Market Access Biosimilars

29

Copyright © 2016 QuintilesIMS. All rights reserved. Market Access Biosimilars Biosimilars weltweit, in Europa und Deutschland Dr. Frank Wartenberg President Central Europe

-

Upload

iqvia-germany -

Category

Healthcare

-

view

696 -

download

0

Transcript of Market Access Biosimilars

Copyright © 2016 QuintilesIMS. All rights reserved.

Market Access BiosimilarsBiosimilars weltweit, in Europa und Deutschland

Dr. Frank Wartenberg President Central Europe

1

57%

17%

5%

8%

12%

US EU5 Pharmerging Japan ROW

The US is driving the biologics market

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

50

100

150

200

250

2011 2012 2013 2014 2015G

row

th, L

CU

S$

Sal

es,

US

$ bi

llion

s

Biologics Sales Biologics growthSmall molecule growth Global Pharma growth

65%

11%

5%

9%

10%

Biologics – 2015 Share of sales

Biologics – Share of 5 yr growth

Global market trendsSales and Growth

Source: IMS Health, MIDAS, MAT Q4 2015; Share of growth in LC$. Brazil and Mexico non-retail included

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

2

Europe makes up 25% of global biologic sales and 87% of biosimilar sales

Source: IMS Health MIDAS Q2 2016

0

5

10

15

20

25

30

35

40

45

50

55

60

65

1,2001,1001,000

900800700

200

600500400300

0100

1,4001,300

PP

G %

11%

Bio

sim

ilar s

ales

, US

$, M

n89%

2016

2%3%8%

87%

2015

2%0%

10%

88%

2014

2%0%

11%

88%

2013

1%0%

12%

87%

2012

0%0%

OtherUSJapanEuropeGlobal Growth

Global Biosimilar market dynamics, $1.4Bn

01

23

45

67

89

1011

1213

14

0

240

220

200

180

160

140

120

100

80

60

40

20

Bio

sim

ilar s

ales

, US

$, B

n

2016

8%

62%

6%

25%

2015

8%

59%

6%

27%

2014

8%

54%

7%

31%

2013

8%

52%

8%

31%

2012

8%

50%

9%

33%

PP

G %

Global Biologic market dynamics, $228Bn

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

3

32%50%

8%

15%

31%

20%

7%

10%

18%

5%

2015 Pipeline (PII - Reg)

n = 848

3%

0%

2015 SalesUS$bn

$221Bn

Oncology and non-traditional areas are risingBiologic sales and Phase II+ pipeline by Therapy Area 2015

All Others

AutoimmuneAntidiabeticsOncologics

MSVaccines

Source: IMS Health MIDAS MAT Q4 2015

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

4

A wave of new markets is on the horizon

9910

121213141414

2125

2731

3642

Dengue fever

No. of pipeline candidates for indication

Uveitis

OsteoporosisStroke

OsteoarthritisMalariaCOPD

Heart failurePain

EbolaParkinson’s

AllergyHIV

AsthmaAlzheimer’s

Biologic pipeline: non-traditionalbiologic indications

(Pre-Clin to Reg)

Total 25% biologic pipeline

• Addressing areas traditionally dominated by small molecules –often highly genericised

• Many are chronic diseases with large patient populations

• Pipeline products initially targeting more severe subsections

• High cost per patient cause payer concern

• Mixed experience to date with pioneer biologics taking this route (Xolair in respiratory, Praluent in hyperlipidemia)

• Biologic specific challenges such as patient targeting, infrastructure and administration

Indication characteristics /challenges (outside vaccines)

VaccinesTherapeutic candidates

Source: IMS Health R&D Focus Q4 2015; Thought Leadership analysis

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

5

But NOBs market is nearly double biosimilarsConcentrated in BRICs and in TA’s with less complex biologics

2.5

2.0

1.5

1.0

0.5

0.0

28%

17%

11%

11%

2012

1.6

29%

18%

10%11%

2011

1.2

29%

20%9%

12%

20.5%

2015

2.1

25%

17%

13%

11%

2014

2.1

27%

16%

11%

11%

2013

1.9

Sal

es (U

S$

bn)

HGFsEPOsDiabetesBlood coagulationInterferonsOncologyOther Hema prodsMSAutoimmuneOthers

