Managing the Malaysian - MIR · Managing the Malaysian 1 Economy Overview When Budget 2001 was...

187

5

Transcript of Managing the Malaysian - MIR · Managing the Malaysian 1 Economy Overview When Budget 2001 was...

5

Managing the MalaysianEconomy1

Overview

When Budget 2001 was formulated last year,the outlook of the global economy was

still uncertain, particularly with respect to themagnitude and duration of the United States(US) economic slowdown. The expectation thenwas for an early recovery commencing from thefourth quarter of 2000. However, towards theend of 2000, global economic activity furtherslowed down, particularly in the US. Since thesecond quarter of this year, it became increasinglyevident that the slowdown has not only becomemore protracted and severe but the contagionhas also spread to other economies. The recentattack on the US has made the prospect of anearly recovery even more uncertain.

The Malaysian economy had recovered fromthe 1997 Asian financial crisis and was on thepath of stronger growth. Real Gross DomesticProduct (GDP) growth, which turned positivesince the second quarter of 1999, had continuedto grow strongly for seven consecutive quarters.Against this background and premised on theassumption of an early global economic recovery,the main strategic thrusts of Budget 2001 werefocussed on stimulating domestic growth andenhancing competitiveness as well as improvingthe quality of life of Malaysians in line with thenation’s agenda of a caring society.

Stimulating Economic Growth

Fiscal Policy

The expansion in domestic aggregate demandin 2001 was expected to be broad-based driven

by both the private and public sectors. The slowerperformance of the private sector reflecting theimpact from the unfavourable external sector,however, necessitated further stimulus measuresby the public sector to support domestic demand.In this regard, Budget 2001 allocation for bothoperating and development expenditure amountedto RM91,050 million, against an expenditure ofRM84,500 million in 2000, an increase of 7.8%.During the course of the year and in responseto the greater-than-expected slowdown in theglobal economy and the resultant deteriorationin the nation’s export performance, theGovernment announced a pre-emptive packagein March 2001 aimed at further stimulatingdomestic demand. Under this package, theGovernment expenditure was further increasedby RM3 billion to supplement the expansionarystance taken during Budget 2001 announced inOctober 2000.

The fiscal stimulus to increase domestic demandalso comprised both tax and non-tax measures.As a means to increase disposable income andencourage consumption, higher tax rebates weregiven. The rebate for individuals was increasedfrom RM110 to RM350 and from RM60 to RM350for wives. The rebate would benefit 1.25 milliontaxpayers and place some RM434 million in thehands of taxpayers. Measures to stimulatedomestic demand also included the reduction ofemployees’ contribution to the EmployeesProvident Fund (EPF) and the removal of taxon credit cards to encourage spending. Toaugment sales of automobiles, civil servants areallowed to apply for car loans once in every fiveyears instead of seven years. To encourage thesales of properties, exemptions were given to

18

stamp duty for the sales and purchase, transferand loan agreements while for civil servants,processing fees were exempted for purchasesof completed properties up to the end of 2001.At the same time, the housing loan eligibility ofcivil servants was increased. Additional criticalallowances were also given to doctors and nurses,headmasters and principals while incentive andmeal allowances were given or increased forthe personnel of the Armed Forces and Police.

Monetary Policy

The thrust of monetary policy in 2001 continuesto focus on complementing the fiscal stimulusin supporting economic activities. Given the lessfavourable external environment, in particularthe slowdown of the US and Japanese economiesat the beginning of the year, the pursuit of aneasier monetary stance is necessary to mitigatethe slack in external demand. The policy stancehas been facilitated by the low inflationaryenvironment as well as the global easing ofinterest rates. The ample liquidity in the bankingsystem helped to maintain low interest rates toensure the financing of economic activities atreasonable costs. Despite the low interest rates,depositors continue to enjoy positive real ratesof return on savings.

The banking sector expanded their financingactivities through loans and private debt securities(PDS) financing, which grew by 4% in the firsteight months of the year. Lending was broad-based, with loans extended for the purchase ofresidential property, manufacturing sector,wholesale trade and the purchase of passengercars. Meanwhile, measures continue to be takento improve the financing of small- and medium-enterprises (SMEs), an important mainstay ofthe economy.

In the foreign exchange market, the ringgit, whichis pegged to the US dollar since September1998, remained relatively strong against mostmajor and regional currencies in tandem withthe strong US dollar in the first seven monthsof 2001. By virtue of the peg, the ringgit mirrorsthe movements of the US dollar. As such, theringgit has since 11 September, depreciated bybetween 0.2% to 3% against major and regional

currencies, following the weakening of the USdollar. Nevertheless, the ringgit peg will be closelymonitored against both domestic and externaldevelopments to ensure that it remains consistentwith macroeconomic fundamentals. Meanwhile,the ringgit peg continues to provide anenvironment of stability and predictability tofacilitate economic activities.

Capital Market

The equity market remains generally lacklustrein 2001, in line with other major and regionalmarkets on concerns of the global economicslowdown. In July and August, the equity marketbegan to improve, but the uptrend was eventuallyaffected by the September attacks on the USand the subsequent fall in stock prices worldwide.The bond market, however, continues to growin 2001, reflecting its increasing significance asan alternative to financing by the banking system.In this regard, the Securities Commission (SC),as the sole regulator of the bond market, continuesto undertake measures to promote the bondmarket, in particular Islamic debt issues andasset-backed securities. The issuance of IslamicPDS has been rising, reflecting its growingacceptance to account for 37% of total new PDSissues approved by SC in the first half of 2001(2000: 25%). The issuance of asset-backedsecurities, however, has yet to pick up. In addition,further amendments were made to the SecuritiesCommission Act, aimed at establishing an efficientregulatory regime for capital raising and in tandemwith developing the capital market as the preferredfund-raising centre for domestic companies.

Knowledge-based Economy

Recognising that technology, skills and innovationare the main drivers to enhance future growth,Budget 2001 further reinforced the strategy totransform the economy from a production-basedto a knowledge-based economy. The knowledge-based economy or K-based economy presentsa strategy to generate and exploit knowledgeto create new value in the economy, therebycontributing to increasing total factor productivityand raising the long-term growth potential. Toenable the transition to the new economy and

19

address present challenges, the Governmentcommissioned the Knowledge-based EconomyMaster Plan in 2000. The Master Plan, recentlycompleted, is holistic in approach and outlinesthe key strategies to transform the economy tobe highly competitive and resilient.

Measures to expedite Malaysia’s transition intoa K-based economy focussed on efforts to attractthe best brains into the country to create a world-class workforce and enhancing computer literacyand information and communications technologies(ICT) through the greater use of computers.Towards this end, Malaysians who are abroadand with the required expertise were givenincentives to return, in particular through thegranting of permanent status to spouse andchildren and tax exemptions on personal effectsand income remitted into the country. By mid-September 2001, of the 356 applications receivedfrom professionals working overseas, 122 wereapproved in the areas of finance, industries,ICT and medicine.

With regard to enhancing computer literacy, ofthe 4,400 schools identified to be equipped withcomputer laboratories, 50 projects have beencompleted, 1,354 are under various stages ofconstruction and the rest are under the planningstage. To enhance accessibility to computers inline with the one-computer-per-family policy,amendments to the EPF Act were made, allowingwithdrawals for the purchase of computers. Byend-August, EPF has approved 467,832applications totall ing RM1,555 mill ion.Government employees also took advantage ofthe more flexible loan facility, which permits thepurchase of computers once in every five yearsfrom just once, previously.

