Margin Expansion: Volume to Value -...

19

Kellogg Company September 7, 2016 Page 1 of 19 Margin Expansion: Volume to Value Barclay’s Global Consumer Staples Conference September 7, 2016 Margin Expansion: Volume to Value 2 This presentation contains, or incorporates by reference, “forward‐looking statements” with projections concerning, among other things, the Company’s global growth and efficiency program (Project K), the integration of acquired businesses, the Company’s strategy, zero‐based budgeting, and the Company’s sales, earnings, margin, operating profit, costs and expenditures, interest expense, tax rate, capital expenditure, dividends, cash flow, debt reduction, share repurchases, costs, charges, rates of return, brand building, ROIC, working capital, growth, new products, innovation, cost reduction projects, workforce reductions, savings, and competitive pressures. Forward‐looking statements include predictions of future results or activities and may contain the words “expects,” “believes,” “should,” “will,” “anticipates,” “projects,” “estimates,” “implies,” “can,” or words or phrases of similar meaning. The Company’s actual results or activities may differ materially from these predictions. The Company’s future results could also be affected by a variety of factors, including the ability to implement Project K as planned, whether the expected amount of costs associated with Project K will differ from forecasts, whether the Company will be able to realize the anticipated benefits from Project K in the amounts and times expected, the ability to realize the anticipated benefits and synergies from the acquisitions in the amounts and at the times expected, the impact of competitive conditions; the effectiveness of pricing, advertising, and promotional programs; the success of innovation, renovation and new product introductions; the recoverability of the carrying value of goodwill and other intangibles; the success of productivity improvements and business transitions; commodity and energy prices; labor costs; disruptions or inefficiencies in supply chain; the availability of and interest rates on short‐term and long‐term financing; actual market performance of benefit plan trust investments; the levels of spending on systems initiatives, properties, business opportunities, integration of acquired businesses, and other general and administrative costs; changes in consumer behavior and preferences; the effect of U.S. and foreign economic conditions on items such as interest rates, statutory tax rates, currency conversion and availability; legal and regulatory factors including changes in food safety, advertising and labeling laws and regulations; the ultimate impact of product recalls; business disruption or other losses from war, terrorist acts or political unrest; and other items. Forward‐looking statements speak only as of the date they were made, and the Company undertakes no obligation to update them publicly. Non‐GAAP Financial Measures. This presentation includes non‐GAAP financial measures. Please refer to the Appendices for a reconciliation of these non‐GAAP financial measures to the most directly comparable GAAP financial measures. Management believes that the use of such non‐GAAP measures assists investors in understanding the underlying operating performance of the company and its segments. Forward‐Looking Statement

Transcript of Margin Expansion: Volume to Value -...

Kellogg Company September 7, 2016

Page 1 of 19

Margin Expansion:

Volume to ValueBarclay’s Global Consumer

Staples Conference

September 7, 2016

Margin Expansion: Volume to Value 2

This presentation contains, or incorporates by reference, “forward‐looking statements” with projections concerning, among other things, the Company’s global growth and efficiency program (Project K), the integration of acquired businesses, the Company’s strategy, zero‐based budgeting, and the Company’s sales, earnings, margin, operating profit, costs and expenditures, interest expense, tax rate, capital expenditure, dividends, cash flow, debt reduction, share repurchases, costs, charges, rates of return, brand building, ROIC, working capital, growth, new products, innovation, cost reduction projects, workforce reductions, savings, and competitive pressures. Forward‐looking statements include predictions of future results or activities and may contain the words “expects,” “believes,” “should,” “will,” “anticipates,” “projects,” “estimates,” “implies,” “can,” or words or phrases of similar meaning.

The Company’s actual results or activities may differ materially from these predictions. The Company’s future results could also be affected by a variety of factors, including the ability to implement Project K as planned, whether the expected amount of costs associated with Project K will differ from forecasts, whether the Company will be able to realize the anticipated benefits from Project K in the amounts and times expected, the ability to realize the anticipated benefits and synergies from the acquisitions in the amounts and at the times expected, the impact of competitive conditions; the effectiveness of pricing, advertising, and promotional programs; the success of innovation, renovation and new product introductions; the recoverability of the carrying value of goodwill and other intangibles; the success of productivity improvements and business transitions; commodity and energy prices; labor costs; disruptions or inefficiencies in supply chain; the availability of and interest rates on short‐term and long‐term financing; actual market performance of benefit plan trust investments; the levels of spending on systems initiatives, properties, business opportunities, integration of acquired businesses, and other general and administrative costs; changes in consumer behavior and preferences; the effect of U.S. and foreign economic conditions on items such as interest rates, statutory tax rates, currency conversion and availability; legal and regulatory factors including changes in food safety, advertising and labeling laws and regulations; the ultimate impact of product recalls; business disruption or other losses from war, terrorist acts or political unrest; and other items.

Forward‐looking statements speak only as of the date they were made, and the Company undertakes no obligation to update them publicly.

Non‐GAAP Financial Measures. This presentation includes non‐GAAP financial measures. Please refer to the Appendices for a reconciliation of these non‐GAAP financial measures to the most directly comparable GAAP financial measures. Management believes that the use of such non‐GAAP measures assists investors in understanding the underlying operating performance of the company and its segments.

