Market Crashes and Modeling Volatile Markets - Risk … · Market Crashes and Modeling Volatile...

47

Market Crashes and Modeling Volatile Markets Prof. Svetlozar (Zari) T.Rachev Chief-Scientist, FinAnalytica Chair of Econometrics, Statistics and Mathematical Finance School of Economics and Business Engineering University of Karlsruhe Department of Statistics and Applied Probability University of California, Santa Barbara

Transcript of Market Crashes and Modeling Volatile Markets - Risk … · Market Crashes and Modeling Volatile...

Market Crashes and Modeling Volatile Markets

Prof. Svetlozar (Zari) T.RachevChief-Scientist, FinAnalytica

Chair of Econometrics, Statistics and Mathematical FinanceSchool of Economics and Business EngineeringUniversity of Karlsruhe

Department of Statistics and Applied ProbabilityUniversity of California, Santa Barbara

Post Modern Portfolio Theory

MPT “translation” for Volatile Markets

Normal (Gaussian) Distributions

– Correlation

– Sigmas

– Sharpe Ratios

– BS Option Pricing

– Markowitz Optimal Portfolios

Fat‐tailed Distributions

– Tail & Asymmetric Dependence

– Expected Tail Loss

– STARR Performance

– Tempered‐Stable Option Pricing

– Fat‐tail ETL Optimal Portfolios

Old World Real World

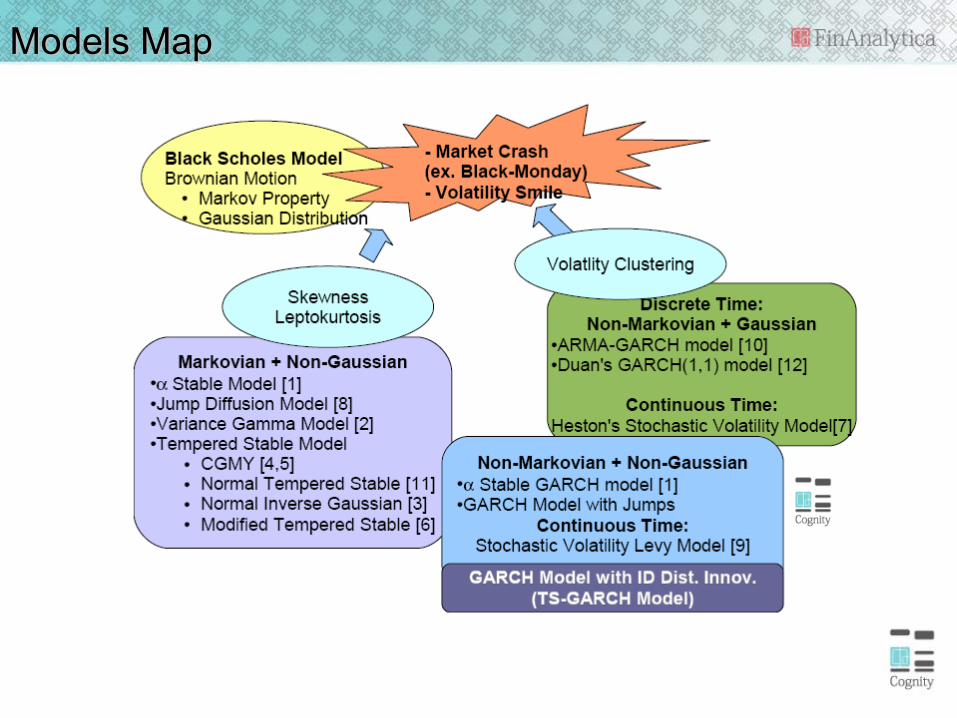

Models Map

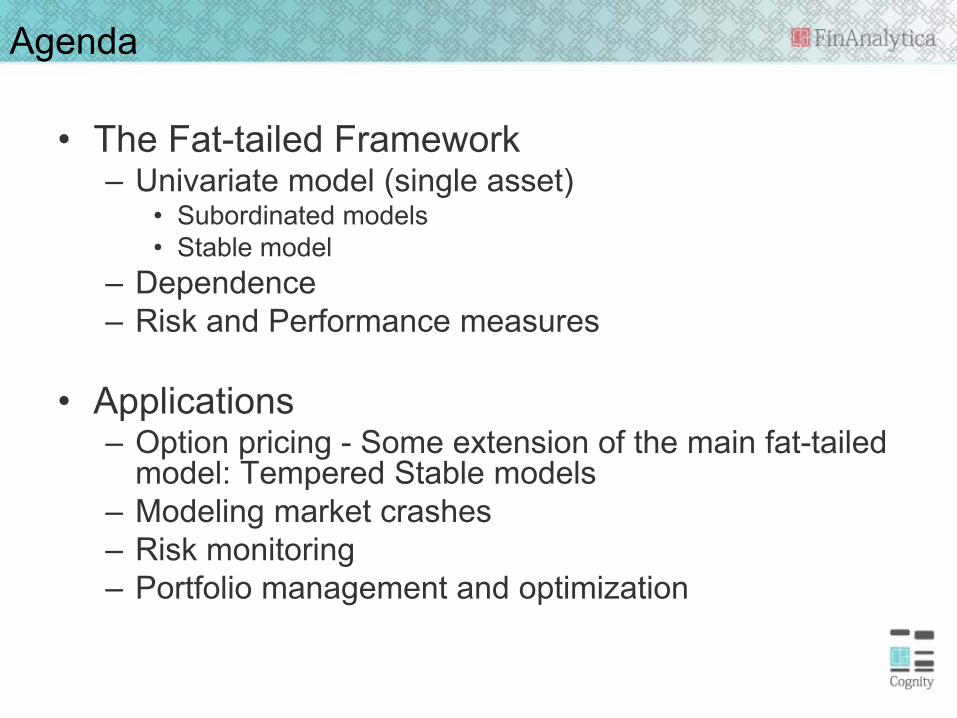

Agenda

• The Fat-tailed Framework– Univariate model (single asset)

• Subordinated models• Stable model

– Dependence– Risk and Performance measures

• Applications– Option pricing - Some extension of the main fat-tailed

model: Tempered Stable models– Modeling market crashes– Risk monitoring– Portfolio management and optimization

Fat-tail Modeling Framework

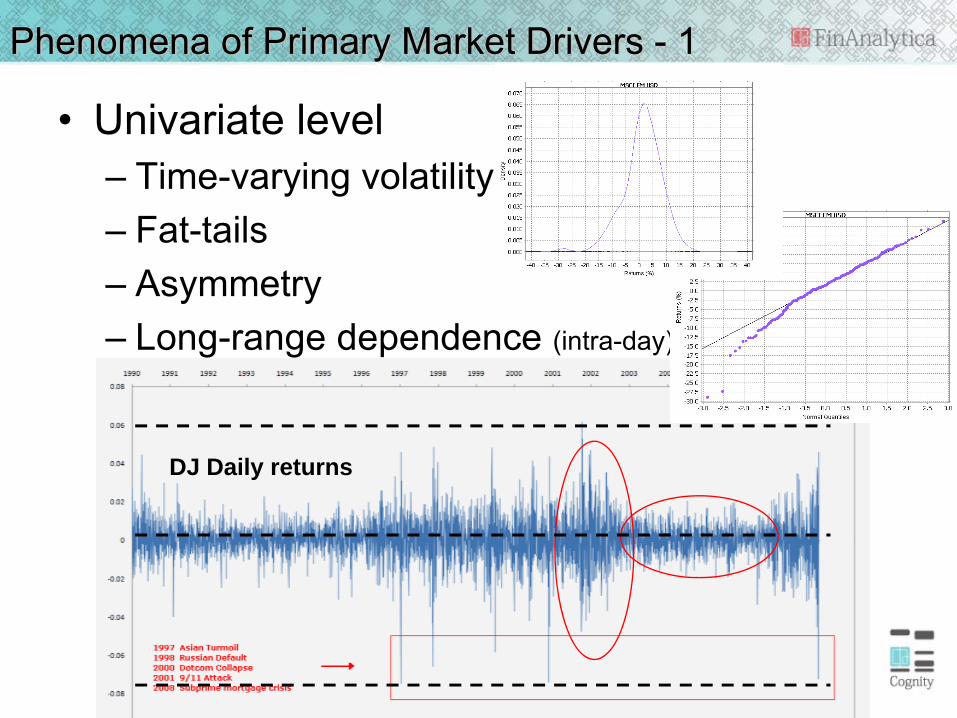

Phenomena of Primary Market Drivers - 1

• Univariate level– Time-varying volatility– Fat-tails– Asymmetry– Long-range dependence (intra-day)

DJ Daily returns

Fat-tailedFat-tailed

Subordinator (g(W)) < 1Subordinator (g(W)) < 1γ <0

( )ZWgWXNZZWgX

tTZtTZtX

++=∈=

==

γμ:)1,0(,)(:

))(()()( o “On the days when no new information is available,

trading is slow and the price process evolves slowly. On days when new information violates old expectations,

trading is brisk, and the price process evolves much faster”.

Clark (1973)

Emp.

