Manufacturing and Production Sales Tax Exemptions:...

81

Manufacturing and Production Sales Tax Exemptions: Not Just for Manufacturers Leveraging Tax-Savings Opportunities as States Create and Expand Reach of Exemptions Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. WEDNESDAY, SEPTEMBER 18, 2013 Presenting a live 110-minute teleconference with interactive Q&A Susan Traylor Bittick, Principal, Ryan, Austin, Texas Stephanie Gilfeather, Senior Multistate Tax Consultant, Deloitte Tax, Seattle Chris Wallace, Senior Manager of State and Local Tax, Weaver LLP, Dallas Scott Edwards, Shareholder, Lane Powell, Seattle For this program, attendees must listen to the audio over the telephone.

Transcript of Manufacturing and Production Sales Tax Exemptions:...

Manufacturing and Production Sales Tax

Exemptions: Not Just for Manufacturers Leveraging Tax-Savings Opportunities as States Create and Expand Reach of Exemptions

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, SEPTEMBER 18, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Susan Traylor Bittick, Principal, Ryan, Austin, Texas

Stephanie Gilfeather, Senior Multistate Tax Consultant, Deloitte Tax, Seattle

Chris Wallace, Senior Manager of State and Local Tax, Weaver LLP, Dallas

Scott Edwards, Shareholder, Lane Powell, Seattle

For this program, attendees must listen to the audio over the telephone.

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Manufacturing and Production Sales Tax Exemptions: Not Just for Manufacturers Seminar

Chris Wallace, Weaver LLP

Scott Edwards, Lane Powell

Sept. 18, 2013

Susan Traylor Bittick, Ryan LLC

Stephanie Gilfeather, Deloitte Tax

Today’s Program

Introduction and Overview

[Scott Edwards]

Legislative Developments

[Susan Traylor Bittick, Stephanie Gilfeather]

Jurisdictions with Broad Manufacturing Exemptions

[Stephanie Gilfeather]

Exemptions for Activities Outside of Direct Production

[Chris Wallace]

Slide 4 - Slide 17

Slide 65 - Slide 80

Slide 43 - Slide 64

Slide 18 - Slide 42

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

INTRODUCTION AND OVERVIEW

Scott Edwards, Lane Powell PC

9 9 ©2013 Lane Powell PC

Manufacturer’s Sales Tax

Exemptions

Introduction and Overview

Scott Edwards

Co-Chair, State and Local Tax

Lane Powell, PC

206.223.7010

10 10 ©2013 Lane Powell PC

Introduction

• Common Exemption -Approx. 37 of 45 Sales Tax

States

• Caveat - This presentation is a survey of concepts

generally but not universally applicable to sales tax

exemptions for manufacturing machinery. Each

state's statutes and interpretive authorities are

different. Similar or identical language may be

interpreted differently from state to state. There are

often other requirements in addition to those

discussed here.

11 11 ©2013 Lane Powell PC

Basic Elements

• Machinery & Equipment

• Used Directly

• Manufacturing Operation

(or other qualifying operation)

–Research & Development

–Testing

12 12 ©2013 Lane Powell PC

Machinery & Equipment

• Definitions Vary

– Arkansas – facilities which cause a recognizable &

measurable action

• Fixtures, Support Structures

• Repair Parts

• Installation Labor

• Pollution Control Equipment

13 13 ©2013 Lane Powell PC

Typical Exclusions

• Hand Powered Tools

• Property w/ useful life less than 1 year

• Buildings (except M&E that becomes a

physical part of the building)

• Fixtures not integral to manufacturing

operation

14 14 ©2013 Lane Powell PC

Used Directly

• Acts upon or interacts with TPP

• Conveys, transports, handles or temporarily stores

TPP at site

• Controls, guides, measures, verifies, aligns,

regulates or tests TPP

• Provides physical support for, or access to, TPP

15 15 ©2013 Lane Powell PC

Used Directly – continued

• Produces power for or lubricates M&E

• Produces other TPP for use in a

qualifying operation

• Places TPP in a container or package

• Integrated Plant Theory v. Physical

Transformation Theory

16 16 ©2013 Lane Powell PC

Dual Use-differing treatment

• Exclusive Use

• Primary or Predominant Use

• Proportional Use

17 17 ©2013 Lane Powell PC

Manufacturing

• Processing, assembling, producing,

combining, refining, fabricating

• Materiality of change?

• Sometimes industry specific

–Agriculture, Lumber, Mining

–Clean Rooms

• Resulting in goods for sale

18 18 ©2013 Lane Powell PC

Manufacturing Operation

• Manufacturing of articles, substances or

commodities for sale as TPP

• Begins where raw materials enter

manufacturing site

• Generally must be used at a manufacturing

site (operation may have multiple sites)

• Cogeneration facility for power consumed at

site & project is integral part

19 19 ©2013 Lane Powell PC

Manufacturing or Not?

• Concrete

• Electricity

• Food Products

• Lumber

• Printing and Publishing

• Rock Crushing

20 20 ©2013 Lane Powell PC

Some Current Issues

• Telephone as manufacturing

• Big box retailer as manufacturer

• When do computers qualify as

manufacturing equipment

Slide Intentionally Left Blank

LEGISLATIVE DEVELOPMENTS

Susan Traylor Bittick, Ryan

Stephanie Gilfeather, Deloitte Tax

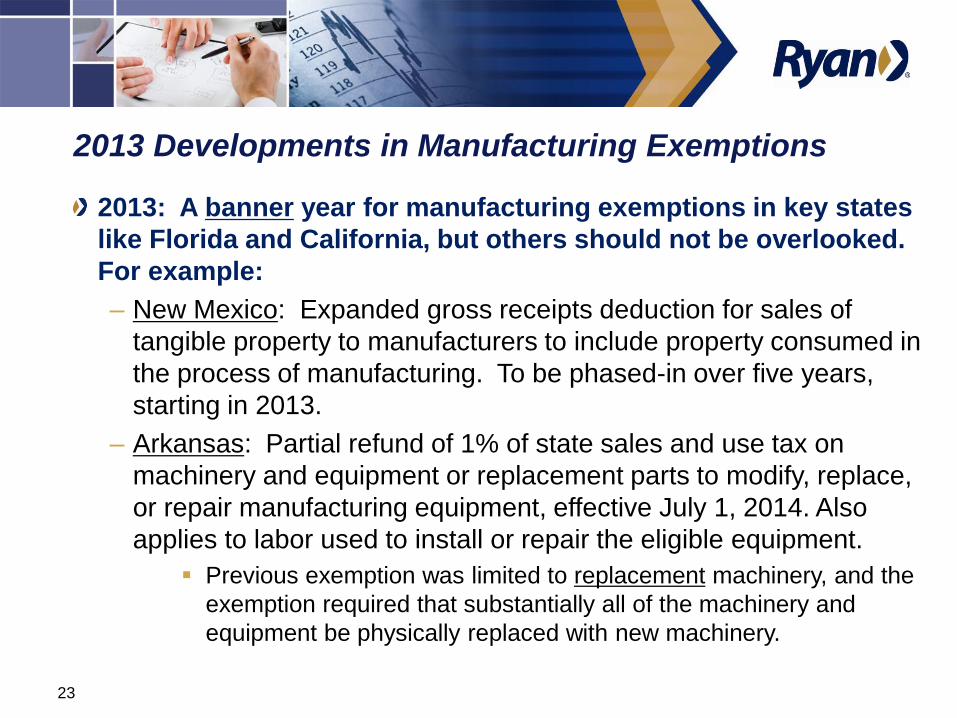

2013 Developments in Manufacturing Exemptions

2013: A banner year for manufacturing exemptions in key states

like Florida and California, but others should not be overlooked.

