Market Insights/Torcivia 37 Hilgert Avenue 610-927 … Insights PPT.pdf · Product/Brand...

32

Market Insights/Torcivia 37 Hilgert Avenue Reading, PA 19607 610-927-2299 [email protected] Market Insights 1

Transcript of Market Insights/Torcivia 37 Hilgert Avenue 610-927 … Insights PPT.pdf · Product/Brand...

Market Insights/Torcivia

37 Hilgert Avenue Reading, PA 19607

610-927-2299

Market Insights1

• Background & Qualifications • U.S. Wood Flooring Market

• Canada Wood Flooring Market

• Brand Positioning • Discussion with Questions & Answers

Market Insights2

• Market Insights: 1997 to present Contributing Editor: Floor Focus magazine Expert Witness in Federal Court (re: Flooring)

• Mannington Mills- 16 years: Business Development & Planning; Business Analysis; Channel Management; Market Research; and, Acquisition & Ventures

• American Bank & Trust (now Wells Fargo)- 8 years • Temple University (Phila., PA): BS- Economics Graduate study Columbia University

Market Insights

3

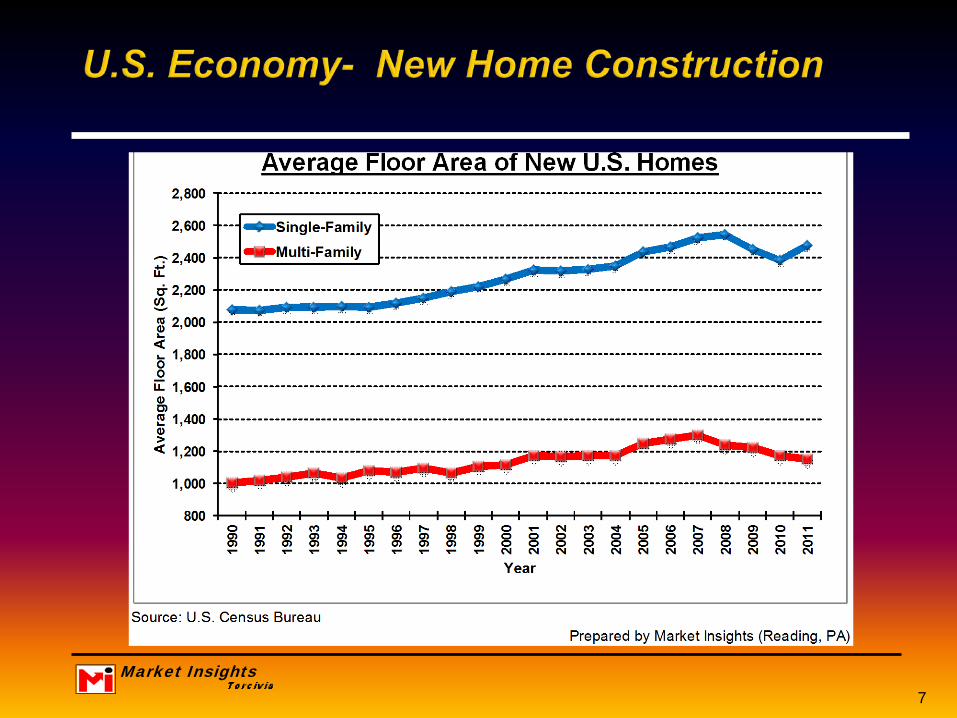

U.S. Wood Flooring Market

Market Insights4

Market Insights5

Market Insights6

Market Insights7

Market Insights8

Market Insights9

Market Insights

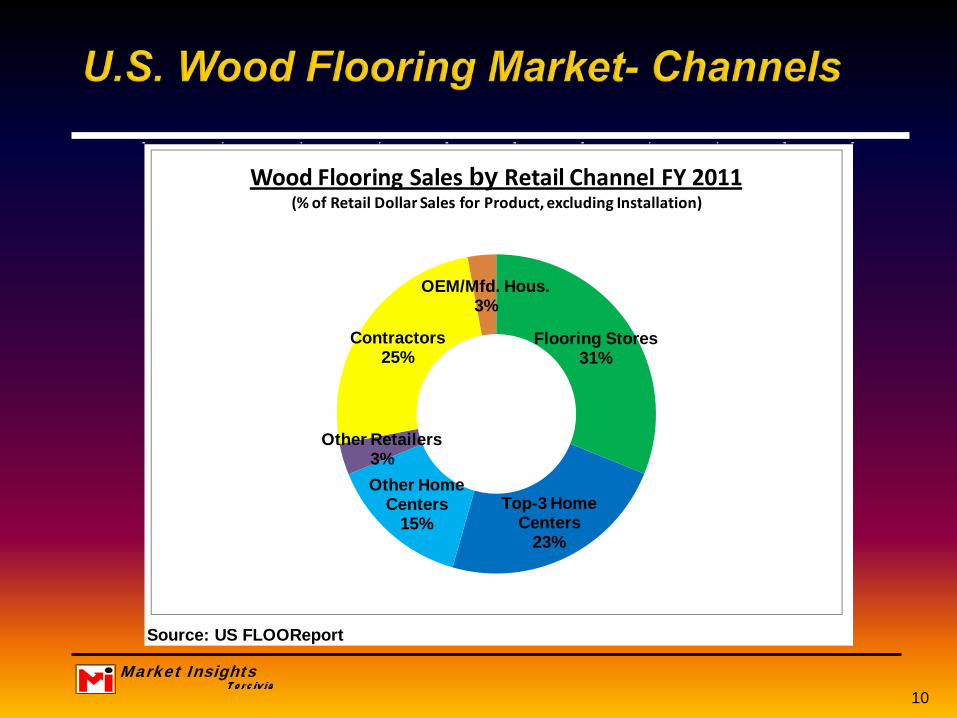

Source: US FLOOReport

Flooring Stores31%

Top-3 Home Centers

23%

Other Home Centers

15%

Other Retailers3%

Contractors25%

