Marcon International, Inc. P.O. Box 1170, 9 NW Front ... · Sales include 91 ocean tank barges...

26

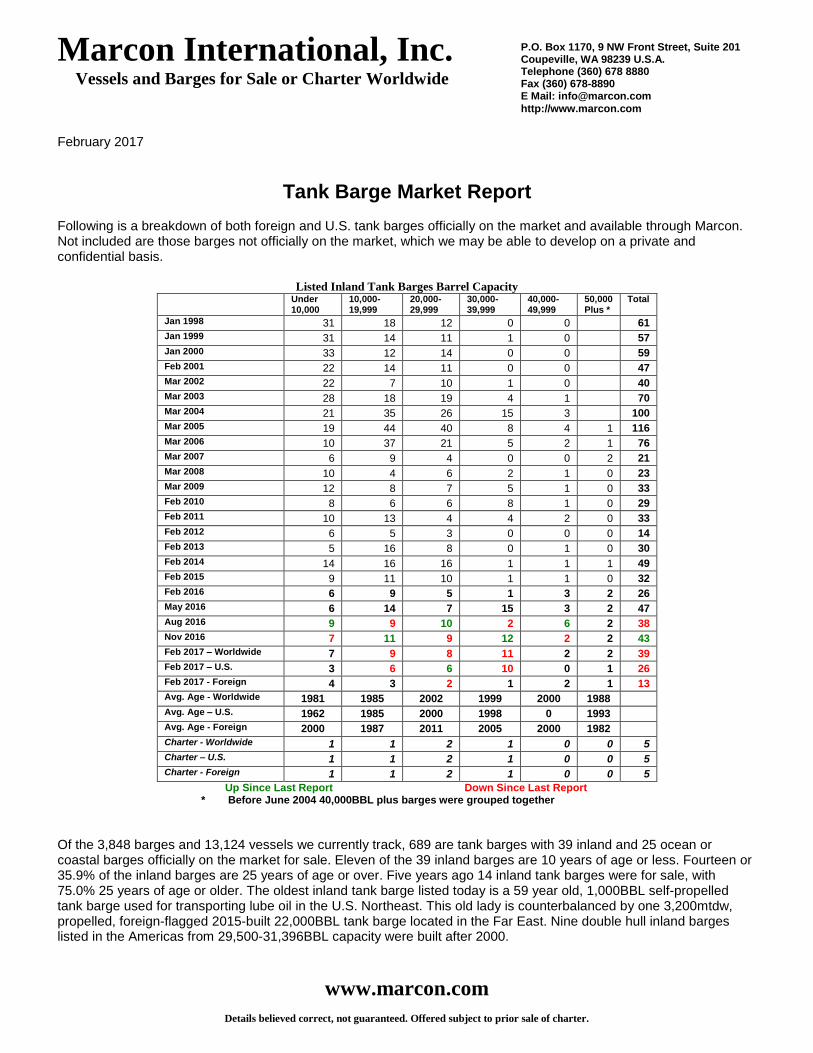

Marcon International, Inc. Vessels and Barges for Sale or Charter Worldwide www.marcon.com Details believed correct, not guaranteed. Offered subject to prior sale of charter. P.O. Box 1170, 9 NW Front Street, Suite 201 Coupeville, WA 98239 U.S.A. Telephone (360) 678 8880 Fax (360) 678-8890 E Mail: [email protected] http://www.marcon.com February 2017 Tank Barge Market Report Following is a breakdown of both foreign and U.S. tank barges officially on the market and available through Marcon. Not included are those barges not officially on the market, which we may be able to develop on a private and confidential basis. Listed Inland Tank Barges Barrel Capacity Under 10,000 10,000- 19,999 20,000- 29,999 30,000- 39,999 40,000- 49,999 50,000 Plus * Total Jan 1998 31 18 12 0 0 61 Jan 1999 31 14 11 1 0 57 Jan 2000 33 12 14 0 0 59 Feb 2001 22 14 11 0 0 47 Mar 2002 22 7 10 1 0 40 Mar 2003 28 18 19 4 1 70 Mar 2004 21 35 26 15 3 100 Mar 2005 19 44 40 8 4 1 116 Mar 2006 10 37 21 5 2 1 76 Mar 2007 6 9 4 0 0 2 21 Mar 2008 10 4 6 2 1 0 23 Mar 2009 12 8 7 5 1 0 33 Feb 2010 8 6 6 8 1 0 29 Feb 2011 10 13 4 4 2 0 33 Feb 2012 6 5 3 0 0 0 14 Feb 2013 5 16 8 0 1 0 30 Feb 2014 14 16 16 1 1 1 49 Feb 2015 9 11 10 1 1 0 32 Feb 2016 6 9 5 1 3 2 26 May 2016 6 14 7 15 3 2 47 Aug 2016 9 9 10 2 6 2 38 Nov 2016 7 11 9 12 2 2 43 Feb 2017 – Worldwide 7 9 8 11 2 2 39 Feb 2017 – U.S. 3 6 6 10 0 1 26 Feb 2017 - Foreign 4 3 2 1 2 1 13 Avg. Age - Worldwide 1981 1985 2002 1999 2000 1988 Avg. Age – U.S. 1962 1985 2000 1998 0 1993 Avg. Age - Foreign 2000 1987 2011 2005 2000 1982 Charter - Worldwide 1 1 2 1 0 0 5 Charter – U.S. 1 1 2 1 0 0 5 Charter - Foreign 1 1 2 1 0 0 5 Up Since Last Report Down Since Last Report * Before June 2004 40,000BBL plus barges were grouped together Of the 3,848 barges and 13,124 vessels we currently track, 689 are tank barges with 39 inland and 25 ocean or coastal barges officially on the market for sale. Eleven of the 39 inland barges are 10 years of age or less. Fourteen or 35.9% of the inland barges are 25 years of age or over. Five years ago 14 inland tank barges were for sale, with 75.0% 25 years of age or older. The oldest inland tank barge listed today is a 59 year old, 1,000BBL self-propelled tank barge used for transporting lube oil in the U.S. Northeast. This old lady is counterbalanced by one 3,200mtdw, propelled, foreign-flagged 2015-built 22,000BBL tank barge located in the Far East. Nine double hull inland barges listed in the Americas from 29,500-31,396BBL capacity were built after 2000.

Transcript of Marcon International, Inc. P.O. Box 1170, 9 NW Front ... · Sales include 91 ocean tank barges...

Marcon International, Inc. Vessels and Barges for Sale or Charter Worldwide

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

P.O. Box 1170, 9 NW Front Street, Suite 201 Coupeville, WA 98239 U.S.A. Telephone (360) 678 8880 Fax (360) 678-8890 E Mail: [email protected]

http://www.marcon.com

February 2017

Tank Barge Market Report Following is a breakdown of both foreign and U.S. tank barges officially on the market and available through Marcon. Not included are those barges not officially on the market, which we may be able to develop on a private and confidential basis.

Listed Inland Tank Barges Barrel Capacity Under

10,000 10,000- 19,999

20,000- 29,999

30,000- 39,999

40,000- 49,999

50,000 Plus *

Total

Jan 1998 31 18 12 0 0 61

Jan 1999 31 14 11 1 0 57

Jan 2000 33 12 14 0 0 59

Feb 2001 22 14 11 0 0 47

Mar 2002 22 7 10 1 0 40

Mar 2003 28 18 19 4 1 70

Mar 2004 21 35 26 15 3 100

Mar 2005 19 44 40 8 4 1 116

Mar 2006 10 37 21 5 2 1 76

Mar 2007 6 9 4 0 0 2 21

Mar 2008 10 4 6 2 1 0 23

Mar 2009 12 8 7 5 1 0 33

Feb 2010 8 6 6 8 1 0 29

Feb 2011 10 13 4 4 2 0 33

Feb 2012 6 5 3 0 0 0 14

Feb 2013 5 16 8 0 1 0 30

Feb 2014 14 16 16 1 1 1 49

Feb 2015 9 11 10 1 1 0 32

Feb 2016 6 9 5 1 3 2 26

May 2016 6 14 7 15 3 2 47

Aug 2016 9 9 10 2 6 2 38

Nov 2016 7 11 9 12 2 2 43

Feb 2017 – Worldwide 7 9 8 11 2 2 39

Feb 2017 – U.S. 3 6 6 10 0 1 26

Feb 2017 - Foreign 4 3 2 1 2 1 13

Avg. Age - Worldwide 1981 1985 2002 1999 2000 1988

Avg. Age – U.S. 1962 1985 2000 1998 0 1993

Avg. Age - Foreign 2000 1987 2011 2005 2000 1982

Charter - Worldwide 1 1 2 1 0 0 5

Charter – U.S. 1 1 2 1 0 0 5

Charter - Foreign 1 1 2 1 0 0 5

Up Since Last Report Down Since Last Report * Before June 2004 40,000BBL plus barges were grouped together

Of the 3,848 barges and 13,124 vessels we currently track, 689 are tank barges with 39 inland and 25 ocean or coastal barges officially on the market for sale. Eleven of the 39 inland barges are 10 years of age or less. Fourteen or 35.9% of the inland barges are 25 years of age or over. Five years ago 14 inland tank barges were for sale, with 75.0% 25 years of age or older. The oldest inland tank barge listed today is a 59 year old, 1,000BBL self-propelled tank barge used for transporting lube oil in the U.S. Northeast. This old lady is counterbalanced by one 3,200mtdw, propelled, foreign-flagged 2015-built 22,000BBL tank barge located in the Far East. Nine double hull inland barges listed in the Americas from 29,500-31,396BBL capacity were built after 2000.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

2

Inland Tank Barges Breakdown by Built & BBL

Built <10000 10000-19999 20000-29999 30000-39999 40000-50000 >50000 Total

1958 1

1

1964

1

1

1966 1

1

1968

1

1

1969

1

1

1973

1

1

1974

1

1

1982

1

1 2

1983

1

1

1987 1

1

1992

1

2

3

1993

1 1

1994

1

1

1995

1

1

1996

2

2

2000

4 1

5

2005

1

1

2006

1

1

2008

1

1

2009

2

2

2012 1

4

5

2015

1

1

Unknown 3

1

4

Total 7 9 8 11 2 2 39

Listed Ocean and Coastal Tank Barges Barrel Capacity

Under 10,000

10,000-19,999

20,000-29,999

30,000-39,999

40,000-49,999

50,000-59,999

60,000-69,999

70,000-79,999

80,000-89,999

90,000-99,999

100,000 Plus

Total

Mar 2002 22 7 10 1 0 0 0 0 0 0 0 40

Mar 2003 28 18 19 4 1 0 0 0 0 0 0 70 Mar 2004 2 15 7 2 2 9 0 0 0 0 0 37 Mar 2005 5 9 5 1 0 1 0 2 1 4 3 31 Mar 2006 3 6 9 3 2 1 0 0 1 0 0 25 Mar 2007 2 11 9 2 3 1 2 0 0 2 3 35 Mar 2008 5 12 10 3 1 1 2 2 0 1 2 39 Mar 2009 5 6 15 8 5 5 4 3 0 1 5 57 Feb 2010 3 15 17 7 3 5 6 6 1 3 10 76 Feb 2011 6 4 18 11 2 6 4 5 1 1 6 64 Feb 2012 5 4 7 7 5 3 0 1 1 1 0 34 Feb 2013 7 3 7 6 4 3 0 2 1 2 2 37 Feb 2014 5 7 8 10 2 1 0 1 1 1 0 36 Feb 2015 4 7 6 12 3 1 0 0 2 1 0 36 Feb 2016 3 3 3 4 1 2 0 1 4 1 0 22 May 2016 3 6 4 4 1 2 0 1 3 1 0 25 Aug 2016 3 6 5 3 1 2 0 1 2 1 2 26 Nov 2016 3 6 7 3 1 2 0 1 2 1 2 28 Feb 2017 – Worldwide 3 6 5 3 1 2 0 1 2 0 2 25 Feb 2017 – U.S. 0 0 1 1 1 1 0 0 1 0 2 7 Feb 2017- Foreign 3 6 4 2 1 1 0 1 1 0 0 19 Avg. Age - Worldwide 1993 1997 1999 1985 1969 1968 0 1971 1976 0 1973 Avg. Age - U.S. 0 0 1980 1961 0 1971 0 0 1976 0 1973 Avg. Age - Foreign 1993 1997 2003 1998 1969 1965 0 1971 1976 0 0 Charter - Worldwide 2 1 2 0 0 2 0 0 0 0 0 7 Charter - U.S. 0 1 0 0 0 2 0 0 0 0 0 3 Charter - Foreign 2 0 1 0 0 1 0 0 0 0 0 4

