SME access to finance schemes: measures to support small ...

MAYBANK’S SME FINANCING SCHEMES –OPPORTUNITIES FOR GREEN TECHNOLOGY SECTOR

KJ BalanHead, Business Development, SME BankingCommunity Financial Services

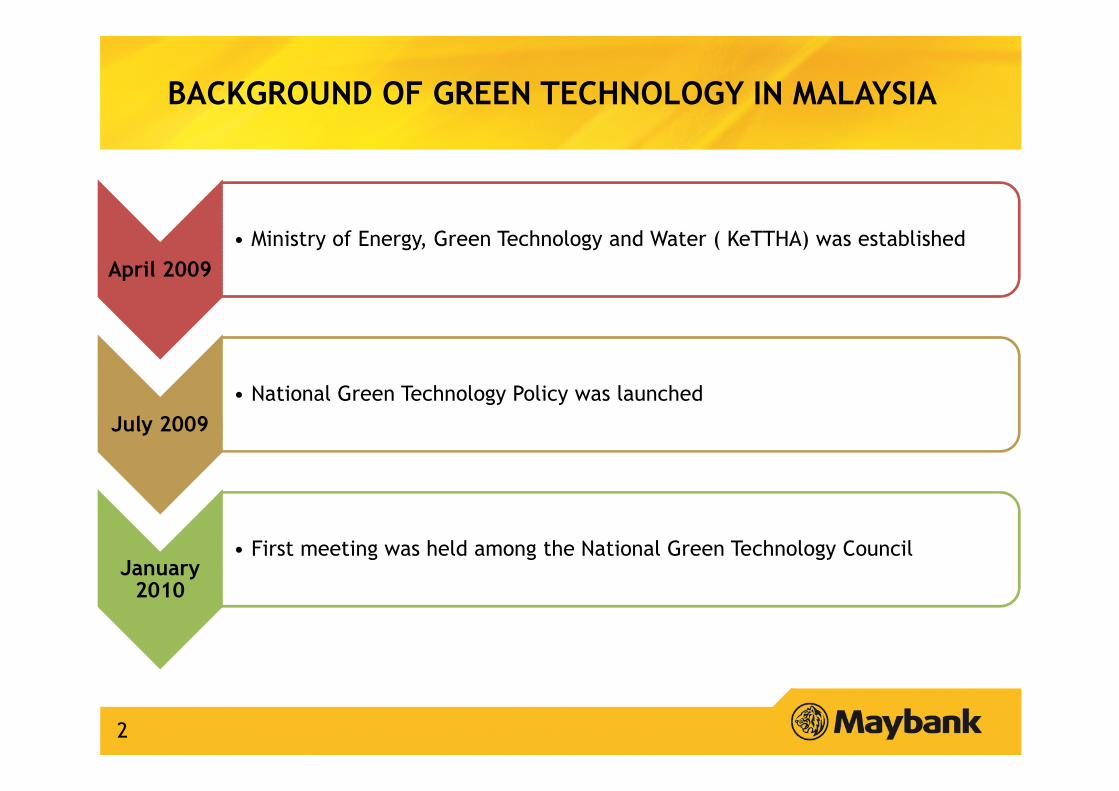

April 2009

• Ministry of Energy, Green Technology and Water ( KeTTHA) was established

July 2009

• National Green Technology Policy was launched

January 2010

• First meeting was held among the National Green Technology Council

BACKGROUND OF GREEN TECHNOLOGY IN MALAYSIA

2

NATIONAL GREEN TECHNOLOGY PILLARS

3

Seek to attain energy

independence and promote sufficient

Conserve and minimize the impact on the environment

Enhance the national economic

development through the

use of technology

Improve the quality of life

for all

ENERGY ENVIRONMENT ECONOMY SOCIAL

FUTURE OF GREEN TECHNOLOGY IN MALAYSIA

4

“I would also like to announce here in Copenhagen

that Malaysia is adopting an indicator of a

voluntary reduction of up to 40 % in terms of

emissions intensity of GDP by the year 2020

compared to 2005 levels. This indicator is

conditional on receiving the transfer of technology

and finance of adequate and correspond to what is

required in order to achieve this indicator”

Reference: YAB PM at COP15, Copenhagen on 17th December 2009

Policy Statement

Green Technology shall be a driver to

accelerate the national economy and

promote sustainable development.

