THE DIRECTORS» REPORT

29

Annual Report 2003

ANNEXURE TO THE DIRECTORS» REPORT

BBOOAARRDD OOFF DDIIRREECCTTOORRSS»» MMEEEETTIINNGGSS

During the year four meetings of the Board were held and attended as follows:

NNAAMMEE OOFF DDIIRREECCTTOORR MMEEEETTIINNGGSS AATTTTEENNDDEEDD

H.E. Sheikh Ebrahim bin Khalifa Al-Khalifa 4Mr. Naser Abdul Mohsen Al-Marri 2Mr. Yousif Saleh Khalaf - *Mr. Tarik Kivanc 3 Mr. Mohamed Abdul-Rehman Hussain 4Mr. Mazen Khalid Al-Braikan 4Mr. Zaigham Mahmood Rizvi 3Mr. Rana Ahmad Humayun 2Mr. Abdulazim M.A. Al-Shamali 1Mr. Ziad Rawashdeh -Mr. Mohammad Ali Qureshi 2Mr. Irfan Siddiqui 4Mr. Ariful Islam 4

During the year Mr. Ziad Rawashdeh nominee of Shamil Bank of Bahrain, Mr. Abdulazim M.A. Al-Shamali and Mr. Mohammad Ali Qureshi, both nominees of Pakistan Kuwait Investment Co. (Pvt.) Ltd.were replaced by Mr. Yousif Saleh Khalaf, Mr. Naser Abdul Mohsen Al-Marri and Mr. Rana AhmadHumayun respectively.

* No meeting was held after his appointment as Director

PPAATTTTEERRNN OOFF SSHHAARREEHHOOLLDDIINNGG

The pattern of shareholding is annexed to the report.

Annu

al Re

port

200

3

28

The purchase & sale of shares by the Directors, Chief Executive, CFO & Company Secretary and theirspouses are given below:

DDIIRREECCTTOORRSS,, CCEEOO && TTHHEEIIRR SSPPOOUUSSEESS::

Name Number of Number of Bonus shares No. of shares Number of shares as at shares received sold during shares as at January 01, purchased during the year December

2003 during the the year 31, 2003year

Mr. Irfan Siddiqui 194,315 2,354,574 12,144 NIL 2,561,033

Mr. Zaigham Mahmood Rizvi 519 606,061 32 NIL 606,612

Mrs. Talat Rizvi w/o Mr. Zaigham Mahmood Rizvi 518 NIL 32 NIL 550

Mr. Rana Ahmad Humayun NIL 200,000 NIL NIL 200,000

Mr. Ariful Islam 136,803 1,000,887 8,550 NIL 1,146,240

CCFFOO && CCOOMMPPAANNYY SSEECCRREETTAARRYY::

Name Number of Number of Bonus shares No. of shares Number of shares as at shares received sold during shares as at January 01, purchased during the year December

2003 during the the year 31, 2003year

Mr. Gohar Iqbal Shaikh 69 78,261 4 NIL 78,334

SHARIAH ADVISOR»S REPORT

31

Annual Report 2003

SHARIAH ADVISOR»S REPORT

■ The sequence/order of the documents■ The purchase deed in the leasing

transactions

After auditing these transactions, we concludethat utmost care has been taken to ensure thecompliance of the transactions within theguidelines of EC or SSB and the previousmistakes have not re-occurred.

It is recommended to physically check the Assetsof Murabaha and Lease on a time-to-time basis.

It was also noted that other products of theBank including Trade Finance, Treasury, CarIjarah and Home Financing are being used inaccordance with the approved format of SSB.

AACCTTIIVVIITTIIEESS OONN TTHHEE LLIIAABBIILLIITTIIEESS SSIIDDEE::On the liability side, the Bank offers a variety ofdeposit products which include current account,savings account, US$ deposits, Certificates ofIslamic Investment, Monthly MusharakahCertificates and Riba Free Certificates. SSBhas also duly approved these products.Currently, Meezan Bank»s product range on thedeposit side offers alternatives for almost allconventional deposit schemes. The totaldeposits of the Bank reached Rs. 7.8 billionrupees as at December 31, 2003. The procedureof calculation of profit, weightage andredemption has been approved by SSB for theseliability side products. The implementation ofthe procedure of calculation of profit is alsobeing checked quarterly and it is noted that dueto the excess liquidity of the Bank and thedecrease of profit rates on the asset side, therate of profit for the deposit schemes have beenreduced. To overcome this problem, themanagement has occasionally lowered itsmanagement fee to the extent of 0% voluntarily.

To cover this problem, the Bank will have toseek innovative, profitable and Shariah-compliant products and increase thetransactions of Musharakah and Mudaraba on

the asset side, as well as develop and implementnew liability products for liquidity management.

