Market power mitigation by regulating contract portfolio risk

10

Market power mitigation by regulating contract portfolio risk Bert Willems a,b, , Emmanuel De Corte c a TILEC and Center, Tilburg University, P.O. Box 90153, NL-5000 LE, Tilburg, The Netherlands b CES, K.U.Leuven, Naamsestraat 69, BE-3000 Leuven, Belgium c TILEC, Tilburg University, P.O. Box 90153, NL-5000 LE, Tilburg, The Netherlands article info Article history: Received 7 March 2007 Accepted 5 July 2008 Available online 15 August 2008 Keywords: European electricity markets Market power mitigation Regulation of contracts abstract Abuse of market power by dominant generation firms is a growing concern in worldwide electricity markets. This paper argues that relying only on general competition rules—as is the case in most European countries—is insufficient and that complementary ex-ante regulation is needed. In particular, regulators should incentivize firms to sign contracts with retailers by regulating their risk exposure. In a simulation model we show that this type of regulation can significantly reduce the deadweight loss in the market, without imposing large costs on regulatees. & 2008 Elsevier Ltd. All rights reserved. 1. Introduction The guiding principle of the European electricity liberalization 1 is to split the electricity market in four separate sectors: power generation, transmission, distribution, and retail. As the genera- tion and retail sectors are considered viable for competition, they are not regulated and subject to general competition rules (and consumer protection rules as far as the retail sector is concerned). The transmission and distribution sectors are regarded as natural monopolies that require regulation. 2 Ten years after the opening of the electricity markets, the results of the liberalization are mixed. Some progress has been achieved, but a competitive internal market for electricity has not (yet) developed. This paper suggests that the European legislator should not solely rely on general competition rules to address market power in the generation sector, but also introduce a new form of ex-ante regulation: it needs to regulate the risk of generators by imposing a capital adequacy requirement. With the capital adequacy requirement, firms will improve their hedging position and sell more through contracts. This type of ex-ante regulation has the following advantages: It reduces market power and complements the existing competition rules. It does not destroy economic incentives for production and investments decisions, unlike more direct forms of regulation by—for instance—a price cap. It might have additional benefits by increasing the security of supply of the electricity system. The structure of the paper is as follows. Section 2 explains why generation market power exists in the EU and why standard competition rules are largely insufficient in the electricity sector. We then argue that an US approach of micro-regulation of generators should not be followed in Europe, and suggest a third approach, which is based on the regulation of contracts. Section 3 proposes to impose a capital adequacy requirement on generation firms. We then develop a dynamic model of contract regulation (Section 4) showing that market power is reduced, without imposing a large burden on generation firms (Section 5). The paper finishes with practical considerations and conclusions (Sections 6 and 7). 2. Problem description and literature review 2.1. Market power in the European electricity market Two technical characteristics inherent to electricity markets make market power abuse particularly attractive. These are the non-storability of electrical energy and the low demand elasticity. Both properties make unilateral withholding of production output highly profitable for firms. Even in relatively un-concentrated markets, relatively small players can find it profitable to withhold output and consequently drive up prices. 3 ARTICLE IN PRESS Contents lists available at ScienceDirect journal homepage: www.elsevier.com/locate/enpol Energy Policy 0301-4215/$ -see front matter & 2008 Elsevier Ltd. All rights reserved. doi:10.1016/j.enpol.2008.07.008 Corresponding author. Tel.: +31134662588. E-mail address: [email protected] (B. Willems). 1 The internal market for electricity was conceived in 1996, with the European Directive 96/92/EC and further specified in a follow-up directive 2003/54/EC (EU Commission, 1997, 2003a). 2 Generation is the production of electricity, transmission is the high-voltage transmission of energy, distribution is the low-voltage distribution of energy and retail is the sale of energy to small end-consumers. 3 The characteristics of the electricity market not only make the unilateral abuse of market power profitable, but could also encourage tacit collusion. Homogenous products, certain demand evolution, and repeated interactions are electricity market characteristics that could make tacit collusion more likely. Energy Policy 36 (2008) 3787–3796

-

Upload

bert-willems -

Category

Documents

-

view

214 -

download

2

Transcript of Market power mitigation by regulating contract portfolio risk

ARTICLE IN PRESS

Energy Policy 36 (2008) 3787–3796

Contents lists available at ScienceDirect

Energy Policy

0301-42

doi:10.1

� Corr

E-m1 Th

Directiv

(EU Com2 G

transmi

retail is

journal homepage: www.elsevier.com/locate/enpol

Market power mitigation by regulating contract portfolio risk

Bert Willems a,b,�, Emmanuel De Corte c

a TILEC and Center, Tilburg University, P.O. Box 90153, NL-5000 LE, Tilburg, The Netherlandsb CES, K.U.Leuven, Naamsestraat 69, BE-3000 Leuven, Belgiumc TILEC, Tilburg University, P.O. Box 90153, NL-5000 LE, Tilburg, The Netherlands

a r t i c l e i n f o

Article history:

Received 7 March 2007

Accepted 5 July 2008Available online 15 August 2008

Keywords:

European electricity markets

Market power mitigation

Regulation of contracts

15/$ - see front matter & 2008 Elsevier Ltd. A

016/j.enpol.2008.07.008

esponding author. Tel.: +31134662588.

ail address: [email protected] (B. Willem

e internal market for electricity was conceive

e 96/92/EC and further specified in a follo

mission, 1997, 2003a).

eneration is the production of electricity, tran

ssion of energy, distribution is the low-voltag

the sale of energy to small end-consumers.

a b s t r a c t

Abuse of market power by dominant generation firms is a growing concern in worldwide electricity

markets. This paper argues that relying only on general competition rules—as is the case in most

European countries—is insufficient and that complementary ex-ante regulation is needed. In particular,

regulators should incentivize firms to sign contracts with retailers by regulating their risk exposure. In a

simulation model we show that this type of regulation can significantly reduce the deadweight loss in

the market, without imposing large costs on regulatees.

& 2008 Elsevier Ltd. All rights reserved.

1. Introduction

The guiding principle of the European electricity liberalization1

is to split the electricity market in four separate sectors: powergeneration, transmission, distribution, and retail. As the genera-tion and retail sectors are considered viable for competition, theyare not regulated and subject to general competition rules(and consumer protection rules as far as the retail sector isconcerned). The transmission and distribution sectors areregarded as natural monopolies that require regulation.2

Ten years after the opening of the electricity markets, theresults of the liberalization are mixed. Some progress has beenachieved, but a competitive internal market for electricity has not(yet) developed.

This paper suggests that the European legislator should notsolely rely on general competition rules to address market powerin the generation sector, but also introduce a new form of ex-anteregulation: it needs to regulate the risk of generators by imposinga capital adequacy requirement. With the capital adequacyrequirement, firms will improve their hedging position and sellmore through contracts. This type of ex-ante regulation has thefollowing advantages:

�

It reduces market power and complements the existingcompetition rules.ll rights reserved.

s).

d in 1996, with the European

w-up directive 2003/54/EC

smission is the high-voltage

e distribution of energy and

�

abu

Hom

elec

It does not destroy economic incentives for production andinvestments decisions, unlike more direct forms of regulationby—for instance—a price cap.

� It might have additional benefits by increasing the security ofsupply of the electricity system.