Reference : National Green Technology Policy

PERSPECTIVE OF GREEN TECHNOLOGY

5

Source: Malaysia Green Technology Corporation

GREEN INVESTMENT OPPORTUNITIES

6

•Economic Transformation Programme (ETP) report in October 2010 aimed to achieved

real GDP growth of 6% per year for the next decade.

•FDI expected to pick up in the next 1-2 years and private investment growth including

green technology in 2011 may hits government forecast of 10.2%

•A minimum of 52,000 jobs are expected to be created to construct, operate and

maintain RE power plants by 2020.

Parameter 2020 2025

No. of Green Jobs 304,968 495,364

National GDP (RM million) 67,332 125,406.90

National GNI (RM million) 65,992.70 122,908.50

Source: Green Technology Roadmap Phase 1

Targeted National Outcomes

7

KEY AREAS (GTFS)

ENERGY SECTOR

BUILDINGS AND TOWNSHIP SECTOR

WATER AND WASTE MANAGEMENT SECTOR

TRANSPORTATION SECTOR

NO. CRITERIA

A TYPE OF ENERGY

Renewable: Hydro, Solar, Fuel Cell,Wind,Kenatic,Biomass and combustible waste.

ENERGY SUPPLY SECTOR:

SCOPE:

Application of Green Technology in power generation and in the energy supply side

management, including co-generation by the industrial and commercial sectors

B ENERGY UTILISATION SECTOR :

SCOPE:

Application of Green Technology in all energy utilisation sectors and in demand side

management programes.

CRITERIA FOR ENERGY SECTOR

8

NO. CRITERIA

A Energy Efficiency & Renewable Energy

B Indoor Environmental Quality

C Sustainable Site Planning & Management

D Materials & Resources

E Water Efficiency

F Innovation

CRITERIA FOR BUILDINGS AND TOWNSHIP SECTOR

9

NO. CRITERIA

A SCOPE:

Technology in the management and utilisation of water resources

TYPE OF WATER: Fresh water (tap or portable), water for industrial processes, agriculture and grey

water

B SCOPE:Waste water treatment, solid waste and sanitary landfill

TYPE OF WASTE: Garden waste, Industrial waste (i.e. spent bleaching earth, waste edible oil, POME),

Municipal waste (MSW), Agricultural waste, Organic waste, Sewage

CRITERIA FOR WATER AND WASTE MANAGEMENT SECTOR

10

NO. CRITERIA

SCOPE:

Incorporation of Green Technology in the transportation infrastructure, vehicles and

fuel, in particular, bio-fuel, electric vehicle and mass public transport system.

A INFRASTRUCTURE

Green infrastructure

B GREEN FUEL

Green fuel production

C VEHICLE

Alternative Fuel and Electric Vehicle (i.e. taxi, bus, etc)

CRITERIA FOR TRANSPORTATION SECTOR

11

12

APPLICATION PROCEDURE

GTFS

APPLICATION

BUSINESS REVIEW BUSINESS REVIEW

PRESENTATION

TECHNICAL

EVALUATION

FINANCING

APPLICATION

GUARANTEE

APPROVAL

GTFS APPLICATION

13

Online via www.gfts.mywebsite

Supporting Document

( mail/hand)

GreenTech Malaysia’s office

GreenTech will give

notification

whether

accepted or rejected

BUSINESS REVIEW PRESENTATION

14

Passed ���� screening process

Present project business

( 30 minutes )

Only applicant that deemed commercial viable will be further

process

TECHNICAL EVALUATION

15

Application will be evaluated

Additional information must be provided

(data/drawing/report)

– technical evaluation purpose

Technical Evaluation team will submit and present the GTFS project to the GTFS Technical

Committee (GTC) for their consideration and approval

All applicants will be officially notified on

their

approval status

Green Project Financing Recommendation Certificate

will be issued

(valid for six (6) months from the issuance date)

FINANCING APPLICATION

16

Successful applicants will apply for

financing at any financial institutions

( FIs ) of their choice.

