Mangalore Refineries & Petrochemicals Nirmal...

20

Transcript of Mangalore Refineries & Petrochemicals Nirmal...

Please refer to the disclaimer towards the end of the document.

Institutional Equities

Initi

atin

g C

over

age

Reuters: MRPL; Bloomberg: MRPL IN

Mangalore Refineries & Petrochemicals

Headwinds Priced In, Tailwinds Being Ignored Mangalore Refineries & Petrochemicals (MRPL) is all set to join the club of complex refiners by September 2013, but its stock price plummeted 20% since the beginning of 2013 due to: (1) The US-led sanctions against Iran leading to a sustained decline in crude oil sourcing by the company from its chief supplier, (2) Delay in full commercial operations of expanded capacity under phase III, and (3) The government mulling product pricing for refiners on the basis of export parity. We, however, believe that all negatives have been priced in and the stock offers great value for long-term investors - in terms of valuation as well as earnings growth. We have assigned a Buy rating to MRPL with a target price of Rs69 to reflect: (1) Attractive valuation at 1.1x FY14E P/BV (below 1SD from the mean), (2) The Nelson complexity index rising to ~10 from 5.0 before the expansion, (3) Likely increase in gross refining margin (GRM) by US$3-US$4/bbl from 1QFY15E, and (4) Expansion project execution risk receding as the secondary units are expected to come on stream by September 2013.

Refinery complexity to show full potential from September 2013: Commercial operations of secondary units under the phase III expansion have been delayed on account of external and internal problems of MRPL. Our channel checks and interaction with the management revealed that the project is 98% mechanically complete and the full potential of the expansion would be felt by July-August 2013. The most critical element for commissioning of secondary units, the captive power plant, is already generating ~20MW from Unit I and is likely to touch 116MW by mid-September 2013. The mechanical commencement of DCU (delayed coker unit) has taken place and its pre-commissioning is expected to start soon. The polypropylene unit is likely to go on stream by the end of October 2013. We have factored in the impact of full commissioning of the expanded capacity to show results from 4QFY14 with a throughput of 14.5mt/15.30mt/15.30mt for FY14E/FY15E/FY16E.

Sustained decline in crude oil sourcing from Iran: MRPL enjoyed the advantage of ~90-day credit facility from Iran, which boosted its GRM by US$1/bbl. Our GRM estimate considers negligible value from this facility. MRPL is aggressively changing its crude oil basket by replacing Iranian crude with crude from Oman, Dubai and Venezuela. The usage of Iranian crude oil dropped from 124kbpd in FY12 to ~76kbpd in FY13E. The management sees no risk to its throughput guidance in the event of stopping Iran crude oil imports completely, although such a scenario is unlikely. The Petroleum and Natural Gas minister recently said the government has no intention to stop crude oil imports from Iran and it plans to create Rs20bn energy insurance pool to resolve the insurance predicament facing Indian refiners.

Outlook and valuation: We have assigned a Buy rating to MRPL with a target price of Rs69 to reflect: (1) Attractive valuation of 1.1x FY14E P/BV (below 1SD from the mean), (2) Negatives from Iran crude oil exposure priced into our GRM assumption, assigning zero value to the increased credit facility benefit, (3) Completion of phase III expansion after a nearly 24-month delay (4) Benefits of higher complexity level likely to reflect from 4QFY14, and (5) The stock price implying a 23% discount to India refinery replacement value and a 45% discount compared to global refiners.

BUY

Sector: Oil & Gas

CMP: Rs48

Target Price: Rs69

Upside: 43%

Ashutosh B [email protected] +91 22 3926 8110

Vivek Sarin [email protected] +91 22 3926 8176

Key Data

Current Shares O/S (mn) 1752.6

Mkt Cap (Rsbn/US$bn) 85.6/1.6

52 Wk H / L (Rs) 74/48

Daily Vol. (3M NSE Avg.) 390,321

Shareholding (%) 4QFY13 3QFY13 2QFY13

Promoter 88.6 88.6 88.6

FII 1.1 0.9 1.0

DII 2.9 2.9 2.7

Corporate 1.0 1.1 1.2

General public 6.6 6.6 6.5

One Year Indexed Stock Performance

Price Performance (%)

1 M 6 M 1 Yr

MRPL (2.8) (25.6) (21.7)

Nifty Index 1.6 2.7 9.5

Source: Bloomberg

Y/E March (Rsmn) FY11 FY12 FY13E FY14E FY15E

Net sales 388,869 537,703 658,531 696,036 619,821

YoY (% ) 21.7 38.3 22.5 5.7 (10.9)

EBITDA 20,483 16,366 9,647 22,782 34,493

EBITDA margin (%) 5.3 3.0 1.5 3.3 5.6

Net profit 11,766 9,086 (3,097) 7,095 15,429

EPS 6.21 4.94 (1.77) 4.05 8.80

RoAE (%) 19.4 13.2 (4.4) 9.9 19.1

RoACE (%) 13.5 7.3 (16.0) 5.5 10.6

P/E (x) 7.9 9.9 (27.7) 12.1 5.6

EV/EBITDA (x) 3.9 9.0 16.1 6.9 4.2

Source: Company, Nirmal Bang Institutional Equities Research

70

80

90

100

110

120

Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13 Apr-13

MANGALORE REFINE NSE CNX NIFTY INDEX

29 April 2013

Institutional Equities

2 ONGC Mangalore Refineries & Petrochemicals

Increased Nelson complexity to expand GRM Post phase III expansion, Nelson complexity would increase to ~10 from 5.0 pre-expansion, leading to higher distillate yield of ~80% from 73% earlier, on the back of commencement of secondary units and the polypropylene unit. We expect the GRM to improve by US$3.5-US$4.0/bbl on the cumulative effect of higher TAN crude oil processing ability, higher distillate yield, savings from SPM (single-point mooring) and earnings from the polypropylene unit, although the total effect would be pruned by US$1.5/bbl after considering the impact of Iran crude oil sourcing and export parity pricing. We have assumed GRMs at US$3.80/US$5.75/US$7.0 for FY13E/FY14E/FY15E, respectively.

Phase III expanded capacity likely to come on stream in September 2013

The phase III expansion, which was scheduled to start in October 2011 but was delayed due to several external and internal problems, is now likely to begin from September 2013. Equipment constraints in respect of the captive power plant have been resolved by Bharat Heavy Electricals’ (BHEL) and one unit of the power plant has already starting operations by generating 20MW and is likely to produce entire 116MW by September 2013. All secondary units, SPM and the polypropylene unit are expected to be operational by Oct 2013.

We have considered Brent crude oil price estimates of US$110/US$105/US$100 for FY13E/FY14E/FY15E, respectively, and India rupee-US dollar exchange rate of Rs54.5/Rs52.0/Rs51.0 per $ for FY13E/FY14E/FY15E, respectively, which leads to the decline in revenue for FY15E despite higher throughput and expanding GRM.

