Market abuse e book

31

The Netherlands | Singapore | Germany I UK I USA Date: Author: January 2016 Double Effect Market Abuse An introduction – Free e-book

-

Upload

doubleeffecttraining -

Category

Economy & Finance

-

view

867 -

download

0

Transcript of Market abuse e book

The Netherlands | Singapore | Germany I UK I USA

Date:

Author:

January 2016

Double Effect

Market AbuseAn introduction – Free e-book

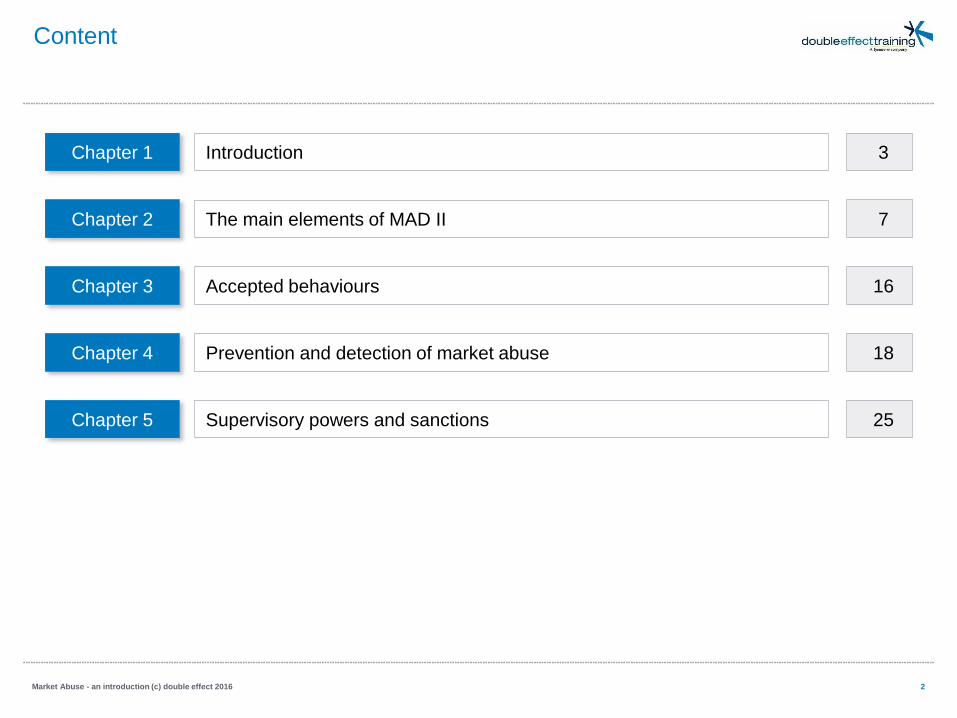

Content

2Market Abuse - an introduction (c) double effect 2016

IntroductionChapter 1 3

The main elements of MAD IIChapter 2 7

Accepted behavioursChapter 3 16

Prevention and detection of market abuseChapter 4 18

Supervisory powers and sanctionsChapter 5 25

1. Introduction - MAD: in the beginning

There is new legislation on the horizon: the Criminal Sanctions for Market Abuse Directive (CSMAD) and the

Market Abuse Regulation (MAR), together called MAD II. With the entry into force on 3 July 2016, MAD II is

getting close. Because of this, it is necessary to assess the regulation and its impact on your firm.

Background of MAD:

In 2003, the first Market Abuse Directive (MAD I) introduced rules on market abuse, which encompasses

insider dealing, the misuse of inside information and the manipulation of market prices through practices such

as dissemination of rumours. In June 2014, the final texts of MAD II were published in the Official Journal of

the EU. MAD II intends to address shortcomings of MAD I by broadening the scope of the regime in several

ways. The aim of the new regime remains unaltered: to ensure the integrity and transparency of EU financial

markets.

This e-book aims at giving an introduction into the rules of MAD II, the areas of impact, timelines, the

implications for individual firms and finally it will provide some suggestions on how to prepare for

compliance.