Subordinator > 1

Stable Family

1.5)Positive skewed densities (α = 0)

Symmetric densities (β =

Rich history in probability theoryKolmogorov and Levy (1930-1950), Feller (1960’s)

Long known to be useful model for heavy-tailed returnsMandelbrot (1963) and Fama (1965)

Fat Tails Study: 17,000+ factors

May 2007

14%

4%

76%

6%

Normal Vol Clust Enhanced Normal

Stable Vol Clust Enhanced Stable

Dec 20087%0%3%

90%

Normal Vol Clust Enhanced Normal

Stable Vol Clust Enhanced Stable

85%, 95%, 97.5%, and 99% VaR tested

Fat Tails Study: Factors Breakdown

Factors Tested Number Percentage

Equities 8346 48.5%

CDS Spreads 7803 45.3%

Interest Rates 528 3.1%

Implied Volatilities 518 3.0%

Currencies 12 0.1%

Total 17207 100.00%

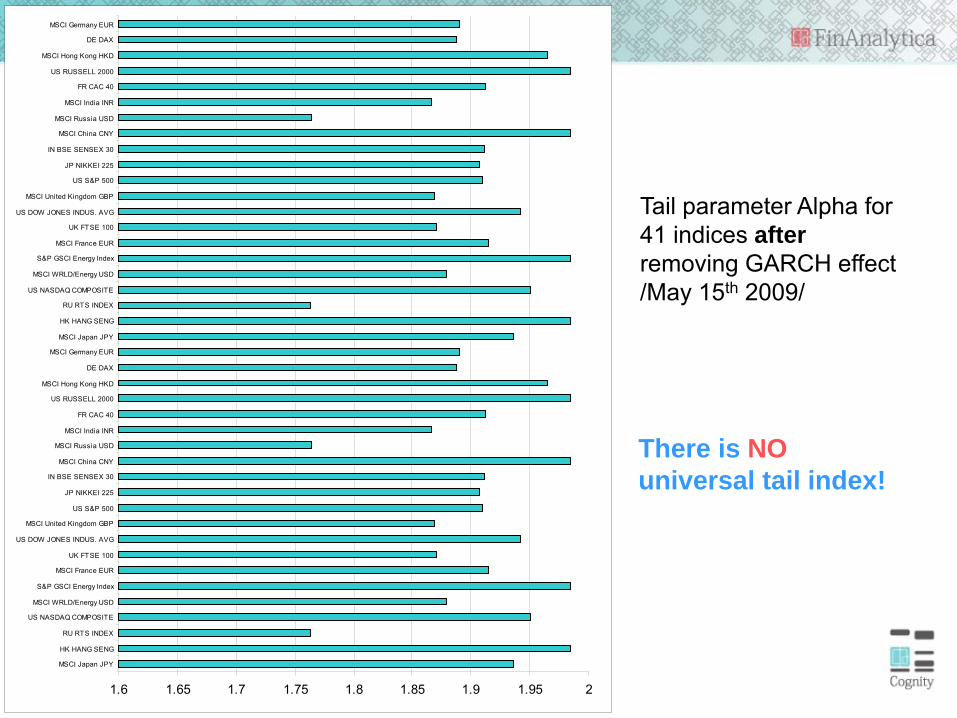

Alpha Tail Parameter: Varies Across Assets & Time• Important to:

– Distinguish tail risk contributors and diversifiers– Changes in the market extreme risk

S&P 500 alpha

1.5

1.55

1.6

1.65

1.7

1.75

1.8

1.85

1.9

1.95

2

15/06/2000 15/06/2001 15/06/2002 15/06/2003 15/06/2004 15/06/2005 15/06/2006 15/06/2007 15/06/2008

after removing GARCH

Tail parameter Alpha for 41 indices afterremoving GARCH effect/May 15th 2009/

1.6 1.65 1.7 1.75 1.8 1.85 1.9 1.95 2

MSCI Japan JPY

HK HANG SENG

RU RTS INDEX

US NASDAQ COMPOSITE

MSCI WRLD/Energy USD

S&P GSCI Energy Index

MSCI France EUR

UK FTSE 100

US DOW JONES INDUS. AVG

MSCI United Kingdom GBP

US S&P 500

JP NIKKEI 225

IN BSE SENSEX 30

MSCI China CNY

MSCI Russia USD

MSCI India INR

FR CAC 40

US RUSSELL 2000

MSCI Hong Kong HKD

DE DAX

MSCI Germany EUR

MSCI Japan JPY

HK HANG SENG

RU RTS INDEX

US NASDAQ COMPOSITE

MSCI WRLD/Energy USD

S&P GSCI Energy Index

MSCI France EUR

UK FTSE 100

US DOW JONES INDUS. AVG

MSCI United Kingdom GBP

US S&P 500

JP NIKKEI 225

IN BSE SENSEX 30

MSCI China CNY

MSCI Russia USD

MSCI India INR

FR CAC 40

US RUSSELL 2000

MSCI Hong Kong HKD

DE DAX

MSCI Germany EUR

There is NOuniversal tail index!

Phenomena of Primary Market Drivers - 2

• Tail Dependence

Zero tail dependenceGaussian copula

Dependence ModelsAsymmetric Dependence

Dependence ModelsModeling of Extreme Dependency in market crashes is critical for taking

correct investment decisionsBi-variate Normal

Fat-tailed indicesGaussian Copula

Fat-tailed indicesFat-tailed copula

Observed returns in Q3 1987

))(),...,((),...,( 111 nnn xFxFCxxF =

F is the multivariate cdf, C is the copula function and Fi are the one-dimensional cdf.