Exhibit 1: One-year forward P/BV Exhibit 2: One-year forward average P/BV

Source: Bloomberg, Nirmal Bang Institutional Equities Research Source: Bloomberg, Nirmal Bang Institutional Equities Research

0.8

1.3

1.8

2.3

2.8

3.3

3.8

Ap

r-0

9

Jun

-09

Au

g-0

9

Oct

-09

De

c-0

9

Fe

b-1

0

Ap

r-1

0

Jun

-10

Au

g-1

0

Oct

-10

De

c-1

0

Fe

b-1

1

Ap

r-1

1

Jun

-11

Au

g-1

1

Oct

-11

De

c-1

1

Fe

b-1

2

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

De

c-1

2

Fe

b-1

3

Ap

r-1

3

(x)

Current P/BV Avg.P/BV 1SD 2SD -1SD -2SD

0

20

40

60

80

100

120

140

160

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-1

1

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Jun

-12

Jul-1

2

Au

g-1

2

Se

p-1

2

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3

(Rs)

Max 3.4x Min 1.2x Avg 2.0x 1.6x 2.7x Daily price

Institutional Equities

3 ONGC Mangalore Refineries & Petrochemicals

Investment Arguments

Refinery entering complexity league

Post phase III expansion, MRPL’s refinery throughput is expected to increase to 15.0mt from 11.8mt before expansion and upgradation. Our channel checks and interactions with the management indicate that the phase III expansion project is 98% mechanically complete and is expected to be commissioned by July-August 2013, with most secondary units and the polypropylene unit set to commence commercial operations by October 2013. We expect the full benefits from expanded capacity to commence from 4QFY14. We have projected refinery throughput at 14.5mt/15.3mt/15.3mt for FY14E/FY15E/FY16E, respectively, which implies refinery capacity utilisation of 102% for all respective years compared to the past five years’ average of 110%. The management has given guidance of refinery throughput at 14.5mmt for FY14E.

Exhibit 3: Refinery throughput and capacity utilisation

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 4: Phase III expansion project and current status

Unit Capacity Status of commissioning

CDU/VDU (crude oil distillation unit/vaccum distillation unit)

3 mmtpa Commissioned in March 2012

PFCC(petro fluidised catalytic cracking) 2.2 mmtpa Likely to be commissioned by September 2013

DCU(Delayed coker unit) 3 mmtpa Mechanical completion done, pre-commissioning phase to

begin in September 2013

DHDT(diesel hydro-treating unit) 3.7 mmtpa Commissioned in November 2012

CHT(coker heavy gas oil hydro-treating unit) 0.65 mmtpa Likely to be commissioned in July 2013

Hydrogen generation unit (HGU) 70 ktpa Commissioned in April 2012

Sulphur recovery unit 3*185tpd Train 1 commissioned, rest two trains to be commissioned by

August 2013

ATF treatment unit 70tph -

Polypropylene unit 0.44 mmtpa Likely to be operational in October 2013

Captive power plant 118MW Currently generating 20MW, rest of the units to operational

by September 2013

Tankage 23 nos. -

Mounded bullets 04 nos. -

Source: Nirmal Bang Institutional Equities Research

0

20

40

60

80

100

120

140

0

2

4

6

8

10

12

14

16

18

FY08 FY09 FY10 FY11 FY12 FY13E FY14E FY15E

(%)(mmt)

Installed capacity Crude oil throughput Utilisation rate (RHS)

Institutional Equities

4 ONGC Mangalore Refineries & Petrochemicals

Exhibit 5: Refinery expansion - Main contractors

Contractor Project undertaken

Technip Design, engineering, supply and installation of fired heater in major units

Jacobs Providing EPC management consulting service for CDU/VDU project

Toyo Engineering EPC contract on lumpsum turnkey basis for setting up the BoP of delayed coker unit

Larsen & Toubro Design, detailed engineering procurement, supply, construction, installation, testing and commissioning of

diesel hydro-treating unit, and hydrogen generation unit

Punj Lloyd Construction of petro fluid catalytic cracking unit

Maire Technimont Heavy coker gas oil hydro-treating unit

Source: Nirmal Bang Institutional Equities Research

Post phase III expansion, which comprises installation of secondary units (to enhance distillate yield) and the polypropylene unit, the Nelson complexity index would increase to ~10.0 from 5.0 currently. The expansion in Nelson complexity index and synchronisation of the polypropylene unit will result in US$3.5-US$4.0/bbl expansion in GRM. Despite attractive valuation, the market has been apprehensive about the stock on account of execution risks in phase III expansion, which has been delayed by almost 24 months. As per the original schedule, Phase III expansion project was supposed to commence from October 2011, but a host of external and internal problems led to the delay. The reasons cited were BHEL’s inability to deliver necessary equipment for the captive power plant and also the emergence of labour problems subsequently.

Our channel checks and interactions with the management indicate that all secondary units under the expansion project would start operations in July-August 2013, with the polypropylene unit expected to start operations in October 2013. BHEL has delivered all units of the captive power plant (CPP), which is already generating 20MW and is likely to touch 116MW by the end of September 2013. Clarity emerging on commissioning of the power plant raises the likelihood of phase III expansion project being commissioned, as being an integrated operation the power plant would facilitate co-generation of power and steam.

Post expansion, the distillate yield would increase to ~80% from 73% prior to expansion. As of 3QFY13 end, the refiner witnessed distillate yield of 76.8% from 75.3% a quarter ago. MRPL expects to commission the project in July-August 2013, with the plant integration likely to be complete by September 2013. As the time lag between the trial run and commercial production would be around one month, the full impact of the expansion would be witnessed only from 4QFY14.

Exhibit 6: Refinery expansion update

3QFY12 4QFY12 1QFY13 2QFY13 3QFY13 4QFY13

Refinery commissioning

Percentage completion 91.5 94.7 95.4 96.4 97.8 98.0

Commissioning guidance Likely to be

commissioned by 15 January 2012

Likely to be commissioned by 15

May 2012 - - - -

Polypropylene unit

Percentage completion 74.3 - 81.6 83.5 85.0 -

Commissioning guidance To be operational by

15 January 2012 Likely completion by

December 2012 -

To be operational by January -

February 2013 -

Commissioning likely by October

2013

CDU/VDU/CHDT

Commissioning guidance Mechanical

completion by March 2012

CDU/VDU commissioned in March 2012, Diesel

hydro-treater and hydrogen-treater to be

commissioned, last unit to be completed by

October 2012

Hydrogen unit completed and

DHDT is nearing completion

DHDT to be completed by the

second week of November 2012

DHDT completed -

Single-mooring project

Commissioning guidance VLCC tanker to be

taken on charter by May 2012

Completion by July 2012 94.6% complete, to be operational by August 2012

96.7% completed, to be operational by November 2012 by

taking on charter Aframax, Suezmax

vessels

Trial operation on 3 January 2013, expected to be

fully operational by February 2013

Likely to start operations from 15

May 2013, full impact of SPM after ISRL builds 48”sub-

sea pipeline

Source: Stock exchange filings, company

Institutional Equities

5 ONGC Mangalore Refineries & Petrochemicals

Looking to aggressively expand its crude oil basket beyond Iran

After the US and the EU imposed sanctions on Iran, MRPL reduced crude oil sourcing from Iran. MRPL met ~55.0%-58.0% of its crude oil requirement from Iran in FY11, which declined to ~48.0% in FY12 and is likely to touch 26.5% in FY13E. Iranian crude oil provided MRPL with the twin benefits of a long-term arrangement for crude oil sourcing along with a 90-day credit period, leading to a positive impact on its GRM by ~US$1/bbl.

We believe the continuous decline in MRPL’s stock price factors in the impact on its GRM following sanctions on Iran. The company is aggressively looking at replacing its crude oil basket with crude from Oman, Dubai, Saudi Arabia and Venezuela. The management is confident that there will be no risk to its FY14 throughput guidance even if crude oil sourcing from Iran is stopped altogether. The street’s sensitivity to crude oil sourcing appears exaggerated as there is no dearth of suppliers, given the general supplier credit period of 25-30 days. Given that post expansion, MRPL will be able to process higher acid crude, it will have the liberty to source more grades of crude oil (particularity lower API and higher sulphur content oil). MRPL’s refinery would be able to source crude oil grades up to 28 API compared to 33.7 before the phase III expansion.