Forward‐Looking Statement

Kellogg Company September 7, 2016

Page 2 of 19

Margin Expansion: Volume to Value

• Strategy & Operating Model John Bryant Chairman & CEO

• Investing for Impact Clive Sirkin Chief Growth Officer

• Improving our Margins Ron Dissinger Chief Financial Officer

• Closing Remarks John Bryant Chairman & CEO

Agenda

3

Margin Expansion: Volume to Value

EvolvingBusinessModel

Increasing Emphasis on

Profit Margins

4

Changing Environment for Packaged Food

ChangingFood Beliefs

New Ways toCommunicate

FoodStart‐Ups

ChangingRetailer Environment

Regulatory & LabellingChanges

New Financial Model

Kellogg Company September 7, 2016

Page 3 of 19

Margin Expansion: Volume to Value

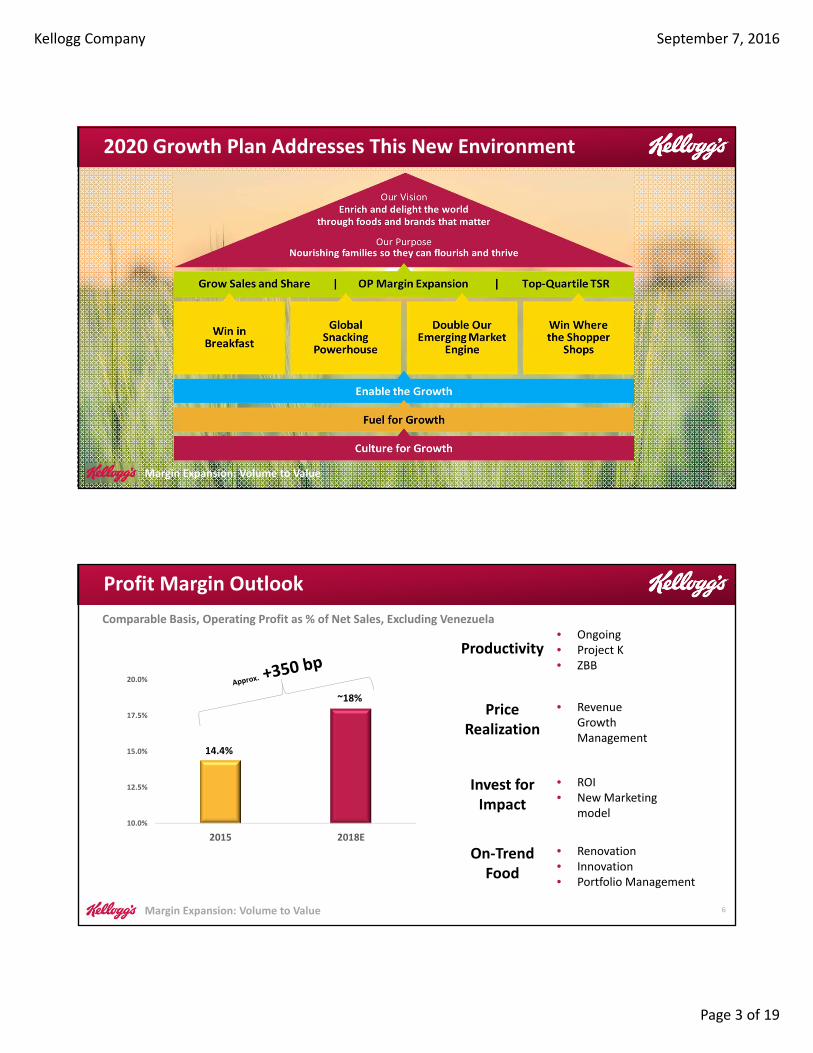

2020 Growth Plan Addresses This New Environment

5Margin Expansion: Volume to Value

Margin Expansion: Volume to Value 6

• Ongoing• Project K• ZBB

Invest forImpact

PriceRealization

Productivity

10.0%

12.5%

15.0%

17.5%

20.0%

2015 2018E

Comparable Basis, Operating Profit as % of Net Sales, Excluding Venezuela

14.4%

• ROI• New Marketing

model

~18%• Revenue

Growth Management

On‐TrendFood

• Renovation• Innovation• Portfolio Management

Profit Margin Outlook

Kellogg Company September 7, 2016

Page 4 of 19

Margin Expansion: Volume to Value

Volumeto

Value

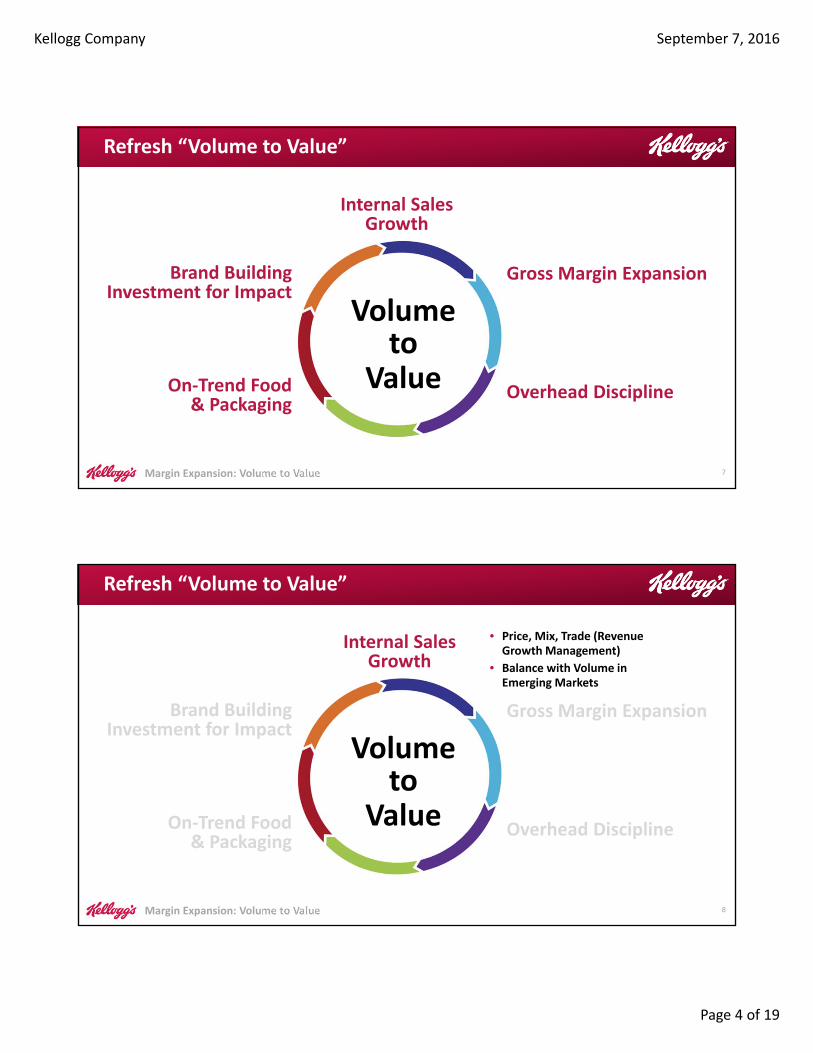

Internal Sales Growth

Overhead Discipline

Gross Margin Expansion

On‐Trend Food & Packaging

Brand Building Investment for Impact

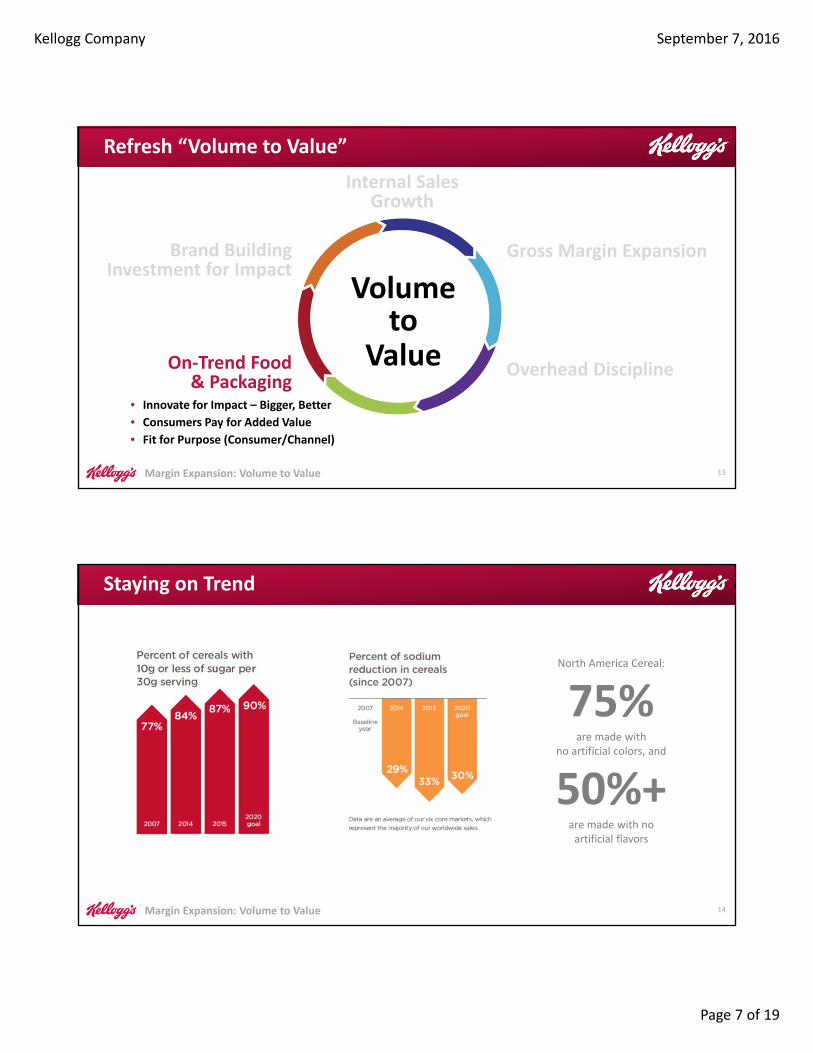

Refresh “Volume to Value”

