Market Trends: Multienterprise/B2B Infrastructure Market,...

13

Market Trends: Multienterprise/B2B Infrastructure Market, Worldwide, 2009-2014 Dataquest Note G00200571, Fabrizio Biscotti, Paolo Malinverno, Benoit J. Lheureux, Thomas Skybakmoen, 14 July 2010, R3569 7142011 During the next five years, the multienterprise/business-to- business (B2B) infrastructure market will continue to grow at a steady pace. This period will offer good opportunities for existing providers and market consolidators and strong potential for new entrants — particularly if they are already players in the application integration and middleware space — although substantial investment in sales, marketing and product functionalities will be required to displace well-established incumbents and to gain market share. In addition, the B2B market is already crowded in some regions (such as the U.S. and parts of Western Europe). Key Findings • The fastest-growing segments are managed file transfer as a service (MFTaaS) for B2B, cloud services integration as a service and B2B integration outsourcing (BIO), which are benefiting from increasing end users’ attention on cloud and managed services. • Between 2010 and 2014, we expect Global 2000 companies to at least double their multienterprise traffic (transactions, documents and process execution events), and this will have a significant impact on the amount of spending that goes toward multienterprise/ B2B infrastructure. • One key driver for the revenue growth of multienterprise/B2B infrastructure technologies will be that midsize to large businesses will need to implement several different styles of multienterprise collaboration to meet diverse external business partner requirements. This is set to be a driver for software segments such as multienterprise/B2B gateways and for service segments such as B2B Integration outsourcing. • E-invoicing projects will be increasingly common, due to new regulations and pressure on reducing costs, especially in some countries of Western Europe (such as Spain and Germany) and of South America (such as Mexico and Brazil).

Transcript of Market Trends: Multienterprise/B2B Infrastructure Market,...

Market Trends: Multienterprise/B2B Infrastructure Market, Worldwide, 2009-2014

Dataquest Note G00200571, Fabrizio Biscotti, Paolo Malinverno, Benoit J. Lheureux, Thomas Skybakmoen, 14 July 2010, R3569 7142011

During the next five years, the multienterprise/business-to-business (B2B) infrastructure market will continue to grow at a steady pace. This period will offer good opportunities for existing providers and market consolidators and strong potential for new entrants — particularly if they are already players in the application integration and middleware space — although substantial investment in sales, marketing and product functionalities will be required to displace well-established incumbents and to gain market share. In addition, the B2B market is already crowded in some regions (such as the U.S. and parts of Western Europe).

Key Findings

• Thefastest-growingsegmentsaremanagedfiletransferasaservice(MFTaaS)forB2B,cloudservicesintegrationasaserviceandB2Bintegrationoutsourcing(BIO),whicharebenefitingfromincreasingendusers’attentiononcloudandmanagedservices.

• Between2010and2014,weexpectGlobal2000companiestoatleastdoubletheirmultienterprisetraffic(transactions,documentsandprocessexecutionevents),andthiswillhaveasignificantimpactontheamountofspendingthatgoestowardmultienterprise/B2Binfrastructure.

• Onekeydriverfortherevenuegrowthofmultienterprise/B2Binfrastructuretechnologieswillbethatmidsizetolargebusinesseswillneedtoimplementseveraldifferentstylesofmultienterprisecollaborationtomeetdiverseexternalbusinesspartnerrequirements.Thisissettobeadriverforsoftwaresegmentssuchasmultienterprise/B2BgatewaysandforservicesegmentssuchasB2BIntegrationoutsourcing.

• E-invoicingprojectswillbeincreasinglycommon,duetonewregulationsandpressureonreducingcosts,especiallyinsomecountriesofWesternEurope(suchasSpainandGermany)andofSouthAmerica(suchasMexicoandBrazil).

2Recommendations

• Endusersshouldplacegreatcareinassessingvendorviability.BecausetheoutsourcingB2Bintegrationfunctionality(integrationasaservice,IaaS)andB2Bprojects(BIO)makesavendorapartnerintheB2Bintegrationproject,vendorviabilitymusthaveasubstantialweightinevaluationsforintegrationserviceprovidersintermsofvendorsizeandsupportqualityinyourlocalgeography

• Vendorsshouldfocusonmodularofferingsinwhichcustomerscanstartsmallandincrementallybuildwithtime.Thisisbecause,giventhestillchallengingeconomicconditions,endusersaremorewaryaboutlargeprojectsandtherelativecostsandprefertostartsmallandgrowincrementallyovertime.

• Vendorsshouldbepreparedwithcustomerreferencesandafocusedgo-to-marketstrategythatwillputthemasapointofcontactforanycompanylookingattherationalizationoftheirB2Binfrastructures.

WHAT YOU NEED TO KNOWGartnerdefinesmultienterpriseinfrastructure(alsoreferredtoasB2Binfrastructure)asanITprojectthatiscomposedofsomecombinationofB2BsoftwareandB2Bservicesthatcompaniesusetoperformmultienterpriseintegrationwithexternalbusinesspartners.

Figure1showstheimportanceofthe$2.7billionmultienterprise/B2Binfrastructuremarketwithinthewiderfamilyofapplicationinfrastructureandmiddleware(AIM)technologies.

©2010Gartner,Inc.and/oritsaffiliates.Allrightsreserved.GartnerisaregisteredtrademarkofGartner,Inc.oritsaffiliates.ThispublicationmaynotbereproducedordistributedinanyformwithoutGartner’spriorwrittenpermission.Theinformationcontainedinthispublicationhasbeenobtainedfromsourcesbelievedtobereliable.Gartnerdisclaimsallwarrantiesastotheaccuracy,completenessoradequacyofsuchinformationandshallhavenoliabilityforerrors,omissionsorinadequaciesinsuchinformation.ThispublicationconsistsoftheopinionsofGartner’sresearchorganizationandshouldnotbeconstruedasstatementsoffact.Theopinionsexpressedhereinaresubjecttochangewithoutnotice.AlthoughGartnerresearchmayincludeadiscussionofrelatedlegalissues,Gartnerdoesnotprovidelegaladviceorservicesanditsresearchshouldnotbeconstruedorusedassuch.Gartnerisapubliccompany,anditsshareholdersmayincludefirmsandfundsthathavefinancialinterestsinentitiescoveredinGartnerresearch.Gartner’sBoardofDirectorsmayincludeseniormanagersofthesefirmsorfunds.Gartnerresearchisproducedindependentlybyitsresearchorganizationwithoutinputorinfluencefromthesefirms,fundsortheirmanagers.ForfurtherinformationontheindependenceandintegrityofGartnerresearch,see“GuidingPrinciplesonIndependenceandObjectivity”onitswebsite,http://www.gartner.com/technology/about/ombudsman/omb_guide2.jsp

Figure 1. AIM Software and Outsourcing Market by Macro Area

Note:theoverallsizeincludedboththeAIMsoftwaremarketrevenueandtheB2BIOrevenue.