3Market Abuse - an introduction (c) double effect 2016

1. Introduction - Objectives of MAD I

4

Harmonization

› Harmonized regime of

insider dealing and market

manipulation regulations

Inside Information

› Elaborated rules on

disclosure and publication

of inside information

Supervision

› A minimally harmonized set

of supervisory and

investigatory powers

Ensure integrity and transparency of EU financial markets

Market Abuse - an introduction (c) double effect 2016

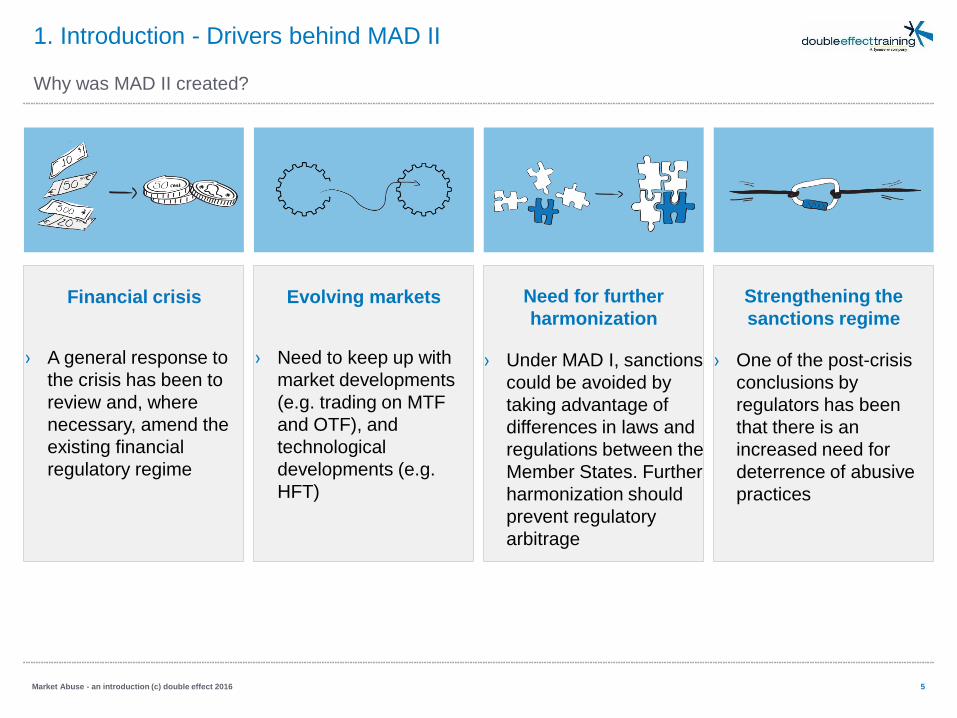

1. Introduction - Drivers behind MAD II

Why was MAD II created?

Financial crisis

› A general response to

the crisis has been to

review and, where

necessary, amend the

existing financial

regulatory regime

Evolving markets

› Need to keep up with

market developments

(e.g. trading on MTF

and OTF), and

technological

developments (e.g.

HFT)

Need for further

harmonization

› Under MAD I, sanctions

could be avoided by

taking advantage of

differences in laws and

regulations between the

Member States. Further

harmonization should

prevent regulatory

arbitrage

Strengthening the

sanctions regime

› One of the post-crisis

conclusions by

regulators has been

that there is an

increased need for

deterrence of abusive

practices

5Market Abuse - an introduction (c) double effect 2016

1. Introduction - Timeline

Expected timeline for MAD II (MAR and CSMAD)

6Market Abuse - an introduction (c) double effect 2016

Jan.

2016

2 Feb.

2015

MAR and delegated

acts apply:

Firms must be

compliant

Commission prepares

and adopts the

implementing acts

MAR and CSMAD

officially published

12 Jun.

2014

3 Jul.

2016

CSMAD transposed into

national law and

application of measures

Sep.

2015

Jul.