Our interaction with MRPL’s management and the MoPNG (Ministry of Petroleum & Natural Gas) reveals slim chances of Iran crude oil sourcing coming to a grinding halt. In February 2013, Indian refineries imported close to 259,000bpd of crude oil from Iran, down 43% from same month a year ago, although the government planned to import 310,000 bpd of crude oil from Iran in FY13. Indian refineries ‘usage of crude oil from Iran reduced to 7.3% in FY13 from 11.0% in FY12. Despite global pressure, the government plans to import ~124,000 bpd of Iranian crude oil in FY14E. MRPL is likely to import ~35,000bpd-40,000bpd of Iranian crude oil in FY14E and the government is preparing a Rs20bn Energy Insurance Pool (EIP) to back Indian firms that insure domestic refineries processing Iranian crude oil. For claims beyond Rs20bn, the government would extend sovereign guarantee up to Rs100bn.

Exhibit 7: Crude oil sourcing beyond Iran

Bought around 650,000bbl of upper Zakum grade during May 1-15, 2013

Crude oil imports from Iran likely to be brought down to 80,000bpd by FY14E

Bought 1.15mn bbl of sour crude though tenders in October 2012

Bought 550,000bbl of Dubai crude oil from BP at a premium of US$1.25/bbl to Dubai crude

Bought 600,000bbl of Omani crude oil from Itochu at a premium of US$2.50/bbl to Dubai crude

For the first time, entered into an annual crude oil deal with Iraq

Short –term crude oil supply arrangement with Azerbaijan Socar

Bought 650,000bbl each of Oman & Banaco Arab medium crude oil from Shell

Purchased 650,000bbl of Yeman's low sulphur Masila crude from Arcadia Petroleum

Increased the size of annual crude oil supply contract with Saudi Aramco to 55,000bbl until FY14

Source: Media reports

Exhibit 8: Crude sourcing from Iran

Year mmt bpd Throughput (mmt) Throughput (bpd) % of throughput

FY10 7.3 146,897 12.5 250,000 58.8

FY11 7.1 142,000 12.6 252,800 56.2

FY12 6.2 124,000 12.8 256,400 48.4

FY13E 3.8 76,000 14.3 286,400 26.5

Source: Nirmal Bang Institutional Equities Research

Exhibit 9: India’s crude oil imports

Iran crude oil sourcing fell to 259,00bpd in February 2013, down 43% from a year ago

The government plans to import 310,000bpd of Iranian crude oil in FY13E

Crude oil imports from Iran fell to 7.3% in FY13E from 11% in FY12

Indian refiners plan to import 124,000 bpd Iranian crude oil in FY14E

Crude oil imports from Latin America rose to 17.3% in 2012 from 9.5% a year ago

Source: Media reports

Institutional Equities

6 ONGC Mangalore Refineries & Petrochemicals

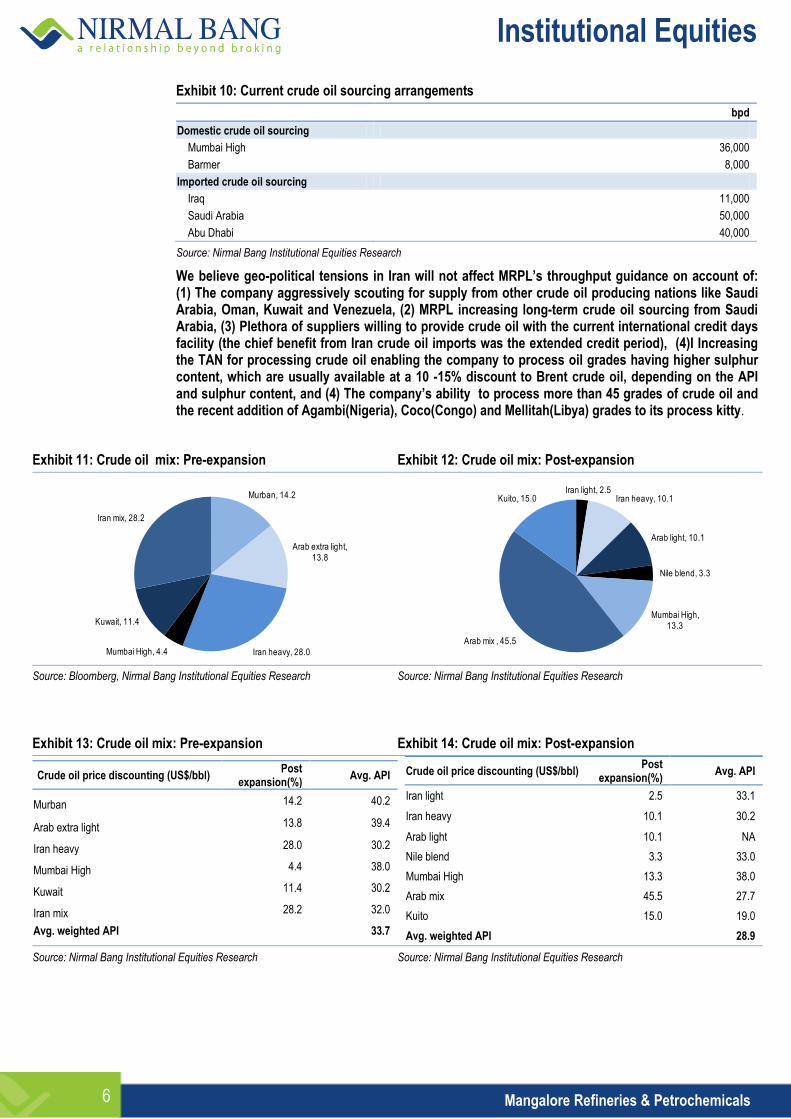

Exhibit 10: Current crude oil sourcing arrangements

bpd

Domestic crude oil sourcing

Mumbai High 36,000

Barmer 8,000

Imported crude oil sourcing

Iraq 11,000

Saudi Arabia 50,000

Abu Dhabi 40,000

Source: Nirmal Bang Institutional Equities Research

We believe geo-political tensions in Iran will not affect MRPL’s throughput guidance on account of: (1) The company aggressively scouting for supply from other crude oil producing nations like Saudi Arabia, Oman, Kuwait and Venezuela, (2) MRPL increasing long-term crude oil sourcing from Saudi Arabia, (3) Plethora of suppliers willing to provide crude oil with the current international credit days facility (the chief benefit from Iran crude oil imports was the extended credit period), (4)I Increasing the TAN for processing crude oil enabling the company to process oil grades having higher sulphur content, which are usually available at a 10 -15% discount to Brent crude oil, depending on the API and sulphur content, and (4) The company’s ability to process more than 45 grades of crude oil and the recent addition of Agambi(Nigeria), Coco(Congo) and Mellitah(Libya) grades to its process kitty.

Exhibit 11: Crude oil mix: Pre-expansion Exhibit 12: Crude oil mix: Post-expansion

Source: Bloomberg, Nirmal Bang Institutional Equities Research Source: Nirmal Bang Institutional Equities Research

Exhibit 13: Crude oil mix: Pre-expansion Exhibit 14: Crude oil mix: Post-expansion

Crude oil price discounting (US$/bbl) Post

expansion(%) Avg. API

Murban 14.2 40.2

Arab extra light 13.8 39.4

Iran heavy 28.0 30.2

Mumbai High 4.4 38.0

Kuwait 11.4 30.2

Iran mix 28.2 32.0

Avg. weighted API

33.7

Crude oil price discounting (US$/bbl) Post

expansion(%) Avg. API

Iran light 2.5 33.1

Iran heavy 10.1 30.2

Arab light 10.1 NA

Nile blend 3.3 33.0

Mumbai High 13.3 38.0

Arab mix 45.5 27.7

Kuito 15.0 19.0

Avg. weighted API

28.9

Source: Nirmal Bang Institutional Equities Research Source: Nirmal Bang Institutional Equities Research

Murban, 14.2

Arab extra light, 13.8

Iran heavy, 28.0Mumbai High, 4.4

Kuwait, 11.4

Iran mix, 28.2

Iran light, 2.5Iran heavy, 10.1

Arab light, 10.1

Nile blend, 3.3

Mumbai High, 13.3

Arab mix , 45.5

Kuito, 15.0

Institutional Equities

7 ONGC Mangalore Refineries & Petrochemicals

Increased Nelson complexity to expand GRM

Post phase III expansion and upgradation, MRPL’s refinery capacity would increase to 15.0mmt from 11.8mmt and Nelson complexity would rise to ~10 from 5 before the expansion, and commencement of operations by the secondary units would help the company to process higher acid crude oil. We expect the GRM to improve by US$3.5-US$4.0/bbl on the cumulative effect of: (1) The rise in Nelson complexity to ~10, (2) Secondary units like DCU, PFCC, DHDT increasing the distillate yield to ~80% from 73% currently, (3) Sulphur recovery unit to enable the processing of more acidic crude oil, and (4) Severity to polypropylene rising to 20% compared to 10%-12% global average, thereby providing more polypropylene volume without comprising on the quality.

