Marcio Do Nascimento Magalhaes

32

Local Content Poli cy and Opportunities for O&G Industry

Transcript of Marcio Do Nascimento Magalhaes

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 1/32

Local Content Policy andOpportunities for O&G Industry

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 2/32

DISCLAIMER

The presentation may contain forward-looking statements aboutfuture events within the meaning of Section 27A of the Securities Actof 1933, as amended, and Section 21E of the Securities Exchange Actof 1934, as amended, that are not based on historical facts and arenot assurances of future results. Such forward-looking statementsmerely reflect the Company’s current views and estimates of futureeconomic circumstances, industry conditions, company

performance and financial results. Such terms as "anticipate","believe", "expect", "forecast", "intend", "plan", "project", "seek","should", along with similar or analogous expressions, are used toidentify such fo rward-looking statements. Readers are cautioned thatthese statements are only projections and may differ materially fromactual future results or events. Readers are referred to thedocuments filed by the Company with the SEC, specifically theCompany’s most recent Annual Report on Form 20-F, which identifyimportant risk factors that could cause actual results to differ fromthose contained in the forward-looking statements, including, amongother things, risks relating to general economic and businessconditions, including crude oil and other commodity prices, refiningmargins and prevailing exchange rates, uncertainties inherent inmaking estimates of our oil and gas reserves including recentlydiscovered oil and gas reserves, international and Brazilian poli tical,economic and social developments, receipt of governmentalapprovals and licenses and our ability to obtain financing.

We undertake no obligation to publicly update or revise anyforward-looking statements, whether as a result of newinformation or future events or for any other reason. Figuresfor 2012 on are estimates or targets.

All forward-looking statements are expressly qualified in

their entirety by this cautionary statement, and you shouldnot place reliance on any forward-looking statementcontained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil andgas resources, that we are not permitted to present indocuments filed with the United States Securities andExchange Commission (SEC) under new Subpart 1200 toRegulation S-K because such terms do not qualify as proved,probable or possible reserves under Rule 4-10(a) ofRegulation S-X.

FORWARD-LOOKING STATEMENTS

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 3/32

PRESENTATION SUMARY

1. PETROBRAS’ Business & Management Plan 2013 – 202. Supply History

3. Local Content Policy4. Supply Chain Challenges5. Foreign Investment in Brazil: Oil and Gas Industry6. Conclusions

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 4/32

1 –PETROBRAS’Business and

Management Plan 2013 –

2017

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 5/32

PETROBRAS TODAYFully integrated across the hydrocarbon chain

• 2.4 mm boedproduction

• 293 producti on fields

• 96% of Brazilianproduction

• 34% of global DW andUDW product ion

Explorationand Production

• 12 refineries (Brazil)

• 2.0 mm bpd refini ngcapacity

• Oil products sales inBrazil: 2,285 Kbpd

• Oil products output inBrazil:1,997 Kbpd

Downstream

• 7,641 service s tations

• 38,1% of market s hare

• 20% share of servicestations

Distribution

• 9,190 km of gaspipelines in Brazil

• NG Supply: 74.9million m³/d

• 3 LNG Regasificationterminals by 2013 with41 MMm³/d capacity

• 7,028 MW ofgeneration capacity

Gas and Power

• 24 countries

• 0.7 Bn bo e of 1P (SPE)

• 243 th. boedproduction

• 231 th. bpd refiningcapacity

International

• 3 Biodiesel Plants

• Ethanol: opening newmarkets

• Largest domesticproducer of biodiesel

• 3rd producer of ethanolin Brazil

Biofuels

(1) Adjusted according average exchange rate. Excludes Corporate and Elimination .

2012 Proven Reserves (SPE Criteria) - Brazil

Deep Water(300-1,500m)

48%

Ultra-Deep Water(> 1,500m)

36%

Onshore8%

Shallow Water(0-300m)