7

Margin Expansion: Volume to Value

Volumeto

Value

Internal Sales Growth

Overhead Discipline

Gross Margin Expansion

On‐Trend Food & Packaging

Brand Building Investment for Impact

• Price, Mix, Trade (Revenue Growth Management)

• Balance with Volume in Emerging Markets

Refresh “Volume to Value”

8

Kellogg Company September 7, 2016

Page 5 of 19

Margin Expansion: Volume to Value

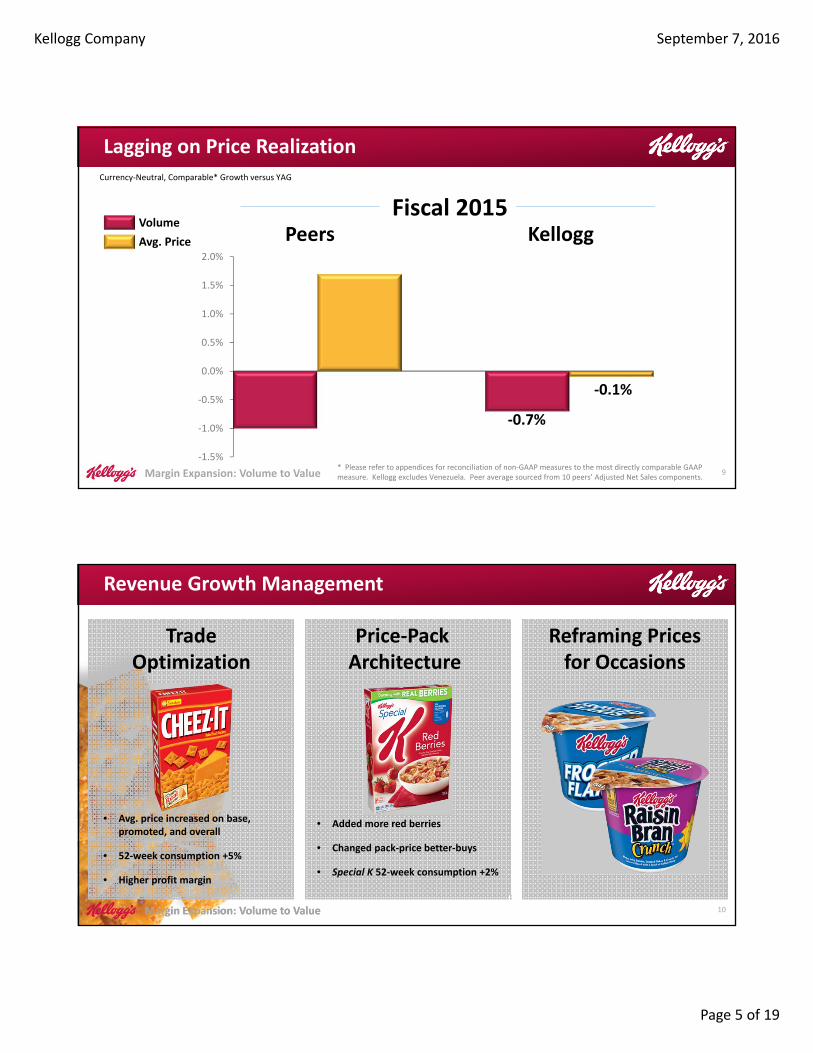

‐0.7%

‐0.1%

‐1.5%

‐1.0%

‐0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

Volume

Avg. Price

Lagging on Price RealizationCurrency‐Neutral, Comparable* Growth versus YAG

Peers Kellogg

9* Please refer to appendices for reconciliation of non‐GAAP measures to the most directly comparable GAAP measure. Kellogg excludes Venezuela. Peer average sourced from 10 peers’ Adjusted Net Sales components.

Fiscal 2015

Margin Expansion: Volume to Value

Trade Optimization

• Added more red berries

• Changed pack‐price better‐buys

• Special K 52‐week consumption +2%

Revenue Growth Management

Price‐Pack Architecture

Reframing Prices for Occasions

• Avg. price increased on base, promoted, and overall

• 52‐week consumption +5%

• Higher profit margin

10Margin Expansion: Volume to Value

Kellogg Company September 7, 2016

Page 6 of 19

Margin Expansion: Volume to Value

Emerging Markets – Growing Amidst Challenging Conditions

11Margin Expansion: Volume to Value

Margin Expansion: Volume to Value

• Strategy & Operating Model John Bryant Chairman & CEO

• Investing for Impact Clive Sirkin Chief Growth Officer

• Improving our Margins Ron Dissinger Chief Financial Officer

• Closing Remarks John Bryant Chairman & CEO

Agenda

12

Kellogg Company September 7, 2016

Page 7 of 19

Margin Expansion: Volume to Value

Volumeto

Value

Internal Sales Growth

Overhead Discipline

Gross Margin Expansion

On‐Trend Food & Packaging

Brand Building Investment for Impact

• Innovate for Impact – Bigger, Better

• Consumers Pay for Added Value

• Fit for Purpose (Consumer/Channel)

Refresh “Volume to Value”

13

Margin Expansion: Volume to Value

Staying on Trend

North America Cereal:

75%are made with

no artificial colors, and

50%+are made with no artificial flavors

14

Kellogg Company September 7, 2016

Page 8 of 19

Margin Expansion: Volume to Value

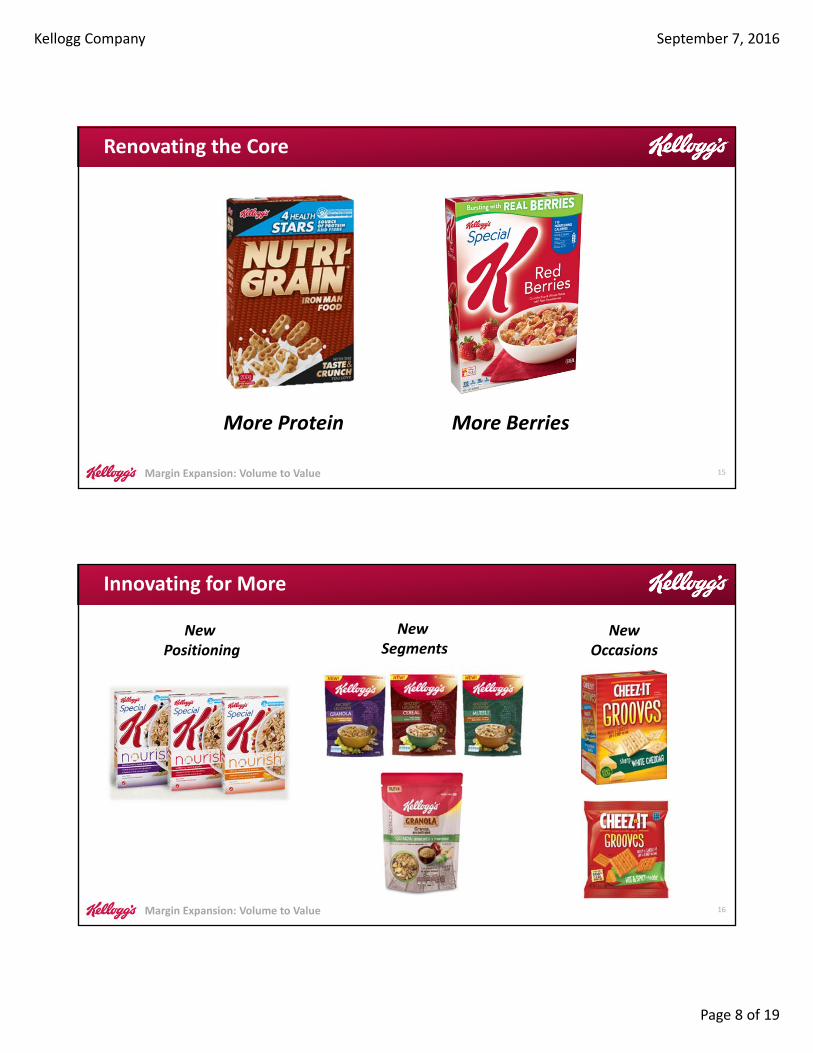

Renovating the Core

More BerriesMore Protein

15

Margin Expansion: Volume to Value

Innovating for More

New Positioning

New Segments

NewOccasions

16

Kellogg Company September 7, 2016

Page 9 of 19

Margin Expansion: Volume to Value

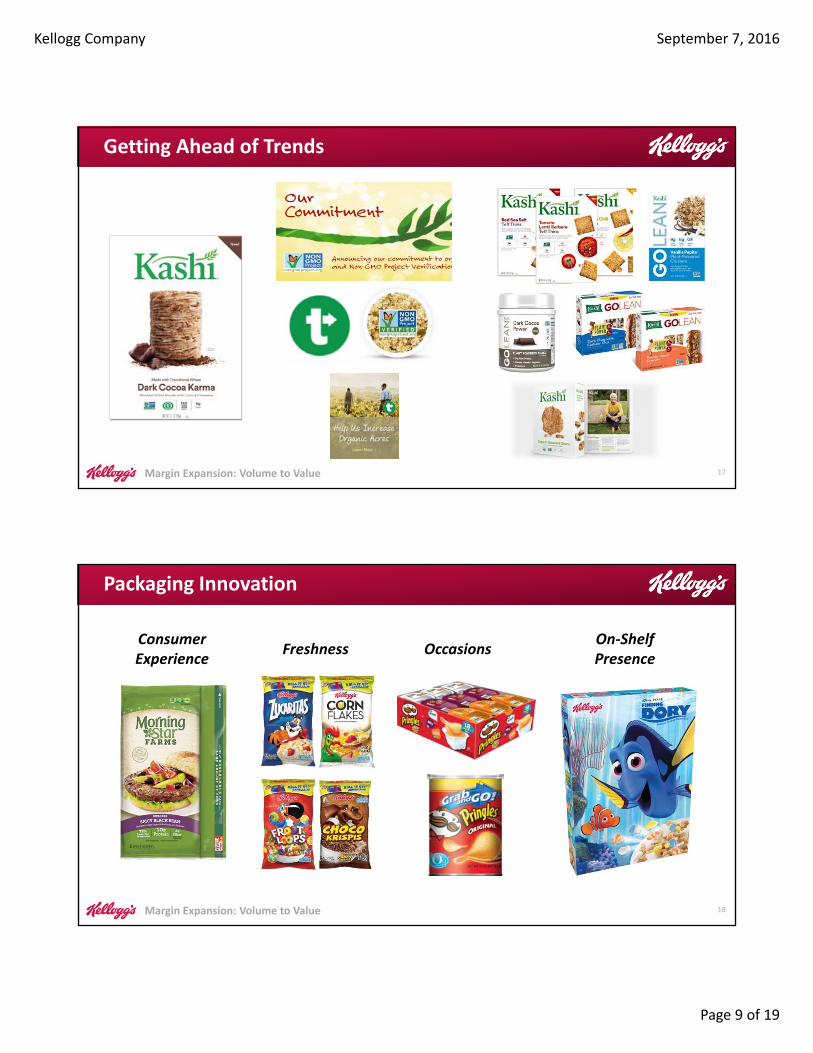

Getting Ahead of Trends

17

Margin Expansion: Volume to Value

Packaging Innovation

We have made Significant Global Progress on Sugar Reductions against our 2020 Food Belief Goals

18

ConsumerExperience

Freshness OccasionsOn‐ShelfPresence

Kellogg Company September 7, 2016

Page 10 of 19

Margin Expansion: Volume to Value

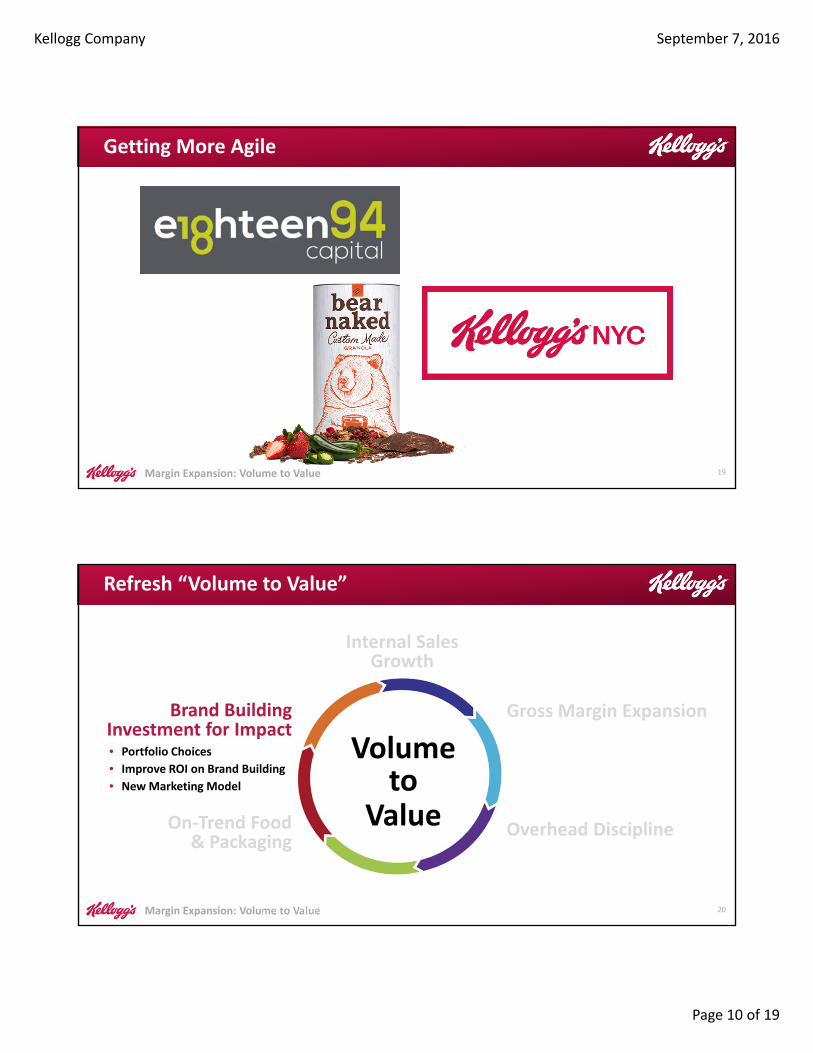

Getting More Agile

19

Margin Expansion: Volume to Value

Volumeto

Value

Internal Sales Growth

Overhead Discipline

Gross Margin Expansion

On‐Trend Food & Packaging

Brand Building Investment for Impact• Portfolio Choices

• Improve ROI on Brand Building

• New Marketing Model

Refresh “Volume to Value”

