Measuring the Value of Islamic Banks - irti.org the Value of Islamic Banks Abdul Ghafar Ismail,...

28

WP# 1435-13 Measuring the Value of Islamic Banks Abdul Ghafar Ismail, Sjaiful Akbar, Siti Manisah Ngalim 3 Ramadan 1435H | June 30, 2014 Islam2c Economics and Finance Research Division IRTI Working Paper Series

Transcript of Measuring the Value of Islamic Banks - irti.org the Value of Islamic Banks Abdul Ghafar Ismail,...

WP# 1435-13

Measuring the Value of Islamic Banks

Abdul Ghafar Ismail, Sjaiful Akbar, Siti Manisah Ngalim

3 Ramadan 1435H | June 30, 2014

Islam2c Economics and Finance Research Division

IRTI Working Paper Series

IRTI Working Paper 1435-13

Title: Measuring the Value of Islamic Banks

Author(s): Abdul Ghafar Ismail, Sjaiful Akbar, Siti Manisah Ngalim

Abstract

This study tries to measure the effect of risk sharing in adding value to Islamic banks. In particular, this study is important to accurately gauging the impact of Islamic banking sector on the real economy. The adoption of risk sharing modes of contracts by Islamic bank as intermediary would leads to the fairness in serving the interest of community as a whole and is expected to promote value creation to the depositors, shareholders and eventually to the economy. In analysing the value added or wealth created by Islamic banks, we will use the Annual Reports of Islamic banks in Malaysia from 2008-2012. Our analysis will focus on main hypothesis, i.e., risk sharing create more value added and equitable distribution of wealth. Our finding shows that the adoption of risk sharing would lead to the fairness in serving the interest of community as a whole and is expected to promote value creation to the depositors, shareholders and eventually to the economy. The treatment on non-performing financing and investment risk allowance might change the distribution of wealth. Financial reporting based on contract might produce a more transparent distribution of wealth.

Keywords: risk sharing, Islamic banks; value added, wealth distribution, economic development

JEL Classification: D30, E01, G02, G21, 047,

Islamic Research and Training Institute

P.O. Box 9201, Jeddah 21413, Kingdom of Saudi Arabia

IRTI Working Paper Series has been created to quickly disseminate the findings of the work in progress and

share ideas on the issues related to theoretical and practical development of Islamic economics and finance

so as to encourage exchange of thoughts. The presentations of papers in this series may not be fully polished.

The papers carry the names of the authors and should be accordingly cited. The views expressed in these

papers are those of the authors and do not necessarily reflect the views of the Islamic Research and Training

Institute or the Islamic Development Bank or those of the members of its Board of Executive Directors or

its member countries.

Measuring the Value Added of Islamic Banks

Abdul Ghafar Ismail1

Islamic Research and Training Institute

Islamic Development Microfinance institution

P.O. Box 9201, Jeddah 21413 Kingdom of Saudi Arabia

e-mail:[email protected]

Sjaiful Akbar2

Research Center for Islamic Economics and Finance

School of Accounting

Universiti Kebangsaan Malaysia

43600, Bangi, Selangor, Malaysia

Siti Manisah Ngalim3

Department of Accounting and Finance

Universiti Putra Malaysia

Serdang

Malaysia

1. Introduction

A significant development and rapid expanding trend of Islamic banking in the present

century can be witnessed in the Muslim countries as well as major western countries

such as United Kingdom, Australia, and Hong Kong. At the outset, the crux of Islamic

banking departure from conventional banking systems is the prohibition of Riba, in

which the orthodoxy equates with interest in general term while promoting risk sharing

as a viable alternative for Islamic bank to operate as intermediary. Leaving itself from

interest as its central allocation tool, Islamic bank has developed an impressive range

of modes of transactions which primarily based on risk sharing that could appeal to

different types of customers. These include two major modes of contracts, namely

mudharabah and musharakah that is desirable in an Islamic context due to the

characteristics on fair sharing of profit/loss and risk between contracting parties. By

offering these modes of contracts, as highlighted by Nik Hassan et.al. (2004) and Ismail

(2010), Islamic banking system should seek for social economic justice in order to

create an environment that promotes cooperation among society. The adoption of risk

sharing modes of contracts by Islamic bank as intermediary would leads to the fairness

1He is head of research division and Professor of Banking and Financial Economics. He is currently on

leave from School of Economics, Universiti Kebangsaan Malaysia. He is also principal research

fellow, Institut Islam Hadhari, Universiti Kebangsaan Malaysia and AmBank Group Resident Fellow

for Perdana Leadership Foundation. 2 Post-graduate student 3 Lecturer of Islamic accounting

* Paper has been presented at 1st International Conference on Islamic Banking and Finance, 17th –

19th April, 2014, Bayero University, Kano-Nigeria

in serving the interest of community as a whole and is expected to promote value

creation to the depositors, shareholders and eventually to the economy.

Unlike risk sharing, instruments that are interest-based are prone to favour the

rich people and against the interests of the common people. For example, when

entrepreneurs borrow huge amounts of money from the bank, they are utilizing

depositors share into their profitable project. However, when they earn profit, they will

pay nothing to the depositors. In the event of losses, it may lead to the bankruptcy of

the bank itself and ultimately depositors will have to bear the whole loss. This is how

interest-based systems create inequity and imbalance in the distribution of wealth to the

economy. Generally, in risk sharing, both depositors and entrepreneur would be willing

to share the results of the project in an equitable manner. In the case of profit, both will

share in pre-agreed ratios and in the case of loss, all financial loss will be borne by the

capital provider (Islamic bank) and labour losses is borne by the entrepreneur. This

would build a link between both parties that have business skills but lack of capital and

capital provider. The beauty of risk sharing attributes as modes of contract, could

facilitate the role of Islamic banks in providing or channelling funds to the skilled

entrepreneur in an effort to encourage economic growth.

According to Matthews, Tlemsani and Siddiqui (2004), the Islamic economic

principles of risk sharing as well as joint involvement in the wealth creation activity

through equity financing by investors and entrepreneurs has a potential to entice

creativity and productivity in an economy. In addition, risk sharing contracts might

drive fairness and subsequently create value for each contracting parties involved.