Up Since Last Report Down Since Last Report Before June 2004 all 50,000BBL plus barges were grouped together

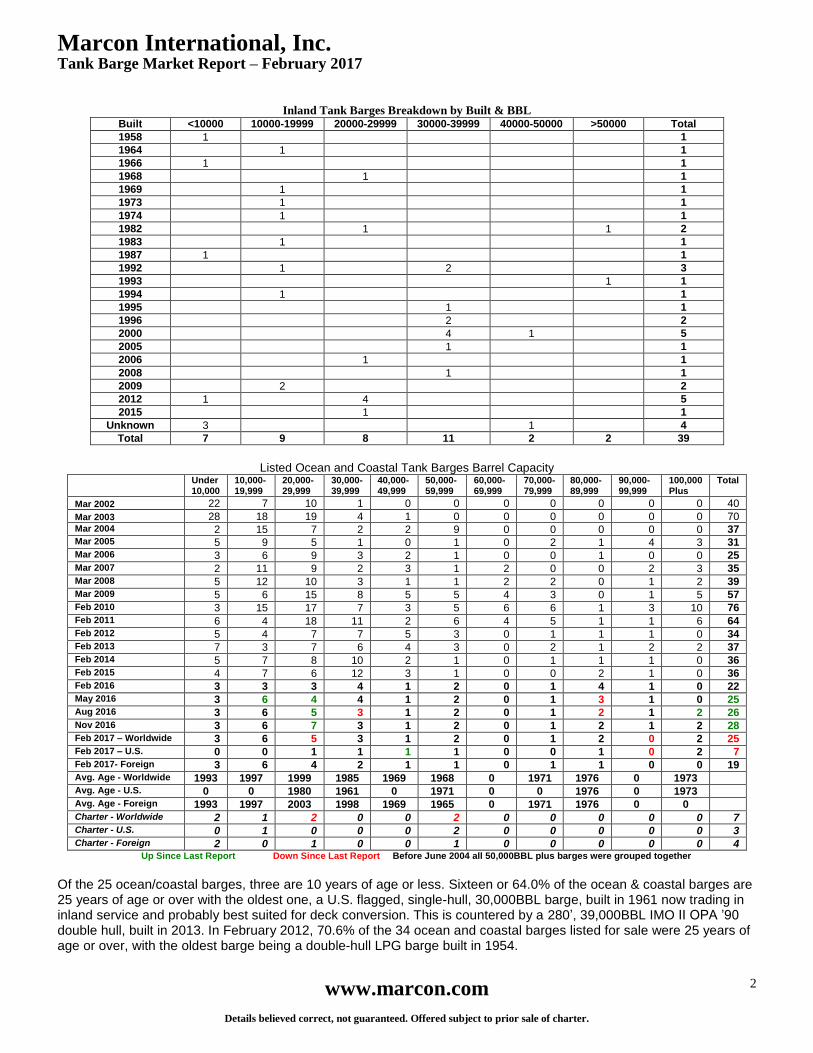

Of the 25 ocean/coastal barges, three are 10 years of age or less. Sixteen or 64.0% of the ocean & coastal barges are 25 years of age or over with the oldest one, a U.S. flagged, single-hull, 30,000BBL barge, built in 1961 now trading in inland service and probably best suited for deck conversion. This is countered by a 280’, 39,000BBL IMO II OPA ’90 double hull, built in 2013. In February 2012, 70.6% of the 34 ocean and coastal barges listed for sale were 25 years of age or over, with the oldest barge being a double-hull LPG barge built in 1954.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

3

Ocean & Coastal Tank Barges Breakdown by Built & BBL

Built <10000 10000-19999

20000-29999

30000-39999

40000-49999

50000-59999

70000-79999

80000-89999 >100000 Total

1961

1

1

1965

1

1

1970

1 1

1971

1 1

2

1976

1

2 1 4

1979 1

1

1982

1

1

1990

1 1

2

1992

2

2

1998 1

1

2000

1

1

2001

1

1

2002 1 1 1

3

2005

1

1

2010

1

1

2012

1

1

2013

1

1

Total 3 6 5 3 1 2 1 2 2 25

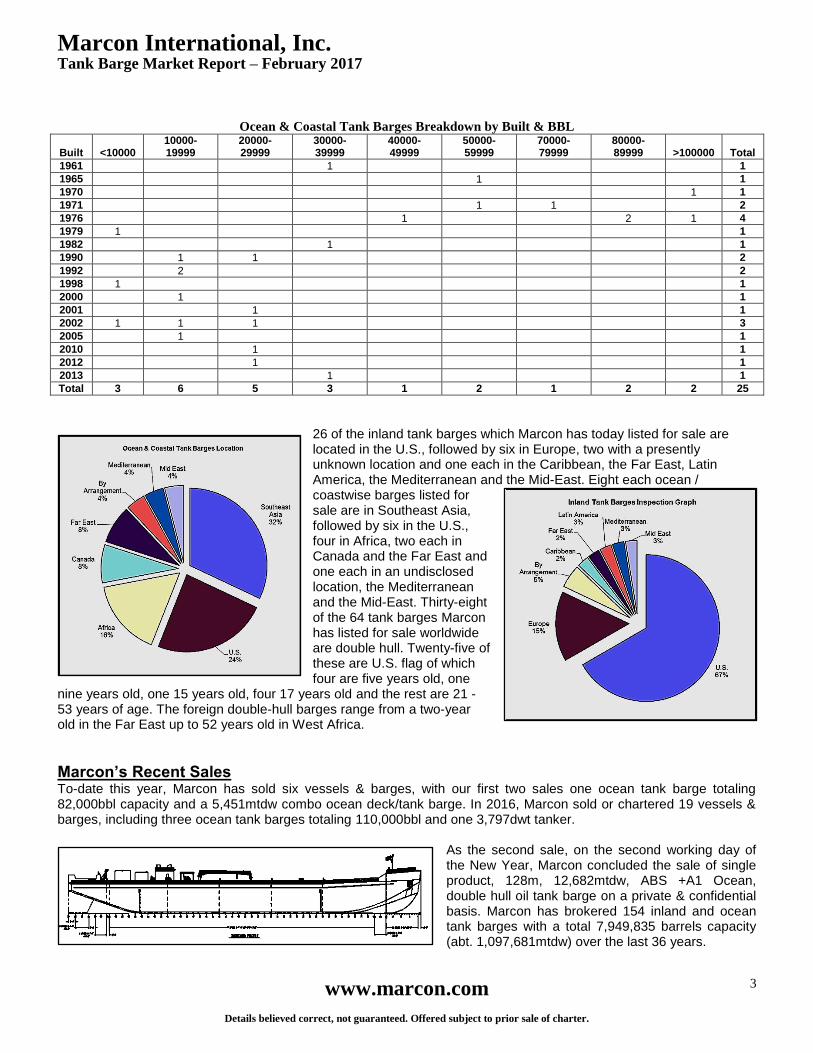

26 of the inland tank barges which Marcon has today listed for sale are located in the U.S., followed by six in Europe, two with a presently unknown location and one each in the Caribbean, the Far East, Latin America, the Mediterranean and the Mid-East. Eight each ocean / coastwise barges listed for sale are in Southeast Asia, followed by six in the U.S., four in Africa, two each in Canada and the Far East and one each in an undisclosed location, the Mediterranean and the Mid-East. Thirty-eight of the 64 tank barges Marcon has listed for sale worldwide are double hull. Twenty-five of these are U.S. flag of which four are five years old, one

nine years old, one 15 years old, four 17 years old and the rest are 21 - 53 years of age. The foreign double-hull barges range from a two-year old in the Far East up to 52 years old in West Africa.

Marcon’s Recent Sales To-date this year, Marcon has sold six vessels & barges, with our first two sales one ocean tank barge totaling 82,000bbl capacity and a 5,451mtdw combo ocean deck/tank barge. In 2016, Marcon sold or chartered 19 vessels & barges, including three ocean tank barges totaling 110,000bbl and one 3,797dwt tanker.

As the second sale, on the second working day of the New Year, Marcon concluded the sale of single product, 128m, 12,682mtdw, ABS +A1 Ocean, double hull oil tank barge on a private & confidential basis. Marcon has brokered 154 inland and ocean tank barges with a total 7,949,835 barrels capacity (abt. 1,097,681mtdw) over the last 36 years.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

4

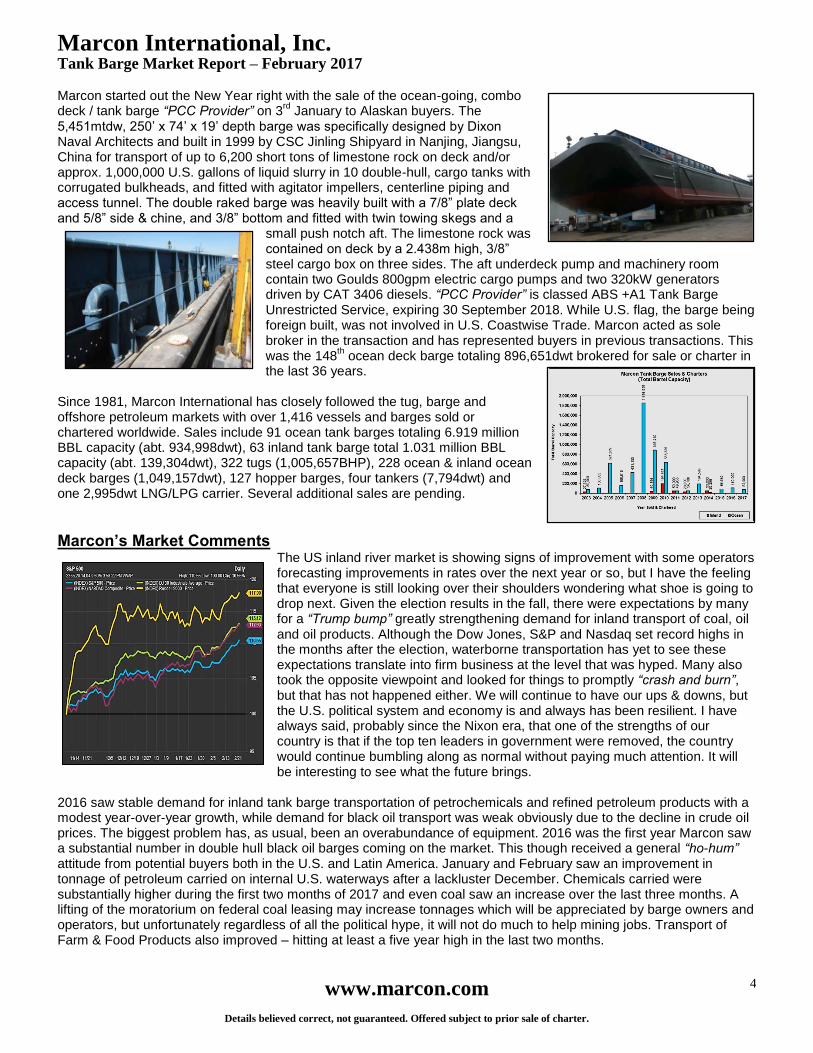

Marcon started out the New Year right with the sale of the ocean-going, combo deck / tank barge “PCC Provider” on 3

rd January to Alaskan buyers. The

5,451mtdw, 250’ x 74’ x 19’ depth barge was specifically designed by Dixon Naval Architects and built in 1999 by CSC Jinling Shipyard in Nanjing, Jiangsu, China for transport of up to 6,200 short tons of limestone rock on deck and/or approx. 1,000,000 U.S. gallons of liquid slurry in 10 double-hull, cargo tanks with corrugated bulkheads, and fitted with agitator impellers, centerline piping and access tunnel. The double raked barge was heavily built with a 7/8” plate deck and 5/8” side & chine, and 3/8” bottom and fitted with twin towing skegs and a

small push notch aft. The limestone rock was contained on deck by a 2.438m high, 3/8” steel cargo box on three sides. The aft underdeck pump and machinery room contain two Goulds 800gpm electric cargo pumps and two 320kW generators driven by CAT 3406 diesels. “PCC Provider” is classed ABS +A1 Tank Barge Unrestricted Service, expiring 30 September 2018. While U.S. flag, the barge being foreign built, was not involved in U.S. Coastwise Trade. Marcon acted as sole broker in the transaction and has represented buyers in previous transactions. This was the 148

th ocean deck barge totaling 896,651dwt brokered for sale or charter in

the last 36 years. Since 1981, Marcon International has closely followed the tug, barge and offshore petroleum markets with over 1,416 vessels and barges sold or chartered worldwide. Sales include 91 ocean tank barges totaling 6.919 million BBL capacity (abt. 934,998dwt), 63 inland tank barge total 1.031 million BBL capacity (abt. 139,304dwt), 322 tugs (1,005,657BHP), 228 ocean & inland ocean deck barges (1,049,157dwt), 127 hopper barges, four tankers (7,794dwt) and one 2,995dwt LNG/LPG carrier. Several additional sales are pending.

