Meet the: Teradyne Health Investment Plan library/hr/benefits/2014-health-investment... · HEALTH...

25

MEET THE: TERADYNE HEALTH INVESTMENT PLAN September 2014

Transcript of Meet the: Teradyne Health Investment Plan library/hr/benefits/2014-health-investment... · HEALTH...

MEET THE:

TERADYNE HEALTH INVESTMENT PLAN

September 2014

AGENDA

• What is the Health Investment Plan?

• Why is this important to Teradyne & our employees?

• Health Investment Plan Videos

• Benefits of an HSA

• Quality of Care

• Real –life Scenarios

• What do you need to consider?

• Resources

• What’s to come

• Questions

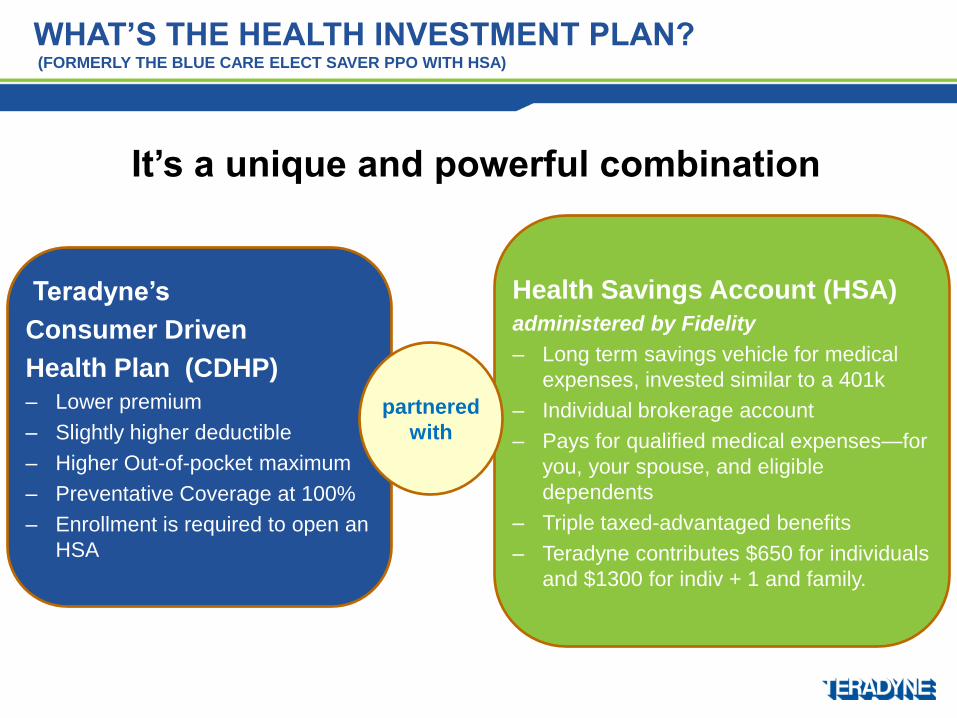

Health Savings Account (HSA)

administered by Fidelity

– Long term savings vehicle for medical

expenses, invested similar to a 401k

– Individual brokerage account

– Pays for qualified medical expenses—for

you, your spouse, and eligible

dependents

– Triple taxed-advantaged benefits

– Teradyne contributes $650 for individuals

and $1300 for indiv + 1 and family.

It’s a unique and powerful combination

Teradyne’s

Consumer Driven

Health Plan (CDHP)

– Lower premium

– Slightly higher deductible

– Higher Out-of-pocket maximum

– Preventative Coverage at 100%

– Enrollment is required to open an

HSA

partnered

with

WHAT’S THE HEALTH INVESTMENT PLAN? (FORMERLY THE BLUE CARE ELECT SAVER PPO WITH HSA)

WHY THE BIG PUSH THIS YEAR?

