Medco Investment Strategy during Downturn Oil...

15

1 1 Medco Investment Strategy during Downturn Oil Era Hilmi Panigoro President Director of Medco Energi International SIEP Conference- Houston Texas, 19 November 2016 Delivering Energy www.medcoenergi.com

Transcript of Medco Investment Strategy during Downturn Oil...

1 1

Medco Investment Strategy during Downturn Oil Era

Hilmi Panigoro

President Director of Medco Energi International

SIEP Conference- Houston Texas, 19 November 2016

Delivering Energy

www.medcoenergi.com

2 2

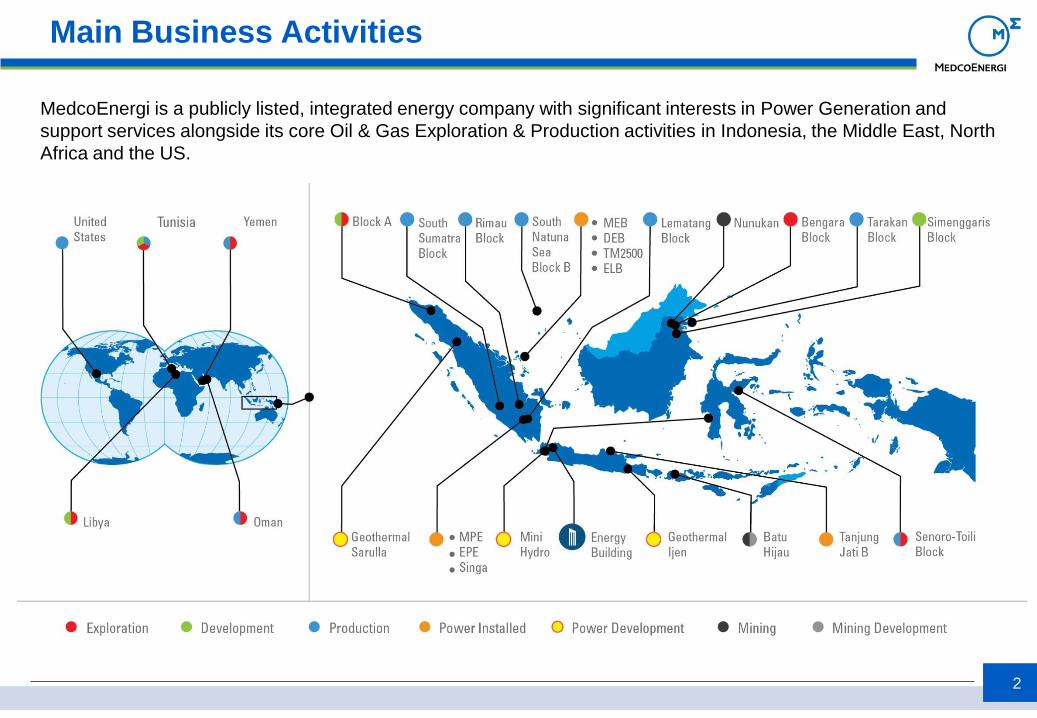

Main Business Activities

MedcoEnergi is a publicly listed, integrated energy company with significant interests in Power Generation and

support services alongside its core Oil & Gas Exploration & Production activities in Indonesia, the Middle East, North

Africa and the US.

3 3

2005

Awarded

EPSA IV PSC

Contract for

Area 47

Libya

1980

Established

as Meta Epsi

Pribumi

Drilling

Company

1994

Initial Public

Offering in

Indonesia

1995

Acquired

100% shares

of Stanvac

Indonesia

from

Exxon/Mobil

1996

Discovered

largest

onshore oil

reserve

(Kaji-

Semoga)

2007

Discovered

352 MMBOE

hydrocarbon

resources in

Area 47

Libya; about

90%

exploration

success ratio

2009

LNG Sales

Agreement

signed with

Japanese &

Korean

buyers, gas to

be supplied

from Senoro-

Toili Block

2010

Obtained 20-

year

extension for

3 PSC

contract area

in Indonesia

(South

Sumatra,

Block A and

Bawean)

2011

Obtained

Commerciality

approval on

Area 47, Libya

Received Final

Investment

Decision for

Senoro-Toili

Gas and LNG

projects

2012

Acquired 25%

in Block 9

Malik, Yemen

First coal

sales

shipment to

China

2006

Awarded

Oman Service

Contract.

