Mediterranean Region Malt&Cyprus

34

1 THE MALTESE AND CYPRIOT ECONOMIES: WEATHERING THE GLOBAL RECESSION Lino Briguglio, University of Malta Andreas Antoniou, Phillips University, Cyprus Gordon Cordina, University of Malta Nadia Farrugia, University of Malta Presentation prepared for the Conference “Sustaining Development in Small States in a Turbulent Global Economy” Commonwealth Secretariat, Marlborough House, London 6-7 July 2009

-

Upload

commonwealth-secretariat -

Category

Documents

-

view

345 -

download

0

Transcript of Mediterranean Region Malt&Cyprus

1

THE MALTESE AND CYPRIOT ECONOMIES: WEATHERING THE GLOBAL RECESSION

Lino Briguglio, University of MaltaAndreas Antoniou, Phillips University, CyprusGordon Cordina, University of MaltaNadia Farrugia, University of Malta

Presentation prepared for the Conference“Sustaining Development in Small States in a Turbulent Global Economy” Commonwealth Secretariat, Marlborough House, London6-7 July 2009

2

INTRODUCTION

Given the high degree of vulnerability to external shocks which characterise small states, one expects that these states, more than any other country grouping, will be highly adversely affected by the current turmoil.

However each region has its own specific circumstances which can not easily be generalised.

As we shall be shown in this presentation, Malta and Cyprus, the two island states members of the EU, are not likely to be as heavily impacted as most other EU member states.

3

INTRODUCTION

The global financial crisis and resulting recession is expected to have profound immediate and long term implications for many small states.

Recent evidence from the IMF’s World Economic Outlook and UNDESA indicate that the smallest and most vulnerable states are already experiencing large terms of trade shocks, declining aid, reduced access to external financing, loss of employment and increasing difficulty in both maintaining the existing progress towards their MDG objectives and making further advances.

4

AREAS OF CONCERN FOR SMALL STATES

For most small states, the major areas of concerns are:

• Drop in remittances from the Diaspora, especially in the Caribbean and Pacific, where they are often the largest or second largest source of foreign exchange;

• Drop in export commodity prices, as a result of the dramatic reduction in global demand;

• Protectionist tendencies in European and North American markets affecting all exports, across the board;

• Drop in tourism revenues;

• Drop in construction activity, especially linked to the tourist industry and residences bought by expatriates and foreigners, across the board;

5

AREAS OF CONCERN FOR SMALL STATES

• Drop in (the already very low) FDI, especially those linked to tourism, construction, and commodity exports, across the board;

• Drop in capital flows due to enhanced political risk, the “flight to quality”, and the focus on short term end of yield curve, across the board;

• Drop in (already low) SME lending, due to the sharp contraction in liquidity and increased risk aversion, even from indigenous banks who take a very short term view, across the board;

6

AREAS OF CONCERN FOR SMALL STATES

• Increase in youth unemployment and crime and illegal immigration, with a growing number of Caribbean, Pacific and Mediterranean countries becoming increasingly vulnerable to these threats to human security;

• Increase in the levels of public debt;

• Renewed and concerted assault by G8 and G22 on so-called “Tax Havens”, in a drive by OECD countries to enhance their fiscal revenues, which affects countries which rely on their International Financial Services Sectors;

• Regulation “externalities” as a result of calls for enhanced, costly, national and international regulation and supervision thus putting additional pressures on already severely capacity-constrained administrations, across the board;

