May-June 2002 Investor Roadshow - CommBank · 2019-08-19 · May-June 2002 Investor Roadshow David...

36

May-June 2002 Investor Roadshow David Murray Chief Executive Officer Stuart Grimshaw Group Executive Financial and Risk Management www.commbank.com.au

Transcript of May-June 2002 Investor Roadshow - CommBank · 2019-08-19 · May-June 2002 Investor Roadshow David...

May-June 2002 Investor Roadshow

David Murray

Chief Executive Officer

Stuart Grimshaw

Group Executive Financial and Risk Management

www.commbank.com.au

2

The material that follows is a presentation of general

background information about the Bank‟s activities

current at the date of the presentations, 27 May 2002.

It is information given in summary form and does not

purport to be complete. It is not intended to be relied

upon as advice to investors or potential investors and

does not take into account the investment objectives,

financial situation or needs of any particular investor.

These should be considered, with or without

professional advice when deciding if an investment is

appropriate.

Disclaimer

3

Speaker’s Notes

Speaker‟s notes for these presentations

are attached below each slide.

To access them, you may need to save

the slides in PowerPoint and view/print

in “notes view.”

4

Agenda

Introduction

Australian economy

Australian share market

History of Commonwealth Bank

Financial performance

Strategy

Strategic issues

Competitive advantage

Strategic imperatives

Looking Forward

Strategic plan

Introduction

Australian Economy & Share Market

Relative GDP performance

Credit growth

MSCI index weighting

7

Relative GDP Performance

Source: Goldman Sachs

GDP Growth

-3.00

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

% G

row

th G

DP

yo

y

US UK Japan Australia

8

Credit Growth

Source: Commonwealth Research

Mar-02

G r o w t h in O u t s t a n d in g s

( 3 m o n t h - e n d e d a n n u a l r a t e s )

- 1 0

0

1 0

2 0

3 0

J u l- 9 7 J u l- 9 8 J u l- 9 9 J u l- 0 0 J u l- 0 1

- 1 0

0

1 0

2 0

3 0

B u s in e s s H o u s e h o ld

H o u s in g O t h e r p e r s o n a l

% %

9

0

10

20

30

40

50

60

USA UK

Japan

Fra

nce

Germ

any

Sw

itzerland

Neth

erlands

Canada

Italy

Australia

Spain

Sw

eden

Fin

aln

d

Hong K

ong

Beguim

Sin

gapore

Denm

ark

Irela

nd

Norw

ay

Portugal

Gre

ece

Austria

New

Zeala

nd

MSCI % Weightings

1.58%

Recent increase in relative weighting

to 10th from 14th on MSCI Index

Source: Australian Stock Exchange

Commonwealth Bank Group

10 Year Share Price Performance

Full Year to 30 June 2001

Half Year to 31 December 2001

Asset Quality

11

$0

$5

$10

$15

$20

$25

$30

$35

$40

9/09

/91

9/06

/92

9/03

/93

9/12

/93

9/09

/94

9/06

/95

9/03

/96

9/12

/96

9/09

/97

9/06

/98

9/03

/99

9/12

/99

9/09

/00

9/06

/01

9/03

/02

December 1990 - the Bank

was converted into a public

company with share capital.

70% shareholding retained by

the Commonwealth

Government.

1991 - The Bank acquired

State Bank of Victoria $1.6

billion.

October 1993 - the

Commonwealth Government

shareholding was reduced to

50.4% and in 1996 the Bank

was fully privatised.

June 2000 - the Bank

acquired Colonial Group

Limited $10 billion.

Commonwealth Bank Group Share Price

Performance Last 10 Years

December 2001 - the Bank‟s

restructure announced.

12

Financial Performance :

Full Year to 30 June 2001

Net operating profit after tax up 9% to $2,262m („cash basis‟*)

- Banking up 12% to $1,793m

- Strong performance from Funds Management, up 34% to $149m

- Weaker life insurance operating margins & investment earnings

below long term expectations

Retail Integration completed ahead of time & to business case

Home lending market share beginning to stabilise

Operating expenses increased above expectations

*before goodwill amortisation and appraisal value uplift

13

Financial Performance :

Half Year to 31 December 2001

Net operating profit after tax up 7% to $1,192m („cash basis‟*)

Banking result up 11% driven by a steady net interest margin

and growth in other banking income

Funds under management result up 23% with strong momentum

in funds inflow maintained through September 11

Australian life insurance operating margin up 22% offset by a weak

offshore life insurance result

Increase in bad and doubtful debt expense, driven by two large

impaired corporate exposures

*before goodwill amortisation and appraisal value uplift

14

Credit Risk: Historical P&L Charge

* Excludes Colonial

% C

harg

e P

er

Half

Bad Debt Expense / RWA

0.00%

0.10%

0.20%

0.30%

Sep-98*

Dec-98*

Mar

-99*

Jun-

99*

Sep-99

Dec-99

Mar

-00

Jun-

00

Sep-00

Dec-00

Mar

-01

Jun-

01

Sep-01

Dec-01

Mar

-02

CBA Other Major Australian Banks (Average)