Marcon’s Market Comments The US inland river market is showing signs of improvement with some operators forecasting improvements in rates over the next year or so, but I have the feeling that everyone is still looking over their shoulders wondering what shoe is going to drop next. Given the election results in the fall, there were expectations by many for a “Trump bump” greatly strengthening demand for inland transport of coal, oil and oil products. Although the Dow Jones, S&P and Nasdaq set record highs in the months after the election, waterborne transportation has yet to see these expectations translate into firm business at the level that was hyped. Many also took the opposite viewpoint and looked for things to promptly “crash and burn”, but that has not happened either. We will continue to have our ups & downs, but the U.S. political system and economy is and always has been resilient. I have always said, probably since the Nixon era, that one of the strengths of our country is that if the top ten leaders in government were removed, the country would continue bumbling along as normal without paying much attention. It will be interesting to see what the future brings.

2016 saw stable demand for inland tank barge transportation of petrochemicals and refined petroleum products with a modest year-over-year growth, while demand for black oil transport was weak obviously due to the decline in crude oil prices. The biggest problem has, as usual, been an overabundance of equipment. 2016 was the first year Marcon saw a substantial number in double hull black oil barges coming on the market. This though received a general “ho-hum” attitude from potential buyers both in the U.S. and Latin America. January and February saw an improvement in tonnage of petroleum carried on internal U.S. waterways after a lackluster December. Chemicals carried were substantially higher during the first two months of 2017 and even coal saw an increase over the last three months. A lifting of the moratorium on federal coal leasing may increase tonnages which will be appreciated by barge owners and operators, but unfortunately regardless of all the political hype, it will not do much to help mining jobs. Transport of Farm & Food Products also improved – hitting at least a five year high in the last two months.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

5

The sale and purchase market for pushboats and inland river barges remains flat with a continuing disconnect between asking prices, what a “willing buyer” will offer and what a “willing seller” may actually accept below his official price - especially for older units. Barge newbuild prices reportedly remain lower than prior years. Mid-February SteelBenchmarker prices in the U.S., East of the Mississippi were generally lower 1 – 9% with the exception of standard steel plate up 5%. The foreign market for US flag surplus equipment remains slow given the general worldwide reduction in various commodities, typical older age of most U.S. second-hand tonnage available, the strong US Dollar and just generally weak demand.

Shipyard News & Deliveries The Shearer Group, Inc. (TSGI) is pleased to announce the completion of a 200’ x 35’ x 12’ double skin tank barge. TSGI was contracted by C&C Marine and Repair, LLC to provide contract design services. The barge is the first of a series of double skin tank barges that will be built by C&C Marine. It is a flush deck barge with externally framed tanks and classed as a Subchapter O, USCG, acid barge. C&C Marine and Repair offers a full range of marine fabrication and repair services to the maritime industry. With its 30-acre facility on the Gulf Intracoastal Waterway minutes from downtown New Orleans, LA, and over 230,000ft2 in full-enclosed shop area,

C&C Marine can complete any marine project, including barge fabrication, barge repairs, new vessel construction, vessel conversions, general fabrication and barge stacking, and other unique or highly-specialized projects. The Shearer Group, Inc. (TSGI) is a global leader for design of inland towboats and barges. Fincantieri Bay Shipbuilding's Sturgeon Bay, WI, shipyard in November 2016, delivered the “Kirby 155-01”, a 155,000-barrel capacity barge, and the MV “Heath Wood”, a 6,000HP tug for Kirby Corporation. The vessels are to be operated as an Articulated Tug-Barge unit and will haul petroleum and chemical products domestically. This is the first unit delivered under a 2014 contract for two identical ATB units. The second ATB unit is scheduled for delivery in the summer of 2017. Houston based Kirby Corporation is America's largest tank barge operator, transporting bulk liquid products throughout the Mississippi River System, the Gulf Intracoastal Waterway, along all

three Unites States coasts, and in Alaska and Hawaii. Kirby currently operates several ATB units built by Fincantieri Bay Shipbuilding in the mid-2000s. "The fact that this ATB was delivered ontime and within contracted costs speaks to the efficiency of our engineering, planning and manufacturing processes," said Todd Thayse, Fincantieri Bay Shipbuilding Vice President and General Manager. "On-time, on budget delivery is critical to our customers, and, along with consistently high-quality build, it is the basis for retaining and reinforcing long-term relationships." Francesco Valente, President and CEO of Fincantieri Marine Group, commented that "the recent expansion of the FBS yard will allow continued support to our established customers along with the opportunity to grow into new markets. The expansion provides additional manufacturing facilities and state-of-the-art manufacturing equipment, that combined with our advanced manufacturing processes, will further enhance our competitive position.”

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

6

Spain's SENER engineering and technology group is to carry out the basic and detail engineering for two double-hulled vessels being built to collect liquid oily waste and solid waste from ships in compliance with MARPOL regulations. The two barges are being built in Galicia's Nodosa shipyard for shipbuilder Tecnología Medio Ambiente (TMA). SENER says its design will help TMA conduct its activities efficiently, reducing its environmental impact to a minimum. The larger barge has six tanks for storing liquid waste, with a total capacity of 230m3. For solid waste, resources have been installed on the cargo deck for loading and unloading six containers, with a hydraulically operated telescopic crane installed for moving the containers. The smaller barge has two MARPOL waste tanks with a capacity of 32.5m3, four containers on deck for collecting solid waste, and a hydraulic crane.

Conrad Shipyard, Morgan City, LA, recently delivered their Hull C01149, the “Double Skin 510A”, a 55,000BBL capacity, 361.0’ x 62.0’ x 24.5’ depth asphalt barge, to Vane Brothers Company of Baltimore, MD. The barge is equipped with a complete loading and discharging system in 10 tank compartments and includes a cargo thermal heating system with over 8 miles of heating coil pipe. Barge is classed ABS +A1, Oil Tank Barge, UWILD, Unrestricted Service. The “Double Skin 510A”

was constructed at Conrad's Deepwater South facility and will operate out of Philadelphia, PA. "We appreciate Vane Brother's confidence in our shipyard, and it is a pleasure doing business with their management team," said Conrad Shipyard Senior Vice President Dan Conrad. "The 55,000-BBL asphalt barge is a beautiful vessel and is a testament to the exceptional skills of our workforce." The end of November 2016, Philly Shipyard, Inc. (PSI) delivered the U.S. flag “American Endurance” (Hull 025), the first of four next generation 50,000dwt product tankers that it is building for American Petroleum Tankers (APT), a subsidiary of Kinder Morgan, Inc. This delivery is the 25th vessel built by PSI (formerly known as Aker Philadelphia Shipyard, Inc.). The next generation 49,828mtdwt product tanker is based on a proven Hyundai Mipo Dockyards (HMD) design that also incorporates numerous fuel efficiency features, flexible cargo capability, and the latest regulatory requirements. The vessel, built at a reported cost of region US$ 125 million, has also received LNG Ready Level 1 approval from the American Bureau of Shipping (ABS). The 183.3m x 32.2m x 19.1m depth / 13.0m draft, double hull IMO Class II tanker has a carrying capacity of abt. 52,909m3 liquid with a flash point under 60 deg. C. at 98% in 6 each P/S epoxy coated tanks and a segregated ballast capacity of abt. 22,428m3. Tanker is fitted with COW, IGS, SBT (Protective), Closed Loading, VRS – Vapor Recovery System, SPM equipped and twelve 600m3/h cargo

pumps. She is powered by a single 8,200kW MAN-B&W 6S50ME-B9 main engine built under license by Hyundai Heavy Industries in South Korea and develops 11,149HP at 99PM. “Today’s delivery of our 25th vessel, aptly named the ‘American Endurance’, is a profound symbol of the shipbuilding legacy we have continued since re-opening in 1997. In collaboration with American Petroleum Tankers, we are proud of our contributions to renew the current tanker fleet with a more modern and environmentally friendly design. This vessel, like all others, was built from the hands and hearts of 1,200 shipbuilders for future crew to operate safely and with the quality expected.” The shipyard has commenced construction of three other 50,000dwt tankers for APT and two 3,600 TEU containerships for Matson Navigation Company,

Inc……The keel laying milestone for the fourth product tanker in the series was held on 12th January 2017. Keeping

with long held shipbuilding tradition, coins were placed on one of the keel blocks before the 650 ton unit was lowered into place in the dry dock. Representatives from Philly Shipyard and Kinder Morgan were in attendance to place the coins as a sign of good fortune and safe travels. The second product tanker the series, “American Freedom” (Hull 026) is expected to be delivered the end of March. The tankers are classed ABS +A1, Chemical Tanker, Oil Carrier, ESP, +AMS, +ACCU, UWILD, ENVIRO, Unrestricted Service. “American Liberty” (Hull 027) and “American Pride” (Hull 028), the third and fourth vessels, are expected to be delivered around August 2017 and December 2017 respectively.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

7

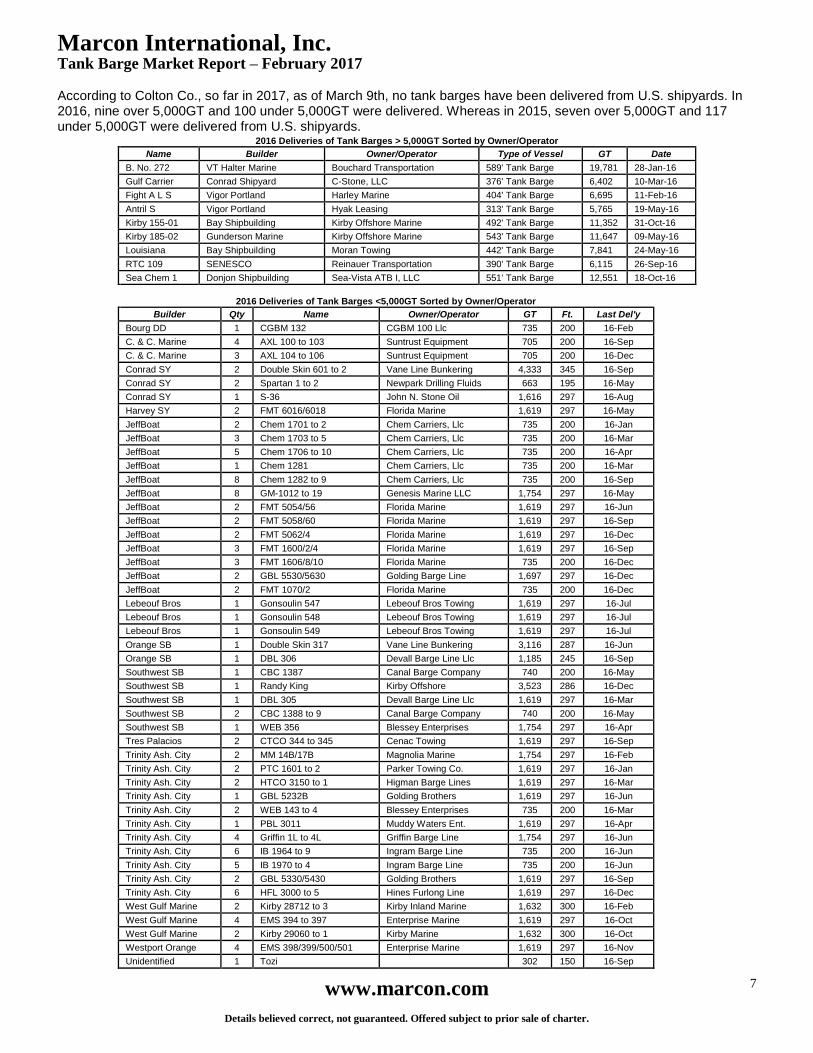

According to Colton Co., so far in 2017, as of March 9th, no tank barges have been delivered from U.S. shipyards. In 2016, nine over 5,000GT and 100 under 5,000GT were delivered. Whereas in 2015, seven over 5,000GT and 117 under 5,000GT were delivered from U.S. shipyards.