2015

Extension of deadline of

the technical standards

to Sep. 2015

28 September 2015

final RTS published by

ESMA

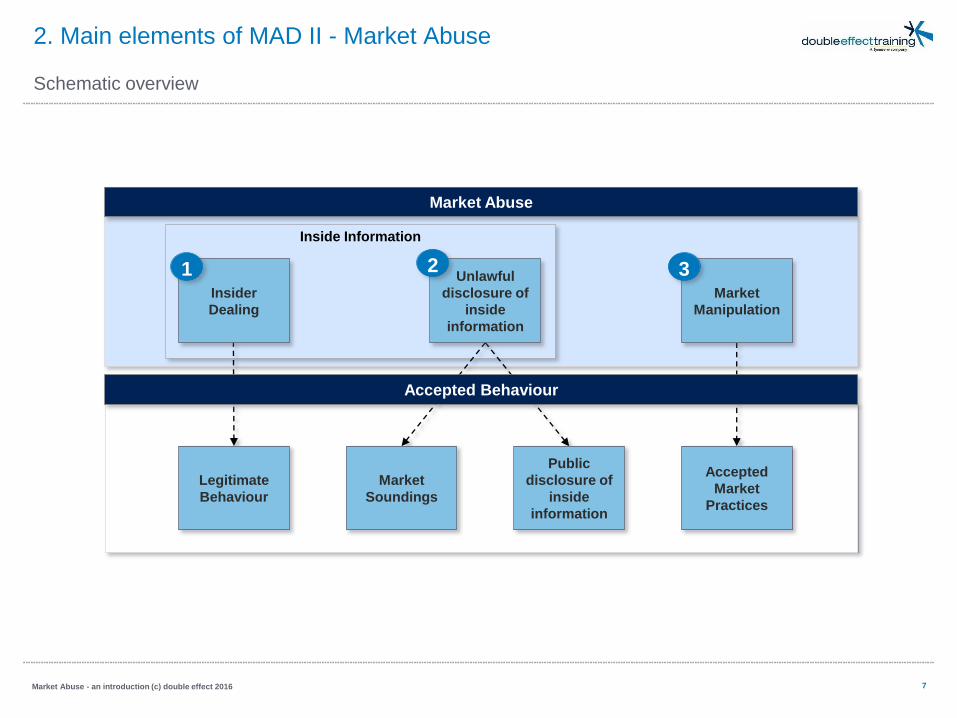

2. Main elements of MAD II - Market Abuse

Schematic overview

7Market Abuse - an introduction (c) double effect 2016

Inside Information

Market Abuse

Unlawful

disclosure of

inside

information

Insider

Dealing

Market

Soundings

Legitimate

Behaviour

Accepted Behaviour

Market

Manipulation

Public

disclosure of

inside

information

Accepted

Market

Practices

1 2 3

Information of a precise

nature which has not been

made public relating directly

or indirectly to one or more

issuers or one or more relevant

instruments which, if made

public would have significant

impact on the price of those

instruments

2. Main elements of MAD II - Inside information

Inside information

› Further criteria concerning the definition of inside

information in relation to commodity derivatives

› Information relating to emission allowances and

related to auctioned products included

› Intermediate step in protracted process can also be

deemed inside information (e.g. state of contract

negotiations)