China68%

Russia12%

Brazil7%

India6%

Vietnam

2%

Turkey

2%

Pakistan

1%

Indonesia

1%

Others3%

Pharmerging: NOBs sales by TACAGR 2011-15

Pharmerging: NOBs sales by country

BRICs account for nearly 93% of NOBs value sales (up from

91% in 2011)

Pharmerging

Source: IMS Health MIDAS, Q4 2015

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

6

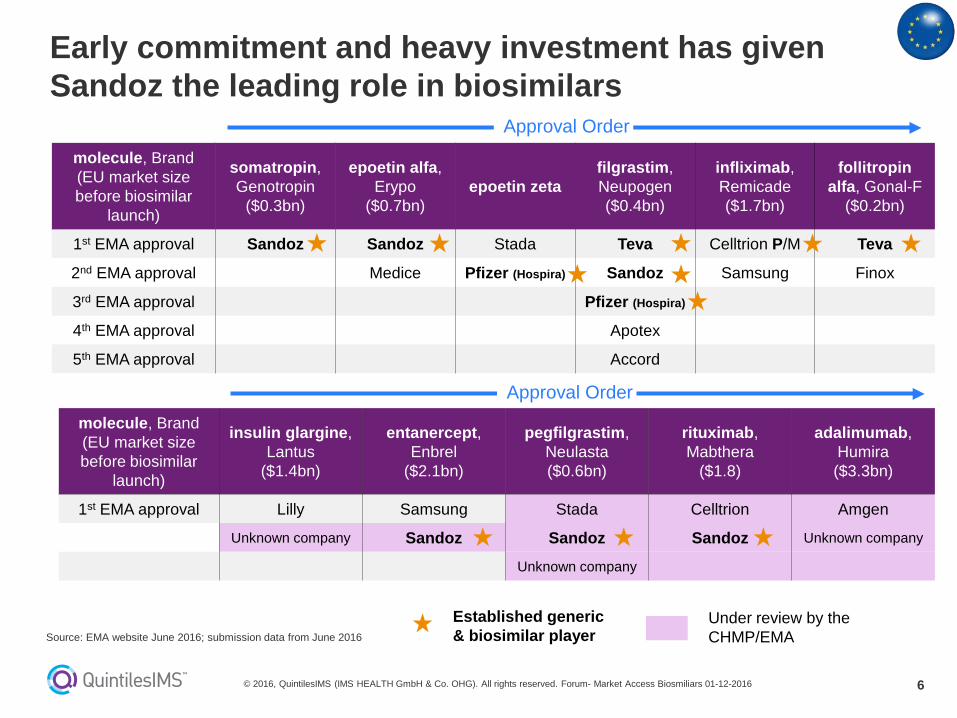

Early commitment and heavy investment has given Sandoz the leading role in biosimilars

molecule, Brand(EU market sizebefore biosimilar

launch)

somatropin, Genotropin

($0.3bn)

epoetin alfa, Erypo

($0.7bn)epoetin zeta

filgrastim, Neupogen($0.4bn)

infliximab, Remicade($1.7bn)

follitropinalfa, Gonal-F

($0.2bn)

1st EMA approval Sandoz Sandoz Stada Teva Celltrion P/M Teva

2nd EMA approval Medice Pfizer (Hospira) Sandoz Samsung Finox

3rd EMA approval Pfizer (Hospira)

4th EMA approval Apotex

5th EMA approval Accord

molecule, Brand(EU market sizebefore biosimilar

launch)

insulin glargine, Lantus

($1.4bn)

entanercept, Enbrel

($2.1bn)

pegfilgrastim, Neulasta($0.6bn)

rituximab, Mabthera

($1.8)

adalimumab,Humira($3.3bn)

1st EMA approval Lilly Samsung Stada Celltrion Amgen

Unknown company Sandoz Sandoz Sandoz Unknown company

Unknown company

Approval Order

Approval Order

Under review by the CHMP/EMA

Established generic& biosimilar player

Source: EMA website June 2016; submission data from June 2016

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

7

Infliximab biosimilar impact is patchy so far

Uptake of biosimilars quite slow in major markets

>90% biosimilar volume share in Denmark, Poland Norway and Finland. Tender system, with switching

Highest uptake of EU5 is 30% in the UK, and the lowest is France with 14%

Price cuts have not been dramatic in major market (at list price)

Discount to originator price pre-biosimilar entrance:

• France 10% (matched by originator)• UK 10%

• Poland 44% discount • Norway 69% discount

1.5

1.0

0.5

0.0

2.0

2016

$1.9Bn

1.7

0.10.1

2015

$1.9Bn

1.8

0.00.0

2014

$1.8Bn0.0

2013

$1.6Bn

2012

$1.5Bn

Infli

xim

ab s

ales

(LC

US

$ B

n)

InflectraRemsima Remicade

EU: Infliximab sales by brand name

Source: IMS Health MIDAS MAT Q1 2016; Uptake data from Feb 2016; Prices based on dosage and formulation with the highest revenue in 2015; price comparison is made some time before biosimilar entrance if the originator pre-emptively dropped price

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

8

The picture in pharmerging markets is fracturedGlobal Biosimilar Landscape

Proposed new concrete biosimilar approval guidelines in 2016

Behind in terms of regulation, particularly on clinical requirements and length of regulatory process

Established biosimilar legislation and guidance (PMDA)

Established biosimilar legislation and guidance aligned to EMA framework.

Fully established framework and solid draft guidance for biosimilar Mab.Substitution not allowed

Guidance published. Global reference product accepted

Regulatory maturity framework

Fully established framework

Lack of a clear framework

Legal pathway established, FDA guidelines published. Pathway now being tested

Pathway under development.Access through national andregional tenders

Guidance finalized in 2010. Dual pathway with abbreviated non-clinical and clinical data

Guidance finalized. No clear clinical criteria for biosimilar approval (case-by-case approach)

• Evolving regulatory framework of biosimilars in EMs varies by countries• Local policies will influence competition of biosimilars vs. NOBs (e.g. PDPs in Brazil)

Approval of a “biosimilar product”requires submission of an “abridged” application to the MOH. Biosimilarshave interchangeable status

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

9© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Im gesamten Pharmamarkt in Deutschland (Retail und Klinik) haben Biologika aktuell einen Umsatz von 9,7 Mrd. €

12%

88%

25%

75%

200524,8 Mrd. Euro

MAT 09/201639,2 Mrd. Euro

Quelle: IMS Dataview® , IMS AMV®, Total Euro Kalenderjahr 2005 zu MAT 9/2016

Biologika Umsätze haben sich verdreifacht

BiologikaNon Biologika

10

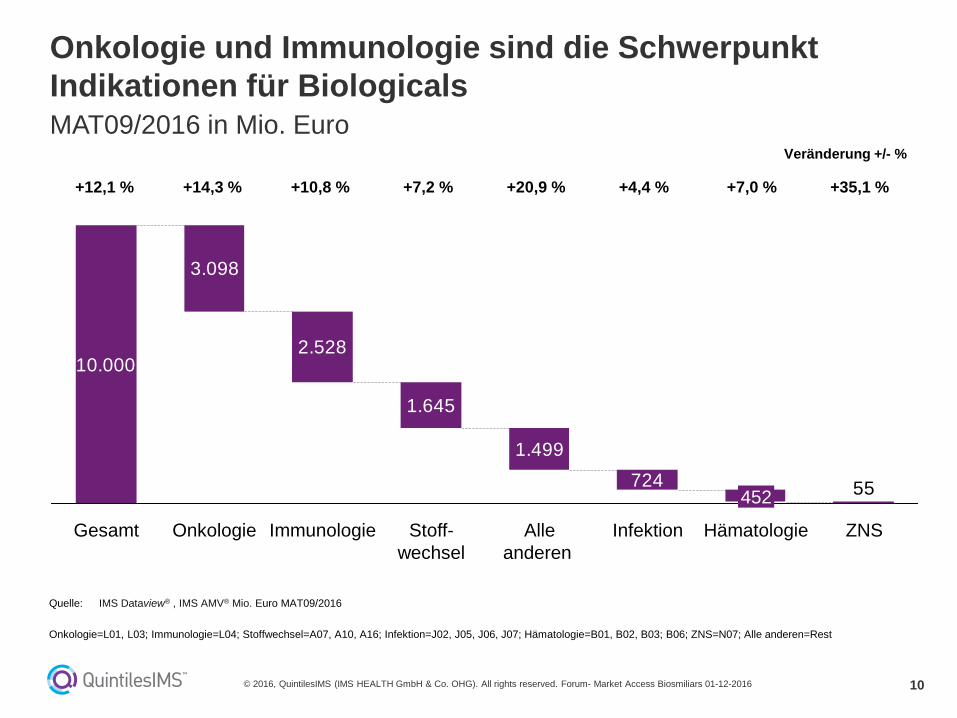

Onkologie und Immunologie sind die Schwerpunkt Indikationen für BiologicalsMAT09/2016 in Mio. Euro