2016 Deliveries of Tank Barges > 5,000GT Sorted by Owner/Operator

Name Builder Owner/Operator Type of Vessel GT Date

B. No. 272 VT Halter Marine Bouchard Transportation 589' Tank Barge 19,781 28-Jan-16

Gulf Carrier Conrad Shipyard C-Stone, LLC 376' Tank Barge 6,402 10-Mar-16

Fight A L S Vigor Portland Harley Marine 404' Tank Barge 6,695 11-Feb-16

Antril S Vigor Portland Hyak Leasing 313' Tank Barge 5,765 19-May-16

Kirby 155-01 Bay Shipbuilding Kirby Offshore Marine 492' Tank Barge 11,352 31-Oct-16

Kirby 185-02 Gunderson Marine Kirby Offshore Marine 543' Tank Barge 11,647 09-May-16

Louisiana Bay Shipbuilding Moran Towing 442' Tank Barge 7,841 24-May-16

RTC 109 SENESCO Reinauer Transportation 390' Tank Barge 6,115 26-Sep-16

Sea Chem 1 Donjon Shipbuilding Sea-Vista ATB I, LLC 551' Tank Barge 12,551 18-Oct-16

2016 Deliveries of Tank Barges <5,000GT Sorted by Owner/Operator

Builder Qty Name Owner/Operator GT Ft. Last Del'y

Bourg DD 1 CGBM 132 CGBM 100 Llc 735 200 16-Feb

C. & C. Marine 4 AXL 100 to 103 Suntrust Equipment 705 200 16-Sep

C. & C. Marine 3 AXL 104 to 106 Suntrust Equipment 705 200 16-Dec

Conrad SY 2 Double Skin 601 to 2 Vane Line Bunkering 4,333 345 16-Sep

Conrad SY 2 Spartan 1 to 2 Newpark Drilling Fluids 663 195 16-May

Conrad SY 1 S-36 John N. Stone Oil 1,616 297 16-Aug

Harvey SY 2 FMT 6016/6018 Florida Marine 1,619 297 16-May

JeffBoat 2 Chem 1701 to 2 Chem Carriers, Llc 735 200 16-Jan

JeffBoat 3 Chem 1703 to 5 Chem Carriers, Llc 735 200 16-Mar

JeffBoat 5 Chem 1706 to 10 Chem Carriers, Llc 735 200 16-Apr

JeffBoat 1 Chem 1281 Chem Carriers, Llc 735 200 16-Mar

JeffBoat 8 Chem 1282 to 9 Chem Carriers, Llc 735 200 16-Sep

JeffBoat 8 GM-1012 to 19 Genesis Marine LLC 1,754 297 16-May

JeffBoat 2 FMT 5054/56 Florida Marine 1,619 297 16-Jun

JeffBoat 2 FMT 5058/60 Florida Marine 1,619 297 16-Sep

JeffBoat 2 FMT 5062/4 Florida Marine 1,619 297 16-Dec

JeffBoat 3 FMT 1600/2/4 Florida Marine 1,619 297 16-Sep

JeffBoat 3 FMT 1606/8/10 Florida Marine 735 200 16-Dec

JeffBoat 2 GBL 5530/5630 Golding Barge Line 1,697 297 16-Dec

JeffBoat 2 FMT 1070/2 Florida Marine 735 200 16-Dec

Lebeouf Bros 1 Gonsoulin 547 Lebeouf Bros Towing 1,619 297 16-Jul

Lebeouf Bros 1 Gonsoulin 548 Lebeouf Bros Towing 1,619 297 16-Jul

Lebeouf Bros 1 Gonsoulin 549 Lebeouf Bros Towing 1,619 297 16-Jul

Orange SB 1 Double Skin 317 Vane Line Bunkering 3,116 287 16-Jun

Orange SB 1 DBL 306 Devall Barge Line Llc 1,185 245 16-Sep

Southwest SB 1 CBC 1387 Canal Barge Company 740 200 16-May

Southwest SB 1 Randy King Kirby Offshore 3,523 286 16-Dec

Southwest SB 1 DBL 305 Devall Barge Line Llc 1,619 297 16-Mar

Southwest SB 2 CBC 1388 to 9 Canal Barge Company 740 200 16-May

Southwest SB 1 WEB 356 Blessey Enterprises 1,754 297 16-Apr

Tres Palacios 2 CTCO 344 to 345 Cenac Towing 1,619 297 16-Sep

Trinity Ash. City 2 MM 14B/17B Magnolia Marine 1,754 297 16-Feb

Trinity Ash. City 2 PTC 1601 to 2 Parker Towing Co. 1,619 297 16-Jan

Trinity Ash. City 2 HTCO 3150 to 1 Higman Barge Lines 1,619 297 16-Mar

Trinity Ash. City 1 GBL 5232B Golding Brothers 1,619 297 16-Jun

Trinity Ash. City 2 WEB 143 to 4 Blessey Enterprises 735 200 16-Mar

Trinity Ash. City 1 PBL 3011 Muddy Waters Ent. 1,619 297 16-Apr

Trinity Ash. City 4 Griffin 1L to 4L Griffin Barge Line 1,754 297 16-Jun

Trinity Ash. City 6 IB 1964 to 9 Ingram Barge Line 735 200 16-Jun

Trinity Ash. City 5 IB 1970 to 4 Ingram Barge Line 735 200 16-Jun

Trinity Ash. City 2 GBL 5330/5430 Golding Brothers 1,619 297 16-Sep

Trinity Ash. City 6 HFL 3000 to 5 Hines Furlong Line 1,619 297 16-Dec

West Gulf Marine 2 Kirby 28712 to 3 Kirby Inland Marine 1,632 300 16-Feb

West Gulf Marine 4 EMS 394 to 397 Enterprise Marine 1,619 297 16-Oct

West Gulf Marine 2 Kirby 29060 to 1 Kirby Marine 1,632 300 16-Oct

Westport Orange 4 EMS 398/399/500/501 Enterprise Marine 1,619 297 16-Nov

Unidentified 1 Tozi 302 150 16-Sep

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

8

Recent News in the Market Genesis Energy, L.P. fourth quarter results for the fourth quarter ended December 31, 2016. generated total Available Cash before Reserves of $95.4 million, a decrease of $6.9 million, or 7%, from fourth quarter 2015. In addition to on and offshore pipelines & refinery services, Genesis operates 74 “brown water” barges and 34 inland river pushboats with a total capacity of abt. 2.1 million barrels. Offshore marine “blue water” operations include nine boats and nine coastwise barges (abt. 0.9 million barrel capacity), plus 330,000bbl capacity tanker “American Phoenix”. Four pushboats and eight “brown water” barges are on order with periodic deliveries through 2017. Grant Sims, CEO, said, “Given the continuing challenging operating environment in the energy midstream space, we continue to be pleased with the financial performance of our diversified, yet increasingly integrated, businesses. Our significant infrastructure projects in the Baton Rouge area were substantially completed in the fourth quarter, and we

anticipate completing our repurposing project in Texas in the second quarter of 2017. We would expect to see contributions from these projects to continue to ramp throughout this year and into 2018. At Raceland, we would expect to see volumes start to ramp in mid-2017 as we will be fully capable of receiving and terminaling heavy crudes via rail and medium sour crudes via pipeline.While we are a bit behind schedule and might arguably have a slightly slower ramp from these major investments, we are very excited and have many reasons to believe that we will ultimately exceed our average base case economics across the projects. The momentum for the rest of this year and into 2018 positions us to do reasonably well

even if things don’t improve in late 2017 or 2018. Given our recent and continuing actions to increase liquidity and strengthen our balance sheet, we believe we are well positioned to continue to deliver long term value to all of our stakeholders without ever losing our absolute commitment to safe, reliable and responsible operations.” Offshore pipeline transportation Segment Margin for the 2016 Quarter increased $10.7 million, or 14%, from the 2015 Quarter. Overall, offshore pipeline operations benefited from the general increase in Gulf of Mexico production as a result of 2016 drilling activity which predominantly occurred near existing infrastructure due to the attractive economics in current pricing conditions. Genesis’ extensive pipeline network benefited ratably from this activity. In addition, the 2016 Quarter benefited from the temporary diversion of certain natural gas volumes from third party gas pipelines onto certain of its gas pipeline assets due to disruptions at onshore processing facilities where such volumes typically flow. Refinery services decreased $2.3 million, or 11% primarily due to a 6% decrease in NaHS sales relative to 2015, which is principally related to lower sales volumes to Genesis’ South American mining customers. Sales volumes between quarters to customers in South America can fluctuate due to the timing of third party vessels available to transport bulk deliveries. Pricing in its sales contracts for NaHS typically includes adjustments for fluctuations in commodity benchmarks (primarily caustic soda), freight, labor, energy costs and government indexes. Marine transportation for the 2016 Quarter decreased $7.3 million, or 31%, from 2015. The decrease is primarily due to a combination of lower utilization and lower day rates across Genesis’ various marine asset classes, excepting the M/T “American Phoenix” which is under long term contract through September 2020. In its offshore barge fleet, as a number of units have come off longer term contracts, Genesis has chosen to primarily place them in spot service or short-term (less than a year) service, as it believes the day rates currently being offered by the market are at, or approaching, cyclical lows. In its inland fleet, Genesis saw somewhat of a strengthening in utilization and stabilization in spot day rates towards the end of the year, especially in the black oil, or heavy, intermediate refined products trade, the trade to which Genesis has almost exclusively committed its inland barges..