15

Aggregate Provisions

* Includes Colonial

$m

illio

ns

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

50

100

150

200

250

300

%

General Provision (Left Axis)

Specific Provision (Left Axis)

Other Major Australian Banks (Average): Total Provisions/Gross Impaired Assets (%)

CBA: Total Provisions/Gross Impaired Assets (%)

Strategy

Strategic Issues

Competitive Advantage

Strategic Imperatives

Strategic Issues

Domestic Growth

Wealth Management

Distribution

Technology & Productivity

Competitive Advantage

Brand

Scale

Innovation

19

Brand : Commonwealth Bank

Share of Mind*

• CBA’s share of mind remains at a consistent level, leading the Big Four.

• Share of mind for Westpac, ANZ and NAB continue to measure at similar

levels.

* Research International November 2001

68 71 6863

7065 63 66 65 64

68 6965 63 66

0

25

50

75

Sept Nov Jan

'01

Mar May Jul Sep Nov

(%)

CBA

Westpac

ANZ

NAB

20

Rank Company

1

2

3

4

5

Source: ASSIRT Service Level Survey - 2001

Adviser brand awareness - overall opinion of organisation

Brand : Colonial First State

7.28

7.52

7.81

7.85

7.98

8.16

5 6 7 8 9 10

Industry

Average

AMP

AMP Financial

Services

Perpetual

Navigator

Colonial First

State

21

Brand: CommSec

22

Australia’s Most Accessible Bank

10 million customers

$

Personal

Lenders

over 700

staff

Direct

Banking

over 62 million

calls *

Branches

1,045

branches

ATMs

nearly

4,000

Premium

Banking

13 Centres

Ezy Banking

over 700 Stores

NetBank

1.5 million

registered

customers

Business Banking

80 centres

Agencies

(Postal &

Private)

over 3,900

Mobile

Bankers

over 180

Statistics as at 31 December 2001

* for 6 months to Dec „01

EFTPOS

over 120,000

merchant

terminals

Financial

Planners

over 620

Third Party Distribution

over 15,000 individual

advisers, brokers and

agents

23

Scale : Low Cost per Customer

Non Interest Expense / Customer

Source: Commonwealth Bank illustration

Revenue per Customer

0

CBA

Increasing

Incre

asin

gpeer banks

24

Dec 2000 Jun 2001 Dec 2001

Home Loans 20.8% 20.4% 20.1%

(Residentially Secured)

Credit Cards^ 21.9% 21.4% 21.4%

Retail Deposits 24.6% 24.0% 24.1%

Retail FUM (Plan for Life) 16.0% 16.5% 16.8%

Superannuation/Annuities 15.7% 15.8% 16.4%

Retail Broking 8.5% 8.7% 8.5%

Inforce Premiums 14.6% 14.4% 14.6%

^ Colonial data captured as part of market share calculation from June 2001

Australian Market Share

Scale : Strong Market Share Positioning

Rank

1

1

1

1

1

2

2

25

Market Share of ASX Transactions

0

5,000

10,000

15,000

20,000

($ 000)

1997 1998 1999 2000 2001

Profitability of CommSec

Innovation : Commsec & NetBank

0 %

2 %

4 %

6 %

8 %

1 0 %

1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 0 2 0 0 1

0

300

600

900

1200

(000

's)

1997 1998 1999 2000 2001

Growth in Customer Numbers

0

40

80

120

160

mil

lio

ns

of

tra

ns

ac

tio

n

1997 1998 1999 2000 2001

Growth in Transaction Volumes

26

Innovation : e-Commerce footprint

NetBank CommSec (discount broking)

Online Home Loan Application BPay Online

Commonwealth Bank Web Site

Funds Direct

> 170,000 Online CustomersVodafone alliance

HomePath

Dec 95

Feb-Mar 97

Sep-Nov 97

Aug 98

Jun 99

Aug-Sep99

Sep 01

Dec 01

> 2,300,000 Online Customers

1,500,000 NetBank Customers

Strategic Imperatives

Segmentation

Productivity

Strategic Issues

Domestic Growth

Wealth Management

Distribution

Technology & Productivity

28

Segmentation: Aligned Domestic

Structure with Customer Needs

Retail BankingServices

PremiumFinancialServices

Investment &InsuranceServices

Institutional &BusinessServices

CustomerGroup

Personalbankingcustomers,Small businessbankingcustomers

Premium clientsincludingprofessionalsand business

Agents, Brokers,Financial Advisers

Institutional,Corporate,Commercialbusinesscustomers

Channels Branch, Ezy-Banking, ATM,EFTPOS,Phone, On-line,Mortgagebrokers

Relationshipmanagers,Premiuminvestmentcentres, phone,on-line.