• Health care costs continue to increase - $20M per year

• Teradyne is Self-Insured

• Current Health Investment Plan enrollment is 8%

(compared to the market 29%)

• 70% of our employees would have been financially better off

in the Health Investment Plan

• Employees are unaware of the opportunity they are missing,

with many leaving money on the table

• Responsibility to ensure employees are making an educated

choice

HEALTH INVESTMENT PLAN VIDEOS

What is the Health Investment Plan?

• https://teradyne.a.guidespark.com/videos/4419

Insider knowledge of the Teradyne Health Investment Plan

• A Teradyne Perspective

MEDICAL CLAIMS COST CURVE ACROSS PLANS

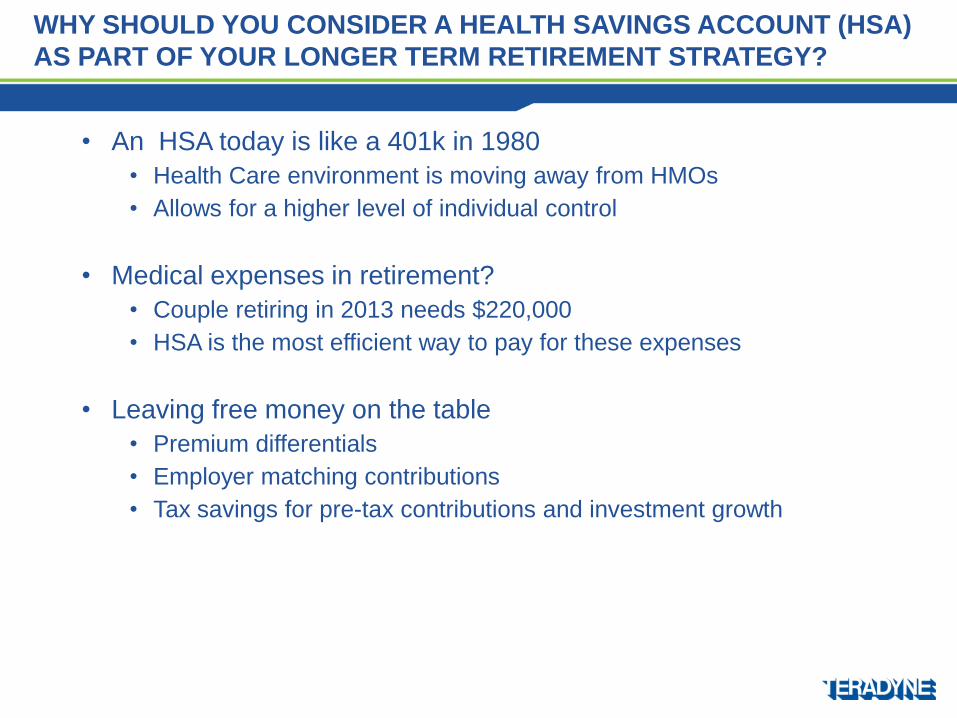

WHY SHOULD YOU CONSIDER A HEALTH SAVINGS ACCOUNT (HSA)

AS PART OF YOUR LONGER TERM RETIREMENT STRATEGY?

• An HSA today is like a 401k in 1980

• Health Care environment is moving away from HMOs

• Allows for a higher level of individual control

• Medical expenses in retirement?

