Matt Manson - s2.q4cdn.coms2.q4cdn.com/850616047/files/doc_presentations/2015/SWY-Quebec...Matt...

26

A Case Study of the 2014 Financing of the Renard Project: C$1B for Québec’s First Diamond Mine Québec Mines, Québec, 26 th November, 2015 Matt Manson President, CEO & Director

Transcript of Matt Manson - s2.q4cdn.coms2.q4cdn.com/850616047/files/doc_presentations/2015/SWY-Quebec...Matt...

A Case Study of the 2014 Financing of the RenardProject: C$1B for Québec’s First Diamond MineQuébec Mines, Québec, 26th November, 2015

Matt MansonPresident, CEO & Director

2

Forward-Looking Information

This presentation contains "forward-looking information" within the meaning of Canadian securities legislation. This information and these statements, referred to herein as“forward-looking statements”, are made as of the date of this presentation and the Corporation does not intend, and does not assume any obligation, to update these forward-looking statements, except as required by law. These forward-looking statements include, among others, statements with respect to our beliefs, plans, objectives, expectations,anticipations, estimates and intentions. Although management considers these assumptions to be reasonable based on information currently available to it, they may prove tobe incorrect.

Forward-looking statements relate to future events or future performance and reflect current expectations or beliefs regarding future events and include, but are not limited to,statements with respect to: (i) the amount of Mineral Resources and exploration targets; (ii) the amount of future production over any period; (iii) net present value and internalrates of return of the mining operation; (iv) assumptions relating to recovered grade, average ore recovery, internal dilution, mining dilution and other mining parameters set outin the 2011 Feasibility Study or the Optimization Study; (v) assumptions relating to gross revenues, operating cash flow and other revenue metrics set out in the 2011Feasibility Study or the Optimization Study; (vi) mine expansion potential and expected mine life; (vii) expected time frames for completion of permitting and regulatoryapprovals related to construction activities at the Renard Diamond Project; (viii) the expected time frames for the completion of the open pit and underground mine at theRenard Diamond Project; (ix) the expected time frames for the completion of construction, start of mining and commercial production at the Renard Diamond Project and thefinancial obligations or costs incurred by Stornoway in connection with such mine development; (x) future exploration plans; (xi) future market prices for rough diamonds; (xii)the economic benefits of using liquefied natural gas rather than diesel for power generation; (xiii) sources of and anticipated financing requirements; (xiv) the effectiveness,funding or availability, as the case may require, of the Stream, the Senior Secured Loan, the COF and the Equipment Facility and the use of proceeds therefrom; (xv) theCorporation’s expectations regarding receipt of the remaining deposits under the Stream and its ability to meet its delivery obligations thereunder; (xvi) the impact of theFinancing Transactions on the Corporation’s operations, infrastructure, opportunities, financial condition, access to capital and overall strategy; (xvii) the foreign exchange ratebetween the US dollar and the Canadian dollar; and (xviii) the availability of excess funding for the construction and operation of the Renard Diamond Project. Any statementsthat express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but notalways, using words or phrases such as “expects”, “anticipates”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “schedule” or variationsthereof or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similarexpressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are made based upon certain assumptions by Stornoway or its consultants and other important factors that, if untrue, could cause the actualresults, performances or achievements of Stornoway to be materially different from future results, performances or achievements expressed or implied by such statements.Such statements and information are based on numerous assumptions regarding present and future business prospects and strategies and the environment in whichStornoway will operate in the future, including the price of diamonds, anticipated costs and Stornoway’s ability to achieve its goals, anticipated financial performance, regulatorydevelopments, development plans, exploration, development and mining activities and commitments, and the foreign exchange rate between the US and Canadian dollars.Although management considers its assumptions on such matters to be reasonable based on information currently available to it, they may prove to be incorrect. Certainimportant assumptions by Stornoway or its consultants in making forward-looking statements include, but are not limited to: (i) required capital investment and estimatedworkforce requirements; (ii) estimates of net present value and internal rates of return; (iii) anticipated timelines for completion of construction, commencement of mineproduction and development of an open pit and underground mine at the Renard Diamond Project, which heavily depend, among other things, on adequate availability andperformance of skilled labour, engineering and construction personnel, performance of mining and construction equipment and timely delivery of components; (iv) anticipatedgeological formations; (v) market prices for rough diamonds and the potential impact on the Renard Diamond Project; (vi) the satisfaction or waiver of all conditions under eachof the Stream, the Senior Secured Loan, the COF and the Equipment Facility to allow the Corporation to draw on the funding available under those financing elements for thecompletion of the development and construction of the Renard Diamond Project; (vii) Stornoway’s interpretation of the geological drill data collected and its potential impact onstated Mineral Resources and mine life; (viii) future exploration plans and objectives; (ix) the receipt of the remaining deposits under the Stream and the Corporation’s ability tomeet its delivery obligations thereunder; and (x) the continued strength of the US dollar against the Canadian dollar. Additional risks are described in Stornoway's most recentlyfiled Annual Information Form, annual and interim MD&A, and other disclosure documents available under the Corporation’s profile at: www.sedar.com.