For example:

– New Mexico: Expanded gross receipts deduction for sales of

tangible property to manufacturers to include property consumed in

the process of manufacturing. To be phased-in over five years,

starting in 2013.

– Arkansas: Partial refund of 1% of state sales and use tax on

machinery and equipment or replacement parts to modify, replace,

or repair manufacturing equipment, effective July 1, 2014. Also

applies to labor used to install or repair the eligible equipment.

Previous exemption was limited to replacement machinery, and the

exemption required that substantially all of the machinery and

equipment be physically replaced with new machinery.

23

2013 Developments in Manufacturing Exemptions, cont.

– Wisconsin: Created exemption for machinery and equipment used

in manufacturing and biotechnology research in 2009; fine-tuned it

in 2013.

2013 amendments:

» Clarified that a member of a combined group qualified for the

exemption if at least one member of the combined group is

engaged in manufacturing or engaged primarily in biotechnology

research, and

» Provided that a qualifying business must be engaged in

manufacturing at a building that is assessed as manufacturing

property under Section 70.995, state statutes.

24

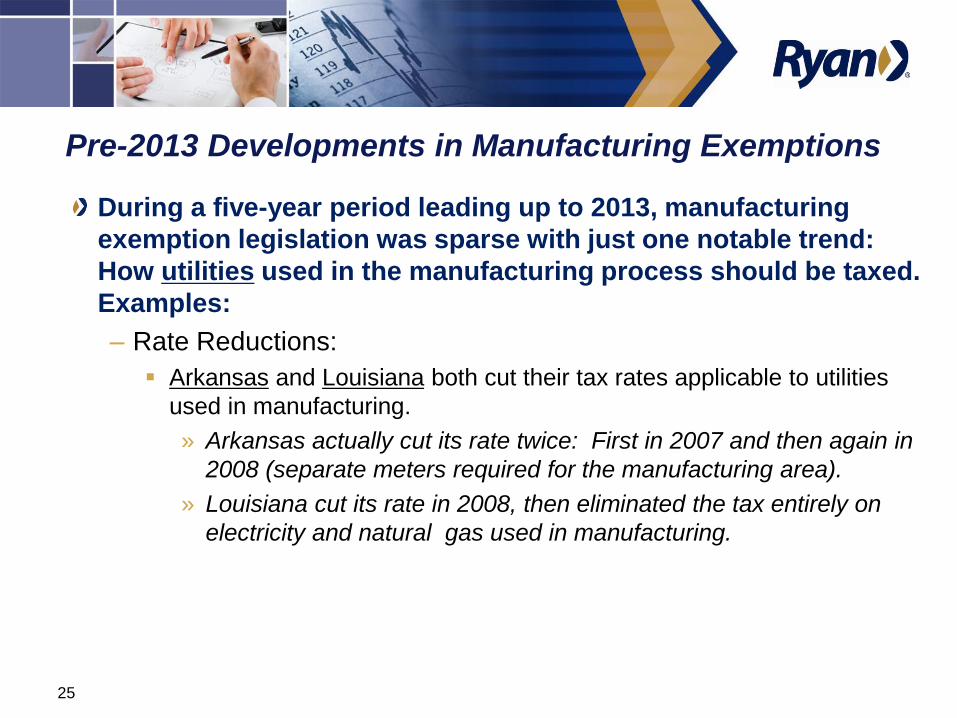

Pre-2013 Developments in Manufacturing Exemptions

During a five-year period leading up to 2013, manufacturing

exemption legislation was sparse with just one notable trend:

How utilities used in the manufacturing process should be taxed.

Examples:

– Rate Reductions:

Arkansas and Louisiana both cut their tax rates applicable to utilities

used in manufacturing.

» Arkansas actually cut its rate twice: First in 2007 and then again in

2008 (separate meters required for the manufacturing area).

» Louisiana cut its rate in 2008, then eliminated the tax entirely on

electricity and natural gas used in manufacturing.

25

Pre-2013 Developments in Manufacturing Exemptions,

cont.

– Temporary Repeals/Scaled-Back Utilities Exemptions:

Colorado eliminated the sales tax exemption on utilities on January 1,

2010, but reinstated effective July 1, 2012.

Kansas temporarily reduced the look-back period for a refund on

sales tax on exempt utilities in 2011, reducing it to 12 months.

Effective July 1, 2012, the state reinstated the original 36-month look-

back period for refunds.

Indiana reduced the look-back period for a refund of sales tax paid on

exempt utility meters to 18 months in 2011. Effective July 1, 2012, the

state restored the prior 36-month look-back period.

26

Pre-2013 Developments in Manufacturing Exemptions,

cont.

– Georgia: New exemption on utilities used in manufacturing:

2013 is the first of a four-year phase-in of a full exemption covering utilities

used in manufacturing in Georgia.

Applies to state sales tax and local tax except taxes dedicated to education.

Applies generally to all energy “necessary and integral” to the production of

tangible personal property at a Georgia manufacturing plant.

Energy includes: natural or artificial gas, oil, gasoline, electricity, solid fuel,

wood, waste, ice, steam, water, or other materials necessary and integral for

heat, light, power, refrigeration, climate control, processing, or any other use in

any phase of the manufacture of tangible personal property.

Phased in:

» 25% exempt in 2013.

» 50% exempt in 2014.

» 75% exempt in 2015.

» 100% exempt in 2016.

27

Targeted Changes to Manufacturing Exemptions

Some state legislatures enacted or considered targeted changes

to manufacturing exemptions. Examples:

– Washington, effective April 11, 2011:

Expanded the definition of a manufacturer to include printers of

newspapers and other materials.

Class A or exceptional quality biosolids by a wastewater treatment

facility are considered to be manufacturing.

– Oklahoma, effective August 26, 2011:

Added businesses classified under NAICS Code 324110 (i.e.,

Petroleum Refineries) to the definition of a manufacturer.