The structure of the paper is as follows. Section 2 explains whygeneration market power exists in the EU and why standardcompetition rules are largely insufficient in the electricity sector.We then argue that an US approach of micro-regulation ofgenerators should not be followed in Europe, and suggest a thirdapproach, which is based on the regulation of contracts. Section 3proposes to impose a capital adequacy requirement on generationfirms. We then develop a dynamic model of contract regulation(Section 4) showing that market power is reduced, without imposinga large burden on generation firms (Section 5). The paper finisheswith practical considerations and conclusions (Sections 6 and 7).

2. Problem description and literature review

2.1. Market power in the European electricity market

Two technical characteristics inherent to electricity marketsmake market power abuse particularly attractive. These are thenon-storability of electrical energy and the low demand elasticity.Both properties make unilateral withholding of production outputhighly profitable for firms. Even in relatively un-concentratedmarkets, relatively small players can find it profitable to withholdoutput and consequently drive up prices.3

3 The characteristics of the electricity market not only make the unilateral

se of market power profitable, but could also encourage tacit collusion.

ogenous products, certain demand evolution, and repeated interactions are

tricity market characteristics that could make tacit collusion more likely.

ARTICLE IN PRESS

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–37963788

In its sector enquiry (EU Commission, 2007) the EuropeanCommission shows that there is a potential abuse of marketpower in the European Union. The Commission clearly stated in itsenquiry that: ‘‘Analysis of generation portfolios also shows that the

main generators have the ability to withdraw capacity to raise

prices.’’ It identified several structural problems, leading toinadequately functioning European energy markets. These hurdlesare among others:

�

pol

A ‘significant level’ of concentration in the generation segment.

� An inadequate level of unbundling at network and supply level.In the electricity markets, transmission assets are oftendirectly or indirectly in the hands of a limited number ofsuppliers, decreasing the essential market input.

� A fundamental lack of sufficient interconnection capacity overwell-known bottlenecks. In the absence of sufficient intrastategeneration capacity, a lack of interstate import capacity onlyadds to the problems already present in the market.

Empirical evidence of the impact on prices resulting from apartial or complete withdrawal of generation capacity can befound in the same sector enquiry. The European Commission usesthe example of the generation markets in Germany and France toindicate how the main generators can indirectly but easilyinfluence price levels just by varying the number of utilizationhours of their power plants (EU Commission, 2007, part II, p. 146).

6 COMP / M.3268-Sykdraft/Graninge.7 See also COMP/M 2890, EDF/Seeboard of 25/07/2002, COMP/M 3007 EON/TXU

Europe Group of 18/12/2002, COMP/M 3268 SYDKRAFT/Graninge of 30/10/2003,

COMP/M 3440 ENI/EDP/GDP of 09/12/2004, COMP/M 3696 EON/MOL of 21/12/2005,

COMP/M 3729 EDF/AEM/Edison of 12/08/2005 and COMP/M 3867 Vattenfall/Elsam

and E2 Assets of 22/12/2005.8 For an example at European level see European Commission, COMP/M 2684

2.2. Traditional anti-trust approach does not work

The European Union relies on standard competition rules todeal with abuse of market power in the generation sector. For thisit relies on Article 82 of the treaty.4 Article 82 prohibits the abuseof a dominant position. A firm with a dominant position can bepunished if it is proven to engage in anti-competitive practicessuch as bundling, price discrimination, predatory pricing, rebates,etc. At pan-European level, the Commission monitors theapplication of the prohibition rules under Article 82 EC andtherefore has been given the power to investigate and imposefines. Since May 2004, the national courts have also beenempowered to apply the rules under Article 82 EC.5 The imposedremedy will typically consist in measures to stop certain practices,impose some regulation or, in extreme cases, an obligation to splitup a firm.

Competition policy has not worked well in the electricitysector. Until now very few cases have been brought to courtaddressing the abuse of a dominant position in the electricitysector. An example of a procedure related to the implementationof the European competition policy under Article 82 EC wherebyproducers partly withdraw production assets to generate priceincreases, can be found in a notice of the EU Commission (2008)which states:

According to the preliminary assessment E.ON is, together withRWE and Vattenfall, collectively dominant on the Germanelectricity wholesale market. The preliminary assessmentexpressed the concern that E.ON may have abused itsdominant position according to Article 82 of the EC Treaty bywithdrawing available capacity (deliberately not offering theproduction of certain plants which were available andeconomical to run) with a view to raising electricity prices to

4 Article 81 is part of the EU-treaty and form the basis of EU-competition

icy (EU Commission, 2002).5 EU Commission (2003b) Article 6.

the detriment of consumers and by deterring third parties frommaking new investments in electricity generation.

Even as the example mentioned above points towards the rightdirection, much more could be done to eliminate abuse of adominant position. There are several reasons for this lack ofactivity under Article 82 EC.

Firstly, Article 82 only applies when a firm is dominant. Legally,this is the case when a firm has the largest market share in therelevant product market.

The relevant product market to evaluate abuse of a dominantposition in the generation segment is described as the wholesale

supply market. This market is best described as the electricitythat is generated locally and is imported over the so-called‘interconnectors’.6 This approach has been reconfirmed inseveral cases.7 From an economic and technical viewpoint thedetermination of relevant markets in a meshed network asthe national markets of each member states is howeverquestionable, as it does not take into account loop-flows, whichcan amplify market power, and internal congestion patternswithin member states that might divide a country in separatesub-markets.

The criterion of market share in a relevant product market iscommonly used as a measure of dominance. When appliedto the electricity sector however, this criterion faces someproblems, due to the specific characteristics of this market.Solely relying on market share as criterion is therefore not anoption. For this reason, the European Commission, in its 2007Sector Inquiry adds the criteria of influence on the PowerExchange (exteriorized by the possibility of imposing excessivepricing) and the generation segment (by partially or totallywithdrawing generation capacity) as two alternative and addi-tional criteria.

The underlying assumption of the dominance criterion is thatfirms which are not-dominant are unable to exercise marketpower. However, the technical characteristics of the electricitysector make it possible for relatively small players to abusemarket power. Wolak (2003b) shows for instance that unilateralmarket power in California can explain the substantial priceincreases in the summer of 2000. Hence, even if firms do not havea dominant position in the strict legal sense, they might be able toabuse market power. An additional problem is that legally firmswill only be dominant, if they are able to sustain their position fora considerable amount of time. In the electricity market, however,it is likely that market power abuse presents itself only duringshort periods of super peak demand in small geographical areas.8

These abuses might have very large economic effects, but are notalways recognized as such by judges.

Secondly, it is hard to legally define ‘‘abuse’’ in the electricitysector. In contrast with other sectors, abuse of market power is notalways related with specific practices, but rather with selling too littleat too high prices, or taking too much time for maintaining a plant.Excessive pricing is prohibited by Article 82(a) but the jurisprudenceis very limited.9 Furthermore, if markets are badly designed andregulation creates arbitrage opportunities which should not exist in

EnBW/EDP/Cajastur/Hidrocantabrico of 19/03/2002. Examples at national level in

the Netherlands can be found in NMa, Case 3386, Nuon/Reliant Group of 21/01/2005;

NMa, Case 6015 Nuon/Essent of 21/05/2007.9 In 40 years of European competition policy, only four cases of excessive

pricing have been brought to court (Motta and de Streel, 2003)

ARTICLE IN PRESS

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–3796 3789

well-designed market, firms should not be held accountable formaximizing profits and arbitraging away price differences.10

Thirdly, oftentimes a judge cannot effectively impose anefficient remedy to deal with market power: structural remediesmight not be available. It might be too hard to forbid firms toforbid certain practices. The only feasible remedy might in thosecases be to impose some form of regulation. Judges are, however,not very keen in taking up the role of a regulator. In severalEuropean countries, VPPs were used as a mean to increasecompetition. Examples can be found in France,11 Belgium,12 Italy,Denmark, and the Czech Republic.

