March 21, 2016 - SKP · PDF fileMarch 21, 2016 Cera Sanitaryware Ltd. ... CERA is now...

20

March 21, 2016 Cera Sanitaryware Ltd. ...margin expansion fuelled with better product mix CMP INR 1772 Target INR 2515 (Re)Initiating Coverage - BUY SKP Securities Ltd www.skpmoneywise.com Page 1 of 20 Company Background Cera Sanitaryware Ltd. (CERA), promoted by Mr. Vikram Somany, is India’s third largest player in sanitaryware products, with organised market share of ~23%, after HSIL (~40%) and Parryware Roca (~30%). It also manufacturer’s faucets and has presence in tiles. It is now putting up its first tile manufacturing facility under JV with Andhara Pradesh based Anjani Tiles Ltd. Investment Rationale Top-line expected to grow at a CAGR of ~17% over FY15-18E The faucet segment reported robust growth with a CAGR of 42% during FY12-15 with the capacity utilization (CU) of ~60%. With ample capacity in hand and ‘asset light model in place’ we expect the segment to grow with a CAGR of 37% during FY15-FY18E with higher CU. Tiles segment grew by 23% y-o-y to Rs 686.4 mn and contributed 8% to total revenue, during FY15. Contribution from tiles rose to 13% during 9MFY16. We expect tiles segment to grow with a CAGR of 65% during FY15-FY18E with own production capacity coming up now as mentioned below. On the backdrop of strong brand equity and distribution network, growing demand due to changing consumer preferences towards premium lifestyle products and increasing disposable income, we expect CERA’s net sales to grow at a CAGR of ~17% during FY15-FY18E to Rs 13,253.2 mn. Margins expected to improve with better operating leverage EBIDTA Margins of the company was under pressure from FY11 to FY15 where in it reduced from 18.9% to 14.3%. Margins improved to 15.3% during Q3FY16 due to lower energy cost and price increase by the company in the sanitaryware segment, by 2-7% during the quarter. Going forward, we expect EBIDTA margins to stabilize at ~15.5% by FY18E on the back of better product mix, in-house tiles manufacturing including more premium products. PAT margin was up by 40 bps to 8.2% in FY15 from 7.8% reported in FY14 which further improved to 8.6 % during Q3FY16. With improvement in segment margins & better operating leverage coupled with low debt levels, we expect PAT margins to improve further to ~9.1% respectively by FY18E. Also, CERA’s focus on enhancing capacities through asset light model not only reduces its capital investments but also de-risks the balance sheet, enhances return ratios and provides faster access to capacities thereby, resulting in continuous low D/E, which we expect to further improve in coming years. Venturing into tiles manufacturing through JV There is an increased demand for life style consumption products, especially from aspiring mass affluent. To meet the resultant demand for tiles, and as a product extension strategy to leverage its sales network, CERA is now venturing into manufacturing of tiles through a JV with Andhra Pradesh based Anjani Tiles. CERA holds 51% stake in the project that is estimated to cost around Rs 680 mn, with the Company’s equity share of ~Rs190 mn. The plant will have an initial capacity of 10,000 square meters per day of tile manufacturing which could be scaled up to 3x-4x, going forward. The facility has a potential to generate additional revenue of ~Rs 750-1200 mn at full CU. We expect the plant to get commissioned by Q4FY16. Valuation Government of India’s initiatives like “Housing for All” and “Swachh Bharat Abhiyan” coupled with strong brand equity & distribution network, changing consumer preferences towards premium & lifestyle products and diverse product basket augurs well for CERA. It has de-risked its growth strategy with an asset light business model, adopting an outsourcing and joint venture route. We have valued the stock on P/E basis and recommend a BUY on CERA with a target price of Rs 2515/- in 18 months (42% upside). Key Share Data Face Value (INR) 5.0 Equity Capital (INR mn) 65.0 Market Cap (INR mn) 23,046.4 52 Week High/Low (NSE) (INR) 2,961/1,510 Avg. Daily Volume (BSE) 2,322 BSE Code 532443 NSE Code CERA Reuters Code CERA.NS Bloomberg Code CRS:IN Shareholding Pattern (Dec 31, 2015) 55% 14% 6% 25% Promoters FII DII Public & Others Particulars FY15 FY16E FY17E FY18E Net Sales 8,216.7 9,484.2 11,203.6 13,253.2 Growth (%) 23.8% 15.4% 18.1% 18.3% EBITDA 1,175.3 1,372.0 1,688.0 2,049.8 PAT 676.7 793.8 965.4 1,211.4 Growth (%) 30.4% 17.3% 21.6% 25.5% EPS (INR) 52.0 61.0 74.2 93.1 BVPS (INR) 270.4 324.0 389.2 470.3 Key Financials (INR Million) Particulars FY15 FY16E FY17E FY18E P/E (x) 34.1 29.0 23.9 19.0 P/BVPS (x) 6.6 5.5 4.6 3.8 Mcap/Sales (x) 2.8 2.4 2.1 1.7 EV/EBITDA (x) 19.9 16.9 13.8 11.1 ROCE (%) 24.8% 25.3% 26.4% 27.8% ROE (%) 19.2% 18.8% 19.1% 19.8% EBITDA Mar (%) 14.3% 14.5% 15.1% 15.5% PAT Mar (%) 8.2% 8.4% 8.6% 9.1% Debt - Equity (x) 0.2 0.1 0.1 0.1 Key Financials Ratios Source: Company, SKP Research Price Performance CERA vs BSEMIDCAP -40% -30% -20% -10% 0% 10% 20% Mar-15 Apr-15 May-15 May-15 Jun-15 Jul-15 Jul-15 Aug-15 Sep-15 Sep-15 Oct-15 Nov-15 Nov-15 Dec-15 Jan-16 Jan-16 Feb-16 Mar-16 CERA BSE Mid Cap Analysts: Nikhil Saboo Tel No: +91-33-40077019; Mobile: +91-9330186643 e-mail: [email protected] Vineet Agrawal Tel No: +91-22-49226006; Mobile: +91-9819510575 e-mail: [email protected]

Transcript of March 21, 2016 - SKP · PDF fileMarch 21, 2016 Cera Sanitaryware Ltd. ... CERA is now...

March 21, 2016

Cera Sanitaryware Ltd.

...margin expansion fuelled with better product mix

CMP INR 1772 Target INR 2515 (Re)Initiating Coverage - BUY

SKP Securities Ltd www.skpmoneywise.com Page 1 of 20

Company Background

Cera Sanitaryware Ltd. (CERA), promoted by Mr. Vikram Somany, is India’s third largest player in sanitaryware products, with organised market share of ~23%, after HSIL (~40%) and Parryware Roca (~30%). It also manufacturer’s faucets and has presence in tiles. It is now putting up its first tile manufacturing facility under JV with Andhara Pradesh based Anjani Tiles Ltd.

Investment Rationale

Top-line expected to grow at a CAGR of ~17% over FY15-18E The faucet segment reported robust growth with a CAGR of 42% during

FY12-15 with the capacity utilization (CU) of ~60%. With ample capacity in hand and ‘asset light model in place’ we expect the segment to grow with a CAGR of 37% during FY15-FY18E with higher CU.

Tiles segment grew by 23% y-o-y to Rs 686.4 mn and contributed 8% to total revenue, during FY15. Contribution from tiles rose to 13% during 9MFY16. We expect tiles segment to grow with a CAGR of 65% during FY15-FY18E with own production capacity coming up now as mentioned below.

On the backdrop of strong brand equity and distribution network, growing demand due to changing consumer preferences towards premium lifestyle products and increasing disposable income, we expect CERA’s net sales to grow at a CAGR of ~17% during FY15-FY18E to Rs 13,253.2 mn.