Developing ICT Industries and Venture Capital

The development of the Multimedia Super Corridor(MSC) marked the beginning of initiatives towardsthe development of a K-based economy. In orderto promote the development of world-class ICTcompanies, various incentives have been providedto attract ICT companies to the MSC. As atSeptember, 563 companies have been awardedMSC-status, of which 48 are world-classcompanies, exceeding the target of 500 and

ahead of the scheduled timeframe of 2003. Thesecompanies have, thus far, invested RM6 billionwhile their exports have increased more thansix times from USD19 million in 1997 to USD127million in 2000 and increasing further to anestimated USD260 million this year. In addition,these companies have also expended a sum of26% of their total expenditure on research anddevelopment (R&D). In terms of employmentgeneration, a total of 11,911 workers wereemployed, of which 82.6% or 9,842 wereknowledge-workers in 2000. The number isexpected to increase to 14,438 and 12,169workers, respectively in 2001.

Further progress in fostering synergy has beenmade with the addition of an eighth MSC flagshipapplication on Technopreneur Development. Thenetwork of incubators set up via this flagshipis expected to provide the necessary impetusto the development of technopreneurship.

New high-technology and knowledge-based aswell as idea-based startups for SMEs requiredifferent and more creative modes of funding.Collateral-based traditional bank lending maynot be forthcoming for activities based onpromising ideas or intangible collaterals. Venturecapital financing provides a viable alternative totraditional lending as it provides seed capital forearly startups and acts as business angels forhigh-risk growth sectors. To close the financinggap, the Government announced theestablishment of a venture capital fund totallingRM500 million in Budget 2001. The fund hasbeen channelled to a newly-formed Governmentcompany, namely the Malaysian Venture CapitalManagement Berhad (MAVCAP) in the form ofinterest-free soft loans for a period of 10 years.MAVCAP will implement the Government’sstrategic mandate to drive the developmentand empowerment of innopreneurs andtechnopreneurs to create wealth in the K-basedeconomy as well as development of the venturecapital industry. MAVCAP is expected to launchits financing facilities to the market in October2001. MAVCAP is negotiating to secure a RM1.9billion soft loan from Japan as a source ofadditional funding. A significant portion of thisfunding would be utilised for debt ventures suchas project-based loans, guarantee to banks andexport finance for the ICT industry and high-

20

KNOWLEDGE-BASED ECONOMY :THE WAY FORWARD

Introduction

The world is fast becoming a single borderless global marketplace which is expedited by rapidadvancements in information and communications technologies (ICT). The global economy ischaracterised by high-technology diffusion, information accessibility, capital mobility and the increasinglysophisticated demands of consumers. As such, competing in the current environment is becomingmore and more knowledge-driven. Growth and wealth creation of economies are increasingly propelledby the knowledge, skills and creativity of the workforce, as evident from the experience of highlyproductive countries.

In the case of Malaysia, the imperative to develop into a knowledge-based (K-based) economyis crucial as a strategy to sustain high growth and to remain competitive in order to achieve Vision2020. The nation’s move to a K-based economy is influenced by challenges from increasing globalisationas well as concerns about intense competition for foreign direct investment from relatively labour-surplus and low-waged economies in the region and elsewhere. The move towards a K-basedeconomy is part of a wider plan to become a fully developed and knowledge-rich nation by 2020.

Understanding the Knowledge-based Economy

A K-based economy is one in which knowledge, creativity and innovation play an increasing andimportant role in generating and sustaining growth. While traditional factors of production willcontinue to remain important, knowledge will be the key factor in driving growth through the creationof value added and enhancing productivity and competitiveness. The nucleus of the K-based economyis human capital with its capacity to create, innovate and commercialise knowledge, while ICT willbe a key enabling tool to facilitate the transformation to a K-based economy. In a broad sense,all sectors of the economy will become K-based through productivity-driven strategies to enhancethe application of knowledge vis-à-vis input-driven strategies involving increased inputs of capitalor labour.

The K-based economy essentially comprises two important types of knowledge industries: the firstbeing industries with knowledge as the major product and the second being industries managing,processing and disseminating information. The first category includes industries such as software,biotechnology and information technology (IT) hardware and occupations such as engineers, scientists,programmers and designers, whose major output is research that translates into new products andservices. The second category comprises industries such as telecommunications, banking, insurance,law, medicine, education and the government services. Occupations in this category include managers,bankers, accountants, doctors and teachers. These industries are typically required to handle andmanage information effectively, rather than breakthrough knowledge creation.

Current Status

Malaysia started to lay down the foundation for the K-based economy in the mid-1990s. Amongothers, measures taken include the launching of the Multimedia Super Corridor (MSC), whichrepresents the first phase of the K-based economy agenda. Meanwhile, continuous efforts havebeen taken to enhance several key areas to effect the transformation towards the K-based economy.These include human resource development, science and technology (S&T), R&D, infrastructure

21

and infostructure as well as incentives and financing. At the same time, with the comprehensiveworld-class infrastructure and infostructure in place, MSC offers an excellent and conducive ICTenvironment to spearhead the development of a K-based economy, in particular in attracting knowledgeworkers and high technology industries. To date, MSC has attracted a total of 563 companies,including 48 world-class companies. In addition, MSC promotes several flagship applications, includingelectronic government, smart schools, multipurpose card and telehealth as well as the new technopreneurdevelopment flagship.