Fourthly, the judicial process if often too slow to deal withmarket power in the electricity sector. One cannot allow firms toabuse their positions for several years until a judge will rule. Suchongoing abuse might destroy the trust in the liberalized markets,and it might be hard to undo the transfers to market power abusewhich went on for years. The size of these transfers is a lot largerthan in most in other sectors.

These four aspects, which are very specific for the electricitymarket, render ex-post competition policy useless but for themost blatant abuses.

2.3. Complementing competition policy: market monitoring

In order to overcome some of the problems with ex-postregulation mentioned above, the EU Commission (2003a) obligesmember states to monitor their wholesale market for electricity.The role of the regulator13 now extends beyond the regulation oftransmission and the distribution sector, and includes monitoringthe generation market. This regulator receives, however, noadditional instruments to influence the generation market.

The monitoring process might improve ex-post competitionpolicy. On the one hand, monitoring improves the transparency ofthe market, by collecting data. This might increase the detectionrate of abuses by generators. On the other hand, monitoring alsointroduces a form of pseudo-regulation. While monitoring theregulator will define relevant markets, test which products aresubstitute and which are supplements, create indicators formarket abuse, determine which players are dominant, etc. Thisform of pseudo-regulation might help competition policy, as itcreates a framework to define Article 82 cases.

This pseudo-regulation can result in several problems:

�

flow

me

as a

Com

offe

ma

Eur

spe

aut

sep

Me

sur

aut

dur

foll

bed

Generators do not receive full legal certainty as courts orcompetition authorities may disagree with the sector regula-tors’ viewpoints.14

10 Firms might for instance profit from the disconnection of physical network

s and the virtual contract relations.11 In France, the VPPs were introduced by EDF as a result of the planned

rger between EDF and EnBW. EDF made the undertaking to enter into the VPPs

mean to get approval for the merger by the European Commission.12 In Belgium, VPPs were introduced by decision of July 3, 2003 of the

petition Authority (Conseil de la Concurrence), whereby Electrabel agreed to

r, under a VPP-regime, 1200 MW. See: http://economie.fgov.be/organization_-

rket/competition/press_releases/press_release_07072003_fr.pdf.13 One should keep in mind that regulatory structures vary greatly between

opean countries. In some countries, for instance the Netherlands, the sector

cific regulator Dte (now called ‘Energiekamer’) is integrated in the competition

hority (NMa), whereby in other countries (for instance Belgium) there are two

arate entities (one competition authority, Conseil de la Concurrence/Raad voor de

dedinging) and one energy sector regulator, CREG) with some form of cooperation.14 During the Nuon–Reliant merger in the Netherlands, disagreements

faced with regard to the definition of relevant markets. The competition

hority NMa argued that the merged firms would obtain a dominant position

ing periods of peak demand, but the appeals court College van Beroep did not

ow them in their reasoning. Decision LJN AZ3274, College van Beroep voor het

rijfsleven, AWB 05/440 of November 28, 2006.

�

Pow

the

req

to p

Moreover, regulators might also change measures of marketpower over time, creating additional time-related uncertaintyfor firms.

� In the monitoring process, regulators might over-emphasizecertain indicators which are not necessarily related to under-lying market fundamentals. For instance, a measure of thelength of time a generator sets the clearing price is probablynot a meaningful indicator for long-term market power, if itexcludes information on production costs, long-term contracts,competition in the retail market, etc.

Although monitoring might improve the efficiency of ex-postcompetition policy, it does not solve the drawbacks mentioned inthe previous sub-section. Ex-ante regulation of generation firmstherefore remains necessary. Most US electricity markets rely onex-ante regulation of the generation market. The next sub-sectiondiscusses the lessons we can draw from this experience.

2.4. Can we draw lessons from the US?

The regulatory framework in the US is very different from theEuropean one. Although electricity markets were liberalized, inthe sense that firms could freely trade and wholesale prices areset on an exchange; FERC, the federal electricity regulator,remained legally responsible for regulating the whole sector,including the generation sector.15

US markets are mostly organized around mandatory powerexchanges (spot markets) in which all generators need toparticipate. Transactions in these spot markets are typicallyregulated. Such regulation can take the form of bid caps or pricecaps. A price cap puts an upper limit on the clearing price themarket can achieve and are present in most power markets. Thecaps are set administratively by the regulator; however, ‘‘softwareconstraints’’, set by power exchanges, also limit prices. Bid caps

restrict the generators’ bid prices but do not restrict the clearingprice of the market. These bid caps can be different for differentplayers and generation plants. Often, they are based uponestimates of the marginal costs of the generator or on historicalbidding of that plant.

Compared with ex-post regulation, spot market regulationmight reduce legal uncertainty, as rules are clearly specified, andallows the regulator to directly intervene in the market to addresspotential market power abuse. It might be very effective inkeeping prices down.

The major drawback of spot market regulation16 is its tendencyto destroy incentives for both the generators and consumers,thereby hindering the development of an efficient electricitymarket. Price caps destroy economic incentives for consumers andgenerators as prices do not reflect scarcity in periods of peakdemand. Consumers do not reduce their consumption and willconsume more than the efficient amount. Generators do not havean incentive to produce during scarcity. For example, they havethe wrong incentives to schedule plant maintenance and may shutdown when they are most needed. Price caps therefore forcenetwork operators to sign bilateral contracts with generators athigher prices to avoid black-outs. Extra regulation is needed toaddress investment problems as prices are too low on average tocover investment costs. Bid caps, on the other hand, limit theplayers’ bids while allowing the free movement of the spot price

15 The FERC, established in 1977, was given legal authority by the Federal

er Act (FPA). The powers given to the federal regulator were later extended by

Energy Policy Act of 2005.16 A complication of spot market regulation (price and bid caps) is that it

uires a well functioning and liquid spot market, in which generators are obliged

articipate. Such markets are currently not available in every European country.

ARTICLE IN PRESS

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–37963790

to clear the market. It has certain advantages over price capregulation. Clearing prices are high during peak demand reflectingthe scarcity of electrical energy. This gives generators the rightincentive to produce electricity during peak periods. Alsoconsumers, in some cases, reduce consumption to avoid payingthe high peak periods prices. The downside is that bid caps do notparticularly reduce market power. To be effective, bid caps shouldbe combined with quantity regulation, which obliges players tobid into the market. This prevents generators from withholdingcapacity and increase prices not by bidding higher prices, but bybidding less.

Spot market regulation might further destroy true marketcompetition as firms game regulatory rules, it hampers innova-tion, and it requires costly, continuous monitoring of the actionsof the firms involved.

3. Contract regulation as a remedy for market power

Both the European system, which relies almost exclusively onex-post competition policy, and the US system, which relies onheavy-handed regulation of mandatory spot markets, have draw-backs. This paper suggests using an alternative regulatorymechanism, complementary to competition policy. We proposethat the regulator regulates the contracts signed betweengenerators and retailers in order to reduce the incentives ofgenerators to exercise market power in the spot market.

These contracts can be plain forward contracts, where retailershave the right and the obligation to take off a fixed quantity at afixed prices from the generators, but also call options, whereretailers have the right but not the obligation to consume a certainquantity at a fixed price, the ‘strike price’.