8%

15.73 Billion boe

2012 Proven Reserves (SPE Criteria) - Brazil

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 6/32

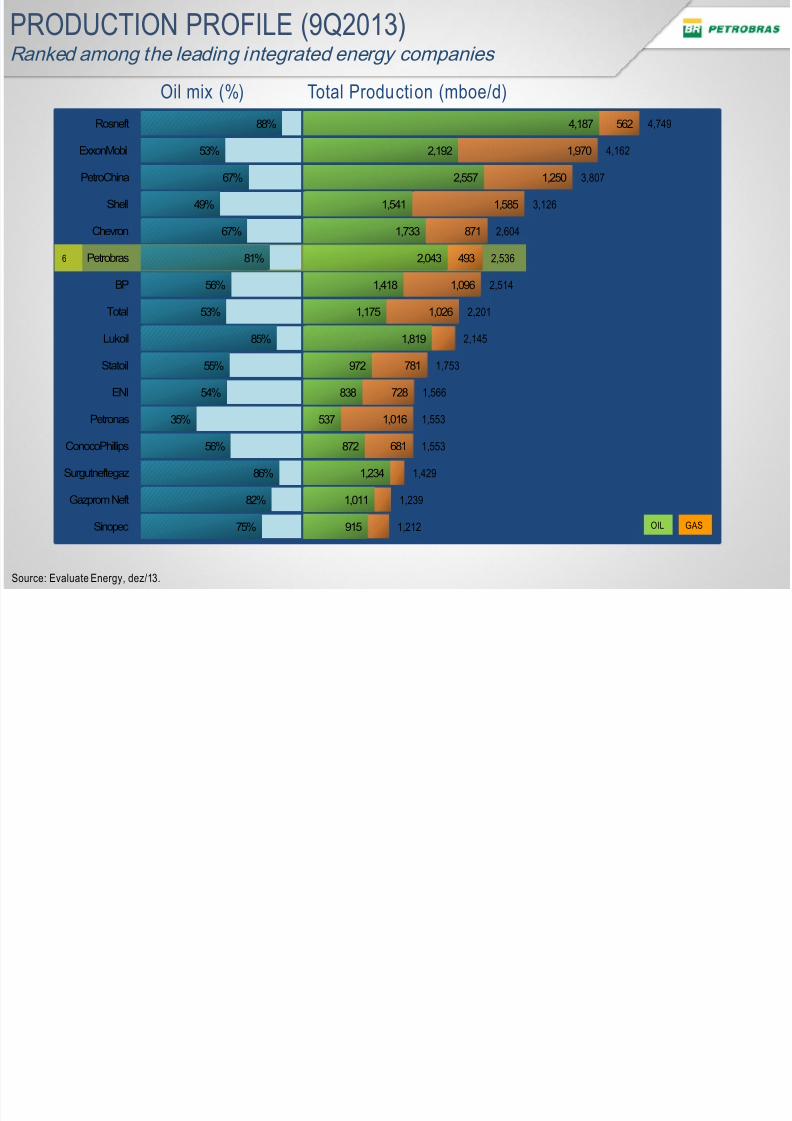

PRODUCTION PROFILE (9Q2013)Ranked among the leading integrated energy companies

Oil mix (%) Total Production (mboe/d)4,187

2,192

2,557

1,541

1,733

2,043

1,418

1,175

1,819

972

838

537

872

1,234

1,011

915

562

1,970

1,250

1,585

871

493

1,096

1,026

781

728

1,016

681

4,749

4,162

3,807

3,126

2,604

2,536

2,514

2,201

2,145

1,753

1,566

1,553

1,553

1,429

1,239

1,212

88%

53%

67%

49%

67%

81%

56%

53%

85%

55%

54%

35%

56%

86%

82%

75%

Rosneft

ExxonMobil

PetroChina

Shell

Chevron

Petrobras

BP

Total

Lukoil

Statoil

ENI

Petronas

ConocoPhillips

Surgutneftegaz

Gazprom Neft

Sinopec

6

Source: Evaluate Energy, dez/13.

OIL GAS

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 7/32

Under Implementation

US$ 207.1 Billion

Under Evaluation

US$ 29.6 Billion

+=Total

US$ 236.7 Billion

All E&P projects in Brazil and projects of the

remaining segments in phase IV

Projects for the remaining segments,

excluding E&P, currently in phase I, II and

770 projects 177 projec ts947 projects

62.3%(US$ 147.5 Billio n) 27.4%

(US$ 64.8 Billio n)

1.0%(US$ 2.3 Billio n)

1.4%(US$ 3.2 Billio n)

1.1%(US$ 2.9 Billio n)

2.2%(US$ 5.1 Billi on)

4.2%(US$ 9.9 Billio n)