Source:Gartner(June2010)

3Theobjectiveofmultienterpriseinfrastructureistoexchangebusinessdata(forexample,customerorsupplygoodsdata)ortolinkandautomatebusinessprocesses(forexample,order-to-cashorprocure-topay)betweentwoormorecompaniesinawaythatiseasiertomanage,faster,more-affordableandmore-accuratethanmanualapproachesorcustomcoding.Toaccomplishtheseobjectives,companiesusearangeofapproaches,suchasbuildingoroutsourcingtheB2Binfrastructure,orusingtraditionalbatchelectronicdatainterchange(EDI)atoneextreme,emergingcloudservicesattheotherextreme,Webservices-basedSOAoracombinationofanyoftheseapproachestoB2B.Forthisreason,therearecurrentlyseveralmultienterprise/B2Binfrastructureofferingsavailableinthemarketwithsimilarlydifferenttractionandprospectsforgrowth.

ThewaveofmergersandacquisitionsthatischaracterizingtheoverallAIMmarketandthespecificB2Bintegrationmarketisamajordisrupterthatwillcontinuetoshapethevendorlandscapeduringtheforecastperiod.Changesinthevendorlandscape(suchas,IBMacquiringSterlingCommercemighttriggeroraccelerateacquisitioningmovesbyitsmaincompetitors)willoffernewopportunities,butalsomorereasonsforcautionbyuserorganizations.OrganizationshavingtoaddressB2Brequirementsmustassesscarefullythebalancebetweenextraspecializedpure-playB2Bvendors(typicallysmallerandnimbler)andvendorsthatofferB2Binconjunctionwithotherintegrationproductsandservices.Dealswillhavetofocusontheabilityofvendorstohavesufficientresourcesanddomainexpertisetomeetdiverse,geographic-andvertical-specificB2Bproject-scoperequirementsthatarelikelytoexpandinthefuture.

AsfarasdiversewaysofdeliveringB2Bcapabilities,wehaveidentifiedninesegments,includingpurelysoftwareofferingsandserviceofferings,composingtheB2Binfrastructureportfolio;eachofthesesegmentsaddressesdifferentB2Bprojectrequirementsandhasspecificprosandcons;somearelegacytechnology,andsomeareemergingofferings,buttheyallplayaroleinthecurrentorganization’squestforB2Bintegrationportfolioconsolidation.Thesegmentscomposingthemultienterprise/B2BInfrastructureportfolioareasfollows:

• BIO

• Traditionale-commerceIaaS

• CloudservicesIaaS

• Managedfiletransfer(MFT)forB2B

• MFTaaSforB2B

• Service-orientedarchitecture(SOA)governancesoftwareforB2B

• Stand-alonemultienterprise/B2Bgateways

• Embeddedmultienterprise/B2Bgateways

• Electronicdatainterchange(EDI)translators(stand-alone)

Stand-aloneEDItranslatorsoftwareistypicallylicensedfromanEDIsoftwareproviderortraditionalvalue-addednetwork(VAN)thatisfocusedprimarilyonthetranslationofEDIdataintointernaldataformats.TherearealsoembeddedEDItranslatorsthatareofferedasfunctionalitywithinmultienterprise/B2Bgateways.However,thisembeddedcomponentisfairlycommoditized,anditsrevenuecontributionisrecognizedintherevenuesizeofmultienterprise/B2Bgateways.

B2Bgatewaysoftwareismiddlewareusedtoconsolidateandcentralizeacompany’smultienterprisedata,application,processintegrationandinteroperabilityrequirementswiththoseofexternalbusinesspartners.

MFTsoftwareenablescompaniestoautomate,compress,restart,secure,log,analyzeandauditthetransferofdatafromoneendpointtoanother,often(notalways)includingexternalbusinesspartners.

SOAgovernancesoftwareforB2BprojectsisdrivenbytheemergenceofSOAoverall,whichhelpscoordinatethegovernanceoftheservicesinvolved.BecauseSOAismakingasignificantinroadintotheB2Bspace,thereisagrowingmarketopportunityforofferingsaddressingthespecificneedsofSOAgovernancewithinB2Bprojects.

IaaSismultienterpriseintegrationcapabilities(suchasthatofB2Bgatewaysoftware)hostedinamultitenantenvironmentanddeliveredasaserviceratherthanassoftware.TraditionallyknownasEDIVANs,vendorsofferingIaaSarecalled“integrationserviceproviders.”Thissegmentiscomposedbytraditionale-commerceIaaS,cloudservicesIaaSandMFTaaSforB2B.

B2BIntegrationoutsourcingisaspecificcategoryofITprojectoutsourcingthatcombinesoutsourcingyourtechnicalB2Binfrastructure(IaaS)andyourB2Bproject(thatis,thepeopleandprocesses).Mostofe-invoicingprojectswillbeinthissegment.

OntheB2Bsoftwareside,akeytrendisthatthemarketforstand-aloneEDItranslators,SOAgovernancetechnologies,andMFTisquicklybeingabsorbedintoB2Bgatewaysoftware.Sofar,mostSOAgovernancesoftwareforB2Bprojectsaresoldasastand-alone,butovertimethisfunctionalitywillincreasinglybecomeavailableasanembeddedfeatureofB2BgatewaysoftwareandcloudserviceIaaS.Ontheserviceside,B2BIntegrationoutsourcingincreasinglyisdeployedusinganIaaSofferingasthetechnologybackbone,whichlowersoverallprojectcostsbecauseitleveragessharedB2Binfrastructure.

KEY TRENDSIntegrationisnolongeraprojectbetweentwoapplications.Itisacross-companyandbetween-companydisciplinethatincreasinglyinvolvesallofanorganization’sapplications,externalbusinesspartnersandcloudservices.The“dumb”networkthatusedtoonlytransferbulkfilesbetweenapplicationsandtradingpartnersisturningintoa“smart”networkthatincorporatesdiverseintegrationfunctionality,includingcommunications,translationandworkflow,increasinglyimplementedbyapplicationvendorsandusersusinganSOA.TheB2Bdisciplinealsonowmustincludecloudservicesintegration—forexample,howtolinkservicesfromsolutionssuchassalesforce.comtoon-premisesapplications.SuccessfulorganizationswillcombinetraditionalintegrationandemergingSOA

4andWeb-nativeapproachessuchasWeb-orientedarchitecture(WOA)andcloudAP’stosolvediverseapplicationintegrationandinteroperabilityrequirements.Thescopeoftheseeffortswillinvolveinternalandexternalapplications,thelatterincludinge-commercetradingpartnersandexternalserviceproviders(ESPs),suchasserviceintegratorsandsoftwareasaservice(SaaS)providers.

AtypicalITinfrastructureincludesadapters;datatransformationenginesandextraction,transformationandloading(ETL)tools;integrationbrokers,managedfiletransferandbusinessprocessmanagerstoorchestratemessageflows,Webserviceschoreographyandbusinessprocessexecution;eventmanagement;andalertingfacilitiesforbusinessactivitymonitoring(BAM).OrganizationswillthenneedB2BinfrastructuretoextendtheirITinfrastructuretoexternalbusinesspartners,includingprovisioningtoolstosimplifytheprocess.