Loan application will be evaluated by FIs

Letter of Offer will be issued

17

GREEN TECHNOLOGY FINANCING SCHEME (GTFS)

Has zero or low green house gas (GHG) emission

Minimises the degradation of the

environment

Safe for use and promotes healthy

and improved environment for all

forms of life

Promotes the use of renewable

resources

Conserves the use of energy and

natural resources

18

PRODUCT FEATURES ( GTFS)

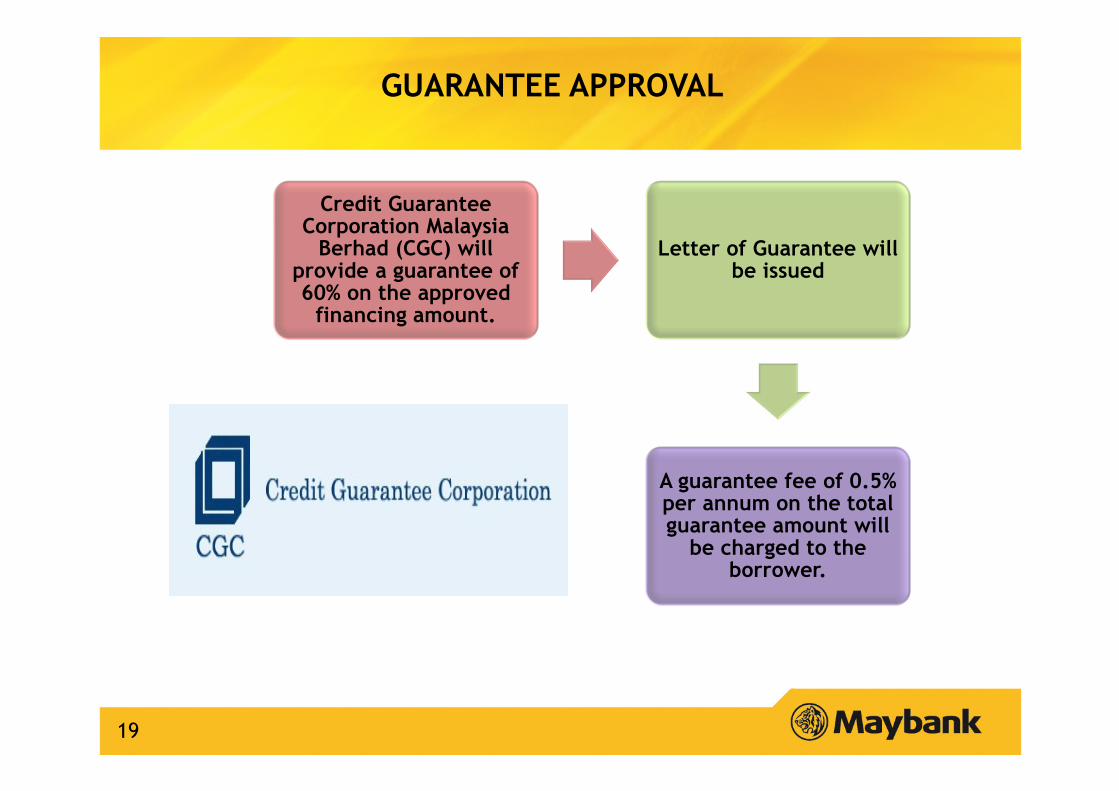

GUARANTEE APPROVAL

19

Credit Guarantee Corporation Malaysia

Berhad (CGC) will provide a guarantee of 60% on the approved

financing amount.

Letter of Guarantee will be issued

A guarantee fee of 0.5% per annum on the total guarantee amount will

be charged to the borrower.

BNM DEFINITION ON SME

20

Sector

Size

Primary Agriculture

Manufacturing (including agro-based) & MRS

Services Sector (Including ICT)

Micro <RM200k <RM250k <RM200k

Small RM200k – RM1 mill RM250k – RM10 mill RM200k – RM1 mill

Medium RM1 mill – RM5 millRM 10 mill – RM 25

mill

RM 1 mill – RM 5

mill

Sector

Size

Primary Agriculture

Manufacturing

(including agro-based) &

MRS

Services Sector

(Including ICT)

Micro < 5 < 5 < 5

Small 5 - 19 5 - 50 5 - 19

Medium 20 - 50 51 - 150 20 - 50

TURNOVER

NUMBER OF EMPLOYEES

NEW SME DEVELOPMENT FRAMEWORK

21

Source: SME Corporation Malaysia

VISION

GOALS

FOCUS AREAS

SUPPORTINSTITUTIONAL

SUPPORT

Creation of globally competitive SME’s across

contribute to the social well being of the nation

Creation of globally competitive SME’s across all sectors that enhance wealth creation and

contribute to the social well-being of the nation

Increase BusinessInformation

Expand Number of High Growth & Innovative

Firms

Raise ProductivityIntensify

Formalisation

Human Capital Development

Innovation & Technology Adaption

Access to Financing

Market AccessLegal & Regulatory

Environment Infrastructure

ACTION PLAN

Reliable Database

Monitoring & Evaluation

Effective Coordination

Effective Business Services

22

Source: SME Census 2011, Department of Statistics, Malaysia (DOSM)