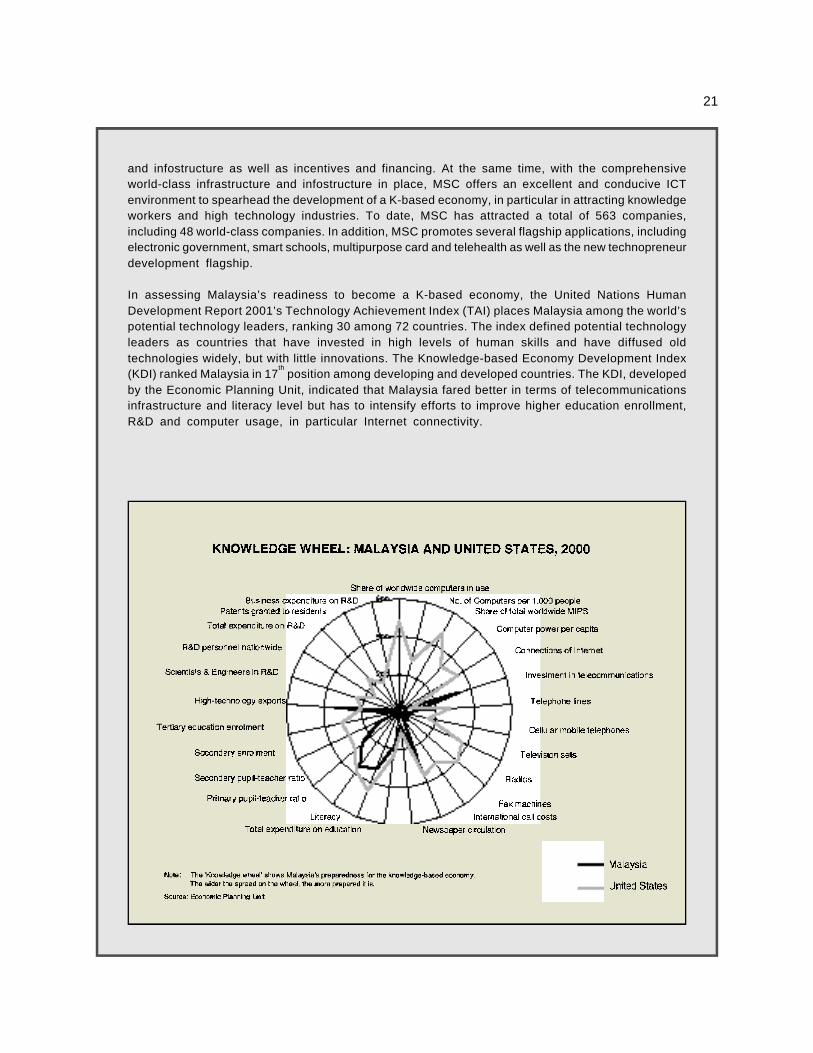

In assessing Malaysia’s readiness to become a K-based economy, the United Nations HumanDevelopment Report 2001’s Technology Achievement Index (TAI) places Malaysia among the world’spotential technology leaders, ranking 30 among 72 countries. The index defined potential technologyleaders as countries that have invested in high levels of human skills and have diffused oldtechnologies widely, but with little innovations. The Knowledge-based Economy Development Index(KDI) ranked Malaysia in 17

th position among developing and developed countries. The KDI, developed

by the Economic Planning Unit, indicated that Malaysia fared better in terms of telecommunicationsinfrastructure and literacy level but has to intensify efforts to improve higher education enrollment,R&D and computer usage, in particular Internet connectivity.

22

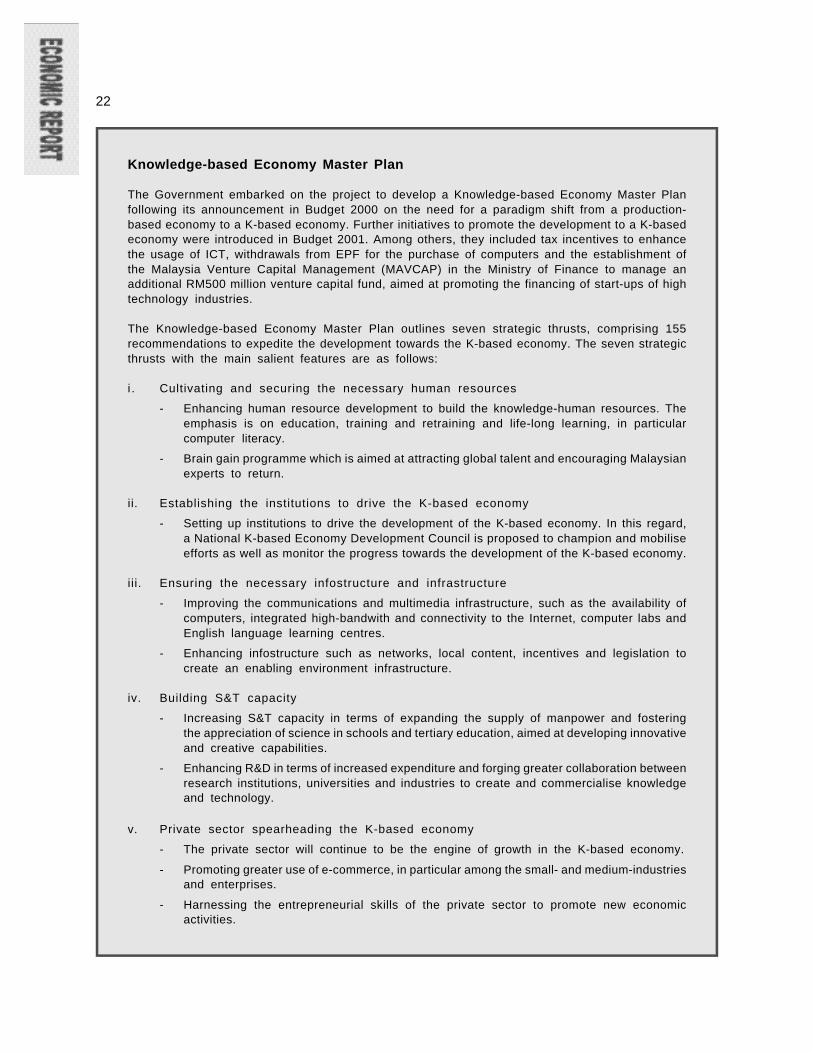

Knowledge-based Economy Master Plan

The Government embarked on the project to develop a Knowledge-based Economy Master Planfollowing its announcement in Budget 2000 on the need for a paradigm shift from a production-based economy to a K-based economy. Further initiatives to promote the development to a K-basedeconomy were introduced in Budget 2001. Among others, they included tax incentives to enhancethe usage of ICT, withdrawals from EPF for the purchase of computers and the establishment ofthe Malaysia Venture Capital Management (MAVCAP) in the Ministry of Finance to manage anadditional RM500 million venture capital fund, aimed at promoting the financing of start-ups of hightechnology industries.

The Knowledge-based Economy Master Plan outlines seven strategic thrusts, comprising 155recommendations to expedite the development towards the K-based economy. The seven strategicthrusts with the main salient features are as follows:

i . Cultivating and securing the necessary human resources

- Enhancing human resource development to build the knowledge-human resources. Theemphasis is on education, training and retraining and life-long learning, in particularcomputer literacy.

- Brain gain programme which is aimed at attracting global talent and encouraging Malaysianexperts to return.

ii. Establishing the institutions to drive the K-based economy

- Setting up institutions to drive the development of the K-based economy. In this regard,a National K-based Economy Development Council is proposed to champion and mobiliseefforts as well as monitor the progress towards the development of the K-based economy.

iii. Ensuring the necessary infostructure and infrastructure

- Improving the communications and multimedia infrastructure, such as the availability ofcomputers, integrated high-bandwith and connectivity to the Internet, computer labs andEnglish language learning centres.

- Enhancing infostructure such as networks, local content, incentives and legislation tocreate an enabling environment infrastructure.

iv. Building S&T capacity

- Increasing S&T capacity in terms of expanding the supply of manpower and fosteringthe appreciation of science in schools and tertiary education, aimed at developing innovativeand creative capabilities.

- Enhancing R&D in terms of increased expenditure and forging greater collaboration betweenresearch institutions, universities and industries to create and commercialise knowledgeand technology.

v. Private sector spearheading the K-based economy

- The private sector will continue to be the engine of growth in the K-based economy.

- Promoting greater use of e-commerce, in particular among the small- and medium-industriesand enterprises.

- Harnessing the entrepreneurial skills of the private sector to promote new economicactivities.

23

vi. Developing the K-based civil service

- The civil service will continue to facilitate the development of the K-based economy interms of providing leadership, strategising and drawing up policies, implementing programmes,regulating the economy and fostering collaboration between the public and private sectors.

- Emphasis will be given to the development of human resources in the civil service, inparticular the instilling of a culture of innovation, improving English language capabilitiesand enhancing the absorption and application of ICT.

vii. Bridging the knowledge and digital divides

- Ensuring the K-based economy does not widen disparities between various segmentsof Malaysian society.

- Empowering the rakyat with knowledge through providing access to education.

- Enhancing the affordability of computers and Internet access.