If the regulator can induce the generators to sell moreelectricity forward, it might be able to reduce market power:generators selling forward contracts to retailers have an incentiveto behave more competitively in the spot market. This is becausegenerators will only compete for the un-contracted retail market.Firms have fewer incentives to drive up prices as they compete forsmaller quantities. This is generally true and is independent of thetype of competition in the spot market.17 This intuition also holdswhen the generator sells electricity with other financial productsthan forwards, such as call options (Willems, 2006).

Compared with spot market regulation, this contract regula-tion has several advantages:

�

(20

Firstly, it does not destroy the short-term production decisionsof generation firms and consumers. A contract will givegenerators the incentive to be available during peak demandperiods. At the same time consumers have the incentive toreduce their consumption when the spot price is high.

� Secondly, generators will receive financial contributions tocover their fixed investment costs if the contracts are sold in acompetitive market. Hence the contracts do not destroy long-term incentives to build new generation capacity. With a pricecap, the firms would not receive such a contribution to theirinvestment costs.

� Thirdly, contracts confer regulators certainty to generators. Forthe contract duration, players are fully knowledgeable of theconditions under which electricity will be supplied. With a pricecap regulation, the cap might be changed at will by the regulator.

� Fourthly, the price of a contract might reflect the costs of theimposed regulatory rule, which allows the design of an optimal

17 See Allaz and Vila (1993) for results with Cournot and Mahenc and Salanie

04) for Bertrand competition.

ene

ma

regulatory system. The cost of regulation is not directlyobservable, for example, when price caps are imposed on themarket.

� Fifthly, contracts might help regulators to commit to a certainregulatory strategy. Such a commitment is ideal to prevent theregulator from exercising too much discretionary power. Theinability to commit will lead to a ratchet effect, which willreduce efficiency (Sappington, 1980).

� Sixthly, contract regulation can be applied in markets such asthe European ones, where mandatory wholesale power poolsdo not exist. Without the obligation to sell through a singlepower exchange, bid and price caps cannot work.

� Seventhly, contracts can exactly reproduce the effect of a bid capfor consumers. If generators sell a call option with a strike priceequal to the bid cap, then these contracts can mimic the effect ofa bid cap without destroying the short-term production decisionsand the long-term investment incentives. The call option behavesas an implicit price cap in the spot market. If a generator bids ahigher price than the strike price, then it will receive a higherprice from the spot market for its energy, but it will have to payout more money for the call option it has sold.

Contract regulation is therefore a promising new strategy toregulate market power. Different approaches to regulate thecontract positions of firms can, however, be envisioned. Severalapproaches, some of them more workable than others, arediscussed in the following sub-sections.

3.1. Additional demand (or supply) for contracts

One potential method for regulating contracts is one in whichthe regulator obliges the network operator to create an extra

demand for forward contracts, i.e. the network operator buys extracontracts on the contract market. It could, for instance, buy‘‘physical’’ contracts for energy, which are backed up by physicalgeneration capacity, on behalf of the consumers and resell theenergy on the spot market. By obliging the system operator to buycontracts, the regulator might try to increase the amount ofcontracts sold by generators, and reduce abuse of market power.18

We could think about this type of regulation as a three stageprocess. First, the regulator decides the amount of physicalcontracts the system operator should buy on the contract market.Then generators decide simultaneously the amount of (physical)contracts they sell. They compete until they cover the full demandof the network operator. Generators do not only sell physicalcontracts to the regulator, but at the same time they sign bilateralcontracts with retailers, and take positions in financial contracts.In the last stage of the game, the spot market operates: generatorsdecide about their production level, the network operator resellsthe capacity it contracted in the spot market, and retailers buyelectricity in the spot market.

When arbitrage is working well, financial and physicalforwards are equivalent, and have identical strategic effects onthe spot market (Willems, 2006). Hence what matters for theeffect of the regulatory intervention is the total amount ofcontracts which each firm sold, but not the exact distributionbetween contracts sold to the regulator, final consumers andarbitrageurs.

If the financial markets are sufficiently complete and liquid,19

generators are able to adjust their contracting portfolio and offset

18 The Colombian electricity market will introduce such a regulated forward

rgy market (Cramton, 2007).19 Market completeness has not been studied extensively in the electricity

rket. See also Willems and Morbee (2008).

ARTICLE IN PRESS

22 Wolak (2001a) suggests obliging incumbent generators to sell hedge

contracts at regulated prices. He states that ‘‘it is an open question what the

optimal sequence is for reducing the levels of these vesting contracts over time and

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–3796 3791

their commitments in physical contracts vis-a-vis the regulator. Inparticular they will reduce the amount of financial contracts theyare selling to speculators and the bilateral contracts to retailers inresponse to the extra demand of the regulator. Hence, there isperfect crowding-out of private contracts, and there is no neteffect of the regulator buying contracts.

An alternative method of regulation is one where theregulator tries to create extra supply of contracts, by obliginggenerators to auction off a number of standardized contracts.For instance, the regulator can order firms to sell so-called virtualpower plants.20 The sale of these virtual power plants will,ceteris paribus, make the generation firms more competitive inthe spot market. In reaction to this regulation, the firms will,however, adjust their contracting portfolio, by reducing theamount of unregulated contracts they sell. Also now generatorswill be able to completely undo the actions of the regulator, aslong as financial markets are sufficiently liquid and sufficientlycomplete.

In other words, if a regulator wants to regulate contracts tomitigate market power, it should regulate all contracts generatorscan sign. It is not sufficient to regulate only a sub-set of thecontracts. Contract regulation should in particular be concernedwith financial transactions which could be used to offset thestrategic effects of regulated contracts. As these financial transac-tions can be very complex, are not readily observed, and need notto be restricted to standard forward contracts, careful considera-tion should be given to their evaluation.

However, if the portfolio of contracts signed by a firm iscomplex, then regulating each individual type of contractseparately would become a gargantuan task for the regulator.We therefore suggest that the regulator should, instead, regulatethe contract risk exposure of firms. The next section looks at thisform of regulation.

3.2. Regulating risk exposure

Above we reasoned that the regulator should regulate thecomplete contracting portfolio of the generation firms in order toreduce the abuse of market power.

Hedging contracts, which reduce the firm’s risk, lessen ingeneral the incentives for market power abuse, whereas spec-ulative contracts, which increase a firm’s risk, tend to encourageabuse. The link between a portfolio’s riskiness and its strategiceffect is however not perfect, and should only be used with care.

The regulatory mechanism that we propose is that the regulatorsgive generation firms an incentive to reduce their exposure to thespot market. This implies that generation firms have to signcontracts with retailers to cover part of their production.21

This new approach entails a different position for the regulator.Two main conditions should be present in order to make thecontract regulation work. These are:

how the prices of these contracts should change if their level is reduced.’’ In our

model, forward prices and contract quantities adjust automatically to changing

market situations.

�com

ma

gen

con

our

23 The Italian regulator obliged ENEL, the incumbent generator, to increase its

sale of electricity by contracts, because it had a dominant position in the Italian

spot market, i.e. the un-hedged sales were very large (Deliberazione 7 ottobre 2005,

Misure per la promozione della concorrenza nel mercato all’ingrosso dell’energia

Extend the powers given to the regulator so that they alsoinclude regulation, thorough surveillance of all contractssigned by the generators. These competences go together withpossibilities to intervene, directly or indirectly.

� elettrica per l’anno 2006, deliberazione n. 212/05, Autorita Per l’Energia Elettrica e ilGas). As a penalty it threatened ENEL with a forced divesture of generation

A direct and unlimited access to all contracts, granted to theregulator.