The B2B Vendor Landscape — More Consolidation Ahead Whenpure-playapplicationintegrationvendorscametomarketinthemid-1990s,productsintroducedhadabasesetoffeaturesthatincludeddatatransformation,intelligentrouting,message-orientedmiddleware,amessagewarehouseandadministration/management.Whenlargesuitevendors(suchasOracle)enteredthemarket(inthelate1990s),theyalsoofferedsimilartypesofbasefeatures.However,thenumberoffeaturesinproductsfrompure-playvendorshasbeenextendedtoincludeworkflow,internalintegrationfeatures(suchasadaptersforpackagedapplications),processvisibilityandotherformsofBAM.Theneteffectofthisovertimeisthatthedistinctionbetweenpure-playB2Bproductsandpure-playinternalintegrationproductsisblurring,andincreasingB2Bcapabilitieswillsimplybeafeatureofanyintegrationmiddleware.Furthermore,webelievethatthepure-playB2Bmarketwillultimatelyceasetoexist,althoughstand-aloneB2Bproductsandserviceswillcontinuetobeavailableforatleastthenextdecade.

WeexpecttheB2BmarkettoconsolidatearoundfewerB2Bspecialists,whilewealsoexpecttraditionalAIMvendors(particularlysuitevendors)toconsiderexpandingintothemultienterprise/B2Binfrastructurespace.Asaconsequence,theB2BsuitevendorsandtheAIMvendorswillincreasinglybattlehead-to-head;theformerwillpromotetheirabilitytodeliverspecificexpertiseandexcellenceintheB2Bspace,includingmuch-neededverticalknowledge,whilethelatterwillcapitalizeontheirabilitytoreachouttoasizableexistingcustomerbaseandtothoseorganizationslookingfora“goodenough”B2Bsolution.

ThemainchallengeforB2Bspecialistswillbetoreachouttothesamevariety(intermsofverticalmarketsandgeography)ofexistingcustomersthatatypicalAIMvendormightbeabletoreach.ThiswillbeincreasinglydifficultwhenfacingamegavendorthatisstartingtoplayinB2B.Furthermore,byexploitingexistingrelationshipsandcross-sellingandupsellingB2Bfunctionalitytotheirexistingcustomers,AIMvendorsobtainthepotentialcompetitiveadvantageofshorteningsalescycletimesandbeingabletooffer(veryoften,goodenough)B2Bfunctionalityatadiscountedrateontopofothermiddlewareofferings.Also,forthecustomers,it’smucheasiertoconnectanyB2BextensionintosomethingthatisalreadypluggedintoandintegratedwiththeirITsystems.

Multienterprise/B2BgatewaysoftwarewouldgenerallybetheentrypointtotheB2BmarketfortraditionalAIMplayersthatcanpotentiallyofferB2Bgatewayfunctionalitieswithinwiderintegrationsuiteofferings.Thisisbecausethemultienterprise/B2Bgatewaymarketiscomposedofmiddlewaretechnologyfrommultipledisciplines,includingintegrationsuites,enterpriseservicebuses,applicationserversandapplicationplatformsuites,EDItranslators,MFTandtheB2B-enabledintegrationmiddlewarethatisincreasinglyavailablewithpackagedapplications.Ingeneral,vendorsofferinganyofthesemiddlewaretechnologieswouldfinditeasiertoalsotrytoaddresstheB2Bgatewayneedsoftheircustomers.

Ontheintegrationservicesside,wehaveseensubstantialmarketconsolidation,whichwillcontinueinthenextyears.RecentexamplesincludeIBM’sacquisitionsofCastIronandSterlingCommerceandtheGXSmergerwithInovis.Overall,theexpansionofpure-playintegrationvendors(mostofwhichalreadyoffersomekindofB2Bfunctionality)willcauseincreasedpressureonsmallerB2Bplayers,someofwhichwillultimatelylosemarketshareand/orbecomeappealingacquisitiontargets.WebelievethattherecentSPSCommerceIPO—wasexecutedatleastinpartbecauseofpressurefromlargerprovidersandaneedtoraisecapitaltobettercompete.

Multienterprise/B2B Infrastructure Market OutlookInsizingthemultienterprise/B2Binfrastructuremarket,weconsideredsomecomponentsthataresoldasaspecificstand-aloneB2Bproductorasafunctionalitypartofasuite.

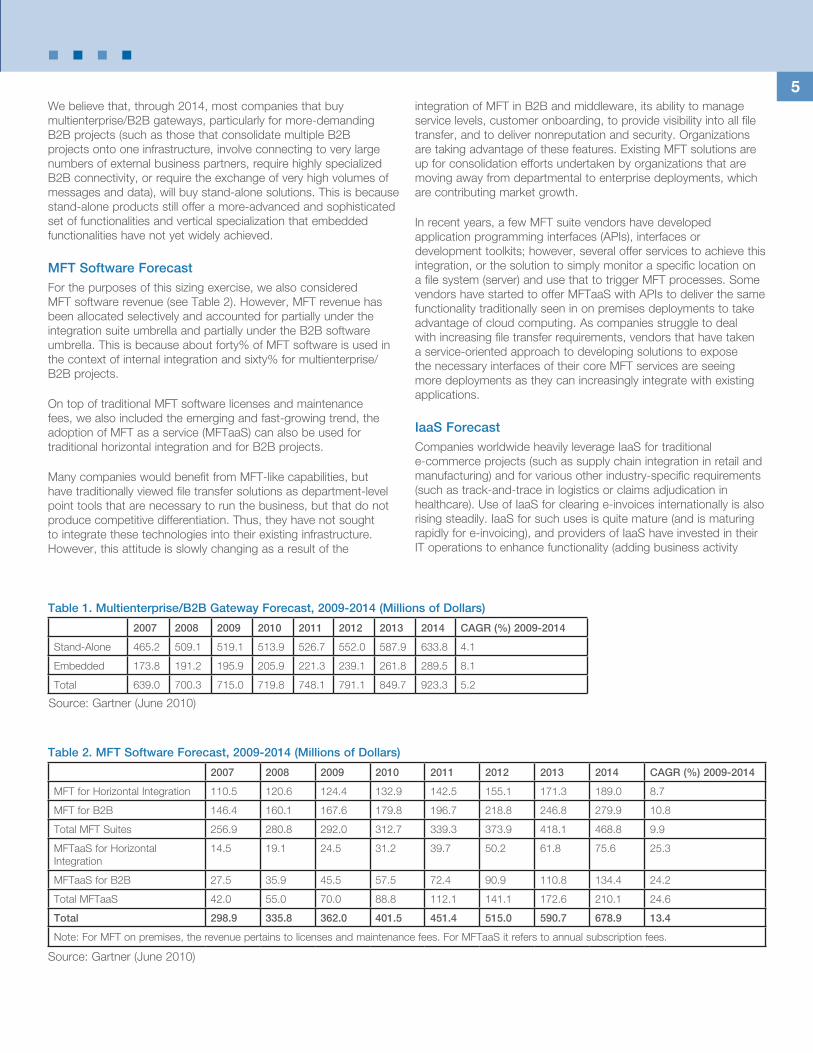

Multienterprise/B2B Gateway Software ForecastMultienterprise/B2BgatewaysolutionsaresoldbyB2Bspecialistsasastand-aloneproduct(suchasthosesoldbySterlingCommerce(nowpartofIBM),Axway,GXS,SeeburgerAG,SoftwareAGandGenerix)orasafunctionalitywithinabroaderintegrationsuite(suchasthosesoldbyTibco,SoftwareAG,OracleandMicrosoft).