OEM/Mfd. Hous.3%

Wood Flooring Sales by Retail Channel FY 2011(% of Retail Dollar Sales for Product, excluding Installation)

10

Market Insights11

Market Insights12

Market Insights13

Market Insights14

Market Insights15

Market Insights

Country of Origin 2008 2009 2010 2011 2011 2012 % Chg.Total Imports- 341 581 462 547 279 312 11.7%

% Change -- 70.4% -20.5% 18.4%

1 China 37% 50% 55% 56% 54% 60%2 Brazil 12% 21% 19% 18% 20% 15%3 Canada 22% 12% 13% 12% 12% 12%4 Malaysia 3% 2% 2% 1% 2% 2%5 Paraguay 1% 1% 1% 2% 2% 1%6 Peru 0% 1% 1% 1% 1% 1%7 Indonesia 4% 2% 1% 1% 1% 2%8 Chile 1% 1% 1% 1% 1% 1%9 Denmark 1% 1% 1% 1% 1% 1%

10 Italy 2% 0% 0% 0% 1% 1%All Others 18% 8% 7% 6% 5% 4%Total Imports- 100% 100% 100% 100% 100% 100%

Notes: -Changes in Harmonozed Tariff System (HTS) codes prevent comparisons with import figures for wood flooring before 2008

-Bamboo flooring not included in wood flooring import figuresSource: U.S. International Trade Commission

Prepared by Market Insights (Reading, PA)

Annual Import Values(US $ in millions at C.I.F.)

Year-to-Date(US$ in millions @ c.i.f.)

Share of Imports

16

Market Insights

U.S.A. Data % of U.S. Data % of U.S.

Total Population in 2011 (MM, mid-year) 310 34 11% 380 122%

Wood Flooring Market FY 2011: Quantity (sq. ft., MM) 715 184 26% 764 107%

Value (US$, MM) 1,636 484 30% n.a. n.a.