- Addressing the digital gap among races, rural-urban areas, gender and disadvantagedgroups.

Conclusion

The K-based economy is an imperative that Malaysia cannot afford to ignore in order to achievesustainable economic growth and remain globally competitive. The experience of developed countriesfurther attest to growth and wealth being increasingly driven by knowledge. Although measureshave and continue to be taken in progressing towards the K-based economy, more concerted andaccelerated efforts need to be instituted, particularly in human resource development, S&T, R&D,infrastructure, infostructure and the digital divide in order to leapfrog to the K-based economy.

growth sectors. Requirements for these lendingfacilities would be flexible and less conditionaland the provision of hard collateral is notnecessary.

The Government has also established the VentureCapital Fund for Technology Acquisition (VCTA),totalling RM190 million to finance activities relatedto venture capital and technology acquisition.The fund is channelled through a newly-formedGovernment company, namely Kumpulan ModalPerdana Sdn. Bhd. (KMPSB) in the form ofinterest-free soft loans for a period of 10 years.KMPSB will be involved in the formulation of amaster plan and the management of programmesfor investment linkages in high-technologyindustries. It will also play a role in the investmentof high-growth and high-technology startups andbe involved in the expansion of companies andidentification of investment opportunities forMalaysia as well as suitable technologies abroadto be transferred to Malaysia.

To facilitate ICT companies to tap funds in thecapital market, the listing requirements of theMalaysian Exchange of Securities Dealing andAutomated Quotation (MESDAQ) were furtherliberalised. The requirement that 70% of listingproceeds be used in Malaysia was replaced.Under the new requirements, applicants arerequired to provide proof that benefit accruesto Malaysia if more than 50% of the listingproceeds is utilised outside Malaysia. As at end-August 2001, there were four companies listedon MESDAQ, with seven more companiesapproved for listing.

Enhancing the Nation’sCompetitiveness

Strengthening the Financial System

The Government continues with efforts tostrengthen the financial system with a view to

24

investors, the Kuala Lumpur Stock Exchange(KLSE) has set up an internationalcommunications team to disseminate accurate,timely and effective information on the equitymarket. In the light of improvements in the equitymarket, the 10% exit levy on repatriations ofportfolio profits within one year was withdrawnon 2 May 2001. With this, the remaining capitalcontrol restriction on portfolio investment wascompletely removed.

Developing Strategic Partnerships

Establishing strategic partnerships withinternational and global players in the servicessector, particularly in ports, airports,telecommunications and ICT, are critical toensuring sustained competitiveness and resiliencewithin the context of a borderless market. Strategicalliances and partnerships are important inbringing about higher technological andmanagerial skills via technology transfers andinvestment in human capital by foreign partners.Smart partnerships also broaden domesticmarkets with increased access to internationalmarkets provided by marketing links of globalnetwork players. During the year, a number ofdiscussions were held to identify strategic partnersfor the Malaysian airport operator as well as thenational air carrier. In this respect, SchipolInternational B.V. of Holland has entered intoa Memorandum of Understanding to acquire anequity stake in Malaysian Airport Holding Berhad(MAHB). Malaysia Airlines (MAS) has also broughton board foreign management expertise tospearhead efforts at turning around its operations.With regard to West Port of Port Klang, thecountry’s leading port is expected to derivesynergistic benefits from the 30% stake held byHutchinson Whampoa. Similarly, the TanjungPelepas Port (PTP) in Johore, which sold 30%of its equity to Maersk Sealand, is expected tobenefit from the increase in cargo handling.

Improving Corporate Governance

Efforts towards enhancing transparency andaccountability continue to be undertaken in orderto further improve investor confidence. By July,29 or 41% out of the 70 recommendations oncorporate governance proposed by the Finance

creating a more competitive, strong and resilientfinancial sector. The Capital Market Master Planand the Financial Sector Master Plan werelaunched on 22 February and 1 March 2001,respectively. Both the master plans chart thestrategic directions of the capital market andfinancial sectors over the next 10 years, aimedat enhancing their efficiency, resilience andcompetitiveness in an increasingly globalisedand integrated environment. The master plansencompass a change programme to beimplemented in phases.

In line with the objective to enhance domesticcapacity to develop a core of strong domesticinstitutions, further progress was achieved inthe restructuring of the financial sector. The bankmerger programme was successfully implementedwith 52 out of the 54 domestic banking institutionsconsolidated into 10 banking groups, resultingin 98% of total assets of the domestic bankingsector rationalised and consolidated by end-September 2001. The two remaining bankinginstitutions are expected to finalise their mergernegotiations soon.

The capital position of the banking systemcontinues to remain strong with the new capitalfund requirement increased to RM2,000 millionfor domestic banking groups and RM300 millionfor the locally-incorporated foreign banks. As atend-August 2001, nine banking groups and eightforeign banking institutions have complied withthis requirement. The risk-weighted capital ratio(RWCR) increased to 12.6% as at end-August2001 (end-2000: 12.3%), well exceeding the Basleminimum requirement of 8%. Non-performingloans (NPLs) ratio on a 6-month classification,which was 6.3% as at end 2000, have risen to8.3% at end-August, following the slowing downin economic activities and the reclassification ofNPLs previously given indulgence. The level is,however, still below the peak of 9% experiencedduring the financial crisis.

In order to further strengthen the capital market,efforts were undertaken to consolidate thestockbroking industry. As at end-August 2001,seven stockbroking companies had entered intoagreements to acquire or merge with three othercompanies. In addition, as a measure to forgebetter communication with investors and tocounteract misperceptions especially by foreign

25

Committee on Corporate Governance have beenimplemented. To ensure smooth and effectiveexecution, an Implementation Project Teamcomprising representatives from the Ministry ofFinance, BNM, the Registrar of Companies andKLSE was set up. Legislation, rules andregulations are being reviewed and updated ona continuous basis to further improve corporategovernance.

In addition, the KLSE listing requirements wererevamped on 22 January to address, amongothers, the issue of corporate governance. Inparticular, the requirements on the reporting ofextent of compliance with the Malaysian Codeon Corporate Governance, disclosure by directorson the state of internal controls, independenceof the board of directors as well as mandatoryaccreditation were emphasised. Directors of publiclisted companies are also required to attendprescribed training programmes as a prerequisiteto continued listing, aimed at enhancing thecompetency and professionalism of companydirectors. Meanwhile, a Minority ShareholdersWatchdog Group, comprising EPF, LembagaTabung Angkatan Tentera, Lembaga Tabung Haji,Social Security Organisation (SOCSO) andPermodalan Nasional Berhad (PNB), has beenset up, aimed at encouraging proactiveshareholders participation in public listedcompanies.

Eliminating Bureaucratic Delays

The Government continues to step up efforts toeliminate bureaucratic delays as a measure toaccelerate project implementation and completionin order to sustain economic growth as well asimprove delivery of public goods and services.In this context, a task force in the Ministry ofFinance was established to closely monitor theprogress, identify and troubleshoot problem areasin order to ensure smooth implementation of allthe measures announced in Budget 2001. A FlyingSquad was also formed in the Ministry to ensureboth public sector development and privatisedprojects proceed as scheduled.

To further reduce red tape and in line with theneed to empower ministries and agencies withbigger financial authority, tender boards at theministerial and departmental levels can nowapprove tenders of up to RM50 million for works

and RM30 million for supplies and services. Thetender boards are also allowed to approverestricted tenders of up to RM5 million. Forquotations, authority has been delegated toministries to approve up to RM200,000. Forstatutory authorities, the ceiling for the approvalof tender awards for all supplies, services andworks has been increased to RM100 million,while for restricted tenders, they have been givenauthority of up to RM10 million.

