Markets and Outlook: Global Agriculture

20

Markets and Outlook: Global Agriculture Agricultural Production and Consumption: Global Trends ― Implications for Development Cooper GIZ, Bonn, 10 December 2015 Jonathan Brooks Head, Agri-Food Trade and Markets Division Trade and Agriculture Directorate, OECD

-

Upload

pascal-corbe -

Category

Food

-

view

453 -

download

1

Transcript of Markets and Outlook: Global Agriculture

Markets and Outlook: Global Agriculture

Agricultural Production and Consumption: Global Trends ― Implications for Development Cooperation GIZ, Bonn, 10 December 2015

Jonathan BrooksHead, Agri-Food Trade and Markets DivisionTrade and Agriculture Directorate, OECD

22OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 2

• Calmer food markets, with strong harvests and abundant stocks for cereals and oilseeds

• Prices for meat and dairy products have come down from record highs

• Low oil prices• Biofuel production generally not profitable

• Weak economic growth globally

Context

33OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 3

• Real food prices expected to decline slightly, but remain above levels before 2007-08 food price crisis.

• Changing relative prices:› Consumption of staples reaching saturation in many countries› Meat and dairy prices increase relative to crops – higher incomes and protein

demand› Coarse grain and oilseed prices increase relative to food staples – feed

demand• Calmer markets but a risk of resurgent volatility• Spread of imports across a large number of countries;

concentration of exports among a few key suppliers

Highlights of the OECD-FAO Outlook

44OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 4

Real prices to remain higher than in the years preceding the 2007-08 price spike

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

40

50

60

70

80

90

100

110

120

130

CerealsDairyMeatOilseeds

Index (2012-14=100)

55OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 5

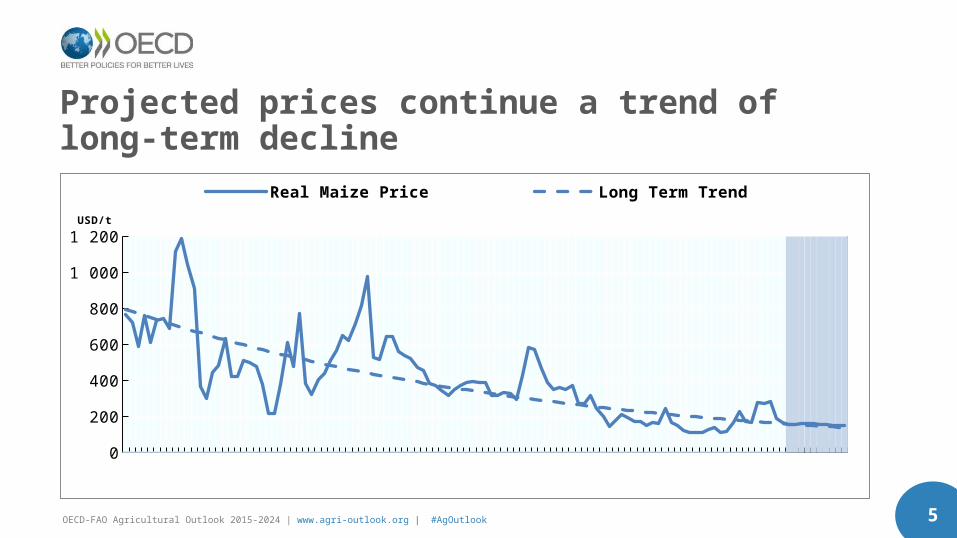

Projected prices continue a trend of long-term decline

0

200

400

600

800

1 000

1 200

Real Maize Price Long Term TrendUSD/t

66OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 6

For most products price volatility has come down

Beef Rice Maize Wheat Soybeans … Food0

0.1

0.2

0.3

0.4

0.5 1970-79 1980-89 1990-99 2000-09 2010-14

Source: IMF, World Bank

Monthly CV

77OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 7

But there is a substantial risk of a further price shock

0

50

100

150

200

250

300

350

400

10th

90th

Nominal maize priceUSD/t

Probability of price outside the 10-90th percentile = 1 – 0.8**10 or approximately 90%

88OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 8

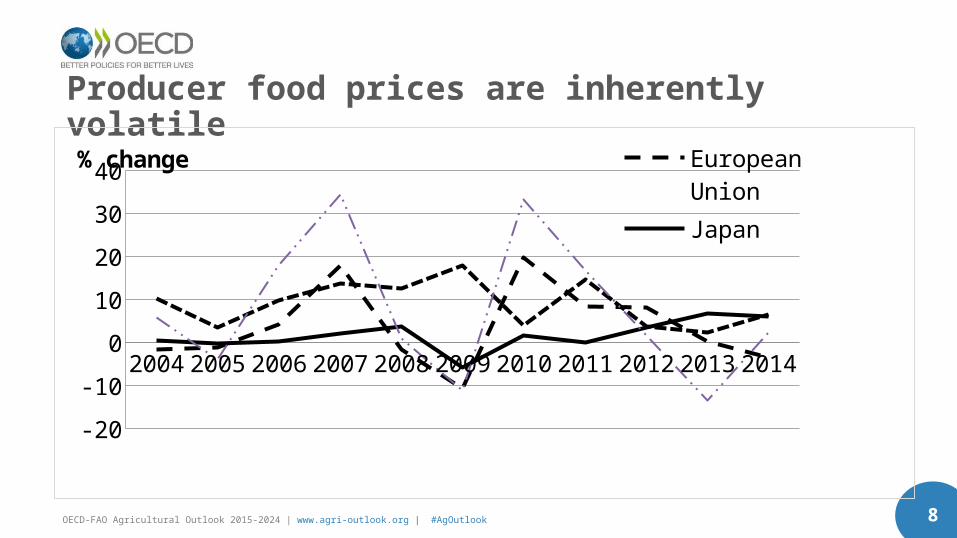

Producer food prices are inherently volatile

20042005200620072008200920102011201220132014

-20-10

010203040 European

UnionJapanBrazil

% change

99OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 9

…consumer prices much less so

20042005200620072008200920102011201220132014

-20-10

010203040 European

UnionJapan

% change

1010OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 10

Per capita food consumption growing modestly

Annual compound per capita growth rate between 2015-2024 (%)

1111OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 11

Centres of per capita production growth differ

Annual compound per capita growth rate between 2015-2024 (%)

1212OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 12

Increasing meat demand

Annual compound per capita growth rate between 2015-2024 (%)

1313OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 13

On current trends, undernourishment will decrease, but not in SSA, and SDG2 will not be met

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

0

200

400

600

800

1000

1200

Other Latin America and Caribbean India China Asia and Pacific (excluding China and India)

Sub-saharan Africa North AfricaMillion

1414OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 14

Trend growth will induce over 200 million workers to transition from agriculture

2005 2015 20240

500

1000

1500

2000

2500

3000

3500

4000

201 million

Non-Agricultural Employment Transition from Agriculture to Non-Agriculture Agricultural EmploymentMillion

1515OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 15

• Global food and energy prices

• Scramble for land in Africa

• Land degradation

• Youth bulge and employment challenges

• Income growth and distribution

• Greater climate variability

• Information communication technology

Forthcoming African outlook will focus on mega-trends

1616OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 16

Levels of support to producers (PSE) in OECD and emerging economies are converging

Source: OECD (2015), "Producer and Consumer Support Estimates", OECD Agriculture statistics (database), http://dx.doi.org/10.1787/agr-pcse-data-en.

Percentage of gross farm receipts

1717OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 17

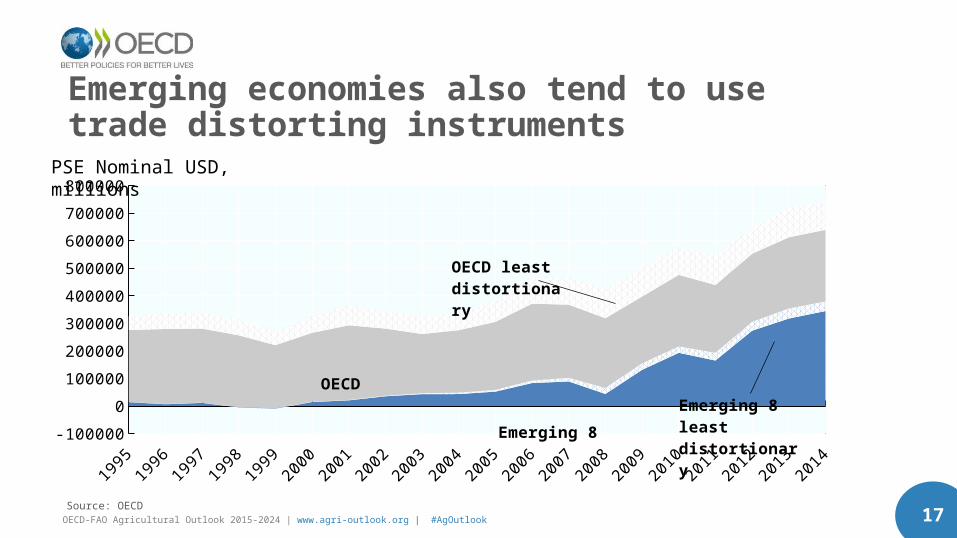

Emerging economies also tend to use trade distorting instruments

Source: OECD19

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

14-100000

0100000200000300000400000500000600000700000800000

Emerging 8

OECD

OECD least distor-tionary

Emerging 8 least distortionary

PSE Nominal USD, millions

1818OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 18

• Need transparent and open agricultural markets• Measures to improve productivity sustainably benefit consumers and

(innovating) farmers• Other actions can increase food availability – reduced post-harvest losses,

reduced waste, less over-consumption…but will not by themselves ensure food security

• Phasing out 1st generation biofuel support would eliminate a factor that can turn a shock into a crisis

• Need to price scarce resources for sustainable use• Risk management tools needed to manage price volatility, not border

measures

OECD’s main policy conclusions:

1919OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 19

The future’s so bright, we gotta wear shades!

2020OECD-FAO Agricultural Outlook 2015-2024 | www.agri-outlook.org | #AgOutlook 20

We invite you to visit our websitewww.agri-outlook.org

Jonathan Brooks, Head of Division

Hubertus Gay, Outlook Coordinator at OECD

[email protected] and Agriculture Directorate(OECD)