7

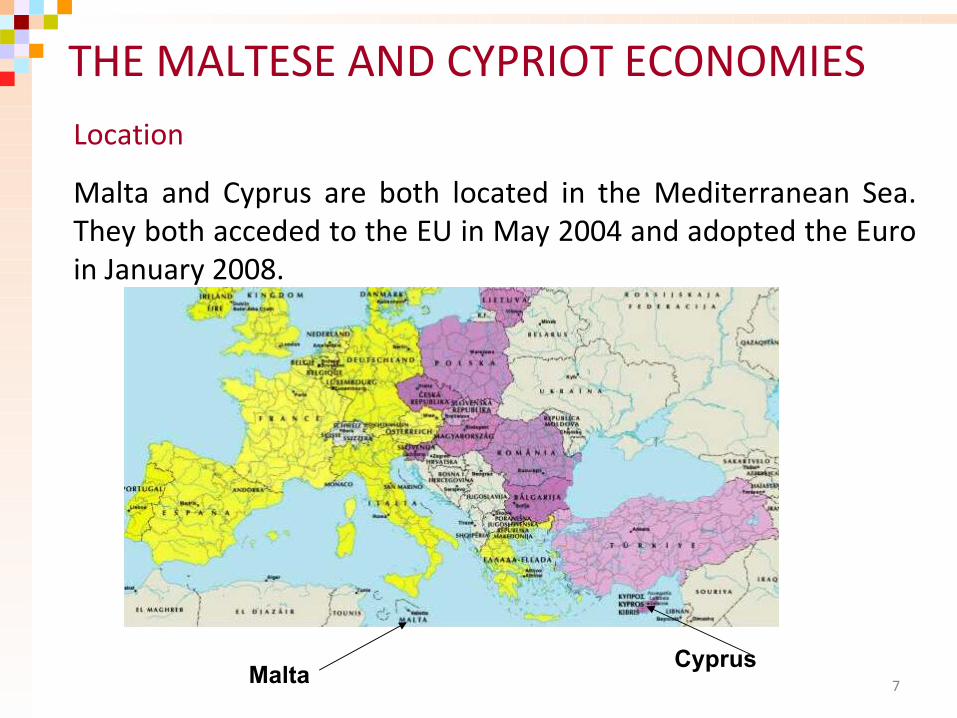

THE MALTESE AND CYPRIOT ECONOMIESLocation

Malta and Cyprus are both located in the Mediterranean Sea. They both acceded to the EU in May 2004 and adopted the Euro in January 2008.

MaltaCyprus

8

THE MALTESE AND CYPRIOT ECONOMIES

Some Comparative Data

Malta CyprusPopulation ’000 (2009) 413 793

Per Capita GDP in PPS as an % of the EU 27 (2008)

76.3% 94.6%

GDP (2008) $10 billion $25 billion

Per Capita GDP $ ‘000 (2008) 23 32 (Greek Cypriots)

Territory Size 316 KM2 9,251 KM2

Population Density 1250 per KM2 90 per KM2

Life Expectancy M=77.1 F= 81.6 M=75.0 F= 80.0

9

THE MALTESE AND CYPRIOT ECONOMIES

Vulnerable Economies

Like many other small states, Cyprus and Malta are inherentlyhighly vulnerable to external shocks. This vulnerability stems from a number of inherent and permanent economic features, including: • a high degree of economic openness, which renders the

economy particularly susceptible to economic conditions in the rest of the world;

• dependence on a narrow range of exports, giving rise to risks associated with lack of diversification;

• dependence on strategic imports, in particular energy and industrial supplies, exacerbated by limited import substitution possibilities.

10

THE MALTESE AND CYPRIOT ECONOMIES

Additional Constraints

Small size leads to additional constraints, such as a limited ability to reap the benefits of economies of scale, high infrastructural, administrative and other overhead costs, and the prevalence of natural monopolies and oligoplistic structures, which lead to high consumer costs.

Small size also creates problems associated with public administration mostly due to the fact that many government functions tend to be very expensive per capita when the population is small, due to the fact that certain expenses are not divisible in proportion to the number of users.

11

THE MALTESE AND CYPRIOT ECONOMIESEconomic Resilience

However, the extent to which the Maltese and the Cypriot economies can cope with their inherent economic vulnerability depends on their economic resilience, that is the policy-induced ability of their economies to withstand or recover from the effects of adverse shocks and to benefit from positive shocks.

In Malta and Cyprus economic governance is overall of a relatively high level. EU accession has improved macroeconomic management and market efficiency.

In addition, the adoption of the Euro in 2008 meant that both Malta and Cyprus had to adhere to the Maastricht criteria, again leading to improvements in macroeconomic management and improved market efficiency .

12

MALTA AND THE GLOBAL FINANCIAL CRISIS

Economic Growth

Indicators of economic growth over the past decade show that the Maltese economy had to grapple with the effects of a global economic slowdown around the turn of the century and continued to experience relatively mild growth until 2004, mainly due to an urgent need for consolidation of its fiscal position with a view of eventual adoption of the euro currency.