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

9

For the years ended December 31, 2016 and 2015, net loss attributable to Seacor Holdings Inc. was $215.9 million and $68.8 million respectively. Results for the year ended December 31, 2016 were significantly impacted by

$160.3 million of net losses related to certain impairments and other non-cash charges, including $77.8 million related to marking to fair value certain vessels owned by Seacor’s Offshore Marine Services segment, $19.2 million related to the impairment of intangible assets and goodwill associated with the restructuring of Seacor’s emergency and crisis services business (Witt O'Brien's), and $21.2 million resulting from marking Seacor’s investment in Dorian LPG Ltd. For the quarters ended December 31, 2016 and September 30, 2016, net loss attributable was $93.7 million and $39.8 million, respectively. For the quarter ended December 31, 2015, net loss attributable to SEACOR Holdings Inc. was $56.9 million. Charles Fabrikant, Executive Chairman and CEO, commented: "Our operating income before depreciation, amortization and impairments was slightly better than the preceding quarter although those results do not deserve accolades. During the past 12 months, our Offshore Marine Services' customers cut back on exploration, development, maintenance, and deferred regulatory requirements when possible. The cutbacks were indiscriminate, impacting projects in deep water and shelf. With the exception of Saudi Arabia and the eastern Mediterranean, every geographic region suffered. The "dismal" outlook prophesied in my annual letter of last April was, sadly, correct. I do think 2017 offers better prospects for activity on the shelf, more dollars for maintenance, and attention to regulatory obligations. I also believe that by the end of 2017, or early 2018, activity will increase in Mexico. The potential is mostly in shallow water. Unfortunately, the prospects for deep water and frontier drilling are still bleak. I also believe that the sale of mature properties, which are no longer major holdings for large oil companies, to "independents" could eventually bring activity as new owners are more likely to focus on squeezing out additional barrels from aging installations. Finally, based on published data, 25 FPSO's are due to be placed in service between 2017 through 2019, and there will be 238 platforms installed although some will be quite simple and not manned. In short, I think there is reason to be somewhat optimistic now, although I make this statement with considerable trepidation, particularly because a swoon in oil prices could easily destroy confidence and suffocate a recovery. Based on our assessment of opportunity, we are activating some equipment which has previously been idle, adding reactivation and operating expenses to

future periods. There is no guarantee that day rates in the short run will justify this decision as current market rates are unrewarding. Our inland river business also bucked headwinds for most of 2016. As noted last April, there is a surfeit of equipment due to the reduced activity in transporting coal as well as sand used in shale drilling ("fracking"). In the last few weeks, we have seen demand for barges to transport sand but the overhang of equipment is still too great to be optimistic. Ironically, the prospects for increased grain exports from South America, which could hurt our business in the United States, could be a positive for our South American joint venture, which mostly moves grain and grain products from Brazil, Bolivia and Paraguay to Argentina and Uruguay for export. Given the impact of impairment charges on 2016 results, a comment is in order. The impairment charges covered a range of assets and investments in our joint ventures. As noted in last April's letter, an impairment analysis is not an exact science. Our marks to "fair value" in 2016 are based on the best information available to us. Time will tell if these marks are also reflective of long-term value."

Inland River Services - Operating income was $8.7 million compared with an operating loss of $1.3 million in the preceding quarter. OIBDA was $15.3 million on operating revenues of $53.0 million compared with $5.0 million on operating revenues of $41.1 million in the preceding quarter. Operating results, excluding gains (losses) on asset dispositions and impairments, were $8.7 million higher compared with the preceding quarter primarily due to improved activity levels associated with the fall harvest and favorable operating conditions. An oversupply of equipment, however, continues to place downward pressure on freight rates. During the fourth quarter, Seacor placed 34 newly built dry-cargo barges in service and acquired five harbor boats and other fleeting and terminal assets as an expansion of its fleeting and terminal business. Equity in losses of 50% or less owned companies of $11.3 million in the fourth quarter included a $7.7 million impairment charge for an other-than-temporary decline in the fair value of the Company's investment in its 50% owned joint venture operating on the Parana-Paraguay River Waterway, SCFCo. In addition, operating results for SCFCo were lower as a consequence of seasonality and continued weakness in the iron ore and grain markets.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

10

Shipping Services - Operating income was $7.6 million compared with $13.9 million in the preceding quarter. OIBDA was $16.5 million (of which $5.3 million was attributable to noncontrolling interests) on operating revenues of $59.6 million compared with $22.1 million (of which $8.0 million was attributable to noncontrolling interests) on operating revenues of $57.4 million in the preceding quarter. Operating results were $6.3 million lower in the fourth quarter compared with the preceding quarter primarily due to regulatory drydocking costs and related

out-of-service time for one U.S.-flag product tanker and higher personnel and mobilization costs for one newly built U.S.-flag product tanker placed into service during the fourth quarter. Subsequent to December 31, 2016, Seacor took delivery of one newly built U.S.-flag product tanker, one U.S.-flag harbor tug and two foreign-flag harbor tugs. Other, net losses of $5.5 million in the preceding quarter were primarily due to impairment charges related to a cost method investment in a foreign container shipping company. Equity in losses of 50% or less owned companies of $2.6 million in the fourth quarter were primarily due to charges of $1.9 million upon Seacor’s purchase of a controlling interest from its partner in a joint venture that had refurbished a U.S.-flag offshore tug. General Dynamics’ National Steel & Shipbuilding Co. (NASSCO) of San Diego, California delivered the “Liberty” (Hull 557), the third and final IMO-II double hull ship to be constructed for SEA-Vista LLC as part of a larger eight-ship ECO Class tanker program. In 2013, NASSCO entered into an agreement with SEA-Vista to design and build three 50,000dwt, LNG-conversion-ready product carriers to include a 330,000 barrel cargo capacity (51,000m3 liquid @ 98% in six port each port and starboard epoxy coated cargo tanks. The 186.0m x 32.2m x 19.1m depth / 13.0m draft tankers are a new “ECO” design, offering improved fuel efficiency and cleaner shipping options. Construction for the first of the three ships for SEA-Vista LLC began in November 2014. The first two ships—the “Independence” (Hull 552) and the “Constitution” (Hull 556) - have been delivered and are servicing the Jones Act trade. The “Liberty” is the seventh vessel in an eight-ship ECO Class tanker program for two separate

customers, SEA-Vista LLC and American Petroleum Tankers. Vessels are classed ABS +A1, Chemical Carrier, Oil Carrier, ESP, +AMS, +ACCU, UWILD, Unrestricted Service and fitted with Crude Oil Washing (COW), IGS, SBT (Protective), Closed Loading, VRS – Vapor Recovery System and SPM equipped. “Liberty”, and her sisters, are powered by a single 7,300kW MAN-B&W 6G50ME-B9 manufactured by Doosan Engine Co. Ltd. in South Korea and developing 9,926HP at 88RPM. The eighth ship of the program, the “Palmetto State” (Hull 558) being built for American Petroleum Tankers, is scheduled to be christened and launched on March 25, 2017, at the NASSCO shipyard in San Diego.

Conrad Industries, Inc. Morgan City, Louisiana’s results for quarter ended December 31, 2016 were net loss of $836,000 compared to net income of $3.4 million during fourth quarter 2015. Conrad had net loss of $1.7 million for the twelve months ended December 31, 2016 compared to net income of $10.6 million the previous year. Conrad’s backlog was $216.5 million at December 31, 2016, $211.8 million at December 31, 2015 and $180.2 million at December 31, 2014. Johnny Conrad, President and CEO stated, “Our results for 2016 reflect a continued challenging operating environment. During 2016 our new construction segment was adversely affected by a soft market for energy transportation, increased pricing pressure, and customer delays on large project orders, while our repair and conversion segment continues to be impacted by low crude oil prices. These factors also had a negative impact on our operating results in 2015, and they may continue to impact our operations during 2017. In addition, our 2016 and 2015 operating results were affected by a $13.2 million loss and a $4.0 million loss, respectively, on the LNG Barge. Despite the losses we have incurred on the construction of the LNG Barge, the first vessel of its kind ever constructed in North America, we believe that we have developed the resources to establish ourselves as a leader in LNG marine-related construction in North America.” Mr. Conrad continued, “Throughout our 69 year history, we have used our cash and debt to make investments in our business, continue to diversify our product mix, take advantage of business opportunities and improve efficiency. Pursuant to our capital improvement program, we have invested an aggregate of $61.9 million in our facilities over the last five years. We believe this has allowed us to remain competitive, meet evolving customer needs and effectively navigate a cyclical business. Although we expect 2017 to be another challenging year, we are optimistic about the long-term prospects of our business. We have met these types of challenges in the past, and we remain confident that with our talented and dedicated employees, strong balance sheet and diversified customer base we can effectively respond to changing market conditions.”

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

11

Trinity Industries, Inc. reported net income of $67.6 million for the fourth quarter ended December 31, 2016. Net income for the same quarter 2015 was $200.0 million. Revenues for fourth quarter 2016 totaled $1.1 billion compared to revenues of $1.5 billion for the same quarter of 2015. ".. 2016 results were slightly ahead of our expectations and reflect our Company’s ability to successfully transition as market conditions shift," said Timothy R. Wallace, Trinity’s Chairman, CEO and President. “Our people have continued to execute well in a challenging business environment. We remain focused on

controlling costs, maintaining a strong balance sheet, and initiatives to improve our performance.” Mr. Wallace added, “Many of the market challenges we faced in 2016 persist in 2017. The oversupply of railcars and barges in North America continues to impact market fundamentals. The flexible nature of Trinity's business model positions our company to respond when market conditions shift.” The Inland Barge Group reported revenues of $75.1 million fourth quarter 2016 compared to revenues of $147.2 million fourth

quarter 2015. Operating profit and profit margin for this Group was $6.7 million and 8.9% in fourth quarter 2016 compared to $20.7 million and 14.1% fourth quarter 2015. The decrease in revenues and operating profit compared to the same quarter last year was primarily due to lower barge deliveries and changes in product mix. As of December 31, 2016, the Inland Barge Group had a backlog of $120.0 million compared to a backlog of $177.3 million as of September 30, 2016.

Greenbrier Companies, Inc. of Lake Oswego, Oregon; parent of Gunderson Marine, reported net earnings for first fiscal quarter ended November 30, 2016 of $25.0 million on revenues of $552.3 million. New railcar backlog as of November 30, 2016 was 25,800 units with estimated value of $2.97 billion (average unit sale price $115,000). Included in backlog are 3,800 covered hopper railcars for energy related sand transportation, of which 2,500 units, scheduled for production in 2018, are for a customer who is negotiating with Greenbrier to modify the order. New railcar deliveries totaled 4,000 units for the quarter, compared to 4,600

units for the quarter ended August 31, 2016. Marine backlog as of November 30, 2016 was approx. $103 million. Greenbrier estimates deliveries of 14,000 – 16,000 units and revenues of $2.0 - $2.4 billion for fiscal year 2017. Kirby Corporation of Houston, Texas’ net earnings for fourth quarter ended December 31, 2016 of $32.4 million compared with $50.7 million for fourth quarter 2015. Consolidated revenues for the 2016 fourth quarter were $435.7 million compared with $484.1 million reported for the 2015 fourth quarter. Kirby reported net earnings for full year 2016 of $141.4 million compared with $226.7 million for 2015. Consolidated revenues for 2016 were $1.77 billion compared with $2.15 billion. David Grzebinski, Kirby's President and CEO, commented, "In the inland marine transportation market, utilization averaged in the mid-80% range, but improved to the high 80% range through most of December. The improvement in utilization was driven by a combination of factors, including winter weather conditions, which led to a significant increase in delay days relative to the third quarter, as well as the retirement of older barges and some modest volume improvement. In the

coastal marine transportation market, utilization was in the low 80% range during the quarter, and customers continued to show a preference for sourcing their coastal transportation needs from vessels trading in the spot market over booking new, or extending existing, term contracts." Kirby’s inland fleet consists of 876 tank barges (17.9m barrels of capacity) and 230 towboats. The coastal tank barge fleet consists of 69 tank barges (6.2 m barrels) and 75 tugs. Kirby also operates six offshore dry-bulk barge and tugboat units and six offshore tugboats primarily transporting dry bulk commodities across the Gulf of Mexico.

