Measuring for Success: Redirect Your KPI’s - CUNA · PDF fileMeasuring for Success:...

31

Measuring for Success: Redirect Your KPI’s David Potterton, Research Director CUNA Technology Council September, 2014

Transcript of Measuring for Success: Redirect Your KPI’s - CUNA · PDF fileMeasuring for Success:...

Measuring for Success: Redirect Your KPI’s

David Potterton, Research Director

CUNA Technology Council

September, 2014

“My own mother even pays bills on her mobile phone and never goes to those expensive mausoleums you see all over town that traditional banks have.”

Stock Analyst Supporting a“BUY” rating for Everbank on CNBC SquakBox – July 31, 2014

Changing Banking Models Hitting the Mainstream

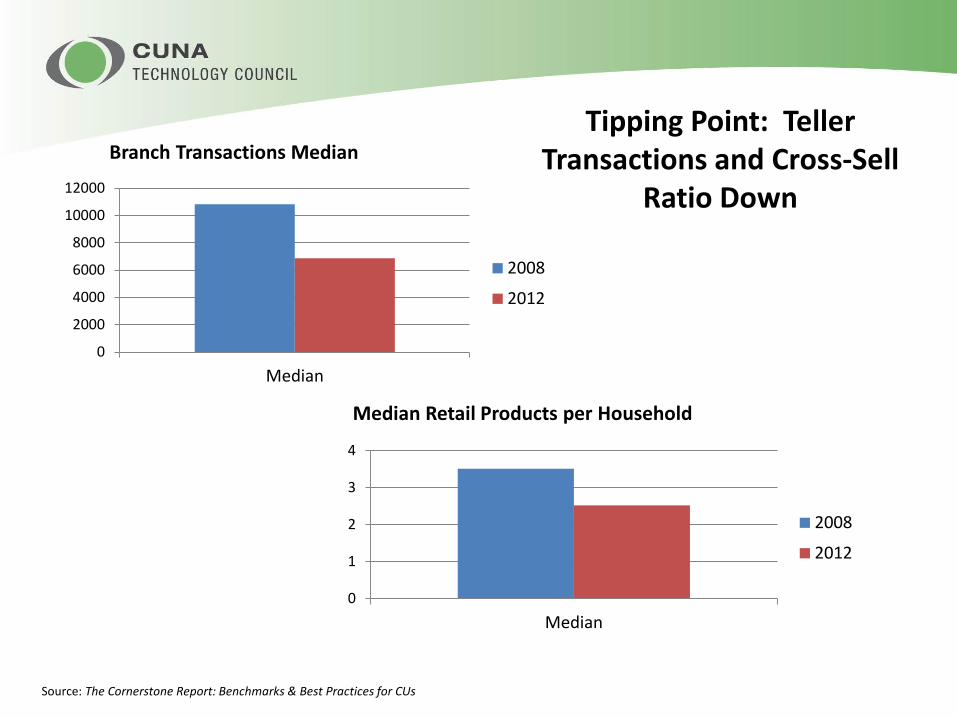

Tipping Point: Teller Transactions and Cross-Sell

Ratio Down

0

2000

4000

6000

8000

10000

12000

Median

2008

2012

Branch Transactions Median