0.4%(US$ 1.0 Billio n)

71.2%(US$ 147.5 Billio n) 20.9%

(US$ 43.2 Billio n)

1.1%(US$ 2.3 Billio n)

1.4%(US$ 2.9 Billi on)

0.5%(US$ 1.1 Billio n)

1.5%(US$ 3.2 Billio n)

2.9%(US$ 5.9 Billi on)

0.5%(US$ 1.0 Bilil on)

73.0%(US$ 21.6 Billio n)

1.0%(US$ 0.3 Billi on)

13.5%(US$ 4.0 Billi on)

6.4%(US$ 1.9 Billio n)

6.1%(US$ 1.8 Billio n)

Phase I: Opportunity Identification; Phase II: Conceptual Project; Phase III: Basic Project ; Phase IV: Execution

* Pbio = Petrobras Biofuel│ETM = Engineering, Technology and Materials │Other Areas = Financial, Strategy and Corporate

International ETM* Other Areas*Pbio*E&P DistribuitionDownstream G&E

2013 – 2017 BMP INVESTMENTSProjects Under Implementation x Under Evaluation

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 8/32

Production Development

US$ 106.9 Billion

Post-SaltPre-SaltTransfer of Rights

Exploration

US$ 24.3 Billion

16%(24.3)

73%11%

Infrastructure and SupportExplorationProduction Development

2013 – 2017 Period

US$ 147.5 Bill ion

11%

70%24%

6%

32%

43%

25%

Aside from Exploration and Production Development, E&P infrastructure investments total US$ 16.3 Billion.

E&P INVESTMENTS

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 9/32

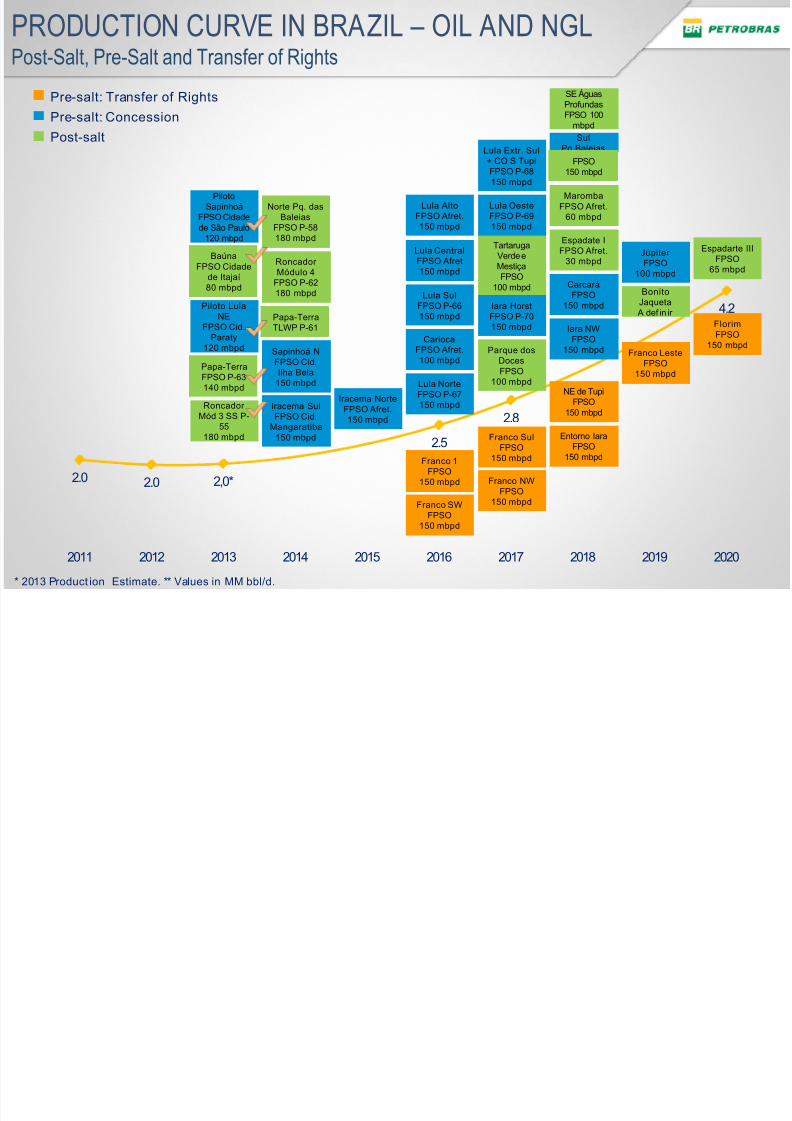

PRODUCTION CURVE IN BRAZIL – OIL AND NGLPost-Salt, Pre-Salt and Transfer of Rights