AsshowninTable1,theoverallmultienterprise/B2Bgatewaymarketisexpectedtogrowatasingle-digitratethrough2014,outpacingtheoverallApplicationInfrastructureandMiddlewaresoftwaremarket.

Multienterprise/B2Bgatewayscontinuetobeinhighdemandfromorganizationsofeverysize,regardlessofindustryexpertise.Vendorshaveexpandedthefunctionalityofthemultienterprise/B2Bgatewayfromprimarilyprovidingameansofconsolidatingandcentralizingacompany’sB2Bcommunications(regardlessofthesizeandtypeofdata),toprovidingsomeinternalintegration(resultingintheeventualexternalizationoftheintegrateddata),andprovidinganinfrastructureincludinginnovativecommunitymanagementcapabilitiesforautomatingandmonitoring(frombothatechnologyandbusinessprocesspointofview)interactionswithexternalbusinesspartners.Thisevolvedfunctionalitygivescompaniestheflexibilitynecessarytosupportthemyriadofcurrentandemergingtransportandcommunicationsprotocols,aswellassecuritystandardsandmechanisms.

5Webelievethat,through2014,mostcompaniesthatbuymultienterprise/B2Bgateways,particularlyformore-demandingB2Bprojects(suchasthosethatconsolidatemultipleB2Bprojectsontooneinfrastructure,involveconnectingtoverylargenumbersofexternalbusinesspartners,requirehighlyspecializedB2Bconnectivity,orrequiretheexchangeofveryhighvolumesofmessagesanddata),willbuystand-alonesolutions.Thisisbecausestand-aloneproductsstillofferamore-advancedandsophisticatedsetoffunctionalitiesandverticalspecializationthatembeddedfunctionalitieshavenotyetwidelyachieved.

MFT Software Forecast Forthepurposesofthissizingexercise,wealsoconsideredMFTsoftwarerevenue(seeTable2).However,MFTrevenuehasbeenallocatedselectivelyandaccountedforpartiallyundertheintegrationsuiteumbrellaandpartiallyundertheB2Bsoftwareumbrella.Thisisbecauseaboutforty%ofMFTsoftwareisusedinthecontextofinternalintegrationandsixty%formultienterprise/B2Bprojects.

OntopoftraditionalMFTsoftwarelicensesandmaintenancefees,wealsoincludedtheemergingandfast-growingtrend,theadoptionofMFTasaservice(MFTaaS)canalsobeusedfortraditionalhorizontalintegrationandforB2Bprojects.

ManycompanieswouldbenefitfromMFT-likecapabilities,buthavetraditionallyviewedfiletransfersolutionsasdepartment-levelpointtoolsthatarenecessarytorunthebusiness,butthatdonotproducecompetitivedifferentiation.Thus,theyhavenotsoughttointegratethesetechnologiesintotheirexistinginfrastructure.However,thisattitudeisslowlychangingasaresultofthe

integrationofMFTinB2Bandmiddleware,itsabilitytomanageservicelevels,customeronboarding,toprovidevisibilityintoallfiletransfer,andtodelivernonreputationandsecurity.Organizationsaretakingadvantageofthesefeatures.ExistingMFTsolutionsareupforconsolidationeffortsundertakenbyorganizationsthataremovingawayfromdepartmentaltoenterprisedeployments,whicharecontributingmarketgrowth.

Inrecentyears,afewMFTsuitevendorshavedevelopedapplicationprogramminginterfaces(APIs),interfacesordevelopmenttoolkits;however,severalofferservicestoachievethisintegration,orthesolutiontosimplymonitoraspecificlocationonafilesystem(server)andusethattotriggerMFTprocesses.SomevendorshavestartedtoofferMFTaaSwithAPIstodeliverthesamefunctionalitytraditionallyseeninonpremisesdeploymentstotakeadvantageofcloudcomputing.Ascompaniesstruggletodealwithincreasingfiletransferrequirements,vendorsthathavetakenaservice-orientedapproachtodevelopingsolutionstoexposethenecessaryinterfacesoftheircoreMFTservicesareseeingmoredeploymentsastheycanincreasinglyintegratewithexistingapplications.

IaaS ForecastCompaniesworldwideheavilyleverageIaaSfortraditionale-commerceprojects(suchassupplychainintegrationinretailandmanufacturing)andforvariousotherindustry-specificrequirements(suchastrack-and-traceinlogisticsorclaimsadjudicationinhealthcare).UseofIaaSforclearinge-invoicesinternationallyisalsorisingsteadily.IaaSforsuchusesisquitemature(andismaturingrapidlyfore-invoicing),andprovidersofIaaShaveinvestedintheirIToperationstoenhancefunctionality(addingbusinessactivity

2007 2008 2009 2010 2011 2012 2013 2014 CAGR (%) 2009-2014

Stand-Alone 465.2 509.1 519.1 513.9 526.7 552.0 587.9 633.8 4.1

Embedded 173.8 191.2 195.9 205.9 221.3 239.1 261.8 289.5 8.1

Total 639.0 700.3 715.0 719.8 748.1 791.1 849.7 923.3 5.2

Table 1. Multienterprise/B2B Gateway Forecast, 2009-2014 (Millions of Dollars)

Source:Gartner(June2010)

2007 2008 2009 2010 2011 2012 2013 2014 CAGR (%) 2009-2014

MFTforHorizontalIntegration 110.5 120.6 124.4 132.9 142.5 155.1 171.3 189.0 8.7

MFTforB2B 146.4 160.1 167.6 179.8 196.7 218.8 246.8 279.9 10.8

Total MFT Suites 256.9 280.8 292.0 312.7 339.3 373.9 418.1 468.8 9.9

MFTaaSforHorizontalIntegration

14.5 19.1 24.5 31.2 39.7 50.2 61.8 75.6 25.3

MFTaaSforB2B 27.5 35.9 45.5 57.5 72.4 90.9 110.8 134.4 24.2

Total MFTaaS 42.0 55.0 70.0 88.8 112.1 141.1 172.6 210.1 24.6

Total 298.9 335.8 362.0 401.5 451.4 515.0 590.7 678.9 13.4

Note:ForMFTonpremises,therevenuepertainstolicensesandmaintenancefees.ForMFTaaSitreferstoannualsubscriptionfees.