28

Targeted Changes to Manufacturing Exemptions, cont.

– Texas: Does “Manufacturing“ Include Oil and Gas Production?

House Bill 3113, filed in 2013, would have amended the

manufacturing exemption to provide that “bringing oil or gas to the

surface of the earth is not considered manufacturing, fabricating or

processing for ultimate sale.”

Died without a hearing.

Filed in response to Southwest Royalties, Inc. v. Combs et al. , now

pending before the state’s Third Court of Appeals, in which taxpayer

seeks refund for taxes paid on downhole equipment under the

manufacturing exemption.

Trial judge initially issued bench ruling for the taxpayer, then, reversed

himself after hearing additional evidence on a motion for

reconsideration.

» Based his reversal on the taxpayer’s failure to show that the

equipment at issue directly causes physical changes to the

petroleum. 29

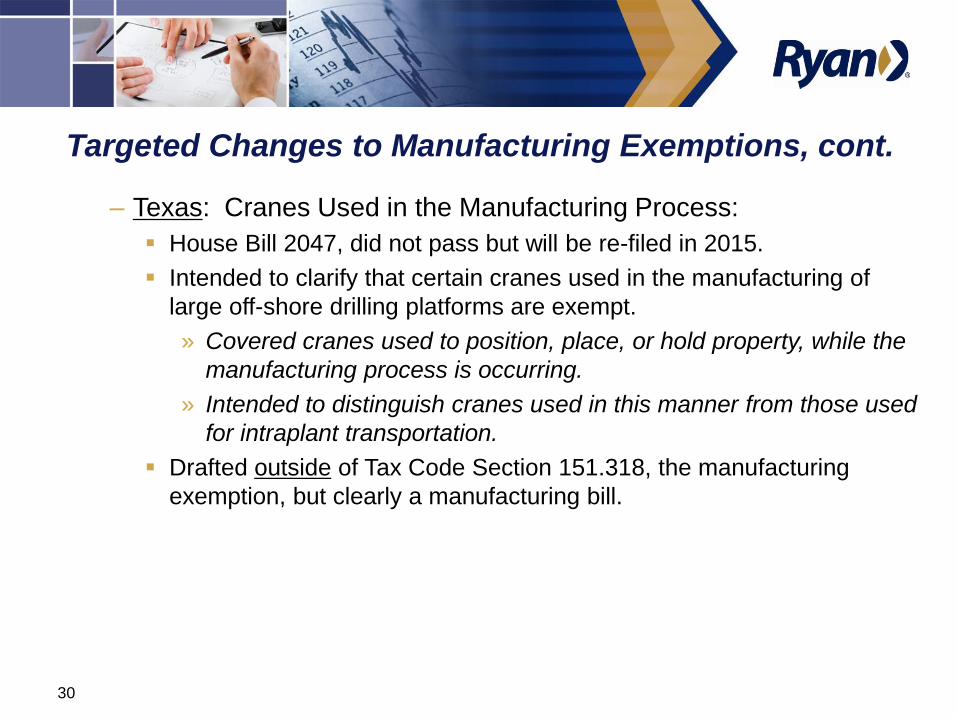

Targeted Changes to Manufacturing Exemptions, cont.

– Texas: Cranes Used in the Manufacturing Process:

House Bill 2047, did not pass but will be re-filed in 2015.

Intended to clarify that certain cranes used in the manufacturing of

large off-shore drilling platforms are exempt.

» Covered cranes used to position, place, or hold property, while the

manufacturing process is occurring.

» Intended to distinguish cranes used in this manner from those used

for intraplant transportation.

Drafted outside of Tax Code Section 151.318, the manufacturing

exemption, but clearly a manufacturing bill.

30

Targeted Changes to Manufacturing Exemptions, cont.

– California: “Green“ Manufacturing:

California created an exemption for manufacturing equipment used to

produce alternative energy.

» Unique program, administered by California Energy and Advanced

Transportation Authority; effective March 24, 2010–January 1,

2021.

» Controversy surrounded this program. It was rewritten effective

January 1, 2013 as the state’s “Advanced Manufacturing”

Exemption, applicable to purchases made by manufacturers in the

fields of science, engineering, and information technology for use in

“advanced manufacturing.”

» “Advanced manufacturing” means processes that create new or improve

existing materials, products, and processes; also includes

advancements in manufacturing systems used to produce materials and

products.

» Qualifying system advancements must increase sustainability and

efficiency.

31

Targeted Changes to Manufacturing Exemptions, cont.

– California: Special Treatment for Makers of “Drones“:

California Assembly Bill 1326 filed in 2013.

Would exempt certain property purchased for use in “unmanned aerial

vehicle manufacturing.“

Would cover “component parts, devices used to operate or maintain

machinery used in the manufacturing process, computers, software,

machinery for pollution control and fuel used during drone production.”

It would also allow exemptions for expenses related to building drone

manufacturing sites.

32

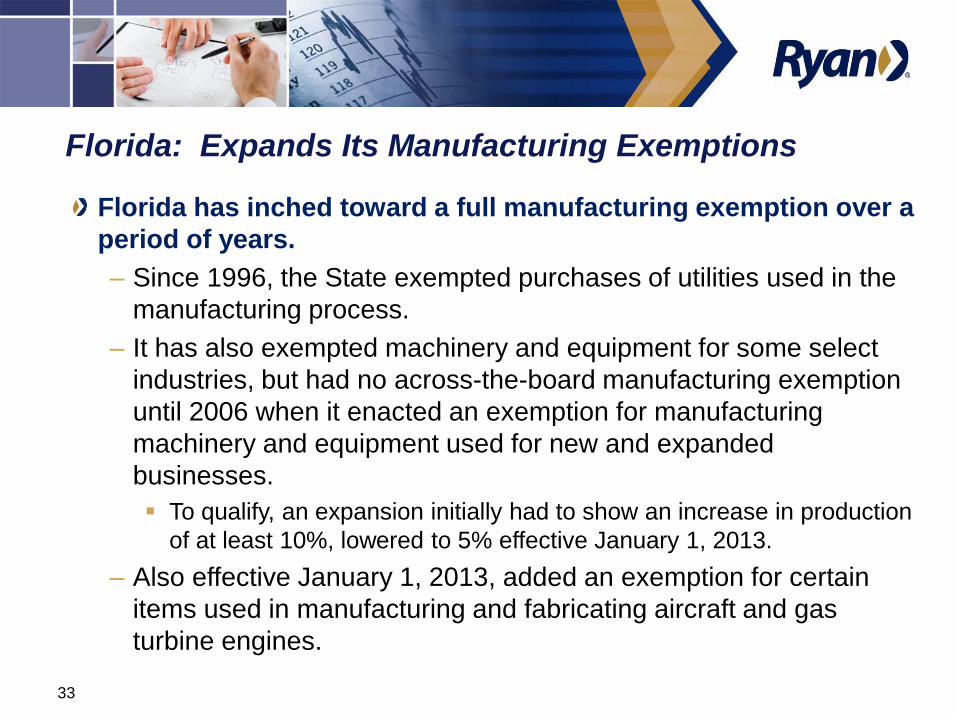

Florida: Expands Its Manufacturing Exemptions

Florida has inched toward a full manufacturing exemption over a

period of years.

