MARKET PULSE Q2’2016 - Nielsen PULSE Q2’2016 ... Country 2015 2016f China 6.9 6.7 ... Impacted...

12

MARKET PULSE Q2’2016 OPPORTUNITIES IN A VOLATILE MARKET

Transcript of MARKET PULSE Q2’2016 - Nielsen PULSE Q2’2016 ... Country 2015 2016f China 6.9 6.7 ... Impacted...

MARKET PULSE Q2’2016

OPPORTUNITIES IN A VOLATILE MARKET

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

GLOBAL GROWTH REMAINS SLUGGISH, EAST ASIA & PACIFIC IS EXPECTED TO EASE MODESTLY

Note: Europe & Central Asia only includes Developing Countries in the region, Euro Area refers to countries with high income

Source: Global Economic Prospects - World Bank Group (June, 2016)

USA

East Asia & the Pacific 2015 2016f

2.4% 1.9% 2015 2016f

6.5% 6.3%

LAC

2015 2016f

-0.7% -1.3%

MENA

2015 2016f

2.6% 2.9%

2015 2016f

1.6% 1.6%

Euro Area

World: 2.4% (unchanged from 2015)

Country 2015 2016f

China 6.9 6.7

Thailand 2.8 2.5

Indonesia 4.8 5.1

Philippines 5.8 6.4

Vietnam 6.7 6.2 #: Increase vs. 2015

#: Decrease vs. 2015

#: No change vs. 2015

Real GDP % Growth Growth prospects weakened throughout the world economy. World Bank projects global growth for 2016 at 2.4%, unchanged from 2015

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3

MODERATE GROWTH DUE TO IMPACT OF UNFAVORABLE WEATHER CONDITIONS, BUT SERVICE SECTOR IS THE STAR

Source: GSO

6.3 6.7

5.5

0

2

4

6

8

10

H1'15 2015 H1'16

Total GDP

Agri-forestry and fishery

Industry & Construction

Services

GDP % GROWTH Y-O-Y KEY HIGHLIGHTS

INDUSTRY & CONSTRUCTION | 33% GDP Mining industry experienced the deepest plunge

MINING ↓2.2%

driven by CRUDE OIL & NATURAL GAS

↓3.7%

SERVICES | 41% GDP

Services recorded the highest growth in the last 5 years

6.1 6.1

5.8 5.9

6.4

RETAIL & WHOLESALE ↑8.1%

AGRI-FORESTRY & FISHERY | 16% GDP

1st time in many years experienced negative growth (-0.2%) Impacted by the most severe drought in Vietnam in 90 years and salinity intrusion in SCC & MKD.

AGRICULTURAL OUTPUT

↓0.7% vs. YA in H1’16

Forecast: • Rice output ↓1.5% • Rice exports ↓10% • Coffee exports ↓25%

2016 Target: 6.7%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

INFLATION SLIGHTLY UP TICKED BUT REMAIN MODERATE

Source: GSO, World Bank (June, 2016)

CPI H1’16

+1.7% vs. YA

6.7

4.8

0.9 1.7

H1'13 H1'14 H1'15 H1'16

Higher CPI growth vs. H1’15 but still low

-9.4

2.5

2.0

2.4

4.1

17.7

1.7

Transportation

Clothes & footware

Food & food stuff

Beverages & Cigarette

Education

Medicine & Healthcare

CPI

Driven by Healthcare & Education fees, while Food & Beverage remain low

Inflation Composition

“CPI inflation is expected to remain moderate mainly due to soft commodity prices and

stay well below 5 percent mark the authorities are aiming for this year”

– World Bank (June, 2016)

6.8 6.0

1.8

0.6

1.7

2012 2013 2014

2015 H1'16

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

Concern about The state of

Economy jumped +4 pts

vs. last quarter

VIETNAMESE CONSUMERS STILL SHOW POSITIVITY BUT STILL CAUTIOUS

Source: Nielsen Global Survey Consumer Confidence Section (Q1’16), Retailer Sentiment Report Q1’16

104 105 108 109 107

Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

CONSUMER CONFIDENCE INDEX (CCI)

Consumer Confidence Index Calculation • Perceptions of local job prospects • Perceptions of state of personal finances over

the next 12 months • Perceptions of good/bad time for people to buy

the things they want and need over the next 12 months

…BUT THAT DOESN’T MEAN THEY WILL HESITATE TO SPEND

41%

HOLIDAY/ VACATIONS

+5

37%

OUT OF HOME ENTERTAINMENT

+3

*compared versus last quarter

Where do Vietnamese consumers channel their spare cash?