• Couple retiring in 2013 needs $220,000

• HSA is the most efficient way to pay for these expenses

• Leaving free money on the table

• Premium differentials

• Employer matching contributions

• Tax savings for pre-tax contributions and investment growth

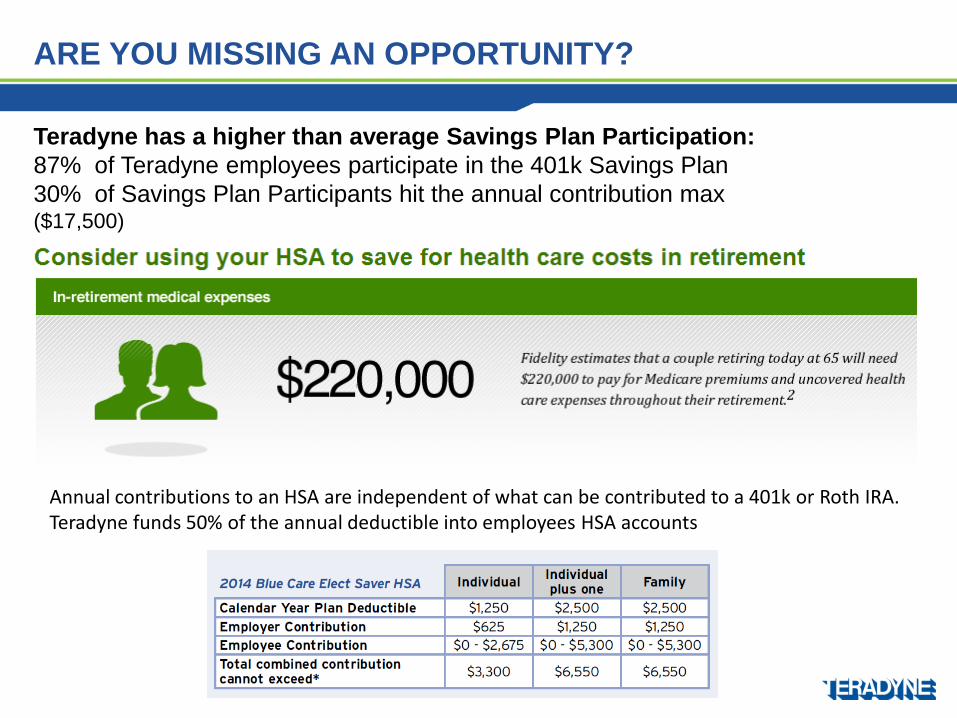

ARE YOU MISSING AN OPPORTUNITY?

Teradyne has a higher than average Savings Plan Participation:

87% of Teradyne employees participate in the 401k Savings Plan

30% of Savings Plan Participants hit the annual contribution max ($17,500)

Annual contributions to an HSA are independent of what can be contributed to a 401k or Roth IRA. Teradyne funds 50% of the annual deductible into employees HSA accounts

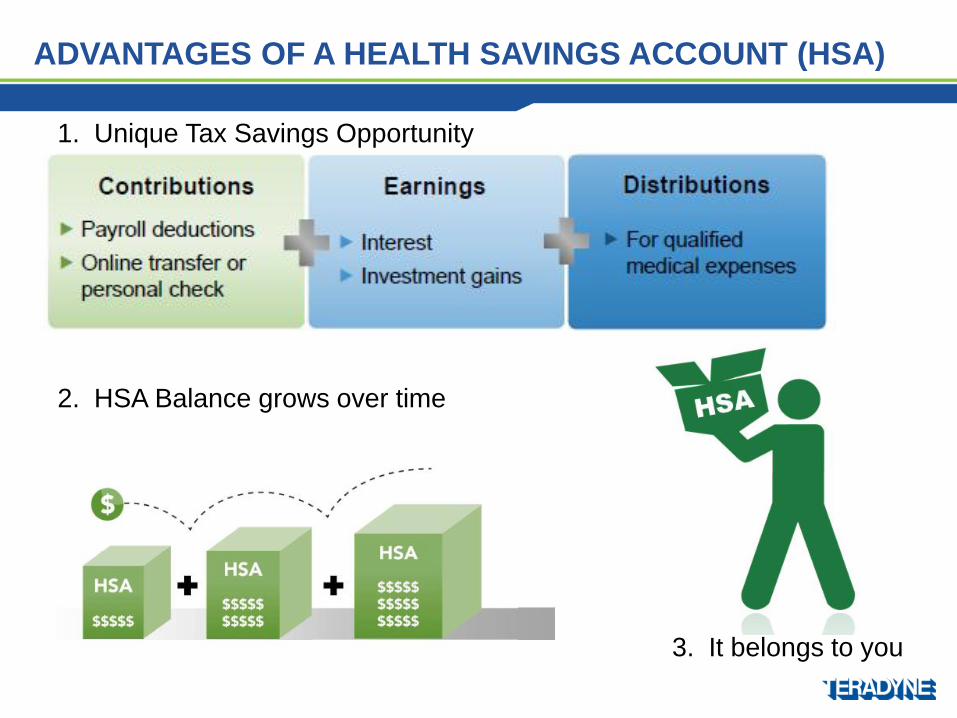

ADVANTAGES OF A HEALTH SAVINGS ACCOUNT (HSA)