– Since 1996, the State exempted purchases of utilities used in the

manufacturing process.

– It has also exempted machinery and equipment for some select

industries, but had no across-the-board manufacturing exemption

until 2006 when it enacted an exemption for manufacturing

machinery and equipment used for new and expanded

businesses.

To qualify, an expansion initially had to show an increase in production

of at least 10%, lowered to 5% effective January 1, 2013.

– Also effective January 1, 2013, added an exemption for certain

items used in manufacturing and fabricating aircraft and gas

turbine engines.

33

Florida: Expands Its Manufacturing Exemptions, cont.

Florida House Bill 7007 (2013) expanded the exemption beyond

new and expanded businesses.

– It’s temporary – in effect from April 30, 2014 through April 30, 2017.

– Applies to businesses whose primary business operations at the

location where the machinery and equipment is located falls within

NAICS Codes 31–33.

» The general “manufacturing” codes cover printing, wood

production, manufacturing paper, food, pharmaceuticals, plastic,

etc.

» “Primary” business activity means more than 50% of the activities

conducted at the location.

– Covers industrial machinery and equipment, defined to mean

three-year depreciable property.

– Must be used in an “integral part” in the manufacturing, processing,

compounding, or production of tangible personal property for sale.

34

Florida: Expands Its Manufacturing Exemptions, cont.

– Includes parts and accessories if purchased prior to the date the

machinery and equipment is placed in service.

– Does not include:

Buildings and structural components of buildings unless they are so

closely related to the machinery and equipment that it houses or

supports the machinery and equipment and would be expected to be

replaced when they are.

Heating and air conditioning unless sole justification is to meet

requirements of the production process.

– Florida Department of Revenue (DOR) has posted a sample

Exemption Certificate which the purchaser can issue to the seller.

If the buyer provides a signed exemption certificate, the seller can rely

on it, and the DOR may only go after the buyer if it believes the

transaction did not qualify for the exemption.

35

Florida: Expands Its Manufacturing Exemptions, cont.

While the change is commonly referred to by practitioners as an

“expansion“ of the existing manufacturing exemption, the

Florida Department of Revenue does not view it that way.

– In its most recent policy statement, the Department noted that the

exemption “does not replace the exemption for qualifying

purchases by new or expanding businesses under 212.08(5)(b) &

(d) which remains in effect without change.”

36

Contacts:

Susan Traylor Bittick

Principal and Practice Leader, Public Affairs

Ryan, LLC

512.476.0022

California’s New Partial

Sales Tax Exemption

Stephanie Gilfeather,

Senior Tax Consultant

Deloitte Tax LLP

September 18, 2013

New Partial Sales & Use Tax Exemption

On July 1, 2013, Governor Brown signed into law Assembly

Bill 93 which provides for a statewide partial sales and use

tax exemption for the purchase of manufacturing and

research and development equipment. The exemption is

now codified in Cal. Tax Code

6377.1.

• Exemption applies to the state portion of the sales tax

rate (4.1875%); local and district sales tax rates still apply

• The exemption is available to qualified persons

(as defined), without an application process

• The exemption applies to qualified purchases

beginning July 1, 2014

39

“Qualified Person” – Engaged in a line of business included

in NAICS Codes 3111-3399 and 541711 & 541712

Includes the Following Industries:

Food Manufacturing Cement Manufacturing

Bakeries and Tortilla Manufacturing Steel Product Manufacturing

Beverage Manufacturing Machine Shops

Apparel Manufacturing Computer and Electronics Products

Wood Product Manufacturing Electrical Equipment Manufacturing

Printing Aerospace Products Manufacturing

Petroleum Refining Shipbuilding

Plastic Product Manufacturing R&D in Biotechnology

Medical Equipment Manufacturing R&D in Physical, Engineering and

Life Sciences 40

New Partial Sales & Use Tax Exemption – Qualified Property

Qualified property includes machinery and equipment with a useful life

greater than one year, used primarily (more than 50%) in manufacturing,

processing, fabricating, refining or recycling of tangible personal property,

as well as research and development, anywhere in California • Includes “qualified tangible personal property purchased for use by a

qualified person to be used primarily to maintain, repair, measure, or test

any qualified tangible personal property.” Cal. Tax Code

6377.1(a)(3).

• Special purpose buildings and foundations used as an integral part of the

manufacturing, processing, refining, fabricating, or recycling process, or

that constitute a research or storage facility used during those processes

are eligible. Cal. Tax Code

6377.1(7)(A)(iv).

• Construction contractors furnishing and installing qualified property for

a qualified purposes may also be eligible

41

New Partial Sales & Use Tax Exemption – Considerations

• Effective for purchases beginning July 1, 2014

• Each qualified person is limited to $200 million in purchases

each calendar year. Cal. Tax Code

6377.1(e)(1)(a).

– Purchases in excess of $200 million are subject to tax at the

full tax rate

• Available for leased equipment classified as ‘continuing

sales’ and ‘continuing purchases.’ Cal. Tax Code

6377.1(f).

• Qualifying purchases must remain in California and

be used in a qualified activity for the first 12 months • Qualified purchasers must provide vendors with an

exemption certificate

42

Senate Bill 1128 (“SB 1128”)

SB 1128, enacted on September 27, 2012, provides a

sales and use tax exclusion for “advanced manufacturing”