Per-Capita Quantity Consumption (sq. ft. per person) 2.30 5.45 236% 2.01 87%

*Europe= Western Europe plus nations of Scandanavia, Hungary, Czech & Slovakian Reps.Prepared by Market Insights (Reading, PA)

Canada Europe*

17

Market Insights18

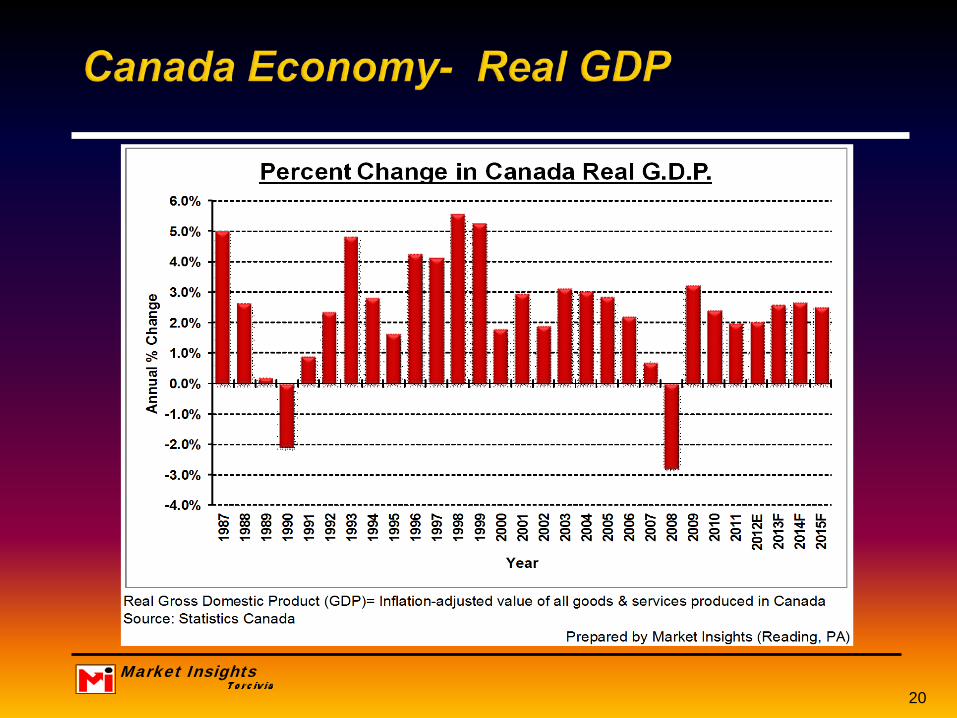

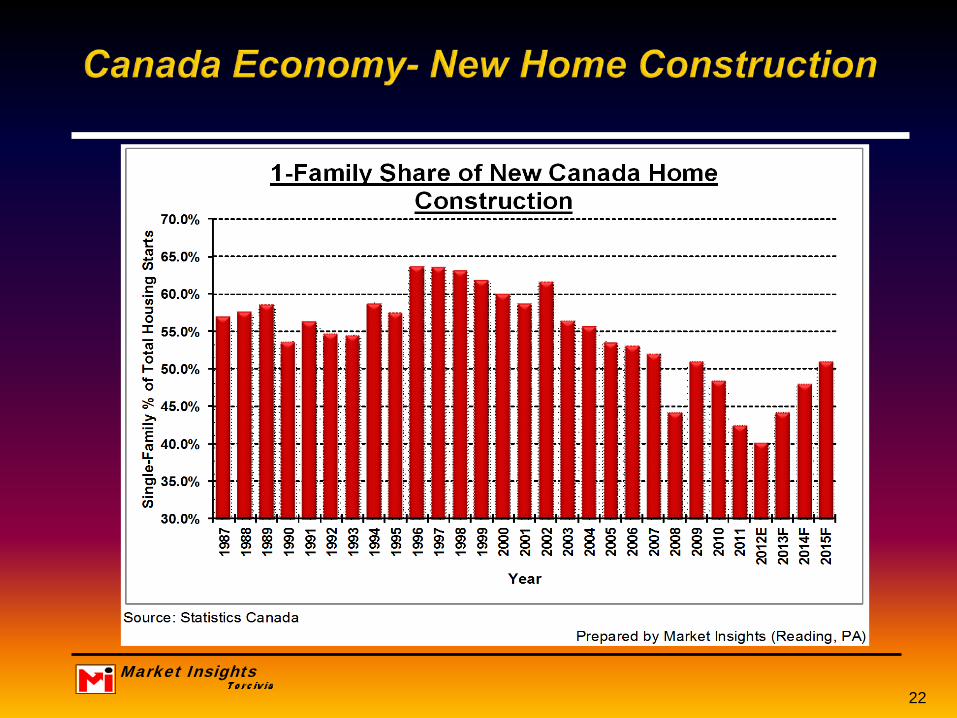

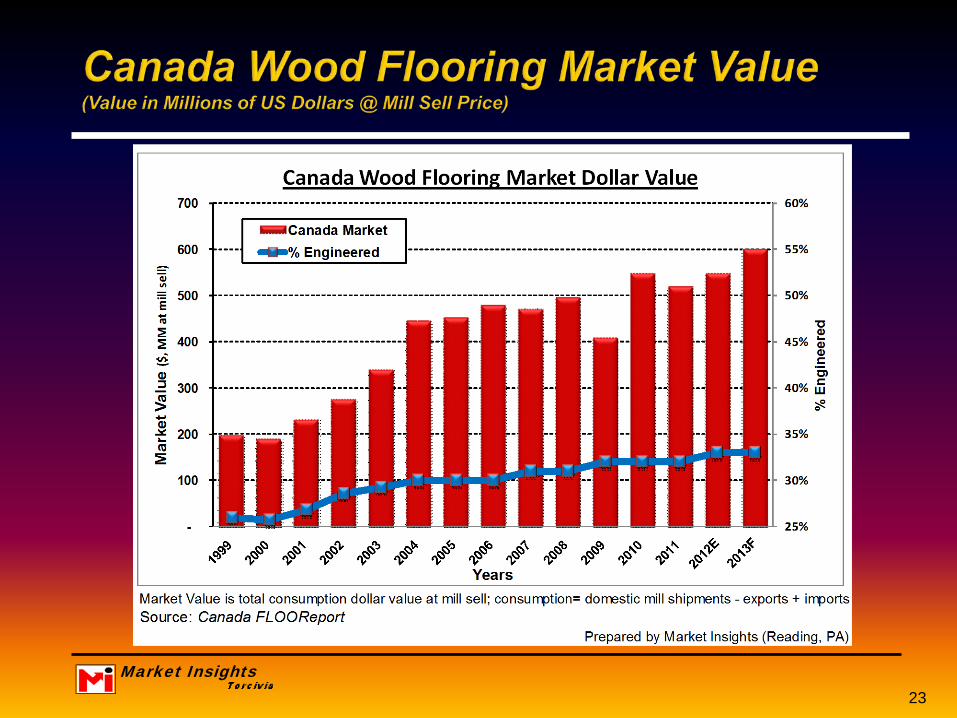

Canada Wood Flooring Market

Market Insights19

Market Insights20

Market Insights21

Market Insights22

Market Insights23

Wood Flooring Brand Positioning

Market Insights24

Market Insights25

High Value/ High PricedProduct/Brand Characteristics:

- Many Product Features/Benefits- High Brand Equity- Very Positive Brand Image- Most Customers are Brand Loyal

Low-Value/ Low-PricedProduct/Brand Characteristics:

Middle-Value/ Mid-Priced - Few/No Product Features/BenefitsProduct/Brand Characteristics: - Some/No Brand Equity- Some Product Features/Benefits - Value-based Brand Image/ or None- Some Brand Equity - Customers are Price Loyal- Somewhat Positive Brand Image- Some Customers are Brand Loyal