3

Forward-Looking Information (contd)

The RenardDiamond Project, September 16, 2015

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that estimates, forecasts, projections andother forward-looking statements will not be achieved or that assumptions do not reflect future experience. We caution readers not to place undue reliance on these forward-looking statements as a number of important risk factors could cause the actual outcomes to differ materially from the beliefs, plans, objectives, expectations, anticipations,estimates, assumptions and intentions expressed in such forward-looking statements. These risk factors may be generally stated as the risk that the assumptions andestimates expressed above do not occur, including the assumption in many forward-looking statements that other forward-looking statements will be correct. Stornowayinvites the reader to take note of the risk and uncertainties set out in the most recently filed Annual Information Form, annual and interim MD&A and other disclosuredocuments available under the Corporation’s profile at: www.sedar.com and cautions the reader that the list of risk and uncertainties set out in these disclosure documents ofthe Corporation and that may affect future results is not exhaustive, and new, unforeseeable risks may arise from time to time.

Readers are also referred to the technical reports dated as of February 28th, 2013 entitled “The Renard Diamond Project, Québec, Canada, Feasibility Study Update, NI 43-101 Technical Report, February 28, 2013” in respect of the January 2013 Optimization Study, and dated October 14, 2015 entitled “2015 Mineral Resource Update, for theRenard Diamond Project, Québec, Canada, NI 43-101 Technical Report”. Disclosure of a scientific or technical nature in this presentation was prepared under the supervisionof Patrick Godin, P. Eng (Québec), Chief Operating Officer and Robin Hopkins, P. Geol. (NT/NU), Vice President, Exploration, both “qualified persons” under NationalInstrument (NI) 43-101 - Standards of Disclosure for Mineral Projects. Ms. Darrell Farrow, PrSciNat, P. Geo. (BC), Ordre des géologue du Québec (Special Authorization #332) of Geostrat Consulting Services Inc. is the independent qualified person responsible for preparation of the mineral resource estimate for the Renard Diamond Project.

44

History of the Renard Project

5The Renard Diamond ProjectQuébec’s First Diamond Mine

Chibougamau

Montréal

Toronto

800km

360km

Renard

1996: Start of initial regional exploration by Ashton & SOQUEM

2001: First kimberlite discovery

2001-08: Drilling, “mini-bulk” sampling, bulk sampling

2008-10: First NI 43-101 Resource and PEA

November 2011: Feasibility Study issued. First mineral reserve

December 2012: ESIA filed

February 2012: Road construction commences under Plan Nord

March 2012: “Mecheshoo Agreement” executed

Nov.-Dec.2012: Mining Lease and Québec Authorizations issued

January 2013: Optimization Study issued

July 2013: Federal Canadian Authorizations Issued

September 2013: Road opens

April-July 2014: $C946m financing completed. Construction commences

2Q 2017: Scheduled Commercial Production

2001: First Kimberlite Discovery

+7-9 Years: First NI 43-101 Resource and PEA

+12 Years: Final Authorisations Issued

+16 Years: Commercial Production

+13 Years: Project Financing

800m

900m

1100m

1200m

1000m

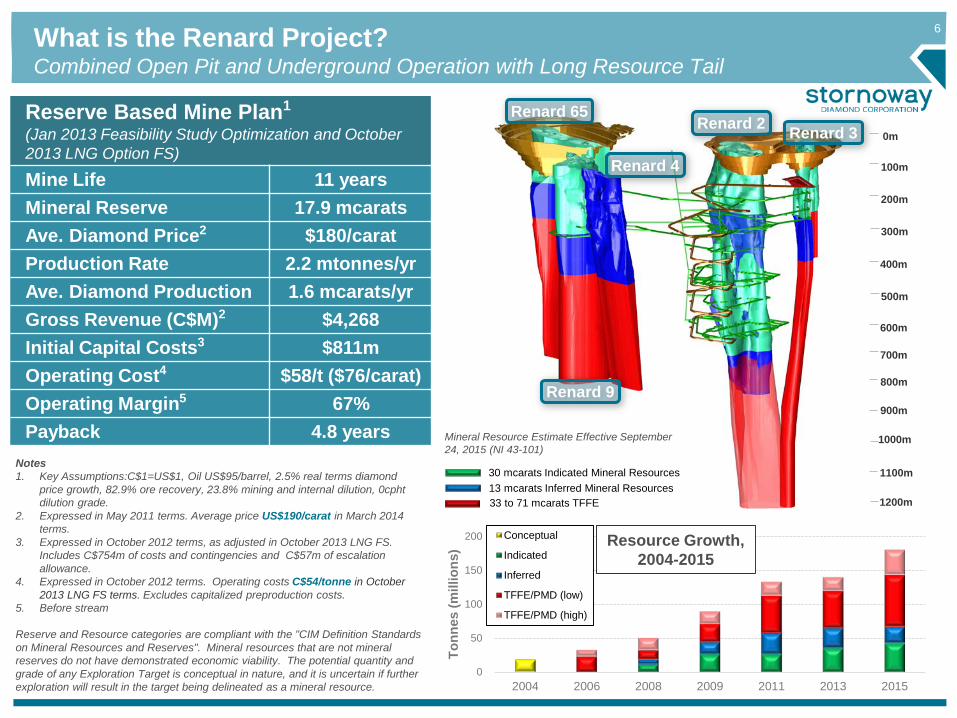

What is the Renard Project?Combined Open Pit and Underground Operation with Long Resource Tail