However, experiences (Abalkhail and Presley, 2000; Ahmed, 2002, Tohirin and Ismail

(2011)) show that there are some inherent problems (asymmetric information, moral

hazard and adverse selection) that might hinders the application of risk sharing. Despite

of that, Al-Jarhi (1999) proposes that Islamic banking needs to have an equilibrium

combination between mark-up modes and profit-sharing modes of financing.

Based on the above studies, it is understood that the adoption of risk sharing

contracts might lead to value creation to the shareholders, customers and economy as a

whole. Besides that, it drives the Islamic banking system to the different platform that

would create balance between the material and social objectives in an effort to provide

fairness and justice. Therefore, the success of the application of risk sharing modes in

Islamic banking systems will depend heavily on the resolution of the imperfections

associated with their use.

However, the studies on the effect of risk sharing in adding value to Islamic

banks are none. This study is important to accurately gauging the impact of Islamic

financial sector on the real economy essential for further work in this area.

This article is structured as follows - Section 2 provides an insight into the

relationship between finance and economy, in Section 3 the conventional measure of

value added is outlined in terms of the current international statistical framework for

the financial sector and subsectors; the general issues surrounding the appropriateness

of national statistical conventions for measuring of financial sector activity, and

specifically banks, are explored in Section 4; and Section 5 concludes.

2. An Insight into the Relationship between Finance and Economy

Analysing the earlier literature on finance and development theory, as proposed by

Schumpeter (1912) and summarised by Ebner (2000), Schumpeter said that “…the

process of economic development by combining the exploration of entrepreneurship

and innovation as internal mechanism of change with the cyclical fluctuations that

shape the contours of the development process.” In short, he analysed the association

between extra cash or capital and the process of economic development through the

exploration of entrepreneurship and innovation as the internal mechanism of change. In

this, entrepreneurs aims at generating profit, where profit is not the end in itself but a

means towards a greater end that includes creating family-dynasty or empire as well as

gaining power, authority and control. As the excess cash becomes financial institutions,

entrepreneurs become companies but the motivation remains.

Since, then, the focus has been on the direction between finance and economic

development. Development has always been portrayed as an increase in income and

wealth or GDP. Nevertheless, it is worth to mention the conclusion made by Lawrence

(2003). He surveyed research on this relationship and concluded from a total of 24

researches done between 1995 and 2003, that there is evidence for causation between

growth and finance, specifically from growth to finance and for bi-directionality. He

suggests that the data gathered from the survey suggested that financial development

thrives where real economy activity is strong.

However, some earlier literatures (see Levine (2004)) could not agree with one

direction of the relationship by looking into both theoretical and empirical work. He

first identified that the problem within the empirical works frequently sourced from

insufficient precise link between theory and measures. He then analyses researches

covering cross-country research, different type of studies (panel, time-series and case-

studies), industry and firm level, bank- or market-based system and reported evidences

of a strong positive link between the functions of the financial system and long-run

economic growth. He concluded that advancement on this area of research should from

now on be on development of a better model that could capture the dynamic of the

interaction between the evolution of financial system and economic growth. More

importantly, as if drawing the attention back to Schumpeterian theory of finance and

growth that looks into the relationship between entrepreneurs and access of capital, he

highlights a more relevant but related issue that is the role of finance in alleviating

poverty and income inequality.

Specifically Levine (2004) highlights the work of Beck, Demirguc-Kunt and

Levine (2004), who made the first attempt in examining whether financial development

exerts a large influence on the poor (rather than the relationship between financial

development and the level of income inequality or level of poverty). They analysed the

relationship between financial development and income distribution, and relationship

between financial development and alleviation of poverty, from data taken from 52

developed economies and 58 developing countries, respectively. They find income of

the poor grows faster than average GDP per capita, income inequality fall more rapidly

and poverty rates decrease at a faster rate, all induced by greater financial development.

Therefore, financial development has empirically reduces poverty by having a positive

effect on the poor.

Demirguc-Kunt and Levine (2008) find evidence that financial development

boost the income growth of the lowest income quintile. Particularly, they found that

expanding individual economic opportunity create positive incentive effects, thus

financial development boost efficiency and equity of opportunity. Demirguc-Kunt and

Levine (2009) further analyse the relationship between finance and inequality,

discussing the theory and finding evidences. They pointed out that in theory, financial

developments reduce inequality of opportunity and enhance aggregate efficiency.

Particularly, financial developments that lower fixed costs of accessing financial

services benefit low-income earners to pay for education and health care thus reduce

inequality of opportunity. In addition, financial developments that operate on a broad

margin could facilitate entrepreneurs who have little to offer as collateral thus enhances

aggregate efficiency. Further financial development provides greater access to risk

management and insurance services that directly improve welfare and allow families to

continuously educate their children. More importantly, financial development that

increases economic activity will stimulate the demand for labour; enhance earnings and

provide a richer range of economic opportunities. In this, Demirguc-Kunt and Levine

(2009) highlighted the need for additional research on finance and economic

opportunity. Although inconclusive, these theories are supported by empirical

evidences and clearly promote economic growth. Consequently, they called for

assessment of financial sector policies that affect economic opportunity and poverty.

In relation to this, another group of research looks into the access of financial

services, as it is a fact that having access to financial services, especially by having a

bank account, is the first step towards gaining financial assistance for both households

and firms (Ramji 2009). It is an important channel for finance to promote growth

through provision of credit to the most promising firms (Beck, Dmirguc-Kunt and

Honohan 2009). However, Ghalib and Hailu (2008) reported that the level of access to

financial services, especially in developing countries, is low and that for rural

population, they lack free and unconstrained access to and use of such services. The

access, again specifically in developing countries, often skewed toward those who are

not in dire needs of finance such as large enterprises and wealthier individuals while

those who are really in needs of financial assistance lack access to finance, hindering

their growth and reducing personal welfare (Beck, Demirguc-Kunt and Maksimovic

2005, Claessens 2006, Sarma and Pais 2008). At the same time evidences suggest that

in entirety, financial development or depth is both pro-growth as well as pro-poor (Beck

et al. 2009), where greater access will make both firms and households able to take

advantage of investment opportunities, smooth consumption and insure themselves

(World Bank 2008).

In a report by World Bank (2008), making financial services available to all

potential customers without discrimination spreads equal opportunity and taps the full

potential in an economy. This financial inclusion is crucial in order to avert poor

individuals and small firms from relying on their personal wealth or internal resources

as such reliance could limit their opportunities to invest in their education, become

entrepreneurs or take advantage of promising growth. It points out the fundamental

trade-off between growth and social justice. This is true since rapid growth need wealth

concentration to finance large and indivisible investment projects while it is a fact that

the rich tend to save compared to the poor. In other words, there should exist a

redistribution of wealth in the economy from the rich to the poor, a principle that is

crucial under Islamic economics.