› Reasonable Investor test included in the regulation

allowing for broader interpretation than under MAD I

New to MAR

8Market Abuse - an introduction (c) double effect 2016

Definition of Inside information serves as the basis for the Insider Dealing and

Unlawful disclosure of inside information offences

Central definition to market abuse offences

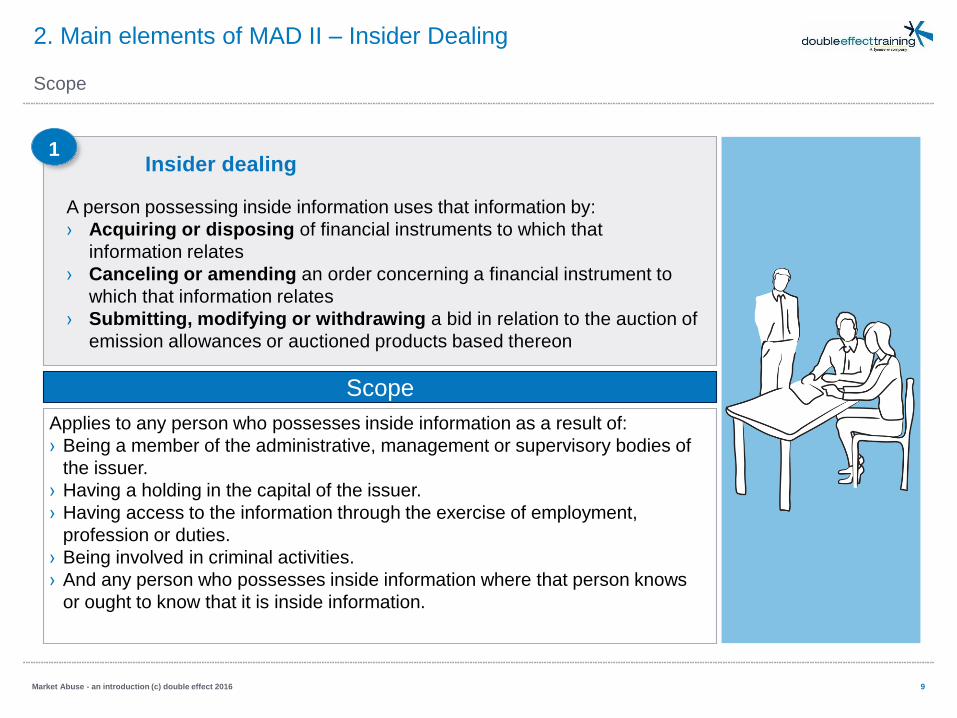

Insider dealing

A person possessing inside information uses that information by:

› Acquiring or disposing of financial instruments to which that

information relates

› Canceling or amending an order concerning a financial instrument to

which that information relates

› Submitting, modifying or withdrawing a bid in relation to the auction of

emission allowances or auctioned products based thereon

2. Main elements of MAD II – Insider Dealing

1

Scope

Applies to any person who possesses inside information as a result of:

› Being a member of the administrative, management or supervisory bodies of

the issuer.

› Having a holding in the capital of the issuer.

› Having access to the information through the exercise of employment,

profession or duties.

› Being involved in criminal activities.

› And any person who possesses inside information where that person knows

or ought to know that it is inside information.

9Market Abuse - an introduction (c) double effect 2016

Scope

2. Main elements of MAD II - Insider Dealing

New to MAR

Insider dealing1

10

New to MAR

› Recommending or inducing others to engage in insider dealing

is prohibited.

› Acting on those recommendations or inducements amounts to

insider dealing if the person who acts knows, or aught to know

that it is based on inside information.

› Cancelling or amending an order can amount to insider

dealing.

Market Abuse - an introduction (c) double effect 2016

Unlawful disclosure of inside information

Unlawful disclosure of inside information arises when a person possesses

inside information and discloses that information to any other person

2

Scope

Applies to any person who possesses inside information as a result of

› Being a member of the administrative, management or supervisory bodies

of the issuer.

› Having a holding in the capital of the issuer.

› Having access to the information through the exercise of employment,

profession or duties.

› Being involved in criminal activities.

› And any person who possesses inside information where that person knows or

ought to know that it is inside information.

11Market Abuse - an introduction (c) double effect 2016

Scope

2. Main elements of MAD II – Unlawful disclosure of inside information

Unlawful disclosure of inside information2

12

New to MAR

› Market abuse now explicitly encompasses the offence of

unlawful disclosure of information.

› Onward disclosure of mentioned recommendations or

inducements can also amount to unlawful disclosure of inside

information where the person disclosing the recommendation

or inducement knows of or ought to know that it was based on

banned inside information.

Market Abuse - an introduction (c) double effect 2016

2. Main elements of MAD II – Unlawful disclosure of inside information

New to MAR

Market manipulation

Market manipulation is the practice of interfering in the free and fair operation

of a market to create a misleading impression in an attempt to gain a market

advantage.

2. Main elements of MAD II – Market Manipulation

3

Scope

The scope of market manipulation is extended in several ways. These are best

explained by the differences with MAD I on the next page.