Notes1. Key Assumptions:C$1=US$1, Oil US$95/barrel, 2.5% real terms diamond

price growth, 82.9% ore recovery, 23.8% mining and internal dilution, 0cpht dilution grade.

2. Expressed in May 2011 terms. Average price US$190/carat in March 2014 terms.

3. Expressed in October 2012 terms, as adjusted in October 2013 LNG FS. Includes C$754m of costs and contingencies and C$57m of escalation allowance.

4. Expressed in October 2012 terms. Operating costs C$54/tonne in October 2013 LNG FS terms. Excludes capitalized preproduction costs.

5. Before stream

Reserve and Resource categories are compliant with the "CIM Definition Standards on Mineral Resources and Reserves". Mineral resources that are not mineral reserves do not have demonstrated economic viability. The potential quantity and grade of any Exploration Target is conceptual in nature, and it is uncertain if further exploration will result in the target being delineated as a mineral resource.

Reserve Based Mine Plan1

(Jan 2013 Feasibility Study Optimization and October 2013 LNG Option FS)

Mine Life 11 yearsMineral Reserve 17.9 mcaratsAve. Diamond Price2 $180/caratProduction Rate 2.2 mtonnes/yrAve. Diamond Production 1.6 mcarats/yrGross Revenue (C$M)2 $4,268Initial Capital Costs3 $811mOperating Cost4 $58/t ($76/carat)Operating Margin5 67%Payback 4.8 years

6

0m

100m

200m

400m

600m

700m

500m

300m

Renard 4

Renard 9

Renard 65Renard 2 Renard 3

Mineral Resource Estimate Effective September 24, 2015 (NI 43-101)

13 mcarats Inferred Mineral Resources33 to 71 mcarats TFFE

30 mcarats Indicated Mineral Resources

0

50

100

150

200

2004 2006 2008 2009 2011 2013 2015

Tonn

es (m

illio

ns)

Conceptual

Indicated

Inferred

TFFE/PMD (low)

TFFE/PMD (high)

Resource Growth, 2004-2015

77

Setting the Stage for Financing and Development: 2010-2013

8Setting the Stage for Financing and Development: 2010-2013Building a “Big Tent” and Building a Team

With the March 2010 Preliminary Economic Assessment it was clear that Renard was a viable mining project

Work began on preparing the project for development• May 2010: Patrick Godin joins as COO; building of the team• July 2010: start of C$28m FS (SNC Lavalin/AMEC)• Nov 2010: start of ESIA work (Roche)

July 2010: Pre-Development Agreement signed with the Grand Council of the Crees (Eeyou Istchee), the Cree Nation of Mistissiniand SOQUEM (via DIAQUEM INC)

Dec. 2010 to Apr. 2011: Stornoway acquires SOQUEM’s 50% project interest making Investissement Québec Stornoway’s largest shareholder

Dec. 2010 to Dec 2013: Pre-development Financings:• Dec 2010: $35m RBC bought deal • March 2012: $15m Scotia bought deal• May 2012: $20m Unsecured debt with the Fonds de solidarité

FTQ/Fonds Régional and Diaquem Inc.• Oct 2013: $20m bridge facility from IQ/RQ• Dec 2013: $10m Dundee bought deal of Flow Through