Margins expected to improve with better operating leverage EBIDTA Margins of the company was under pressure from FY11 to FY15

where in it reduced from 18.9% to 14.3%. Margins improved to 15.3% during Q3FY16 due to lower energy cost and price increase by the company in the sanitaryware segment, by 2-7% during the quarter. Going forward, we expect EBIDTA margins to stabilize at ~15.5% by FY18E on the back of better product mix, in-house tiles manufacturing including more premium products.

PAT margin was up by 40 bps to 8.2% in FY15 from 7.8% reported in FY14 which further improved to 8.6 % during Q3FY16. With improvement in segment margins & better operating leverage coupled with low debt levels, we expect PAT margins to improve further to ~9.1% respectively by FY18E.

Also, CERA’s focus on enhancing capacities through asset light model not only reduces its capital investments but also de-risks the balance sheet, enhances return ratios and provides faster access to capacities thereby, resulting in continuous low D/E, which we expect to further improve in coming years.

Venturing into tiles manufacturing through JV

There is an increased demand for life style consumption products, especially from aspiring mass affluent. To meet the resultant demand for tiles, and as a product extension strategy to leverage its sales network, CERA is now venturing into manufacturing of tiles through a JV with Andhra Pradesh based Anjani Tiles.

CERA holds 51% stake in the project that is estimated to cost around Rs 680 mn, with the Company’s equity share of ~Rs190 mn. The plant will have an initial capacity of 10,000 square meters per day of tile manufacturing which could be scaled up to 3x-4x, going forward.

The facility has a potential to generate additional revenue of ~Rs 750-1200 mn at full CU. We expect the plant to get commissioned by Q4FY16.

Valuation Government of India’s initiatives like “Housing for All” and “Swachh Bharat Abhiyan” coupled with strong brand equity & distribution network, changing consumer preferences towards premium & lifestyle products and diverse product basket augurs well for CERA. It has de-risked its growth strategy with an asset light business model, adopting an outsourcing and joint venture route. We have valued the stock on P/E basis and recommend a BUY on CERA with a target price of Rs 2515/- in 18 months (42% upside).

Key Share Data

Face Value (INR) 5.0

Equity Capital (INR mn) 65.0

Market Cap (INR mn) 23,046.4

52 Week High/Low (NSE) (INR) 2,961/1,510

Avg. Daily Volume (BSE) 2,322

BSE Code 532443

NSE Code CERA

Reuters Code CERA.NS

Bloomberg Code CRS:IN

Shareholding Pattern (Dec 31, 2015)

55%

14%

6%

25%

Promoters

FII

DII

Public & Others

Particulars FY15 FY16E FY17E FY18E

Net Sales 8,216.7 9,484.2 11,203.6 13,253.2

Growth (%) 23.8% 15.4% 18.1% 18.3%

EBITDA 1,175.3 1,372.0 1,688.0 2,049.8

PAT 676.7 793.8 965.4 1,211.4

Growth (%) 30.4% 17.3% 21.6% 25.5%

EPS (INR) 52.0 61.0 74.2 93.1

BVPS (INR) 270.4 324.0 389.2 470.3

Key Financials (INR Million)

Particulars FY15 FY16E FY17E FY18E

P/E (x) 34.1 29.0 23.9 19.0

P/BVPS (x) 6.6 5.5 4.6 3.8

Mcap/Sales (x) 2.8 2.4 2.1 1.7

EV/EBITDA (x) 19.9 16.9 13.8 11.1

ROCE (%) 24.8% 25.3% 26.4% 27.8%

ROE (%) 19.2% 18.8% 19.1% 19.8%

EBITDA Mar (%) 14.3% 14.5% 15.1% 15.5%

PAT Mar (%) 8.2% 8.4% 8.6% 9.1%

Debt - Equity (x) 0.2 0.1 0.1 0.1

Key Financials Ratios

Source: Company, SKP Research

Price Performance CERA vs BSEMIDCAP

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

Mar

-15

Ap

r-1

5

May

-15

May

-15

Jun

-15

Jul-

15

Jul-

15

Au

g-1

5

Sep

-15

Sep

-15

Oct

-15

No

v-1

5

No

v-1

5

Dec

-15

Jan

-16

Jan

-16

Feb

-16

Mar

-16

CERA

BSE Mid Cap

Analysts: Nikhil Saboo

Tel No: +91-33-40077019; Mobile: +91-9330186643

e-mail: [email protected]

Vineet Agrawal

Tel No: +91-22-49226006; Mobile: +91-9819510575

e-mail: [email protected]

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 2 of 20

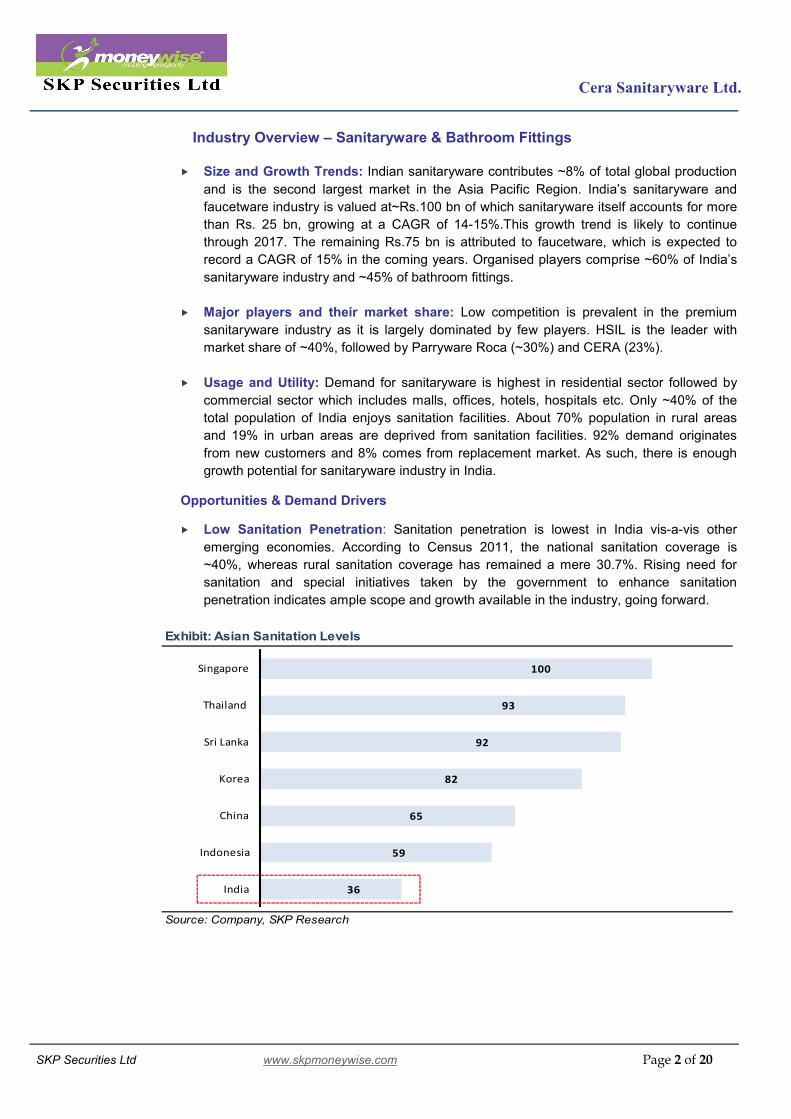

Industry Overview – Sanitaryware & Bathroom Fittings Size and Growth Trends: Indian sanitaryware contributes ~8% of total global production

and is the second largest market in the Asia Pacific Region. India’s sanitaryware and

faucetware industry is valued at~Rs.100 bn of which sanitaryware itself accounts for more

than Rs. 25 bn, growing at a CAGR of 14-15%.This growth trend is likely to continue

through 2017. The remaining Rs.75 bn is attributed to faucetware, which is expected to

record a CAGR of 15% in the coming years. Organised players comprise ~60% of India’s

sanitaryware industry and ~45% of bathroom fittings.