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

10.000

3.098

2.528

1.645

1.499724 55

Stoff-wechsel

ImmunologieOnkologie Hämatologie

452

InfektionAlle anderen

Gesamt ZNS

+12,1 % +14,3 % +10,8 % +7,2 % +20,9 % +4,4 % +7,0 % +35,1 %

Quelle: IMS Dataview® , IMS AMV® Mio. Euro MAT09/2016

Onkologie=L01, L03; Immunologie=L04; Stoffwechsel=A07, A10, A16; Infektion=J02, J05, J06, J07; Hämatologie=B01, B02, B03; B06; ZNS=N07; Alle anderen=Rest

Veränderung +/- %

11© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Der Anteil der Biologika ist besonders hoch bei Onko-logie, Immunologie und Stoffwechselerkrankungen

ZNS

6%

Hämatologie

17%

Infektion

19%

Alle anderen

7%

Stoffwechsel

61%

Immunologie

77%

Onkologie

53%

Quelle: IMS Dataview® , IMS AMV® MAT05/2016

Onkologie=L01, L03; Immunologie=L04; Stoffwechsel=A07, A10, A16; Infektion=J02, J05, J06, J07; Hämatologie=B01, B02, B03; B06; ZNS=N07; Alle anderen=Rest

Biologika

5,1 Mio. Euro

3,6 Mio. Euro

2,5 Mio. Euro

5,1 Mio. Euro

19,0 Mio. Euro

2,4 Mio. Euro

0,6 Mio. Euro

12

Abhängig von der Indikation gibt es große Unterschiede für die Absatzanteile von BiosimilarsAbsatz in DDD im MAT 09/2016

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Quelle: IMS Dataview® , IMS PSN®, Gesamtmarkt DDD im MAT 09/2016

Epoetine (B03C):7,7 Mio. DDD

Filgrastim:0,1 Mio. DDD

Infliximab:2,3 Mio. DDD

Somatropin:1,5 Mio. DDD

Biosimilar 60%

Biotech BiosimilarBiosimilar 79%

Biotech Biosimilar

Biosimilar 15 %Biotech Biosimilar

Biosimilar 31%

Biotech Biosimilar

Etancercept:2,3 Mio. DDD

Biosimilar 4 %

Biotech Biosimilar

14

Die Marktdurchdringung von Insulin Glargin-Biosmilarsin Deutschland liegt bei etwa 5%

Wochendaten: Absatz Lantus/Toujeo (Original) und Abasaglar (Biosimilar) 2015 - 2016

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Quelle: IMS PharmaTrend® Rx Weekly – KW 46/2016

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

Toujeo + P

Insulin Glar

Lantus + P

4540353025 20151051 4640353025

Abasaglar +

20151051 50

Absatz absolut

53

Absatzeinbruch durch die Feiertage

15

Auf KV Ebene gibt es eine unterschiedliche Durchdringung der Infliximab-BiosimilarsGKV Defined Daily Dosages in Tsd. , 3. Quartal 2016

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Quelle: IMS Dataview® , IMS PharmaScope® National, Biosimilar INFLIXIMAB GKV DDD Tsd. CalQTR 3/2016 auf KV-Landesstellen Ebene

58%49% 49% 45% 43%

38% 38% 38%33% 31% 28% 28% 27% 27% 26% 25%

16%

42%51% 51% 55% 57%

62% 62% 62%67% 69% 72% 72% 73% 73% 74% 75%

84%

BremenBayernNieder-sachsen

Rheinland-Pfalz

HessenNordrheinSaarlandWestfalen-Lippe

SachsenBaden-Wuerttem-

berg

Schleswig-Holstein

ThueringenBranden-burg

Sachsen-Anhalt

BerlinHam-burg

Mecklen-burg-

Vorpommern

BiosimilarBiotech

16

Auch Biosmilar Anteil bei Etanercept in KV-WestfalenLippe deutlich höher, als in anderen KVenGKV DDD in Tsd. im CalQtr. 03/2016