2.0 2.0 2,0*

2.5

2.8

4.2

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Norte Pq. dasBaleias

FPSO P-58180 mbpd

RoncadorMód 3 SS P-

55180 mbpd

Piloto LulaNE

FPSO Cid.Paraty

120 mbpd

PilotoSapinhoá

FPSO Cidadede São Paulo

120 mbpdJúpiterFPSO

100 mbpd

Franco LesteFPSO

150 mbpd

BonitoJaqueta

A def in ir

Espadarte IIIFPSO

65 mbpd

FlorimFPSO

150 mbpd

RoncadorMódulo 4

FPSO P-62180 mbpd

Sapinhoá NFPSO Cid.Ilha Bela

150 mbpd

Iracema SulFPSO Cid.

Mangaratiba150 mbpd

Iracema NorteFPSO Afret.150 mbpd

Lula NorteFPSO P-67150 mbpd

Franco SWFPSO

150 mbpd

Lula SulFPSO P-66150 mbpd

Franco 1FPSO

150 mbpd

CariocaFPSO Afret.100 mbpd

Lula CentralFPSO Afret150 mbpd

Lula AltoFPSO Afret.150 mbpd

TartarugaVerde eMestiça

FPSO100 mbpd

Lula Extr. Sul+ CO S TupiFPSO P-68150 mbpd

Iara HorstFPSO P-70150 mbpd

Lula OesteFPSO P-69150 mbpd

Franco SulFPSO

150 mbpd

Franco NWFPSO

150 mbpd

Parque dosDocesFPSO

100 mbpd

Espadate IFPSO Afret.

30 mbpd

CarcaráFPSO

150 mbpd

NE de TupiFPSO

150 mbpd

Entorno IaraFPSO

150 mbpd

MarombaFPSO Afret.

60 mbpd

Iara NWFPSO

150 mbpd

SE ÁguasProfundasFPSO 100

mbpd

SulPq.BaleiasFPSO

150 mbpd

Papa-TerraFPSO P-63140 mbpd

BaúnaFPSO Cidade

de Itajaí80 mbpd

Papa-TerraTLWP P-61

Pre-salt: Concession

Post-salt

Pre-salt: Transfer of Rights

* 2013 Product ion Estimate. ** Values in MM bbl/d.