June 2012: SWY Head Office relocated from Vancouver to Longueuil

Head Office Opening in Longueuil

Developing Relationships

Site Visits

9

The Mecheshoo Agreement, March 2012

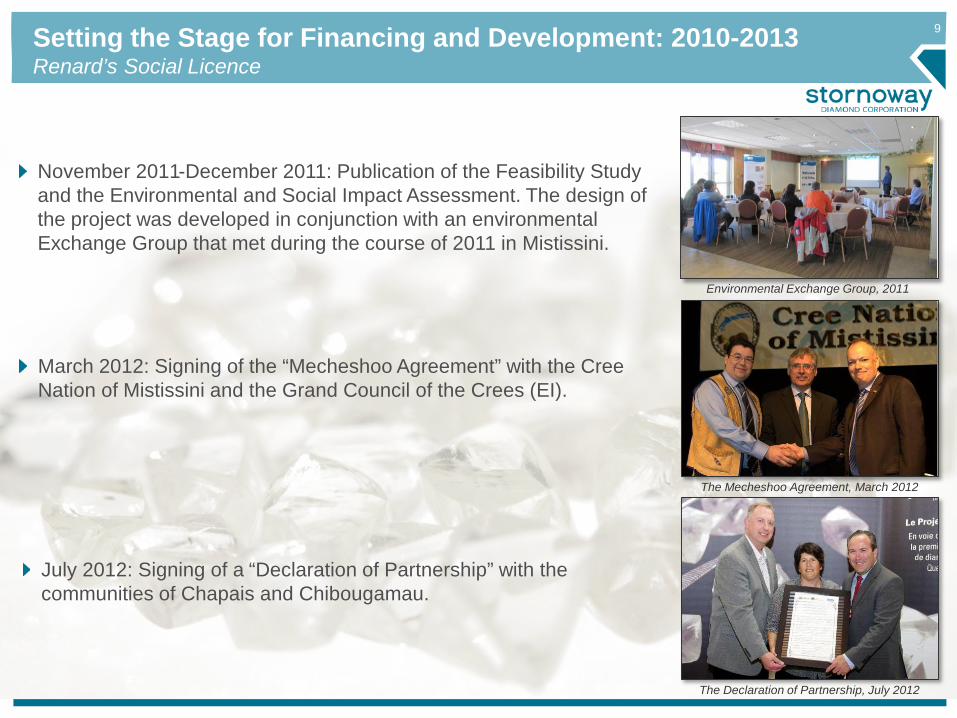

Setting the Stage for Financing and Development: 2010-2013 Renard’s Social Licence

The Declaration of Partnership, July 2012

Environmental Exchange Group, 2011

November 2011-December 2011: Publication of the Feasibility Study and the Environmental and Social Impact Assessment. The design of the project was developed in conjunction with an environmental Exchange Group that met during the course of 2011 in Mistissini.

July 2012: Signing of a “Declaration of Partnership” with the communities of Chapais and Chibougamau.

March 2012: Signing of the “Mecheshoo Agreement” with the Cree Nation of Mistissini and the Grand Council of the Crees (EI).

10Setting the Stage for Financing and Development: 2010-2013 Embracing the Plan Nord:The 240km long Route 167 Extension

Eastmain River Bridge

July 2014

Jan 2015

July 2014

In July 2011 Stornoway embraced the Plan Nord and signed a financing partnership agreement with Québec for the construction of the 240km Route 167 Extension.

In December 2011 Stornoway assumed the construction of the northern 97km of road under an $85m debt financing agreement with Finances Québec, repayable upon commercial production.

The road was open to the project by September 2013 for a cost to Stornoway of C$70m.

$7m of the remaining debt facility was used to construct the Renard airport.

Sept 2015

11Setting the Stage for Financing and Development: 2010-2013 Stornoway’s Strengths and Weaknesses going into Project Financing

Good asset with strong margins and long potential mine life

Location: Québec

Route 167 Extension under construction

Permitting going well

Good social license and partnerships

Strong, supportive lead shareholder (IQ/RQ)

Strengths

Bad equity market

Low market cap (C$100m-C$150m) in relation to Cap-ex (C$811m)

Diamonds: education required, no hedging possible, no terminal market

Renard’s resource tail: Substantial resource upside difficult to convert and difficult to underwrite.

Weaknesses

No precedent deals for a 100% owned greenfield diamond development project

financed in a bad market

10.15 carat gem quality octahedron

1212

Project Financing: December 2011 to July 2014

13

Financing Structure 1: Traditional Debt-Equity

Starting in November 2011, Stornoway commenced negotiations towards a traditional Senior Project Debt/Equity financing structure:• 50% Debt: Draft Term sheet negotiated for up to $475m syndicated facility with commercial lenders

Scotiabank, BMO, Soc-Gen, Nedbank, IQ, EDC, Caterpillar • 50% Equity: c.$475m equity to be raised in market. Scotiabank advising.• Cost Overrun Facility: >C$100m required by lenders, equity based, unconditional

Simultaneously, Stornoway pursued the de-risking of the project• Optimized Feasibility Study (Jan 2013)• FS for a powerline and then, subsequently, LNG power (October 2013)• EPCM negotiated with SNC-Lavalin and AMEC• Federal and Québec Certificates of Authorization• Road construction

Positives Negatives

• Strong Debt Appetite and Capacity • Traditional Equity Market closed to a 6x market cap financing

• P/E Equity available, but unrealistic buyer expectations

• Streams available, but without equity commitment only served

to cannibalize bank debt capacity

• Cost overrun facilities available, but not un-conditional and

hence unacceptable to commercial bank lenders

14

Interregnum: “Bulking Up” as a Project Finance Strategy

In December 2011, shortly after the release of the Renard FS, BHP Billiton announced its intention to sell the Ekati Diamond Mine in the NWT.

