Market Analysis. The Degree of Competition Classifying markets number of firms freedom of entry to...

43

Market Analysis

-

Upload

ross-fleming -

Category

Documents

-

view

217 -

download

1

Transcript of Market Analysis. The Degree of Competition Classifying markets number of firms freedom of entry to...

Market Analysis

The Degree of Competition

Classifying markets number of firms freedom of entry to industry nature of product nature of demand curve

The four market structures perfect competition monopoly monopolistic competition oligopoly

Features of the four market structuresFeatures of the four market structures

Features of the four market structuresFeatures of the four market structures

Features of the four market structuresFeatures of the four market structures

Features of the four market structuresFeatures of the four market structures

Features of the four market structuresFeatures of the four market structures

Features of the four market structuresFeatures of the four market structures

The Degree of Competition Classifying markets

number of firms freedom of entry to industry nature of product nature of demand curve

The four market structures perfect competition monopoly monopolistic competition oligopoly

Structure conduct performance

Perfect Competition

Assumptions

firms are price takers

freedom of entry

identical products

perfect knowledge

Short-run equilibrium of the firm

price, output and profit

O

£

(b) Firm

Q (thousands)

O

(a) Industry

P

Q (millions)

S

D

Pe

MC

ARD = AR

= MR

Qe

AC

AC

Short-run equilibrium of industry and firm under perfect competition

Qe

P1

D1 = AR1

= MR1

AR1

O O

(a) Industry

P £

Q (millions)

S

D

(b) Firm

MC AC

AC

Q (thousands)

Loss minimising under perfect competitionLoss minimising under perfect competition

Perfect Competition

Assumptions firms are price takers freedom of entry identical products perfect knowledge

Short-run equilibrium of the firm price, output and profit

The short-run supply curve of the firm

O O

(a) Industry

P £

P1

Q (millions)

S

D1

(b) Firm

D1 = MR1

MC

P2

D2 = MR2

D2

P3

D3 = MR3

D3

Q (thousands)

Deriving the short-run supply curveDeriving the short-run supply curve

a

b

c

= S

Perfect Competition

Long-run equilibrium of the firm

all supernormal profits competed away

LRAC = AC = MC = MR = AR

O O

(a) Industry

P £

Q (millions)

S1

D

(b) Firm

LRAC

PL

P1

QL

Se

AR1 D1

ARL DL

Q (thousands)

Long-run equilibrium under perfect competition New firms enterSupernormal profits

Profits returnto normal

£

Q O

(SR)AC

(SR)MC

LRAC

AR = MR

DL

LRAC = (SR)AC = (SR)MC = MR = AR

Long-run equilibrium of the firm under perfect competition

Perfect Competition Benefits of perfect competition

price equals marginal cost

prices kept low

firms must be efficient to survive

In a perfectly competitive market supply and demand functions are

Qs = 1000P + 500 Qd = 5000 – 500P If variable cost function of a firm is

TVC = 103Q – 0.5Q2 1. Profit maximizing output for the firm 2. Economic profit?

XYZ Ltd., operating in a perfectly competitive market, sells a stationery item at Rs.10 per unit. The cost function is given as

TC = 4,000 + 4Q + 0.02Q2

1.The profit maximizing output for the firm?

Softy Cereals Inc. (SCI) produces and markets Tasties, a popular ready-to-eat breakfast cereal. The

demand and supply functions of Tasties are as follows:

QD = 150– 3P QS = 50 +10P.

If excise tax of Rs.3 is imposed on Tasties, what is the proportion of tax that will be borne by the consumers ?

Demand and supply functions for a product are: Qd = 10,000 – 4P Qs = 2,000 + 6P If the government imposes a sales tax of

Rs.100 per unit, what will be the new equilibrium price?

Monopoly Defining monopoly Barriers to entry

economies of scale economies of scope product differentiation and brand loyalty lower costs for an established firm ownership/control of key factors ownership/control over outlets legal protection mergers and takeovers aggressive tactics intimidation