20 Virtual power plants are standardized call options which have been used by

petition authorities as part of merger review processes.21 In order to cope with abuse of market power in the California energy

rket, the market surveillance committee (MSC) advised FERC to oblige

erators to sell 75% of their expected annual sales in the form of 2-year forward

tracts at regulated prices (Wolak, 2001b, 2003a; Wolak and Nordhaus, 2001). In

paper we assume that the forward prices are not regulated.

This regulation does not specify strict targets for eachgenerator, but specifies targets relative to their market shares,and if firms do not achieve their target contract quantity, firmswill have to pay a penalty. By making the contract quantitiesendogenous, the regulation automatically takes into account theheterogeneity of firms and accommodates for changes in theindustry through time.22

The penalty that firms have to pay might be explicit, a fine fornot achieving a target, or, more likely, an implicit penalty withincreased costs for under-contracting firms.23 An example of suchimplicit penalty is the imposition of capital adequacy require-ments on firms.

With this requirement, the regulator intends to ensure that firmsare financially healthy and have a sufficient amount of liquid assetsto deal with unexpected events. One way to achieve this is to obligefirms to hold capital commensurate with the level of risk in theirportfolio. A crude measure of a portfolio’s risk is the un-hedgedposition of a firm, equal to the difference between quantities sold inthe spot market and the contract market. A capital adequacyrequirement forms an implicit penalty for under-contracting, asfirms incur the opportunity cost of holding capital.

Several papers studied the contracting decisions of oligopolis-tic firms, but our paper is the first to study how a regulator mighttry to change contracting incentives of firms. The main result ofthe literature on endogenous contracting is that firms might usecontracts as a commitment device. By signing contracts, playerscan influence the equilibrium in the spot market and increasetheir overall profit. The precise strategy depends on the type ofcompetition. If generators compete a la Cournot, then they willsell forward contracts to compete more aggressively in the market(Allaz and Vila, 1993), which increases their market share at theexpense of the other participants. On the other hand, if generatorscompete a la Bertrand, then there is an incentive to buy forwardcontracts, i.e. to speculate, and commit to being less aggressive(Mahenc and Salanie, 2004).24 Hence, strategic contracting willmake Cournot markets more competitive and Bertrand marketless competitive. This paper builds upon the Allaz and Vila (1993)model and complements their model with contract regulation.

4. Model

4.1. Model description

This paper develops a two-stage game to model the effect ofcontract regulation on the strategic behavior of firms. Fig. 1sketches the two stages of the game.

capacity. The decision was later blocked by court, but in a subsequent procedure of

the competition authorities under Article 82. ENEL settled by selling 1000 MW of

long-term contracts.24 Newbery (1998) studies the case where firms compete with supply

functions. He shows that if firms coordinate on the high price equilibrium, they

will sell contracts, and make the spot market more competitive. Green (1999)

conducts a more detailed analysis and shows that if firms compete in linear supply

functions in the spot market, and have Cournot conjectures in the forward market,

then firms will not sell contracts. Harvey and Hogan (2000) review these results.

ARTICLE IN PRESS

Stage 1Market Design Period 1

Stage 2

Period t

Generator i sellsqi

1 in spot marketki

1 in contract market

Regulator sets-Procedure to Evaluate Risk-� Penalty Paramter

Generator i sellsqi

t - kit−1 in spot market

kit in contract market

Period T

Generator i sellsqi

T -kiT−1 in spot market

.….…

Time

Fig. 1. Two-stage game with regulated contracts.

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–37963792

In the first stage, the regulator designs a regulatory frameworkthat is aimed at inducing firms to increase their contract cover, i.e.to sell more on the forward market and less on the spot market.More in particular, the regulator will impose a penalty on firmswhose profits have a large exposure to changes in the spot price.

In the second stage of the model, generators compete with eachother for T time periods, selling energy on the contract market andon the spot market. In each period, firms simultaneously decidehow much energy they sell in the spot market for immediatedelivery, and how much they sell forward for delivery the nextperiod. In each period generators therefore receive revenue fromthe spot- and contract market, incur production costs and pay apenalty in function of the riskiness of their portfolio.

The paper takes the following simplifying assumptions:

�

Consumers are price takers with linear time-invariant demandfunction P(q) ¼ 1�q. �25 The formal definition of the sub-game Nash equilibrium of this game can be

found in the appendix.

Two generators i ¼ 1, 2 produce energy with constant marginalproduction costs c, which is normalized to zero.

In each time period t ¼ 1yT of stage 2, generator i sets itsproduction level qi

t , sells kit contracts in the forward market for

delivery in period t+1, and sells qit � ki

t�1 in the spot market. Totalproduction in period t is equal to sum of the production of bothfirms qt ¼ q1

t þ q2t , and the spot price is pt ¼ Pðq1

t þ q1t Þ.

To simplify notation, we present the decisions of player i inperiod t with gi

t ¼ ðqit ; k

itÞ. Likewise, the decisions taken by both

generators is a vector gt ¼ ðq1t ; k

1t ;q

2t ; k

2t Þ.

Player i’s profit in period t is equal to the revenue in the spotand forward market, minus production costs, and minus thepenalty for firm i’s ‘exposure’ to the spot price, i.e. ‘‘how much riskit takes’’:

pitðgt ; gt�1Þ ¼ ptðq

it � ki

t�1Þ þ f tðkitÞ � cqi

t

� Penaltyðgit ; g

it�1Þ (1)

We will measure this exposure by looking at the un-hedgedposition of the firm, as expressed by the difference betweenforward sales and total production. Formally, the penalty can beexpressed as a function of the decisions of firm i in the previousperiod gi

t�1 and the current period git . Below (Section 4.2) we

discuss different assumptions with respect to the penaltyfunction.

The forward price ft for the delivery of energy at period t+1 issuch that all inter-temporal arbitrage possibilities are exhausted,i.e. ft ¼ dpt+1, with d the discount factor. By lending money fromthe bank, buying in the forward market, and selling on the spotmarket, an arbitrageur will make zero profit.

Firm i’s second stage profit is the discounted sum of the single-period profits:

Wiðg1; . . . ; gT Þ ¼

XT

t¼1

dt�1pitðgt; gt�1Þ (2)

Note that the profit of firm i depends not only on its ownactions, but also on the actions of the other firm.

We solve this game for a sub-game-perfect Nash equilibrium.This can be found by backward induction. For this we start in the

last period of the game. We solve for the Nash equilibrium in theperiod T conditional on the actions of period T�1 and calculatethe continuation pay-offs of period T�1. We then calculate theNash equilibrium of period T�1, and the continuation profits ofperiod T�2. We repeat this until we reach the first period of thesecond stage of the game.25

4.2. Penalty function

The regulator uses the penalty to induce firms to sign contractsand to become less exposed to changes in the spot market price.As a result of the higher contract cover, generators will have fewerincentives to manipulate the spot price away from the competi-tive price. The regulator imposes a penalty which depends on thenet trade of a firm in the spot market. For simplicity we assumethat the penalty is a quadratic function.

Penaltyðgit ; g

it�1Þ ¼ lðProductioni

� Forward salesiÞ2 (3)

In the model we look at three regulatory systems to determinethis penalty:

1.

In the first regulatory system, the penalty is a function ofthe actual un-hedged position that is realized in the currentperiod t. Hence,Penalty ¼ lðqitþ1 � ki

tÞ2 (4)

with l a penalty parameter. We will call this regulatorysystem the regulation of the ‘‘actual risk exposure’’. The penaltyis an increasing function of the actual sales in the spot marketin period t. The more a firm sells into the spot market, thelarger the penalty.

2.