13Market Abuse - an introduction (c) double effect 2016

Scope

2. Main elements of MAD II – Market Manipulation

Market manipulation3

14

New to MAR

› Manipulating benchmarks, particularly by transmitting false or

misleading information or providing misleading inputs where

the perpetrator knows or ought to know that the information or

inputs are false or misleading.

› Attempted market manipulation is now prohibited.

› Market manipulation rules now extend to spot commodity

contracts.

› Placing, cancelling or modifying orders to manipulate supply,

demand or price is now prohibited.

› A non-exhaustive list of indicators and example practices are

provided in ESMA’s Technical Advice.

Market Abuse - an introduction (c) double effect 2016

New to MAR

2. Main elements of MAD II – Exemptions

Buy-Back & stabilisation

Market Abuse - an introduction (c) double effect 2016 15

Relevant for Member States, members

of the ESCB, a ministry, agency or SPV

of a Member State.

Exemption

Monetary and public

debt management

Buy-back programsExempted from Insider

dealing and Market

Manipulation

Scope

New to MAD II: Comparable to MAD I, but conditions in more detail.

Relevant for issuers

Relevant for issuers, offerors or other

entities undertaking the stabilisation.

Exempted from the

whole of MAR

Stabilisation

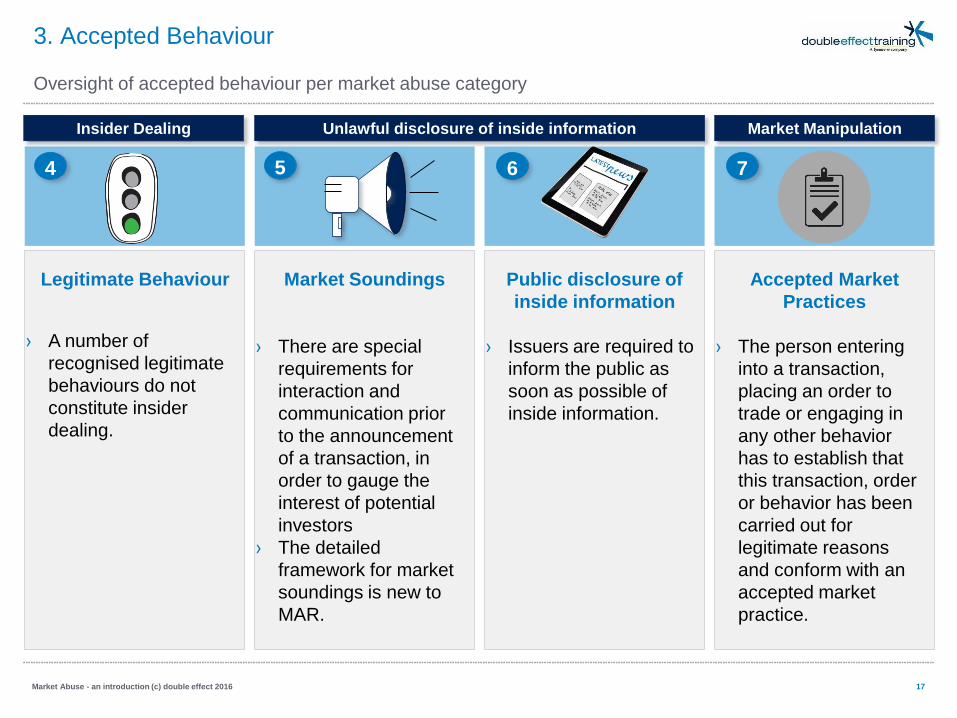

3. Accepted Behaviour

Schematic overview

16Market Abuse - an introduction (c) double effect 2016

Inside Information

Market Abuse

Unlawful

disclosure of

inside

information

Insider

Dealing

Market

Soundings

Legitimate

Behaviour

Accepted Behaviour

Market

Manipulation

Public

disclosure of

inside

information

Accepted

Market

Practices

4 5 6 7

Unlawful disclosure of inside information

Legitimate Behaviour

› A number of

recognised legitimate

behaviours do not

constitute insider

dealing.