Major players and their market share: Low competition is prevalent in the premium

sanitaryware industry as it is largely dominated by few players. HSIL is the leader with

market share of ~40%, followed by Parryware Roca (~30%) and CERA (23%).

Usage and Utility: Demand for sanitaryware is highest in residential sector followed by

commercial sector which includes malls, offices, hotels, hospitals etc. Only ~40% of the

total population of India enjoys sanitation facilities. About 70% population in rural areas

and 19% in urban areas are deprived from sanitation facilities. 92% demand originates

from new customers and 8% comes from replacement market. As such, there is enough

growth potential for sanitaryware industry in India. Opportunities & Demand Drivers Low Sanitation Penetration: Sanitation penetration is lowest in India vis-a-vis other

emerging economies. According to Census 2011, the national sanitation coverage is

~40%, whereas rural sanitation coverage has remained a mere 30.7%. Rising need for

sanitation and special initiatives taken by the government to enhance sanitation

penetration indicates ample scope and growth available in the industry, going forward.

Exhibit: Asian Sanitation Levels

Source: Company, SKP Research

36

59

65

82

92

93

100

India

Indonesia

China

Korea

Sri Lanka

Thailand

Singapore

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 20

Changing demographics to drive demand: With 50% of India population below the age

of 30, the country’s ‘youth bulge’ is unequivocal about change, and demands better quality

products. Shift in consumer preferences along with greater brand awareness, higher

disposable income and superior standards of living has opened opportunities for new

products, leading to a shift from unorganised to organised sector.

Government’s Initiatives to improve sanitation: GoI is taking special initiatives to

improve sanitation penetration in India. It has launched a multi-million dollar sanitation

project, ‘Nirmal Bharat Abhiyaan’ to raise awareness and improve sanitation levels.

Although, this may not have a direct impact on premium quality producers like CERA,

there will certainly be a rub off effect. GoI also plans to develop 100 smart cities in India,

which would further boost the demand for sanitaryware products, including premium ones.

Heavily dependent on real estate market: Sanitaryware industry is quite dependent on

real estate sector as majority demand comes from new construction. Various initiatives of

Central and State Governments will revitalise the real estate and housing sector in the

country. With increasing urbanisation and infrastructure growth, urban population is

expected to reach to about 600 mn by 2031 which would lead to enhanced demand for

modern housing and building products thereby increasing demand for sanitaryware.

The middle income segment has become one of the principal drivers for real estate boom.

This segment has grown from 11 mn households in 2001-02 to 31 mn households in 2010-

11and is further expected to grow to 114 mn households by 2025-26.

Indian Tiles Industry – An Overview:

Ceramic Tiles market can be broadly divided into two sub-segments viz Ceramic Tiles and Vitrified Tiles. Vitrified Tiles can be further sub divided in to Polished Vitrified Tiles (PVT) and Glazed Vitrified Tiles (GVT).

Market Size: Ceramic tiles are an essential building material now. Despite the industrial slowdown in the past few years, Indian Tiles market grew from 494 million sq. Meters (MSM) in CY09 to 748 MSM in CY13 witnessing a CAGR of ~11%.

Structural shift from ceramic to vitrified tiles: A major change took over the ceramic tiles industry in the recent past with the introduction of the next generation vitrified tiles and porcelain tiles.

Globally, these tiles account for ~50% of total tile sales (by value). In India, contribution of these products is increasing year-on-year, with structural shift in consumer preference for superior, value added products.

Source: Somany Ceramics Presentation – Feb 2015

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 20

India is the third largest tiles producer, globally, with lowest per capita consumption: Top 3 tile producing countries in CY13 and per capita consumption is given below:

Country Production

(MSM) Production (% Share)*

Consumption (MSM)

Consumption (% Share)**

Per Capita Consumption

(sqm)

China 5700 48% 4556 39% 3.4

Brazil 871 7% 837 7% 4.1

India 748 6% 748 6% 0.5

Source: Somany Ceramics Presentation – Feb 2015; * Global Market Size in CY13 11913MSM; ** Global Consumption 11574 MSM

Despite the double digit growth (~11%) of tiles market in India, its per capita consumption is about a third of global average. Majority demand of tiles come from residential segment followed by commercial and replacement segment.

Break-up of domestic tiles market at a glance:

Source: Industry

Unorganised market losing sheen: Earlier the unorganised market was highly

competitive due to low cost manufacturing on account of tax evasion and low operating

cost due to usage of coal based fuel, presence in highly fragmented tier-I cities, low level

of premiumisation – ceramic tiles dominated sales, with no technology innovation.

Unorganised market is now loosing sheen due to –

Change in Consumer Preference: With change in consumer preference for branded value-added building products (from ceramic to vitrified tiles) demand for GVT and PVT tiles are increasing, which offers better designs than ceramic tiles.

Policy Shift - Ban on coal based plant: Ban on usage of coal for manufacturing tiles has further marred liquidity of small players as natural gas is 30% costlier than coal, leading them to increase prices of ceramic tiles, thus, making their pricing competitive with organized players.

Government’s move to curb black money: Liquidity crunch is expected to occur due to Central Government’s engineered move towards curbing black money and will lead to reduced cash transactions in building material segment, impacting the turnover of small unorganised players.

Demand Drivers: Opportunity landscape for the industry is quite wide in India. Following

are the demand drivers which could propel tiles market in the near future:

70%

15%

15%

Residential Demand

Commercial

Replacement

49%51%Organised

Unorganised

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 20

Increasing Urbanization: India is rapidly organizing, which is gradually

translating into more demand for ceramic tiles. A report by McKinsey Global Institute projects 40% of India’s population would be urbanized by 2030.

Growing Mass Affluent Segment: India’s mass affluent – probably the largest such segment in the world in PPP terms – is expected to grow from 58 mn in 2010 to 110 mn by 2020 (40% of the total national households from 24% in 2010). This segment is evolving towards international standards of lifestyle, translating into upsurge in demand for modern tiles.

Rising disposable income: With growing middle class and rising income, real household disposable income has increased by about four times since 1990, translating into greater investment in homes. Rising disposable income at a glance:

Source: Somany Ceramics Presentation – Feb 2015

Growth in real estate: Urban household development, demand for pucca houses and changing consumer preference towards tiles is encouraging the demand for tiles to go up. There is a growth in demand for tiles owing to the water seepage problem that leads to mould formation in walls and ceilings.

Government’s Initiatives: GoI plans to develop 100 smart cities,

development of industrial corridors, housing for all by 2022, etc., all will lead

to a boost in demand for ceramic tiles. ‘Swaccha Bharat Abhiyaan’ will lead

to building of toilets and community toilets.

Organized market gaining ground: Gradually, organized market is stemming up from the unorganized predominance previously, for the reasons mentioned above. This is encouraging for better control purposes and price mechanisms to play.

With more and more unorganized players becoming part of the organized players, market segmentation is skewing towards creation of a centralized market, which can be brought under the purview of regulations. A proper government support and other infrastructural reforms could lead to a better play for Indian ceramic tiles industry in years to come.