In the second regulatory system, the penalty is based onthe spot market and forward markets sales of the currentperiod t:

Penalty ¼ lðqit � ki

tÞ2 (5)

We will call this regulatory system the regulation of the‘‘projected risk exposure’’, as it takes the current productionlevels and uses them to project future ones. With thisregulatory system the firm has to pay a penalty if it sells lesson the forward market for delivery in the next period, than itsells currently in the spot market.

3.

In a third regulatory system, the penalty for contracting dependson spot market sales of the previous period t�1. Hence,Penalty ¼ lðqit�1 � ki

tÞ2 (6)

Under this system, the firm receives an incentive to sell forwardfor delivery in the next period, based on its historical productionlevel. We call this regulatory scheme the ‘‘historical risk exposure.’’

We will show in the next section that the first regulatoryscheme has very different effects on the exercise of market powerthan the latter two.

ARTICLE IN PRESS

0

Projected Risk

Actual Risk

0.2

0.25

0.3

0.35

0.4

0.45

0.5Quantity

Price

0.6

0.5

0.4

0.3

0.2

0.1

0.0

Penalty �

Contract

Contract

Production

Production

0.5 1 1.5 2 2.5 3

Fig. 2. Production level and contract positions.

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–3796 3793

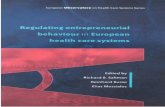

5. Simulation results

This section reports the results of the model for the regulatorysystems described above. For the numerical simulations weassume a discount factor of d ¼ 0.8, and present the results for arange of penalty parameters l.26 The results of numericalsimulations are presented in Fig. 2. As the projected risk andhistorical risk regulatory system are not significantly different, wewill only report the results under the regulatory system based onactual risk exposure and the projected risk exposure.

We first check whether contract regulation is able to reduceabuse of market power (feasibility), then we study whether theregulation reduces market deadweight loss without creating toohigh a burden for the regulated firm (effectiveness).

In all regulatory systems, the generators have an incentive tosign more contracts to align their contract position more closelywith their production levels. The three types of regulation aretherefore effective in inducing firms to sign more contracts.

However, the overall effect of the regulatory systems is verydifferent:

�

fact

futu

forw

lim

pro

With actual risk regulation, players have an incentive tocompete less fiercely in the spot market as they are punishedfor deviating from their contract position. In the extreme case,where the penalty becomes very large, the firms will no longersell in the spot market, and all trade takes place in the forwardmarket. As a result, equilibrium prices will go up. Hence thistype of regulation shifts market power from the spot market tothe contract market and reduces welfare.

� With projected and historical risk regulation, where the benchmarkfor regulating contracts is based on current or past productionlevels, this ‘direct effect’ on the spot price does not play a role.Firms are not penalized for deviating from their contractedposition by selling in the spot market. Instead the incentivesfor the firms to produce and contract are more complex.

� When firms set their spot market sales under the historical riskregulation, they will take into account that production

26 Equilibrium price levels are not very sensitive to the choice of the discount

or. With a lower discount factor, markets become slightly more competitive, as

re profits matter less, compared to revenue today. Firms will therefore sell more

ard contracts to obtain profit today, then to wait for future profit. Note that in the

it case, for discount factors equal to 1 (future profit’s matters as much as today’s

fits), a stable price profile is no longer guaranteed when the penalties are large. lite

decisions today will change their incentives to contract in thenext period, and, through a change in contract positions, intheir production incentives two periods from now. The effect ofhistorical risk regulation is that firms will produce more inperiod t, as this (through the penalty function) works as acommitment device to sell more in the forward market inperiod t+1, which will give them a larger market share inperiod t+2. This commitment effect makes markets morecompetitive.

� A similar effect is present in the regulation based on theprojected risk exposure. Firms have an incentive to increasetheir contract positions in period t, as this increases theirmarket share in period t+1 (the standard effect of contracts),and as this immediately reduces the penalty they need to payin period t.

Fig. 2 clearly shows that both regulations give firms incentivesto contract, but that only the projected risk regulation makes themarket more competitive.

We therefore conclude that the regulator should use historicalor current production quantities to regulate contracting decisionsof firms today. This updating of regulation targets is similar towhat happens in the theory of dynamic regulation of a singlemonopolist.27 The regulator uses information of the performanceof the firm in previous periods (when available) to set newregulatory targets.

In order to have a better idea of the effectiveness of theregulation, we turn to the quantitative results of the simulations(Table 1). How effective is the regulation in lowering the prices forfinal consumers in comparison with the penalty that firms wouldhave to pay? Table 1 shows that with a penalty factor l equal to0.7, prices drop with 40% (from 0.17 to 0.10), and that thedeadweight-loss decreases with about 70%. Hence, marketefficiency has increased considerably. The cost for firms is,however, very moderate: firms pay, in equilibrium, a penaltywhich is equal to 2.6% of their total profits.

We conclude that the regulation of contracts has a largepositive effect on welfare, by giving firms an incentive to increasecontract positions and to increase production, while the costs ofthe penalty for the firms remain limited.

27 Section 3.2 in Armstrong and Sappington (forthcoming) reviews the

rature on the dynamic aspects of regulation.

ARTICLE IN PRESS

Table 1Market outcome with ‘‘projective contract regulation’’

Penalty factor l

0 0.2 0.5 0.7 1 1.5 2

q production/firm 0.41 0.44 0.45 0.45 0.46 0.46 0.46

k contract sales/firm 0.24 0.35 0.40 0.41 0.43 0.44 0.44

p price 0.17 0.13 0.10 0.10 0.09 0.08 0.08

p profit/firm 0.071 0.055 0.046 0.043 0.041 0.039 0.037

Penalty payment as % of profit firm 0.0 2.9 2.9 2.6 2.2 1.7 1.4

Dead weight loss as % of welfare first best 3.0 1.6 1.1 0.9 0.8 0.7 0.7

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–37963794

6. Discussion and practical considerations

Section 5 shows, at least conceptually, that the regulation ofthe risk exposure of firms might reduce the abuse of marketpower of generation firms. The regulatory mechanism canhowever not be put in place overnight, as a lot of issues remainto be studied. Some of these issues are discussed in this section.

In order for contract regulation to be welfare improving, thepenalty should not be wasted, i.e. the money that the firms haveto pay, is recovered and redistributed. Implicit penalties require acareful evaluation of social costs. For instance, a capital adequacyrequirement creates an ‘‘opportunity cost’’ for society, but system-wide stability benefits for the electrical system might outweighthese costs.

When the regulator regulates the contract positions of firms, itchanges incentives of firms to hedge. With regulation, firms mightdecide to take less risk, or more risk than without regulation. This‘‘hedging’’ effect might have a positive or a negative effect onwelfare. In order to study this in more detail, we need to build amodel that combines the regulation of contracts, market power,and uncertainty.

Green (2003) argues that security of supply will be hamperedwhen retailers do not sign a sufficient number of electricitycontracts with a long duration. In Green’s paper, retailers do notsign contracts because the electricity regulator imposes that finalconsumers should be able to switch retailer on short notice.Without regulation firms might therefore under-hedge. Contractregulation potentially has a positive spillover to the security ofsupply of the energy industry. In order to obtain additionalinsights, new models with risk averse oligopolistic firms;uncertainty and contract regulation need to be developed.