Agents, Branches,Brokers, FinancialAdvisers, Premiuminvestment centresDirectDealerships

Relationshipmanagers,Business centres

Services Group Technology, Back Office Operations, Procurement, Shared Services

Support Finance, Risk Management, Human Resources, Strategy, Legal, Secretariat

29

Retail Share of Wallet and Cost to Serve

Source : Commonwealth Bank of Australia ^ Excludes Finance Companies

Banking

0

10

20

30

40

50

60

70

80

90

100

Total Complex

Needs

Mainstream

/Transactors

Youth

%

CBA WBC ^ NAB ANZ ^

Investment

0

10

20

30

40

50

60

70

80

90

100

Total Complex

Needs

Mainstream

/Transactors

Youth

%

CBA WBC ^ NAB ANZ ^

CBA Personal Customers :

Segment share

6%

34%

31%

29%

Complex Needs Mainstream Transactors Youth

Overall

0

10

20

30

40

50

60

70

80

90

100

Total Complex

Needs

Mainstream

/Transactors

Youth

%

CBA WBC ^ NAB ANZ ^

30

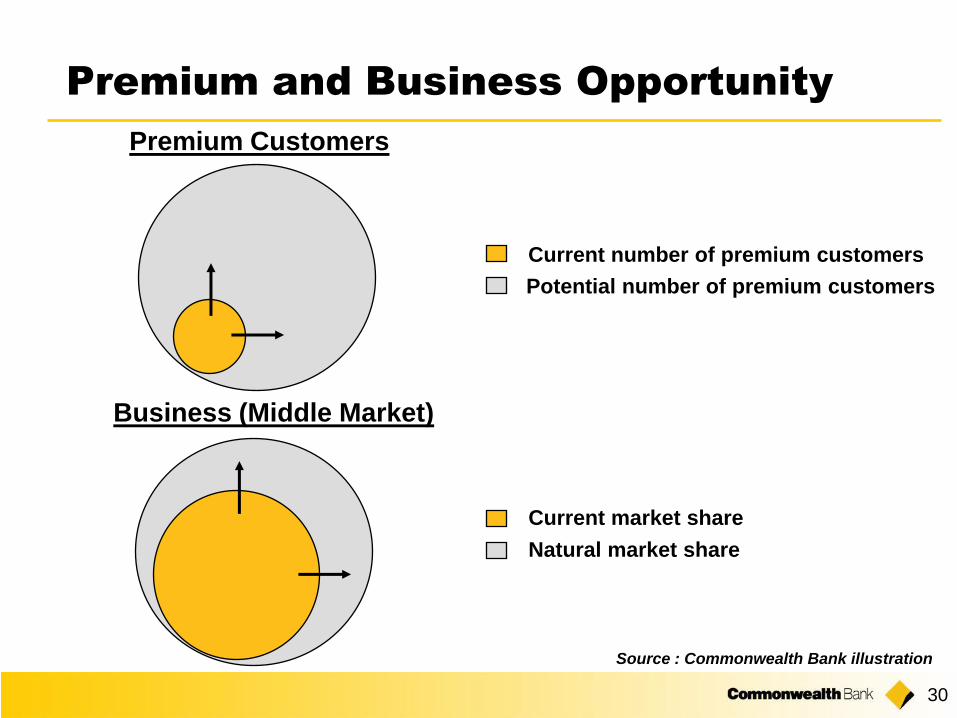

Premium and Business Opportunity

Business (Middle Market)

Premium Customers

Source : Commonwealth Bank illustration

Current market share

Natural market share

Current number of premium customers

Potential number of premium customers

31

Funds Management Opportunity

Source: Plan for Life, CBA

Retail Funds Management

(Non-Life & Life)

0

100

200

300

400

500

600

1997 1999 2001 2003 2005 2007

$B

illio

n

Retail FUM (Commonwealth Bank Group)

Retail FUM (Industry)

32

Growth through Retail Masterfunds

33

Segmentation : premium banking

Simplified transaction accounts

Browser based workflow enabled systems

Credit risk architecture

7 level organisation structure

Shared services : HR and finance

Productivity

Looking Forward

35

Business Driver Profile 5 Year Plan

Growth in Market Share

Funds under managementHome LoansCredit CardsLife InsuranceCredit ProductsBusiness FinancingRetail Deposits

At or above market

Margins Comparable for business mix Continuing decline

Sources of Income Comparable Financial Institutions Rebalance toward non-interest income

Costs Reduction in cost/income – Bestpractice

3%-6% p.a. productivitychange

Capital ManagementOptimise regulatory capital andmaintain rating.

Rating AA-

Total Shareholder Return Top quartile Deliver top quartile TSR.

Strategic Plan to June 2006 is

Underpinned by Growth Assumptions

May-June 2002 Investor Roadshow

David Murray

Chief Executive Officer

Stuart Grimshaw

Group Executive Financial and Risk Management

www.commbank.com.au