• Means manufacturing processes that improve existing,

or create entirely new materials, products, and

processes through the use of science, engineering, or

information technologies, high-precision tools and

methods, a high-performance workforce, and

innovative business or organizational models utilizing

in specified technology areas

• Includes micro and nano-electronics, semiconductors,

advanced materials, integrated computational

materials engineering, nanotechnology, additive

manufacturing and industrial biotechnology

43

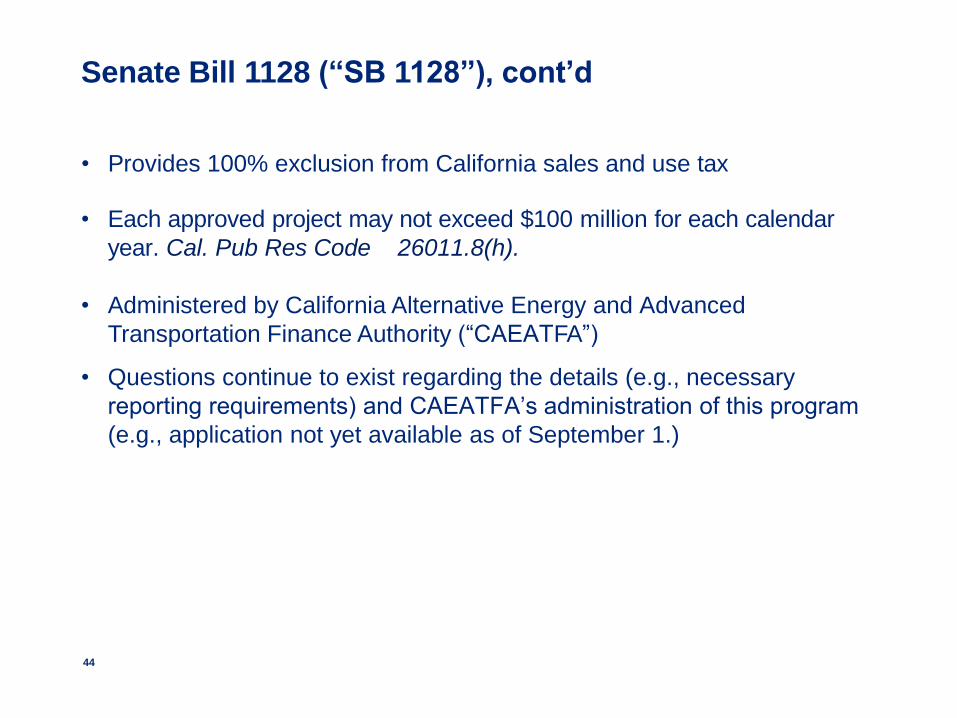

Senate Bill 1128 (“SB 1128”), cont’d

• Provides 100% exclusion from California sales and use tax

• Each approved project may not exceed $100 million for each calendar

year. Cal. Pub Res Code

26011.8(h).

• Administered by California Alternative Energy and Advanced

Transportation Finance Authority (“CAEATFA”)

• Questions continue to exist regarding the details (e.g., necessary

reporting requirements) and CAEATFA’s administration of this program

(e.g., application not yet available as of September 1.)

44

Slide Intentionally Left Blank

JURISDICTIONS WITH BROAD MANUFACTURING EXEMPTIONS

Stephanie Gilfeather, Deloitte Tax

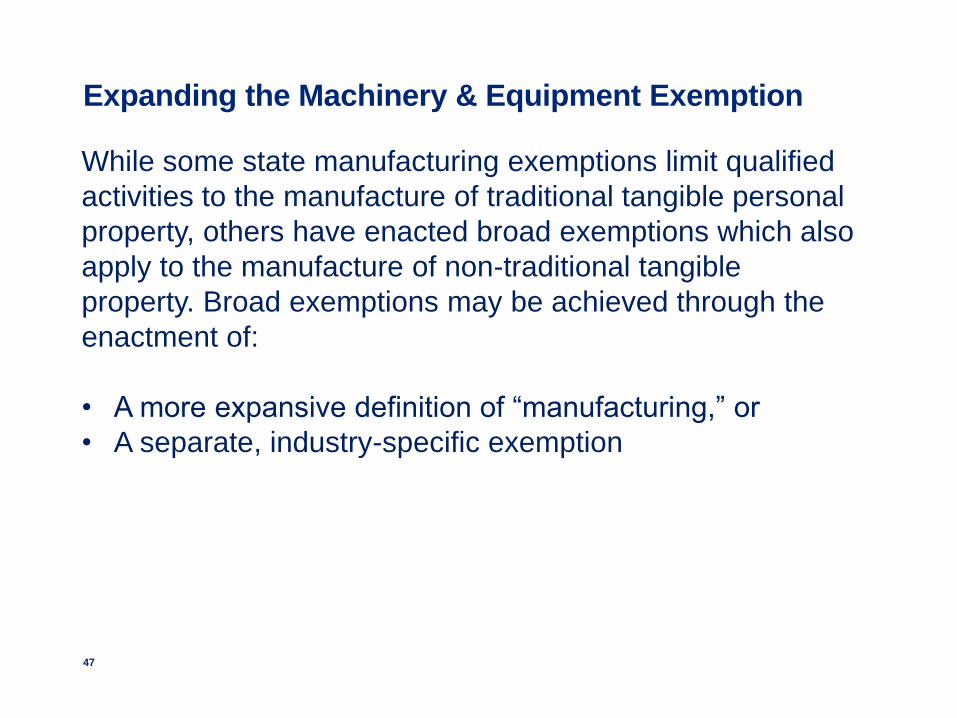

Expanding the Machinery & Equipment Exemption

While some state manufacturing exemptions limit qualified

activities to the manufacture of traditional tangible personal

property, others have enacted broad exemptions which also

apply to the manufacture of non-traditional tangible

property. Broad exemptions may be achieved through the

enactment of:

• A more expansive definition of “manufacturing,” or

• A separate, industry-specific exemption

47

Electricity Production as “Manufacturing”

Examples of states which define electricity production to qualify

as a manufacturing operation:

• Kansas: “Electricity power generation” is included in the list of

“manufacturing or processing business.” K.S.A.

79-

3606(kk)(2)(D).

• New York: “Machinery or equipment for use or consumption

directly and predominantly in the production of…electricity…by

manufacturing, processing” is exempt. N.Y. Tax. Law

1115(a)(12).

• Pennsylvania: “Electricity for non-residential use” is included

in the statutory definition of “tangible personal property,” 72

P.S.

7201(m). The definition of “sale at retail” does not

include “[t]he manufacture of tangible personal property.” 72

P.S.

7201(k)(8)(ii)(A).

48

Exemption for Electricity Used in Manufacturing

These exemptions take a variety of forms.

• Nebraska: “Sales and purchases of such energy sources

or fuels [electricity, coal, gas, fuel oil etc.] are exempt when

more than fifty percent of the amount purchased is for use

directly in processing, manufacturing, or refining.” Neb.

Code.

77-2704.13(2).

• Texas: There is an exemption for “gas and electricity when

used directly in manufacturing.” 34 Tex. Admin. Code

3.300(d)(13).

11

Reduced Levy Upon Receipts from the Sale of

Electricity to a Manufacturer

• Arkansas: “Beginning July 1, 2014, in lieu of the gross receipts or

gross proceeds tax…there is levied an excise tax on gross

receipts or gross proceeds derived from the sale of natural gas

and electricity to a manufacturer for use directly in the actual

manufacturing process at the rate of one percent (1%)” rather

than the gross receipts rate of 2.625%. Ark. Code

26-52-

319(a)(1)(A). On July 1, 2015, the rate will decrease to 0%. Ark.