Table 2. MFT Software Forecast, 2009-2014 (Millions of Dollars)

Source:Gartner(June2010)

6monitoringandimprovedcommunitymanagement),andtodriveincreasingscaleandefficiencies(switchingtomore-modern,scalableIaaSarchitectures).ThoseITmodernizations,combinedwithincreasingadoptionandtheprevailingperceptionthatIaaSisincreasinglyacommodity,havebeendrivingdownIaaSpricesfornearlyadecade.Nevertheless,IaaSfortraditionale-commerceisstillavaluableITserviceforcompaniesdoingB2Bintegration;therefore,adoptioncontinuestoincrease,asindicatedbytheincreasingnumbersofcompaniesandtransactionshandledbytheprovidersofIaaSeachyear(generallyrangingfroma10%to100%increaseinthenumberofcompaniesservedandtransactionsexchangedperyear,dependingonthesizeoftheprovider).Thistrendhasbeenconsistentworldwideyeartoyear—evenduringthecurrentworldwiderecession—asmorecompaniesseekoutsourcing(subscription)alternativestothesignificant(capital)costofexpandingB2BinfrastructureandstaffingwhenitisnecessarytoscaleuptheirB2Bprojects.AsIaaSincreases,SaaSapplicationsusingIaaSwillincreasesteadilytoo.Table3showsthesizeandgrowthrateofthedifferentcomponentsoftheIaaSsegment.

CloudserviceintegrationisarelativelynewB2Bintegrationprojectscenario,yetthebuyersofIaaSforcloudserviceintegrationrangefromline-of-businessITbuyers—primarilyonlyfocusedonthecloudservicetoon-premisesintegrationproblem—tomore-traditionalITbuyers—focusedoncloudserviceintegrationandontraditionale-commerceintegration.ProvidersofIaaSforcloudserviceintegrationoftenselldirectlytoITend-users;theyalsosellasubstantialproportionoftheirIaaSservices(weestimate50%)throughITchannelpartners.

ThisisbecausemanyITservicesproviders—particularlySaaSproviders—mustaddresscloudserviceintegration,yetwouldprefertoinvesttheirlimitedR&Dcapabilitiesondifferentiatedfunctionalitythatbuildsabarriertoentryintheirtargetmarkets,ratherthanmakingsubstantialinvestmentstosolveatechnicallycomplicatedintegrationproblem.FouryearsagotherewasbasicallynomarketforIaaSforcloudserviceintegration.Today,

weestimatethatcompaniesspend$50milliononIaaSforcloudserviceintegration,andthatthisITmarketsegmentwillgrowat23.5%CAGRforthenextfiveyears.

Overall Multienterprise/B2B Infrastructure Market ForecastThemultienterprise/B2Binfrastructuremarketispoisedforgoodgrowthduringthenextfiveyears.Itwillbedrivenbytheincreasingmaturityandadoptionofvariousrelatedstandards—suchasXML,SOA,Webservices,cloudcomputing,globaldatasynchronization(GDS),andforecasting—combinedwiththeincreasingmaturityandflexibilityoftheintegrationofSaaS.

Furthermore,thereisalreadyagoodsetofreferenceorganizationssuccessful(generallyintermsofprocessimprovementsandcostsavings)inmultienterprisecollaboration,reportingbottom-lineandtop-linerevenueincreasesattributedtoincreasedautomation,lowercostsandimprovedprocessexecution,whichimprovesbusinesspartnerrelationshipsandattractsnewbusiness.Theprospectsforgrowthremainpositivebecausetheneedforinterenterprisecollaborationdoesnotshowanysignsofdiminishing.

Tosizethemarket,weconsideredtotalsoftwarerevenue(fromnewlicenses,maintenanceandtechnicalsupport)generatedbysalesofstand-aloneandembeddedmultienterprise/B2Bgateways,MFTforB2B,EDItranslators(stand-alone),andSOAgovernancesoftwareforB2Bproducts.ForIaaS,weconsideredsubscriptionrevenue(inourdefinition,partofmaintenance),andforB2BIntegrationoutsourcing,weestimatedrevenuegeneratedexcludingprofessionalservicesfees.

In2009,weestimatetheoverallmultienterprise/B2Binfrastructuremarketgeneratedalmost$2.8billion(seeFigure2).Themarketwillgrowata9.0%CAGR,whichisabout2percentagepointshigherthanthegrowthweexpectfortheoverallapplicationinfrastructureandmiddlewaremarket.

7

2007 2008 2009 2010 2011 2012 2013 2014 CAGR (%) 2009-2014

TraditionalE-CommerceIaaS

946.3 969.2 849.2 775.5 714.0 662.0 617.9 573.5 -7.5

CloudServicesIaaS 35.3 41.7 50.4 61.5 75.8 94.3 116.9 145.0 23.5

MFTaaSforB2B 27.5 35.9 45.5 57.5 72.4 90.9 110.8 134.4 24.2

Total 1,009.0 1,046.7 945.1 894.5 862.1 847.2 845.6 853.0 -2.0

Table 3. IaaS Forecast, 2009-2014 (Millions of Dollars)

Source:Gartner(June2010)

Figure 2. Multienterprise/B2B Infrastructure Market Forecast, 2009-2014

Source:Gartner(June2010)

8Intermsofrevenuesize,traditionale-commerceIaaSisthelargestsegment,closelyfollowedbyB2BIntegrationoutsourcingandthenmultienterprise/B2Bgatewaysstand-alone(seeFigure3).

However,thepictureisverydifferentwhenlookingatthegrowthratesoftheindividualsegments(seeFigure4).Infact,thefastest-growingsegmentisexpectedtobeMFTaaSforB2Bdrivenbywhattraditionallyhavebeenasmallmarketandfewvendors,tobeanalternativedeploymentoptionforMFTsolutions.TheincreasedbusinessneedforsendingandreceivinglargefilesandincreasedfocusoncompliancehavehelpedMFTaaSvendorsthathavebeenabletoofferrapiddeploymentsfororganizationsthatneedtosolve

Figure 3. Multienterprise/B2B Infrastructure Market Forecast by Segment, 2007-2012

Source:Gartner(June2010)

theirfiletransferissuestodayratherthantomorrow.Weexpectthismarkettocontinuetogrowandassolutionsmature,tocompetemorewithonpremisesMFTvendors.CloudservicesIaaSisexpectedtobethesecond-fastest-growingsegment

B2BIntegrationoutsourcingisalsoexpectedtobeamongthefastest-growingmarketswithasoliddouble-digitCAGRonamuchlargerrevenuebase—nearly$800million——thatwillmakethissegmentthelargestbytheendof2010,displacingmarketgrowththatwouldhaveoccurredinTraditionale-commerceIaaSisdrivenlargelybyITusersthatincreasinglydesiremorefunctionalityfromtheirserviceproviderthanjustB2Btransport.

9

SOAgovernanceforB2Bwillcontinuetoprosper,drivenbytheincreasingadoptionanddeploymentofSOAbutalsobythefactthatitisgrowingfromarelativelysmallinstalledbase.

Multienterprise/B2BgatewayandMFTforB2Bwillcontinuetogrowatasolidpace,outpacing,byamargin,traditionale-commerceIaaS,whichweexpecttodecline,andEDItranslators,whichwepredictwillfaceadramaticfallasstand-aloneproducts.