2. HSA Balance grows over time

3. It belongs to you

1. Unique Tax Savings Opportunity

HEALTH INVESTMENT PLAN: QUALITY OF CARE?

• Same network of high quality doctors and services

• Recent HSA studies prove cost savings to employees and company

while maintaining quality of care (e.g. chronic conditions like, well

managed Diabetes)

• Higher compliance with wellness programs and preventative care –

Covered at 100%

REAL-LIFE SCENARIOS

1. Family coverage with usage over the year

2. Individual coverage with a significant event

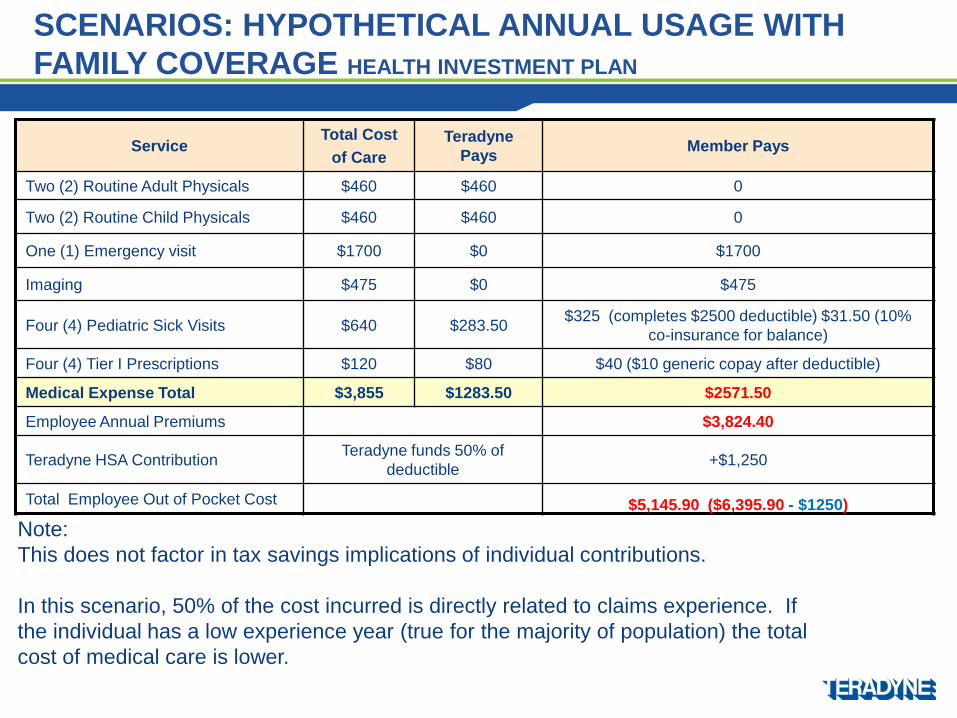

SCENARIOS: HYPOTHETICAL ANNUAL USAGE WITH

FAMILY COVERAGE HEALTH INVESTMENT PLAN

Service Total Cost

of Care

Teradyne

Pays Member Pays

Two (2) Routine Adult Physicals $460 $460 0

Two (2) Routine Child Physicals $460 $460 0

One (1) Emergency visit $1700 $0 $1700

Imaging $475 $0 $475

Four (4) Pediatric Sick Visits $640 $283.50 $325 (completes $2500 deductible) $31.50 (10%

co-insurance for balance)

Four (4) Tier I Prescriptions $120 $80 $40 ($10 generic copay after deductible)

Medical Expense Total $3,855 $1283.50 $2571.50

Employee Annual Premiums $3,824.40

Teradyne HSA Contribution Teradyne funds 50% of

deductible +$1,250

Total Employee Out of Pocket Cost $5,145.90 ($6,395.90 - $1250)

Note:

This does not factor in tax savings implications of individual contributions.