20

Kellogg Company September 7, 2016

Page 11 of 19

Margin Expansion: Volume to Value

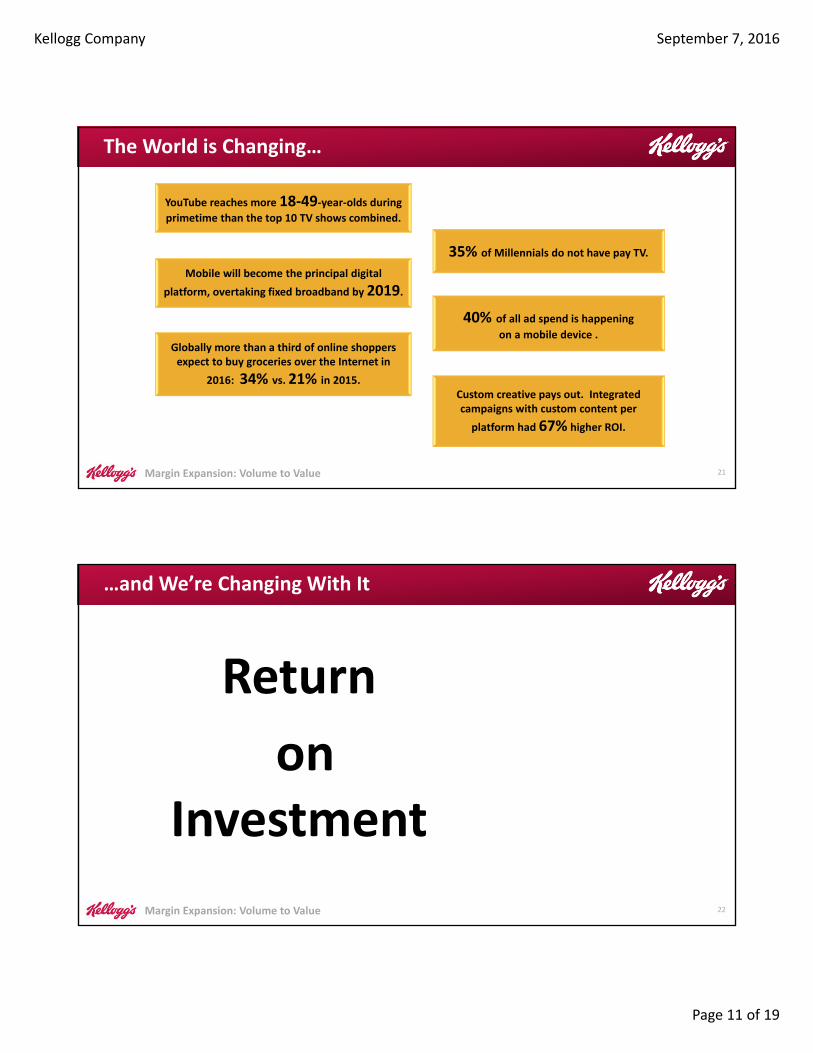

The World is Changing…

YouTube reaches more 18‐49‐year‐olds during primetime than the top 10 TV shows combined.

35% of Millennials do not have pay TV.

Custom creative pays out. Integrated campaigns with custom content per

platform had 67% higher ROI.

Globally more than a third of online shoppers expect to buy groceries over the Internet in

2016: 34% vs. 21% in 2015.

40% of all ad spend is happening

on a mobile device .

Mobile will become the principal digital

platform, overtaking fixed broadband by 2019.

21

Margin Expansion: Volume to Value

Return

onInvestment

…and We’re Changing With It

22

Kellogg Company September 7, 2016

Page 12 of 19

Margin Expansion: Volume to Value

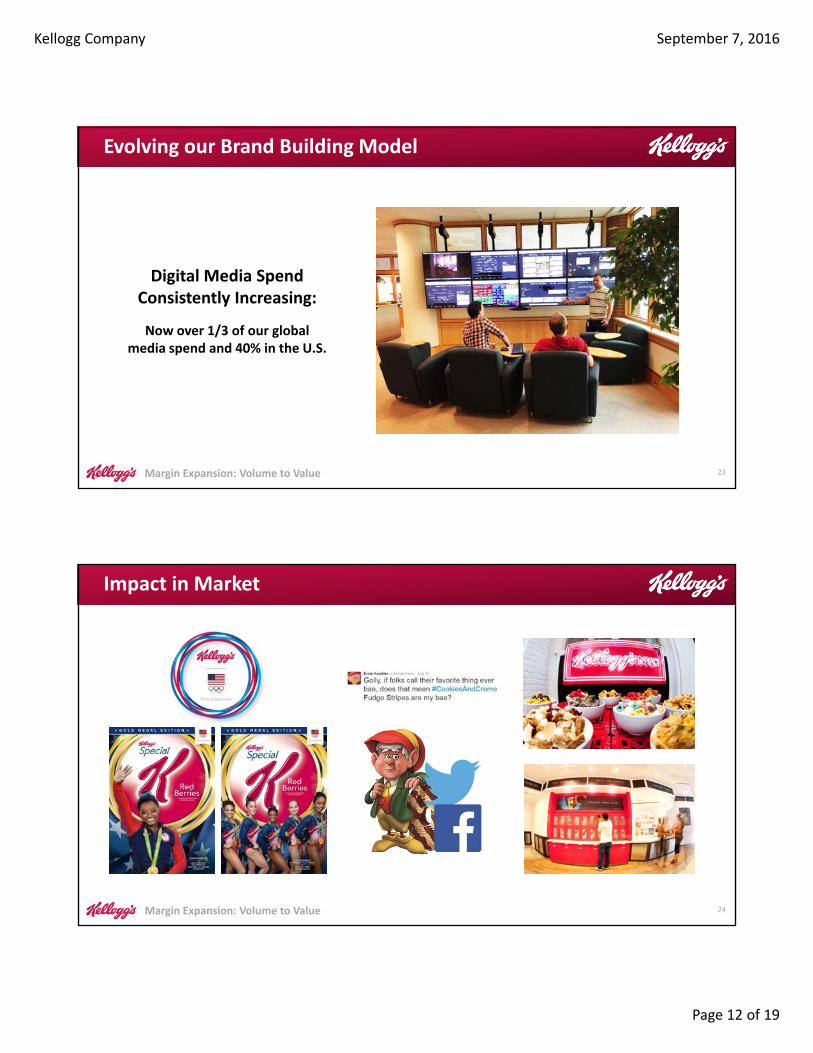

Evolving our Brand Building Model

Digital Media Spend Consistently Increasing:

Now over 1/3 of our global media spend and 40% in the U.S.