It is also recommended to increase the portfolioof SME and micro financing to help smallenterprises and entrepreneurs. The Qurdh-e-Hasanah and Charity should also be used fromthe Charity fund of Rs.2.7 million to give awayamounts of charity to various hospitals, schoolsor any other institutions for welfare, health anddevelopment. (The amount of the Charity Fundincludes the amounts of late payment and somenon-Shariah compliant transactions directed byEC of SSB to give it to charity.)

It is appreciated that the Bank is working withSSB to develop new commercial bankingproducts conforming to the tenets of IslamicShariah. These products include Takaful,alternative of Carry Over Transactions andFuture transactions. Efforts are also underwayto refine the existing products of the Bank.

May Allah bless us with best Tawfeeq toaccomplish these cherished tasks, make ussuccessful in this world and in the Hereafter,and forgive our mistakes.

Wassalam Alaikum Wa Rahmat Allah WaBarakatuh.

DDRR.. MMUUHHAAMMMMAADD IIMMRRAANN UUSSMMAANNIIMember, Shariah Supervisory Board

& Shariah Advisor

Annu

al Re

port

200

3

30

The year under review was the first full year ofIslamic Commercial Banking for Meezan Bank.During the year, the Bank has continued with thedevelopment of Islamic Commercial BankingProducts. Three new products have been launchedsuccessfully after the approval of the ShariahSupervisory Board (SSB), which are as follows:

1. Islamic Housing Finance based on AlMusharakat AlMutanaqisa (DiminishingMusharakah): The Bank»s product develop-ment team has developed this product afterextensive research. Since it was the firstIslamic Housing finance product approvedby the Shariah Scholars, it has gainedwidespread interest among the masseswithin a short span of time. We hope that it would provide a great facility forconsumers who want to get home financingin a Shariah compliant way.

2. Islamic Export Refinance Scheme Part II:Islamic Export Refinance Scheme based onMusharakah was Pakistan»s first IslamicExport Refinance Scheme (IERS). It waslaunched last year successfully. This yearanother Shariah-compliant product forPart II of the Scheme has been developedand the State Bank of Pakistan has alsoapproved that product. The currentportfolio outstanding under the scheme isRs. 989 million.

3. Equity Investments: As a part of itsinvestment activities, the Bank also investsin listed securities. For this purpose,during the previous year the ShariahSupervisory Board developed a list ofcriteria to be followed to ensure that theinvestments are made within the bounds ofShariah. Following the same criterion theBank»s subsidiary Al Meezan InvestmentManagement Ltd. has successfullylaunched Meezan Islamic Fund. InitialPublic Offering of the Fund got recordsubscriptions of Rs. 900 million.

It is appreciated that the management of theBank worked closely with the member(s) of theSSB to develop and implement innovativeIslamic Banking products to fulfill the needs ofa diverse range of commercial bankingcustomers under one roof. During the year, atthe time of approval of any financing facility, itwas checked by myself or ExecutiveCommittee (EC) of the SSB that the facility isgiven under Shariah compliant mode. However,due to the repetitive nature of disbursementunder the approved facilities, eachdisbursement was not checked and thereforethe procedure of Shariah Audit has beenadopted. The report of which is as follows:

AACCTTIIVVIITTIIEESS OONN TTHHEE AASSSSEETT SSIIDDEE OOFF TTHHEE BBAANNKK::On the asset side, the two primary modes offinancing used were Murabaha and Ijarah.However two new transactions of Musharakahand Tawarruq have also been used forfinancing during this period after the approvalof EC of SSB.

The Bank»s total financing portfolio reached Rs. 7.4 billion as of December 31, 2003. TheStandard Agreements used by the Bank are inaccordance with the principles of IslamicShariah and have been approved by the ShariahSupervisory Board.

During the Shariah audit of 2002 sometechnical mistakes in the process of executionof Murabaha and Ijarah transactions werefound. EC of SSB directed to ensure non-repetition of such mistakes in future. Thedirections of EC were scrutinized during thecurrent year»s audit and the following matterswere specifically reviewed:

■ Standard agreements■ Murabaha declarations■ The attached description of assets■ The relevant invoices■ The proportionate ownership/equity of

the Bank in description of asset

33

Annual Report 2003

STATEMENT OF COMPLIANCE WITH THE CODE OF CORPORATE GOVERNANCE

compliance with the requirements of theCode and fully describes the salientmatters required to be disclosed.

12. The financial statements of the Bank wereduly endorsed by the CEO and CFO beforeapproval of the Board.

13. The Directors, CEO and executives do nothold any interest in the shares of theBank, other than that disclosed in thepattern of shareholdings.

14. The Bank has complied with all thecorporate and financial reportingrequirements of the Code.

15. The Board has formed an Audit Committee.It comprises of three members, of whomtwo are non-executive directors. The CEOis also a member of the committee.