We expect GRMs of US$3.80/US$5.95/US$7.00 per bbl for FY13E/FY14E/FY15E, respectively, after considering the erosion in its working capital advantage due to reduced Iran crude oil sourcing together with the probable impact of export parity pricing. We expect the company’s GRMs to remain at a discount to benchmark Singapore refining margins in FY13/FY14, with the spread likely to narrow once all the benefits of complexity kick in. We expect Singapore refining margins at US$7.3/US$6.8 for FY14E/FY15E, respectively, compared to US$7.8/bbl in FY13E. We expect refining margins to remain under pressure, with nearly ~7.2mb/d of refining capacity coming up globally, thereby keeping the utilisation level depressed.

Exhibit 15: Refining margin Exhibit 16: Quarterly Singapore complex GRM

Source: Company, Reuters Source: Reuters

Exhibit 17: Monthly Singapore complex GRM

Source:Reuters

0

1

2

3

4

5

6

7

8

9

FY10 FY11 FY12 FY13E FY14E FY15E

(US$/bbl)

Singapore complex margin MRPL refining margin

4

5

6

7

8

9

10

11

12 M

ar-

11

Ma

y-1

1

Jul-1

1

Se

p-1

1

No

v-1

1

Jan

-12

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Se

p-1

2

No

v-1

2

Jan

-13

Ma

r-1

3

(US$/bbl)

Quarterly GRM Average GRM

0

2

4

6

8

10

12

Jan

-11

Ma

r-1

1

Ma

y-1

1

Jul-1

1

Se

p-1

1

No

v-1

1

Jan

-12

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Se

p-1

2

No

v-1

2

Jan

-13

Ma

r-1

3(US$/bbl)

Institutional Equities

8 ONGC Mangalore Refineries & Petrochemicals

As per the Organisation of Petroleum Exporting Countries’ (OPEC) energy outlook, around 7.2mb/d of new crude oil distillation capacity would be added to the global refining system until 2016. The major portion of this new capacity is expected to materialise in Asia, mainly in China and India, together accounting for more than 40%, or 3.2mb/d, of additional capacity. China alone would expand its refining sector by more than 2mb/d, in line with the objective specified in its 12th Five Year Plan. The speed of expansion in India, however, seems to be slowing down with the change in the tax rate policy.

As regards the other three regions with likely highest capacity addition until 2016 - Middle East, Latin America and FSU (former Soviet Union) - the drivers are a combination of local demand and polices aimed at capturing the demand for value-added products through domestic refining operations.

Exhibit 18: Distillation capacity addition in existing projects - 2012-16

Note: OPEC energy outlook

In the Middle East, demand is expected to grow by 0.6mb/d in the medium term, whereas crude oil distillation capacity is likely to rise by 1.8mb/d. In Latin America, the demand is expected to increase by 0.5mb/d versus 0.8mb/d additional distillation capacity and FSU to witness expansion in demand of only 0.2 mb/d compared to 0.5mb/d, primarily driven by the polices designed to encourage the export of products rather than crude oil. Based on the above, it is clear that new refineries in Middle East could have a major impact on inter-regional product movement, at least in the medium term.

-

0.5

1.0

1.5

2.0

2.5

US & Canada

Latin America

Africa Europe FSU Middle East

China Other Asia

(mnbpd)

Institutional Equities

9 ONGC Mangalore Refineries & Petrochemicals

Exhibit 19: Refinery capacity addition in Asia

Company Capacity (kbpd)

2012

PetroChina 100

Sinopec Qingdao 40

Sinopec Anqing 50

Sinopec Jinling 100

Sinopec, Shanghai 80

HPCL, Bhatinda 180

Essar Vadinar 120

Total 670

2013

PetroChina, Huabei 100

PetroChina, Sichuan 200

Sinopec, Shijiazhuang 80

Sinopec, Fujian 40

Sinopec, Maoming 130

Sinopec Wuhan 40

Byco, Pakistan 120

MRPL, India 60

Total 760

2014E

PetroChina, Lianing 200

PetroChina, Henan 200

CNPC, Tianjin 261

CNPC, Jieyang 400

Sinopec, Tangshan 200

Sinopec, Jiangsu 90

Sinopec, Henan 160

Sinopec, Gaoqiao 240

Sinochem, Quanzhou 240

IOC, Paradip 300

Nargarjuna, Cuddalore 120

Total 2,411

2015E

PetroChina, Yunan 200

Sinopec Shandong 200

Sinopec Jiejiang 300

CNOOC Huizhou 200

Dung Quat, Vietnam 70

Nghi son, vietnam 200

Total 1,170

Source: Nirmal Bang Institutional Equities Research

Exhibit 20: Refinery expansion in the Middle East (2012-16)

Jubail, Saudi Arabia

Yanbu, Saudi Arabia

Ruwais, UAE

Karbala, Iraq

Isfahan, Iran

Rabigh, Saudi Arabia

Jizan Industrial city, Saudi Arabia

Ras Tanura, Saudi Arabia

Al Zour, Kuwait

Iraq building four new units having a total capacity of 0.75mb/d

UAE plans refinery at Fujairah

Oman considering 230,000b/d refinery at Duqm

Institutional Equities

10 ONGC Mangalore Refineries & Petrochemicals

Additional refining capacity of 1.8mb/d in 2012-16 by other countries

Source: OPEC energy outlook

Future refinery capacity utilisation rate prospects are often seen as good indicators of margins and thereby the profitability in the refining business. Utilisation rate depends on a set of factors that comprise development in demand for refined products, including their mix, the structure of available feedstock, existing refinery capacity and changes therein. The GRM increase in 4QFY13 is largely attributed to the significant number of outages that took place, which led the Singapore complex margin to top US$10/bbl. The key reason for GRM expansion in 2012 and in the first-half of 2013 was high net refining shutdown, which means refining shutdowns were more than refining restarts, thereby leading to low supply in the market. In 2012, net refining shutdown stood at 1,052kbpd and first-half of 2013 is believed to have witnessed 1,056kbpd shutdown. In 2012, refining restarts were to the extent of 3424kbpd and refining shutdown at 4,476kbpd, while in the first-half of 2013 refining restarts are likely to the extent of 1204kbpd and refinery shutdowns at 2,250kbpd, thereby holding the capacity utilisation rate in the first-half of 2013.

Exhibit 21: Refinery maintenance shutdown Exhibit 22: Global crude oil demand, refining capacity & crude runs

Source: Nirmal Bang Institutional Equities Research Source: Nirmal Bang Institutional Equities Research

The most critical factor for the utilisation rate is the number of closures offsetting the impact of additional capacity. Cumulative capacity closures since 2008, including known closures announced in 2013 and 2014, have already reached 4mb/d and are heading towards the 5mb/d mark, as currently there are at least 15 refineries on sale globally. The paradigm shift that the refining sector has seen is closure. The largest closures are in Europe, with ~1.7mb/d closed (0.45mb/d in Germany, 0.4mb/d in the UK, ~0.4mb/d in France and 0.3mb/d in Italy).