Risk & Performance Measures

Downside risk penaltyand upside reward

Symmetric risk penaltyσ

μ frSHARPE

−=

ETLr

STARR

qrrEETRVaRrrEETL

f−=

>=−<−= −−

μεεεε )|()|( 11

ETLETRRatioR =−

Downside risk penalty

Why not Normal ETL?

Summary

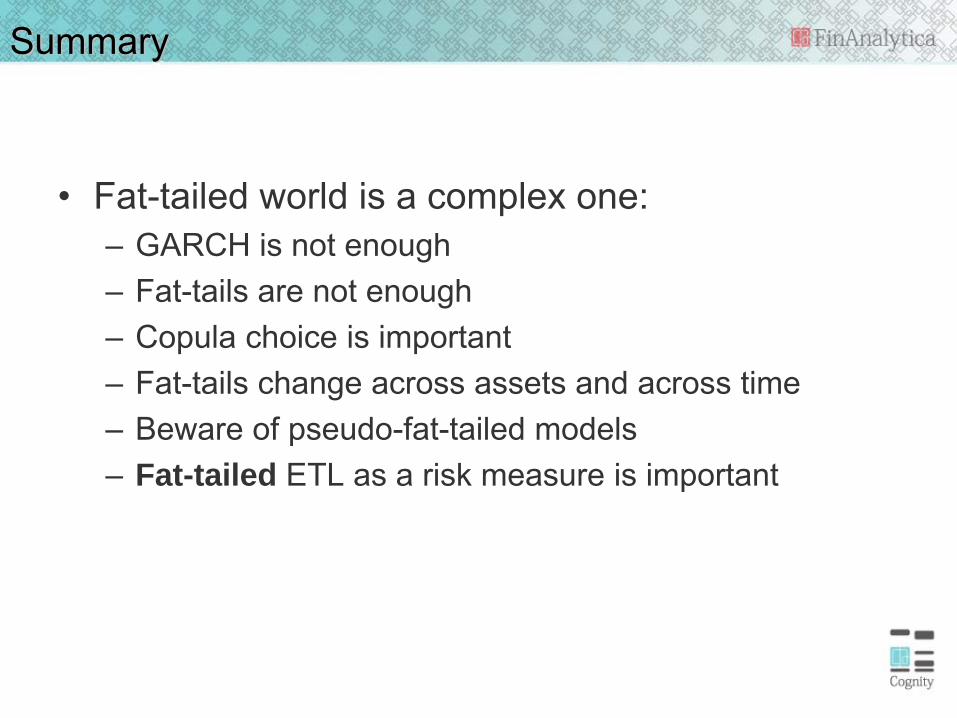

• Fat-tailed world is a complex one:– GARCH is not enough– Fat-tails are not enough– Copula choice is important– Fat-tails change across assets and across time– Beware of pseudo-fat-tailed models– Fat-tailed ETL as a risk measure is important

Application 1 – Option pricing Stable and Tempered Stable Distributions

Tempered Stable Models Introduction

• The stable model does not allow for unique equivalent martingale measure

• Take a stable model and make the very end of the tails lighter (still much heavier than the Gaussian)

• All moments exist• No-arbitrage option pricing exists

Tempered Stable

Tempered Stable

Map of Tempered Stable Distributions

Rapidly Decreasing

Tempered Stable(RDTS)

Smoothly Truncated

Stable(STS)

Kim-Rachev(KR)

ClassicalTempered

Stable(CTS)

NormalTempered

Stable(NTS)

ModifiedTempered

Stable(MTS)

Incorporating GARCH Effect

other tempered stable models

Is GARCH Enough? … No!

• QQ plots between the empirical residual and innovation distributions for daily return /data for IBM/