A significant recovery from these external and internal policy shocks was registered between 2005 and 2007, when real economic growth averaged around 3.5% per annum. With the onset of the global recession in 2008, the growth of the Maltese economy slowed down markedly, evidence of its pronounced openness.

13

MALTA

Sectors most highly hit by the global crisis

The sectors of activity which were immediately hit included mainly manufacturing oriented towards mass markets, such as suppliers to the automotive industry and to producers of electronic goods. Tourism was also very negatively affected.

As a result the Maltese economy has entered in a recession in 2009. A slight recovery in activity is expected by 2010.

14

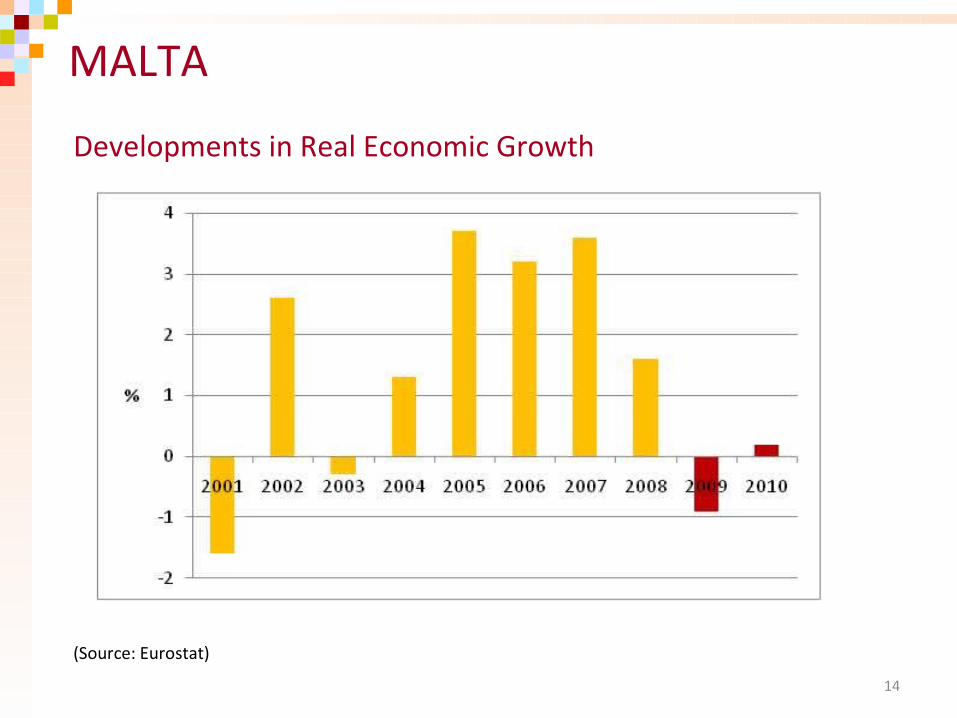

MALTA

Developments in Real Economic Growth

(Source: Eurostat)

15

MALTA

Malta’s business cycle

Malta’s business cycle was very much synchronized with that of the EU15 countries between 2000 and 2008, but business cycle fluctuations in Malta tended to be three times as pronounced as those of the EU15 group. This is explainable by Malta’s openness to trade with these countries, whereby shocks to international demand would influence its output to a relatively large extent. According to EU Commission forecasts, this relationship is expected to be broken in 2009 and 2010, with Malta falling into recession but to a much moderate extent than the group of EU15 countries. Indeed, EU Commission forecasts indicate that whereas the EU15 group of countries are expected to experience a drop in GDP of over 4% in 2009, Malta’s GDP is expected to drop, but by only 0.9%, in the same year.

16

MALTAConfidence in the financial system

The principal cause of the economic crisis around the world, namely the collapse of the confidence in the financial system which led to a freezing of credit lines and to substantial increases in interest rate risk margins, is largely absent from Malta. This may be ascribed to a number of factors, including:• sound banking practices thanks to which Maltese banks did not

enter into risks that were not fully understood• an almost complete reliance on domestic retail deposits, which

constitute a stable source of financing, rather than the significantly more volatile wholesale funds

• and strong regulatory framework which is in line with international best practices

• the introduction of euro, which led the credibility of a global currency to the domestic financial system.