Exhibit 23: Global refinery closures

Cumulative capacity closure since 2008, including those announced in 2013/14, touched 4mb/d

Closures could touch 5mb/d, as at least 15 refineries are believed to be on sale globally

Europe

Around 1.7mb/d of capacity closed in Europe, of which 0.45mb/d each in Germany/UK, and 0.4mb/d in France

Japan

More than 0.8mb/d of capacity closed

Closure mainly due to the new guideline for meeting the cracking to crude distillation ratio of 13% by March 2014

Meet requirement refiners either closed distillation unit or increase residue upgrading

Nippon Oil shut down 0.26mb/d of capacity in June 2012 and another 0.25mb/d of capacity to be shut by 2014

China

China raised minimum capacity limit to 40,000b/d

With effect from 2014, anything below 40,000b/d capacity to be closed down

US and Canada

Between 2010 and 2011, five refineries closed on the East coast

Two other refineries, Sunoco in Philadelphia and Phillips66 in Trainer ,witnessed a narrow escape from closure

Source: OPEC energy outlook

-

1,000

2,000

3,000

4,000

5,000

6,000

J F M A M J J A S O N D

5-yr average 2012 2013

50

60

70

80

90

100

1980 1985 1990 1995 2000 2005 2010 2015 2016

(mnbpd)

Crude runs Oil demand Distillation capacity

Institutional Equities

11 ONGC Mangalore Refineries & Petrochemicals

Exhibit 24: Cumulative refinery capacity closure (2008-14) Exhibit 25: Global oil demand, refining capacity and crude runs

Source: OPEC energy outlook Source: OPEC energy outlook

The situation for the refining sector, in terms of average utilisation rate, would not change significantly over the medium term. It is critical, however, to recognise that this relatively balanced increase in refining capacity and demand for refined products is happening in the context of the industry experiencing a capacity surplus that has been gradually building up since 2009. In the years that immediately followed, crude oil demand gradually recovered and with that crude runs, although the pace of crude run growth was slower because of increasing non-crude supplies (ethanol and natural gas liquids, in particular).

The closure of around 5mb/d of capacity across the US, Europe, Japan and other places so far has primarily removed surplus capacity and it had little impact on margins. Shutting down a further 2mb/d for a combined total 7 mb/d should lead to improved margins as global refinery utilisation rates in this case would then increase to 82%, but it is potentially misleading to infer refining margins purely as function of distillation capacity utilisation. As per OPEC, in order to restore the refining margin to long-term viable level, it is necessary to exclude much more than 7 mb/d from the market, which would then restore the utilisation rate to 82%. Thus, closure to the extent of 10 mb/d is required to touch global refinery utilisation rate of 85%. It should be noted that global refinery utilisation rate has not touched 85% since 1980.

We have projected GRMs of US$3.8/US$5.95/US$$7.00 per bbl for FY13E/FY14E/FY15E, respectively. MRPL’s management has given guidance of GRM improvement of US$3.5-US$4.0/bbl once the entire phase III expanded capacity is commissioned. We expect improvement in the GRM on account of multiple levers such as: (1) Light- heavy crude oil upgrade to provide an incremental US$1.5/bbl to GRM, (2) Increase in distillate yield to 80% from 73% to offer a positive delta of US$0.5/bbl, (3) Polypropylene having a severity of 20% compared to global average of 10%-12% to give higher quantity, while maintaining the quality to add another US$1.5/bbl, (4) Single mooring point will give the advantage of saving US$0.5/bbl as the company would be served by VLCCs (very large crude carriers) compared to the current procurement via Aframax grade tankers, and (5) MRPL enjoying deferred VAT payment facility on products except gasoline/diesel, which would be ultimately paid after 15 years.

Exhibit 26: GRM bridge for FY15E

Source: Nirmal Bang Institutional Equities Research

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014

(mnbpd)

Europe US & Canada Asia Latin America

0

2

4

6

8

10

1990 1995 2000 2005 2010 2015

(mnbpd)

Effect of refinery closures

5.0

7.0

1.50 0.50

1.00 0.50 (1.00)

(0.5)

0

1

2

3

4

5

6

7

8

9

Core GRM before

expansion

Light-Heavy crude oil

advantage

Distillate improvement

Polypropylene effect

SPM advantage

Iran sourcing Export parity Core GRM

(US$/bbl)

Institutional Equities

12 ONGC Mangalore Refineries & Petrochemicals

Exhibit 27: Refinery product slate comparison

Pre-expansion Post-expansion

Production (mmt) % of total Production (mmt) % of total

LPG 0.3 2.6 1.01 7.1

Gasoline 1.19 10.1 1.17 8.3

Mixed xylene 0.08 0.7 0.25 1.7

Naphtha 0.9 7.6 1.14 8.0

Light distillate 2.47 21 3.57 25.1

Kerosene 0.34 2.9 1.05 7.4

Diesel 5.28 44.9 5.75 40.6

ATF 1.09 9.2 2.06 14.6

Middle distillate 6.71 57 8.86 62.6

FO 2.27 19.3 0.57 4.0

LSHS 0.01 - 0.22 1.5

Bitumen 0.21 1.8 0.23 1.7

CRMB 0.04 0.3 - -

Sulphur 0.06 0.5 0.25 1.8

Heavy ends 2.59 21.9 1.27 9

Polypropylene - - 0.45 3.2

Total 11.77 100 14.15 100

Light distillate to total - 21.0 - 25.2

Middle distillate to total - 57.0 - 62.6

Heavy ends - 22.0 - 9.0

Source: Nirmal Bang Institutional Equities Research

Exhibit 28: SPM project details

Project Amount to be spent

(Rsmn) Capex distribution

SPM sys & 48"sub-sea pipeline 3,640 Entire capex to borne by MRPL

Cavern storage 2,200 Capex in the ratio of 1:4, with Indian strategic resources

Booster pumping system 1,300 Entire capex to borne by MRPL

36" pipeline to refinery 280 Entire capex to absorbed by MRPL

Land development and oil spill management

70 Entire capex to absorbed by MRPL

Sub-total 7,490

Other 3,000 Shared between MRPL and Indian strategic resource

ltd(ISRL)

Total 10,490

Source: Nirmal Bang Institutional Equities Research

Exhibit 29: Factors behind GRM expansion

Project Pre-expansion Post-expansion

Nelson complexity 5.00 10.00

API (%) 33.70 28.80

Distillate yield(%) 73.00 80.00

Capacity(mmt) 11.80 15.00

Theortical GRM(US$/bbl) 5.00 8.50

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

13 ONGC Mangalore Refineries & Petrochemicals

Exhibit 30: Expansion of units - How it would help in boosting GRM

PFCC unit Maximising production of propylene

(Petro fluidised catalytic cracking) FCC naphtha to be utilised for producing paraxylene

Higher capacity enables the processing of more heavy crude oils

DCU Upgrade high sulphur residue into distillate and naphtha

(Delayed coker unit) Used for higher production of diesel using DHDTU

Higher coker distillate to be used for hydro-cracking units(HCU)