Between December 2011 and May 2012, Stornoway participated in the bidding, and arranged debt and equity financing components for a >C$500 million transaction.

Stornoway’s objective was to create a larger company, with cash flow and a stronger balance sheet, better able to project finance Renard.

BHP Billiton ultimately sold the Ekati mine to Dominion Diamond Corporation.

Stornoway’s demonstrated ability to finance a major asset acquisition against better established competitors raised the profile of the company. Stornoway’s failure to buy Ekati started the process that led to the successful financing of Renard.

15

Financing Structure 2: Hybrid Package

By the fall of 2013, Stornoway had determined a “Hybrid Package” of Debt-Equity-Stream could be successful with the following features: • Full package: “One-Shot” financing to fully fund project to completion, including all ancillary costs• All elements co-dependent: each participant gets to be “Last Money In”• Rates of return commensurate with risk across the separate equity, debt and stream pieces• Purchase of the stream was tied to underwriting other elements of the capital structure• Financing partners able to work constructively in a “Shuttle Diplomacy” effort led by the company

The “Layer Cake” was then built:• Orion Mine Finance and the CDPQ purchased the stream and underwrote equity, convertible and COF• Investissement Québec and Ressources Québec purchased equity and senior debt• Caterpillar Finance provided an equipment financing facility• Marketed public equity finished it off (Scotia, Dundee and RBC co-leads)

Positives Negatives

• Fully financed plan removed risk for project team and investors

• C$48m COF debt based and sized to project

• Senior debt C$ denominated; stream US$ denominated

• Much less indebtedness than traditional debt/equity

• Security could be shared between senior lender and streamers

• Created strong shareholders motivated to see project success

• Complexity, and negative prejudice

that the “upside had been sold to the

streamers”. Public equity deal

required 120 meetings over 3 weeks

marketing. Ultimately successful.

16Renard Project Financing Transaction StructureLaunched on April 7th 2014. Closed July 8th 2014

Type Amount (% of Total) Description

Common Equity C$374M (40%)• C$132M marketed public equity offering of subscription receipts• C$242M private placement to Orion (US$110M), RQ (C$100M) and Caisse (C$22M)

Diamond Stream US$250M (29%) • 20% diamond stream (Orion 16%, Caisse 4%) with ~US$56/ct(1) ongoing payment

Convertible Debentures US$81M (9%) • Provided by Orion; 7 year, 6.25% coupon, 35% conversion premium to equity issue price

Senior Debt C$120M (11%) • Provided by IQ; 7 year amortizing payment, Fixed (QC Bond)+5.75% or Prime +4.75%

Equipment Financing US$35M (4%) • Provided by Caterpillar

Cost Overrun Facility C$48M (5%) • C$20M provided by IQ (same terms as senior debt)• C$28M provided by Caisse (unsecured, 7 year term, 10% coupon)

Total C$946M (100%)

Assumes US$1.00 = C$1.101. Includes reimbursement of marketing expenses

Counter-Party Amount (% of Total)

Orion Mine Finance C$367M (39%)

Investissement Québec/ Ressources Québec C$240M (25%)

Caisse de dépôt et placement du Québec C$105M (11%)

Caterpillar Financial C$39M (4%)

Public C$195M (21%)

Total C$946M (100%)

C$77M

C$811MC$946M

C$70M

C$67M

Financing Funding Requirements

New Financing

Existing Financing

C$48M COF & C$27M Working Capital

Financing Costs & Interest During Construction

Renard Mine Road

Initial Capex & Escalation Allowance

17Traditional Debt/Equity Financing Vs. Hybrid FinancingLess Debt and Less Equity under Hybrid Financing

The decision to go with the Hybrid financing model resulted in:• Less debt ($249 million + $48 million debt

COF vs. $475 million senior debt); and• Less equity ($374 million vs. $475 million

+ $125 million equity COF)

As a result, Stornoway will enter commercial production with• A less leveraged balance sheet; and• Greater flexibility related to cash flow

utilization than a traditional debt/equity transaction.

With the Hybrid model, Stornoway is better able to benefit from a lower C$:• US$ funds in from equity and stream,

rather than out to indebtedness• Bulk of SWY’s debt is C$ denominated

Debt

Debt

Equity

Equity

Stream

COF (Equity)

COF (Debt)

0

200

400

600

800

1,000

1,200

C$

mill

ions

TotalC$1,075m

TotalC$946m1

Traditional Debt/Equity Hybrid ModelNotes

1. Assumes US$1.00 = C$1.10

18The Renard Diamond StreamThe World’s First Diamond Streaming Arrangement

The buyers of the Renard stream purchased 20% of the LOM production from R2, R3, R4, R9 and R65 for US$56/carat1, escalating at 1% per annum on 3rd anniversary of commercial production.

Stornoway is to receive US$250million as a deposit on the streaming agreement, funded in three tranches, representing 34% of the initial capital for the project and 29% of the overall financing plan.

The high operating margins of the Renard project and front-ended capital requirements make it ideally suited for a streaming arrangement.