In this scenario, 50% of the cost incurred is directly related to claims experience. If

the individual has a low experience year (true for the majority of population) the total

cost of medical care is lower.

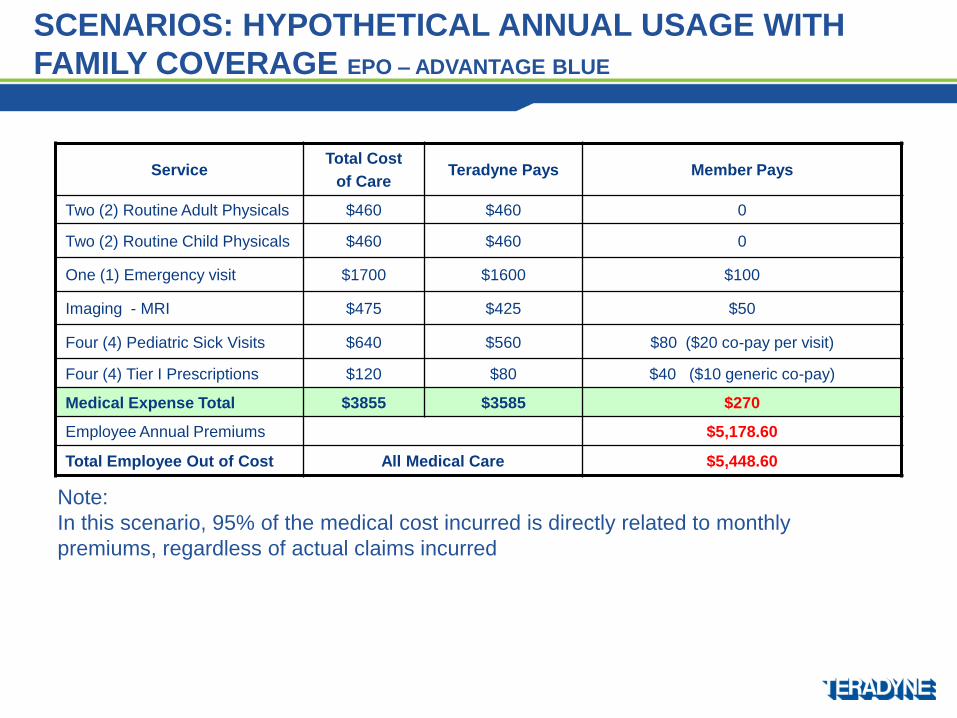

SCENARIOS: HYPOTHETICAL ANNUAL USAGE WITH

FAMILY COVERAGE EPO – ADVANTAGE BLUE

Service Total Cost

of Care Teradyne Pays Member Pays

Two (2) Routine Adult Physicals $460 $460 0

Two (2) Routine Child Physicals $460 $460 0

One (1) Emergency visit $1700 $1600 $100

Imaging - MRI $475 $425 $50

Four (4) Pediatric Sick Visits $640 $560 $80 ($20 co-pay per visit)

Four (4) Tier I Prescriptions $120 $80 $40 ($10 generic co-pay)

Medical Expense Total $3855 $3585 $270

Employee Annual Premiums $5,178.60

Total Employee Out of Cost All Medical Care $5,448.60

Note:

In this scenario, 95% of the medical cost incurred is directly related to monthly

premiums, regardless of actual claims incurred

SCENARIO: HYPOTHETICAL SKI ACCIDENT

(INDIVIDUAL ON HEALTH INVESTMENT PLAN)

• Medical Expenses • Hospital Stay

• MRI’s

• Surgery

• Physical Therapy

• Ambulance

• Total Claims Cost: $120k

• Employee Cost • 100% of the costs up to

the deductible: $1,250

• 10% of the costs up to the out-of-pocket maximum: $3,500

• Teradyne’s contribution to the employee HSA can be used to cover deductible and out-of-pocket costs: -$625

• Total Cost: $2,875

WHAT DO YOU NEED TO CONSIDER?