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 10/32

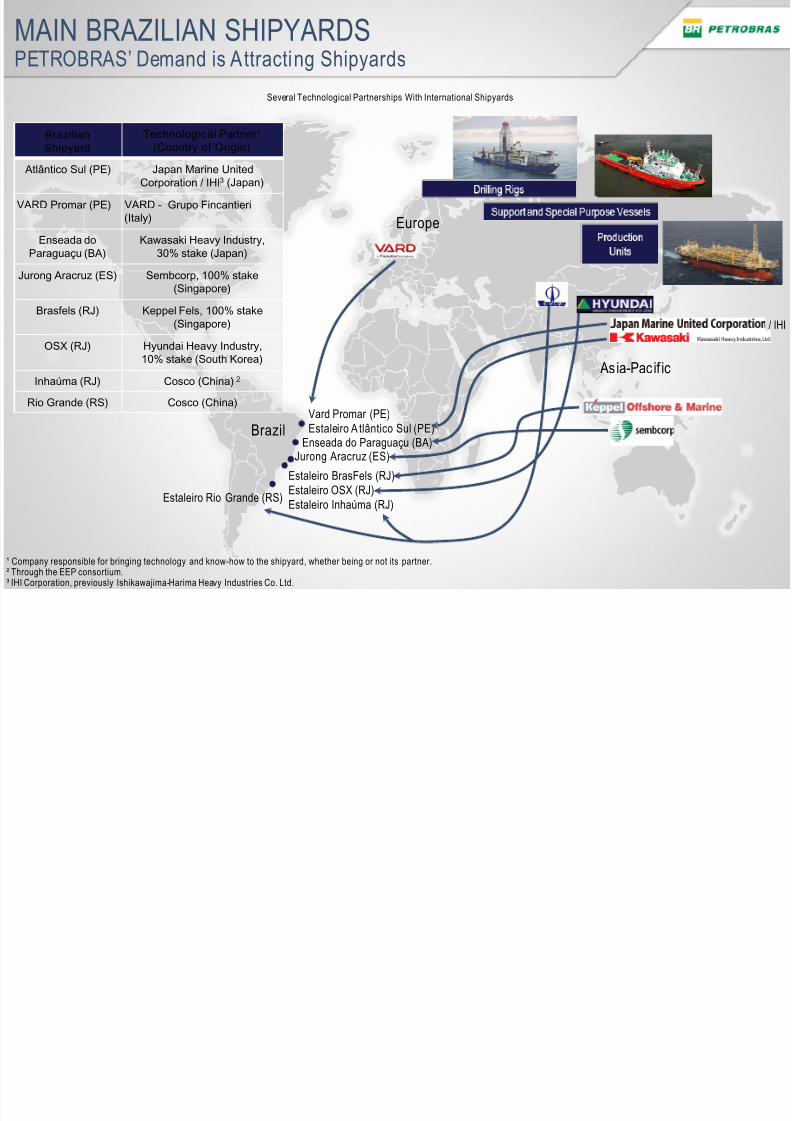

BrazilVard Promar (PE)Estaleiro Atlântico Sul (PE)

Estaleiro BrasFels (RJ)Estaleiro OSX (RJ)Estaleiro Inhaúma (RJ)

Enseada do Paraguaçu (BA)Jurong Aracruz (ES)

Estaleiro Rio Grande (RS)

Europe

Asia-Pacific

BrazilianShipyard Technological Partner¹(Country of Origin)

Atlântico Sul (PE) Japan Marine UnitedCorporation / IHI 3 (Japan)

VARD Promar (PE) VARD - Grupo Fincantieri(Italy)

Enseada doParaguaçu (BA)

Kawasaki Heavy Industry,30% stake (Japan)

Jurong Aracruz (ES) Sembcorp, 100% stake(Singapore)

Brasfels (RJ) Keppel Fels, 100% stake(Singapore)

OSX (RJ) Hyundai Heavy Industry,10% stake (South Korea)

Inhaúma (RJ) Cosco (China) 2

Rio Grande (RS) Cosco (China)

/ IHI

¹ Company responsible for bringing technology and know-how to the shipyard, whether being or not its partner.² Through the EEP consortium.³ IHI Corporation, previously Ishikawajima-Harima Heavy Industries Co. Ltd.

MAIN BRAZILIAN SHIPYARDSPETROBRAS’ Demand is Attracting Shipyards

Several Technological Partnerships With International Shipyards

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 11/32

BrasFels Shipyard – RJ

1

23

Overview of Estaleiro BrasFels in A ngra do s Reis - RJ (31/08/12).

(1) P-61 (CL:65%): HULL'S Constructio n of TOPSIDE's TLWP and integr ation (deckbo xand built mo dules in Singapore).(2) São Paulo Ci ty FPSO (CL: 65%): HULL's Conversion in China and integrati on of t he 16 mod., Built in Brasf els (5 mod), Enaval (1 mod), Thailand (8 mod) and Chi(3) Par at y Ci ty FPSO (CL: 65%): HULL's Conversio n in Sing apore and in tegration of 15 mod ules buil t in t he Brasfels (5), Nuclep (4), Enaval (2), and Singap ore (4).

• 1 Hull Constructions (P-61)

• 5 Building Modules, Topside andIntegration (São Paulo, Mangaratiba,Itaguaí, P-66, P-69) and P-61 (onlyintegration)

• 6 Drilling Rigs

FPSO Cid. Paraty:

Producing since Jun6 th , 2013

FPSO Cid. São Paulo:Producing since Jan

5 th , 2013

P-61

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 12/32

FPSO Cid. Itajaí:Producing since Feb.