23

Margin Expansion: Volume to Value

Impact in Market

24

Kellogg Company September 7, 2016

Page 13 of 19

Margin Expansion: Volume to Value

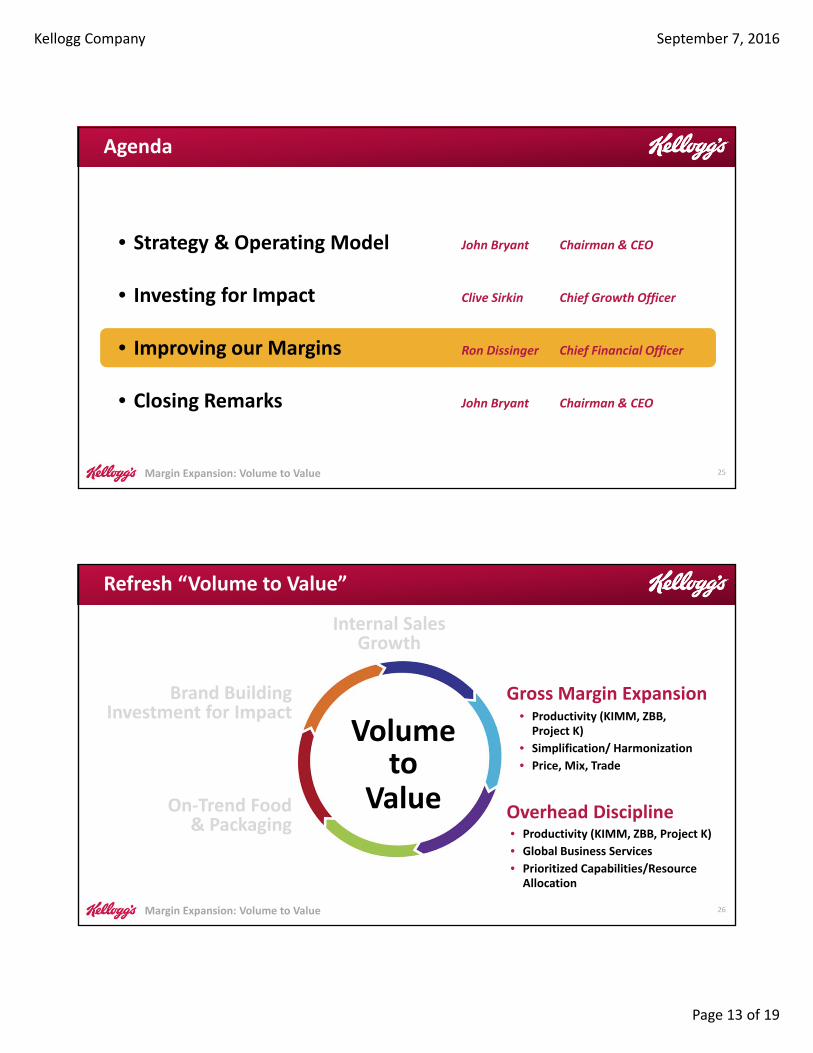

• Strategy & Operating Model John Bryant Chairman & CEO

• Investing for Impact Clive Sirkin Chief Growth Officer

• Improving our Margins Ron Dissinger Chief Financial Officer

• Closing Remarks John Bryant Chairman & CEO

Agenda

25

Margin Expansion: Volume to Value

Refresh “Volume to Value”

Volumeto

Value

Internal Sales Growth

Gross Margin Expansion

On‐Trend Food & Packaging

Brand Building Investment for Impact • Productivity (KIMM, ZBB,

Project K)

• Simplification/ Harmonization

• Price, Mix, Trade

Overhead Discipline• Productivity (KIMM, ZBB, Project K)

• Global Business Services

• Prioritized Capabilities/Resource Allocation

26

Kellogg Company September 7, 2016

Page 14 of 19

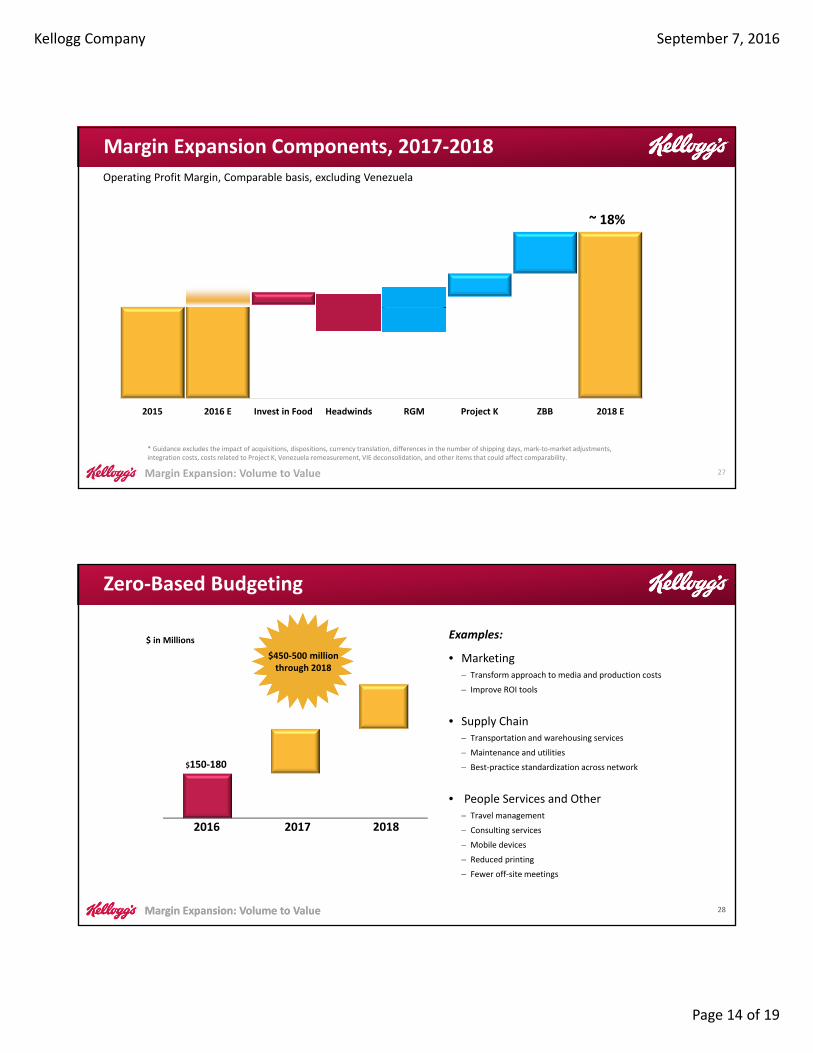

Margin Expansion: Volume to Value

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

2015 2016 E Invest in Food Headwinds RGM Project K ZBB 2018 E

Operating Profit Margin, Comparable basis, excluding Venezuela

Margin Expansion Components, 2017‐2018

27

~ 18%

* Guidance excludes the impact of acquisitions, dispositions, currency translation, differences in the number of shipping days, mark‐to‐market adjustments, integration costs, costs related to Project K, Venezuela remeasurement, VIE deconsolidation, and other items that could affect comparability.

Margin Expansion: Volume to Value

Examples:

• Marketing Transform approach to media and production costs

Improve ROI tools

• Supply Chain Transportation and warehousing services

Maintenance and utilities

Best‐practice standardization across network

• People Services and Other Travel management

Consulting services

Mobile devices

Reduced printing

Fewer off‐site meetings

2016 20182017

$150‐180

$ in Millions

Zero‐Based Budgeting

28Margin Expansion: Volume to Value

$450‐500 million through 2018

Kellogg Company September 7, 2016

Page 15 of 19

Margin Expansion: Volume to Value 29

(a) 2016 guidance excludes the impact of acquisitions, dispositions, currency translation, differences in the number of shipping days, mark‐to‐market adjustments, integration costs, costs related to Project K, Venezuela remeasurement, VIE deconsolidation, and other items that could affect comparability.