• How do you plan to pay for medical expenses in retirement?

• Are you currently maximizing all of your tax-free savings

plan contributions?

• What are your anticipated medical needs?

• Involve the other decision makers in your household.

• Research & understand the plans well before the two weeks

of Open Enrollment

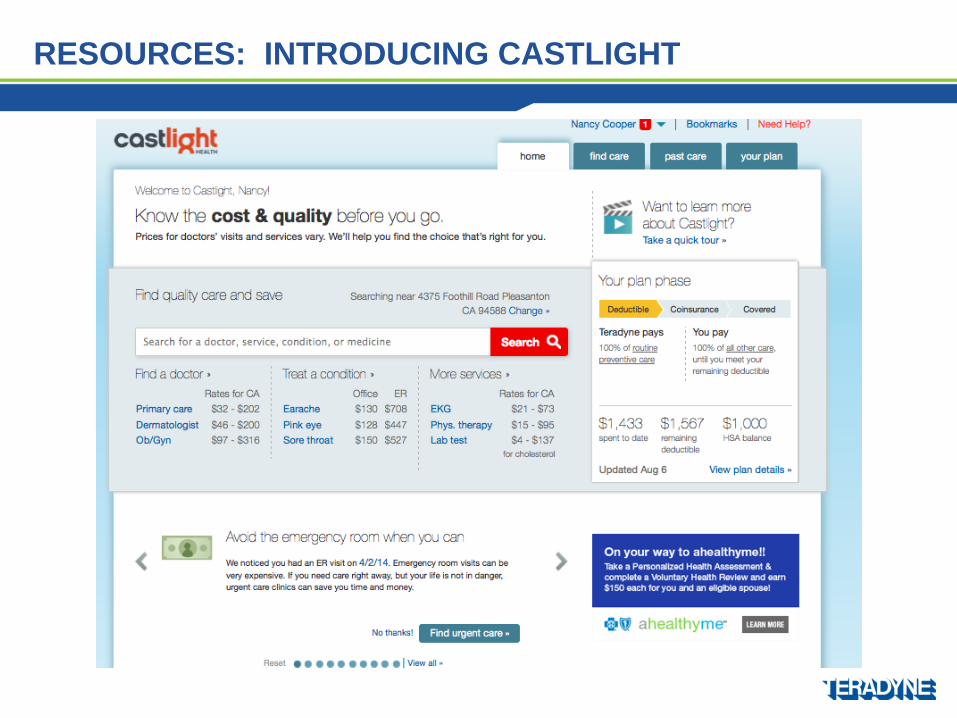

RESOURCES: INTRODUCING CASTLIGHT

RESOURCES

• Updated Teradyne Benefits Portal

• Plan Comparisons and Summary Plan Descriptions • www.teradyne.com/benefits

• Enhanced Health Plan Cost Modeling Tool powered by

Fidelity

• Compare Cost Estimates: www.bcbsma.com – Under Find

a Doctor

• Go to: www.401k.com (look under the Health Savings

Account tile)

• Contact the HR Service Center • Phone: 978-370-3041 Email: [email protected]