Notes1. includes reimbursement of marketing expenses.2. Average over 11 Year Mineral Reserve Case, Nominal Terms. 3. Shows the impact of a US$1.00 = C$1.25 exchange rate compared to the US$1.00 = C$1.00 rate utilized in the January 2013 Optimization Study

$58.92$5.04

$20.43

$76.63 $7.76 $58.92

OS Jan 2013 LNG OS Oct 2013 Stream Exchange Rate Cash cost/ct

Effective Project Cash Cost, Before and After Stream (US$/ct)1

19Investment Case for Stornoway? Renard’s Cash Flow Potential, Based on Base Case Economics

Renard is Expected to Generate Substantial Cash Flow over its first 11 years of Mining

After Tax, After Stream Operating Cash Flow of between $150 and $250 million, or $0.20 to $0.30 per share

Assumptions

Mineral reserve case only, averaging 1.6mcarats per annum at US$190/carat

Capital and operating cost parameters as established in the January 2013 Optimization Study and October 2013 LNG FS

Base case diamond pricing from March 2014; No “special” diamonds.

2.5% annual real diamond price escalation

C$:US$ conversion rate of C$1.10

Based on terms of Financing Transaction closed on July 8th 2014

Assumes full conversion to equity of US$81million of Convertible Debentures giving 825 million shares outstanding.

20

Investor - Issuer Date Size ($ MM) DescriptionFranco-Nevada - Lundin Oct-14 US$648 Franco-Nevada to receive 68% of payable Au and Ag production until 720k oz Au and 12MM oz Ag are delivered

from 100% of Candelaria; thereafter reduces to 40% of LOM payable metals from 100% of the mine. Acquisition f inancing package also consists of C$50MM private placement exclusive of stream value.

Orion Mine Finance & Caisse de dépôt - Stornoway

Apr-14 US$250 Stream agreement for 20% interest on run of mine diamond production from certain kimberlite bodies from the Renard Project. Investors to pay the Issuer in 3 deposits.

Gold Holding - Banro Aug-14 US$121 Streams on Banro's Tw angiza and Namoya mines for US$41MM and US$80MM, respectively. Investor to receive 40k oz Au from Tw angiza mine over 4 years. Investor to also receive 10% LOM Au production from Namoya including Au processed at the site from other mines w ithin 20 km; maximum deliverable Au of 12k oz per annum.

Franco-Nevada & Sandstorm - True Gold Aug-14 Up to US$120 Franco-Nevada (75%) & Sandstorm (25%) to receive 100k oz Au over 5 years, and 6.5% LOM Au production from True Gold's Karma Project thereafter. True Gold holds an 18 month option to increase funding by US$20MM for an additional 30k oz Au. Ongoing payments of 20% of spot Au.

Royal Gold - Rubicon Feb-14 US$75 Royal Gold to receive 6.3% of Au production from Rubicon's Phoenix Project until 135k oz have been delivered and 3.15% LOM Au production thereafter. Ongoing payments of 25% spot Au. Advance deposit payments from Royal Gold payable in 5 installments.

Orion Mine Finance - Aldridge Aug-14 US$40 Consists of US$5MM private placement and US$35MM 2-year bridge loan facility. Bridge loan bears interest at 9% plus the greater of 3 month USD LIBOR and 1%. Aldridge also entered into offtake agreements w ith Orion for ~20% of Pb & ~50% of Au production over the f irst 10 years of the mine plan.

Franco-Nevada - Klondex Feb-14 US$35 Franco-Nevada to receive 38k oz Au by December 31, 2018, and a 2.5% NSR royalty on Klondex's Fire Creek and Midas properties commencing 2019. Gold f inancing package provided to support Klondex's acquisition of the Midas Mine and Mill Complex from New mont.

JMET - Santacruz Silver Sep-14 US$28 5-year pre-paid forw ard silver purchase agreement. JMET to receive 4.6MM oz Ag through August 2019 w ith no ounces delivered over the f irst 12 months. Ongoing payments of spot Ag less an undisclosed f ixed discount.

Quintana - Arian Silver Oct-14 US$16 Quintana to receive 78.2% of Zn and Pb from San José until 32MMlbs and 38MMlbs, respectively, are delievered, and 27.4% thereafter for 50 years. Issuer can buy 50% of stream for US$11MM before 2017. Investor also acquires US$16MM of senior secured convertible notes to be restructured into new notes (8% interest).

Orion Mine Finance - Claude Mar-14 US$12 3.0% NSR royalty on Claude's Seabee Gold Operation. The NSR provides Claude w ith the option to repurchase half of the NSR for US$12MM until December 31, 2016.

BlackRock - Avanco Jul-14 US$12 2.0% NSR royalty on Cu; 25.0% NSR royalty on Au and 2.0% NSR royalty on all other metals produced from the Issuer's Antas North and Pedra Branca licensed areas. Additionally, BlackRock to receive a 2% NSR Royalty on other discoveries w ithin Avanco's current licence portfolio.