(b) 2016 guidance excludes the impact of currency translation, differences in the number of shipping days, mark‐to‐market adjustments, integration costs, costs related to Project K, Venezuela remeasurement, and other items that could affect comparability. Does include the impact of prior acquisitions and investment in JVs.

EPS(b)Currency‐Neutral Comparable

Operating Profit(a)Currency‐Neutral Comparable

Net Sales(a)Currency‐Neutral Comparable

+4‐6%

+15‐17%

$4.11 ‐ $4.18

+0‐2%

+4‐6%

• Still expecting return to slight growthin 2H

• Now expected to be low end of range

• Expanded ZBB savings in North America, and early ZBB savings in International

• Now expected to be high end of the range

Previous: 0‐2%Previous: 4‐6%

Previous: 4‐6%

• Venezuela performance and ZBB savings• Comparable EPS comes down to $3.58‐

$3.65 (from previous $3.64‐3.71 guidance) for European currency translation

Previous: $4.00‐$4.07

Previous: 11‐13%

* Please refer to appendices for reconciliation of non‐GAAP measures to the most directly comparable GAAP measure.

Note: Excluding Venezuela

Currency‐NeutralComparable *

2016 Guidance

Guidance from Q2 Earnings Call, Aug. 4, 2016

Margin Expansion: Volume to Value 30

($ in millions, currency‐neutral comparable performance,* excluding Venezuela, year‐over‐year change)

Net Sales Low end, 0‐2%

Operating Profit

~ flat

HSD CAGR2017‐2018

2016

High end, +4‐6%

Preliminary Outlook, 2017‐2018

2017‐2018

OP Margin:~18%,+350 bpfrom 2015

* Guidance excludes the impact of acquisitions, dispositions, currency translation, differences in the number of shipping days, mark‐to‐market adjustments, integration costs, costs related to Project K, Venezuela remeasurement, VIE deconsolidation, and other items that could affect comparability.

Kellogg Company September 7, 2016

Page 16 of 19

Margin Expansion: Volume to Value

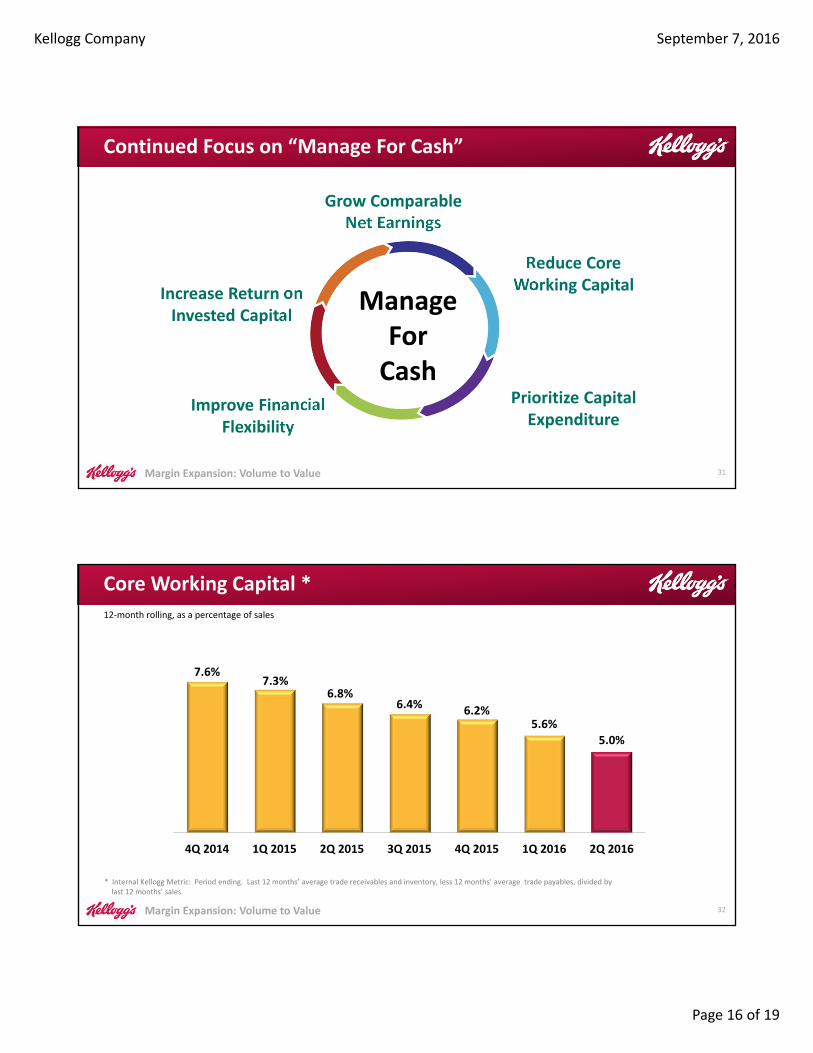

Grow Comparable Net Earnings

Reduce Core Working Capital

Improve Financial Flexibility

Increase Return on Invested Capital

Prioritize Capital Expenditure

ManageForCash

Continued Focus on “Manage For Cash”

31

Margin Expansion: Volume to Value 32

12‐month rolling, as a percentage of sales

* Internal Kellogg Metric: Period ending. Last 12 months’ average trade receivables and inventory, less 12 months’ average trade payables, divided bylast 12 months’ sales.