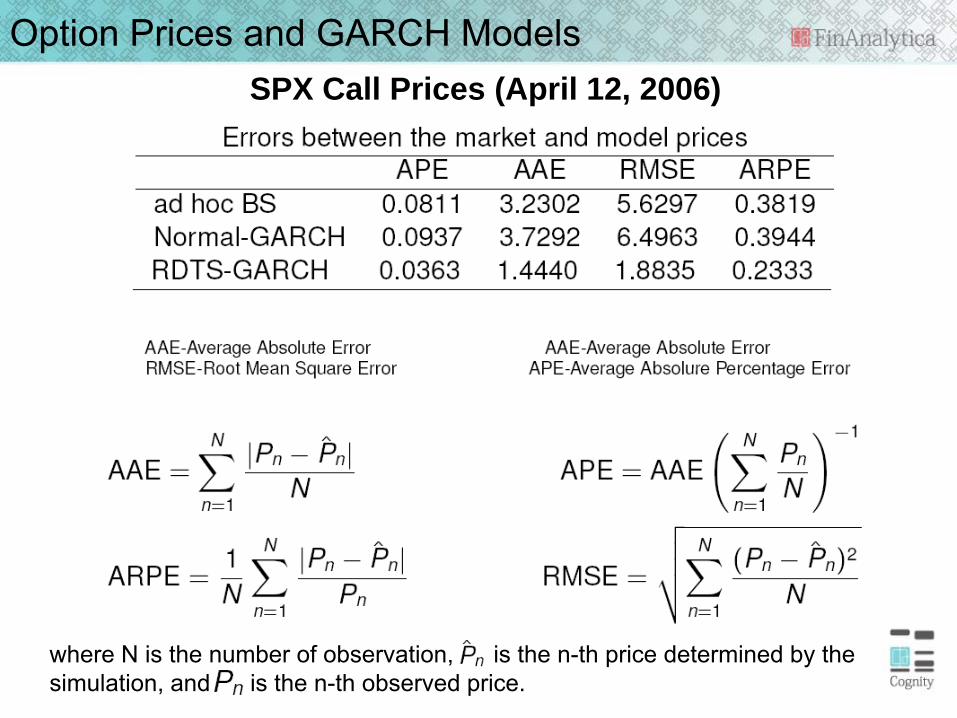

Option Prices and GARCH Models

where N is the number of observation, is the n-th price determined by thesimulation, and is the n-th observed price.

SPX Call Prices (April 12, 2006)

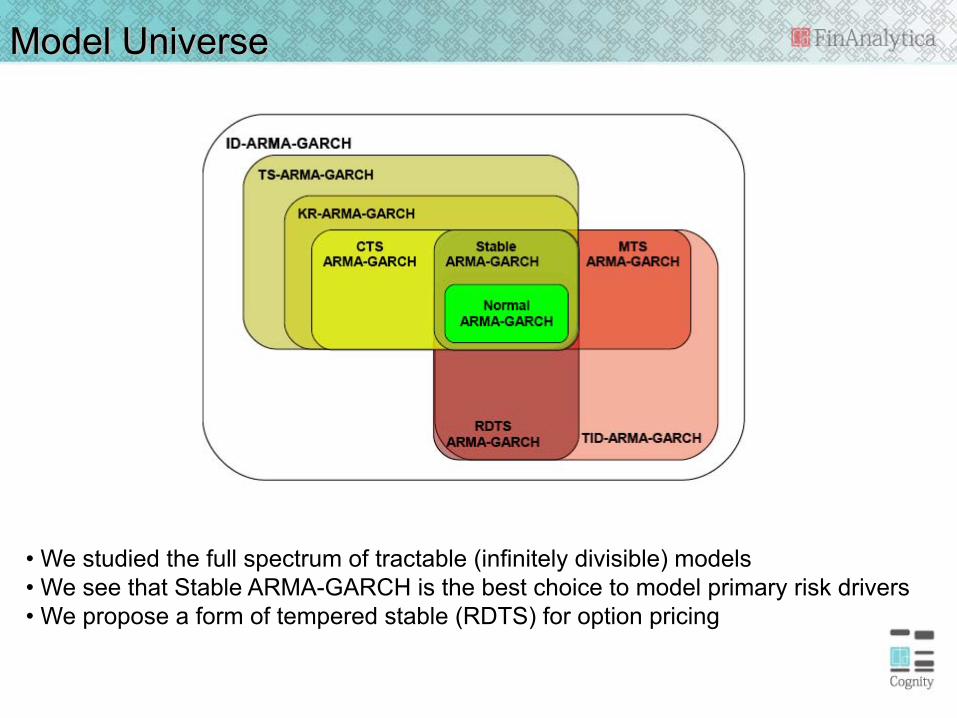

Model Universe

• We studied the full spectrum of tractable (infinitely divisible) models• We see that Stable ARMA-GARCH is the best choice to model primary risk drivers• We propose a form of tempered stable (RDTS) for option pricing