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

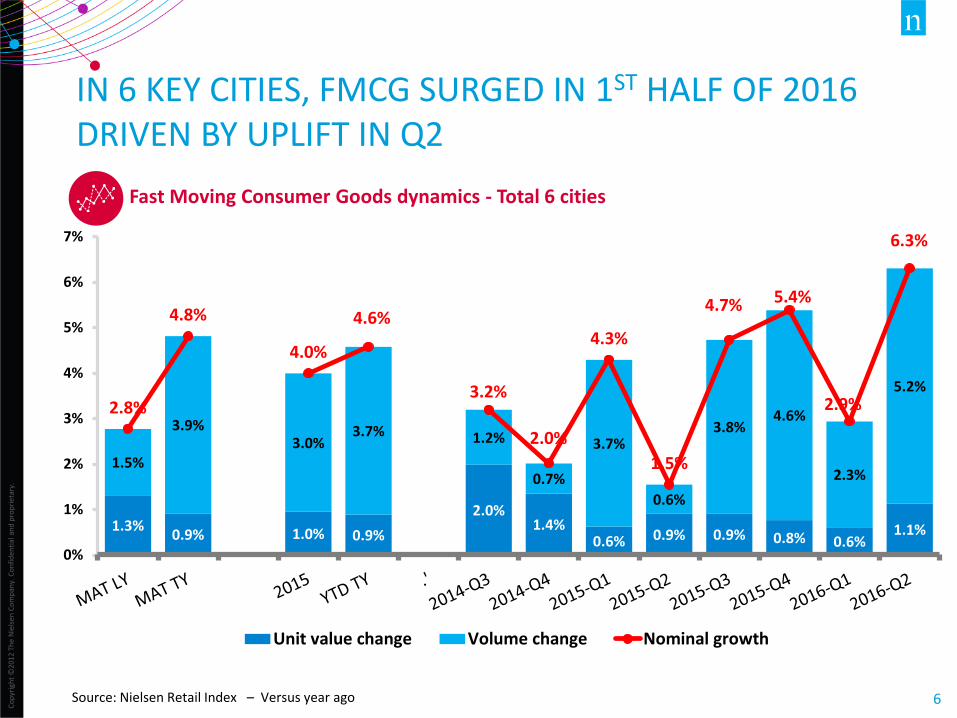

1.3% 0.9% 1.0% 0.9%

2.0% 1.4%

0.6% 0.9% 0.9% 0.8% 0.6% 1.1%

1.5%

3.9% 3.0%

3.7% 1.2%

0.7%

3.7%

0.6%

3.8% 4.6%

2.3%

5.2%

2.8%

4.8%

4.0%

4.6%

3.2%

2.0%

4.3%

1.5%

4.7% 5.4%

2.9%

6.3%

0%

1%

2%

3%

4%

5%

6%

7%

Unit value change Volume change Nominal growth

IN 6 KEY CITIES, FMCG SURGED IN 1ST HALF OF 2016 DRIVEN BY UPLIFT IN Q2

Source: Nielsen Retail Index – Versus year ago

Fast Moving Consumer Goods dynamics - Total 6 cities

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

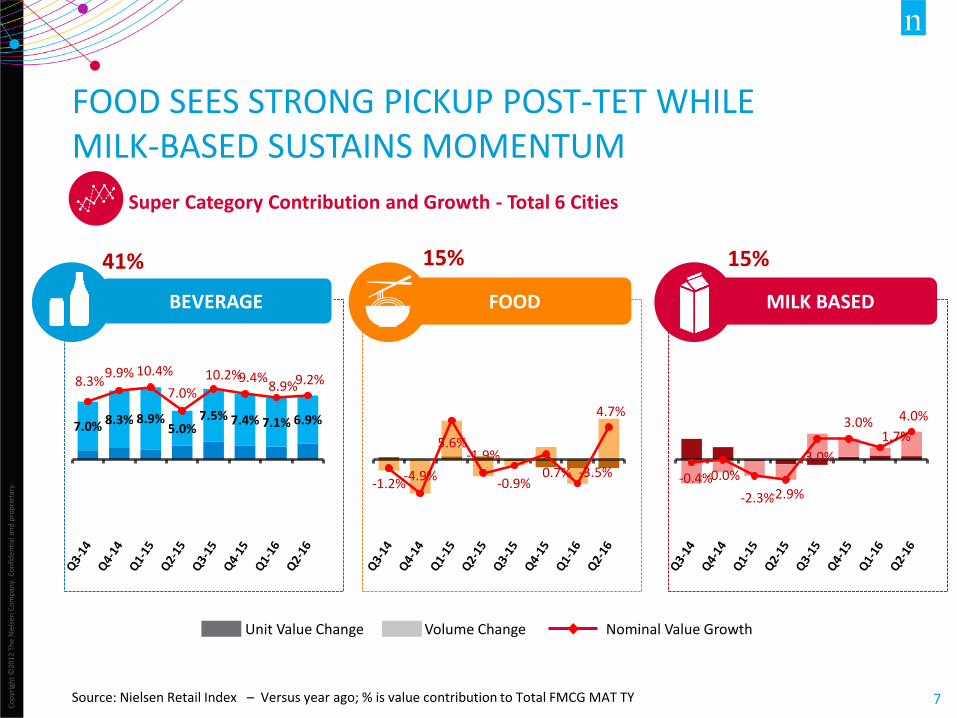

Super Category Contribution and Growth - Total 6 Cities

FOOD SEES STRONG PICKUP POST-TET WHILE MILK-BASED SUSTAINS MOMENTUM

Source: Nielsen Retail Index – Versus year ago; % is value contribution to Total FMCG MAT TY