DISTRIBUTION(%) OF SME’s BY SIZE & LEGAL STATUS

SME’s ESTABLISHMENT BY SECTOR

23

Sector Total Establishments

(a)

Total SMEs (b) Percentage (%) of SMEs over Total Establishments (b) / (a) *100

Overall Total 662,939 645,136 97.3

Services 591,883 580,985 98.1

Manufacturing 39,669 37,861 95.4

Agriculture 8,829 6,708 76.0

Construction 22,140 19,283 87.1

Mining & Quarrying 418 299 71.5

Source: Economic Cencus 2011, Profile of Small & Medium Enterprise

FINANCIAL LANDSCAPE FOR SME’s

24

FINANCIAL LANDSCAPE FOR SME’s

BANKING INSTITUTIONS

DEVELOPMENTFINANCIAL

INSTITUTIONS

BNM Special Funds

and Guarantee

Schemes

Credit Guarantee

Schemes

Government Crisis

Funds

Credit Bureau

Malaysia

Government Funds

& Schemes

Venture Capital

Companies

Leasing &

Factoring

Ar-Rahnu & Pawn

Booking

Microfinance

Institution

Source: SME Annual Report 2011/12

SOURCE OF FINANCING OF SMEs

25

Source: Economic Cencus 2011, Profile of Small & Medium Enterprise

FINANCING OUTSTANDING AS AT END – JUNE 2012

26

Source: SME Annual Report 2011/12

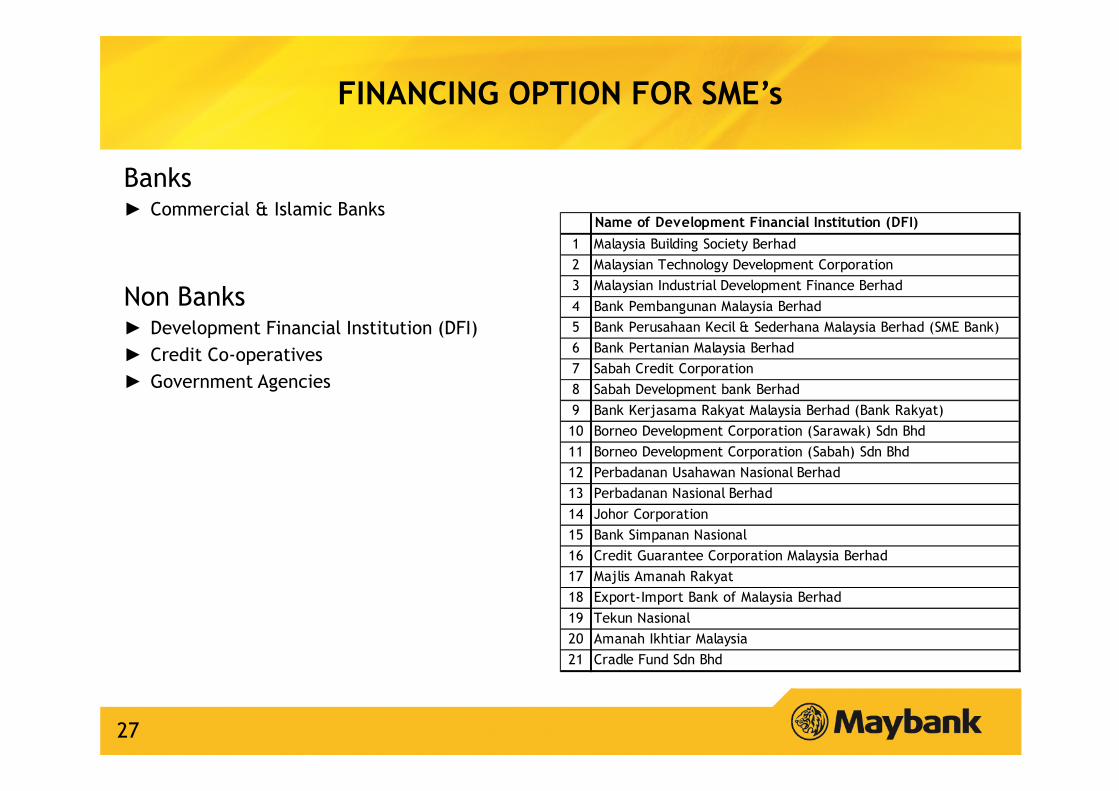

Banks► Commercial & Islamic Banks

Non Banks► Development Financial Institution (DFI)