The Option Pricing Models Universe

References

Application 2 - Modeling Market Crashes

Daily Returns: S&P 500 Index

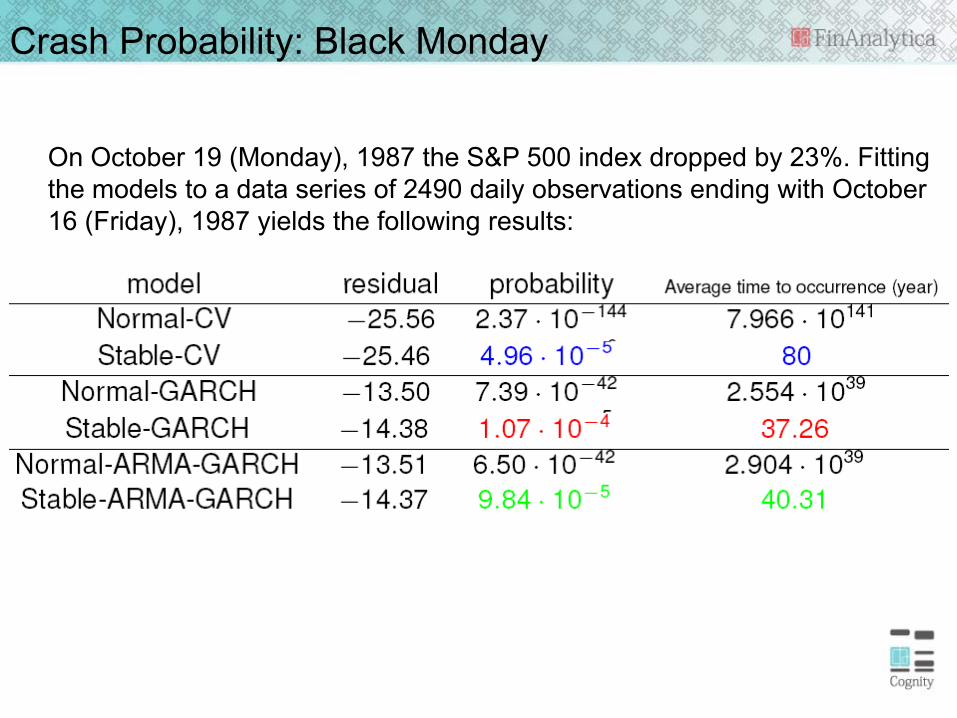

Crash Probability: Black Monday

On October 19 (Monday), 1987 the S&P 500 index dropped by 23%. Fitting the models to a data series of 2490 daily observations ending with October 16 (Friday), 1987 yields the following results:

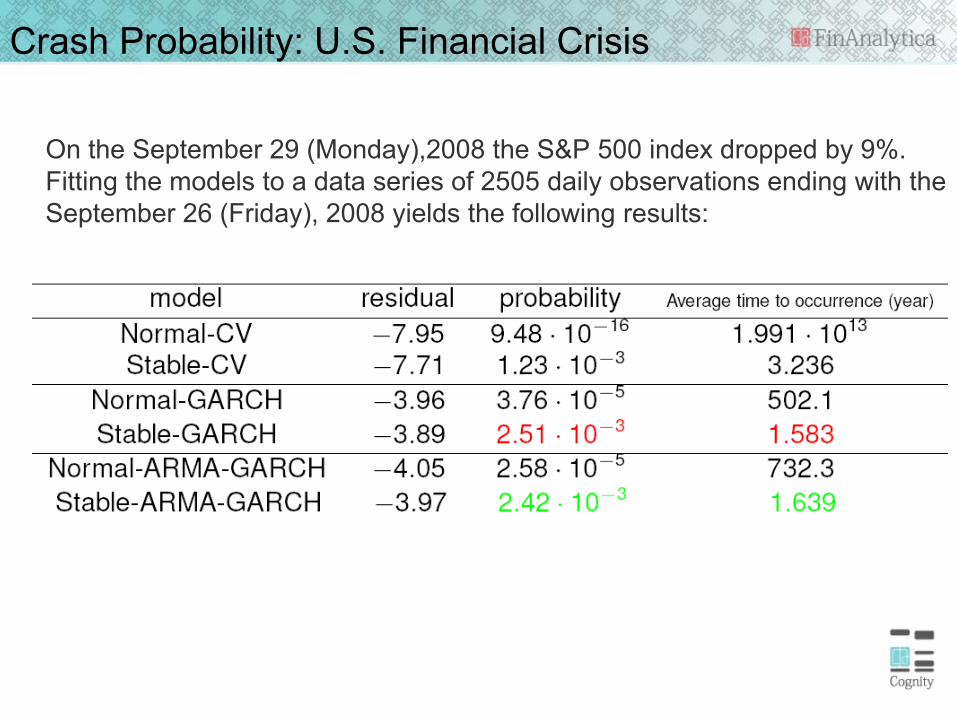

Crash Probability: U.S. Financial Crisis

On the September 29 (Monday),2008 the S&P 500 index dropped by 9%. Fitting the models to a data series of 2505 daily observations ending with the September 26 (Friday), 2008 yields the following results:

S&P Backtest

-0.3

-0.25

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.1520

03-1

1-11

2004

-01-

07

2004

-03-

04

2004

-04-

30

2004

-06-

28

2004

-08-

24

2004

-10-

20

2004

-12-

16

2005

-02-

11

2005

-04-

11

2005

-06-

07

2005

-08-

03

2005

-09-

29

2005

-11-

25

2006

-01-

23

2006

-03-

21

2006

-05-

17

2006

-07-

13

2006

-09-

08

2006

-11-

06

2007

-01-

02

2007

-02-

28

2007

-04-

26

2007

-06-

22

2007

-08-

20

2007

-10-

16

2007

-12-

12

2008

-02-

07

2008

-04-

04

2008

-06-

02

2008

-07-

29

2008

-09-

24

2008

-11-

20

2009

-01-

16

2009

-03-

16

2009

-05-

12

Return normal GARCH VaR 99% fat tail GARCH VaR 99% fat tail GARCH ETL 99%

References

Application 3 – Risk Monitoring

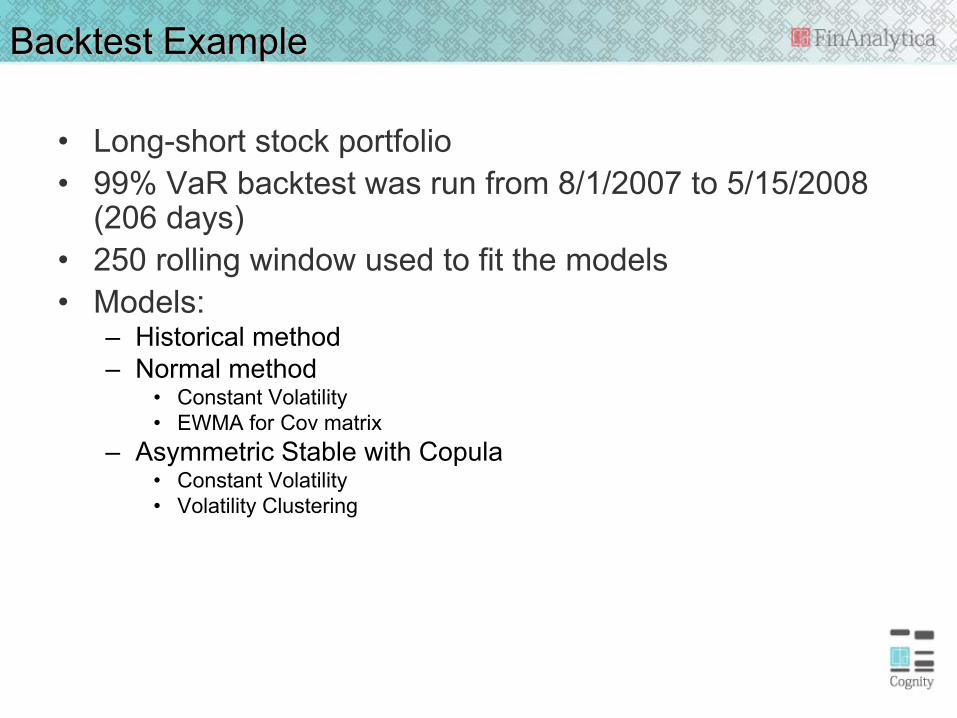

Backtest Example

• Long-short stock portfolio• 99% VaR backtest was run from 8/1/2007 to 5/15/2008

(206 days)• 250 rolling window used to fit the models• Models:

– Historical method– Normal method

• Constant Volatility• EWMA for Cov matrix

– Asymmetric Stable with Copula• Constant Volatility• Volatility Clustering

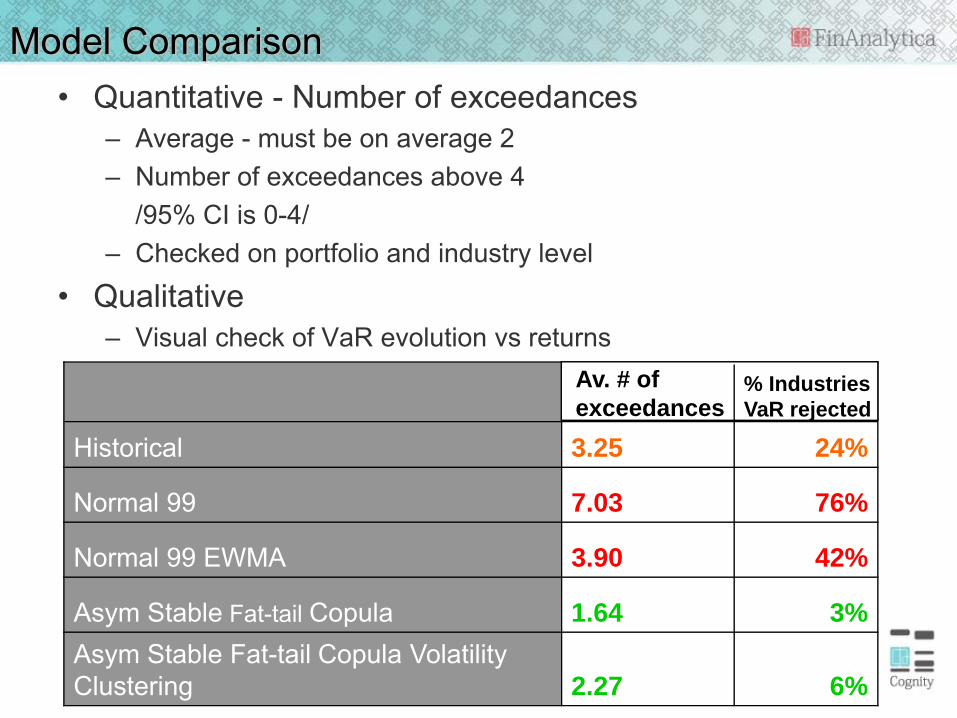

Model Comparison• Quantitative - Number of exceedances

– Average - must be on average 2– Number of exceedances above 4

/95% CI is 0-4/– Checked on portfolio and industry level

• Qualitative– Visual check of VaR evolution vs returns

Historical 3.25 24%

Normal 99 7.03 76%

Normal 99 EWMA 3.90 42%

Asym Stable Fat-tail Copula 1.64 3%Asym Stable Fat-tail Copula Volatility Clustering 2.27 6%