1679 1776

2896

3290

3619

4395

4913 4931

6005

6671

0

1000

2000

3000

4000

5000

6000

7000

1990 1995 2004 2005 2006 2007 2008 2009 2010 2011

USD

Per

House

hold

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 20

Outlook:

With increasing construction activities, especially in tier - II & tier - III cities, tiles market in the country is set to flourish. Demand from institutional customers is outpacing the retail demand in many regions of the country.

The overall Indian tiles market is expected to witness CAGR of more than 18% for next five years. However, during the same period demand for vitrified tiles is expected to grow at CAGR of 21% due to increasing institutional sales and changing consumer preferences.

Global Scenario:

The world ceramic tiles production is growing at a healthy CAGR of 8.5% over 2009-13, with the market size of 11,913 MSM. China is the world’s largest tiles producer with 47% market share. Brazil is the second largest tile producer with production capacity of 871 MSM followed by India at 748 MSM.

In terms of exports China is the largest exporter followed by Spain and Italy. These top three countries together contribute close to 66% to the overall world ceramic tiles exports.

Top Ten Ceramic Tiles Producing Nations Top Ten Ceramic Tiles Exporting Nations

Source: Somany Ceramics Annual Report 2015

India has not grown much in terms of exports of ceramic tiles and currently consists of less than 0.5% of global market. As per ‘Indian Council of Ceramic Tiles and Sanitaryware’, India has exported tiles worth USD 441 mn in 2014. India Exports ceramics to markets such as UAE, Saudi Arabia and Malaysia.

Peer Comparison

Source: SKP Research

HSIL CERA HSIL CERA HSIL CERA HSIL CERA HSIL CERA

FY15 16.8% 14.3% 4.3% 8.2% 10.9% 24.8% 0.4 0.2 22.0 34.1

FY16E 17.4% 14.5% 6.1% 8.4% 12.0% 25.3% 0.4 0.1 16.4 29.0

FY17E 17.3% 15.1% 6.5% 8.6% 13.0% 26.4% 0.4 0.1 13.6 23.9

FY18E 17.2% 15.5% 6.9% 9.1% 14.5% 27.8% 0.3 0.1 11.4 19.0

P/E (X)Peers

EBIDTAM (%) PATM (%) ROCE (%) D/E (X)

1148

318 303

114 88 80 63 51 50 48

0

200

400

600

800

1000

1200

1400

Ch

ina

Spai

n

Ital

y

Iran

Turk

ey

Me

xico

Bra

zil

UA

E

Vie

tnam

Po

lan

d

MSM

5700

871 748500 420 390 363 340 300 228

0

1000

2000

3000

4000

5000

6000

Ch

ina

Bra

zil

Ind

ia

Iran

Spai

n

Ind

on

esi

a

Ital

y

Turk

ey

Vie

tnam

Me

xico

MSM

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 20

Company Profile

The Company was incorporated in 1980 as Madhusudan Ceramics, an entity of

Madhusudan Industries Ltd; at Kadi, Gujarat; with the sanitaryware installed capacity of

0.3 mn pieces per annum and marketed its products under the brand name CERA.

During 2001, Ceramic Division of the Company was de-merged to a separate group

company named Madhusudan Oils and Fats Ltd, pursuant to the Order of Hon’ble Gujarat

High Court. Later, Company’s name was changed to Cera Sanitaryware Ltd (CERA).

Under the leadership of Mr. Vikram Somany, Chairman and Managing Director, with ~30

years industry experience, CERA has now become the third largest sanitaryware company

in India, with ~23% organised market share and claims to be largest in premium segment.

During 2007-08, CERA installed gas based captive power plant and wind turbine

generator, at Kadi and became the first sanitaryware company to use natural gas.

In 2010-11, CERA successfully commissioned faucet manufacturing plant, with the initial

capacity of 2,500 pieces per day and increased it to 7,200 pieces per day during FY15.

The plant is scalable up to 10,000 pieces per day.

During FY13, in order to capitalize on the low per capita consumption of tiles and the

growing demand in the industry, the Company launched CERA tiles, on outsourcing basis

and sold under the brand name ‘CERA’ in India. The entry into faucets and tiles is part of

CERA’s effort to position itself as a one-stop-shop bathroom solutions provider and

establish itself more firmly in the premium segment.

Source: The Company

CERA Business Model – One-stop-shop Bathroom Solutions Provider

Outsourcing Manufacturing

In-House Mfg Contract Mfg

Imported

Sanitaryware

Lifestyle products

viz. premium

bathroom products

comprising

bathtubs, jacuzzi,

steam cubicles,

shower partitions,

shower panels and

allied sanitaryware

products

Sanitaryware

Faucets

Sanitaryware

Faucets

Ceramic and

Vitrified tiles

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 20

In-house Manufacturing:

Sanitaryware: CERA has its state-of-the-art manufacturing facility in Kadi, Gujarat with

total manufacturing capacity at 3.0 mn pieces per annum and utilization level at around 97-

98%.The segment contributed ~35% to the total revenues (excluding allied products which

contributed ~14%)in FY15. Being the oldest, this segment will continue to be the mainstay

of the company.

Source: The Company & SKP Research

Faucets: The facility at Kadi also has the capacity to produce 7,200 pieces of faucets per

day, which could be ramped up, up-to 10,000 pieces per day. Currently, the facility is

working at ~60% utilization levels and contributed 8% to the total revenues, in FY15.

Source: The Company & SKP Research

The faucets plant is equipped with high tech energy saving induction furnaces, gravity die-

casting machines, auto-plating nickel-chrome plant and some special purpose machines to

produce quality confirming products.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Capacity (mn Pieces/Annum)

Capacity Utilization (mn Pieces/Annum)

0

500000

1000000

1500000

2000000

2500000

3000000

FY14 FY15 FY16E FY17E FY18E

Capacity (Pieces/Annum)

Capacity Utilization (Pieces/Annum)

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 9 of 20

Contract Manufacturing and Outsourcing:

Sanitaryware: CERA follows asset-light model by outsourcing, premium category

sanitaryware through contract manufacturing, from Gujarat based manufacturers with

whom it procures about 50,000 pcs per month.

CERA also outsource sanitaryware from China and have dedicated manufacturers with

quality control team in place. Production and packaging is done in China, in accordance

with the designs selected by CERA (including labelling), which are dispatched in India.

CERA focus on enhancing capacities through asset light model not only reduces its capital

investments, but also de-risks the balance sheet, enhances return ratios and provides

faster access to capacities. 40% of total revenues from sanitaryware segment are

contributed by outsourcing.

Faucets: Majority faucets are outsourced from Northern India and also from Gujarat.

Outsourcing contributes about ~50% (value-wise) of total faucet revenues of CERA.

Tiles: During FY13, the Company launched CERA tiles, on outsourcing basis and sold

under the brand name ‘CERA’ in India. This segment contributed Rs 686.4 mn to the total

revenue in FY15.

Keeping in view the benefits of outsourcing and JV model, CERA is in the process of

setting up a JV facility for tiles with Anjani Tiles Ltd., Andhra Pradesh and has acquired

controlling stake of 51% in Anjani Tiles recently.