2nd , 2013

JURONG Shipyard (Singapore)

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 13/32

Honório Bicalho Shipyard – RS

P-63: Producingsince Nov 11 th , 2013

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 14/32

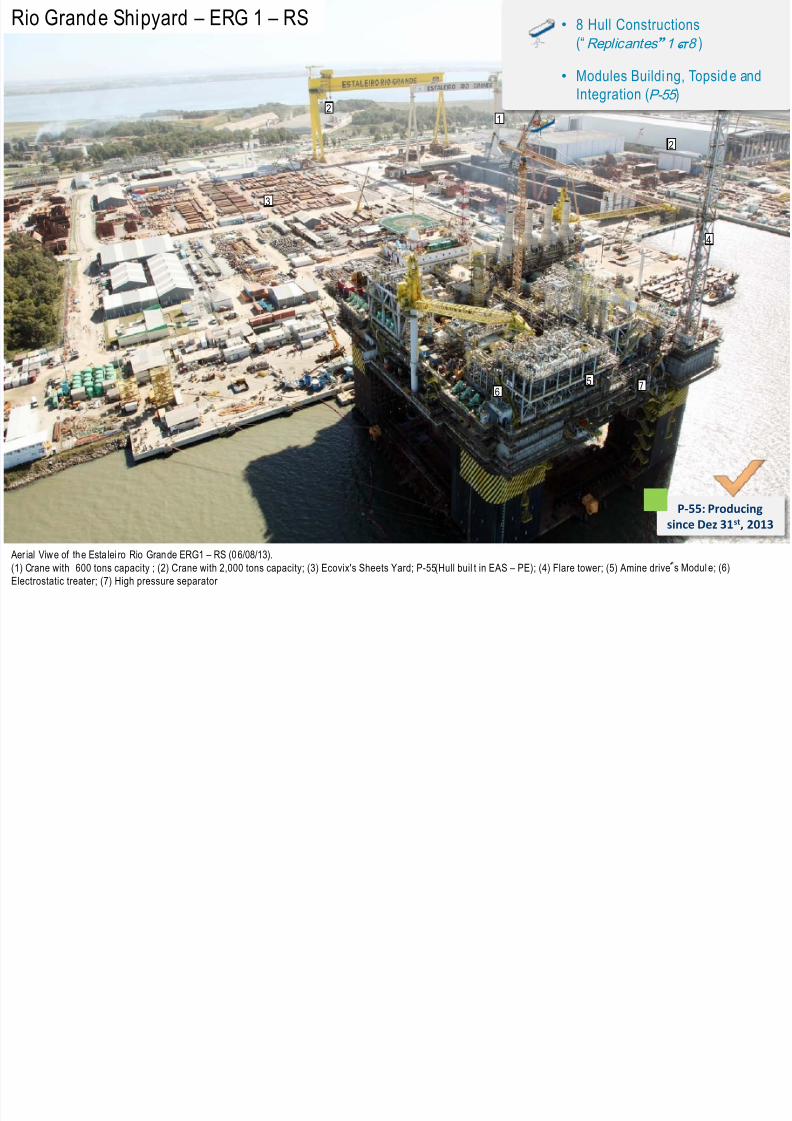

Rio Grande Shipyard – ERG 1 – RS

Aerial Viwe of the Estalei ro Rio Grande ERG1 – RS (06/08/13).(1) Crane with 600 tons capacity ; (2) Crane with 2,000 tons capacity; (3) Ecovix's Sheets Yard; P-55 (Hull buil t in EAS – PE); (4) Flare tower; (5) Amine drive

s Modul e; (6)Electrostatic treater; (7) High pressure separator

12

3

4

56 7

P-55: Producingsince Dez 31 st , 2013

2

• 8 Hull Constructions(“Replicantes” 1 – 8 )

• Modules Building, Topside andIntegration (P-55 )

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 15/32

PRE-SALT PRODUCTION IS A REALITYProduction reached 390 thousand barrels of oil per day in Jan/14/2014

Pre-Salt ProductionOil Production record of 390 kbpd in

January, 14 th 2014

Production of 1 MMbpd operated byPetrobras will be reached by 2017 and2.1 MMbpd by 2020.