Code.

26-52-319(a)(1)(B)(i).

11

Telecommunication Services

Certain states exempt machinery & equipment used in the

provision of telecommunications services. Some broadly exempt

all equipment purchased by the telecommunication business

while others exempt only specific equipment listed in the statute.

• Arizona: Arizona provides a broad-based exemption for

“[t]angible personal property sold to persons engaged in

business classified under the telecommunications

classification.” AZ. Rev. Stat.

42-5061(B)(3).

• New York: The exemption is for “[t]angible personal property

for use or consumption directly and predominantly in the

receiving, initiating, amplifying, processing, transmitting,

retransmitting, switching or monitoring of switching of

telecommunications services for sale or internet access

services for sale or any combination thereof.” N.Y. Tax. Laws

1115(a)(12-a). 51

Distribution Industry

Washington provides a partial exemption to “[w]holesalers or third-party

warehousers who own or operate warehouses or grain elevators and

retailers who own or operate distribution centers.” The partial exemption

applies to the state portion of the sales tax rate (3.25%); local and district

sales tax rates still apply. RCW

82.08.820.

• “For grain elevators with bushel capacity of one million but less than

two million, the remittance is equal to fifty percent of the amount of tax

paid.”

• “For warehouses with square footage of two hundred thousand or

more and for grain elevators with bushel capacity of two million or

more, the remittance is equal to one hundred percent of the amount of

tax paid for qualifying construction, materials, service, and labor, and

fifty percent of the amount of tax paid for qualifying material-handling

equipment and racking equipment, and labor and services rendered in

respect to installing, repairing, cleaning, altering, or improving the

equipment.”

52

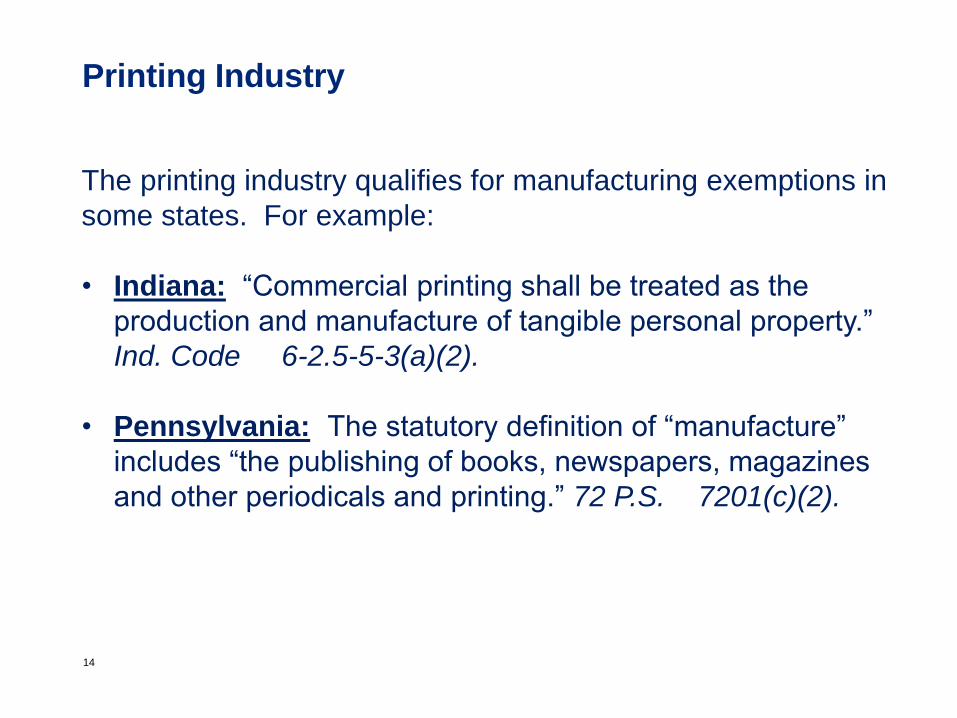

Printing Industry

The printing industry qualifies for manufacturing exemptions in

some states. For example:

• Indiana: “Commercial printing shall be treated as the

production and manufacture of tangible personal property.”

Ind. Code

6-2.5-5-3(a)(2).

• Pennsylvania: The statutory definition of “manufacture”

includes “the publishing of books, newspapers, magazines

and other periodicals and printing.” 72 P.S.

7201(c)(2).

14

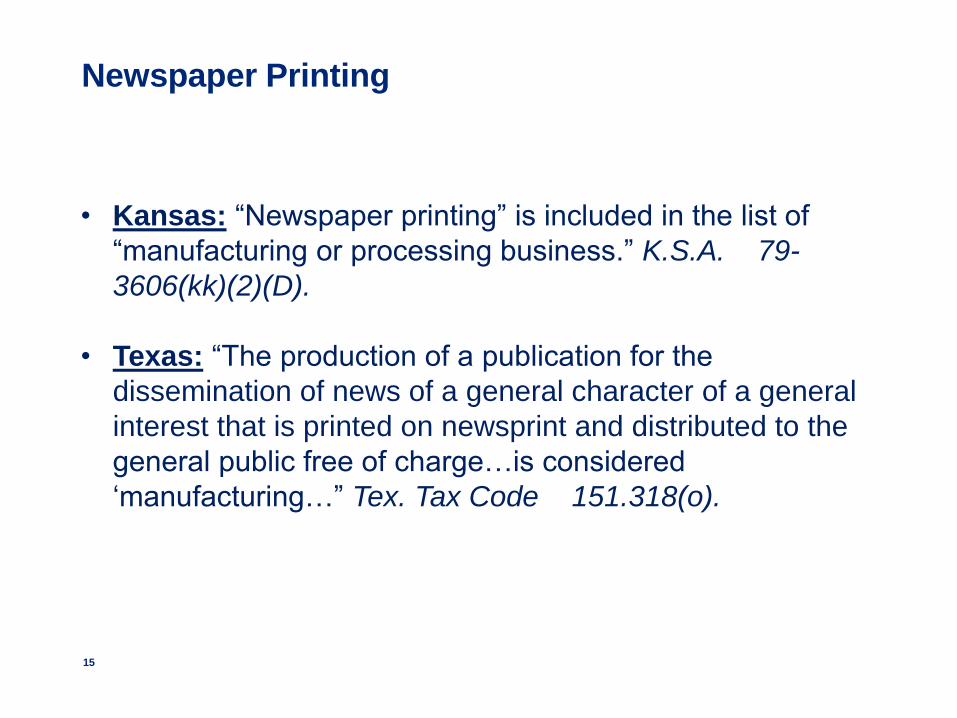

Newspaper Printing

• Kansas: “Newspaper printing” is included in the list of

“manufacturing or processing business.” K.S.A.