Increased

production up

to 100% in 5-

years time

Senoro and

DSNLG

commence

operation

25 year of

extension for

Karim, Oman

Rimau Block

received 5th

Gold PROPER

Award

Medco Journey to World Class Energy Company

Acquired new

assets in

Tunisia and

Oman

Get Project

Financing for

DSLNG and

Sarulla from

JBIC of

USD 2.7 Billion

2014 2015

Signed SPA with

ConocoPhillips to

acquire 40% WI in the

Block B South Natuna

Sea

Finalized acquisition

50% PT Amman Mineral

Investama which

indirectly control 82.2%

WI in PT Newmont Nusa

Tenggara.

2016

4 4

Changing energy mix

• Fossil fuels continue to provide most of the

world’s energy

• Natural gas is the fastest growing fossil fuel

• Oil grows remain stable

• Coal is the slowest growing fuel

• Continuous rapid growth in renewables

Global Energy Market faces continuous change

Continuous change is the norm for energy markets

Source : BP & Woodmac 2015

5 5

Fluctuation of oil price impacts to company’s strategy

• Oil price fluctuations are common and sharply 5 times within 30 years.

• A challenge for oil and gas companies is how to adapt in a fluctuating environment,

conducts adaptation and mitigation so that the company's goals can be achieved through

the right strategy

6 6

Leveraging MedcoEnergi’s strong domestic position …

• Medco will create value by evaluating each opportunity

against our return and profitability benchmarks.

• With commodity prices projected to remain low, there will

be opportunities to acquire domestic resources.

• The acquisition of PT Newmont Nusa Tenggara and

South Natuna Sea Block B are excellent examples of how

targeted domestic resource acquisitions can create value

for the Company’s stakeholders.

7 7

• Transaction is completed on 2 November 2016

• 87,000 ha Copper & Gold mine located SW

Sumbawa Island, W. Nusa Tenggara Province,

550 m above sea level. 81 km from Mataram.

• 4th generation CoW signed 1986, for 30 years

operation from start of production in 2000

• Producing Mine

Batu Hijau Mine Copper Gold

Proved

Reserves

2.6 bil lbs 2.7 mil oz

Resources 10.3 bil lbs 13.9 mil oz

2015

Production

239.6 mil lbs 0.3 mil oz

Facilities 120,000 tpd processing facility, grinding

facility, pipe assembly facilities for tailings

management, warehousing, 158 mw

coal-fired powerplant, port with ferry

terminal, air services and town site for

housing and school

Batu Hijau mine

PT Amman Mineral Nusa Tenggara

MedcoEnergi Leads “Indonesia, Inc.” to Bring Back Indonesia’s Strategic Assets from Newmont

8 8

Potential Development: Elang with est. resources 12,945 mil lbs

copper, 19.7 mil oz gold with potential to produce 300-430 mil lbs

copper and 0.35-0.60 mil oz gold annually

PT Amman Mineral Nusa Tenggara

MedcoEnergi Leads “Indonesia, Inc.” to Bring Back Indonesia’s Strategic Assets from Newmont

9 9

South Natuna Sea Block B (SNSB)

• An offshore PSC located in the South Natuna Sea with

world class operating scale and large hydrocarbon base

(gross 3P resources > 569 mmboe)

• Current Ownership Structure:

• ConocoPhillips : 40% (Operator)

• INPEX : 35%

• Chevron : 25%

• Current gross production: 266 mmcfd gas and 19 mbopd

oil/condensate

• Current net production 28 mboepd

• SNSB is Operator of the PSC and the West Natuna

Transportation System (WNTS), a 650 km natural gas

pipelines, which services gas sales from 3 producing

PSCs in the South Natuna Sea to the Onshore Receiving

Facility in Singapore

• In place gas-liquids processing, storage and export

infrastructure with additional capacity for future

expansion

• Best in class Health, Safety, and Environmental Records

• Highly experienced and proven operating team of 800

employees and 320 contractors

Sourc

e: C

onocoP

hilip

s O

ct 2

015

Enhancing capabilities through the integration of world-class offshore operations.