Monopoly

The monopolist’s demand curve downward sloping

MR below AR

Equilibrium price and output Equilibrium output, where MC = MR

Profit maximising under monopolyProfit maximising under monopoly

MR

£

Q O

MC

Qm

Monopoly

The monopolist’s demand curve downward sloping

MR below AR

Equilibrium price and output Equilibrium output, where MC = MR

Equilibrium price, found from demand curve

£

Q O

MC

AC

Qm

MR

AR

AC

Profit maximising under monopolyProfit maximising under monopoly

AR

Monopoly

The monopolist’s demand curve downward sloping

MR below AR

Equilibrium price and output Equilibrium output, where MC = MR

Equilibrium price, found from demand curve

Profit Measuring profit

£

Q O

MC

AC

Qm

MR

AR

AC

Profit maximising under monopolyProfit maximising under monopoly

AR

Total profit

Monopoly The monopolist’s demand curve

downward sloping

MR below AR

Equilibrium price and output Equilibrium output, where MC = MR

Equilibrium price, found from demand curve

Profit Measuring profit

Supernormal profit can persist in long run

Monopoly

Disadvantages of monopoly high prices / low output: short run

AR = D

MC

MR

£

Q O Q1

P1

Monopoly

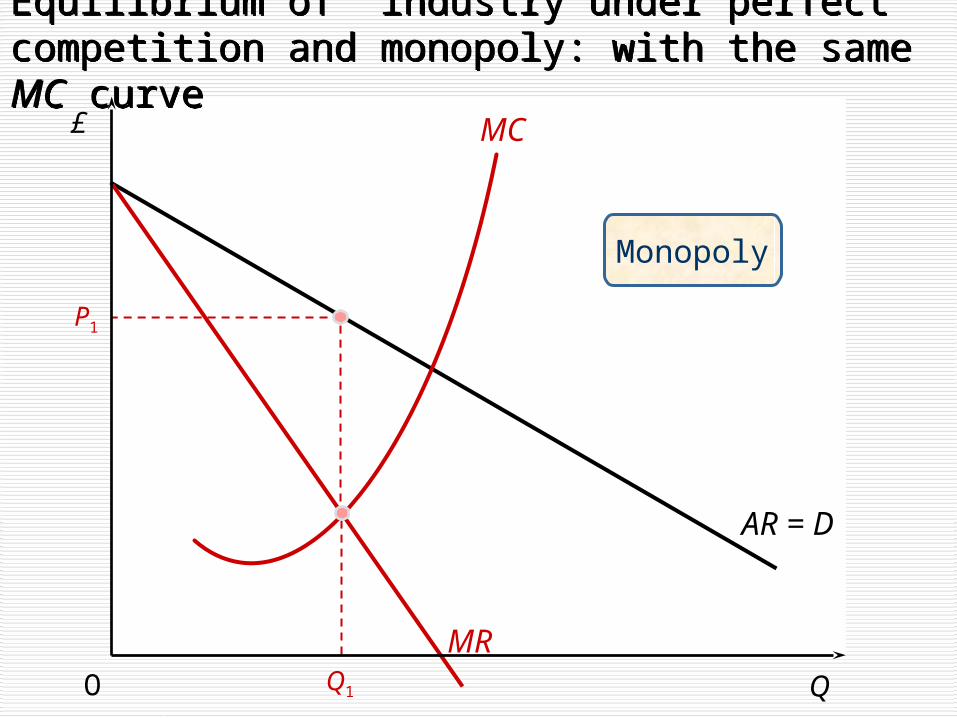

Equilibrium of industry under perfect competition and monopoly: with the same MC curve

Equilibrium of industry under perfect competition and monopoly: with the same MC curve

£

Q O

MC ( = supply under perfect competition)

Q1

MR

P1

P2

Q2

AR = D

Comparison withPerfect competition

Equilibrium of industry under perfect competition and monopoly: with the same MC curve

Equilibrium of industry under perfect competition and monopoly: with the same MC curve

Monopoly

Disadvantages of monopoly high prices / low output: short run

high prices / low output: long run

Monopoly

Disadvantages of monopoly high prices / low output: short run

high prices / low output: long run

lack of incentive to innovate

Monopoly

Disadvantages of monopoly high prices / low output: short run

high prices / low output: long run

lack of incentive to innovate

Monopoly

Disadvantages of monopoly high prices / low output: short run

high prices / low output: long run

lack of incentive to innovate

Advantages of monopoly

Monopoly

Disadvantages of monopoly high prices / low output: short run

high prices / low output: long run

lack of incentive to innovate

Advantages of monopoly economies of scale

£

Q O Q1

MR

P1

MCmonopoly

AR = D

Equilibrium of industry under perfect competition and monopoly: with different MC curves

Equilibrium of industry under perfect competition and monopoly: with different MC curves

£

Q O

MC ( = supply)perfect competition

Q1

MR

P1

P2

Q2

MCmonopoly

AR = D

x

Q3

P3

Equilibrium of industry under perfect competition and monopoly: with different MC curves

Equilibrium of industry under perfect competition and monopoly: with different MC curves

Monopoly

Disadvantages of monopoly high prices / low output: short run

high prices / low output: long run

lack of incentive to innovate

Advantages of monopoly economies of scale

profits can be used for investment

Demand functions of a monopolist in two effectively segmented markets are:

Qa = 1,000 – 50Pa

Qb = 800 – 25Pb

Total cost function of the monopolist is TC = 500 + 10Q. If the monopolist does not practice price discrimination,

what is the sales maximizing price ?

Price Discrimination

A firm sells in two markets and has constant marginal costs of production equal to $2 per unit. The demand and demand and marginal revenue equations for the two markets are as follows:

Market 1 Market 2 P1 = 14 – 2Q1 P2 = 10 – Q2

MR1 = 14 – 4Q1 MR2 = 10 – 2Q2

Using third-degree price discrimination, what are the profit-

maximizing prices and quantities in each market? Show that greater profits result from price discrimination than would be obtained if a uniform price were used.