In order to accelerate project implementation aswell as reduce processes, the Governmentappointed project management consultants(PMCs) to supervise public sector projects.Projects were also awarded on turnkey anddesign-and-build basis to shorten processing timeas well as expedite project completion.

In terms of expediting payments, all ministriesand agencies are required to make paymentsup to 50% of the value claimed within 14 daysand full payment within 30 days upon receiptof full documentation as per contract requirement.For projects undertaken through PMCs, the latterare allowed to submit claims for payment directto the Accountant General’s office, for whichpayment will be made within 10 days. To facilitateearly project startups, all contractors implementinggovernment projects are given advance paymentsof 15%, while for those implementing smallprojects under the pre-emptive package, advancepayments of up to 75% are allowed.

The Government also implemented the two-yearbudgeting process for the 2002-2003 Budget,with a view to improving the efficiency in thepreparation and examination of the annual budget.The two-year system will facilitate efficientplanning for fund utilisation and programmeimplementation while enabling greater efforts tobe directed towards project monitoring andevaluation.

Continuing the Agenda for CaringSociety

As in previous years, Budget 2001 incorporateda policy on caring society as a national agendain line with the Government’s empathy to theneeds of the less fortunate. In this respect, the

26

CORPORATE GOVERNANCE :AN UPDATE

Introduction

The importance of good corporate governance is increasingly recognised worldwide, particularlyin the context of enhancing investor confidence. Investment inflows are generally drawn to countrieswith credible corporate governance practices. In light of the keen competition for investment, theadherence to good corporate governance practices is an imperative that cannot be ignored. Evenwithin the country, good corporate governance practices will help boost the confidence of domesticinvestors and ultimately induce more stable sources of financing for industries and the capitalmarket. A recent survey on emerging markets also indicated the strong correlation between corporategovernance and price performance of stocks.

Efforts to address corporate governance in Malaysia began way before the Asian financial crisis,although the crisis provided the impetus to accelerate corporate governance reforms. A high levelFinance Committee was established in 1998, comprising both government and industry representatives.The committee was tasked with establishing a framework for corporate governance and settingbest practices for the industry.

Understanding Corporate Governance

There is no one standard definition of corporate governance. The Finance Committee Report defines“Corporate governance as the process and structure used to manage the business and affairs ofthe company towards enhancing business prosperity and corporate accountability, with the ultimateobjective of realising long-term shareholder value, whilst taking into account the interests of otherstakeholders”.

Corporate governance is premised on the principles of transparency, accountability, fairness andresponsibility, which are universal in their application. The implementation of corporate governanceis usually a combination of regulation by the appropriate authorities and self-regulation by themarket. It is, however, observed that statutory regulation alone cannot promote effective governance.Corporate governance initiatives tend to win most support when driven from the bottom up vis-à-vis from the top down.

Finance Committee Report on Corporate Governance

The Finance Committee on Corporate Governance released the Report on Corporate Governancein March 1999, comprising 70 recommendations. The thrust of reform efforts is focussed on strengtheningthe influence of minority shareholders, enhancing the role of boards of public listed companies(PLCs), strengthening regulatory enforcement and promoting high standards of corporate governancethrough training and education. The key recommendations of the Finance Committee Report centredon effecting legal reforms alongside the introduction of a Malaysian Code on Corporate Governanceas well as facilitating training and education at all levels and promoting active participation of minorityshareholders.

An Implementation Project Team (IPT) was also formed and tasked to lead and oversee the implementationof the recommendations of the Report. The progress of the IPT is monitored by the FinanceCommittee to ensure the necessary balance between public and private sector interests in addressingthe various implementation issues. Significant progress has been made in the implementation ofthe Report’s recommendations, particularly in respect of disclosure requirements as well as enhancedstandards of corporate governance and investor protection.

27

■ Malaysian Code on Corporate Governance

The Malaysian Code on Corporate Governance was released in March 2000. The code essentiallyaims at setting out best practices in corporate governance. Although compliance to the code isvoluntary, it is coupled with a requirement in the Listing Requirements of the Kuala Lumpur StockExchange (KLSE), which mandates disclosure of the extent of compliance with principles and bestpractices.

■ Legal and Regulatory Reforms

Effective 1 July 2000, amendments to the securities legislation were made to enhance primarymarket disclosures. The amendments have effectively delineated and streamlined the responsibilitiesof the Securities Commission and the Registrar of Companies with regard to prospectuses, thusresulting in greater legal and regulatory certainty in the area of public offerings of securities.

Further changes have been recommended to the securities and company laws. Among the intendedchanges include the requirement for auditors to report suspected breaches of securities laws, thecodification of key duties of directors and provisions to curb a controlling shareholder’s right tovote in cases involving related party transactions. The implementation of these measures is currentlyunder way.

The revamped Kuala Lumpur Stock Exchange (KLSE) Listing Requirements, released on 22 January2001 are primarily aimed at enhancing standards of corporate governance and investor protection.New provisions have been introduced with existing provisions strengthened in areas relating todisclosure, internal controls, continuing listing obligations, financial reporting and protection ofminority shareholders.

■ Minority Shareholder Watchdog Group

A Minority Shareholder Watchdog Group has been set up to encourage proactive shareholderparticipation in PLCs. It comprises the Employees Provident Fund (EPF), Armed Forces Fund,Pilgrims Fund Board, Social Security Organisation (SOCSO) and Permodalan Nasional Berhad(PNB), representing the largest institutional funds in the country. The Watchdog Group, which isintended to harness the ability of large, albeit minority institutional investors to monitor and institutechange where necessary in the companies they have invested, is expected to be fully operationalin the near future.

■ Training and Education

Amendments were made to the KLSE Listing Requirements to introduce the mandatory accreditationof directors of PLCs as a prerequisite to continued listing. As a measure to enhance standardsof competency and professionalism amongst company directors, directors of PLCs are requiredto attend a prescribed training programme. In this regard, the Malaysian Institute of CorporateGovernance (MICG) is currently undertaking on-going training and education for directors as wellas company secretaries, auditors and investors on corporate governance.

■ Capital Market Master Plan

The Capital Market Master Plan (CMP), which was released in February 2001, comprehensivelycharts the strategic positioning of the Malaysian capital market over the next 10 years. Of the152recommendations in the CMP, there are 10 recommendations related directly to corporate governance.The CMP builds on the Finance Committee Report’s recommendations and further develops thecorporate governance reform agenda in a number of key areas relating to the disclosure of timelyand accurate corporate information, accountability of company directors, financial controllers andmanagement as well as strengthening the role of auditors, encouraging greater institutional investor

28

participation in corporate governance and promoting shareholder activism. The CMP further reinforcesthe corporate governance agenda as a strategic thrust to further enhance investor confidence aswell as developing an efficient and competitive capital market.