17

MALTAExpansionary fiscal stance

Another reason for the expected relatively buoyant performance of aggregate demand in Malta is the continued expansionary fiscal stance. Malta had one of the highest fiscal deficit to GDP ratios among EU countries in 2008, amounting to 4.7%. This was conditioned by two exceptional factors, namely the provision of subsidies to households on electricity and water services, as well as redundancy payments to workers upon the closure of the ship-repair industry. Exceptional as they were, these payments contributed to sustain aggregate demand in 2008. For 2009, the Government is implementing a fiscal stimulus package amounting to 1.6% of GDP, in line with practices in other EU Member States. This effort will mostly go to capital expenditure, investment in human capital and a reform of taxation towards promoting energy-efficient transport.

18

MALTA

Longer term dangers of the fiscal stimulus

The fiscal stimulus efforts are at this stage necessary to act as a buffer against the downturn in external demand. They could however delay the eventual recovery of the Maltese economy in line with international developments if the mechanisms for revenue growth are not sufficient, thereby leaving the fiscal accounts with a structural deficit, and if expenditure resources are not deployed productively

19

MALTA

Investment and aggregate demand

Aggregate demand in 2009 and 2010 is expected to be supported by an expansion in investment expenditure. This will in part reflect public expenditure referred to above, but it will also result from the expenditure on projects to be financed by European Union Structural Cohesion and other Funds.

As an Objective 1 country, Malta will be benefiting from funding amounting to €1.15 billion in the period 2007-2013. This is equivalent to around 2% of GDP per year.

20

MALTA

The resilience of the Maltese economy

The argument regarding the relative resilience of the Maltese economy in this recessionary period can be explored from a production perspective. Malta’s vulnerability lies in those sectors of economic activity which are mostly export-oriented, while it is less resilient in those sectors which lack competitiveness. Vulnerable sectors include the tourism sector, namely transport & communication and hotels & restaurants, and high-tech manufacturing, namely electrical & optical, which depend mainly on foreign demand. It is less resilient in those sectors which lack competitiveness, such as other manufacturing.

21

MALTA

Effects on Employment

Employment is likely to be affected by the recession.After increasing significantly in 2007, employment growth increased by just over 1% during 2008, while in 2009 such growth is expected to be negative. Similar to GDP growth, employment growth during 2010 is expected to rise marginally.

The defence of jobs is crucial to overcome the downturn and to minimize the impact on the economy’s living standards. However, it should be cautioned that short-term and temporary measures to curtail job losses do not come at the expense of labour market flexibility, as this would jeopardise the eventual recovery and result in less potential growth when jobs recover in the medium term.

22

CYPRUS

Benefits of EU accession

Like Malta, Cyprus has benefited from its accession to the EU and the adoption of the Euro via, inter alia, the implementation of structural reforms.

The adoption of the Euro as from January 2008, has protected the Cypriot economy from the severe implications of the current financial crisis.

23

CYRPUS

Relatively good performance

In Q4 of 2008, the real (seasonally adjusted) GDP growth rate in Cyprus was nearly 3 per cent, the highest in the Eurozone, while for the entire year the rate was 3.7 per cent, the third highest in the Eurozone. [1],

This growth was achieved in conditions of near full employment, with unemployment rate for the same year 3.7 per cent, while employment grew at 2.8 per cent and inflation has kept under 2 per cent.

[1] See for more details, see Cyprus Ministry of Finance, Cyprus, a well managed and resilient Euro member: Investors’ Presentation. May 2009; see also, Η Κυπριακή Οικονομία-Ανασκόπηση και Προοπτικές. Παρουσίαση, Υπουργός Οικονομικών, 3ο Συνέδριο Οικονομίας ΟΕΒ, 26. 3. 2009, http://www.mof.gov.cy.

24

CYRPUS

Resilient Economy

In 2009, despite an unavoidable deceleration in its rate of growth, resulting from the particularly adverse external environment, the economy is coping relatively well. Overall the financial sector remains sound, with a strong liquidity position and a comfortable capital adequacy as well as sufficient profitability. Indeed, in Q1 of 2009, GDP grew at an impressive (under the circumstances) 1.6 per cent, the only economy in the EU27 to have a positive growth, while for 2009, it is now expected to grow at around 1 per cent. This, although positive, is well below the one anticipated at the end of 2008, namely 2.9 per cent. It is also worth noting that this positive growth rate is expected to be achieved again under conditions of near full employment and price stability.