79-

3606(kk)(2)(D).

• Texas: “The production of a publication for the

dissemination of news of a general character of a general

interest that is printed on newsprint and distributed to the

general public free of charge…is considered

‘manufacturing…” Tex. Tax Code

151.318(o).

15

Bakeries

Bakeries qualify for a manufacturing or processing

exemption in certain states. For example

• Maryland: “The sales and use tax does not apply to a

sale of equipment that is used by a retail food vendor to

manufacture or process bread or bakery goods for resale

if: (1) the taxable price of each piece of equipment is at

least $2,000; and (2) the retail food vendor operates a

substantial grocery or market business.” MD Code

11-

210(c)(2). A substantial grocery or market business is “a

business at which at least 10% of all sales of food are

sales of grocery or market items, not including food

normally consumed on the premises even though it is

packaged to carry out.” MD Code

11-206(a)(6).

55

Bakeries

• Pennsylvania: The definition of “processing” includes

“cooking or baking of bread, pastries, cakes, cookies,

muffins and donuts”…but only when the baker sells the

items at bakeries and donut shops rather than at an

“establishment from which ready-to-eat food and

beverages are sold. For purposes of this clause, a

bakery, a pastry shop and a donut shop shall not be

considered an establishment from which ready-to-eat

food and beverages are sold.” 72 P.S.

7201(d)(13).

56

Mining & Refining Industry

• Kansas: Manufacturing exemption statute exempts “all sales of

tangible personal property which is consumed in the

production, manufacture, processing, mining, drilling, refining or

compounding of tangible personal property, the treating of by-

products or wastes derived from any such production process,

the providing of services or the irrigation of crops for ultimate

sale at retail within or without the state of Kansas.” K.S.A.

79-

3606(n).

• Pennsylvania: Definition of “manufacturing” includes “refining,

blasting, exploring, mining and quarrying for, or otherwise

extracting from the earth or from waste or stock piles or from

pits or banks any natural resources, minerals and mineral

aggregates including blast furnace slag.” 72 P.S.

7201(c)(3).

57

Video and Movie Production

• New York: “Tangible personal property for use or

consumption directly and predominantly in the production,

including editing, dubbing and mixing, of a film for sale

regardless of the medium by means of which the film is

conveyed to a purchaser. For purposes of this paragraph,

the term ‘film’ means feature films, documentary films,

shorts, television films, television commercials and similar

productions.” N.Y. Tax. Laws

1115(a)(39).

• Texas: Texas has a statutory exemption for “tangible

personal property that is necessary or essential to and used

or consumed in or during: (A) the production of a motion

picture or video or audio recording…; or (B) the production

of a broadcast by or for a cable program producer or by or

for a radio or television station…” Tex. Tax Code

151.3185(2).

58

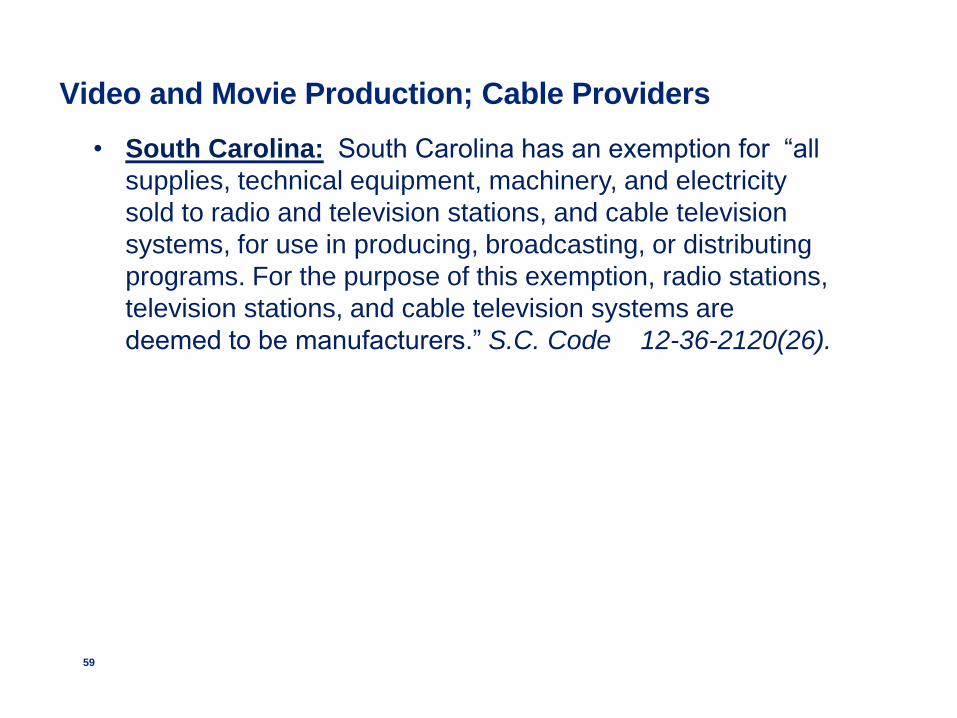

Video and Movie Production; Cable Providers

• South Carolina: South Carolina has an exemption for “all

supplies, technical equipment, machinery, and electricity

sold to radio and television stations, and cable television

systems, for use in producing, broadcasting, or distributing

programs. For the purpose of this exemption, radio stations,

television stations, and cable television systems are

deemed to be manufacturers.” S.C. Code

12-36-2120(26).

59

Agricultural Industry

• California: California exempts “the sale of, and the storage and use of, or

other consumption in this state of, farm equipment and machinery, and the

parts thereof, purchased for use by a qualified person to be used primarily

in producing and harvesting agricultural products.” Cal. Tax Code

6356.5.

• Texas: Machinery and equipment used as follows are exempt from sales

and use tax:

• “exclusively used or employed on a farm or ranch in the building or

maintaining of roads or water facilities or in the production of: (A) food

for human consumption; (B) grass; (C) feed for animal life; or (D) other

agricultural products to be sold in the regular course of business.” Tex.

Tax Code

151.316(7).

• “exclusively used in, and pollution control equipment required as a

result of, the processing, packing, or marketing of agricultural products

by an original producer at a location operated by the original producer

for processing, packing, or marketing the producer’s own products.”

Tex. Tax Code

151.316(8).

60

Data Center Operators

• New York: New York exempts “machinery, equipment and

other tangible personal property…sold to a person operating

an internet data center located in this state for use in such a

center, where such property: (A) will be located or installed in

a facility or structure which is an internet data center and (B) is

required for and directly related to the provision of internet

website services for sale by the operator of the center.” N.Y.

Tax. Laws

1115(a)(37)(i). Certain services are also exempt.

N.Y. Tax. Laws

1115(y).