Segment Wise Revenue Contribution at a glance

Source: The Company & SKP Research

73%

15%

8%4%

FY15

Sanitaryware

Faucets

Tiles

Wellness

51%

24%

22%

2%

FY18E

Sanitaryware

Faucets

Tiles

Wellness

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 10 of 20

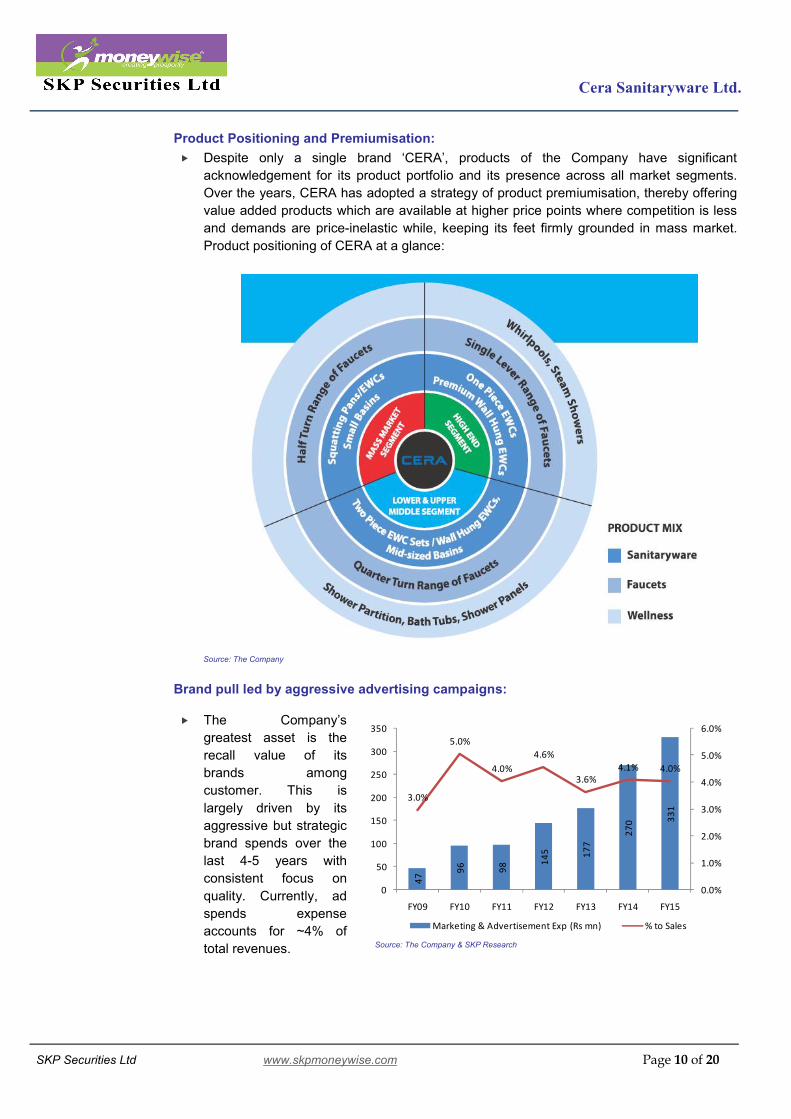

Product Positioning and Premiumisation:

Despite only a single brand ‘CERA’, products of the Company have significant

acknowledgement for its product portfolio and its presence across all market segments.

Over the years, CERA has adopted a strategy of product premiumisation, thereby offering

value added products which are available at higher price points where competition is less

and demands are price-inelastic while, keeping its feet firmly grounded in mass market.

Product positioning of CERA at a glance:

Source: The Company

Brand pull led by aggressive advertising campaigns:

The Company’s

greatest asset is the

recall value of its

brands among

customer. This is

largely driven by its

aggressive but strategic

brand spends over the

last 4-5 years with

consistent focus on

quality. Currently, ad

spends expense

accounts for ~4% of

total revenues.

47

96

98 1

45 17

7

27

0 33

1

3.0%

5.0%

4.0%

4.6%

3.6%4.1% 4.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0

50

100

150

200

250

300

350

FY09 FY10 FY11 FY12 FY13 FY14 FY15

Marketing & Advertisement Exp (Rs mn) % to Sales

Source: The Company & SKP Research

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 11 of 20

Robust distribution network:

Over the years, CERA has established a strong and widespread distribution network,

encompassing ~1400 distributors/dealers (authorised stockists) and 14,000 retailers

across India. To supplement the distribution network, CERA also has 20 major stock

points, 10 zonal sales & service offices and 10 bath studios across the country.

A major marketing exercise of expanding dealer and retailer network is in progress. The

company has also been sponsoring TV programs, arranging architect and plumber meets

on regular intervals etc. to create its brand image in the market. This has helped CERA to

reach wide spectrum of retail customers and maintain its dominating position in the

sanitaryware industry.

Cera’s wide distribution network at a glance:

Source: The Company

Raw Materials: Sanitaryware and faucetware: The basic ingredients for making ceramics is Kaolinite,

clay, feldspar and quartz sand which form the basis for this extremely durable and hard

material. The basic raw material used in manufacturing faucet is brass, since it is highly

resistant to corrosion and calcification.

Tiles: Sand and white clay are the main raw materials for manufacturing tiles, apart from

Feldspar, dolomite and some other minerals.

Procurement and Pricing: CERA procures the above mentioned raw materials locally.

There is not much fluctuation in the prices of raw materials of tiles and sanitaryware. Raw

material cost to sales ratio for CERA reflects a gradual increasing trend from 4.2% in FY10

to 6.3% during FY15.

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 12 of 20

Investment Rationale

1. Cera venturing into tiles manufacturing through JV:

Indian GDP is expected to grow ~8% in the coming years, resulting in increased buying

power in the hands of a growing and aspiring mass affluent segment. Keeping this in view

CERA is venturing into manufacturing of tiles through JV.

Cera has entered into a joint-venture agreement with an Andhra Pradesh based Anjani

Tiles Ltd to set up a ceramic vitrified tiles facility in Nellore, Andhra Pradesh.

CERA holds 51% stake in the project that is estimated to cost around Rs 680 mn, with the

Company’s equity share of ~190 mn. The plant will have an initial capacity of 10,000

square meters per day of tile manufacturing which could be scaled up to 3x-4x, going

forward.

The JV partners would fund the project with a mix of equity of around Rs 360 mn and

balance in debt to the tune of Rs 320 mn. The plant will be commissioned by March 2016.

Cera’s focus is to manufacture double charge and soluble salt tiles, initially.

The facility has a potential to generate additional revenue of ~Rs 750-1200 mn at full

capacity. Currently, tiles segment contributes ~13% (9MFY16) to the total revenues of the

company which is fulfilled by outsourcing. With the facility getting commissioned, we

expect the contribution from tiles segment to rise to 23% in FY18E.

Deferment of sanitaryware capex: CERA has deferred the capacity expansion plan of

sanitaryware from 3.0 mn pieces to 3.3 mn pieces due to sluggish demand. 2. Top-line expected to grow at a CAGR of ~17% over FY15-18Eled by faucets and tiles

segment:

Faucets Segment: In FY15, CERA reported net sales of Rs 8.21 bn, registering a growth

of 24% y-o-y on account of robust growth in faucet ware segment backed by strengthening

and enlargement of product basket, intensifying and enlargement of distributor reach. The

segment reported robust growth with a CAGR of 43%during FY12-15.

With ample of capacity in hand and well balanced ‘asset light model in place’ we

further expect the segment to grow with a CAGR of 37% during FY15-FY18E.

Source: The Company & SKP Research

69

3.7

98

7.5

12

23

.5

19

46

.0

25

09

.9

31

65

.1

62%

42%

24%

59%

29%26%

0%

10%

20%

30%

40%

50%

60%

70%

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

FY13 FY14 FY15 FY16E FY17E FY18E

Faucet Revenue % Growth

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 13 of 20

Tiles segment grew by 23% y-o-y to Rs 686.4 mn and contributed 8% to overall revenue,

during FY15. The contribution to total revenue rose to 13% during 9MFY16. With JV

capacity with Anjani tiles in place by March 2016, we further expect tiles segment to

grow with a CAGR of 65% during FY15-FY18E.