Market Soundings

› There are special

requirements for

interaction and

communication prior

to the announcement

of a transaction, in

order to gauge the

interest of potential

investors

› The detailed

framework for market

soundings is new to

MAR.

Public disclosure of

inside information

› Issuers are required to

inform the public as

soon as possible of

inside information.

Accepted Market

Practices

› The person entering

into a transaction,

placing an order to

trade or engaging in

any other behavior

has to establish that

this transaction, order

or behavior has been

carried out for

legitimate reasons

and conform with an

accepted market

practice.

Insider Dealing Market Manipulation

17Market Abuse - an introduction (c) double effect 2016

3. Accepted Behaviour

Oversight of accepted behaviour per market abuse category

4 5 6 7

4. Prevention and detection of market abuse

18

Insider lists

› MAD II renews and revises

insider lists. Also, such lists

may serve issuers or such

persons to control the flow of

inside information and thereby

help manage their

confidentiality duties.

1

Market Abuse - an introduction (c) double effect 2016

3 important themes

Organizations will have extended responsibilities in preventing and detecting market abuse.

Internal systems and

procedures

› Market operators and

investment firms that operate a

trading venue shall establish

and maintain effective

arrangements, systems and

procedures aimed at

preventing and detecting

insider dealing, market

manipulation and attempted

insider dealing and market

manipulation.

3

Manager’s transactions

› Greater transparency of

transactions conducted by

persons discharging

managerial responsibilities and

persons closely associated

with them. This is valuable for

both market participants and

competent authorities.

2

Insider lists

Issuers or any person acting on their behalf shall:

› Draw up a list of all persons who have access to inside information and

are under employment or otherwise performing tasks.

› Update the insider list promptly in case of certain changes.

› Provide the insider list to the competent authority as soon as possible

upon its request.

4. Prevention and Detection of Market Abuse – Insider Lists

1

Scope

Applies to:

› Issuers who have requested or approved admission to a Regulated Market.

› In the case of instruments only traded on an MTF or OTF: Issuers who have

approved trading of their financial instruments on an MTF or OTF, or have

requested trading on an MTF.

› It also applies to emission allowance market participants.

19Market Abuse - an introduction (c) double effect 2016

Scope

4. Prevention and Detection of Market Abuse – Insider Lists

Content

Insider lists 1

20

Content

› Identity of any person having access to inside information.

› The reason for including that person on the list.

› The date and time at which that person obtained access to

inside information.

› The date and time at which the person ceased to have access

to the information.

Market Abuse - an introduction (c) double effect 2016

Manager’s transactions

Persons discharging managerial responsibilities, as well as persons closely

associated with them shall notify the issuer and the competent authority of

every transaction conducted on their own account relating to the shares

or debt instruments of that issuer.

4. Prevention and Detection of Market Abuse – Manager’s transactions

2

Scope

› Applies once the total amount of transactions has reached the threshold of

€ 5000,- .

› Applies to issuers who have requested or approved admission of their

financial instruments to trading on a regulated market or an MTF, or have

approved trading on an OTF.

21Market Abuse - an introduction (c) double effect 2016

Scope

4. Prevention and Detection of Market Abuse – Manager’s transactions

Content

Manager’s transactions2

22

Content

› Name of the person.

› Reason for notification.

› Name of relevant issuer or emission allowance market

participant.

› Description and identifier of the financial instrument.

› Nature, date and place of transaction.

› Price and volume of transaction.

Market Abuse - an introduction (c) double effect 2016

Internal systems and procedures

› Market operators and investment firms that operate a trading venue shall

establish and maintain effective arrangements, systems and procedures

aimed at preventing and detecting insider dealing, market manipulation

and attempted insider dealing and market manipulation.

› Any person professionally arranging or executing transactions shall

establish and maintain effective arrangements, systems and procedures

to detect and report suspicious orders and transactions.

.

4. Prevention and detection of market abuse: Internal systems and

procedures

3

Scope

› Market Operators and Investment Firms operating a trading venue.

› Any person professionally arranging or executing transactions.