0

1

2

3

4

Median

2008

2012

Median Retail Products per Household

Source: The Cornerstone Report: Benchmarks & Best Practices for CUs

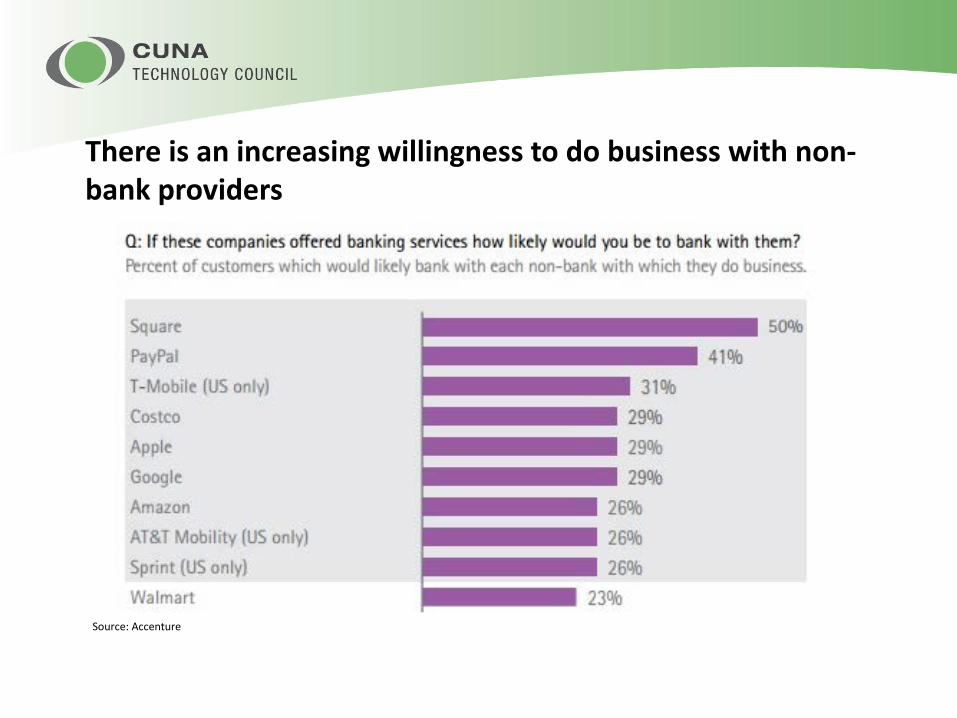

There is an increasing willingness to do business with non-bank providers

Source: Accenture

Business Model Under Attack

Gather Deposits Lending

Expensive Branch Network and Overhead (NIE)

Noninterest Income

Deposits fund loans

Returns for Shareholders/

Members

Earn spread between loans and deposits

Leverage deposit accounts for cross selling opportunities to generate fee income.

Use noninterest income to offset overhead costs.

Funds to Reinvest in the

Business

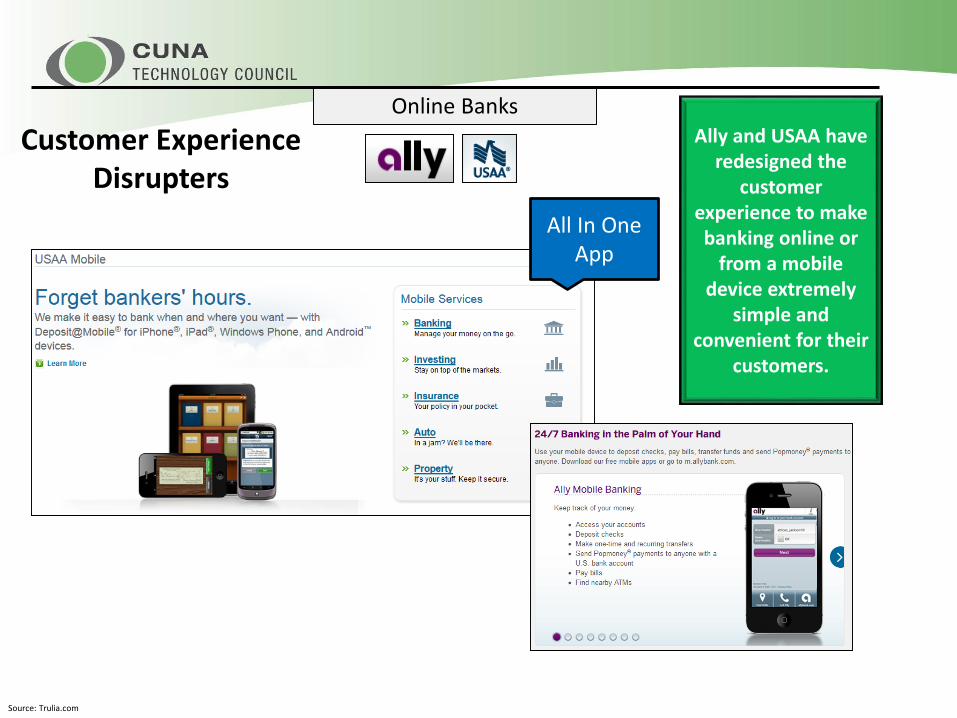

Customer Experience Disrupters

Online BanksAlly and USAA have

redesigned the customer

experience to make banking online or

from a mobile device extremely

simple and convenient for their

customers.