Marine Transportation - Marine transportation revenues for the 2016 fourth quarter were $356.2 million compared with $399.8 million for the 2015 fourth quarter. Operating income for fourth quarter 2016 was $59.1 million compared with $87.9 million for the 2015. Demand for inland tank barge transportation of petrochemicals, refined petroleum products, and agricultural chemicals was stable with modest year over year volume growth. The volume of crude oil and natural gas condensate carried increased over the 2016 third quarter, while demand for the transportation of black

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

12

oil (heavy fuel oil, asphalt, vacuum gas oil) was weak. Kirby's inland tank barge utilization improved from the low 80% range to the high 80% range over the course of the quarter. Prices for inland equipment on spot contracts were flat sequentially, but both term and spot contract pricing in the fourth quarter were at lower levels relative to last year. Difficult weather during the quarter contributed to better utilization, but also created a number of operating challenges, as dense fog and high winds restricted movements along the Gulf Coast for much of the quarter. Additionally, ice on the Illinois River presented some short-term challenges for upriver transit times and efficiency. Delay days in the fourth quarter increased 124% over the third quarter, but only modestly relative to the 2015 fourth quarter when Kirby experienced delays due to lock closures and high water conditions. In the coastal marine transportation market, demand for the transportation of black oil, petrochemicals, and dry products was stable. In refined petroleum products, a surplus of available industry-wide spot market vessel capacity, and the normal seasonal decline related to the cessation of operations in Alaska, resulted in reduced sequential utilization. Utilization for the coastal tank barge fleet was in the low 80% range. During the fourth quarter, Kirby took delivery of a new 155,000bbl articulated tank barge and tugboat unit (see page 5), which transported ethanol from the Great Lakes to the Northeast on its maiden voyage in late November. Commenting on 2017 first quarter and full year market outlook, Mr. Grzebinski said, "earnings guidance for the 2017 first quarter is $0.40 to $0.55 per share and our full year 2017 guidance is $1.70 to $2.20 per share. Both our first quarter and full year guidance ranges contemplate inland marine transportation utilization in the mid-80% to low 90% range and the full year effect of pricing declines experienced in 2016. We expect industry-wide retirements, lack of new-builds, and additional petrochemical volumes to improve year over year utilization and lead to a modestly better pricing environment in the second half of 2017. In our coastal market, we expect utilization in the mid-70% to mid-80% range both for the first quarter and the full year, as a result of more coastal equipment trading in the spot market. Our guidance range encompasses pricing on coastal market contract renewals declining in the mid-single to low double-digit percentage range relative to year ago levels.” Kirby expects 2017 capital spending to be $165 to $185 million range. Capital spending includes approx. $50 million in progress payments on new coastal equipment, including a 155,000bbl ATB, two 4,900BHP and six 5,000BHP coastal tugs, and final costs on a new petrochemical tank barge. The balance of $115 to $135 million is primarily for two inland tank barges and capital upgrades and improvements to existing inland and coastal marine equipment and facilities, as well as diesel engine services facilities.

Aegean Marine Petroleum Network’s net income for the quarter ended December 31, 2016 was $16.0 million, an increase of $6.3 million or 64.9% compared 2015. Total revenues for fourth quarter 2016 was $1.2 billion, an increase of 29.0% compared to same period 2015, primarily due to the drop in oil prices. E. Nikolas

Tavlarios, Aegean's President, commented, "The fourth quarter marked the end of another strong year for Aegean, despite volatile commodity markets and increased competition. Our flexible business model continued to enable Aegean to capitalize on growth opportunities across our unique platform. As evidenced by consistent portfolio rationalization, we are focused on strengthening our operations and enhancing efficiencies across our business. Our global footprint now includes more than 30 markets and 51 ports......." Spyros Gianniotis, Aegean's CFO, stated, "Our solid results and accomplishments during the quarter demonstrate the long-term potential of our financial strategy. During the fourth quarter we continued our focus on driving higher margins and profitable volume and improved our financial strength. We have maintained a strong balance sheet and are confident our flexibility will support Aegean's continued success. Looking ahead, we will continue to deploy our resources into the most effective and profitable markets to generate the greatest return for Aegean shareholders." Aegean owns two barges, the “Mediterranean” and “Umnenga”, as floating storage facilities in Greece and South Africa. It also operates on-land storage facilities in Las Palmas, Fujairah, Tangiers, Panama, the U.S.A., Hamburg and Barcelona.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

13

Overseas Shipholding Group, Inc. reported results for the fourth quarter and full year 2016. “We are pleased with our performance for the fourth quarter and full year 2016 despite challenging market conditions throughout most of the year,” said Sam Norton, OSG’s president and CEO. “We also successfully executed on our strategic goal of streamlining our operating structure and enhancing our focus by completing the spin-off of International Seaways.” Mr.

Norton continued, “Going forward, OSG will be a diversified U.S. Flag shipping company with a trusted operating franchise and a leading portfolio in the Jones Act market. Our unique position as the only operator of shuttle tankers in the U.S. Gulf Coast, the only licensed operator of lightering vessels in the Delaware Bay, and the only operator of tankers in the Maritime Security Program (“MSP”) helps provide stability against market volatility. We are well-positioned to build on the Company’s strengths, address future growth opportunities and drive shareholder value.” Time Charter Equivalent (TCE) revenues for fourth quarter 2016 were $109.6 million, a decrease of $5.0 million, or 4%, compared with fourth quarter 2015, primarily due to lower average daily rates earned, which accounted for a $9.4 million decrease in TCE revenues. This decrease was partially offset by a $2.9 million increase in Delaware Bay lightering revenues and a 52-day increase in revenue days for its Jones Act fleet, excluding its modern lightering ATBs, driven by fewer drydock and repair days resulting in a $1.5 million increase in TCE revenues. Shipping revenues were $114.8 million for the quarter, down 3% compared with fourth quarter 2015. TCE revenues for full year 2016 were $446.2 million, a decrease of $2.9 million, or 1%, compared with full year 2015. Shipping revenues were $462.4 million 2016, down 1% compared with full year 2015. Net loss for the fourth quarter was $275.5 million, compared with net income of $9.3 million for fourth quarter 2015. Net income from continuing operations for the fourth quarter was $64.7 million compared with a net loss from continuing operations of $34.2 million for fourth quarter 2015. The increase reflects the reversal of the deferred tax liability on unremitted earnings of INSW in the current quarter compared with a provision in the fourth quarter of 2015, reductions in interest expense due to OSG’s significant debt reductions in the fourth quarter of 2015 and in 2016, partially offset by the vessel impairment recognized in the current quarter. OSG completed the separation of its business into two independent publicly-traded companies through the spin-off of its then wholly-owned subsidiary INSW on November 30, 2016. The spin-off separated OSG and INSW into two distinct businesses with separate management. OSG retained the U.S. Flag business and INSW holds entities and other assets and liabilities that formed OSG’s former International Flag business. The spin-off transaction was in the form of a pro rata distribution of INSW’s common stock to OSG’s stockholders and warrant holders of record as of the close of business on November 18, 2016. Settoon Towing, LLC of Pierre Part, Louisiana, operating one of the newest tank barge fleets in the industry, has sold their liquid Bulk division, consisting of 35 towboats and 63 liquid tank barges with a total capacity of nearly two million barrels to Savage Inland Marine, LLC. Russ A. Settoon, Chairman & CEO, commented “This sale positions us better

to serve our customers in the Gathering & Storage and Logistics & Vessel Management divisions where we have been providing first class marine transportation since 1968. We look forward to growth in the future and will continue to invest in our people and our equipment to deliver the safest and most reliable marine transportation to all our customers.” Settoon’s Gathering & Storage segment consists of over 25 boats and 60 barges used to transport and store crude oil and produced water throughout the inland waterways of the U.S. Gulf Coast. RBC Capital Markets and Simmons & Company were financial advisors to Settoon Towing on this transaction. Savage Inland Marine will use the

marine assets to transport a variety of liquid products on the Intracoastal and inland waterways, operating out of south Louisiana. As part of the agreement, Savage Inland Marine expects to hire approximately 250 current Settoon employees. “These strategic assets will strengthen our ability to serve customers in the inland waterway. We look forward to welcoming the Settoon employees involved in this business segment, as Savage Team Members,” said Kirk Aubry, Savage President and CEO. “During a brief transitional period, we will be working closely with Settoon under an operating agreement that will ensure a seamless transition for the customers we serve.” With existing operations in Orange County, Texas, Savage Inland Marine currently provides monitored barge fleeting, operates inland push boats and provides dock services on the Neches River. Savage Inland Marine is an American Waterways Operators member and AWO accredited Responsible Carrier, and is also a member of the Texas Waterway Operators Association, Gulf Intracoastal Canal Association, Mississippi Valley Trade & Transport Council and Oil Companies International Marine Forum. “Marine transportation continues to be among the lowest-cost and safest methods for moving freight,” said Aubry. “With the country’s petrochemical renaissance and expansion of refineries and other facilities along the Intracoastal and inland waterways, we see a bright future for barge transportation in the Gulf Coast and beyond.”

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

14

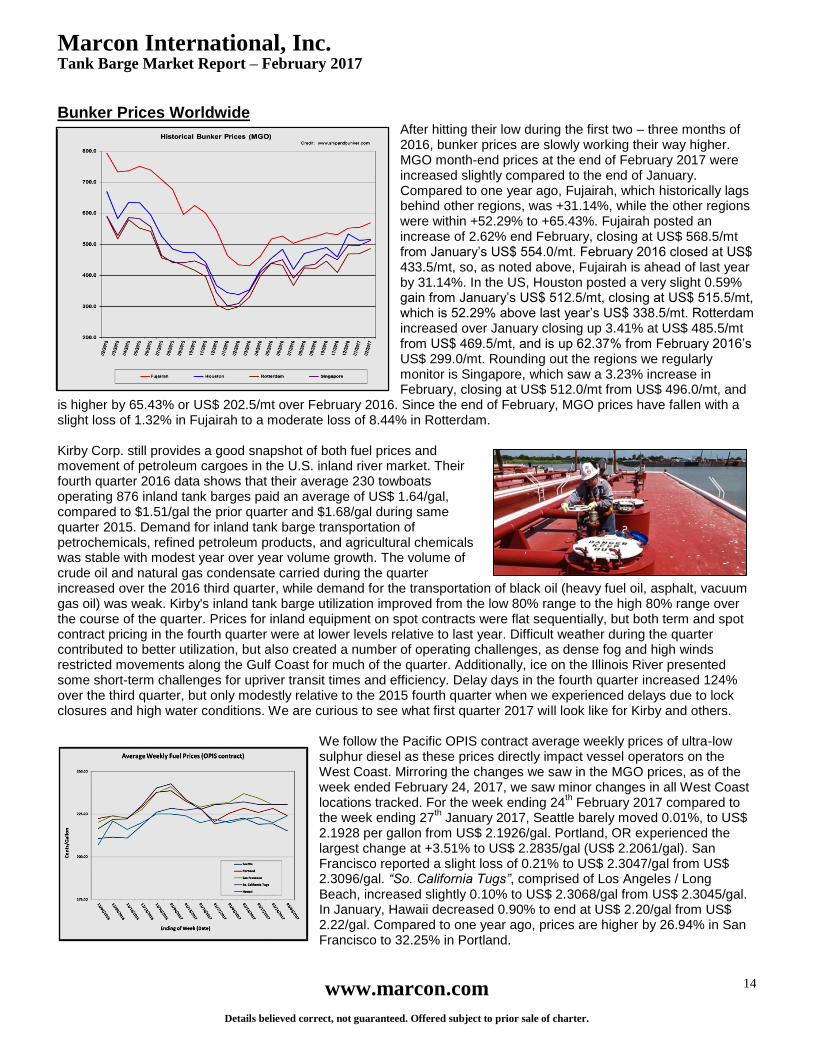

Bunker Prices Worldwide After hitting their low during the first two – three months of 2016, bunker prices are slowly working their way higher. MGO month-end prices at the end of February 2017 were increased slightly compared to the end of January. Compared to one year ago, Fujairah, which historically lags behind other regions, was +31.14%, while the other regions were within +52.29% to +65.43%. Fujairah posted an increase of 2.62% end February, closing at US$ 568.5/mt from January’s US$ 554.0/mt. February 2016 closed at US$ 433.5/mt, so, as noted above, Fujairah is ahead of last year by 31.14%. In the US, Houston posted a very slight 0.59% gain from January’s US$ 512.5/mt, closing at US$ 515.5/mt, which is 52.29% above last year’s US$ 338.5/mt. Rotterdam increased over January closing up 3.41% at US$ 485.5/mt from US$ 469.5/mt, and is up 62.37% from February 2016’s US$ 299.0/mt. Rounding out the regions we regularly monitor is Singapore, which saw a 3.23% increase in February, closing at US$ 512.0/mt from US$ 496.0/mt, and

is higher by 65.43% or US$ 202.5/mt over February 2016. Since the end of February, MGO prices have fallen with a slight loss of 1.32% in Fujairah to a moderate loss of 8.44% in Rotterdam. Kirby Corp. still provides a good snapshot of both fuel prices and movement of petroleum cargoes in the U.S. inland river market. Their fourth quarter 2016 data shows that their average 230 towboats operating 876 inland tank barges paid an average of US$ 1.64/gal, compared to $1.51/gal the prior quarter and $1.68/gal during same quarter 2015. Demand for inland tank barge transportation of petrochemicals, refined petroleum products, and agricultural chemicals was stable with modest year over year volume growth. The volume of crude oil and natural gas condensate carried during the quarter increased over the 2016 third quarter, while demand for the transportation of black oil (heavy fuel oil, asphalt, vacuum gas oil) was weak. Kirby's inland tank barge utilization improved from the low 80% range to the high 80% range over the course of the quarter. Prices for inland equipment on spot contracts were flat sequentially, but both term and spot contract pricing in the fourth quarter were at lower levels relative to last year. Difficult weather during the quarter contributed to better utilization, but also created a number of operating challenges, as dense fog and high winds restricted movements along the Gulf Coast for much of the quarter. Additionally, ice on the Illinois River presented some short-term challenges for upriver transit times and efficiency. Delay days in the fourth quarter increased 124% over the third quarter, but only modestly relative to the 2015 fourth quarter when we experienced delays due to lock closures and high water conditions. We are curious to see what first quarter 2017 will look like for Kirby and others.