7.6%7.3%

6.8%6.4% 6.2%

5.6%

5.0%

4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015 1Q 2016 2Q 2016

Core Working Capital *

Kellogg Company September 7, 2016

Page 17 of 19

Margin Expansion: Volume to Value

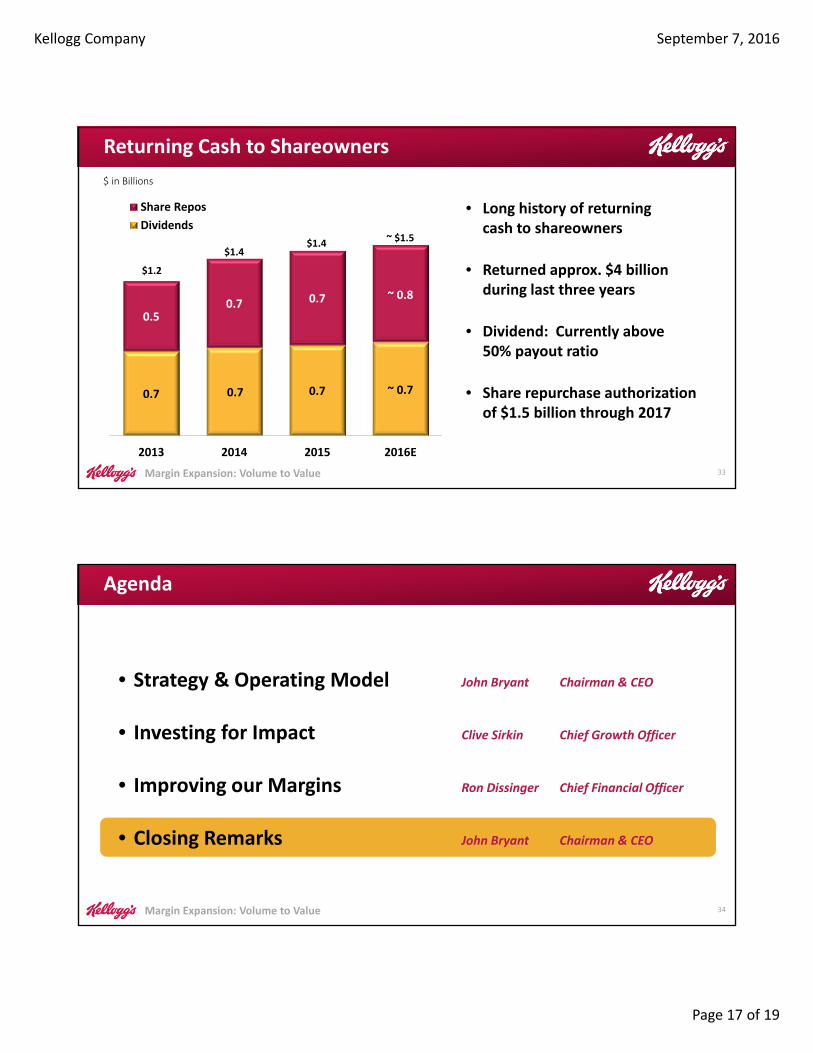

• Long history of returning cash to shareowners

• Returned approx. $4 billion during last three years

• Dividend: Currently above 50% payout ratio

• Share repurchase authorization of $1.5 billion through 2017

0.7 0.7 0.7

0.50.7 0.7

2013 2014 2015 2016E

Share Repos

Dividends

$1.2

$1.4

$ in Billions

$1.4

~ 0.8

~ 0.7

~ $1.5

Returning Cash to Shareowners

33

Margin Expansion: Volume to Value

• Strategy & Operating Model John Bryant Chairman & CEO

• Investing for Impact Clive Sirkin Chief Growth Officer

• Improving our Margins Ron Dissinger Chief Financial Officer

• Closing Remarks John Bryant Chairman & CEO

Agenda

34

Kellogg Company September 7, 2016

Page 18 of 19

Margin Expansion: Volume to Value

• Clear Strategy – 2020 Growth Plan

• Volume to Value –Margin Expansion

• Earnings Visibility – Project K, ZBB,

In Summary…

35

Revenue Growth Management

September 7, 2016

Kellogg CompanyBarclay’s

Global Consumer Staples Conference

Q&A

Kellogg Company September 7, 2016

Page 19 of 19

Margin Expansion: Volume to Value

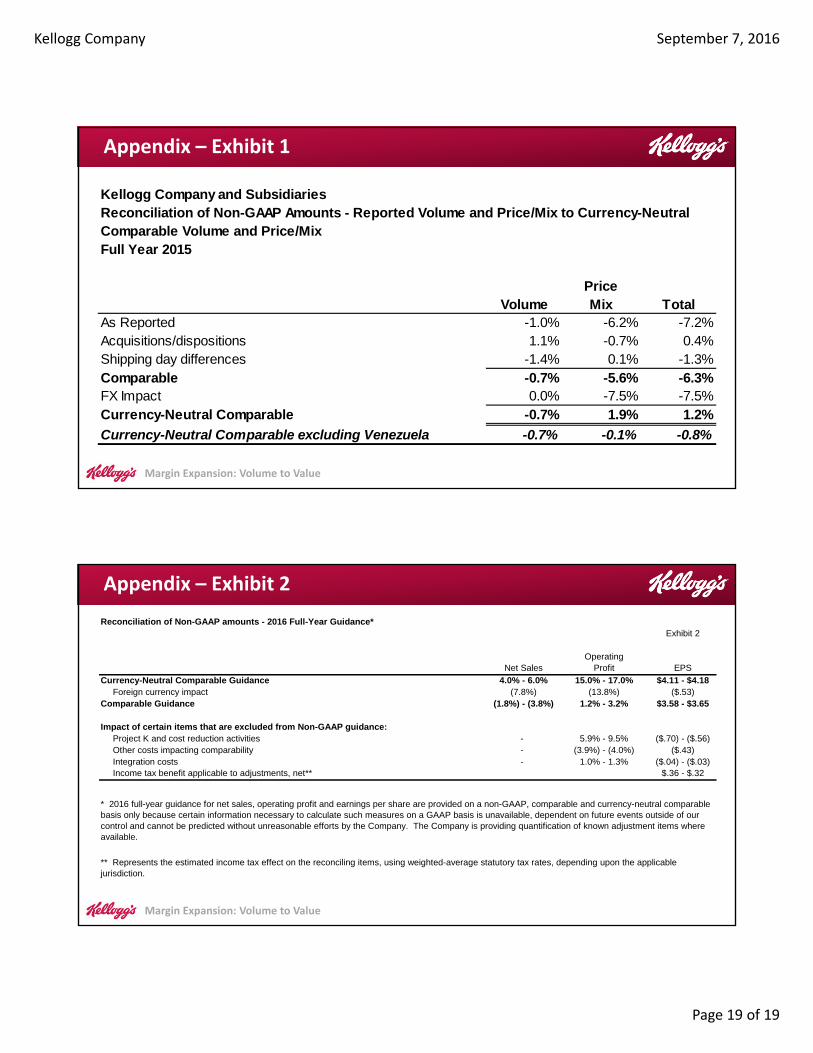

Appendix – Exhibit 1

Kellogg Company and SubsidiariesReconciliation of Non-GAAP Amounts - Reported Volume and Price/Mix to Currency-NeutralComparable Volume and Price/MixFull Year 2015

PriceVolume Mix Total

As Reported -1.0% -6.2% -7.2%Acquisitions/dispositions 1.1% -0.7% 0.4%Shipping day differences -1.4% 0.1% -1.3%Comparable -0.7% -5.6% -6.3%FX Impact 0.0% -7.5% -7.5%Currency-Neutral Comparable -0.7% 1.9% 1.2%

Currency-Neutral Comparable excluding Venezuela -0.7% -0.1% -0.8%

Margin Expansion: Volume to Value

Appendix – Exhibit 2

Reconciliation of Non-GAAP amounts - 2016 Full-Year Guidance*Exhibit 2

OperatingNet Sales Profit EPS

Currency-Neutral Comparable Guidance 4.0% - 6.0% 15.0% - 17.0% $4.11 - $4.18Foreign currency impact (7.8%) (13.8%) ($.53)

Comparable Guidance (1.8%) - (3.8%) 1.2% - 3.2% $3.58 - $3.65

Impact of certain items that are excluded from Non-GAAP guidance:Project K and cost reduction activities - 5.9% - 9.5% ($.70) - ($.56)Other costs impacting comparability - (3.9%) - (4.0%) ($.43)Integration costs - 1.0% - 1.3% ($.04) - ($.03)Income tax benefit applicable to adjustments, net** $.36 - $.32

* 2016 full-year guidance for net sales, operating profit and earnings per share are provided on a non-GAAP, comparable and currency-neutral comparable basis only because certain information necessary to calculate such measures on a GAAP basis is unavailable, dependent on future events outside of our control and cannot be predicted without unreasonable efforts by the Company. The Company is providing quantification of known adjustment items where available.

** Represents the estimated income tax effect on the reconciling items, using weighted-average statutory tax rates, depending upon the applicable jurisdiction.

![New Himax Investor Presentation 2013 May Website [相容模式] · 2018. 8. 28. · z2011 4Q marks the inflection point for gross margin expansion zGross margin improvement zSuccessful](https://static.fdocuments.net/doc/165x107/6056fa842764ab7b8a17ad5f/new-himax-investor-presentation-2013-may-website-c-2018-8-28-z2011.jpg)