The vast research on finance and income inequality and poverty alleviation,

demonstrate how important it is to look beyond the relationship between finance and

development as portrayed earlier. It implies that there occur a bigger objective of

financial existence and a deeper meaning of development such as alleviating poverty,

securing education, insuring health and make equal opportunity available for all

entrepreneurs without losing focus on the functions of financial intermediaries in

ensuring development of an economy. Regardless of different conclusions from

literature reviews on finance and development by Lawrence (2003) and Levine (2004),

researchers agreed on the important role that financial system plays.

Islamic banking by function is no different than the conventional banking. Kahf

(2007) and Wan-Ibrahim and Ismail (2014) make a very clear and direct comparison

between Islamic banking and conventional banking. Financial intermediaries is the

major function of the conventional banking system, where they receive funds from

depositors/savers and reallocate those funds to borrowers/entrepreneurs who need the

funds for their economic transactions and activities. Islamic banks, also as an

intermediary, are doing exactly the same. Similarly, financing in general is the

provision of factors of production, means of payments of goods and services without

requiring an immediate counterpart to be paid by the receiver. It is equal to what offered

by Islamic financing, which provides factors of production, goods and services for

which payment is deferred. Nevertheless, Islamic banking does not involve lending and

borrowing because interest, is prohibited by the guiding law, the Sharia (Algaoud and

Lewis 2007). Instead it relies on three principles that involve sharing of the actual, real-

life outcomes of production process, namely sharing, leasing and sale (Kahf 2007 and

Wan-Kamarudin and Ismail (2013)). Reliance on these contracts is what makes Islamic

banking a more active stimulant of growth in an economy as compared to conventional

banking.

Khan (1987) illustrated the economic effect of substituting interest with Islamic

financing and found that essentially the same market forces are operative and profit-

shares instead of interest equilibrate the market loanable funds. Given an adequate

supply of loanable funds, under Islamic financing two direct effects will take place.

First, investment maybe higher since entrepreneur can pass part of the uncertainty of

the production to the financiers and no competing financial assets diverting funds from

real investments. Second, the ability to pass part of risk to financier will encourage

composition of investment towards more risky and reduce cost pressure for business

efficiency which fixed interest rate imposed. At the same time it may also lower cost

of production and encourage output, whereas specification of a profit-share will not

affect the price output decision.

Hence, the risk sharing based financing musharaka is the preferred Islamic

mode of financing because it adheres most closely to the principle of profit and loss

sharing (Mirakhor and Zaidi 2007, and Ismail and Tohirin (2009)). Comparing profit-

sharing (mudaraba) with interest-taking (conventional loan) Uthman (2006) found that

workers’ share of profit has a positive impact upon the national profit rate and share.

This condition implies that profit-sharing is more conducive to investment, capital

accumulation and hence job creation than the interest-based system, which is in line

with the Islamic economics aim to redistribute wealth and social justice, maintaining a

balance with individual interests (Khan 2008). Also, financing modes that depend on

profit and loss sharing bring important advantage since they have almost same effect of

direct investment, which brings pronounce returns to economic development (Al-Jarhi

and Iqbal 2001).

3. Measuring Value Added from Islamic Bank’s Balance Sheet

Theoretically, GDP can be viewed in three different ways: The production approach

sums the “value-added” at each stage of production, where value-added is defined as

total sales less the value of intermediate inputs into the production process. For

example, flour would be an intermediate input and bread the final product; or an

architect’s services would be an intermediate input and the building the final product.

The expenditure approach adds up the value of purchases made by final users -

for example, the consumption of food, televisions, and medical services by households;

the investments in machinery by companies; and the purchases of goods and services

by the government and foreigners. Gross savings are calculated as the difference

between GNI (Gross National Income) and public and private consumption plus net

current transfers. GNI and GNI per capita are the sum of gross value added by all

resident producers plus any product taxes (less subsidies) that are not included in the

valuation of output plus net receipts of primary income (compensation of employees

and property income) from abroad. To smooth fluctuations in prices and exchange rates,

World Bank uses a special Atlas method of conversion.4 This is relatively difficult for

an individual financial firm such as Islamic bank. Hence, the income approach is much

more reliable.

The income approach sums the incomes generated by production - for example,

the compensation employees receive and the operating surplus of companies (roughly

sales less costs).

For financial firm, like Islamic bank, the approach to measuring value added

has never been touched before. Firstly, the expenditure approach does not appropriately

capture the full balance sheet composition of the Islamic banks as shown by the

example in Table 1. It only captures the liabilities of Islamic banks.

4 This applies a conversion factor that averages the exchange rate for a given year and the two preceding

years, adjusted for differences in rates of inflation between the country and the G-5 countries. Per capita

is GNI divided by the midyear population?

Table 1: Calculating Wealth from Islamic Banks’s Balance Sheet

In thousand Ringgit Malaysia

Assets 2009 2010 2011 2012

Cash

44,444,333.00

40,022,812.00

55,809,442.00

43,051,750.00

Financing

107,660,630.00

135,185,530.00

188,188,118.00

233,254,753.00

Investment

18,817,183.00

27,154,411.00

25,151,949.00

35,087,066.00

Other Assets

13,641,942.00

16,415,786.00

23,316,069.00

34,514,385.00

Total Asset

184,564,088.00

218,778,539.00

292,465,578.00

345,907,954.00

Equity and

Liabilities

Deposits

67,901,030.00

80,444,219.00

120,267,641.00

160,819,161.00

Investment

92,009,721.00

110,254,031.00

139,155,854.00

140,808,583.00

Other

Liabilities

12,481,960.00

12,345,937.00

14,827,676.00

23,159,234.00

Equity

12,171,377.00

15,734,352.00

18,214,407.00

21,120,976.00

Total Liabilities

Equity

184,564,088.00

218,778,539.00

292,465,578.00

345,907,954.00

Secondly, Islamic banks’ output omits other features such as capital gains and losses,

impaired financings, capital injections and promissory notes. Value added measures a sector’s

output based on production (or transactions) in a given time period. During each period net

income and expense flows accumulate in a profit or loss which is then carried forward to the

balance sheet. Profits in the years preceding the recession, contributed positively to value added

and the balance sheet position of the sector. The losses on Islamic banks’ assets which

materialised subsequently are not, however, treated as negative output in national accounts, as

they are not part of production. Instead, they are only reflected as a reduction in the sectorial

balance sheet. This leads to an asymmetry in the treatment of profits and of holding gains/losses

in national accounts, particularly in the measurement of value added.