10 10

The largest single-contract geothermal power project in the world

Production Well Drilling Progress

• Located in Tapanuli Utara district, North

Sumatra with contracted capacity of

3X110MW.

• 30 years Energy Sales Contract with PT PLN

with Take or Pay 90% capacity factor. Joint

Operating Contract with PT PGE.

• Ownership:

₋ MPI (18.9975%),

₋ INPEX (18.2525%),

₋ ORMAT (12.75%),

₋ ITOCHU (25%),

₋ KYUSHU (25%)

• Total project investment cost of US$1.6 billion.

• Secured project financing of US$1.17 billion

for 20 years with JBIC, ADB, and 6

commercial banks.

• As of September 2016 Phase I and Phase II

power plant construction progress have

reached 95.8% and 51.8% respectively. Power Plant Construction Front View

Sarulla Phase I – Geothermal Power Development

11 11

Cost and capital efficiency, operational effectiveness

• Sustainable reductions in our

cash cost structure

• Manage base production

decline and reduce downtime

• Deferral and renegotiation of

exploration commitments

• Selectively capture the

benefits of further supplier

market deflation

Improving unit cash cost°

Managing capital delivery

11 119

4 4

4

Lifting Cost

G&A Cost

9M1

6

7.9

4.7

3.2

2014

A

15

2013

A

16

2016

G*

<10

6-7

2-3

2015

A

13

87

315

357

288

2013

A

2016

G*

100-145

2015

A

2014

A

9M1

6

Capex

US$/BOE

US$ mn

° Cash cost without Oman Service Contract | * Excluding

acquisitions

12 12

Well balanced 2P reserves

57.2%

Domestic

Foreign

152

76.0%

9.4% 146

34.3%

14.6% SNSB 8.5%

• Large well balanced 2P

reserves backed by a strong

resource base

• Monetize our resources

through capital discipline and

project execution

• Prioritize domestic projects for

early cash generation

• Focus on lower risk, cost

effective near field resources

and exploration

• South Natuna Sea Block B

acquisition will add 35 mmboe

of 2P reserves and 23 mmboe

of contingent resources

2P Reserves – 298

Reserves and resources in mmboe, Reserve life index in years

Gas Oil

17 Reserve Life Index

Foreign

Domestic

SNSB

Resources > 380

71.3%

Oil

22.7%

SNSB

Gas

6.0% 6.0%

SNSB

Foreign

71.4%

Domestic

22.5%

13 13

Phase I COD

Q1 2018

Iliran

High

Block A

Simeng

-garis 2013

Appraise Select Define Execution Production

Senoro II

Telisa

Semoga

Matang 2012

Kuala

Langsa 1992

Temelat 2011

Tunisia 2014

Arung 2013 Sarulla

Geo-

Thermal

North

Temelat 2009

Libya 2007

POD Submission

2016

FEED

Completed

2016

Phase I COD

Q4 2016

Libya 2007

Oil Gas Power

Ijen

Geo-

Thermal

Cibala-

pulang

Mini

Hydro

Healthy project pipeline

14 14

619 657566 572

865

1,054982

1,342

623

792

1,102 1,085

884

680

272

0

200

400

600

800

1,000

1,200

1,400

1,600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Tax

GOI's Shares

Total Contribution

Medco’s contribution to the Government of Indonesia in 2015 is

US$ 272 million (IDR 3.6 Trillion) and US$ 12.1 billion in the last 15 years

MedcoEnergi’s contribution to Goverment of Indonesia

15 15

• Global energy market faces continuous change. Changing energy mix, energy pattern and energy prices

• Oil price fluctuations are common and fluctuate sharply 5 times within 30 years.

• A challenge for oil and gas companies is how to adapt in a fluctuating environment, conducts adaptation and mitigation so that the company's goals can be achieved through the right strategy

• Medco will create value by evaluating each opportunity against our return and profitability benchmarks.

• With commodity prices projected to remain low, there will be opportunities to acquire domestic resources.

• The acquisition of PT Newmont Nusa Tenggara and South Natuna Sea Block B are excellent examples of how targeted domestic resource acquisitions can create value for the Company’s stakeholders

Delivering

in 2016

Solid

Liquidity

Looking

Forward

Conclusion