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

35%

15% 11% 12% 12% 10% 10% 7% 9%

65%

85% 89% 88% 88% 90% 90% 93% 93% 91% 92% 94% 96% 95% 94% 96% 97%

7% 6%5%4%6%8% 4%

Sachsen

209

3%Thueringen

71

Hamburg

55

Branden-burg

126

Mecklen-burg-

Vorpommern

97

Sachsen-Anhalt

113

Bremen

9

Saarland

25

Schleswig-Holstein

114

Berlin

103

Bayern

244

Nieder-sachsen

238

Rheinland-Pfalz

91

Hessen

179

Baden-Wuerttemberg

234

Nordrhein

196

Westfalen-Lippe

185

Quelle: IMS Dataview® , IMS PharmaScope® National, Biosimilar Etanercept GKV DOT Tsd. CalQtr. 03/2016 auf KV-Landesstellen Ebene

BiosimilarBiotech

17© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

KV-spezifische Biosimilar-Quoten bei Epoetin-Präparaten (B03C) in DDD* für 2016 vs. tatsächlicher Marktanteil im CalQtr. 03 / 2016 (%) deutlich angestiegen

Quelle: IMS PharmaScope®, *Verordnungen in DDD=Defined Daily Dosages , jeweils für die KV-Region nach den Arzneimittelvereinbarungen 2016 geltende Quoten , bei KVenohne Quotenwert wurde keine Quote vereinbart,

70,1

82,1

89,0

89,3

89,4

93,763,5

56,4

49,5

55,0

47,5

58,2

63,3

60,3

59,5

51,1

55,0

60,9

55,0

68,2

52,2

21,2

47,5

92,3

90,2

88,2

88,0

87,8

86,8

86,1

86,0

74,2

70,4

58,6

Westfalen-Lippe

Berlin

Sachsen

Hamburg

Nordrhein

Sachsen-Anhalt

Schleswig-Holstein

Niedersachsen

Saarland

Rheinland-Pfalz

Brandenburg

Bremen

Hessen

Baden-Württemberg

Thüringen

Bayern

Mecklenburg-Vorpommern

Marktanteil Biosimilar/Epoetin-Präparaten Q3 / 2016KV-Biosimilar-Quote bei Epoetin-Präparaten 2016

18

Anteil Biosimilar an GKV-Markt sehr gering, am Biotechmarktsegment mit Biosmiliarkonkurrenz 16%3. Quartal 2016

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

ÜBRIGE76%

BIOSIMILAR1%

BIOTECH23%

GKV-gesamt9,5 Mrd. Euro zu AVP real*

Apothekenverkaufspreis nach Abzug Herstellerzwangsabschläge und Apothekenabschlag, 3. Quartal 2016

16%84%

GKV-Biotechmarkt mit Biosimilarkonkurrenz

433 Mio. Euro zu AVP real*

Anteil nur an Biotech3,1 %

19© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Auch bei Infliximab erfolgt der Großteil der Abgabe unter Rabattvertrag

83%90% 87%

98%

17%10% 13%

INFLECTRA

2%

REMSIMAREMICADEInfliximab

Quelle: IMS Dataview® , IMS Contract Monitor ® Account Anteil RV UN CalQTR 3/2016

MIT RB VERTRAGOHNE RB VERTRAG

82,9 Mio. UN 55,2 Mio. UN 5,5 Mio. UN 6,5 Mio. UN

17%

20%

62%

alle übrigenREMSIMA

INFLECTRA

REMICADE

InfliximabGKV UN

CalQTR 3/2016

1%

24,5 Mio. UN

20

Große Unterschiede beim Infliximab Biosimilar Einsatz,EU5 immer noch zurück, aber wachsendEuropa: Infliximab Biosimilar Marktanteil nach Behandlungstagen

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

0%

20%

40%

60%

80%

100%

M0 M10 M20 M30

Infli

xim

ab B

iosi

mila

r upt

ake

(trea

tmen

t day

s)

Denmark Poland Norway ItalyUK Spain Germany FranceFinland Croatia Hungary Czech Republic

97%

94%

39%

50%

30%

19%

27%

EU5

Tender system markets

Other European countries

100%

90%

Source: QuintilesIMS MIDAS MTH July 2016 ; Denmark data from MIDAS Monthly Restricted database; Latvia excluded because only biosimilar manufacturers present in market

21© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Tender Typen und ihre Implikationen