Source: Trulia.com

All In One App

Lending DisruptersMortgage Lending

Impact: Interest Income, Origination Fees, Loan Growth, Cross-Selling Opportunities.

When people change the way they shop for homes, it is likely to impact the way they shop for mortgages as well.

One Click…

Source: Trulia.com

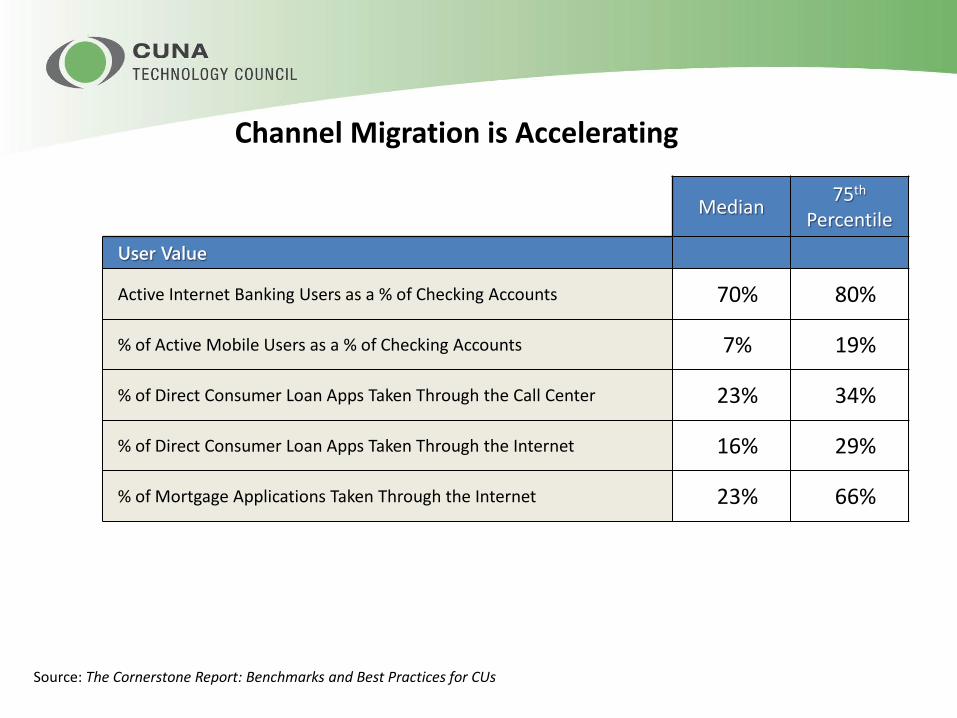

Median 75th

PercentileUser Value

Active Internet Banking Users as a % of Checking Accounts 70% 80%

% of Active Mobile Users as a % of Checking Accounts 7% 19%

% of Direct Consumer Loan Apps Taken Through the Call Center 23% 34%

% of Direct Consumer Loan Apps Taken Through the Internet 16% 29%

% of Mortgage Applications Taken Through the Internet 23% 66%

Channel Migration is Accelerating

Source: The Cornerstone Report: Benchmarks and Best Practices for CUs

Delivery Redirect is about facing up to the tough choices concerning resources, the sales force, and new organizational capabilities that financial institutions must address in order to be viable in 2020 and beyond

Delivery Redirect is not about just migrating transactions but REVENUE PRODUCTION –the optimal mix of channels and resources • to successfully influence the

buying behavior of current and future consumers and businesses

• to drive new and cross sell/upsell revenue

”Channel Of Choice” Is Impractical –Delivery Redirect Is Strategic• It costs too much money to offer

all functionality through all channels

• Rather, institutions need to think about the “right channel” for their members

• It’s not about transactions, but buying interactions and balancing member/customer experience, cost, and security

As Delivery Redirect efforts begin, keep the following Brutal Truths in mind

Stop Trying To Please All Your Customers/Members • Not everyone customers will like their

financial institutions Delivery Redirect efforts

• Perhaps it just wasn’t a good fit from the beginning or these customers are stuck in a banking model which is not in the best interest of the institution’s customer base as a whole