We follow the Pacific OPIS contract average weekly prices of ultra-low sulphur diesel as these prices directly impact vessel operators on the West Coast. Mirroring the changes we saw in the MGO prices, as of the week ended February 24, 2017, we saw minor changes in all West Coast locations tracked. For the week ending 24

th February 2017 compared to

the week ending 27th January 2017, Seattle barely moved 0.01%, to US$

2.1928 per gallon from US$ 2.1926/gal. Portland, OR experienced the largest change at +3.51% to US$ 2.2835/gal (US$ 2.2061/gal). San Francisco reported a slight loss of 0.21% to US$ 2.3047/gal from US$ 2.3096/gal. “So. California Tugs”, comprised of Los Angeles / Long Beach, increased slightly 0.10% to US$ 2.3068/gal from US$ 2.3045/gal. In January, Hawaii decreased 0.90% to end at US$ 2.20/gal from US$ 2.22/gal. Compared to one year ago, prices are higher by 26.94% in San Francisco to 32.25% in Portland.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

15

In 2016, U.S. on-highway diesel fuel prices hit an annual low of just under $2 per gallon during the week of February 15

th. Average

U.S. diesel prices had not been below $2 per gallon since 2005. Prices increased steadily through the end of June 2016 then stabilized with a small jump at the end of the year to just over $2.50 / gal. However, prices remain well below the 5-year average by more than 90 cents / gal. Low diesel fuel prices help keep costs low for all modes of transportation as well as on-farm operational costs. For the week ending February 27, the U.S. average weekly retail on-highway diesel fuel prices increased 1 cent from the previous week, 59 cents above the same week last year.

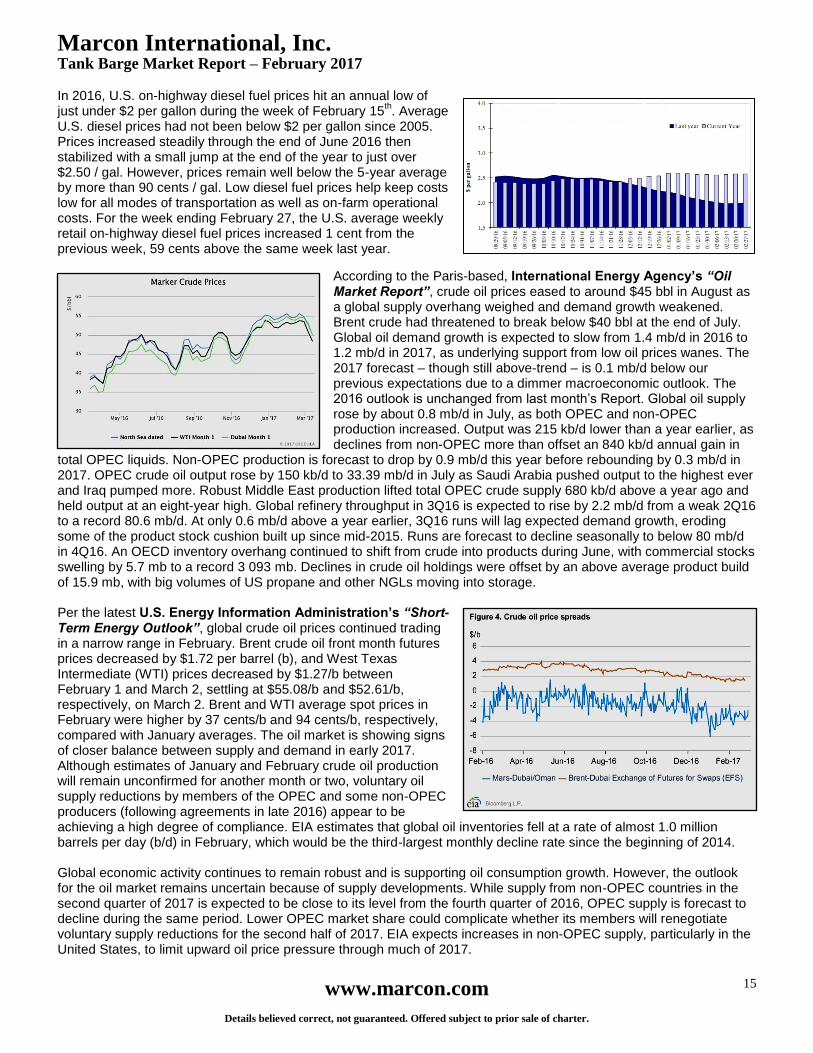

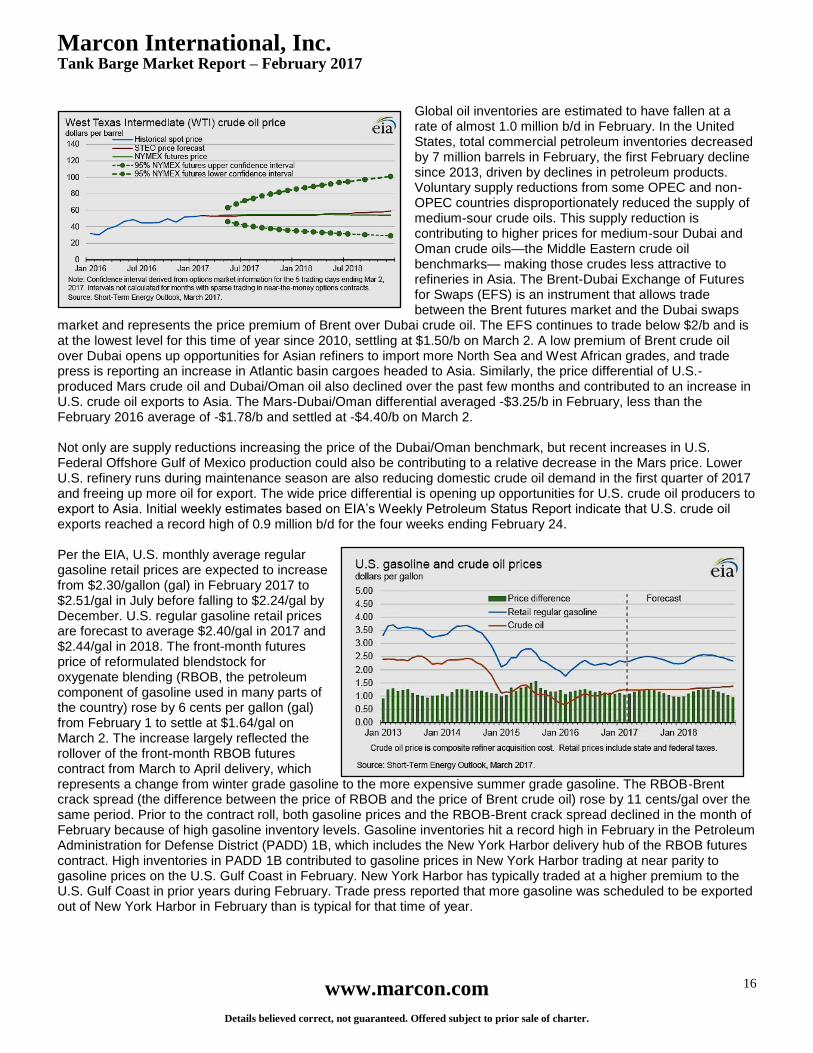

According to the Paris-based, International Energy Agency’s “Oil Market Report”, crude oil prices eased to around $45 bbl in August as a global supply overhang weighed and demand growth weakened. Brent crude had threatened to break below $40 bbl at the end of July. Global oil demand growth is expected to slow from 1.4 mb/d in 2016 to 1.2 mb/d in 2017, as underlying support from low oil prices wanes. The 2017 forecast – though still above-trend – is 0.1 mb/d below our previous expectations due to a dimmer macroeconomic outlook. The 2016 outlook is unchanged from last month’s Report. Global oil supply rose by about 0.8 mb/d in July, as both OPEC and non-OPEC production increased. Output was 215 kb/d lower than a year earlier, as declines from non-OPEC more than offset an 840 kb/d annual gain in

total OPEC liquids. Non-OPEC production is forecast to drop by 0.9 mb/d this year before rebounding by 0.3 mb/d in 2017. OPEC crude oil output rose by 150 kb/d to 33.39 mb/d in July as Saudi Arabia pushed output to the highest ever and Iraq pumped more. Robust Middle East production lifted total OPEC crude supply 680 kb/d above a year ago and held output at an eight-year high. Global refinery throughput in 3Q16 is expected to rise by 2.2 mb/d from a weak 2Q16 to a record 80.6 mb/d. At only 0.6 mb/d above a year earlier, 3Q16 runs will lag expected demand growth, eroding some of the product stock cushion built up since mid-2015. Runs are forecast to decline seasonally to below 80 mb/d in 4Q16. An OECD inventory overhang continued to shift from crude into products during June, with commercial stocks swelling by 5.7 mb to a record 3 093 mb. Declines in crude oil holdings were offset by an above average product build of 15.9 mb, with big volumes of US propane and other NGLs moving into storage. Per the latest U.S. Energy Information Administration’s “Short-Term Energy Outlook”, global crude oil prices continued trading in a narrow range in February. Brent crude oil front month futures prices decreased by $1.72 per barrel (b), and West Texas Intermediate (WTI) prices decreased by $1.27/b between February 1 and March 2, settling at $55.08/b and $52.61/b, respectively, on March 2. Brent and WTI average spot prices in February were higher by 37 cents/b and 94 cents/b, respectively, compared with January averages. The oil market is showing signs of closer balance between supply and demand in early 2017. Although estimates of January and February crude oil production will remain unconfirmed for another month or two, voluntary oil supply reductions by members of the OPEC and some non-OPEC producers (following agreements in late 2016) appear to be achieving a high degree of compliance. EIA estimates that global oil inventories fell at a rate of almost 1.0 million barrels per day (b/d) in February, which would be the third-largest monthly decline rate since the beginning of 2014. Global economic activity continues to remain robust and is supporting oil consumption growth. However, the outlook for the oil market remains uncertain because of supply developments. While supply from non-OPEC countries in the second quarter of 2017 is expected to be close to its level from the fourth quarter of 2016, OPEC supply is forecast to decline during the same period. Lower OPEC market share could complicate whether its members will renegotiate voluntary supply reductions for the second half of 2017. EIA expects increases in non-OPEC supply, particularly in the United States, to limit upward oil price pressure through much of 2017.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