Nonexclusive Tender Exclusive Tender Class Tender

Positivliste fürArzneimittel

Das Originalpräparat und typischerweise ein Biosimilarwerden in die Positivliste aufgenommen

Nur ein Produkt pro INN wird in die Positivliste für neue und existierende Kunden aufgenommen

Alle Produkte einer Klasse werden in die Positivliste aufge-nommen und nach Kosten sortiert

Implikationen Ärzte verschreiben Produkte nach eigenem Ermessen und gesetzlichen Richtlinien/Vorgaben

Alle Patienten werden auf das Produkt, das den Tendervertrag gewonnen hat umgestellt

Das Produkt, das die Ausschreibung ge-wonnen hat, soll der Richtlinie nach ver-schrieben werden, Ärzte können von dieser Vorgabe abweichen

Märkte

22

• Ausschreibung durch Krankenkassen i.d.R. alle zwei Jahre (den größten Markteinfluss hat hier die AOK als größte Krankenkasse [~35% aller Versicherten])– Kriterium: Behandlungskosten eines

Patienten im ersten Jahr– Gewährte Rabatte fallen unter den

Wettbewerbsschutz– Welches das günstigste Produkt ist,

kann zwischen den Krankenkassen (bzw. Krankenkassenvertretungen) variieren, je nachdem wie hoch der Rabattvertrag ausfällt bzw. ob mit diesem Hersteller überhaupt ein Vertrag abgeschlossen worden ist– 118 Krankenkassen laut GKV [2016]

• Staatliche Ausschreibung einmal jährlich– Kriterium: Behandlungskosten eines

Patienten im ersten Jahr– Gebotene Rabatte nachträglich

öffentlich einsehbar– Vier regionale Krankenkassen in

Norwegen– Das Produkt, das bei der

Ausschreibung den Zuschlag erhält, hat automatisch die landesweite Abdeckung sicher

• Rabatte in Höhe von bis zu 89% (im Hospital-) und 25% - 50% (im Nicht-Hospitalbereich)

Rabattverträge/Tender ContractsNorwegen

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Deutschland

23

• Staatliche Ausschreibungen– Kriterium: Behandlungskosten eines

Patienten im ersten Jahr– Eine staatliche Krankenkasse, in der

jeder Erwerbstätige versichert ist Das Produkt, das bei der

Ausschreibung den Zuschlag erhält, hat automatisch die landesweite Abdeckung sicher und wird an alle Krankenhäuser des Landes geliefert Während in anderen Ländern das

Originalprodukt ebenso vom Arzt verschrieben werden könnte, wird in Polen nur das Produkt verschrieben, das die Ausschreibung gewonnen hat

• Staatliche Ausschreibung einmal jährlich– Kriterium: Behandlungskosten eines

Patienten im ersten Jahr– Fünf regionale Krankenkassen– Das Produkt, das bei der

Ausschreibung den Zuschlag erhält, hat automatisch die landesweite Abdeckung sicher und wird an alle Krankenhäuser des Landes geliefert Es findet eine Umstellung nicht nur

bei neuen Kunden, sondern auch existierenden Kunden statt (so konnte Infliximab in so kurzer Zeit eine Marktabdeckung von 97% erreichen)

Rabattverträge/Tender ContractsDänemark

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Polen

24

Information an ÄrzteUmfrage des Deutschen Arzt Portals (28.09.2016)

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

25© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Zitate

„Die sowohl von pharmazeutischen Unternehmern der Originalpräparate als auch von Ärzten geäußerten Bedenken gegen die Verordnung von Biosimilarsbetrafen vor allem ihre Wirksamkeit und Sicherheit (aufgrund der potenziellen Immunogenität aller Biologika), aber auch die Austauschbarkeit mit dem Referenzarzneimittel. Marktrücknahmen von Biosimilars aufgrund von unzureichender Wirksamkeit oder schwerer Nebenwirkungen, die gegen eine Austauschbarkeit zwischen Biosimilars und Referenzarzneimitteln sprechen würden, sind jedoch bisher nicht erfolgt.“

Arzneimittelverordnungsreport 2016

„Nach derzeitigem Diskussionsstand im CHMP und seinen Arbeitsgruppen können Biosimilars grundsätzlich nach erwiesener Äquivalenz und erfolgter Zulassung so eingesetzt werden wie Originatorprodukte auch. Dies beinhaltet implizit daher sowohl Patienten, die vorher noch keine Therapie mit Biologikaerhalten, als auch solche Patienten, die vorher das Originatormolekülbekommen haben.“