Conclusion

It is imperative to move forward in addressing corporate governance issues, particularly in the lightof investors being driven more by sentiment and perception, rather than fundamentals. This is evenmore pertinent given the increasing integration and dynamism of global financial markets, wherelarge flows of funds can be easily transferred across the globe within seconds, facilitated bytechnology advancements. Although notable progress has been achieved in corporate governance,companies need to institute measures to continuously innovate and adapt their corporate governancepractices in order to meet new challenges and seize opportunities. The Government, on its part,is committed towards the enhancement of corporate governance. Measures have and will continueto be taken to further accelerate the corporate governance agenda towards developing the Malaysiancapital market as the preferred fund raising centre for Malaysian companies as well as in attractingforeign investment.

Government has intensified efforts to ensure amore equitable distribution of wealth and benefits,and avoid marginalisation of the disadvantagedgroups. Thus, higher allocations have beenchannelled towards programmes aimed atincreasing the incomes of the poor, enhancingrural accessibility to public utilities and amenities,upgrading rural health facilities and services aswell as improving opportunities for better educationand employment prospects.

In recognition of the contributory role of womenin development, the Government has establishedthe Ministry of Women and Family Development.With the formation of the Ministry, issues andproblems specific to women, including childrenand family, will be given greater focus andattention. Since its establishment, a significantachievement was the amendment of Article 8(2)of the Federal Constitution to include the word‘gender’ so that there would no longer be anylaw or policy which discriminates against women.The Ministry also launched the Women AgainstViolence or WAVE campaign in July 2001, whichis targetted to eliminate all forms of violence,especially violence against women. Efforts willcontinue to be undertaken to further theparticipation and involvement of women in thesocial and economic development of the countryas well as develop Malaysia into a nation of

character, built by families that are resilient, ethical,healthy, knowledgeable and harmonious.

Attack on the US - - - Managing Uncertainties

Following the attack on the US, the outlook ofthe global economy becomes increasinglyuncertain. The attack has not only altered theprospects for an early recovery, but also increasedthe risk of the US economy entering into arecession. The US being the largest economyin the world and accounting for about one-fifthof world output and exports, the contagion onthe economies of major industrialised countriesand the rest of the world would be significant.

Even before the attack, there was increasedevidence of a more protracted slowdown of theworld economy, primarily on account of the sharperdecline in output growth in the three maineconomic blocks, namely the US, Japan andthe euro area. The decline in the US manufacturingoutput continued to worsen, its equity marketbecame increasingly volati le, while theunemployment rate edged upwards and businesssentiment deteriorated. At the same time, Japan,the second largest economy, has not shown anysign of recovery. Depressed consumer demand,

29

weak external sector and a lacklustre pace offinancial and corporate sector restructuring havepointed towards a contraction in Japan’s outputgrowth. The outlook for the euro area becamemore pessimistic with Germany, its largesteconomy, experiencing a stronger downturn,particularly in its industrial sector. The rigiditiesin the labour market and constraints in theEuropean Central Bank (ECB) monetary policyalso contributed to the greater pessimism.

In the aftermath of the attack, the US equitymarket was badly affected with the Dow Jonesdeclining by 684.8 points when it reopened on17 September to close below 9,000 points, thelargest one-day fall ever recorded. There werealso heavy sell-offs across major bourses andfinancial markets. On the day of the attack, stockprices worldwide fell sharply lower, with amongothers, the DAX index plunging by 8.5% in itsbiggest one-day fall and the FTSE index by5.7%, marking its largest single-day fall since1987. The Nikkei index, which had already fallento a 17-year low of 10,196 points on 10 September,declined further by 5.7% to a new low of 9,610.1points on 11 September. Other regional bourses,such as the Hang Seng and the STI also declinedby 8.9% and 7.4%, respectively. Similarly, indicesof the Taiwan, Thailand and Kuala Lumpur stockmarkets, which reopened on 13 September, fellby between 3.8% and 6.7%.

The US dollar has shown signs of greaterpressures as investors liquidate into other ‘safehaven’ currencies. The dollar has beendepreciating against the euro and yen since Julythis year, triggered by changing marketperceptions that the US stance on a strong dollarpolicy had softened as well as the weakeninginvestor sentiment, as reflected by the declinein the US stock market. Since the attack, thedollar has further weakened, declining by 2.4%and 2.5% against the yen and euro, respectivelyas at 27 September.

In response to these adverse developments,the US Administration has put in place a seriesof measures to arrest the slide in investorsentiment and consumer confidence as well asto contain any further decline in the equity markets.The US Fed has injected liquidity into the financialsystem and undertook a further cut in interest

rates. The US Congress has approved USD40billion fiscal allocations for reconstruction, reliefwork and security. A bail-out package of USD15billion has also been approved for the airlines.

In response to the US move, other monetaryauthorities have also taken measures to containand ease the immediate adverse impact on theireconomies. In this regard, a coordinated actionby major central banks has also been taken toreduce interest rates to improve confidence. TheECB has reduced the repo rate by 50 basispoints to 3.75% while the Bank of Japan (BOJ)reduced the discount rate by 15 basis points to0.10%. In addition, with the US dollar depreciatingbroadly against all major currencies, there areexpectations of joint foreign exchange interventionby the G7 authorities, particularly should excessivevolatility occur.

In addition to the impact on global equity andfinancial markets as well as the real economy,the September 11 attack has also clouded effortsin international financial cooperation. Theinternational community’s attention has now beendiverted to address issues pertaining to security,combatting terrorism as well as immediaterecovery measures to counter the deteriorationin the global economic environment. Severalmajor international meetings, such as the WorldBank and International Monetary Fund (IMF)Meetings as well as the Commonwealth meetingsat the level of Finance Ministers and Heads ofGovernments have either been cancelled orpostponed. In the light of these developments,progress on important international financial issuesof concern for developing countries could facea setback, such as efforts in reforming theinternational financial architecture, enhancingsupport for least developed countries (LDCs)through debt relief and leveraging trade fordevelopment, combatting money laundering,strengthening corporate governance as well asother initiatives in the pipeline. The turn of eventshas cast further uncertainty over future effortsto deliberate on collaborative initiatives, includingthe possibility of depriving developing countriesthe opportunity of putting forth issues of concern,particularly relating to the multilateral tradingsystem at the upcoming Fourth World TradeOrganisation (WTO) Ministerial Conferencescheduled in November 2001 in Doha, Qatar.The impact of such delays could have far-reachingimplications for developing countries.

30

Malaysia, being an open economy, where tradeaccounts for more than 200% of GDP, was alsoadversely affected by these externaldevelopments. The growth forecast of theMalaysian economy, which was reviseddownwards to 5-6% for 2001 in March from theBudget 2001 estimate of 7.5%, is being furtheradjusted to 1-2%, following primarily the recentdevelopments in the US.

Notwithstanding this, the strong fundamentalsof the Malaysian economy continue to providesufficient policy flexibility to implement growth-supporting measures to stimulate domesticeconomic activities without jeopardising thesustainability of the nation’s potential growthprospects in the medium- and long-term. Thenation’s current account in the balance ofpayments continues to register strong surplusessince 1998. The external reserves has stabilizedat a higher level and is sufficient to finance 4.6months of retained imports and is 6.2 timesshort-term liabilities, while external debt remainslow and inflation subdued.