Av. # of exceedances

% Industries VaR rejected

Fat-tailed VaR with constant volatility provides long-term equilibrium VaR

Fat-tailed VaR with volatility clustering provides dynamic short-term view of the tail risk (VaR)

Both are important!

Returns

Normal 99

Normal 99 EWMA

Asym Stable Fat-tail Copula

Asym Stable Fat-tail Copula Vol Clustering

Risk Backtest

Application 4 – Portfolio Management and Optimization

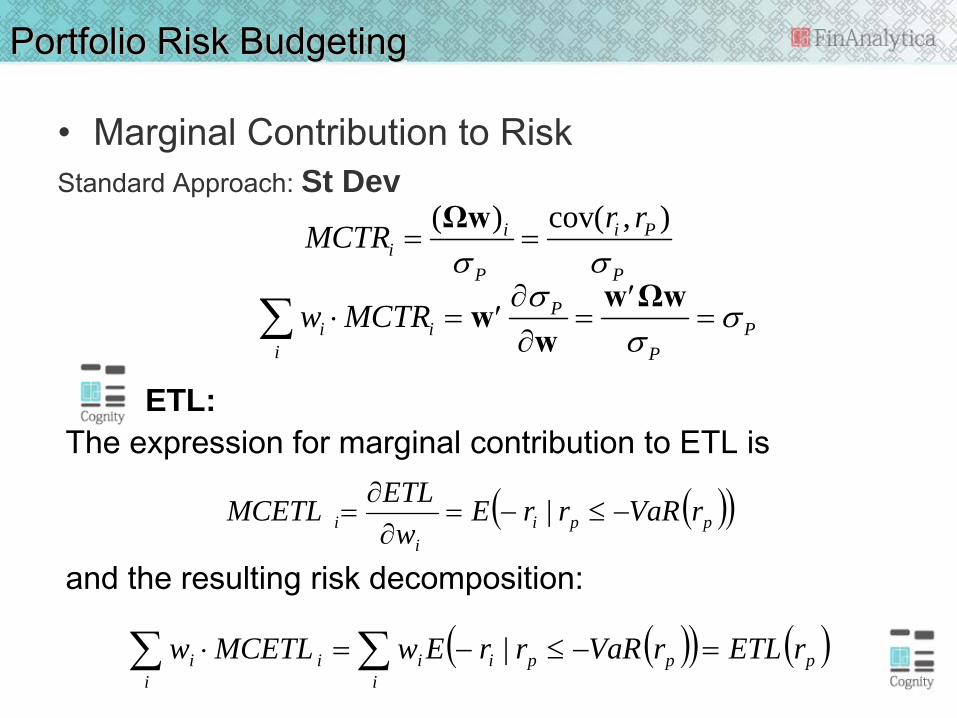

Portfolio Risk Budgeting

• Marginal Contribution to RiskStandard Approach: St Dev

( ) cov( , )i i Pi

P P

r rMCTRσ σ

= =Ωw

Pi i P

i P

w MCTR σσ

σ∂ ′

⋅ = = =′∂∑ w Ωwww

( )( )ppii

i rVaRrrEw

ETLMCETL −≤−=∂

∂= |

The expression for marginal contribution to ETL is

and the resulting risk decomposition:

( )( ) ( )pi

ppiii

ii rETLrVaRrrEwMCETLw =−≤−=⋅ ∑∑ |

ETL:

Portfolio Optimization

• Flexibility in problem types, a very general formulation is

where the first ETL is of a tracking-error type, the second one measures absolute risk and l ≤ Aw ≤ u generalizes all possible linear weight constraints

If future scenarios are generated, there are two choices: • Linearize the sample ETL function and solve as a LP• Solve as a convex problem

( ) ( )

⎪⎪

⎩

⎪⎪

⎨

⎧

≤≤=

−+−

uAwlew

ts

Erwrwrrw

T

TTb

T

w

1..

ETLETL min 21 αβ λλ

Portfolio Optimization References

Summary

• Modeling Fat-tailed world is a complex taskBUT crucial for:

• Option pricing– Explaining volatility smile– Identifying statistical arbitrage opportunities

• Crash warning indicators– Helps identify changes in the market structure faster

• Risk monitoring– Realistic understanding of risk and its evolution

• Portfolio construction and optimization– Achieve higher risk-adjusted returns

Q&A…

Thank you!