APPENDIX

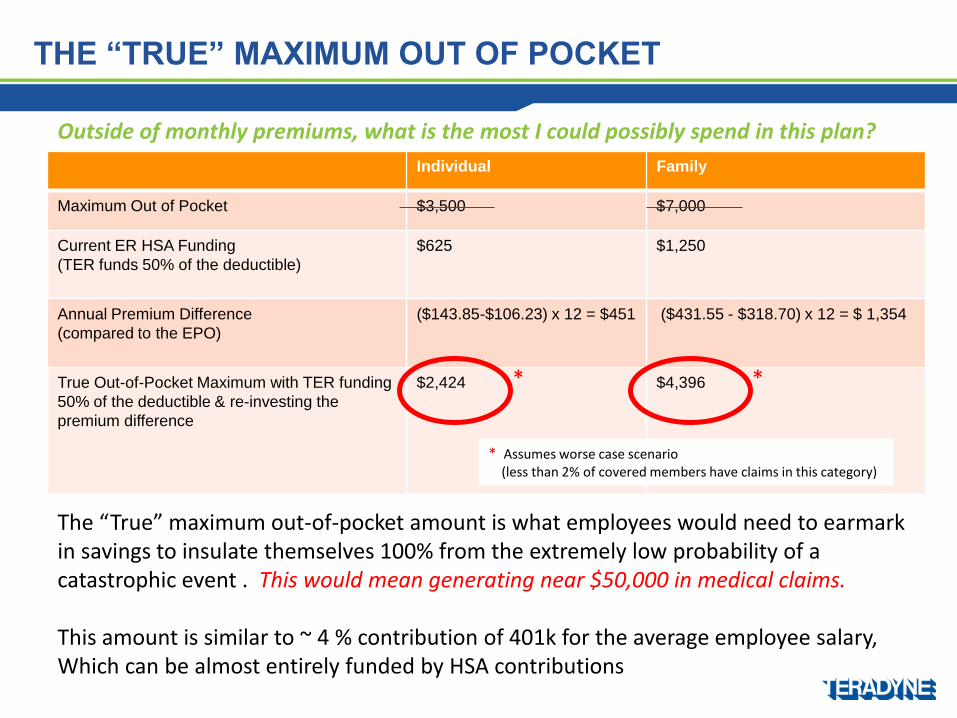

THE “TRUE” MAXIMUM OUT OF POCKET

Individual Family

Maximum Out of Pocket $3,500 $7,000

Current ER HSA Funding

(TER funds 50% of the deductible)

$625 $1,250

Annual Premium Difference

(compared to the EPO)

($143.85-$106.23) x 12 = $451 ($431.55 - $318.70) x 12 = $ 1,354

True Out-of-Pocket Maximum with TER funding

50% of the deductible & re-investing the

premium difference

$2,424

$4,396

The “True” maximum out-of-pocket amount is what employees would need to earmark in savings to insulate themselves 100% from the extremely low probability of a catastrophic event . This would mean generating near $50,000 in medical claims. This amount is similar to ~ 4 % contribution of 401k for the average employee salary, Which can be almost entirely funded by HSA contributions

* Assumes worse case scenario (less than 2% of covered members have claims in this category)

* *

Outside of monthly premiums, what is the most I could possibly spend in this plan?