Source: The Company & SKP Research

Sanitaryware Segment: In FY15, sanitaryware segment reported net sales of Rs 5,963.6

mn, registering y-o-y growth of 24%. The division is continuously working on the optimum

capacity utilization of 97-98% for last many years. With the deferment of increasing the

capacity further, on account of subdued demand of real estate, we anticipate muted

growth in the segment, going forward.

Source: The Company & SKP Research

557.0 686.41235.5

2124.5

3068.1

23%

80%

72%

44%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

500

1000

1500

2000

2500

3000

3500

FY14 FY15 FY16E FY17E FY18E

Tiles Revenues (Rs mn) % Growth

38

78

.1

48

14

.0

59

63

.6

59

93

.8

63

22

.1

67

70

.4

45%

24% 24%

1%

5% 7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1000

2000

3000

4000

5000

6000

7000

8000

FY13 FY14 FY15 FY16E FY17E FY18E

Sanitaryware Revenue (Rs mn) % Growth

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 14 of 20

Overall sales and revenue contribution at a glance:

Overall Sales Revenue Contribution

Source: The Company & SKP Research

3. Margins expected to improve with better operating leverage

EBIDTA Margins of the company was under pressure from FY11 to FY15, when it reduced

from 18.9% to 14.3%. Margins improved to 15.3% during Q3FY16 due to lower energy

cost and price increase taken by the company in sanitaryware segment by 2-7% during

the quarter.

Going forward, we expect EBIDTA margins to stabilize at ~15% by FY18E on the

back of better product mix with more premium products. Furthermore, we expect

margins from captive tiles manufacturing to be better than margins from outsourced

model.

Source: The Company & SKP Research

45

8.3

53

3.7

75

3.3

94

9.4

11

75

.3

13

72

.0

16

88

.0

20

49

.8

18.9%

16.7%15.4%

14.3% 14.3% 14.5%15.1% 15.5%

0.0%

5.0%

10.0%

15.0%

20.0%

0

500

1000

1500

2000

2500

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

PA

T M

argi

n (

%)

EBID

TA (

`m

n)

24

29

.5

31

93

.9

48

78

.7

66

36

.9

82

16

.7

94

84

.2

11

20

3.6

13

25

3.2

0

2000

4000

6000

8000

10000

12000

14000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Ove

rall

Ne

t R

eve

nu

es

(`m

n)

Overall Revenue

83% 79%73% 73%

63% 56% 51%

13%14%

15% 15%21%

22%24%

8% 8% 13% 19% 23%

3% 6% 4% 4% 3% 2% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Sanitaryware Faucets Tiles Welness

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 15 of 20

PAT margins (PATM) were up by 40 bps to8.2% in FY15 from 7.8% reported in FY14

which further improved to 8.6 % during Q3FY16.

With improvement in segment margins and better operating leverage coupled with low

debt, we expect PATM to improve further to ~9.1% respectively by FY18E.

PAT Margins, ROE and ROCE at a glance:

Source: The Company & SKP Research

4. Focus on ‘asset light model’ helps in De-leveraged Balance Sheet: As mentioned above, CERA has been focusing on enhancing its production volumes by

entering into outsourcing contracts both indigenously and from China. Recently, it has also

entered in to joint venture with Anjali tiles for manufacturing tiles.

CERA’s focus on enhancing capacities through asset light model not only reduces its capital

investments but also de-risks the balance sheet, enhances return ratios and provides faster

access to capacities thereby, resulting into continuous low debt equity ratio (D/E). CERA’s

D/E is significantly low at 0.2x in FY15 (as shown in the graph below).

Debt position of CERA at a glance:

Source: The Company & SKP Research

265.4320.4

462.1519.1

676.7

793.8965.4

1211.410.9%

10.0%9.5%

7.8%8.2% 8.4% 8.6%

9.1%

0%

2%

4%

6%

8%

10%

12%

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

PA

T M

argi

n (

%)

PA

T (`

mn

)

23.8%23.0%

25.7%

23.2%

19.2% 18.8% 19.1%19.8%

27.4%

25.3%

28.1%

31.0%

24.8% 25.3%26.4%

27.8%

15%

17%

19%

21%

23%

25%

27%

29%

31%

33%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

ROE (%) ROCE (%)

25

6.3

8

93

.68

11

6.2

2

14

8.9

2

90

.00

14

2.3

8

27

3.4

2

22

5.9

6

17

8.5

0

15

.75 2

25

.97

29

5.9

5 40

0.4

9

33

3.6

1

45

0.2

0

29

4.0

1

31

3.7

0

33

1.3

3

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

0

50

100

150

200

250

300

350

400

450

500

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6E

FY1

7E

FY1

8E

x

`m

n

Long Term Debt (LHS) Short Term Debt (LHS) D/E (RHS)

13.811.4

9.3

12.8 13.2

23.1 22.8

30.1

0.3 0.3 0.3

0.20.2

0.10.1

0.1

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

Interest Coverage (x) - RHS

D/E (x) - LHS

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 16 of 20

Key Concerns

Competition from unorganised players: The building product industry is dominated by

small unorganized players. Though, Indian consumers are gravitating towards the

organized segment, offering branded products, any increase in the competitive intensity

from unorganized segment may be detrimental for the company. The proposed GST will

remove the cascading effect of interstate transfers; will create a level playing field for

organised players and will result in a huge shift from the unorganised market to the

organised market.

Extended slowdown in real estate sector may dampen business sentiments: All

product segments of CERA are highly dependent on real estate sector. Any extension of

slowdown to Tier –I and Tier –II cities may dampen the business prospects of CERA.

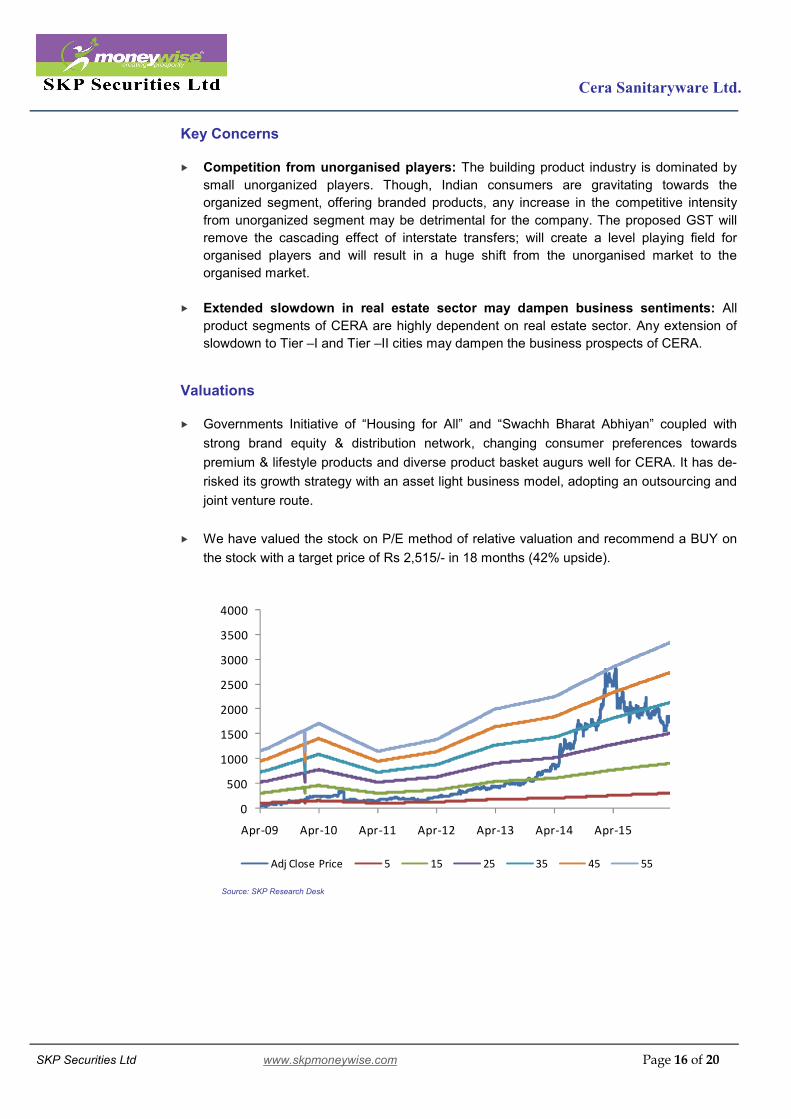

Valuations

Governments Initiative of “Housing for All” and “Swachh Bharat Abhiyan” coupled with