As an example, let say, both Islamic banks (A and B) seek to maximise profits, and

have financing books worth RM100 on the asset side of their balance sheets. Bank A operates

a simplified balance sheet and funds its financing book mainly through its deposit base of

RM80. It charges mark-up rate 3 per cent for financing and pays a hiba rate of 1% on deposits.

Bank B raises funds mainly in the wholesale funding market and uses the proceeds onward to

entrepreneurs. It receives 3 per cent mark-up rate on financing and pays 1 per cent on both

deposits and sukuk. An interbank mudarabah rate of 2 per cent prevails.

Table 2: Calculating Value Added from Islamic Banks’s Profit and Loss

In thousand Ringgit Malaysia

2009 2010 2011 2012

Panel A:

Income derived

from investment

of depositors’

funds & others

7,529,747.00

9,837,222.00

10,222,763.0

0

14,231,437.0

0

Financing

income &

hibah

7,215,123.00 9,492,007.00 9,564,415.00 13,411,036.0

0

Other

dealing

income

75,724.00 70,644.00 78,701.00 121,311.00

Other

operating

income

44,771.00 64,278.00 388,848.00 329,081.00

Fee &

commissi

on

192,698.00 206,358.00 185,306.00 362,579.00

Other

income

1,431.00 3,935.00 5,493.00 7,430.00

(-) Allowance

for losses on

financing

(1,139,409.00)

(1,275,674.00)

(780,616.00)

(669,568.00)

(-) Provision

for commitments

& contingencies

(10,978.00) 12,795.00 (54,375.00) (17,640.00)

(-) Impairment

loss from dealing

& investment

securities

(investment risk

reserves)

(26,256.00) (75,089.00) 48,397.00 14,207.00

(-) Transfer

to/(from) profit

equalization

reserve

32,896.00

133,746.00

83,571.00 10,929.00

(-) Other

expenses directly

attributable to the

investment of the

(54,957.00) (103,401.00) (46,771.00) (122,421.00)

depositors and

shareholders’ funds

Panel B:

Total

distributable

income

6,331,043.00 8,529,599.00 9,472,969.00 13,446,944.0

0

(-) Income

attributable to the

depositors

(3,222,239.00)

(3,917,055.00)

(4,784,190.00)

(7,173,697.00)

Deposits

from

customers

Mudaraba

h Fund

Non-

Mudaraba

h Fund

2,282,209.00

2,886,315.00

3,633,550.00

5,617,253.00

Deposits

&

placement

s of banks

& other

financial

institution

s

Mudaraba

h Fund

Non-

Mudaraba

h Fund

1,667,507.00

614,702.00

940,030.00

2,106,397.00

779,918.00

1,030,740.00

2,534,424.00

1,099,126.00

1,150,640.00

3,085,169.00

2,532,084.00

1,556,444.00

Others

74,216.00

48,291.00

42,501.00

155,608.00

Panel C:

Income

attributable to the

shareholders

3,108,804.00 4,612,544.00 4,688,779.00 6,273,247.00

( + ) Income

derived from the

investment of

shareholders’/Isla

mic Banking funds

1,128,414.00

1,349,314.00

1,275,696.00

1,708,353.00

Financing

income &

hibah

693,999.00 900,707.00 834,191.00 1,073,154.00

Other

dealing

income

29,091.00 21,704.00 29,088.00 74,708.00

Other

operating

income

146,038.00 95,254.00 61,312.00 105,626.00

Fee &

commissi

on

241,093.00 318,256.00 341,176.00 436,231.00

Other

income

18,193.00 13,393.00 9,929.00 146,038.00

Panel D:

Total net income

4,237,218.00 5,961,858.00 5,964,475.00 7,981,600.00

( - ) Personnel

expenses

(625,323.00)

(947,427.00)

(862,144.00)

(1,006,381.0

0)

( - ) Other

overheads &

expenditures

(1,572,978.0

0)

(1,983,763.0

0)

(1,891,204.0

0)

(2,649,186.0

0)

( - )

Amortisation of

intangible assets

(7,309.00) (11,131.00) (2,434.00) (4,194.00)

( - )

Impairment loss

from property,

plant & equipment

and other assets

-

(18.00)

-

-

( - ) Finance

cost

(37,580.00)

(39,631.00)

(70,184.00)

(117,755.00)

Panel E:

Profit before

zakat & taxation

1,994,028.00

2,979,888.00

3,138,509.00

4,204,084.00

(-) Zakat

(22,755.00)

(27,479.00)

(28,772.00)

(36,305.00)

(-) Taxation

(503,001.00)

(703,500.00)

(770,840.00)

(1,053,530.00)

Panel F:

Profit after zakat

& taxation

1,468,272.00

2,248,909.00

2,338,897.00

3,114,249.00

(-)

Extraordinary item

-

-

-

-

Panel G:

Profit after the

extraordinary

item

1,468,272.00

2,248,909.00

2,338,897.00

3,114,249.00

(-) Minority

interest

-

(51.00)

(1,325.00)

1,732.00

Panel H: Net

profit for the

financial year

1,468,272.00

2,248,858.00

2,337,572.00

3,115,981.00

The statistical framework treats the operating surplus of these two banks differently.

Firstly, the calculation of banks’ operating surplus is confined to their financing and deposit

portfolio and is not fully representative of their entire balance sheet. Bank A’s profits of

RM1.80, comprise financing book related profits of RM1 = [RM100*(0.03 - 0.02)], and profits

from its deposit book of RM0.80 = [80*(0.02 - 0.01)]. The total profits related to Bank B’s

financing and deposits, are lower, amounting to RM1.20, comprising financing profits of RM1

= [RM100*(0.03 - 0.02)] and deposit profits of RM0.20 = [20*(0.02 - 0.01)]. The sukuk

issuance in the wholesale funding market by Bank B of RM70 is ignored as are its equity assets.