23Market Abuse - an introduction (c) double effect 2016

Scope

4. Prevention and detection of market abuse: Internal systems and

proceduresContent

Internal systems and procedures3

24

Content

› Automated surveillance systems: Dependent upon size,

nature and activities of the entity concerned. If there’s little

contact between client and front office, an automated system

will need to be in place.

› Training: ESMA emphasizes the importance to train all

relevant staff in the detection of market abuse. There should

always be an element of human analysis in detecting market

abuse.

› Reporting obligation: In case of reasonable suspicion of

insider dealing, the person shall notify the competent authority.

› Record keeping: Suspicious Transactions and Other Reports

(STORs) need to be kept for a period of 5 years.

Market Abuse - an introduction (c) double effect 2016

4. Prevention and detection of market abuse

25

General Information

› Name of individual

› Name of firm/trading venue

› Position within entity

› Address of reporting entity

› Acting capacity of entity with

respect to suspicious activity

› Type of activity of trading desk

involved (if available)

› Relationship with subject of

suspicion

› Contact/Compliance officer

Market Abuse - an introduction (c) double effect 2016

Reporting and Record Keeping

Suspicious Transactions and Other Reports (STORs) need to be kept for a period of 5 years.

Description of suspected

breach

› Describe activity, how it came to

reporters attention and reasons for

suspicion.

› For OTC derivatives, details

concerning transactions/orders in

the underlying asset and information

on possible link between dealings in

the cash market of the underlying

and dealings in the OTC derivative.

› For instruments admitted to trading

on/traded on a trading venue,

describe suspicious order book

interactions/transactions.

Transaction information

› Date and time of suspicious activity

(specify time zone)

› Market (trading venue where the

activity occurred)

› Location (country, if available)

If outside a trading venue:

› Specify transaction reference

number/order reference number

› Settlement date

› Name and type of security (ISIN)

MADII

MAD

26

MAD I failed to harmonize supervisory powers and sanctions

› MAD I implementation differed per regulatory regime.

› Competent authorities were left with a tool kit that was not equipped to deal

with changes in the market landscape after MiFID.

› Due to lack of harmonized powers and possibility to sanction disruptive

behaviour, the intended goals of MAD could not be achieved.

› MAR introduces increased investigatory powers for competent authorities like

the possibility to seize documents and access to recorded telephone

conversations.

› MAR requires member states to introduce administrative sanctions.

› CSMAD requires member states to implement criminal sanctions for serious

cases of market abuse.