• Those banks who know their target segments well will win

It’s Revolution Not Evolution• Executives will need to make some very strategic and tough choices

in order for their institution to be one of the winners in 2020• The need for speed is paramount as newer and more nimble

competitors continue to challenge the status quo• Technology companies are reaching over into financial services so

banks and credit unions need to think more like technology start-ups

Members Buy The Channel Experience Not Products • Members are focused on channels as this is the way they interact

with their financial institution• In this channel centric (and increasingly mobile) relationship, it’s time

to re-think organizational alignment and focus on capabilities per channel rather than products

Divest to Invest• Delivery Redirect means casting off those channels which no longer

make economic sense• This is not a pure cost play however• Money saved from Delivery Redirect should be utilized to improve

delivery capabilities which promise higher returns in the future

The Branch Will No Longer Be The Primary Channel For Customer Acquisition • There will continue to be physical channel niche players but the

number of branches and physical locations will continue to shrink (and in some cases disappear)

• This traditional method of branding, customer awareness, and acquisition needs a new strategy

• Successful financial institutions will help customers and prospects “discover” their great services and how easy it is to do business with their firms

Delivery Channel Spectrum

• Measurability– Is there an clear, objective definition of the metric?– Can the metric be measured and reported in a timely fashion, e.g. it is

“actionable”?• Peer comparisons

– Do we need to compare ourselves to a peer group to analyze performance?

• If yes, is there a common definition peers use and objective third party data available?

• If no, what is our internal “base” against which we will measure performance or progress?

• Reporting Levels– Is this a corporate-level metric or do we need to shoe it at a more

detailed level (e.g. by branch, by employee)?

Setting Performance Metrics – Key Issues

Sales and Growth

RiskCost and Efficiency

ObjectivesCustomer Acquisition, Loyalty and RetentionTools• Experience and Process Mapping• Service Level Standards• Customer Satisfaction Surveys

Sales/Growth Metrics• New relationships by channel• Account applications by channel

– Deposits– Loans (consumer, mortgage)

• Cross-sell by channel

Cost and Efficiency Metrics• New accounts closed per employee

– Deposits– Loans

• Blended cost per new account acquisition• Self-service transactions as a % of total transactions• Accounts serviced per branch/call center employee• Blended cost per servicing transaction

Risk Metrics• Losses by channel• Delinquencies by channel• Number of Risk FTE’s per asset size• Dollar amount of risk spending by asset size

Sales and Growth

Risk

Cost and Efficiency

First Step• First understand your organizations business strategy; long-term vision,

business model, brand, objectives and priorities, in order to realize the impact to your channels especially across Channel Performance and Potential

Branch• Full Service• Sales Branch• Tech Branch• Loan Production Office

• Identify the impact of various factors related to rationalizing the branch network– Strategic Objectives– Market Demographics– Branch Performance Metrics

• Determine the best-fit, future state strategy for each branch location– Traditional Branch– Social/Service Branch– No Branch/Closure– Kiosk Branch

• Identify the ATM locations that are delivery positive Net Income– Maximize capital investment

decisions: infrastructure, lease, outsourcing, and surcharge-free strategies

• Identify functionality required that best meets the FI’s channel strategy goals per location– Image & Video/Audio

• Maximize ATM marketing benefits – Onscreen and physical

ATM/Self Service

• On Premise/Off Premise• Kiosk/Remote Teller

• Assess transactions and productivity and sales performance

• Assess technology, routing and tools/reporting

• Assess staffing/skills model • Evaluate emerging tech capabilities

(chat, text, video)