As the demand for energy is stochastic, there are largevariations in production levels from one period to the other.There is therefore a risk that contract target quantity based onhistorical production levels, will not take into account futuredevelopments of the markets. One solution to this problem wouldbe that the regulator uses a combination of the projected and thehistorical risk-based regulation. The penalty function will have thefollowing form:

Penalty ¼ l gqit�1 þ ð1� gÞq

it � ki

t

h i2(7)

with g a weighting factor. The penalty induces firms to sellcontracts based on the average of their production in the currentand the previous period. By using average production quantities,the regulation quantities become less sensitive to periods withoutliers. The beneficial effects on market power of the averageproduction level are similar as for the projected risk and historical

risk-based regulatory systems. Additional analysis is required toaddress these questions in more detail.

One of the drawbacks of contract regulation is that it creates abarrier to entry which might foreclose the market. In order to test

how entry is affected by contract regulation, we simulate a modelwhere in period 1, only one firm is active in the market,g0 ¼ ðq

10; k

10;0;0Þ, and calculate how long it takes before we reach

a symmetric equilibrium where both firms share the marketequally. The speed of convergence is a measure of the difficultythat a firm would face to enter the market. For identicalparameters of the example taken before, the entrant would need5 periods, with projected risk-based systems, up to 13 periods,with historical risk-based systems, before it has an equal marketshare as incumbent. We therefore conclude that the regulatorshould not put too much weight on production quantities in thepast, as this will make entry more difficult.

In order to reduce the possibility of entry deterrence it isimportant that the forward contracts which are signed do notcontain conditions which might hinder competition such asexclusivity claims. Argenton and Willems (2008), show thatstandard financial forward contracts can lead to efficient entryand optimal risk sharing, while exclusive contracts might allowfor optimal risk sharing, but lead to inefficient entry.

Contracts might have a countervailing effect on the ability ofgenerators to sustain tacit collusion by increasing incentives forcollusion, making abuse of collective dominance more likely. Itlowers the profits when deviation from the tacit agreement occursand decreases the maximum punishment a player will receive. SeeLe Coq (2003) and Green and Le Coq (2006). In our model we donot study tacit collusion, instead we look only to a sub-gameperfect Nash equilibrium of a finitely repeated game.

As all these issues remain still open for further study, wepropose to introduce risk regulation gradually. A first regulatorystep would be to require firms to analyze the risk of their owncontracting portfolio and to report this to the regulator. This willallow the sector to reach a consensus on the best practices formeasuring risk. We think that some form of VaR estimator can beestablished. In order to give flexibility to the generation firms, theregulator should only impose minimal requirements for the riskanalysis, but larger firms should be able to set up own moredetailed models for evaluating risk. In a next step the regulatorcan then introduce a capital adequacy requirement.

7. Conclusion

The European Commission (2007) is concerned with thepotential abuse of market power by dominant generation firms.This paper argues that relying only on general competition rules isinsufficient to address those concerns, given the specific char-acteristics of the electricity market and the high level ofconcentration in some segments. We therefore suggest thatcomplementary ex-ante regulation is needed. In particular,regulators should incentivize firms to sign contracts with retailersby regulating their contract portfolio risk exposure.

ARTICLE IN PRESS

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–3796 3795

The role of contracts has, to a large extend, been neglected inthe European debate on market power mitigation methods. Theaim of this paper is to emphasize the potential benefits of such acontract regulation compared with several alternatives, and toopen the debate on its implementation.

In the first part of the paper, we show that contract regulationhas certain advantages over other forms of regulation as the onesused in the US. American markets rely on mandatory power poolscombined with price cap or bid cap regulation. This form ofregulation destroys short- and long-term incentives of generatorsand consumers. Contract regulation is a softer and less intrusiveform of regulation which keeps the incentives of generators andconsumers largely intact.

In the second part, we develop a model of contract regulationin which firms endogenously decide on contracting and produc-tion. It is shown that contract regulation can significantly reducethe deadweight loss due to market power in the market, withoutimposing large costs on regulatees. The regulatory system shouldhowever be designed very carefully.

�

Cali

com

pac

EUR

of

com

cap

pro

Firstly, while regulating the contract position of the firms,one should use production information which predates thedelivery period of the contract, in order to avoid distorting spotmarket decisions. This historical information is not alwaysavailable, especially not in the case of new entrants in themarket.

� Secondly, the regulator should take care that the penalties,which are incurred by the firms, are not a loss for society.Penalties which take the form of extra capital requirements,might be beneficial for society if they increase systemstability.

This paper’s model concentrated on the effects of contractregulation on market power, and has neglected additional benefits

on the stability of the electricity system, and on the (positive ornegative) effects of market contestability. Future formal work isneeded to jointly address the regulatory process, the contractingand investment decisions of firms, and the impact of marketimperfections such as market power, market incompleteness, andthe lack of consumers’ response.We do not believe that contract regulation can substitute for asound market design and a lowly concentrated market structure.These two problems should be dealt with head-on, and requireadditional legislation at the EU- and national level.28 Insteadcontract regulation and capital adequacy requirements shouldbecome an extra tool for sector specific regulators. We suggest thefollowing regulatory changes to introduce contract portfolioregulation:

�

Firstly, firms should be obliged to analyze and report theircontract position and risk exposure. Sector regulators shouldobtain an additional role of oversight on the security of supplyin the sector, and be able to put in place reporting require-ments on the risk firms take, and regulations with respect tothe solvency of market participants. The regulator should workin close co-operation with financial regulators and competitionauthorities.28 In this respect, Harvey and Hogan (2000) contend that given the flaws in

fornian market design, it was unlikely that contract regulation would

pletely eliminate the abuse of market power. The proposed third liberalization

kage of the European Commission (see: Proposal for a DIRECTIVE OF THE

OPEAN PARLIAMENT AND OF THE COUNCIL, amending Directive 2003/54/EC

the European Parliament and of the Council of 26 June 2003 concerning

mon rules for the internal market in electricity, improving cross-border

acity and network unbundling) is likely to be a step in the right direction, but

bably not sufficiently far-reaching.

�

Secondly, part of the monitoring role of the regulator shouldshift from the regulator to the network operator and/or thepower exchanges. As the network operator is responsible forbalancing demand and supply, it has the right incentives toensure that generation firms do not threaten system stabilityby taking too much risk. The network operator also has thecapacities to deal with the large amount of data which areavailable in the market. This requires that the networkoperator is sufficiently independent of the generation firms.Acknowledgments

We thank colleagues at the Florence School of Regulation andits director Pippo Ranci for useful discussions on the topics; LolaOdusanya, Carmen Oprea, Jens Weinmann, and participants toseminars in Tilburg University, at Essent N.V., ACLE Law andEconomics conference in Amsterdam for their numerous com-ments and suggestions. Three anonymous referees have providedinsightful comments and suggestions to improve the paper. Thispaper was made possible by financial support in the framework ofthe Essent TILEC co-operation contract, and a Jean Monnetfellowship at the European University Institute in Florence.

Appendix A

A.1. Sub-game perfect equilibrium

Define firm i’s continuation profit Vitþ1ðgtÞ in period t+1 as the

net present value of firm i’s profit over the time periods i ¼ t+1 toT when both firms play their equilibrium strategy, conditional ontheir actions in period t being equal to gt.

We further define the equilibrium price function Ft+1(gt) inperiod t+1, as the equilibrium spot price in period t+1 when bothfirms play their equilibrium strategy, conditional on their actionsin period t being equal to gt.