► Credit Co-operatives

► Government Agencies

FINANCING OPTION FOR SME’s

27

Name of Development Financial Institution (DFI)

1 Malaysia Building Society Berhad

2 Malaysian Technology Development Corporation

3 Malaysian Industrial Development Finance Berhad

4 Bank Pembangunan Malaysia Berhad

5 Bank Perusahaan Kecil & Sederhana Malaysia Berhad (SME Bank)

6 Bank Pertanian Malaysia Berhad

7 Sabah Credit Corporation

8 Sabah Development bank Berhad

9 Bank Kerjasama Rakyat Malaysia Berhad (Bank Rakyat)

10 Borneo Development Corporation (Sarawak) Sdn Bhd

11 Borneo Development Corporation (Sabah) Sdn Bhd

12 Perbadanan Usahawan Nasional Berhad

13 Perbadanan Nasional Berhad

14 Johor Corporation

15 Bank Simpanan Nasional

16 Credit Guarantee Corporation Malaysia Berhad

17 Majlis Amanah Rakyat

18 Export-Import Bank of Malaysia Berhad

19 Tekun Nasional

20 Amanah Ikhtiar Malaysia

21 Cradle Fund Sdn Bhd

BANKING & FINANCIAL INSTITUTION

28

Which banks provide conventional loans and Islamic financing?

Bank Conventional Islamic

1 Affin Bank Berhad ✔ ✔2 Al Rajhi Banking & Investment Corporation (Malaysia) Berhad ✔3 Alliance Bank Malaysia Berhad ✔ ✔4 AmBank (M) Berhad ✔ ✔5 Asian Finance Bank Berhad ✔6 Bank Islam Malaysia Berhad ✔7 Bank Muamalat Malaysia Berhad ✔8 Bangkok Bank Berhad ✔9 Bank of America Malaysia Berhad ✔10 Bank of China (Malaysia) Berhad ✔11 Bank of Tokyo-Mitsubishi UFJ (Malaysia) Berhad ✔12 BNP Paribas Malaysia Berhad ✔13 CIMB Bank Berhad ✔ ✔14 Citibank Berhad ✔15 Deutsche Bank (Malaysia) Berhad ✔16 Hong Leong Bank Berhad ✔ ✔17 HSBC Bank Malaysia Berhad ✔ ✔18 Industrial and Commercial Bank of China (Malaysia) Berhad ✔19 JP Morgan Chase Bank Berhad ✔20 Kuwait Finance House (Malaysia) Berhad ✔21 Malayan Banking Berhad (Maybank) ✔ ✔22 Mizuho Corporate Bank (Malaysia) Berhad ✔23 National Bank of Abu Dhabi Malaysia Berhad ✔24 OCBC Bank (Malaysia) ✔ ✔25 Public Bank Berhad ✔ ✔26 RHB Bank Berhad ✔ ✔27 Standard Chartered Bank Malaysia Berhad ✔ ✔28 Sumitomo Mitsui Banking Corporation Malaysian Berhad ✔29 The Bank of Nova Scotia Berhad ✔30 The Royal Bank of Scotland Berhad ✔31 United Overseas Bank (Malaysia) Bhd ✔

CREDIT EVALUATION FRAMEWORK

29

DOCUMENTS TO BE COLLECTED FROM CUSTOMERS EVALUATION PURPOSE

1. Form 24 & Form 49 (for Sdn Bhd) or Business

Registration/Business License (for SPP) 1. Experiences

2. Genuineness of a business2. Memorandum & Article of Association and Certification of

Incorporation (for Sdn Bhd only)

3. Latest two (2) years Financial Statements 1. Financial track record

2. Feasibility & resilience4. Latest six (6) months Bank Statements

5. NRIC of Directors/ Shareholders/ Partners/ Proprietor/

Guarantors (where applicable) 1. Conduct of account

2. Credit behaviour

6. Duly signed Credit Bureau Malaysia Consent Form*

7. Other collateral information (where applicable) 1. Commitment & support

2. Economic condition & viability8. Other income information (where applicable)

30

THANK YOU