Contact• Contact Center• Automated Voice

Response• Video banking

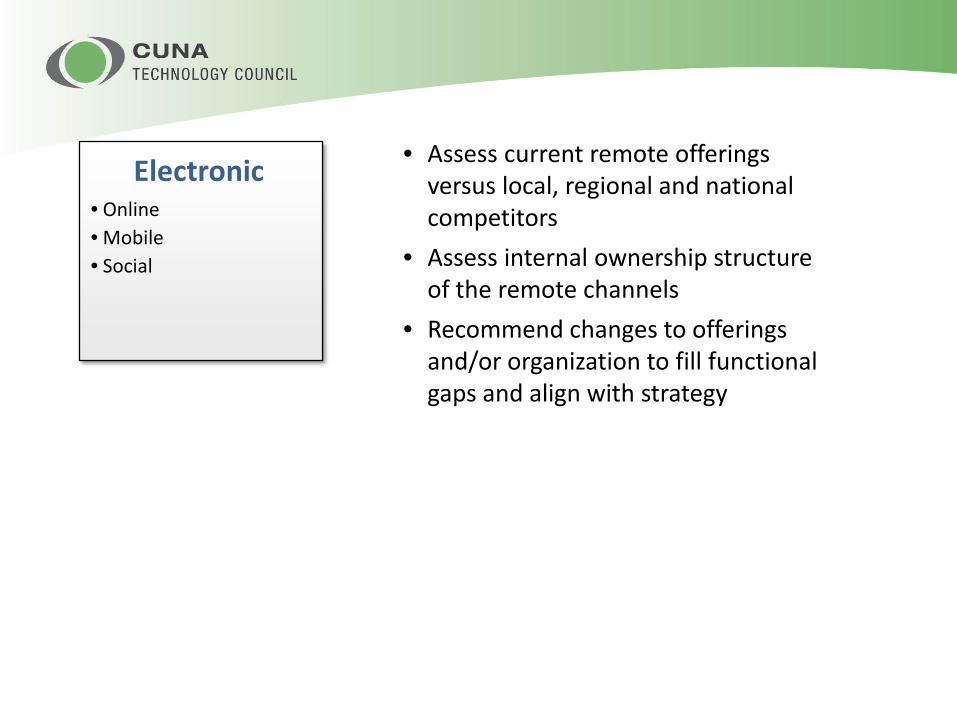

• Assess current remote offerings versus local, regional and national competitors

• Assess internal ownership structure of the remote channels

• Recommend changes to offerings and/or organization to fill functional gaps and align with strategy

Electronic• Online• Mobile• Social

Channel Performance• User Value – How much do customers value the channel?

– Your transaction data, channel usage metrics, and available survey metrics should help you answer this question

• Efficiency Value – How cost effective is the channel?– Compare your direct cost (staff, facility, other unallocated) to your

deposits as well as your direct cost to non-interest income plus funding credit

• Sales Value – How is the channel contributing to production?– Understand your open/close ratios, number of new accounts overall

and by type (e.g. checking), value of direct consumer/small business loan production as well as investment and mortgage referrals

In developing your action plans for each channel, keep the following in mind:

Branch ATM/Self Service Call Center Web Mobile

User Value

# of service transactions 275,000 345,000 43,000 281,000 34,567

% of transactions 27% 34% 4% 27% 3%

# of deposits 81,000 14,200 0 0 1,823

Sales Value

# of new deposit accounts 653 0 112 78 0

# of consumer loan applications 600 0 255 345 0

# of mortgage applications 70 0 24 145 0

# of investment referrals 56 0 14 9 0

Efficiency Value

Total Monthly Direct Cost

$2.6 million $695,000 $221,000 $127,000 $51,000

Direct Cost Per Transaction $9.45 $2.01 $5.13 $0.45 $0.78

The Delivery Channel Scorecard

Sample Application Assessment,Process Assessment, andCompetitive Analysis

Go Forth• Survey the organization regarding current channel volume/usage/ capabilities

• Utilize external research and internal user data to assess the market potential of all delivery channels

• Interview executive and delivery channel managers to understand the organization’s strategy and current channel priorities

• Complete a thorough benchmarking and assessment of delivery channel capabilities versus both peers and best practice leaders

• Facilitate a Channel Planning session with key stakeholders

• Develop a formal Delivery Channel Road Map

• Develop specific Action Plans around each component of the Delivery Channel Road Map

• Determine financial impact and develop a Delivery Channel Scorecard with performance goals and KPI’s to accompany the Delivery Channel Plan

American Banker calls GonzoBanker a “hip and flip” email newsletter.

Don’t miss out – sign up for your FREE subscription today at www.gonzobanker.com

A collection of observations, ruminations, predictions and random thoughts on financial services from the team at Cornerstone Advisors

GonzoBanker™ is a publication of Cornerstone Advisors, a Scottsdale, Arizona-based consulting firm specializing in best practices strategy, technology and process improvement

for banks and credit unions.

Visit our Web site at www.crnrstone.com

![Redirect Splash Page Redirect[1]](https://static.fdocuments.net/doc/165x107/54ff1faf4a7959592e8b5354/redirect-splash-page-redirect1.jpg)