16. The meetings of the Audit Committee wereheld at least once every quarter prior toapproval of interim and final results of theBank. The terms of reference of thecommittee have been formed, approved bythe Board and advised to the committeefor compliance.

17. The Board has set-up an effective internalaudit function the members of which areconsidered suitably qualified andexperienced for the purpose and areconversant with the policies andprocedures of the Bank and they areinvolved in the internal audit function on afull-time basis.

18. The statutory auditors of the Bank haveconfirmed that they have been given asatisfactory rating under the qualitycontrol review programme of the Instituteof Chartered Accountants of Pakistan, thatthey or any of the partners of the firm,their spouses and minor children do nothold shares of the Bank and that the firm

and all its partners are in compliance withthe International Federation of Accountants(IFAC) guidelines on code of ethics asadopted by the Institute of CharteredAccountants of Pakistan.

19. The statutory auditors or the personsassociated with them have not beenappointed to provide other servicesexcept in accordance with the listingregulations and the auditors haveconfirmed that they have observed IFACguidelines in this regard.

20. We confirm that all other materialprinciples contained in the Code have beencomplied with.

IIRRFFAANN SSIIDDDDIIQQUUIIPresident & CEO

Annu

al Re

port

200

3

32

This statement is being presented to complywith the Code of Corporate Governance framedby the Securities and Exchange Commission ofPakistan for the purpose of establishing aframework of good governance, whereby alisted company is managed in compliance withthe best practices of corporate governance.

The Bank has applied the principles containedin the Code in the following manner:

1. The Bank encourages representation ofindependent non-executive directors. Atpresent the Board has eight non-executivedirectors.

2. The directors have confirmed that none ofthem is serving as a director in more thanten listed companies, including this Bank.

3. All the resident directors of the Bank areregistered as taxpayers and none of themhas defaulted in payment of any loan to abanking company, a DFI or an NBFI or,being a member of a stock exchange, hasbeen declared as a defaulter by that stockexchange.

4. Three directors retired during the year andwere replaced. No casual vacancy occurredduring the year ended December 31, 2003.

5. Statement of Ethics and Business Practiceshas been approved and signed by thedirectors and employees of the Bank.

6. The Board has developed a vision andmission statement and an overallcorporate strategy. The Bank afteramalgamation with Societe Generale hasadopted its policies and procedures,wherever these are not contradictory tothe Shariah Principles. The Board hasadopted three significant policies of theBank and is in the process of approvingfurther eight policies in the forthcomingmeeting. In addition, the management has

issued various directives for differentproducts and procedures to ensure smoothoperations of the Bank. A complete recordof the significant policies along with thedates on which they were approved oramended has been maintained.

7. All powers of the Board have been dulyexercised and decisions on materialtransaction, including appointment anddetermination of remuneration and termsand conditions of employment of the CEOand other executive directors have beentaken by the Board.

8. There was no new appointment of CFO,Company Secretary or Head of InternalAudit during the year ended December31, 2003.

9. The meetings of the Board were presidedover by the Chairman. The Board met atleast once in every quarter during the yearended December 31, 2003. Written noticesof the Board meetings, along with agendaand working papers, were circulated atleast seven days before the meetings. Theminutes of the meetings were appropriatelyrecorded and circulated.

10. The management of the Bank hascirculated a summary of provisions ofvarious laws i.e. the Companies Ordinance,1984, the Code of Corporate Governance,the Banking Companies Ordinance, 1962,the Prudential Regulations of the StateBank of Pakistan and the ListingRegulations of the Karachi Stock Exchangeas required under Clause (xiv) of the Codei.e. with respect to the «Orientation Course»of directors to acquaint them of their dutiesand responsibilities and enable them tomanage the affairs of the Bank on behalf ofshareholders.

11. The Directors» report for the year endedDecember 31, 2003 has been prepared in

STATEMENT OF COMPLIANCE WITH THE CODE OF CORPORATE GOVERNANCE

AUDITORS» REPORT TO THE MEMBERS

35

Annual Report 2003

REVIEW REPORT TO THE MEMBERS ON STATEMENT OF COMPLIANCE WITH BEST PRACTICES OF

CODE OF CORPORATE GOVERNANCE

We have audited the annexed balance sheet ofMeezan Bank Limited as at December 31, 2003and the related profit and loss account, cash flowstatement and statement of changes in equity,together with the notes forming part thereof (here-in-after referred to as the «financial statements»)for the year then ended, in which are incorporatedthe unaudited certified returns from the branchesexcept for three branches which have beenaudited by us and we state that we have obtainedall the information and explanations which, to thebest of our knowledge and belief, were necessaryfor the purposes of our audit.