DHDTU (Diesel hydro-treating unit) Increase the production of Euro III/IV fuels

New CDU/VDU Able to process higher heavier and sour crude oils

Source: Nirmal Bang Institutional Equities Research

Exhibit 31: Special incentives from Karnataka government

Plant & machinery Exemption from entry tax during the initial period of four years from the date of

commencement of project implementation

Crude oil Exemption from entry tax on the crude oil required for the third phase (3mmt) for 15 years

from the start of production

CST Exemption for 15 years on sales made out of the Phase III throughput

VAT

Interest-free soft loans at 100% of eligible gross VAT during the first three years and thereafter at 60% of gross VAT on sale of PP, petcoke, LSHS, naphtha, liquefied

petroleum gas (incremental production), mixed xylenes and reformate to non-SEZs for 15 years and to be repaid in 15 equal installments thereafter with a maximum limit of Rs5bn per

annum

Source: Nirmal Bang Institutional Equities Research

Exhibit 32: Refinery expansion - Cost advantage

Capacity

(mtpa) Capacity

(bpd) Capex

(US$mn) Capex/

bbl Nelson

complexity Capex/Nelson

complexity Complexity/

bbl

Essar Oil 20 400,000 5,158 12,895 11.8 1,093 2.99

Bina, BPCL 9 180,000 2,553 14,183 9 1,576 4.32

Bhatinda, HPCL 9 180,000 4,000 22,222 9 2,469 6.76

Paradip, IOC 15 300,000 6,600 22,000 9 2,444 6.70

Reliance Industries’ SEZ 29 580,000 7,300 12,586 14 899 2.46

MRPL post- expansion 15 300,000 4,434 14780 10 1,478 4.05

Source: Nirmal Bang Institutional Equities Research

Exhibit 33: Benefits from Karnataka and Central governments

Karnataka government

Interest-free soft loan at the rate of 100% of eligible gross VAT for the first three years

60% of eligible gross VAT on sale of polypropylene, pet coke, LSHS, naphtha

LPG, mixed xylenes to non-SEZ units for12 years to be repaid after 15 years by 15 EMIs limited to Rs5,000mn per annum

Central government

Eligible for income-tax benefits under Section 80(IB) of the Income Tax Act, 1962

Successfully commissioned CDU/VDU, meeting the March 2013 deadline

Source: Nirmal Bang Institutional Equities Research

Comfortable debt position to help in funding capex

The total capex likely to be incurred on phase III expansion would be around ~Rs145bn. Peak debt is likely to touch Rs75.61bn in FY14E from Rs61.8bn in FY12 and the rest would be met from internal accruals. The debt-to-equity ratio is expected to peak in FY14E, at 1.01x, and later decline once the cash flows from phase III expansion start flowing in. Being a subsidiary of ONGC, the company enjoys the privilege of lower interest cost loans at 7% per annum and OIDB(Oil Industry development board) loans at 9% per annum. The company has given guidance of peak debt at Rs75bn.

Institutional Equities

14 ONGC Mangalore Refineries & Petrochemicals

Exhibit 34: Comfortable debt position to aid in funding capex

FY09 FY10 FY11 FY12 FY13E FY14E FY15E

Capex (Rsmn) 3,337 14,564 37,917 30,263 43,707 26,000 11,000

Debt (Rsmn) 19868 16964 15570 61831 69809 75615 68483

Debt-equity ratio (x) 0.42 0.30 0.24 0.86 1.01 1.01 0.79

Interest payment/EBITDA(x)

15.27 13.27 19.57 7.92 2.35 4.56 6.42

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 35: Phase III capex scenario

Total capex(Rsbn)

Amount spent so far (Rsbn)

Project completion in percentage terms

Refinery expansion and upgradation 122 115 94.6

Polypropylene project 18 13 72.2

SPM 10 7 67.0

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 36: Debt status

Outstanding Approved debt (Rsbn) Availed till now(Rsbn) Interest rate (%)

Debt as of Now(Rsbn) 56 - - -

OIDB(Rsbn) 8 - 8 9.5

ECB(Rsbn) 15 US$650mn US$300mn 6.0

ONGC(Rsbn) 33 50 33 9.5

Source: Company, Nirmal Bang Institutional Equities Research

Impact on earnings with expanded capacity expected to go fully on stream from FY15

We expect EBITDA to post a 28% CAGR over FY12-FY15E at Rs34,493compared to a negative 9% CAGR over FY09-FY12. EBITDA growth is largely on account of the entire effect of increase in complexity and operational efficiencies to start kicking in from 4QFY14. EBITDA margin is expected at 5.6% in FY15E compared to the past five years’ average of 3.6%. Profits are expected to post a 20% CAGR over FY12-FY15E at Rs15,429mn and PAT margin is likely to improve to 2.5% versus the past five years’ average of 1.8%. We expect the RoE to improve to 19.1% in FY15E from 13.2% in FY12.

Exhibit 37: Gross profit growth Exhibit 38: EBITDA growth

Source: Company, Nirmal Bang Institutional Equities Research Source: Company, Nirmal Bang Institutional Equities Research

(50)

(40)

(30)

(20)

(10)

0

10

20

30

40

50

60

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

FY10 FY11 FY12 FY13E FY14E FY15E

(%)(Rsmn)

Gross profit Growth YoY (RHS)

(100)

(50)

0

50

100

150

200

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY10 FY11 FY12 FY13E FY14E FY15E

(%)(Rsmn)

EBITDA Growth YoY (RHS)

Institutional Equities

15 ONGC Mangalore Refineries & Petrochemicals

Exhibit 39: EBITDA/PAT margin

Source: Nirmal Bang Institutional Equities Research

Outlook and valuation

We have assigned a Buy rating to MRPL with a target price of Rs69 - on the basis of EV/EBITDA methodology - assigning a multiple of 5.5x FY15E earnings (20% discount to the average global multiple of 7.0x) considering the cyclical nature of the refining industry. We have valued the stock at a 20% discount to global refining companies’ stocks on account of: (1) The company’s policy against going in for any forex hedging covers for inventories and finished products, thereby leading to sharp fluctuations in quarterly earnings, (2) Delay in phase III expansion by almost two years, and (3) Uncertainty on the pricing front, with the finance ministry exerting pressure for export parity mechanism for subsidised petroleum products. At the target price of Rs69, the stock trades at 5.6x FY15E earnings, which is at ~30% discount to global refining companies’ average and 1.1x FY14E book value, which is ~26% discount to the global refining companies’ average.

Exhibit 40: MRPL’s valuation

Methodology Value

(Rs/share) Remarks

EV/EBITDA 69.4 EV/EBITDA multiple of 5.5x, 20% discount to global average

P/E 70.0 PE multiple of 8x, with 20% discount to global average

P/BV 69.0 P/BV multiple of 1.4x

DCF 75.0 WACC of 11.85% and terminal value of 1%

Source: Nirmal Bang Institutional Equities Research

We have chosen the EV/EBITDA methodology on account of: (1) Capex of Rs150bn to be capitalised in FY15E to increase interest costs and depreciation by ~Rs6bn and sway earnings, and (2) Given the cyclical nature of the refining industry, EBITDA to be a key indicator for gauging refining business operations.

Exhibit 41: What the market sidetracks

Execution risk of Phase III expansion project receding

All units under Phase III expansion project achieving mechanical completion

GRM expansion of US$3.5-US5.0/bbl from current core GRM of US$5.0/bbl

Significant exposure ~20%-50% to export markets gives protection if export parity prices implemented

Ability to meet throughput guidance despite having zero exposure to Iranian crude oil

Post commercial run, DHTDS units can earn additional income of Rs2,000/t from diesel

MAT paying company from FY15 on account of benefits under Section 80IB from the current tax rate of 33%

Increased acidic crude oil processing ability would lead to sourcing of ~80% high sulphur crude oil

Acquiring ~2mmt of high sulphur African crude oil currently having API of 25-28

Source: Nirmal Bang Institutional Equities Research

(1)

0

1

2

3

4

5

6

FY10 FY11 FY12 FY13E FY14E FY15E

(%)

EBITDA margin PAT margin

Institutional Equities

16 ONGC Mangalore Refineries & Petrochemicals

We have assigned Buy rating to MRPL to reflect: (1) The company entering complexity league, which would led to GRM expansion of US$3.5-US$4.0/bbl (2) Ability to maintain the guided throughput with even nil exposure to Iranian crude oil, (3) Higher GRM leading the RoAE to increase to 19.1% in FY15E from 12% in FY13E, (4) Earnings CAGR of 20% likely over FY12-FY15E from a negative CAGR of 8.7% over FY09-FY12, (5) Stock price implying that it is trading at a 22% discount to Indian refining companies’ average and a 45% discount to global refining companies’ average, and (6) The stock trading at an attractive valuation of 1.1x FY14 book value, which is ~1 SD below the mean.