In response to the adverse developments in theexternal sector and with a view to minimisingits immediate adverse spillover effects, theGovernment announced another stimulus packageof RM4.3 billion on 25 September 2001. Apartfrom adding further stimulus to domestic economicactivities, the package also aims to cushion theimplications on the poor and other less advantagedsegments of the society from the impact of theeconomic slowdown, generating business andincome opportunities for small enterprises aswell as providing skills training. The largestallocation of RM1 billion is provided for smallprojects in rural and selected urban areasincluding, among others, the construction andupgrading of roads, bridges, water and electricitysupply, and community-based projects. In addition,computer laboratories will be constructed in 2,000more schools, while maintenance works ongovernment buildings and facilities will be steppedup. The package also provides for the doublingof current rates of welfare payments, monthlyallowance for degree and diploma holders tolearn IT, mathematics and languages as well asthe promotion of tourism.

Monetary policy continues to be accommodativeto reinforce fiscal stimulus to sustain economicgrowth. The adoption of an easier monetary stancewill continue to be monitored against domesticand external developments. Following the cuts

in interest rates in the US, BNM reduced its3-month intervention rate on 20 September by50 basis points to 5%. The reduction marks thefirst cut by BNM in more than two years, andis in line with the action taken by several othercentral banks, following the worsening externalenvironment. It is also aimed at enhancingdomestic business sentiment and consumerconfidence to support economic activities.

On the medium-term impact, the prospects remainuncertain as events continue to unfold. ForMalaysia, the diff iculties in the externalenvironment have emerged at the time whenthe nation is just at its first year of the ThirdOutline Perspective Plan (OPP3), 2001-2010 andthe Eighth Malaysia Plan, 2001-2005. To achievethe long-term objective of Vision 2020 of attaininga developed nation status, both Plans projectedan average GDP growth of 7.5% per annum.The slower growth of 1-2% this year and moderaterecovery of 4-5% anticipated next year, however,would necessitate greater efforts at acceleratinggrowth in the subsequent years to recoup lostground during the first two years of the Plans.Given the strong foundation already in place forthe economy, the prospects of accelerating GDPgrowth remain plausible. The Asian financial crisishas shown that despite experiencing the worst-ever recession with the economy contracting by7.4% in 1998, Malaysia was able to recoverstrongly in the following years, with growth ratesof 6.1% and 8.3% in 1999 and 2000, respectively,thereby achieving the growth target of 7.5 % ofthe Second Outline Perspective Plan (OPP2).

Conclusion

The recent development in the US has led togreater uncertainties. As events continue to unfold,the prospect of an early recovery in the US andthe global economy, generally, has becomeincreasingly difficult. In the light of this, theGovernment will constantly monitor and assessdevelopments in the external sector and theirimpact on the economy. Further measuresprimarily premised on promoting growththrough strengthening resil ience andenhancing competitiveness will be put inplace to contain and minimise any immediateadverse spillover effects on the economy and,thus, avoiding further slide in the nation’sgrowth. With the strong economic fundamentalscoupled with flexible and pragmatic policyresponses, the nation will be able to return toits stronger growth path.

Performance and Prospects of theMalaysian Economy2

Overview Of The MalaysianEconomy In 2001

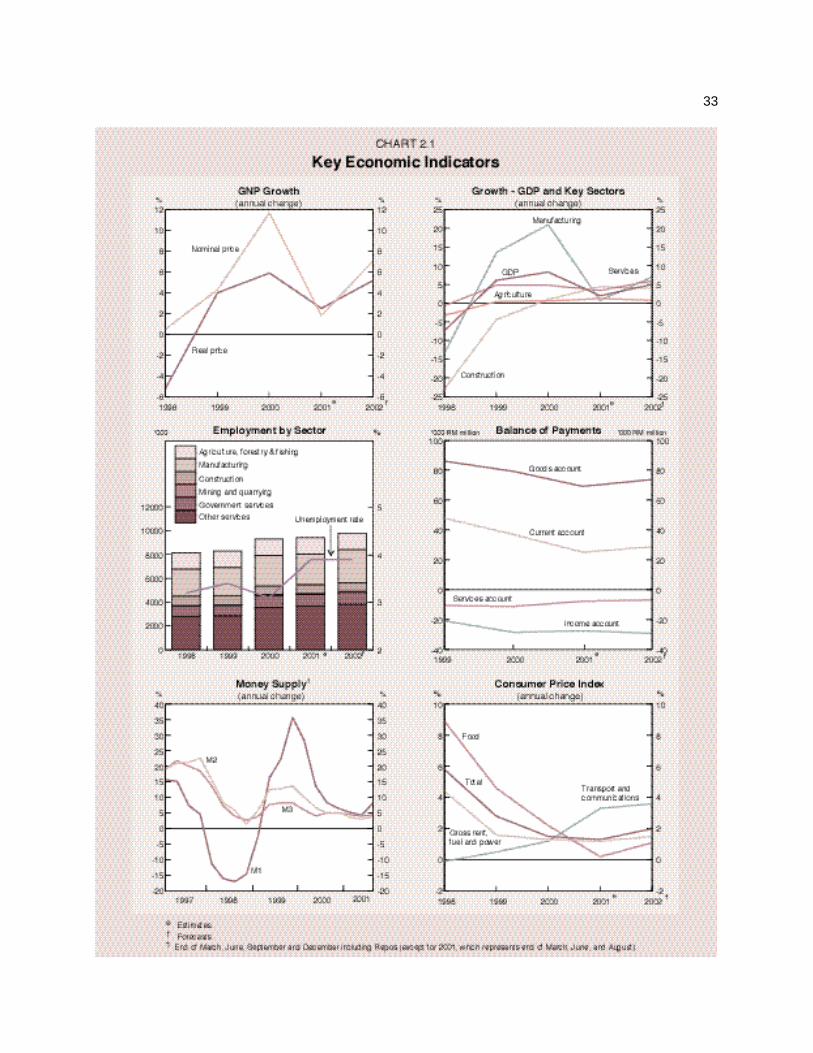

T he performance of the Malaysian economyin 2001 has been adversely affected by the