Lula Pilot production growth per well:from 15 Kbpd (Proj. approval by

Ago/2008) to 25 Kbpd

TechnologicalChallenges High Resolution Seismic: higherexploratory success

Geological and numerical modelling:better production behavior forecast

Reduction of well construction timefrom 134 days in 2006 to 70 day in2012: lower costs

Selection of new materials: lowercosts

Qualification of new systems forproduction gathering: highercompetitiveness

Separation of CO2 from natural gas indeep waters and reinjection: loweremissions and increase in recoveryfactor

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 16/32

2 – Supply History

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 17/32

1950 1960

Contracting of goods andservices abroad.

1970 1980

Substitution of importing, similaritylaw, nationalization, “reverse

engineering”, local market protection,contracts in Brazil.

2002

1990 2000

2003

Opening of the market to importing,globalization, international bids.Focus on competitiveness. R&D inBrazil and abroad.

Focus on the Brazilian industry.Increase of the Local Content in thegoods and services contracting(competitiveness and technological adherence).

Most of the equipmentand materials

are acquired abroad

Substitution of importedequipment and materials

Opening of theBrazilian market for

importing

HISTORY

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 18/32

3 – Local ContentPolicy

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 19/32

LOCAL CONTENT

PETROBRAS LOCAL CONTENT POLICY

The projects and contracts for PETROBRAS

must withstand the challenges of the StrategicPlan and maximize Local Content in competitiveand sustainable basis, accelerating thedevelopment of the markets where it operates

and guided by the ethics and continuedinnovation.

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 20/32

E&PExploração e

Desenvolvimento:comprovações para

ANP para novoscontratos de

concessão, partilha ecessão onerosa

AbastNão existe exigênciade Conteúdo Local.Operadora declarameta e comprovaíndice realizado

G&ENão existe exigênciade Conteúdo Local.Operadora declarameta e comprovaíndice realizado

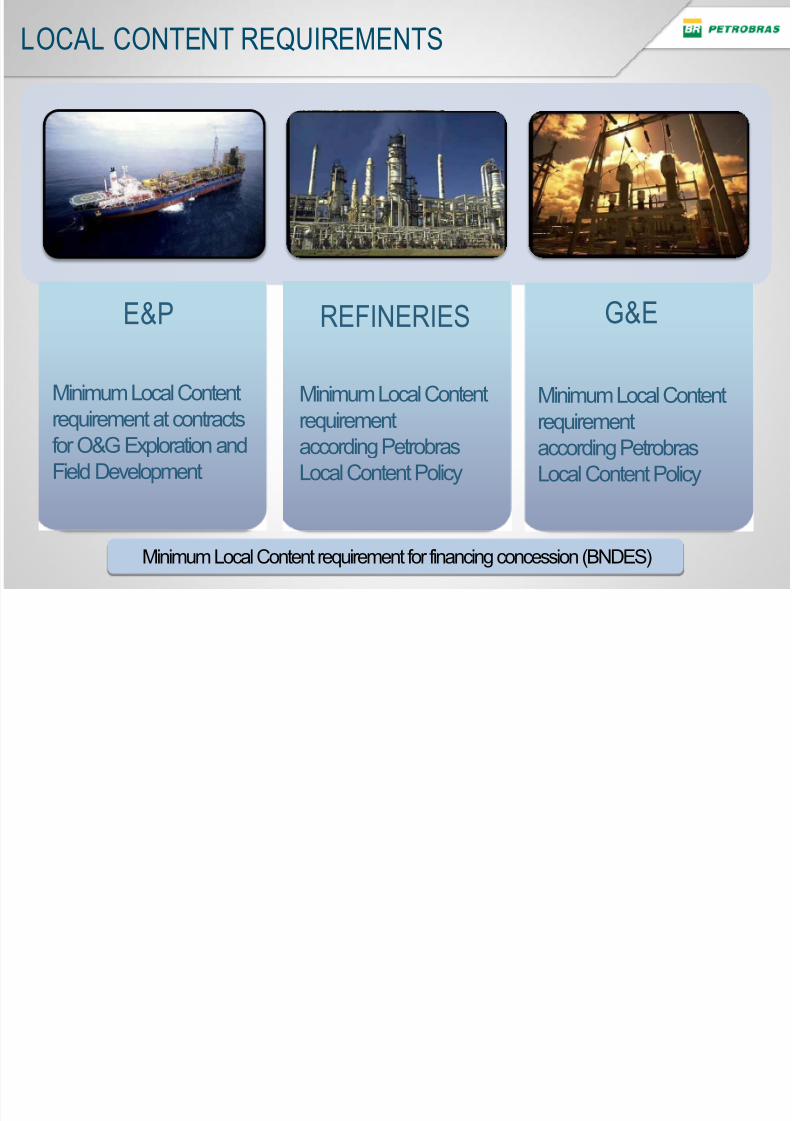

LOCAL CONTENT REQUIREMENTS

Minimum Local Contentrequirement at contractsfor O&G Exploration andField Development