Sprott - Veris Gold Apr-14 US$8 0.5% NSR royalty on Veris Gold's Jerritt Canyon mines and processing plant.

How Stornoway’s Project Financing Ranked in 2014Alternative Finance Agreements

Source: Company Disclosure.

21

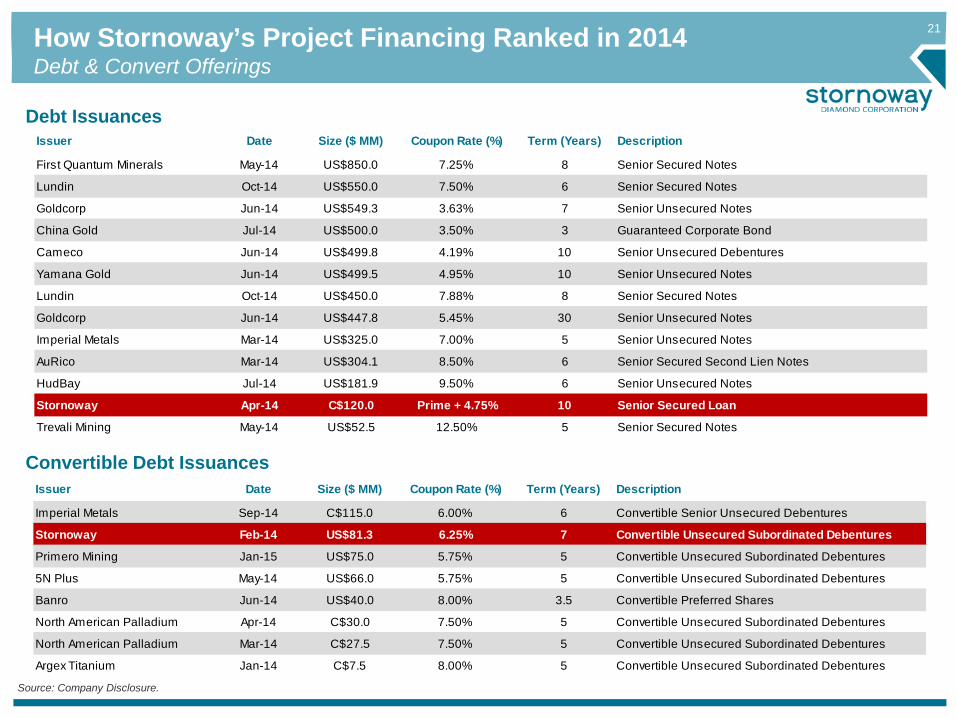

Issuer Date Size ($ MM) Coupon Rate (%) Term (Years) Description

Imperial Metals Sep-14 C$115.0 6.00% 6 Convertible Senior Unsecured Debentures

Stornoway Feb-14 US$81.3 6.25% 7 Convertible Unsecured Subordinated Debentures

Primero Mining Jan-15 US$75.0 5.75% 5 Convertible Unsecured Subordinated Debentures

5N Plus May-14 US$66.0 5.75% 5 Convertible Unsecured Subordinated Debentures

Banro Jun-14 US$40.0 8.00% 3.5 Convertible Preferred Shares

North American Palladium Apr-14 C$30.0 7.50% 5 Convertible Unsecured Subordinated Debentures

North American Palladium Mar-14 C$27.5 7.50% 5 Convertible Unsecured Subordinated Debentures

Argex Titanium Jan-14 C$7.5 8.00% 5 Convertible Unsecured Subordinated Debentures

Issuer Date Size ($ MM) Coupon Rate (%) Term (Years) Description

First Quantum Minerals May-14 US$850.0 7.25% 8 Senior Secured Notes

Lundin Oct-14 US$550.0 7.50% 6 Senior Secured Notes

Goldcorp Jun-14 US$549.3 3.63% 7 Senior Unsecured Notes

China Gold Jul-14 US$500.0 3.50% 3 Guaranteed Corporate Bond

Cameco Jun-14 US$499.8 4.19% 10 Senior Unsecured Debentures

Yamana Gold Jun-14 US$499.5 4.95% 10 Senior Unsecured Notes

Lundin Oct-14 US$450.0 7.88% 8 Senior Secured Notes

Goldcorp Jun-14 US$447.8 5.45% 30 Senior Unsecured Notes

Imperial Metals Mar-14 US$325.0 7.00% 5 Senior Unsecured Notes

AuRico Mar-14 US$304.1 8.50% 6 Senior Secured Second Lien Notes

HudBay Jul-14 US$181.9 9.50% 6 Senior Unsecured Notes

Stornoway Apr-14 C$120.0 Prime + 4.75% 10 Senior Secured Loan

Trevali Mining May-14 US$52.5 12.50% 5 Senior Secured Notes

How Stornoway’s Project Financing Ranked in 2014Debt & Convert Offerings

Debt Issuances

Convertible Debt Issuances

Source: Company Disclosure.