-1.2% -4.9%

5.6% -1.9%

-0.9% 0.7% -3.5%

4.7% 7.0% 8.3% 8.9%

5.0% 7.5% 7.4% 7.1% 6.9%

8.3% 9.9% 10.4%

7.0% 10.2% 9.4%

8.9% 9.2%

-0.4% -0.0%

-2.3% -2.9%

3.0%

3.0% 1.7%

4.0%

BEVERAGE FOOD MILK BASED

41% 15% 15%

Unit Value Change Volume Change Nominal Value Growth

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

OTHER CATEGORIES HAVE ALSO BOUNCED BACK IN Q2

Source: Nielsen Retail Index – Versus year ago; % is value contribution to Total FMCG MAT TY

4.5%

-0.7% 3.9%

0.4% -0.5% 6.1%

-1.5%

4.6%

5.4%

3.8%

7.5%

2.3% -0.1%

-0.8% -5.6%

2.2%

-2.7%

-4.8% -3.5%

-2.8% 3.1%

6.4% 4.6%

8.1%

0.7%

-10.1%

-11.5%

-6.0%

3.3% 2.7%

-4.7% -4.1%

HOME CARE PERSONAL CARE CIGARETTE BABY CARE

6% 8% 13% 3%

Super Category Contribution and Growth - Total 6 Cities

Unit Value Change Volume Change Nominal Value Growth

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

4.6%

10.3%

4.9% 5.0% 3.8% 1.5%

6.5% 6.8%

10.5% 10.0%

8.7%

14.1%

7.3% 8.1%

7.1%

5.4%

11.7% 10.6%

13.9% 14.3%

FOR THE FIRST TIME, NON-ALCOHOLIC BEVERAGE GROWTH IS SLUGGISH, SHOWING OPPOSITE TREND WITH BEER

Source: Nielsen Retail Index – Versus year ago; % is value contribution to Total FMCG MAT TY

BEER

Unit Value Change Volume Change Nominal Value Growth

Beverages (Soft Drink, Energy Drink, Packaged Water, RTD Tea, Sport Drink, Fruit Juice, Coffee, Tea Bag and Healthy Food Drink)

9.7%

3.2%

9.1% 11.7%

14.4%

8.6% 8.7% 8.1%

3.1% 3.4%

9.9%

3.9%

9.5%

12.0%

14.2%

8.7% 8.7% 8.3%

3.7% 4.1%

NON-ALCOHOLIC BEVERAGE

Super Category Contribution and Growth - Total 6 Cities

22% 19%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

4.4%

5.6% 4.9%

4.3% 5.2%

3.1%

5.5% 5.9%

4.6%

6.3%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Total Urban

Unit Value change Volume change Nominal growth

Fast Moving Consumer Goods dynamics - Urban vs Rural

Source: Nielsen Retail Index – Versus year ago Note: This slide only includes Feminine Protection, Hair Conditioner, Shampoo, Toothpaste, Toothbrush, Personal Wash, Dishwashing Liquids, Fabric Softener, Laundry Products, Bouillon-MSG, RTDM, Soft Drink, Packaged Water, Energy Drink, RTDT, Cigarette, Sport Drink, Sweet Condensed Milk, Fruit Juice , Household Cleaners, Beer, Instant Noodles, Household Insecticide

IN URBAN & RURAL AREA, FMCG SOFTENS THIS YEAR AND SHOWS MUCH VOLATILITY TO BE PREDICTABLE

54% 46%

Rural

Urban

4.0%

7.6%

3.9% 2.2%

6.0% 3.8%

9.3%

9.8%

6.0%

5.6%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Total Rural

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

7.0% 8.3% 8.4% 7.8% 8.6% 3.3% 7.4% 8.7% 6.4% 10.3%

2.8% 3.2% -1.8% -5.2% -3.4% -1.5%

7.7% 9.7% 3.9% 2.3%

6.4% 6.2%

1.0%

4.6%

8.3%

3.4%

6.9% 7.2% 6.7% 5.6%

6.2%

2.9% 4.7%

1.0%

4.1% 6.3%

7.5% 6.8%

3.7% 2.1%

6.2% 6.5% 6.1% 4.5% 5.5%

2.5%

7.8% 9.0% 5.5%

7.5%

FMCG Nominal Value Growth vs. YA by regions

NORTH 25%

CENTRAL 28%

SOUTH 47%

FMCG SOFTENS PARTICULARLY IN NORTH, CENTRAL & MKD DUE TO UNFAVORABLE WEATHER CONDITIONS

Val % SOT – FMCG – YTD TY

S.East (33%)

MKD (14%)

Cold Winter

Salinity intrusion

Drought