Themultienterprise/B2Binfrastructuremarketissettochangesignificantlyduringtheforecastperiodintermsofsegmentsizeandpotentiallyvendorweight.AsB2BIntegrationoutsourcing

acquiressizeandvisibility,vendorswilllookatthissegmentwithmoreinterestandmoveintoitwithacquisitionsorlookcloselyatstrategicpartnershipswithB2BIntegrationoutsourcingplayers.

TheTraditionale-commerceIaaSsegmenthashighlyevolvedinthelastfiveyears(forexample,toincorporatein-linetranslationasan“ondemand”capability),butthemostchangeitwillseeinthenextfiveyearswillcomefrommarketconsolidationandimprovedoperationalefficiencies,suchase-invoicing.Traditionale-commerceIaaSwillcontinuetobemorecommonlyleveragedasthetechnologytosupport,andembeddedwithintheserviceportfolioofferingof,thefast-growingB2BIntegrationoutsourcingmarketsegment.

Figure 4. Multienterprise/B2B Infrastructure Market Revenue Growth by Segment, 2009-2014

Source:Gartner(June2010)

10CONTRIBUTING FACTORS TO TRENDSMultienterprise/B2Binfrastructureproductswillcontinuetoseetractioninthemarketbecausemultienterprisecollaborationofallformswillcontinuetoproliferate.Thereareseveraldriversandinhibitorsofthismarket,bothonthetechnologysideandthebusinessside.

Market DriversTechnologydriversincludethefollowing:

• Morecompaniesareadoptingalong-termplantoconsolidatediversemultienterpriseprojectsontoasharedinfrastructure.Thiswilllikelytakeyears,andinsomecases,fullconsolidationisnotevenpossible,butthegeneralapproachisconsistentwithouradviceforconsolidatinginternalintegrationprojectsontoasharedinfrastructure,withsimilarbenefitsandchallenges.BenefitsincludelowerB2Bprojectcosts(fromeconomiesofscale),amore-consistentapproachtodoingintegration,betterprovisioningtools,consistentapplicationofsecuritypolicies,andimprovedandmore-consistentprocessvisibilityandgovernance.

• Themarketisbeinghelpedbytheincreasingmaturityandadoptionofvariousrelatedstandards,suchasXML,SOA,Webservices,portals,GDS,CPFR,RosettanetandeXML.

• Thewholemarketisgettinganincreaseinspendingandaninjectionofinnovationbecauseoftherapidproliferationofcloudservices,andtheneedtointegratethosewitheachother(cloudtocloud)andwithon-premisesapplications.

• SaaScustomersincreasinglyneedtointegratetheirinternalapplicationsdirectlywiththesoftwarefunctionalityavailablefromSaaSproviders.Manycompaniesarebeginningtoshopforasingle-sourcesolutionofB2Binfrastructuredeliveredassoftwareandservices.

Businessdriversincludethefollowing:

• MultienterpriseB2Binquiriesaredrivenbyincreasedcompliancerequirements,suchasthatmandatedbytheU.S.Sarbanes-OxleyAct,theHealthInsurancePortabilityandAccountabilityAct,BaselII,e-invoicingregulationsinEuropeandSouthAmerica,andconcernsaboutconsistentsecurityandauditing.Toprotectthemselvesfromfuturesecurityviolationsandcompliancerisk,companiesareincreasinglyconsideringlimitingtheproliferationofuncoordinatedB2Bprojects.Theynowlookatdeployingacompanywidemultienterpriseintegrationstrategy,perhapsusingaphasedapproachtocontrolcostsandminimizedisruptiontocurrentprojects.

• Themarketisbeinghelpedbymore-visiblebusinessimpact,withcompaniesthataresuccessfulinmultienterprisecollaborationreportingbottom-lineandtop-linerevenueincreasesandcostsavingsattributedtoincreasedautomation,lowercostsandimprovedprocessexecution(visibilityand

control).Thisimprovesbusinesspartnerrelationshipsandattractsnewbusiness,particularlywhenmultienterpriseprojectsincludeprocessmonitoringandintelligence(suchasdatavalidation,compliancemanagement,andsupplierandvendorrelationshipmanagement).

• Multienterprise/B2Binfrastructuredeploymentshaveextensivelyprovedtoincreasetop-linerevenuevianewservicesandcustomers,andincreasedcompetitivedifferentiation.Thereisalreadyasizablenumberofreferenceaccountsofmultienterprisesuccessesacrossregionsandverticalmarketsthathelpdecisionmakersleantowardmultienterprise/B2Binfrastructureadoption.

• Theever-increasinginternationalizationofeconomiesandincreasedinterdependenceoforganizationsoperatingacrossregionsalsohelpsthismarket.

• Therapidadoptionofe-invoicing(especiallyinareaswhereregulationsmandateit)andlogisticsvisibilityisexpandingexistingB2Bprojectsandcreatingnewones.

• OutsourcingofnoncorecompetencieswillincreasinglysustainIaaSuseandgrowB2Bintegrationoutsourcing.SMBscanbenefitfromB2BoutsourcingbecauseB2Bprojectsaregenerallyaresource-intensive,complexITtaskthatcanbecost-effectivelyoutsourcedtoESPs.LargecompaniescanalsobenefitfromB2Boutsourcing,particularlywhenthereisadesiretoapplylimitedinternalITresourcestohigher-priorityinternalITprojects,suchasERPupgradesorCRMprojects,orwhenconsolidatingexisting(frequentlynationallybased)B2Binfrastructures.

Market InhibitorsDespiterecentgains,therearestillinhibitorstoadoptingvariousformsofenterprisecollaboration,whichpressurethemarketnottogrowatthedouble-digitratesseeninthepast.

Technologyinhibitorsincludethefollowing:

• Securityinteroperability(forexample,therearenoubiquitousformsofauthentication)anddifficultiesinintegration(mostinternalapplicationsarestillnot“multienterpriseready”)remainissues.Furthermore,intherushtomarket,manycompanieslookingtointegratevariousinfrastructureandapplicationsalsooverlookthesecurityvulnerabilitiescausedbyboltingtogetherinternalandexternalsystems.

• Technicalcompatibilityisstillanunresolvedissuebecausemostapplicationsarenotinherentlydesignedforcollaboration.

• B2Bstandardsaretoonumerousandstillincomplete,andcustomizationisstillneeded(WebservicesandSOAarenotwidelyusedinB2Bprojects).

11• Masterdatamanagementispoorlyunderstoodinhighly

distributedsystems.

• Therearefearsrelatedtolegalissuesandintellectualproperty(IP)protectioninherentinanyformofcollaboration.Oneaspectofthisistheexposureofsensitiveorproprietarybusinessprocesslogicordatatoexternalbusinesspartners.AnotheraspectofthisisestablishingclearIPownershipforIPimplementedbetweencompanies(suchaswithinanIaaSorB2BIntegrationoutsourcingsolution).