strong brand equity & distribution network, changing consumer preferences towards

premium & lifestyle products and diverse product basket augurs well for CERA. It has de-

risked its growth strategy with an asset light business model, adopting an outsourcing and

joint venture route.

We have valued the stock on P/E method of relative valuation and recommend a BUY on

the stock with a target price of Rs 2,515/- in 18 months (42% upside).

Source: SKP Research Desk

0

500

1000

1500

2000

2500

3000

3500

4000

Apr-09 Apr-10 Apr-11 Apr-12 Apr-13 Apr-14 Apr-15

Adj Close Price 5 15 25 35 45 55

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 17 of 20

Q3FY16 & 9MFY16 Standalone Result Review

(All data in Rs mn unless specified, Y/e March)

Particulars Q3 FY16 Q3 FY15 % Change Q2 FY16 % Change 9MFY16 9MFY15 % Change

Net Sales 2335.3 2092.9 11.6% 4293.9 -45.6% 6531.0 5712.3 14.3%

Total Expenditure 1977.7 1796.3 9.2% 3537.7 -44.1% 5599.5 4897.8 12.5%

Raw Material Consumed 56.6 -8.8 -742.2% 501.6 -88.7% 442.9 166.0 166.8%

% to Sales 2.4% -0.4% -- 11.7% -- 6.8% 2.9% --

Purchase of traded goods 1016.7 973.6 4.4% 799.5 27.2% 2584.1 2419.3 6.8%

% to Sales 43.5% 46.5% -- 18.6% -- 39.6% 42.4% --

Employee Expenses 279.5 243.5 14.8% 559.4 -50.0% 813.8 710.6 14.5%

% to Sales 12.0% 11.6% -- 13.0% -- 12.5% 12.4% --

Fuel Cost 83.2 95.3 -12.7% 610.2 -86.4% 221.2 240.0 -7.8%

% to Sales 3.6% 4.6% -- 14.2% -- 3.4% 4.2% --

Marketing & Advertisement 0.0 0.0 -- 0.0 -- 0.0 0.0 --

% to Sales 0.0% 0.0% -- 0.0% -- 0.0% 0.0% --

Other Expenses 541.8 492.7 10.0% 1067.0 -49.2% 1537.5 1362.0 12.9%

% to Sales 23.2% 23.5% -- 24.8% -- 23.5% 23.8% --

EBIDTA 357.6 296.6 20.6% 756.2 -52.7% 931.5 814.4 14.4%

EBIDTA Margin 15.3% 14.2% -- 17.6% -- 14.3% 14.3% --

Depreciation 44.5 41.9 6.1% 289.6 -84.6% 120.8 109.8 10.0%

EBIT 313.1 254.7 22.9% 466.6 -32.9% 810.7 704.6 15.1%

EBIT Margin 13.4% 12.2% -- 10.9% -- 12.4% 12.3% --

Other Income 16.2 14.9 8.7% 11.1 45.9% 63.6 43.7 45.7%

Interest 11.0 21.8 -49.7% 91.8 -88.1% 40.4 52.8 -23.5%

Exceptional Items 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Forex Difference 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Tax 117.2 86.2 36.0% 142.6 -17.8% 297.4 240.1 23.9%

Extraordinary Items 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Prior period taxes written bk. 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Minority Interest 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Share of Associate Company 0.0 0.0 -- 0.0 -- 0.0 0.0 --

Reported Profit After Tax 201.2 161.6 24.5% 243.3 -17.3% 536.6 455.5 17.8%

PAT Margin 8.6% 7.7% -- 5.7% -- 8.2% 8.0% --

Diluted EPS (Rs) 15.5 12.8 21.1% 3.4 358.8% 41.3 36.0 14.6%

Source: The Company

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 18 of 20

Exhibit: Income Statement Exhibit: Balance Sheet

Particulars FY15 FY16E FY17E FY18E Particulars FY15 FY16E FY17E FY18E

Total Income 8,216.7 9,484.2 11,203.6 13,253.2 Share Capital 65.0 65.0 65.0 65.0

Growth (%) 23.8% 15.4% 18.1% 18.3% Reserve & Surplus 3,452.1 4,148.3 4,996.6 6,052.0

Expenditure 7,041.4 8,112.2 9,515.6 11,203.4 Shareholders Funds 3,517.1 4,213.3 5,061.7 6,117.0

Material Cost 521.3 635.4 728.2 861.5 Total Debt 592.6 567.4 539.7 509.8

Pur of Traded Goods 3,321.6 3,736.8 4,403.0 5,182.0 Deferred Tax (Net) 278.2 278.2 278.2 278.2

Employee Cost 917.4 1,185.5 1,400.5 1,656.6 Other Long Term Liab 92.7 107.0 95.2 112.7

Power & Fuel & Othr Exp. 1,949.7 2,171.9 2,532.0 2,968.7 Total Liabilities 4,480.6 5,166.0 5,974.8 7,017.8

EBITDA 1,175.3 1,372.0 1,688.0 2,049.8

Depreciation 154.6 161.0 211.5 210.6 Net Block inc. Capital WIP 2,223.4 2,619.3 2,607.9 2,597.3

EBIT 1,020.7 1,211.0 1,476.5 1,839.2 Investments 477.6 368.2 368.2 368.2

Other Income 65.9 75.9 89.6 106.0 Non-Current Asset - 17.0 20.0 23.7

Interest Expense 77.3 52.4 64.8 61.2 Inventories 1,258.9 1,327.8 1,736.6 1,988.0

Profit Before Tax (PBT) 1,009.3 1,234.5 1,501.4 1,884.0 Sundry Debtors 1,612.2 1,640.8 2,240.7 2,518.1

Income Tax 332.6 440.7 536.0 672.6 Cash & Bank Balance 295.3 363.5 292.1 723.6

Profit After Tax (PAT) 676.7 793.8 965.4 1,211.4 Other Current Assets 2.7 3.1 3.6 4.3

Growth (%) 30.4% 17.3% 21.6% 25.5% Loans & Advances 572.4 872.5 1,064.3 1,259.1

Diluted EPS 52.0 61.0 74.2 93.1 Current Liabilities & Prov 1,961.8 2,046.1 2,358.7 2,464.4

Net Current Assets 1,779.7 2,161.5 2,978.7 4,028.6

Total Assets 4,480.6 5,166.0 5,974.8 7,017.8

Exhibit: Cash Flow Statement Exhibit: Ratio Analysis

Particulars FY15E FY16E FY17E FY18E Particulars FY15 FY16E FY17E FY18E

Profit Before Tax (PBT) 1,009.3 1,234.5 1,501.4 1,884.0 Earning Ratios (%)