Basically, Islamic banks process payments and other transactions for customers and

nonfinancial companies, screening and monitoring projects, as well as underwriting a variety

of sukuk. The value of such services (Panel A, Table 2), net of items such as allowance for

losses on financing and provision for commitments and contingencies, gives us the Islamic

bank industry’s value added (Panel B, Table 2), which is the industry’s direct contribution to

GDP.

Although, it is difficult to measure the RM amount (let alone the inflation-adjusted real

value) of Islamic banks’ value added. This is primarily because they often do not charge

explicitly for services. Instead, they earn a spread between the mark-up received and the hibah

rates paid (income attributable to depositors), as well as fees for writing sukuk products. But

earning spread is not in and of itself a productive activity that contributes to GDP. This is

obviously sensible in the case of passive investors who buy market sukuk (in the secondary

market) and then merely receive return or dividends without producing new goods or services.

In reality, Islamic banks are not mere passive investors. They do hire workers (see

Panel C) and equipment, and also buy and sell commodities to carry out various services. When

the compensation for such services is not earned explicitly but bundled with asset returns that

arise purely because of risk differentials, the question becomes how to tease out that portion of

an Islamic bank’s overall income that is implicit revenue for services. The net income of an

Islamic bank after these adjustments is a correct measure of its contribution to economic output.

Islamic bank, functioning as the intermediaries between sources of funds and users of

funds, could offer services that would give opportunity to create employment (by spending on

personnel expenses and other overhead and expenditures (Panel D, Table 2), thus assist in

fulfilling the removal of poverty and need fulfilment and also via zakat payment (Panel E).

Finally, Islamic banks also create wealth to shareholders (Panels E, F and G). In addition,

Islamic banks could also be able to provide the freedom of the people in the sense of free from

unnecessary debt, mostly due to spending more than what earned. Banks could assist this notion

of freedom by providing the opportunity to save and invest rather than to spend beyond their

means, which could be related to the offering of credit card. Education is essential to develop

human self, either to develop their intellectuals or to prepare them for employment and self-

employment, which in turn would remove poverty. Though it is not obligated for banks to offer

educational financing, offering such financing would give the opportunity for the public to earn

higher education. Nevertheless, it is noted that banks might also spend their wealth in offering

sponsorship and donation towards education instead of offering financing.

4. Findings

In analysing the value added or wealth created by Islamic banks, we will use the Annual

Reports of Islamic banks in Malaysia from 2009-2012. Our analysis will focus on how

much of the income received by Islamic banks is compensated for actual services

provided to their customers and how much is merely for taking on risk, such as funding

risky financing with short-term deposits?

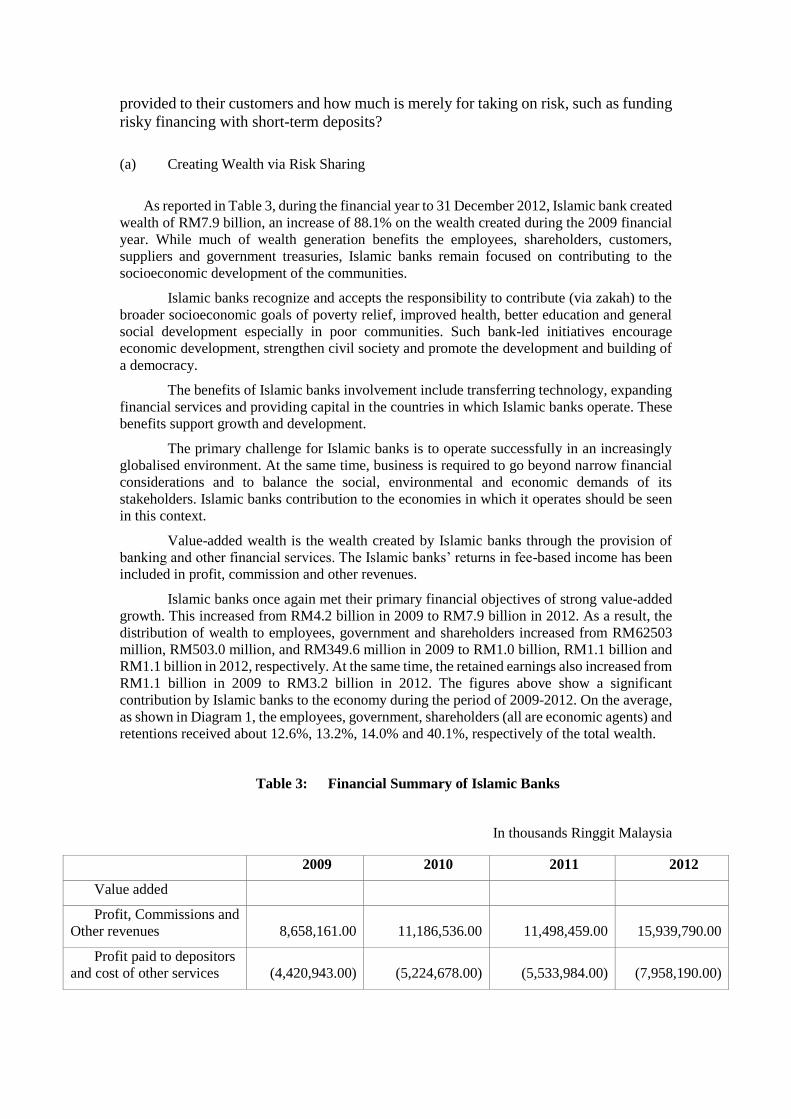

(a) Creating Wealth via Risk Sharing

As reported in Table 3, during the financial year to 31 December 2012, Islamic bank created

wealth of RM7.9 billion, an increase of 88.1% on the wealth created during the 2009 financial

year. While much of wealth generation benefits the employees, shareholders, customers,

suppliers and government treasuries, Islamic banks remain focused on contributing to the

socioeconomic development of the communities.

Islamic banks recognize and accepts the responsibility to contribute (via zakah) to the

broader socioeconomic goals of poverty relief, improved health, better education and general

social development especially in poor communities. Such bank-led initiatives encourage

economic development, strengthen civil society and promote the development and building of

a democracy.

The benefits of Islamic banks involvement include transferring technology, expanding

financial services and providing capital in the countries in which Islamic banks operate. These

benefits support growth and development.