22How Stornoway’s Project Financing Ranked in 2014Marketed Public Equity Offerings

2014 Public Equity Offerings Issuer Date Size ($ MM)

Lundin Oct-14 C$674.2

Franco Nevada Aug-14 US$500.4

Primero Mar-14 C$224.3

Fortress (Lundin Gold) Oct-14 C$200.0

HudBay Jan-14 US$172.7

Detour Gold Feb-14 C$172.5

Torex Gold Jan-14 C$143.8

Ivanhoe Mines May-14 C$143.8

Stornoway Apr-14 C$132.0

Rubicon Minerals Feb-14 C$115.1

Platinum Group Metals Sep-14 US$113.8

MAG Silver Jun-14 C$79.0

Mountain Province Diamonds Sep-14 C$75.0

Pretium Jul-14 US$69.0

Altius Minerals Apr-14 C$65.0

Source: Company Disclosure.

Mining Issuance: 2014 and 2015 YTD

Sub-Sector # Deals C$MM

Gold 35 $1,687.2

Uranium 6 $78.3Silver 3 $1,828.5Rare Earth 2 $79.0

Zinc 0 $0.0

Coal 0 $0.0Molybdenum 0 $0.0

Nickel 2 $10.0

Total 63 $5,346

2015 YTDMining Sector Breakdown

Diamonds 6 $169.8Diversified 7 $1,480.8

Lithium 1 $8.0

Iron Ore 0 $0.0

Sub-Sector # Deals C$MM

Gold 64 $2,396.4Diversified 23 $1,407.0

Uranium 12 $166.2Copper 4 $188.5

Lithium1 $15.8

Silver 5 $127.3Rare Earth

4$37.8

Coal1

$0.0Molybdenum

0$0.0

Nickel

0

$10.2

Total 129 $4,789

2014Mining Sector Breakdown

Zinc

4$36.2

Iron Ore2

$3.0

Diamonds 9 $400.6

$12.9

$7.9

$19.9

$12.1

$8.2 $6.9 $5.5 $4.8 $5.3

255

110

188

303261

148 129 12963

2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD

C$Bn #

Copper 1 $4.0

Total Mining Issuance

23

Developments Subsequent to the Closing of the FinancingThe first two of three tranches of the RenardStream deposit funded in March and September 2015, on schedule. The third and final tranche is scheduled for March 2016.

In April 2015 Blackstone Tactical Opportunities acquired a significant equity position in Stornoway and a minority ownership interest in the Renard stream by way of a secondary market transaction with Orion.

Since July 2014 diamond prices have fallen an estimated 15-20% but the C$ has devalued from US$0.92 to US$0.75.

Stornoway has seen a substantial F/X gain on the US$ components of the financing (stream, Orion private equity, convertible debenture).

Stornoway’s equity has outperformed the sector of diamond producers and developers.

As of July 31, 2015, Stornoway forecasts excess financing capacity available to complete the

project of approximately $101 million comprised of $53 million of cash, receivables and expected mine tax credits and $48 million

of undrawn cost overrun facilities(1).Notes1. This forecast assumes a project cost of $811 million (which includes assumed levels of escalation and contingencies), the satisfaction of all covenants and

conditions precedent for future funding, and a CAD$:US$ exchange rate of $1.25 for unfunded US dollar denominated financing commitments. As construction of the Renard Diamond Project progresses, this forecast is expected to change quarter to quarter based on the timing of expenditures and receipts, volatility in the CAD$:US$ exchange rate, and any change to the forecast cost of the project.

-80.0%

-40.0%

0.0%

40.0%

80.0%

Equity Performance of Diamond Producers and Developers

Since July 8, 2014

SWY DDC GEMD LUC PDL FDI MPV

SWY

24

Construction at the Renard Diamond Project began on July 10th 2014, two days after the closing of the Project

Financing on July 8th, 2014

Building Québec’s First Diamond Mine

www.stornowaydiamonds.com

Progress as of September 30th, 2015Construction 47% complete compared to 43% in plan.

Forecast cost to complete within C$811m budget.

On schedule for plant commissioning 2H 2016, and commercial production 2Q 2017.

September 16, 2015

July 10, 2014

September 24, 2015

25

Principal Financial Advisor to SWYScotia Capital

Principal Advisor on Project FinancingBrent Cochrane

Fairness OpinionPrimary Capital

Legal CounselNorton Rose FulbrightSullivan and Cromwell

Principal SponsorsOrion Mine FinanceInvestissement Québec/Ressources QuébecCaisse de dépôt et placement du QuébecCAT Financial

Public Equity SyndicateScotia Capital (co-lead)Dundee Capital Markets (co-lead)RBC Dominion Securities (co-lead)Desjardins SecuritiesNational Bank FinancialLaurentian Bank SecuritiesParadigm Capital

Acknowledgements

2626

Thank You