16

Global oil inventories are estimated to have fallen at a rate of almost 1.0 million b/d in February. In the United States, total commercial petroleum inventories decreased by 7 million barrels in February, the first February decline since 2013, driven by declines in petroleum products. Voluntary supply reductions from some OPEC and non-OPEC countries disproportionately reduced the supply of medium-sour crude oils. This supply reduction is contributing to higher prices for medium-sour Dubai and Oman crude oils—the Middle Eastern crude oil benchmarks— making those crudes less attractive to refineries in Asia. The Brent-Dubai Exchange of Futures for Swaps (EFS) is an instrument that allows trade between the Brent futures market and the Dubai swaps

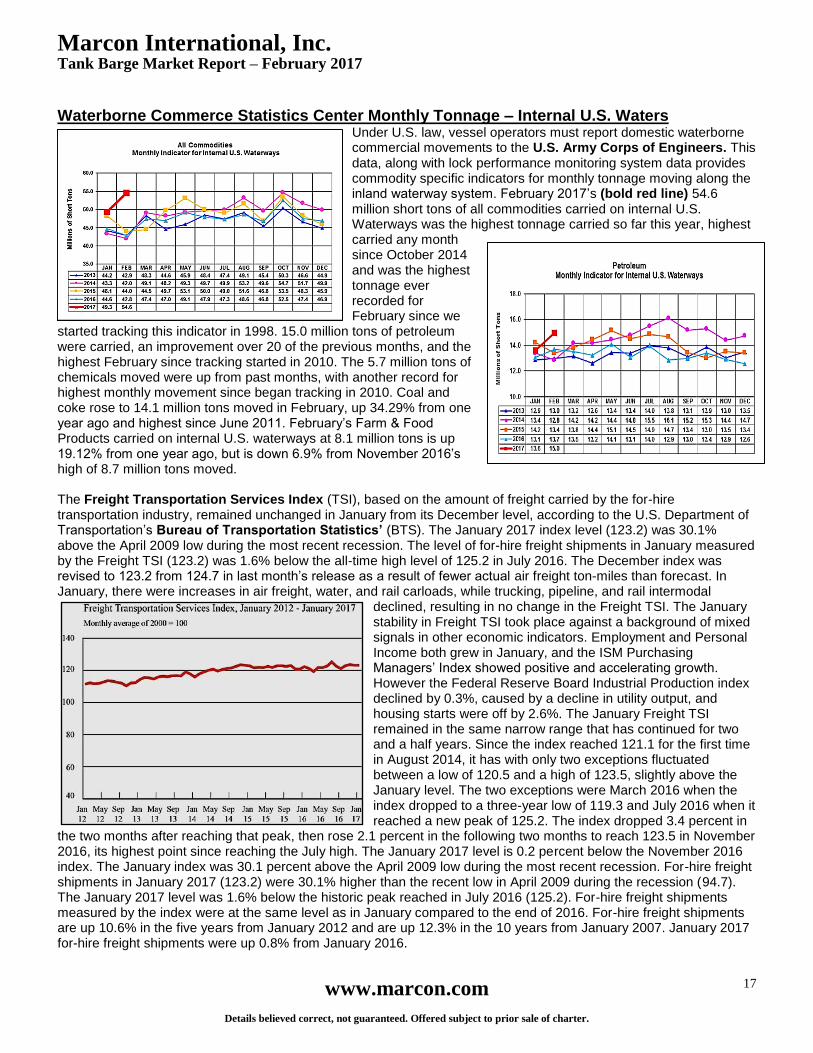

market and represents the price premium of Brent over Dubai crude oil. The EFS continues to trade below $2/b and is at the lowest level for this time of year since 2010, settling at $1.50/b on March 2. A low premium of Brent crude oil over Dubai opens up opportunities for Asian refiners to import more North Sea and West African grades, and trade press is reporting an increase in Atlantic basin cargoes headed to Asia. Similarly, the price differential of U.S.-produced Mars crude oil and Dubai/Oman oil also declined over the past few months and contributed to an increase in U.S. crude oil exports to Asia. The Mars-Dubai/Oman differential averaged -$3.25/b in February, less than the February 2016 average of -$1.78/b and settled at -$4.40/b on March 2. Not only are supply reductions increasing the price of the Dubai/Oman benchmark, but recent increases in U.S. Federal Offshore Gulf of Mexico production could also be contributing to a relative decrease in the Mars price. Lower U.S. refinery runs during maintenance season are also reducing domestic crude oil demand in the first quarter of 2017 and freeing up more oil for export. The wide price differential is opening up opportunities for U.S. crude oil producers to export to Asia. Initial weekly estimates based on EIA’s Weekly Petroleum Status Report indicate that U.S. crude oil exports reached a record high of 0.9 million b/d for the four weeks ending February 24. Per the EIA, U.S. monthly average regular gasoline retail prices are expected to increase from $2.30/gallon (gal) in February 2017 to $2.51/gal in July before falling to $2.24/gal by December. U.S. regular gasoline retail prices are forecast to average $2.40/gal in 2017 and $2.44/gal in 2018. The front-month futures price of reformulated blendstock for oxygenate blending (RBOB, the petroleum component of gasoline used in many parts of the country) rose by 6 cents per gallon (gal) from February 1 to settle at $1.64/gal on March 2. The increase largely reflected the rollover of the front-month RBOB futures contract from March to April delivery, which represents a change from winter grade gasoline to the more expensive summer grade gasoline. The RBOB-Brent crack spread (the difference between the price of RBOB and the price of Brent crude oil) rose by 11 cents/gal over the same period. Prior to the contract roll, both gasoline prices and the RBOB-Brent crack spread declined in the month of February because of high gasoline inventory levels. Gasoline inventories hit a record high in February in the Petroleum Administration for Defense District (PADD) 1B, which includes the New York Harbor delivery hub of the RBOB futures contract. High inventories in PADD 1B contributed to gasoline prices in New York Harbor trading at near parity to gasoline prices on the U.S. Gulf Coast in February. New York Harbor has typically traded at a higher premium to the U.S. Gulf Coast in prior years during February. Trade press reported that more gasoline was scheduled to be exported out of New York Harbor in February than is typical for that time of year.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

17

Waterborne Commerce Statistics Center Monthly Tonnage – Internal U.S. Waters

Under U.S. law, vessel operators must report domestic waterborne commercial movements to the U.S. Army Corps of Engineers. This data, along with lock performance monitoring system data provides commodity specific indicators for monthly tonnage moving along the inland waterway system. February 2017’s (bold red line) 54.6 million short tons of all commodities carried on internal U.S. Waterways was the highest tonnage carried so far this year, highest carried any month since October 2014 and was the highest tonnage ever recorded for February since we

started tracking this indicator in 1998. 15.0 million tons of petroleum were carried, an improvement over 20 of the previous months, and the highest February since tracking started in 2010. The 5.7 million tons of chemicals moved were up from past months, with another record for highest monthly movement since began tracking in 2010. Coal and coke rose to 14.1 million tons moved in February, up 34.29% from one year ago and highest since June 2011. February’s Farm & Food Products carried on internal U.S. waterways at 8.1 million tons is up 19.12% from one year ago, but is down 6.9% from November 2016’s high of 8.7 million tons moved. The Freight Transportation Services Index (TSI), based on the amount of freight carried by the for-hire transportation industry, remained unchanged in January from its December level, according to the U.S. Department of Transportation’s Bureau of Transportation Statistics’ (BTS). The January 2017 index level (123.2) was 30.1% above the April 2009 low during the most recent recession. The level of for-hire freight shipments in January measured by the Freight TSI (123.2) was 1.6% below the all-time high level of 125.2 in July 2016. The December index was revised to 123.2 from 124.7 in last month’s release as a result of fewer actual air freight ton-miles than forecast. In January, there were increases in air freight, water, and rail carloads, while trucking, pipeline, and rail intermodal

declined, resulting in no change in the Freight TSI. The January stability in Freight TSI took place against a background of mixed signals in other economic indicators. Employment and Personal Income both grew in January, and the ISM Purchasing Managers’ Index showed positive and accelerating growth. However the Federal Reserve Board Industrial Production index declined by 0.3%, caused by a decline in utility output, and housing starts were off by 2.6%. The January Freight TSI remained in the same narrow range that has continued for two and a half years. Since the index reached 121.1 for the first time in August 2014, it has with only two exceptions fluctuated between a low of 120.5 and a high of 123.5, slightly above the January level. The two exceptions were March 2016 when the index dropped to a three-year low of 119.3 and July 2016 when it reached a new peak of 125.2. The index dropped 3.4 percent in

the two months after reaching that peak, then rose 2.1 percent in the following two months to reach 123.5 in November 2016, its highest point since reaching the July high. The January 2017 level is 0.2 percent below the November 2016 index. The January index was 30.1 percent above the April 2009 low during the most recent recession. For-hire freight shipments in January 2017 (123.2) were 30.1% higher than the recent low in April 2009 during the recession (94.7). The January 2017 level was 1.6% below the historic peak reached in July 2016 (125.2). For-hire freight shipments measured by the index were at the same level as in January compared to the end of 2016. For-hire freight shipments are up 10.6% in the five years from January 2012 and are up 12.3% in the 10 years from January 2007. January 2017 for-hire freight shipments were up 0.8% from January 2016.

Marcon International, Inc. Tank Barge Market Report – February 2017

www.marcon.com

Details believed correct, not guaranteed. Offered subject to prior sale of charter.

18

St. Lawrence Seaway total traffic for 2016 was 36,250 thousand tonnes, down 3.42% from 2015. Only all grain and liquid bulk commodity groups ended the year on a positive note. All grain was up 3.75% from 10,859 thousand tonnes to 11,266 thousand tonnes. Liquid bulk cargoes were up 18.87% from 3,100 thousand tonnes to 3,685 thousand tonnes. Iron ore had the largest decline of 13.20% down to 6,233 from 7.181 in 2015. Coal and dry bulk each decreased just under 10%, with coal down 9.97% and dry bulk down 9.86%. General cargo had a slight decline of 1.91% for the year. Total vessel transits followed this trend, by being down by 7 transits, or 0.19% over the same time period. After opening the 2016 season on March 21, the St. Lawrence Seaway closed on December 31, enjoying a navigation season of 286 days. This performance ties the record first established in 2008 and matched in 2013 for the longest navigation season.

Lake Carriers’ Association represents U.S.-flag vessel operators on the Great Lakes. U.S.-flag Great Lakes freighters (lakers) moved 2.1 million tons of dry-bulk cargo in January, a decrease of 125,000 tons compared to a year ago. This January’s float was, however, down nearly a quarter from the month’s 5-year average. Iron ore cargos for steel production

increased by 120,000 tons, but coal cargos, mostly for power generation, dipped by 17,000 tons . No limestone was loaded in January. Lake Carriers’ Association represents 13 American companies operating 49 U.S.-flag vessels on the Lakes and carry the raw materials that drive the nation’s economy: iron ore and fluxstone for the steel industry, aggregate and cement for construction, coal for power generation, as well as salt, sand and grain. Collectively, these vessels can transport more than 100 million tons of cargo per year. Per the Association of American Railroads (AAR), carload traffic in February totaled 1,044,040 carloads, up 6.7 percent or 65,141 carloads from February 2016. U.S. railroads also originated 1,068,439 containers and trailers in February 2017, up 1.8 percent or 19,350 units from the same month last year. For February 2017, combined U.S. carload and intermodal originations were 2,112,479, up 4.2 percent or 84,491 carloads and intermodal units from February 2016. In February 2017, 11 of the 20 carload commodity categories tracked by the AAR each month saw carload gains compared with February 2016. These included: coal, up 19.2 percent or 57,589 carloads; crushed stone, gravel, and sand, up 13.1 percent or 10,091 carloads; and primary metal products, up 6.8 percent or 2,357 carloads. Commodities that saw declines in February 2017 from February 2016 included: petroleum and petroleum products, down 12.4 percent or 5,543 carloads; motor vehicles and parts, down 4.8 percent or 3,746; carloads and metallic ores, down 19.1 percent or 2,793 carloads. Excluding coal, carloads were up 1.1 percent or 7,552 carloads in February 2017 from February 2016. Total U.S. carload traffic for the