25

CYRPUS

Public finances

The public finances will inevitably show deterioration this year, being negatively affected by the slowdown of the economy, as well as the changed composition of growth.

A deficit of around 2-2.5% of GDP is expected. In this respect, it is worth observing that the fiscal policy will remain prudent. Indicative of the sound fundamentals of the Cypriot economy, has been the response of European investors to the government’s recent Euro bond EUR billion 1.5 issue which was oversubscribed by over 450%, at a relatively favourable cost (3.75 per cent).

26

CYRPUS

Mild repercussions

Given these relatively mild repercussions of the current GFC on the Cyprus economy the policy response by the Government and the Central Bank, have been, muted, cautious and targeted. In the heals of an already modestly expansionary 2009-10 budget, the response to the crisis followed a two-prone approach, a macroeconomic stimulus accompanied by a number of targeted measures, aiming at a positive impact on GDP 2009, of around 1.5 per cent

27

CYPRUS

Policy responses

More specifically, an additional fiscal stimulus package of EUR million 470 was announced to be implemented in two packages, the first in December 2008 and the second, in February 09. The stimulus focused on four strategic sectors: infrastructure projects/employment, tourism, construction and banking and financial sector, and was accompanied by a series of other policy initiatives aimed at accelerating and facilitating budget implementation.

28

CYRPUS

Investment and fiscal stimulus

In particular, EUR million 207 were earmarked for infrastructure projects and pro-employment policies, EUR million 63 for the tourism sector and EUR million 200 for the construction and housing sector. In addition, with a trusted and well regulated banking and financial system and a robust banking sector, the initiatives regarding the financial sector focused on a series of major liquidity injections through the issue of government bonds, EUR million 315, temporary deposits of government liquidity in the banking sector, EUR million 700, the extensive use of guarantees to facilitate access to low-interest sources of finance by the banks, the injection of some EUR million 300 earmarked for low-interest loans to SMEs, and moral suasion for the reduction of interest rates, which nevertheless remain unusually high.

29

CYRPUS

Other policy initiatives

Other policy initiatives included, the acceleration/simplification of public tender procedures, the continued implementation of the structural reforms under the EU’s National Reform Programme, but also the on ongoing modernisation of the public sector with a view to reducing wage-related expenditures and raising total productivity, the enhancement of public debt and cash management systems, further improvement in tax collection, and the continued close monitoring of the liquidity and capital adequacy of the three major banking groups.

30

CYRPUS

Credit rating

It is therefore not surprising to note that despite the global financial crisis, Cyprus is still rated in the double A category by two of the three major rating agencies, Moody’s and Fitch, and A+/Stable by Standard and Poor.

31

CONCLUSIONS

Why Cyprus and Malta have been “spared”

The current global crisis is and will be presenting difficulties to the Maltese and Cypriot economies, but the effects are not as dramatic as is the case in the USA and the UK.

These effects have been relatively subdued due to:• the soundness of the financial system• the provision of fiscal stimuli• investment projects expected in the short term• a reduction in inflation• resilience in the productive sectors of the economy

32

CONCLUSIONS

Short-run and long-run solutions

In order to improve the resilience of the Maltese and the Cypriot economies and thus reduce the negative impacts of the global recession, focus needs to be placed on timely and targeted solutions in the short-term.

But in the medium and long term, these small states need to focus on more specific niche markets, which would be less susceptible to fluctuations in foreign demand.

33

CONCLUSIONS

Supply side policies

It is important that these small states focus on supply-side policies to render their economies more competitive and consequently more resilient.

Indeed, it may argued that in the case of small economies, where market failure is more prevalent and the supply side is burdened with additional constraints, the use of supply-side policies is even more important than in larger countries.

Such policies should be aimed at improving the proper functioning of markets and overcome the additional costs which such countries face due to their inability to reap scale economies and their lack of economic diversification.

34

CONCLUSIONS

Small states will remain vulnerable, but they can do something about it

It is important to note that the relative good performance that the Maltese and Cypriot economies may be enjoying at present, relative to other larger economies, does not negate their economic vulnerability. They will remain very open to external shocks and highly dependent on strategic imports.

However, the resilience elements that these economies have developed over the years, including the strength and stability of the financial system, and the growth in investment in new economy services, are assisting them to better weather these difficult times.