The primary challenge for Islamic banks is to operate successfully in an increasingly

globalised environment. At the same time, business is required to go beyond narrow financial

considerations and to balance the social, environmental and economic demands of its

stakeholders. Islamic banks contribution to the economies in which it operates should be seen

in this context.

Value-added wealth is the wealth created by Islamic banks through the provision of

banking and other financial services. The Islamic banks’ returns in fee-based income has been

included in profit, commission and other revenues.

Islamic banks once again met their primary financial objectives of strong value-added

growth. This increased from RM4.2 billion in 2009 to RM7.9 billion in 2012. As a result, the

distribution of wealth to employees, government and shareholders increased from RM62503

million, RM503.0 million, and RM349.6 million in 2009 to RM1.0 billion, RM1.1 billion and

RM1.1 billion in 2012, respectively. At the same time, the retained earnings also increased from

RM1.1 billion in 2009 to RM3.2 billion in 2012. The figures above show a significant

contribution by Islamic banks to the economy during the period of 2009-2012. On the average,

as shown in Diagram 1, the employees, government, shareholders (all are economic agents) and

retentions received about 12.6%, 13.2%, 14.0% and 40.1%, respectively of the total wealth.

Table 3: Financial Summary of Islamic Banks

In thousands Ringgit Malaysia

2009 2010 2011 2012

Value added

Profit, Commissions and

Other revenues

8,658,161.00

11,186,536.00

11,498,459.00

15,939,790.00

Profit paid to depositors

and cost of other services

(4,420,943.00)

(5,224,678.00)

(5,533,984.00)

(7,958,190.00)

Wealth distribution over four years (%)

2009 2010 2011 2012

Employees

Government

Shareholders

Retentions

Zakat

Others

14.76

11.87

8.25

28.46

0.54

36.13

15.89

11.80

12.32

29.33

0.46

30.19

14.45

12.92

13.71

33.17

0.48

25.25

12.61

13.20

13.96

40.15

0.45

19.63

Wealth created

4,237,218.00

5,961,858.00

5,964,475.00

7,981,600.00

Distribution of wealth

Employees

Salaries and other

benefits

(625,323.00)

(947,427.00)

(862,144.00)

(1,006,381.00)

Governments

(503,001.00)

(703,500.00)

(770,840.00)

(1,053,530.00)

Zakat

(22,755.00)

(27,479.00)

(28,772.00)

(36,305.00)

Shareholders

Dividends paid to

shareholders

(349,561.00)

(734,267.00)

(817,721.00)

(1,114,402.00)

Earnings attributable to

outside and preference

shareholders

-

-

-

-

Retentions to support

future business growth

(1,205,816.00)

(1,700,191.00)

(1,978,984.00)

(3,204,223.00)

Retained surplus

(1,127,032.00)

(1,588,974.00)

(1,958,059.00)

(3,174,963.00)

Depreciation &

amortization

(78,784.00)

(111,217.00)

(20,925.00)

(29,260.00)

Others

(2,706,456.00)

(1,848,994.00)

(1506,014.00)

(6,414,841.00)

Wealth distributed

(4,237,218.00)

(5,961,858.00)

(5,964,475.00)

(7,981,600.00)

Graph 1(a): value added and total assets; (for 2009)

Value added in 10,000 RM

Total Asset in 100,000 RM

-

50,000

100,000

150,000

200,000

250,000

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Value Added

Total Asset

Graph 1(b): value added and total assets; (for 2010)

Value added in 10,000 RM

Total Asset in 100,000 RM

Graph 1(c): value added and total assets; (for 2012)

Value added in 10,000 RM

Total Asset in 100,000 RM

-

50,000

100,000

150,000

200,000

250,000

300,000

- 50,000

100,000 150,000 200,000 250,000 300,000 350,000 400,000 450,000 500,000

Value Added

Total Asset

-

100,000

200,000

300,000

400,000

500,000

600,000

- 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000 900,000

1,000,000

Value Added

Total Asset

Graph 1(d): value added and total assets (for 2009-2012)

13 Islamic Banks in Malaysia

Value added in 10,000 RM

Total Asset in 100,000 RM

Graph 2(a): y-axis: value added and total financings (for 2009)

Value added in 10,000 RM

Total Financing in 100,000 RM

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

2009 2010 2011 2012

Value Added

Total Asset

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

-

50,000

100,000

150,000

200,000

250,000

300,000

Value Added

Total Financing

Graph 2(b): value added and total financings (for 2010)

Value added in 10,000 RM

Total Financing in 100,000 RM

Graph 2(c): value added and total financings (for 2012)

Value added in 10,000 RM

Total Financing in 100,000 RM

-

50,000

100,000

150,000

200,000

250,000

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Value Added

Total Financing

- 50,000 100,000 150,000 200,000 250,000 300,000 350,000 400,000 450,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Value Added