Businessinhibitorsincludethefollowing:

• Theeconomyin2008and2009hitthemanufacturingsectorparticularlyhard;thissectorisastrongconsumerofB2Btechnologies.Although2010issettobetheyearofrecovery,itisanticipatedtobeafairlyslowyearformosteconomicallymatureregionsintheworldinwhichthebulkofmultienterprise/B2Binfrastructurespendingisconcentrated.Atthisstage,theimpactofspendingfromemergingregionsinthismarketisminimalandnotsettoovercomeanycontinuedsluggishperformanceofEuropeortheU.S.Theeconomyremainsacrucialfactorinthefortunesofthismarketovertheforecastperiod.

• Resistancetochangehashurtthemarket,ashastheaversiontowardtheculturaladaptationneededwhenimplementingamultienterprisestrategicdeployment.Departmentalstaffgenerallyresistschange,andinsomecases,keydecision-makingindividualsmighthaveahiddenagendathatwouldbeunderminedbyanyformofopennessandcollaboration.Forexample,thefearofworkforcereductionorlossofcontrolwhenoutsourcingaB2BprojectcouldmakeinternalITmanagersreluctanttooutsourceB2Bprojects(versusimplementingthemin-house).

• Mostcompaniesarestillattheearlystagesofimplementingmultienterprise/B2Binfrastructure,developingbestpracticesfortrustandIPandestablishingmutuallybeneficialincentives,investments,risksandrewards.Thispartneruneasinessshowsitselfalsointheunwillingnesstoinvesttimeandresourcesincollaboration.

• ComparedwiththeirunderstandingofthebusinessvalueofinternalITprojects,ITstaffmembersonB2Bprojectshavelessexperienceofmeasuringandmakingthebusinessvalueofmultienterprise/B2Binfrastructureunderstoodatthemanagementlevel.Realmeasurementsofvalueareofparamountimportance.

• Differentnationalregulationswillstillmakethedeploymentofinternationale-invoicingprojectschallenging:thesolutionofthosechallenges,especiallyfromaBIOperspective,willstillremainoneoftheirmajorsellingpointsintheshortterm(twotothreeyears),whilethedifferencewillsmoothupininternationalmarket.

ANALYSISThemultienterprise/B2Bgatewaysoftwaremarketispoisedtogrowatasteadypaceduringthenextfiveyears.Thismarketofferstheopportunityforvendorsto“gettheirfootinthedoor”ofasegmentoftheAIMmarketthatisamongthefastest-growingandthathassomeofthemostpotential.

Infact,allthemajorintegrationandplatformvendorshaveanarticulatedconsistentandfocusedstrategyofexploitingmultienterprise/B2Bgateways,usedforthemanagementofexchangeddataandprocesses,tocreaterecurringsalesopportunitiesforvendors.Thepresenceoftheirmultienterprise/B2Bgatewaysinacompany’sinfrastructurecouldpresumablycreatevendorpresenceandvendoropportunitytoselllarger,more-expensivetechnologies,especiallynowthatthemegavendorshavestartedtoplayinB2B.ThisiswhywebelievethattheembeddedB2Bgatewayfunctionalitieswithinsuiteswillcontinuetothrive.

Ontheotherhand,stand-alonesolutionswillcontinuetooffergood(andinmanycasesbetter)verticalfunctionalityandexpertise.Unlikeseveralmiddlewaretechnologiesthatarehorizontalinnature(suchasapplicationservers),integrationplatformsareexpectedtocomewithsomevertical“flavor”fromaproductperspectiveandfromago-to-marketapproach.Here,verticalmarketscansignificantlyinfluencethedevelopmentoftheproduct,andsomeindustrieswilldemandthatspecificprotocols(suchasRosettaNetforhigh-techmanufacturing,Odettefortheautomotiveindustry,theChemicalIndustryDataExchange,thePetroleumIndustryDataExchange,theSocietyforWorldwideInterbankFinancialTelecommunication,ACORDforinsuranceandHealthLevel7forhealthcare)beincorporatedinmultienterprise/B2Btransactions.

Multienterprise/B2Binfrastructuretoolscontinuetobeinhighdemandfromorganizationsofeverysize,butparticularlyfrommidsizeandlargecompanies,regardlessofindustrysector,ascompaniescontinuetolookfortheflexibilitynecessarytosupportthemyriadofcurrentandemergingtransportandcommunicationsprotocols,securitystandards,auditingandprocesstracking,andexternalbusinesspartnerprovisioningmechanisms.

Vendor Recommendations

• By2014,weexpectatleastone-thirdoforganizationswithuncoordinatedB2Binfrastructurestore-implementthemascentralizedB2Bgateways(andtwothirdsasBIO).RationalizationoftechnologyandproductswillbeadrivingforceacrossITdepartmentslookingatB2Bprojects.Bepreparedwithcustomerreferencesandacleargo-to-marketstrategythatputsyouasapointofcontactforanycompanylookingattherationalizationoftheirB2Binfrastructures.

• Focusyourvaluepropositiononthebusinessissuesyousolve,suchasimprovingbusinessprocessdiscovery,design,integrationandmanagement,orimprovingoperatingcosts(suchasforsupplychainintegrationprojects)orsolvingmandatorycompliancetospecificregulationsratherthanonthemerefeatureandfunctionalitiesofyourproduct.

12• Newcustomersarestillhardtocomeby,eveninthisgrowing

market,sogiveyourcurrentcustomerbasemoreattentionforbothretentionandupsellingopportunities.Insomeregions,notablyEurope,butalsoSouthAmerica,thismeansnotonlyprovidingbetterlocalizedsoftwarebutalsospecializedsolutionsfortheregionalmarket,intermsofsupportinggeospecificpackages,protocols,standards,regulationsandbusinesspractices.

• Traditionally,multienterprise/B2Bgatewaydealshavebeenreasonablylow-priced,andtheaveragedealsizeisincreasing,althoughmoderately.Focusonmodularofferingsinwhichcustomerscanstartsmallandincrementallybuildwithtime.

• Multienterprise/B2Binfrastructuretechnologyisnowbeingadoptedbymainstreamorganizations,whicharenotasinterestedintechnologyforthetechnology’ssakebutwishtofindsolutionstobusinessproblemsinstead.Vendorsmusthaveasolution-oriented/verticallyfocusedvalueproposition:ThisismostlikelytoincludesomeformofIaaSandBIO.

• Pickaviableandcommittedintegratorforeachlocationandsizeofcompanythatyoutarget.NorthAmericancompaniesprefertousepackagedbusinessapplications,whichtheydonotcustomize.Europeancompaniesprefertouselegacyapplications.WhenEuropeancompaniesbuypackagedapplications,theytendtocustomizethemmore.Asaresult,theinfluenceofserviceproviders,especiallysystemintegrators,ismuchstrongerinEuropethanintheU.S.Regionalspecificandcountry-specificsystemintegratorsarekeychannelstomarketforB2Bsoftware,especiallywhenitcomestotacklingthemidmarket.