Exhibit 42: Implied EV/bbl valuation

CMP 49

EV (Rsmn) 160,591

EV (US$mn) 2,947

Capacity(mt) 15

Capacity(bbl) 300,000

EV(US$/bbl) 9,822

Replacement value for Indian refiners(US$/bbl) 12,746

Replacement value for global refineries(US$/bbl) 18,000

Replacement discount to Indian refiners (%) (23)

Replacement discount to global refiners (%) (45)

Source: Nirmal Bang Institutional Equities Research

Exhibit 43: GRM sensitivity

Impact in FY14E 4.50 5.00 5.50 5.75 6.25 6.75

Revenue (Rsmn) 696,036 696,036 696,036 696,036 696,036 696,036

EBITDA (Rsmn) 15,856 18,627 21,397 22,782 25,553 28,323

PAT (Rsmn) 2,455 4,311 6,167 7,095 8,951 10,808

EPS (Rs/share) 1.40 2.46 3.52 4.05 5.11 6.17

Valuation (Rs/share) 69 69 69 69 69 69

Impact in FY15E 5.50 6.00 6.50 7.00 7.50 8.00

Revenue (Rsmn) 619,821 619,821 619,821 619,821 619,821 619,821

EBITDA (Rsmn) 25,949 28,797 31,645 34,493 37,341 40,189

PAT (Rsmn) 9,704 11,612 13,520 15,429 17,337 19,245

EPS (Rs/share) 5.54 6.63 7.71 8.80 9.89 10.98

Valuation (Rs/share) 42 51 60 69 78 87

Source: Nirmal Bang Institutional Equities Research

Exhibit 44: Refinery throughput utilisation sensitivity

Impact in FY14E 95.0 97.5 100 102.5 105 107.5 110

Revenue (Rsmn) 696,036 696,036 696,036 696,036 696,036 696,036 696036

EBITDA (Rsmn) 21,276 21,814 22,352 22,890 23,428 23,966 24504

PAT (Rsmn) 6,086 6,446 6,807 7,167 7,528 7,888 8249

EPS (Rs/share) 3.47 3.68 3.88 4.09 4.30 4.50 4.71

Valuation (Rs/share) 69 69 69 69 69 69 69.17

Impact in FY15E 95.0 97.5 100 102.5 105 107.5 110

Revenue (Rsmn) 619,821 619,821 619,821 619,821 619,821 619,821 619,821

EBITDA (Rsmn) 32,184 33,009 33,833 34,658 35,482 36,307 37,131

PAT (Rsmn) 13,882 14,434 14,987 15,539 16,092 16,644 17,196

EPS (Rs/share) 7.92 8.24 8.55 8.87 9.18 9.50 9.81

Valuation (Rs/share) 62 65 67 70 72 75 77

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

17 ONGC Mangalore Refineries & Petrochemicals

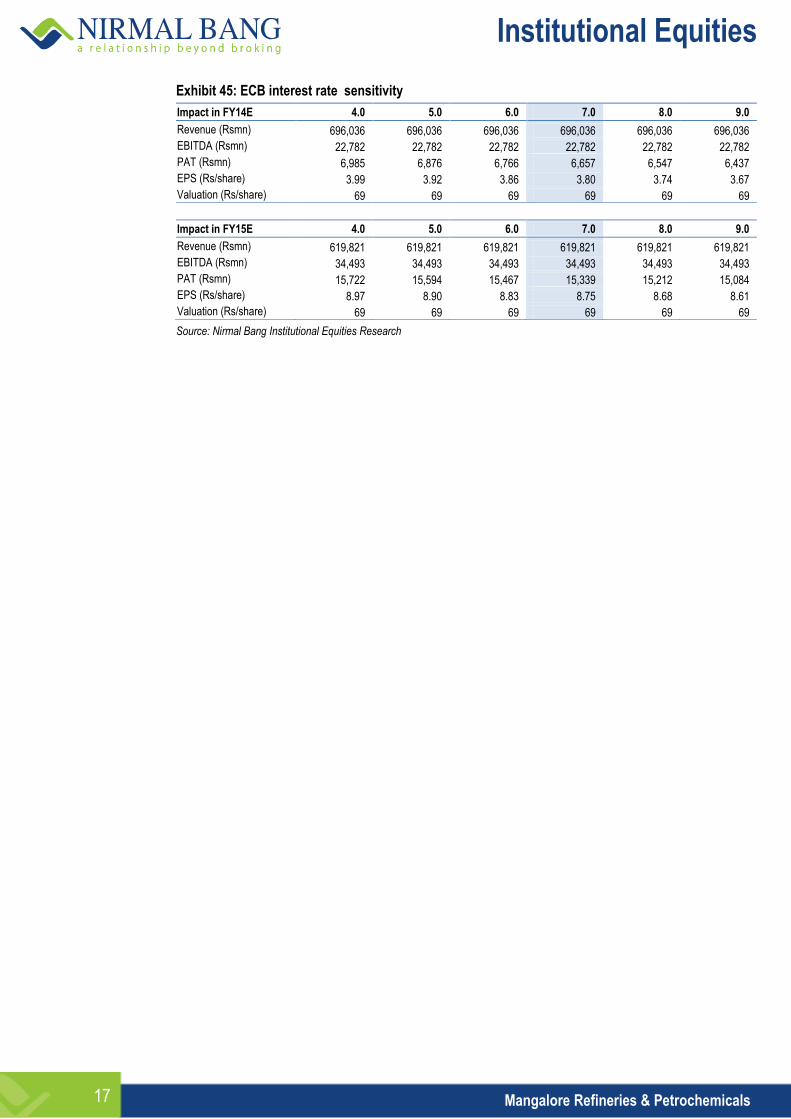

Exhibit 45: ECB interest rate sensitivity

Impact in FY14E 4.0 5.0 6.0 7.0 8.0 9.0

Revenue (Rsmn) 696,036 696,036 696,036 696,036 696,036 696,036

EBITDA (Rsmn) 22,782 22,782 22,782 22,782 22,782 22,782

PAT (Rsmn) 6,985 6,876 6,766 6,657 6,547 6,437

EPS (Rs/share) 3.99 3.92 3.86 3.80 3.74 3.67

Valuation (Rs/share) 69 69 69 69 69 69

Impact in FY15E 4.0 5.0 6.0 7.0 8.0 9.0

Revenue (Rsmn) 619,821 619,821 619,821 619,821 619,821 619,821

EBITDA (Rsmn) 34,493 34,493 34,493 34,493 34,493 34,493

PAT (Rsmn) 15,722 15,594 15,467 15,339 15,212 15,084

EPS (Rs/share) 8.97 8.90 8.83 8.75 8.68 8.61

Valuation (Rs/share) 69 69 69 69 69 69

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

18 ONGC Mangalore Refineries & Petrochemicals

Exhibit 46: Income statement

Y/E March (Rsmn) FY11 FY12 FY13E FY14E FY15E

Net sales 388,869 537,703 658,531 696,036 619,821

% growth 21.7 38.3 22.5 5.7 (10.9)