Depreciation 154.6 161.0 211.5 210.6 EBITDA Margin (%) 14.3% 14.5% 15.1% 15.5%

Interest Provided 75.8 52.4 64.8 61.2 PAT Margins (%) 8.2% 8.4% 8.6% 9.1%

Chg. in Working Capital (534.8) (316.3) (903.3) (604.6) ROCE (%) 24.8% 25.3% 26.4% 27.8%

Direct Taxes Paid (295.5) (440.7) (536.0) (672.6) ROE (%) 19.2% 18.8% 19.1% 19.8%

Other Charges (3.7) - - - Per Share Data (INR)

Operating Cash Flows 405.6 690.9 338.3 878.6 Diluted EPS 52.0 61.0 74.2 93.1

Capital Expenditure (853.3) (557.0) (200.0) (200.0) Cash EPS (CEPS) 63.9 73.4 90.5 109.3

Investments (407.6) 109.4 - - BVPS 270.4 324.0 389.2 470.3

Others 88.1 - - - Valuation Ratios (x)

Investing Cash Flows (1,172.7) (447.6) (200.0) (200.0) P/E 34.1 29.0 23.9 19.0

Changes in Equity 706.0 - - - Price/BVPS 6.6 5.5 4.6 3.8

Inc / (Dec) in Debt 199.1 (25.2) (27.8) (29.8) EV/Sales 2.8 2.5 2.1 1.7

Dividend Paid (inc tax) (74.0) (97.5) (117.1) (156.1) EV/EBITDA 19.9 16.9 13.8 11.1

Interest Paid (75.8) (52.4) (64.8) (61.2) EB/EBIT 22.9 19.2 15.8 12.4

Financing Cash Flows 755.3 (175.1) (209.6) (247.1) Balance Sheet Ratios

Chg. in Cash & Cash Eqv (11.8) 68.2 (71.3) 431.5 Debt - Equity 0.2 0.1 0.1 0.1

Opening Cash Balance 307.1 295.3 363.5 292.1 Current Ratio 1.9 2.1 2.3 2.6

Closing Cash Balance 295.3 363.5 292.1 723.6 Fixed Asset Turn. Ratios 3.8 3.6 4.3 5.1

Source: Company Data, SKP Research

Figures in INR Million Figures in INR Million

Figures in INR Million

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 19 of 20

Notes:

The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg,

Thomson First Call & Investext Myiris, Moneycontrol, Tickerplant and ISI Securities.

DISCLAIMER:

This document has been prepared by SKP Securities Ltd, hereinafter referred to as SKP to provide information about the company(ies)/sector(s), if any, covered in the report and may be distributed by it and/or its affiliates. SKP Securities Ltd., offers broking and depository participant services and is regulated by Securities and Exchange Board of India (SEBI). It also distributes investment products/services like mutual funds, alternative investment funds, bonds, IPOs, etc., renders corporate advisory services and invests its own funds in securities and investment products. We declare that no material disciplinary action has been taken against SKP by any regulatory authority impacting Equity Research Analysis. As a value addition to its clients, it offers its research services and reports in various formats to its clients and prospects. As such, SKP is making these disclosures under SEBI (Research Analysts) Regulations, 2014, under which it is in the process of seeking registration.

Terms & Conditions and Other Disclosures:

This research report (“Report”) is for the personal information of the selected recipient(s), does not construe to be any investment, legal or taxation advice, is not for public distribution and should not be copied, reproduced or redistributed to any other person or in any form without SKP’s prior permission. The information provided in the Report is from publicly available data, which we believe, are reliable. While reasonable endeavors have been made to present reliable data in the Report so far as it relates to current and historical information, but SKP does not guarantee the accuracy or completeness of the data in the Report. Accordingly, SKP or its promoters, directors, subsidiaries, associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained and views and opinions expressed in this publication. Past performance mentioned in the Report should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment of its original date of publication by SKP and are subject to change without notice. The price, value of and income from any of the securities mentioned in this report can rise or fall. The Report includes analysis and views of individual research analysts (which, hereinafter, includes persons reporting to them) covering this Report. The Report is purely for information purposes. Opinions expressed in the Report are SKP’s or its research analysts’ current opinions as of the date of the Report and may be subject to change from time to time without notice. SKP or any person connected with it does not accept any liability arising from the use of this document. Investors should not solely rely on the information contained in this Report and must make investment decisions based on their own investment objectives, judgment, risk profile and financial position. The recipients of this Report may take professional advice before acting on this information. SKP, along with its affiliates, are engaged in various financial services and so might have financial, businesses or other interest in other entities, including the subject company or its affiliates mentioned in this report, for which it might have received any compensation in the past twelve months. SKP does not provide any merchant banking or market making service and does not manage public offers. However, SKP encourages independence in preparation of research reports and strives to minimize conflict in preparation of research reports.SKP and its analysts did not receive any compensation or other benefits from the subject company mentioned in the Report or from a third party in connection with preparation of the Report. Accordingly, SKP and its Research Analyst do not have any material conflict of interest at the time of publication of this Report. SKP’s research analysts may provide input into its other business activities. Investors should assume that SKP and/or its affiliates are seeking or will seek business assignments from the company(ies) that are the subject of this material and that the research analysts who are involved in preparing this material may educate investors on investments in such businesses. The research analysts responsible for the preparation of this document may interact with trading desk/sales personnel and other parties for the purpose of gathering, applying and interpreting information. Our research analysts are paid on the profitability of SKP, which may include earnings from business activities for which this Report is being used, but not for the preparation of this report. SKP generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any company(ies) that the analyst covers. Additionally, SKP generally, prohibits its analysts and persons reporting to analysts from serving as an officer, director or advisory board member of any companies that the analyst cover. The following Disclosure of Interest Statement, clarifies it further: SKP or its Research Analyst(s) engaged in preparation of this Report or his/her relative (i) do not have any financial interests in the subject company mentioned in this report (ii) do not own 1% or more of the equity securities of the subject company mentioned in the report as of the last day of the month preceding the publication of the research report (iii) do not have any other material conflict of interest at the time of publication of the research report. The distribution of this document in other jurisdictions may be strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

Cera Sanitaryware Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 20 of 20

Analyst Certification

The views expressed in this research report accurately reflect the personal views of the analyst about the subject securities or issues, which are subject to change without prior notice and does not represent to be an authority on the subject. No part of the compensation of the research analyst was, is, or will be directly or indirectly related to the specific recommendations and views expressed by research analyst in this report. The research analysts, strategists, or research associates principally responsible for preparation of SKP research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

Disclosure of Interest Statement

Analyst ownership of the stock NIL

Served as an officer, director or employee NIL

SKP Securities Ltd

Contacts Research Sales

Mumbai Kolkata Mumbai Kolkata

Phone 022 4922 6006 033 4007 7000 022 4922 6000 033 4007 7400

Fax 022 4922 6066 033 4007 7007 022 4922 6066 033 4007 7007

E-mail [email protected] [email protected] [email protected]

Member: NSE BSE NSDL CDSL NCDEX* MCX* MCX-SX FPSB

*Group Entities INB/INF: 230707532, BSE INB: 010707538, CDSL IN-DP-CDSL-132-2000, DPID: 021800, NSDL IN-DP-NSDL: 222-2001, DP ID: IN302646, ARN: 0006, NCDEX: 00715, MCX: 31705, MCX-SX: INE 260707532

Institutional & Retail Broking Wealth Advisory & Distribution Investment Banking