E&P REFINERIES G&E

Minimum Local Contentrequirementaccording PetrobrasLocal Content Policy

Minimum Local Contentrequirementaccording PetrobrasLocal Content Policy

Minimum Local Content requirement for financing concession (BNDES)

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 21/32

For the Country For the Oil Companies

Local Economy Diversification

Sustainable Economic Growth

Increase Country s Attractiveness for Investors

Local Productive CapacityDevelopment

Proximity between Suppliers andthe Operation

Reduced Dependence onExpatriated Workforce

Suppliers Innovation CapacityIncreased

Logistic Risks Reduction

Operating Costs ReductionEmployment and Income Generation

Local Technical Assistance Availabil ityTax Revenue Increase

Local Content

WHY LOCAL CONTENT? Advantage and Facilities to Oil Industry in Brazil

Potential Gains

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 22/32

RESEARCH & DEVELOPMENTEstablishing research centers enhances long term future of Brazil as hub

Companies with R&D centers in operation, construction or plans for Brazil:

• Schlumberger

• Baker Hughes

• FMC Technologies

• Halliburton

• General Electric

• Vallourec

• Usiminas

• TenarisConfab

• Cameron

• IBM

• Technip

• Weatherford

• Wellstream

PETROBRAS’ partnerships with more than 120 universities and research centers have led Brazil to have a prominent worldwide applresearch complex

Technological Park

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 23/32

HOW TO MEASURE LOCAL CONTENT (LC)

+ +=BODY

PLUG & SEATINGBONNET

VALVE

90%=

Local ContentCertificate * L

o c a

l C o n

t e n

t A c c o u n

t i n g

P r o c e

d u r e s a s

A N P R e s o

l u t i o n

1 9 / 2 0 1 3

.

£10

£100NET TOTAL SYSTEM PRICE

(NET OF TAXES)

1 X 100CL (%) =

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 24/32

‘Brazilian companies’ means companies thathave manufacturing processes and after-sales

services in Brazil, thus creating jobs and

collecting taxes in the country.

BRAZILIAN COMPANIES

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 25/32

25

4 – Supply ChainChallenges

<nº>/nº

SUBSEA AND DRILLING EQUIPMENT

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 26/32

SUBSEA AND DRILLING EQUIPMENTChallenges & Investments

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 27/32

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 28/32

5 – Foreign Investment Brazil: Oil and Ga

Industry

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 29/32

PETROBRAS’Partners

Brazilian Trade and Investment Promotion Agencyhttp://www2.apexbrasil.com.br/en/invest-in-brazil/apex-brasil-services-to-help-you

APEX Brazil

FOREIGN INVESTMENT IN BRAZIL: O&G INDUSTRY

ONIPNational Organization of the Petroleum Industryhttp://www.onip.org.br/areas-of-activity/?lang=en

Foreign Companies Support in BrazilEmbassies, Consulates, Chambers of Commerce, etc.

Legal Guide for Foreign Investors in BrazilMinistry of External Relations

http://www.brasilglobalnet.gov.br/arquivos/publicacoes/manuais/pubguialegali.pdf

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 30/32

6 – Conclusions

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 31/32

PETROBRAS has a robust projects’ portfolio, which is atypical in the current globaleconomic situation;There are huge opportunities for already installed companies and newcomers in theBrazilian market of suppliers, services and engineering due to the scale provided bythe project portfolio;The Challenges to put Pre-Salt fields into operation are known and the Subsea

Equipment Industry plays a key role considering the demands;Local Content is a consolidated practice for E&P Projects;The association between Brazilian and foreign manufacturers is the best approachas to provide the solutions for technological bottlenecks.

CONCLUSIONS

<nº>/nº

8/13/2019 Marcio Do Nascimento Magalhaes

http://slidepdf.com/reader/full/marcio-do-nascimento-magalhaes 32/32

Thank you!