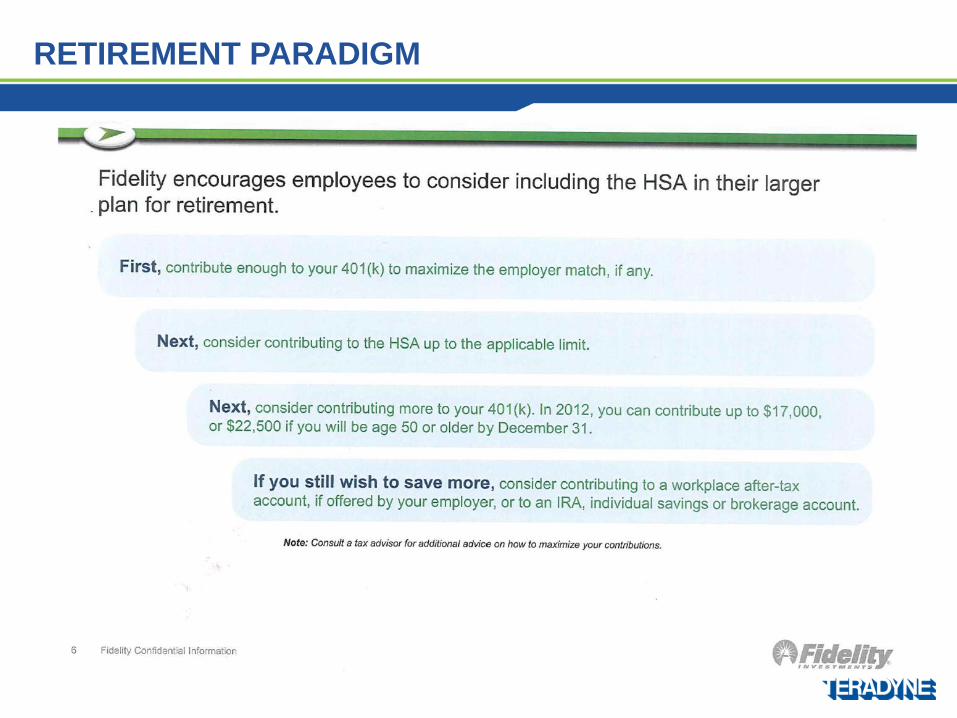

RETIREMENT PARADIGM

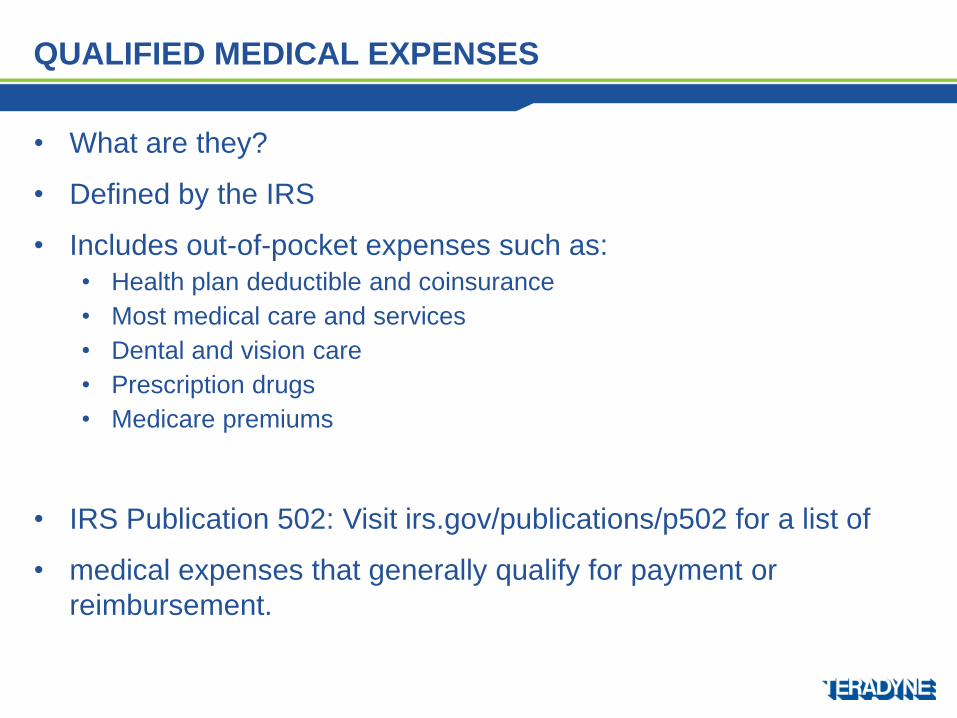

QUALIFIED MEDICAL EXPENSES

• What are they?

• Defined by the IRS

• Includes out-of-pocket expenses such as:

• Health plan deductible and coinsurance

• Most medical care and services

• Dental and vision care

• Prescription drugs

• Medicare premiums

• IRS Publication 502: Visit irs.gov/publications/p502 for a list of

• medical expenses that generally qualify for payment or

reimbursement.

Massachusetts physicians and hospitals are now required by law to provide cost

information for procedures and services to patients who request it.

The new price transparency regulations became effective for physicians and

hospitals on January 1, 2014.