The sub-game prefect Nash equilibrium in period t, SNEt( � ) is afunction which maps actions of period t�1 to actions of period t. Itdescribes for each firm its equilibrium actions in period t,conditional on the actions for both firm in period t�1 to be gt�1:

SNEt : R4! R4 : gt�1 7!gt ¼ SNEtðgt�1Þ

such that for i ¼ 1;2:

git ¼ arg max

git¼ðq

it ;k

it Þ

pitðgt ; gt�1Þ þ dVi

tþ1ðgtÞ

n o

s:t: f t¼ dptþ1 ¼ dFtþ1ðgtÞ (8)

The continuation profit and the equilibrium price function Ft(gt)are determined by the following recursive relations:

Vitðgt�1Þ ¼ pi

tðNEtðgt�1Þ; gtÞ þ dVitþ1ðNEtðgt�1ÞÞ (9)

Ftðgt�1Þ ¼ PðNEtðgt�1ÞÞ (10)

The Nash equilibrium of the whole game is determinedby Eqs. (8)–(10), combined with the following end-recursiveconditions:

�

In period t ¼ 0, the firms are unable to sell in the spot and theforward market, as the markets do not exist:g0 ¼ ð0;0;0;0Þ (11)

�

In period t ¼ T+1, the game is finished, the continuation profitof the firms is zero, and the forward price can be set equal to

ARTICLE IN PRESS

B. Willems, E. De Corte / Energy Policy 36 (2008) 3787–37963796

zero without restrictions:

ViTþ1ðgtÞ ¼ 0

FTþ1ðgtÞ ¼ 0 (12)

For a given penalty function, these equations can be solvedusing analytical and numerical techniques, as explained inSection 4.

In the following section we discuss three different penaltyfunctions the regulator could use. In Section 3 we then compareand discuss market outcomes for the different types of regulation.

A.2. Calculation method

This section describes the calculation methods underlying ournumerical results.

We are interested in the long run effects of the regulation onthe behavior of the firms, and not in the transition effects at thestart of the end of the second stage. In order to solve for this long-run equilibrium, two approaches can be used.

The first solution to this problem is to solve this problemanalytically for a large number of time periods such that thedecisions of the firms become stable. For this method we useMathematica and solve the sub-game perfect Nash equilibriumfor T ¼ 200, and check whether the decisions are sufficientlystationary around t ¼ 100.

The second solution method consists of calculating thestationary solution numerically. A numerical solution can befound by assuming a functional form for the continuation profitfunction and the price function:

VðgÞ ¼ a0 þ a1k1 þ a11k21 þ a2k2 þ a22k2

2 þ a12k12

FðgÞ ¼ b0 þ b1k1 þ b2k2 (13)

and to impose explicitly that the solution is stationary.

8g Vitþ1ðgÞ ¼ Vi

tðgÞFtþ1ðgÞ ¼ FtðgÞ (14)

By jointly solving Eqs. (14), (9), and (10), we will find severalsets of parameters a and b which satisfy all equations. We needhowever to restrict the solution to these values where:

�

The parameters are real. Complex solutions of the equationsare irrelevant. � The optimization problem that each firm faces should beconcave, in order to ensure that the solution is a localmaximum, and not a local minimum.

� The equilibrium of the set of equations should be stable: after asmall deviation of the decisions that the firms take, the firmsshould return to their long-term equilibrium.

By imposing these three restrictions we find only one stablestationary solution. The stationary solution is identical to the oneto which we converged in the analytical solution.

As there is only one stationary and stable equilibrium, we alsoknow that all analytical solutions will converge to the sameequilibrium, independent on conditions that we impose in thefirst or the last period of stage 2.

A.3. Mathematica code

The Mathematica code of the program is available on requestfor the referees.

References

Allaz, B., Vila, J.L., 1993. Cournot competition, forward markets and efficiency.Journal of Economic Theory 59, 1–16.

Argenton, C., Willems, B., 2008. Exclusivity as (in)Efficient Insurance. TilburgUniversity, Mimeo.

Armstrong, M., Sappington, D., 2007. Recent developments in the theory ofregulation. In: Armstrong, Porter (Eds.), Handbook of Industrial Organization,vol. 3, pp. 1557–1700.

Cramton, P., 2007. Colombia’s forward market. Paper presented at the Confe-rence on ‘‘The Economics of Energy Markets,’’ Toulouse, France, June 20–21,2008.

EU Commission, 1997. Directive 96/92/EC of the European Parliament and of theCouncil of 19 December 1996 concerning common rules for the internalmarket in electricity (OJ 1997 L 27/20).

EU Commission, 2002. Consolidated version of the Treaty establishing theEuropean Community. Report No. C325.

EU Commission, 2003a. Directive 2003/54/EC of the European Parliamentand of the Council of 26 June 2003 concerning common rules forthe internal market in electricity and repealing Directive 96/92/EC (OJ 2003L 176/37).

EU Commission, 2003b. Council Regulation (EC) No. 1/2003 of 16 December2002 on the implementation of the rules on competition laid down in Articles81 and 82 of the Treaty (text with EEA relevance) (OJ 2003 L 1, art.6).

EU Commission, 2007. DG competition report on energy sector inquiry (SEC(2006)1724, 10 January 2007).

EU Commission, 2008. Notice published pursuant to Article 27(4) of CouncilRegulation (EC) No. 1/2003 in cases COMP/B-1/39.388—German ElectricityWholesale Market and COMP/B-1/39.389—German Electricity BalancingMarket (OJ 2008 C 146/09).

Green, R., 1999. The electricity contract markets in England and Wales. Journal ofIndustrial Economics 47 (1), 107–124.

Green, R., 2003. Electricity Contracts and Retail Competition. University of Hull.Green, R., Le Coq, C., 2006. The length of contracts and collusion. Report No.

WP-154, Berkeley.Harvey, S.M., Hogan, W.W., 2000. California electricity prices and forward market

hedging. Harvard Electricity Policy Group.Le Coq, C., 2003. Long-term supply contracts and collusion in the electricity

markets. Report No. 552. Stockholm School of Economics.Mahenc, P., Salanie, F., 2004. Softening competition through forward trading.

Journal of Economic Theory 116 (2), 282–293.Motta, M., de Streel, J., 2003. Exploitative and exclusionary excessive prices in EU

law, Florence.Newbery, D.M., 1998. Competition, contracts, and entry in the electricity spot

market. Rand Journal of Economics 29 (4), 726–749.Sappington, D., 1980. Strategic firm behavior under a dynamic regulatory

adjustment process. The Bell journal of economics 11 (1), 360–372.Willems, B., 2006. Virtual divestitures, will they make a difference?

Cournot Competition, Option Markets and Efficiency. Report No. WP150,Berkeley.

Willems, B., Morbee, J., 2008. Risk management in electricity markets: hedging andmarket incompleteness. In: Conference Proceedings, ‘‘Policymaking Benefitsand Limitations from Using Financial Methods and Modelling in ElectricityMarkets,’’ Oxford.

Wolak, F.A., 2001a. An empirical analysis of the impact of hedge contracts onbidding behavior in a competitive electricity market. Report No. Working Paper8212, NBER.

Wolak, F.A., 2001b. A comprehensive Market Power Mitigation Plan for theCalifornian Electricity Market. California Market Surveillance Committee.

Wolak, F.A., 2003a. Lessons from the California electricity crisis. Report no. WP 110,Center for the Study of Energy Markets (CSEM).

Wolak, F.A., 2003b. Measuring unilateral market power in wholesale electricitymarkets: the California market, 1998–2000. The American Economic Review93, 425–430.

Wolak, F.A., Nordhaus, R., 2001. An analysis of the June 2000 price pikes in theCalifornia ISO’s energy and ancillary services market. Market SurveillanceCommittee (MCS) of the California Independent System Operator.