MAD II mandates an increase in investigatory powers and sanctions

I

Market Abuse - an introduction (c) double effect 2016

Increase in investigatory powers and sanctions

5. Supervisory powers and sanctions: MAD I compared to MAD II

27

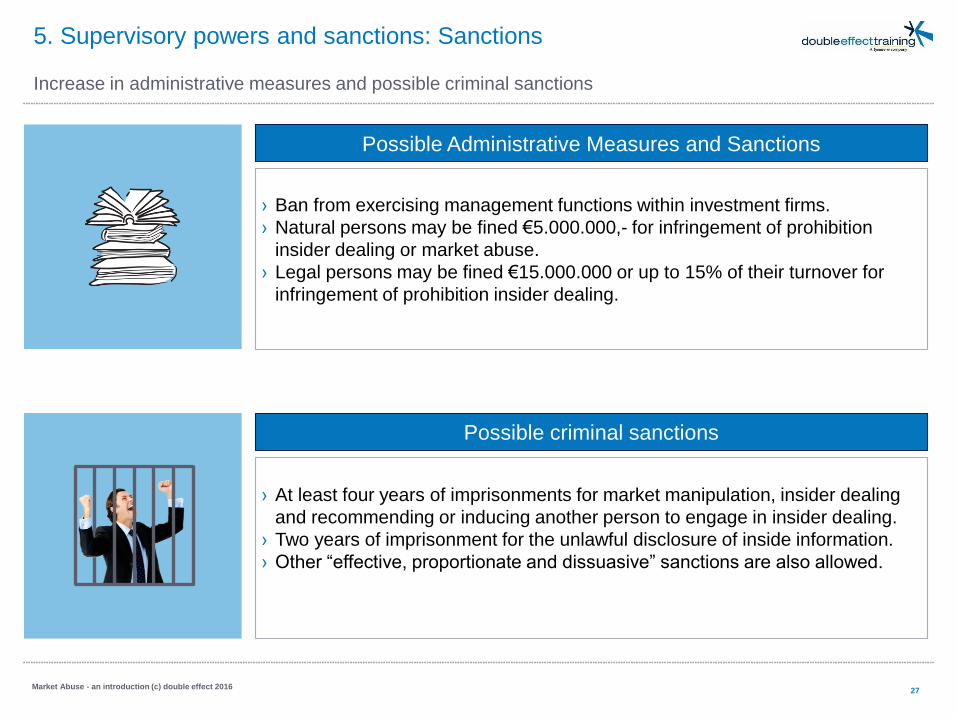

Possible Administrative Measures and Sanctions

› Ban from exercising management functions within investment firms.

› Natural persons may be fined €5.000.000,- for infringement of prohibition

insider dealing or market abuse.

› Legal persons may be fined €15.000.000 or up to 15% of their turnover for

infringement of prohibition insider dealing.

› At least four years of imprisonments for market manipulation, insider dealing

and recommending or inducing another person to engage in insider dealing.

› Two years of imprisonment for the unlawful disclosure of inside information.

› Other “effective, proportionate and dissuasive” sanctions are also allowed.

Possible criminal sanctions

Market Abuse - an introduction (c) double effect 2016

Increase in administrative measures and possible criminal sanctions

5. Supervisory powers and sanctions: Sanctions

5. Supervisory powers and sanctions: STORs

The AFM (NL) procedure for STORs is described below

28

Start STOR Close

STOR is enriched with

information available

to AFM. Request for

information send out

Discuss possible

handover for criminal

measures with public

prosecutor

Based on first

assessment decision

is made on follow up

of STOR

Further investigation

and write up of finding

plus proposed

measures

Administrative

measures prepared by

AFM staff and vetted

by AFM legal

Sanctioning by AFM

and possible appeals

of administrative

measures

Market Abuse - an introduction (c) double effect 2016

Want to learn more?

Follow our training course!

29Market Abuse - an introduction (c) double effect 2016

› During our MAD II training course all the elements of

MAD II will be discussed in much more detail and a

much closer look will be taken on the impact on

firms. The training course is very suitable for anyone

involved in MAD II in his work. This varies from sales

employees to operations and compliance staff. And

also project managers and business analysts

responsible for the implementation of MAD II.

› For more information and registration visit our

website:

http://www.doubleeffecttraining.com/

Want to know more?

Please contact our MAD II experts

30Market Abuse - an introduction (c) double effect 2016

The Netherlands

Crown Building South

Hullenbergweg 361

1101 CP Amsterdam

Singapore

20 Collyer Quay #23-01Singapore 049319

United Kingdom

99 Bishopsgate, Level 15EC2M 3XD, London

USA

212 South Tryon Street, Suite 980

Charlotte, NC 28281

Joris Hillebrand

› Practice Lead

› +31 6 116 495 65

Kimberley van Til

› Lead Consultant

› +31 6 531 459 04

Willem den Blanken

› Consultant

› +31 6 151 664 36

Rick Bonhof

› Consultant

› +31 6 461 844 07

Disclaimer

This document has been prepared by Double Effect and is solely intended to provide general information about the Market

Abuse Directive II (MAD II). The information in the document is strictly proprietary, unless otherwise stated and is being supplied

to you solely for your information. The document is informative in nature and does not constitute legal, regulatory or other

advice nor does it express any recommendations and may not be used for such purposes. Everyone using this document

should acquaint themselves with and adhere to the applicable legislation. No reliance may be placed for any purposes

whatsoever on the information, opinions, forecasts and assumptions contained in the document or on its completeness,

accuracy or fairness. No representation or warranty, express or implied, is given by or on behalf of Double Effect, or any of its

directors, officers, affiliates or employees as to the accuracy or completeness of the information contained in this document. No

liability is accepted for any loss, arising, directly or indirectly, from any use of such information.

31Market Abuse - an introduction (c) double effect 2016