Market Insights

% Adv./SalesBrand 2007 2008 2009 2010 2011 Amount Share (2007 - 2011)

($, 000) ($, 000) ($, 000) ($, 000) ($, 000) ($, 000)Armstrong 18,114 11,374 5,975 6,380 - 41,843 52% 1.9%Bellawood (Lumber Liq.) 2,420 716 1,034 1,612 3,356 9,138 11% 2.4%Mirage (Boa Franc) 2,644 2,269 1,177 1,509 760 8,359 10% 4.3%BR-111 4,936 2,467 - 265 - 7,668 10% 5.6%Carlisle Wide Width Planks 558 2,500 296 1,589 386 5,329 7% n.a. Teragren (bamboo) 955 1,074 322 - - 2,351 3% n.a. Shaw* - - 909 142 - 1,050 1% 0.1%Mohawk - 1,024 - - - 1,024 1% 0.1%Bella Cera - - - 636 377 1,013 1% n.a. Listone Giordano (Marg.)* 497 - - - - 497 1% n.a. Mullican - - - 411 - 411 1% 0.1%T. Morton/ Armstrong 302 - - - - 302 0% n.a. Max Windsor 272 - - - - 272 0% n.a. Wicanders (cork) 269 - - - - 269 0% n.a. Pianto Legano 255 - - - - 255 0% n.a.

Totals- 31,222 21,424 9,713 12,544 4,879 79,781 100% 1.0%% of Residential $ Sales 1.5% 1.3% 0.7% 0.9% 0.3% 1.0%Source: Kantar Media

Total 2007- 2011

26

Market Insights

Product Category 2007 2008 2009 2010 2011Resilient Flooring 0.2% 0.2% 0.0% 0.0% 0.7%Laminate Flooring 2.3% 2.8% 2.4% 2.0% 0.0%Wood Flooring 1.5% 1.3% 0.7% 0.9% 0.3%Ceramic Tile 0.6% 0.7% 0.6% 0.3% 0.0%Carpet 0.3% 0.3% 0.2% 0.1% 0.1%

Flooring Manufacturers- 0.6% 0.6% 0.5% 0.4% 0.2%

Carpet Fiber 0.2% 0.1% 0.1% 0.2% 0.1%Total Flooring & Fibers- 0.7% 0.7% 0.6% 0.5% 0.2%

Source: Kantar Media and US FLOOReport

27

Market Insights

(Mkt. Sh.) (Mkt. Sh.)Top-5 Retailers 8% Top-5 Retailers 20%Color Tile The Home DepotNew York Carpet World LowesSears Lumber LiquidatorsSherwin Williams Empire TodayCarpetland USA Sherwin Williams

Private Label Brands Private Label BrandsBrand Name Retailer Brand Name Retailer(None) Trafficmaster THD

Surface Source LowesBellawood Lmbr. Liq.

20121993

28

Market Insights

Brand EquityProduct

Higher Profits Differentiation: - Image

Higher Margin - Performance - Product Development - Cost/ Price - Adv./Brand Development - Research & Development - Capital Investment - Earnings & Bonus'

CommodityNo/Low Brand Equity

29

Market Insights30

• Large retailers gaining channel power • Retailer brands increasing

• Manufacturer brands decreasing

• Brand equity= higher margins= increased brand equity

• Brand equity is an investment= equipment maintenance • Commodity status= lower margins= low brand equity

• IT IS NOT TOO LATE….

Market Insights31

• Economy future is election dependent ???? • Wood Flooring: U.S.= +12% in $ Sales in 2013

Can.= +9% in $ Sales in 2013

• Channel Sales: about 35% each H.C’ers, Flooring, & Contractors

• Channel power shifting to retailers • Adv. & Brand Investment declining for manufacturers and increasing for retailers • Future is your choice= ….Brand equity or Commodity status

Discussion Questions & Answers

Market Insights32