Staff costs 1,845 1,606 1,794 1,773 1,867

Raw materials 364,041 510,865 637,709 668,160 579,948

Other expenses 2,755 9,097 12,604 4,149 4,369

Total expenditure 368,641 521,569 652,107 674,082 586,183

EBITDA 20,483 16,366 9,647 22,782 34,493

% growth 33.6 (20.1) (41.1) 136.2 51.4

EBITDA margin (%) 5.3 3.0 1.5 3.3 5.6

Other income 2,359 3,706 3,224 827 855

Interest costs 1,047 2,067 4,100 4,996 5,373

Depreciation 3,914 4,339 5,866 10,517 9,512

Profit before tax 17,371 13,202 518 10,590 23,028

% growth 2.7 (24.0) - - -

Tax 5,604 4,116 3,615 3,495 7,599

Effective tax rate (%) 32.3 31.2 697.9 33.0 33.0

Net profit 11,766 9,086 (3,097) 7,095 15,429

% growth 5.8 (22.8) (134.1) (329.1) 117.5

EPS (Rs) 6.21 4.94 (1.77) 4.05 8.80

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 48: Balance sheet

Y/E March (Rsmn) FY11 FY12 FY13E FY14E FY15E

Equity 17,619 17,573 17,573 17,573 17,573

Reserves 47,670 54,719 51,622 57,154 69,182

Net worth 65,289 72,292 69,195 74,726 86,755

Total loans 15,570 61,831 69,809 75,615 68,483

Short term loans 0 18,551 9,275 3,710 1,113

Long term loans 15,570 43,280 60,534 71,905 67,370

Deferred tax liabilities 3,472 4,531 4,531 4,531 4,531

Liabilities 84,330 138,654 143,535 154,873 159,769

Gross block 76,198 90,243 150,243 190,243 190,743

Depreciation 45,301 49,644 55,510 66,027 75,539

Net block 30,896 40,598 94,733 124,216 115,204

CWIP 54,674 70,892 54,599 40,599 51,099

Long-term Investments 948 423 423 423 423

Inventories 40,974 78,176 61,738 64,070 55,611

Debtors 25,266 34,593 34,280 36,232 32,265

Cash 24,151 22,347 504 317 4,415

Other current assets 284 1,241 1,241 1,241 1,241

Loans & advances 7,605 13,292 13,292 13,292 13,292

Total current assets 98,280 149,648 111,054 115,152 106,823

Creditors 96,874 119,572 117,273 123,952 110,379

Provisions 3,594 3,334 - 1,564 3,400

Total current liabilities 100,469 122,906 117,273 125,515 113,780

Net current assets (2,188) 26,741 (6,219) (10,364) (6,956)

Total assets 84,330 138,654 143,535 154,873 159,769

Source: Company, Nirmal Bang Institutional Equities Research

Financials

Exhibit 47: Cash flow

Y/E March (Rsmn) FY11 FY12 FY13E FY14E FY15E

PBT 17,371 13,202 518 10,590 23,028

(Inc.)/dec. in working capital 11,537 (29,674) 11,117 3,958 690

Cash flow from operations 28,908 (16,472) 11,635 14,548 23,718

Depreciation 3,914 4,339 5,866 10,517 9,512

Interest paid (-) 1,047 2,067 4,100 4,996 5,373

Tax paid (-) 5,604 4,116 3,615 3,495 7,599

Dividends paid (-) (2,444) (2,037) 0 (1,564) (3,400)

Net cash from operations 37,377 (9,413) 21,186 29,405 41,927

Capital expenditure (-) (37,917) (30,263) (43,707) (26,000) (11,000)

Net cash after capex (540) (39,675) (22,521) 3,405 30,927

Other income 2,096 3,462 4,030 4,150 4,275

Inc./(dec.) in LT borrowings (1,394) 27,711 17,253 11,371 (4,535)

Inc./(dec.) in ST borrowings 0 18,551 (9,275) (5,565) (2,597)

(Inc.)/dec in investments 15,288 525 0 0 0

Equity issue/(buyback) 0 (46) 0 0 0

Cash from financial activities 15,450 10,528 (10,513) 13,361 28,070

Others (39) 4 0 0 0

Opening cash 23,440 24,151 22,347 504 317

Closing cash 24,152 22,347 504 316 4,415

Change in cash 15,411 10,532 (10,513) 13,361 28,070

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 49: Key ratios

Y/E March FY11 FY12 FY13E FY14E FY15E

Per share

EPS 6.2 4.9 (1.8) 4.0 8.8

Book value per share 37.3 41.2 39.5 42.6 49.5

Dividend per share 1.2 1.0 0.0 0.8 1.7

Cash EPS per share 8.9 7.7 1.6 10.0 14.2

Free cash flow per share 3.2 (25.1) (14.7) 0.3 11.4

Valuation (x)

P/E 7.9 9.9 (27.7) 12.1 5.6

P/BV 1.3 1.2 1.2 1.1 1.0

EV/EBITDA 3.9 9.0 16.1 6.9 4.2

Margins (%)

EBITDA margin 5.3 3.0 1.5 3.3 5.6

Net profit margin 3.0 1.7 (0.5) 1.0 2.5

Asset-based ratios (%)

RoAE 19.4 13.2 (4.4) 9.9 19.1

RoACE 13.5 7.3 (16.0) 5.5 10.6

DuPont analysis RoE

PAT/PBT (%) 67.7 68.8 (597.9) 67.0 67.0

PBT/EBIT (%) 106.5 111.7 13.7 86.3 92.2

EBIT/sales (%) 4.2 2.2 0.6 1.8 4.0

Sales/assets (x) 4.6 3.9 4.6 4.5 3.9

Assets/equity (x) 1.3 1.9 2.1 2.1 1.8

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

19 ONGC Mangalore Refineries & Petrochemicals

Disclaimer Stock Ratings Absolute Returns

BUY > 15%

HOLD 0-15%

SELL < 0%

This report is published by Nirmal Bang’s Institutional Equities Research desk. Nirmal Bang has other business units with independent research teams separated by Chinese walls, and therefore may, at times, have different or contrary views on stocks and markets. This report is for the personal information of the authorised recipient and is not for public distribution. This should not be reproduced or redistributed to any other person or in any form. This report is for the general information for the clients of Nirmal Bang Equities Pvt. Ltd., a division of Nirmal Bang, and should not be construed as an offer or solicitation of an offer to buy/sell any securities. We have exercised due diligence in checking the correctness and authenticity of the information contained herein, so far as it relates to current and historical information, but do not guarantee its accuracy or completeness. The opinions expressed are our current opinions as of the date appearing in the material and may be subject to change from time to time without notice. Nirmal Bang or any persons connected with it do not accept any liability arising from the use of this document or the information contained therein. The recipients of this material should rely on their own judgment and take their own professional advice before acting on this information. Nirmal Bang or any of its connected persons including its directors or subsidiaries or associates or employees or agents shall not be in any way responsible for any loss or damage that may arise to any person/s from any inadvertent error in the information contained, views and opinions expressed in this publication.

Team Details:

Name Email Id Direct Line

Rahul Arora CEO [email protected] +91 22 3926 8098 / 99

Hemindra Hazari Head of Research [email protected] +91 22 3926 8017 / 18

Sales and Dealing:

Neha Grover AVP Sales [email protected] +91 22 3926 8093

Ravi Jagtiani Dealing Desk [email protected] +91 22 3926 8230, +91 22 6636 8832

Sudhindar Rao Dealing Desk [email protected] +91 22 3926 8229

Pradeep Kasat Dealing Desk [email protected] +91 22 3926 8102/8103, +91 22 6636 8831

Michael Pillai Dealing Desk [email protected] +91 22 3926 8100/8101, +91 22 6636 8830

Nirmal Bang Equities Pvt. Ltd.

Correspondence Address

B-2, 301/302, Marathon Innova,

Nr. Peninsula Corporate Park

Lower Parel (W), Mumbai-400013.

Board No. : 91 22 3926 8000/1

Fax. : 022 3926 8010