Total Financing

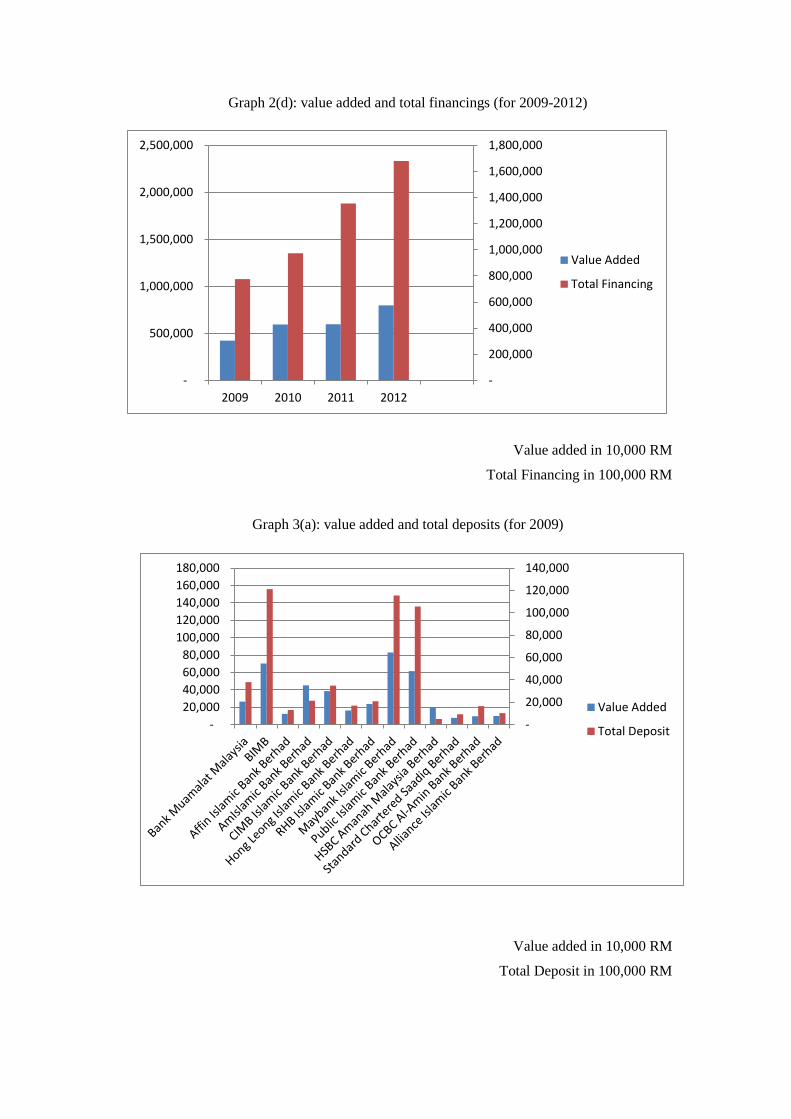

Graph 2(d): value added and total financings (for 2009-2012)

Value added in 10,000 RM

Total Financing in 100,000 RM

Graph 3(a): value added and total deposits (for 2009)

Value added in 10,000 RM

Total Deposit in 100,000 RM

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2009 2010 2011 2012

Value Added

Total Financing

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Value Added

Total Deposit

Graph 3(b): value added and total deposits (for 2010)

Value added in 10,000 RM

Total Deposit in 100,000 RM

Graph 3(c): value added and total deposits (for 2012)

Value added in 10,000 RM

Total Deposit in 100,000 RM

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

- 20,000 40,000 60,000 80,000

100,000 120,000 140,000 160,000 180,000 200,000

Value Added

Total Deposit

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

-

100,000

200,000

300,000

400,000

500,000

600,000

Value Added

Total Deposit

Graph 3(d): value added and total deposits (for 2009-2012)

Value added in 10,000 RM

Total Deposit in 100,000 RM

Graph 4(a): histogram: distribution of wealth by each bank (2009)

In 1,000 RM

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2009 2010 2011 2012

Value Added

Total Deposit

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

Others

Zakat

Retentions

Shareholders

Government

Employees

Graph 4(b): histogram: distribution of wealth by each bank (2010)

In 1,000 RM

Graph 4(c): histogram: distribution of wealth by each bank (2012)

In 1,000 RM

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Others

Zakat

Retentions

Shareholders

Government

Employees

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

Others

Zakat

Retentions

Shareholders

Government

Employees

Benefiting Employees, Customers and Communities

In Islam, wealth should be circulated within and economy in order to ensure equitable

distribution of wealth and could also be the source for employment and self-

employment. Therefore, Islamic bank should redistribute its income and wealth back to

the economy. There are at least several parties that should be considered in

redistributing the wealth as shown in Table 2 and these redistribution are divided into

two, obligatory and voluntarily.

Islamic bank A, as shown in Table 3, paid the employees RM8.5 billion during

2008. The amount paid in 2007 was RM7.6 billion. A conservative economic estimate

indicates that more people directly depend on Islamic bank A for their livelihood.

Customers received an amount of RM31.2 billion during 2008. It contributed a

substantial amount to their wealth. Furthermore, Islamic bank A contribute to the economy by providing affordable,

effective banking and financial services to diverse individuals and organizations; contributing

over RM2.9 billion to the government in the form of taxes in 2008; and promoting economic

stability and convenience in local communities through extensive branch networks.

5. Conclusion

The role of Islamic banks includes: to clear and settle payments; to aggregate (pool)

and disaggregate wealth and to allow flow of funds so that both large-scale and small-

scale projects can be financed; to transfer economic resources over time, location, and

sectors; to accumulate, process and disseminate information for decision-making

purposes; to provide ways for managing uncertainty and controlling risk; and to provide

ways for dealing with risks and return issues that arise in financial contracting. These

roles can be performed by offering financial transactions, pooling savings and

channeling funds. By performing these roles, Islamic banks play a valuable and integral

part in the development of the national economy by creating wealth for individuals and

the community. Therefore, there are a number of suggestion for future research: first,

the adoption of RISK SHARING modes of financing by Islamic bank as intermediary

would leads to the fairness in serving the interest of community as a whole and is

expected to promote value creation to the depositors, share holders and eventually to

the economy. Could a higher RISK SHARING create a better distribution? Second,

regulation such regulation on non-performing financing and investment risk allowance

might change the distribution of wealth. Third, financial reporting based on contract

might produce a more transparent distribution of wealth.

Islamic banks play a valuable and integral part in the development of the national economy.

By focusing on sustainable economic wealth, Islamic banks can economically empower

employees, shareholders and business partners, and can also contribute to the sustainability of

state treasuries and a diverse spectrum of important social development projects. In essence

Islamic banks are able to generate employment and to increase the shareholder’s and

entrepreneur’s wealth. The economic contribution of Islamic banks can be seen by looking at

the following example.

It appears likely that the study states the Islamic banks’ contribution to GDP, and we

now have evidence that this is indeed the case. To the extent that risk sharing is one the

suggested model for Islamic banking, we have a method for proving the superiority of

this method and to arrive at a ‘clear’ evidence of the contribution that Islamic banks

make to GDP. In order to estimate the model’s ability to redistribute wealth, however,

we need to go further and analyse their distribution. Better measures of real financial

output may overturn the current consensus that the financial industry accounted for a

significant portion of the country productivity acceleration over the period 2009 to

2012.

Referencies

Abalkhail, M. and Presley, J.R. (2002), How informal risk capital investors manage

asymmetric information in profit/loss-sharing contracts, in Iqbal, M. and

Llewellyn, D.T. (2002), Islamic Banking and Finance, New Perspectives on

Profit-Sharing and Risk. Edward Elgar, Cheltenham, UK, Northampton, MA,

USA, 111-134.

Ahmed, H. (2002), Incentive-compatible profit-sharing contracts:a theoretical

treatment, in Iqbal, M. and Llewellyn, D.T. (2002), Islamic Banking and

Finance, New Perspectives on Profit-Sharing and Risk. Edward Elgar,

Cheltenham, UK, Northampton, MA, USA, 40-54.