• Thecombinationofproliferatingmultienterpriseprojects,differentimplementationapproachestomultienterpriseinteroperabilityandsourcingoptionsiscreatingagrowingmarketsegmentofuserswhowanttoprocuremultienterprise/B2Binfrastructure,includingB2BsoftwareandB2Bservices,fromoneprovider.Despitethistrend,mostcompaniestodaycontinuetoseparatelyprocureB2BsoftwareandB2Bservicesfortheirmultienterpriseprojects(indifferentgeographies).Thus,vendorscontinuetocompeteaggressivelyintheseparateB2Bsoftwareandservicemarkets.Inresponse,savvyB2BvendorsshouldincreasinglyofferahybridB2Binfrastructureportfolio,includingsoftwareandservices,orpartnerwithvendorsofferingacomplementarysoftwareandservicesolutionthattheyaremissingintheirownportfolio.

• Vendorsshouldunderstandthekeytrendsthataredrivingend-userpreferencesfortheirmultienterprise/B2Binfrastructureandbalancetheirproductportfolio,marketingmessageandstrategicalliancesaccordingly.Somekeyissuesinthemindsofendusersinclude:

• TheneedtosynchronizetheirB2Bstrategywiththeirinternalintegrationstrategy,businessprocessmanagementstrategyandapplicationsourcingstrategy.

• Thechallengeofimplementinga“portfolioapproach”toB2Bprojectsbyleveragingmatureandinnovativeapproaches,suchasEDIandSOA.

• ThedecisiontomakeorbuyB2Binfrastructuresolutions.

• TheneedtoconsolidatetheirB2BprojectsontoonesharedB2Binfrastructure—Consolidatebuy-sideandsell-sideprojectsontothesameinfrastructureandconsolidatemultipleVANcontractstoonevendor(andlowertheirrates).Thisdriver,inparticular,ismakingmoreITusersseekaB2BsolutionthatcansupportallformsofB2Binteraction,includingEDIandXML,batchanddiscretetransactions,andsoforth.

• TheneedtoleverageprocessvisibilityandBAMintheirB2Bprojects.

User Recommendations

• Theexpectedmoderateeconomicgrowththrough2014willputpressureonITbudgets.Buyersneedtomastertheirabilitytousetheirmore-containedITbudgets,whichinvariablywillleavelittleroomtomaneuverforexperimentationandforenterprisewidedeployments,aswellasformore-targetedandoftendepartmentalpurchases.

• Vendorsareunderpressurefromincreasedcompetitioninthemultienterprise/B2Bgatewaysoftwarespacecomingfrommegavendors,suiteprovidersandbusinessapplicationvendorsexpandingtheirfunctionalitiesintothisfieldandfromITservicescompaniesofferingalternativewaysofdeliveringB2Bintegration(suchasIaaS).Vendorswillbeeagertoconcludeasaleatatimeinwhichdealsarebecomingfiercelycompetitive;therefore,thepossibilitiesforaskingfordiscountsandfavorablecontracttermshaveincreased.

• Recognizingtheinevitablebusinesspressureposedbycross-companyandbetween-companycollaborationandmatchingittoonesetoftechnologies,insteadofaseriesofprojects,isthefirststepfororganizationstowardaneffectiveandfunctionalB2Bproject.Organizationsshouldestablishwell-setexpectationsfor“justgoodenough”ITandsharedincentivesandriskwiththeirexternalbusinesspartnerswithintheircollaborationnetwork.

• Beawarethatmultienterprise/B2Binfrastructureprojectswillincreasinglyinvolveavarietyoftechnologiesasthe“dumb”networkevolvestobecomea“smart”networkthatincorporatesdiverseintegrationandcollaborationfunctionality,includingcommunications,translation,BPMandcollaborativetools,increasinglyimplementedusinganSOA.Successfulcompanieswillleveragetraditionalandprocessintegration,aswellasSOA,tosolvediverseapplicationintegrationandinteroperabilityrequirements.InternalITinfrastructurewillincludeadapters;datatransformationenginesandETLtools;integrationbrokersandbusinessprocessmanagerstoorchestratemessageflow,Webserviceschoreographyandbusinessprocessexecution;andeventmanagementandalertingfacilitiesforBAM.

13• Recognizethatthefirststepindevelopingaviable

multienterprisestrategyisacknowledgingthatmultiple,autonomousmultienterprise/B2Binfrastructureprojectsanda“onesizefitsall”approachtomultienterprisecollaborationarelong-terminhibitorstodevelopingaholistic,flexibleapproachtodiversebusinessrequirements.Abigchallengeforcompaniesispreventingpreconceivedassumptions—suchas“EDIisdead,”“Webservicesarecool,”or“wecanuseonestandardforallmultienterprise/B2Bcollaboration”—fromunintentionallyhinderingtheimplementationofaflexibleandbalancedapproachtoamultienterprisecollaborationstrategy.

• Organizationsplanningtoembarkintoamultienterprise/B2Binfrastructureprojectshouldemphasizetheskillsandbusinessabilitiesnecessarytohandlesuccessfullyavarietyoftechnologies.

• Bewarethatabigchallengewillbeorganizationalandculturalchange—slowlyelevatingseparatemultienterprise/B2Binfrastructureprojectsfrombeing“whollyowned”bydiscreteITgroupstobeingpartofaholistic,companywide,multienterprisestrategy,andideally,asharedmultienterpriseITinfrastructure,whichcomeswithafreshsetofgovernanceissues.Solutions—intheformofmodernmultienterprise/B2BgatewaysoftwareorasIaaSfrommodernintegrationserviceproviders—canhelpcompaniesconsolidatetheirB2BITinfrastructuresandbettermeettherequirementsestablishedinamultienterprisestrategy.Business-levelmetricsandtheircrediblemeasurementswillhelpbusinessexecutivesestablishalinkbetweenthequalityofexecutionoftheirmultienterprise/B2Binfrastructureprojectsandcompanyprofitability.

• Companieswithinternationalmultienterpriseintegrationrequirementsshouldusetechnologyandservicevendorswithsufficientfunctionality,resourcesanddomainexpertisetomeetdiverse,country-specificmultienterprise/B2Binfrastructureproject-scoperequirements.Thisisparticularlytruefore-invoicing.Usersofsmallermultienterprise/B2Binfrastructuretechnologyprovidersshouldanticipatetheimpactofmergersandfurtherconsolidation.Multienterprisesoftwareandserviceprovidersshouldcontinuetoinvestinexpandingcross-countrymultienterprise/B2Binfrastructureprojectopportunities.

• Nomatterwhatverticalorfinancialshapeyourcompanyisin,lookfore-invoicingprojectsavingsopportunities.Don’twaitforregulationsandinteroperabilitytogetbetter;youcanreapgoodbenefitsfrome-invoicingtoday.

Acronym Key and Glossary Terms

AIM applicationinfrastructureandmiddleware

APS applicationplatformsuite

B2B business-to-business

BAM businessactivitymonitoring

BIO B2Bintegrationoutsourcing

BPM businessprocessmanagement

CPFR collaborativeplanning,forecastingandreplenishment

EDI electronicdatainterchange

ESP externalserviceprovider

ETL extraction,transformationandloading

GDS globaldatasynchronization

IaaS integrationasaservice

IP intellectualproperty

MFT managedfiletransfer

MFTaaS filetransferasaservice

SaaS softwareasaservice

SOA service-orientedarchitecture

VAN value-addednetwork