- Paul Ehrlich Institut

26© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

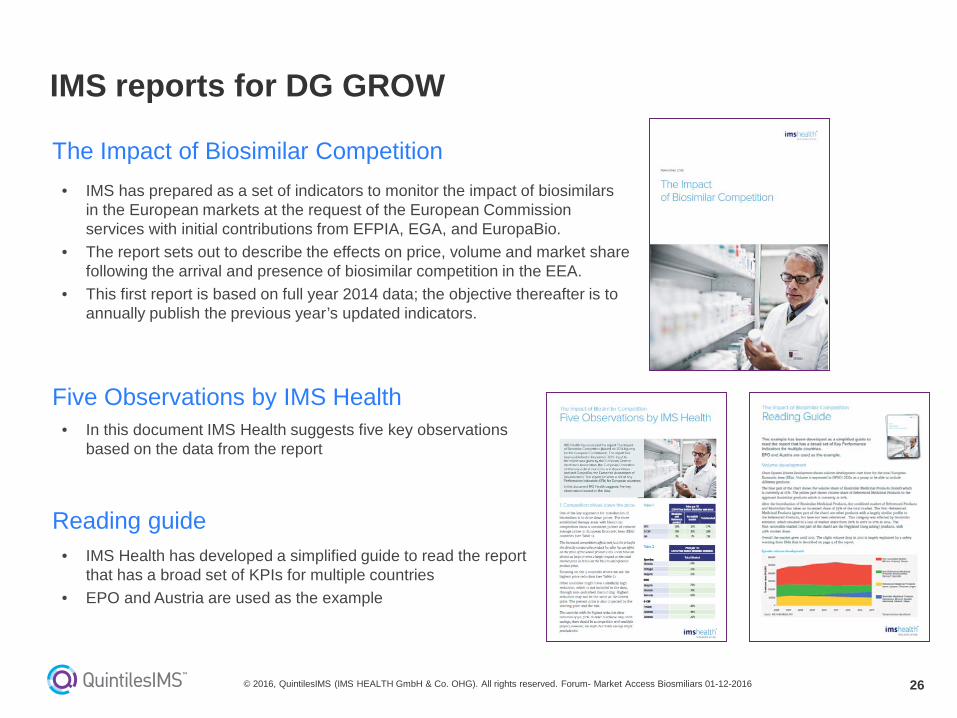

IMS reports for DG GROW

• IMS has prepared as a set of indicators to monitor the impact of biosimilars in the European markets at the request of the European Commission services with initial contributions from EFPIA, EGA, and EuropaBio.

• The report sets out to describe the effects on price, volume and market share following the arrival and presence of biosimilar competition in the EEA.

• This first report is based on full year 2014 data; the objective thereafter is to annually publish the previous year’s updated indicators.

The Impact of Biosimilar Competition

Five Observations by IMS Health

Reading guide

• In this document IMS Health suggests five key observationsbased on the data from the report

• IMS Health has developed a simplified guide to read the report that has a broad set of KPIs for multiple countries

• EPO and Austria are used as the example

27

Should you require further information, I would be pleased to assist:

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Dr. Frank WartenbergPresident Central Europe

[email protected]+49 (0) 69 6604-4315

28© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

Contact us at

quintilesims.com

29

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG)

All rights reserved. This information may not be reproduced, stored, processed, or made accessible in any way in whole or in part, without the prior express permission of QuintilesIMS (IMS HEALTH GmbH & Co. OHG).

The terms "patient," "physician," "physician's office," "prescriber," or "pharmacy" possibly used in this document in connection with data do not refer to personal information but exclusively (pursuant to § 3 (6) Federal Data Protection Act) to anonymous information.

Through the use of state-of-the-art technologies and processes, IMS ensures that its services comply with data protection regulations, regardless of how the data are linked to each other

© 2016, QuintilesIMS (IMS HEALTH GmbH & Co. OHG). All rights reserved. Forum- Market Access Biosmiliars 01-12-2016

![[SAMPLE] Specialty Physicians Discuss Their Opinions of the U.S. Biosimilars Market](https://static.fdocuments.net/doc/165x107/554b9490b4c905463d8b4a5c/sample-specialty-physicians-discuss-their-opinions-of-the-us-biosimilars-market.jpg)