• Texas: Effective September 1, 2013, tangible personal

property purchased for use at a qualifying data center is

exempt from the sales/use tax by a qualifying owner, qualifying

operator, or qualifying occupant (owner, operator, and

occupant may be the same or different entities). Significant

requirements must be met to qualify for this exemption

61

Data Center Operators (cont’d)

• Virginia: Virginia exempts “computer equipment or

enabling software purchased or leased for the

processing, storage, retrieval, or communication of data,

including but not limited to servers, routers, connections,

and other enabling hardware.” The data center must be

(i) located in a Virginia facility, (ii) result in a new capital

investment of at least $150 million, and (iii) result in the

creation of at least 50 new jobs (or 25 new jobs if the

data center is located in certain high unemployment

areas) by the data center operator and its tenants,

collectively, associated with the operation or

maintenance of the data center. Va. Tax Code 58.1-

609.3(18).

62

Contacts

Stephanie Gilfeather

Senior Tax Consultant, Seattle

206.716.6401,

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering

accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a

substitute for such professional advice or services, nor should it be used as a basis for any decision or action that

may affect your business. Before making any decision or taking any action that may affect your business, you should

consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies

on this presentation.

About this presentation

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member

firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal

structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the

legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of

public accounting.

Copyright © 2013 Deloitte Development LLC. All rights reserved.

Member of Deloitte Touche Tohmatsu Limited

Slide Intentionally Left Blank

EXEMPTIONS FOR ACTIVITIES OUTSIDE OF DIRECT PRODUCTION

Chris Wallace, Weaver

68

Direct Production Exemptions

• Resale exemption

• Applies to property transferred to the purchaser – raw materials, packaging, etc.

• Processing exemption

• Covers equipment and/or consumables that cause a chemical or physical change to the product

69

Indirect Exemptions

• Intraplant transportation equipment

• Pollution control

• Quality control

• Research and development

• Utilities

Slide Intentionally Left Blank

71

States of Interest

• Texas

• New York

• Illinois

• Michigan

• Pennsylvania

• Ohio

• North Carolina

• Virginia

72

Texas Indirect Exemptions

• Pollution control – if directly related to the manufacturing process

• Quality control – does not apply to raw materials

• Safety equipment – apparel worn by manufacturing employees

• Utilities – electricity and gas predominantly used in the manufacturing process

73

Texas Indirect Exemptions

• R&D credit

• Signed into law 6/14/13

• Effective 1/1/14 – 12/31/26

• Choice of franchise tax credit for R&D expenditures or sales tax exemption for equipment and software used in R&D

• Applies to “Qualified research expenses” as defined in IRC Section 41

74

Texas Indirect Exemptions

• R&D credit (cont.)

• Franchise tax credit equals 2.5% of QRE (assuming consistent expenditures)

• Bonus credit for working with institutions of higher learning

• Labor-intensive R&D lends itself towards the franchise tax credit

• Capital-intensive R&D means the sales tax credit may offer more benefit

75

New York Indirect Exemptions

• Pollution control – exempt if used directly and predominantly for waste from a manufacturing or industrial facility

• Utilities – electricity and gas used directly and EXCLUSIVELY in the production process

76

Illinois Indirect Exemptions

• Pollution control – specific exemption for low sulfur dioxide emission coal fueled devices

• Pollution control – additional exemption for TPP exclusively used in a pollution control facility in an Illinois Enterprise Zone

77

Michigan Indirect Exemptions

• Engineering – if related to industrial processing

• Pollution control – processing or recycling of scrap, waste and used materials for disposal or sale

• Quality control – covers all steps prior to the completion of the manufacturing process

• R&D – applies to the development, discovery or modification of a product or a product-related process

78

Pennsylvania Indirect Exemptions

• Intraplant transportation equipment

• Pollution control – for waste generated in the manufacturing process

• Quality control – applies to testing and inspection throughout the production operation

• R&D – if related to producing a new or improved product or manufacturing process

79

Ohio Indirect Exemptions

• Intraplant transportation equipment

• Quality control – applies to raw materials, in-process materials and finished goods

• R&D - if related to producing a new or improved product or manufacturing process

80

North Carolina Indirect Exemptions

• Pollution control – if related to the manufacturing process

• Utilities – electricity and gas used in the manufacturing process

81

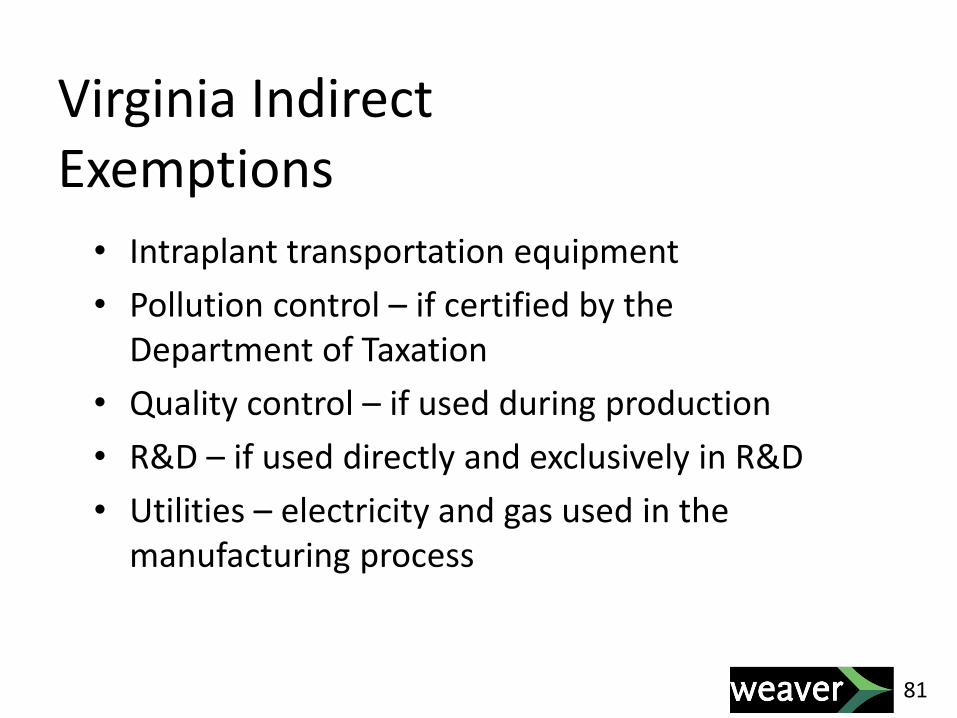

Virginia Indirect Exemptions

• Intraplant transportation equipment

• Pollution control – if certified by the Department of Taxation

• Quality control – if used during production

• R&D – if used directly and exclusively in R&D

• Utilities – electricity and gas used in the manufacturing process