Algaoud, Latifa A. and Lewis, Mervyn K. 2007. Islamic critique of conventional

financing. In Handbook of Islamic Banking. Hassan, M. Kabir and Lewis,

Mervyn K. (editors). Edward Elgar: Cheltenham. Pg. 38 – 48.

Al-Jarhi, Mabid Ali (1999), Islamic economics from a vantage point, Keynote lecture,

International Conference on Islamic Economics towards the 21st century, Kuala

Lumpur, Malaysia.

Al-Jarhi, A.M. and Iqbal, M. 2001. Islamic Banking: Answers to Some Frequently

Asked Questions. Occasional Paper No. 4, Islamic Development Bank, Islamic

Research Training Institute.

Beck, Thorsten, Demirguc-Kunt, Asli and Levine, Ross. 2004. Finance, inequality and

poverty: cross-country evidence. NBER Working Paper Series. (downloaded

from http://www.nber.org/papers/w10979 as at July 2011).

Beck, T.Demirguc-Kunt, A., and V.Maksimovic, “Financial and Legal Constraints to

Firm Growth: Does Firm Size Matter?”, Journal of Finance, 2005, 137-177

Beck, Thorsten, Demirgüç-Kunt, Asli and Honohan, Patrick. 2009. Access to Financial

Services: Measurement, Impact and Policies. World Bank Res Obs. 24 (1): 119-

145.

Claessens, Stijn. 2006. Access to Financial Services: A Review of the Issues and Public

Policy Objectives. The World Bank Research Observer. Vol. 21, no. 2: 207–240

Demirguc-Kunt, Asli, and Levine, Ross. 2009. Finance and inequality: theory and

evidence. NBER Working Paper Series. (downloaded from

http://www.nber.org/papers/w15275 as at July 2011).

Demirgüç-Kunt, Asli and Levine, Ross. 2008. Finance and Economic Opportunity. The

World Bank Development Research Group Finance and Private Sector Team

Policy Research Working PapeR 4468

Ebner, Alexander. 2000. Schumpeterian Theory and the Sources of Economic

Development: Endogenous, Evolutionary or Entrepreneurial? Paper presented

at the International Schumpeter Society Conference on ‘Change, Development

and Transformation: Transdisciplinary Perspectives on the Innovation

Process’, Manchester, 28 June – 1 July 2000

Ghalib, Asad Kamran and Hailu, Degol. 2008. Banking the Un-Banked: Improving

Access to Financial Services. Policy research brief of International Poverty

Centre. Oct/2008, no. 9

Ismail, A.G. and A. Tohirin (2009) Islamic law and finance. Humanomics, 26 (no. 3):

178-199.

Ismail, A.G. (2010) Money, Islamic Banks and the Real Economy. Singapore: Cengage

Learning.

Kahf, Monzer. 2007. Islamic banks and economic development. In Handbook of

Islamic Banking. Hassan, M. Kabir and Lewis, Mervyn K. (editors). Edward

Elgar: Cheltenham. Pg. 277 – 284.

Khan, Shahrukh R. 1987. Profit and Loss Sharing: an Islamic Experiment in Finance

and Banking. Karachi: Oxford University Press

Khan, Salar. M. 2008. Islamic Banking & Finance Rationale, Framework and

Prospectus. In Khan, Salar. M. (editor), Islamic Banking & Finance: Shariah

Principles and Practices. India: IFA Publications.

Levine, Ross. 1997. Financial Development and Economic Growth: Views and

Agenda, Journal of Economic Literature, Vol. XXXV, pp. 688 – 726.

Levine, Ross. 2004. Finance and Growth: Theory and Evidence. NBER Working Paper

No. w10766 (downloaded from http://www.nber.org/papers/w10766 as at July

2011)

Lawrence, Peter. 2003. Fifty Years of Finance and Development: Does Causation

Matter? Keele Economics Research Papers (KERP 2003/07) (downloaded from

http://ideas.repec.org/p/kee/kerpuk/2003-07.html as at July 2011)

Matthews, R., Tlemsani, I., and Siddiqui, A. (2004), Islamic banking and the mortgage

market in the UK, in Shanmugam, Bala. et.al. (2004), Islamic Banking: An

International Perspective, Universiti Putra Malaysia Press, Serdang, Malaysia.

Mirakhor, Abbas and Zaidi, Iqbal. 2007. Profit-and-loss sharing contracts in Islamic

finance. In Handbook of Islamic Banking. Hassan, M. Kabir and Lewis, Mervyn

K. (editors). Edward Elgar: Cheltenham. Pg. 49 – 63.

Nik Hassan, N.M. and Musa, M (2004), An evaluation of Islamic Banking

Developmant in Malaysia, in Shanmugam, Bala. et.al. (2004), Islamic Banking:

An International Perspective, Universiti Putra Malaysia Press, Serdang,

Malaysia. Ramji, Minakshi. 2009. Financial Inclusion in Gulbarga: Finding Usage in Access.

Institute for Financial Management and Research Centre for Micro Finance

Working Paper Series No. 26

Sarma, Mandira and Pais, Jesim. 2008. Financial Inclusion and Development: A Cross

Country Analysis (Preliminary draft for presentation at the Annual Conference

of the Human Development and Capability Association, New Delhi, 10-13

September 2008)

Tohirin, A. and A.G., Ismail (2011) MMM in the Finance-Growth Nexus. Investment

Management and Financial Innovations 7 (issue no. 3), 130-147

Uthman, Usamah A. 2006. Profit-sharing versus Interest-taking in the Kaldor-Pasinetti

of Income and Profit Distribution. Review of Political Economy 18 (2): 209 –

222.

Wan-Ibrahim, W.H. and A.G. Ismail (2014) Conventional Bank and Islamic Banking

as Institutions: As Many Similarities as Differences. Humanomics

(forthcoming)

Wan-Kamarudin, W.N., and A.G., Ismail (2013) Profit sharing and loss bearing in

financial intermediation theory. Investment Management and Financial

Innovations 10 (no.2): 184-192.

World Bank (The). 2008. Access to Finance and Development: Theory and

Measurement. Finance for All: Policies and Pitfalls in Expanding Access. A

World Bank Policy Research Report. The World Bank: Washington DC. –pg

21-53.