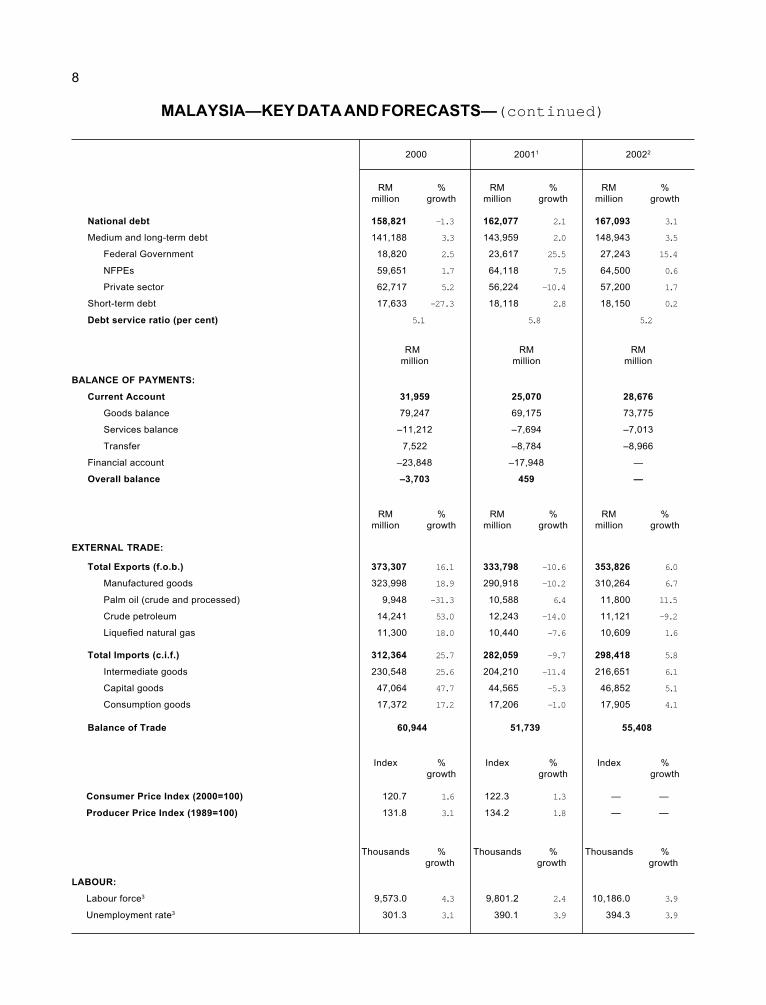

greater-than-expected slowdown in the worldeconomy, particularly in the United States (US)as well as the continuing weak performance ofthe Japanese economy. The recent attack onthe US has led to greater uncertainties withrespect to the severity and duration of the recoveryin the US. There are concerns on the risks ofthe US economy entering into a recession andits contagion on other industrialised anddeveloping economies. In the light of the moredifficult environment, real GDP growth of theMalaysian economy is projected to grow by 1-2% for 2001. Following the lower growth in nominalvalue, Gross National Product (GNP) of 1.8%,GNP per capita is forecast to be somewhat lowerat RM13,333 or USD3,509 (2000: RM13,411 orUSD3,529). In terms of purchasing power parity,however, per capita income is expected toincrease by 1.3% to USD8,944 (2000: USD8,831),after taking into account lower domestic inflation.

All major sectors are expected to be adverselyaffected by the slower growth in the economy,particularly manufacturing which is estimated torecord a sharp deterioration in output growth.The steep decline in value added of themanufacturing sector has, however, to someextent been offset by the better performancefrom the agriculture, construction and servicessectors. The services sector has provided thelead in the growth of the economy on accountof better performance of government servicesand other services sub-sectors. In the construction

sector, fiscal stimulus efforts by the Government,particularly for infrastructure projects coupledwith the construction of low-and medium- costresidential houses, have contributed towards itshigher growth. In the agriculture sector, the higheroutput from palm oil has resulted in a higherrate of growth for the sector.

Given the growing difficulties in the externalenvironment, growth in real GDP has been largelydomestic-led. Expansion in aggregate domesticdemand is driven largely by public sectorinvestment and consumption on account of largerfiscal expansion. Private sector demand in nominalvalue is expected to decline markedly, given theweaker-than-expected external demand whichhas affected investment in manufacturing activitiesas well as the continued reduction in investmentin the property sector, particularly office space,hotels and retail outlets. Given the significantslowdown in private investment activities, thepublic sector implemented additional fiscalstimulus packages to stimulate domestic activities.Consequently, public expenditure, both investmentand consumption, expanded significantly tocontinue registering double-digit growth.Notwithstanding the rapid expansion in publicsector expenditure, the nation’s resource positionremains in surplus although gross national savingsis estimated to decline on account of slowergrowth in income.

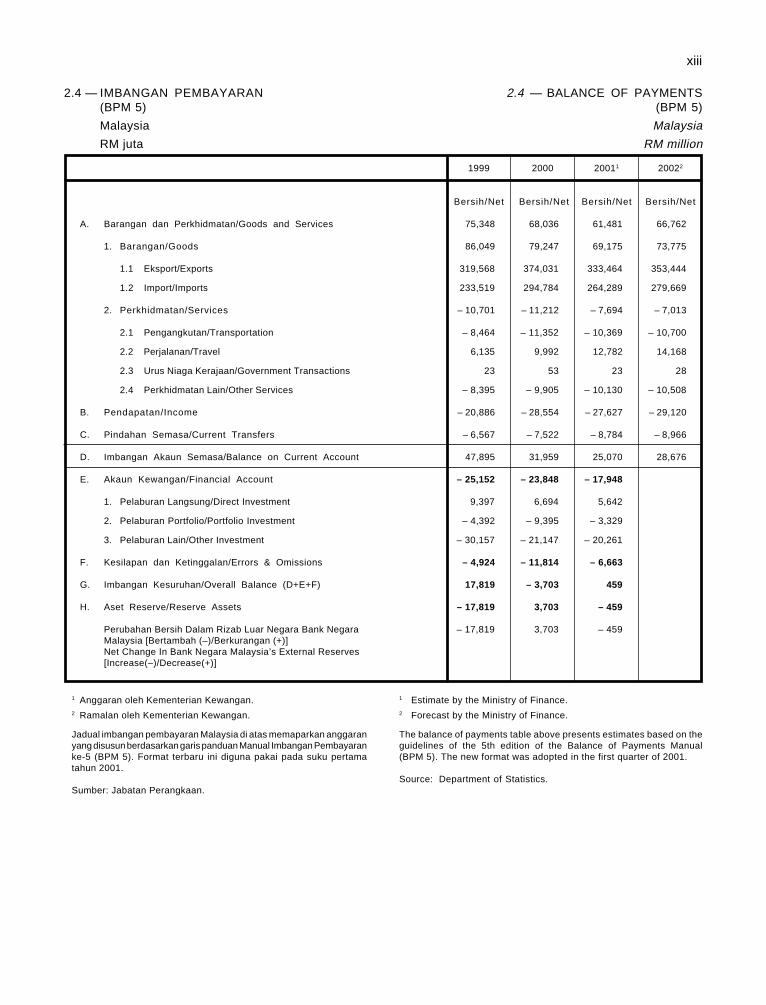

The balance of payments position continues toremain favourable. The current account surplus,while narrowing, remains strong. The lower surplusin the current account is partly attributable to asmaller surplus in the goods account against awidening deficit in the transfers account. Thegoods account is expected to register a smaller

32

surplus due to the sharp contraction in exports,while the transfers account deficit continue towiden as a result of higher remittance by foreignworkers. Nevertheless, the services account deficitis likely to improve due to higher net inflow inthe travel account and lower net outflow in thetransport account. Consequently, the currentaccount of the balance of payments is projectedto record a smaller surplus of 7.9% of GNP.With the deficit in the financial account likely toimprove due to smaller net outflows of portfolioand other investments, the overall balance ofpayments is expected to turn around to recorda surplus of RM459 million.

Malaysia’s economic growth continues to beachieved within an environment of low inflationand unemployment. Inflation remains subduedand stable largely on account of the moderationin private sector demand as well as measuresimplemented by the Government to contain priceincreases. In spite of higher retrenchments, thenation still enjoys full employment.

Sectoral Output Performance

The output of major sectors in the economy isexpected to register a slower growth, with thesharpest deterioration expected in themanufacturing sector. The performance of theprimary sector is mixed, with agriculture registeringhigher growth and the mining sector almoststagnating. In the secondary sector, the mostaffected sector is manufacturing with growthdeteriorating significantly, while the constructionsector has benefitted from the fiscal expansionof the public sector. The services sectorperformance is also mixed with sub-sectors suchas electricity and gas and transportation affectedby the slowdown in the manufacturing sector toregister moderate growth, while the governmentservices and other services sub-sectors areanticipated to register higher rates of growth.

The manufacturing sector is expected todecelerate significantly to 0.2% in 2001 (2000:21%) after seven consecutive quarters of robustdouble-digit growth. The decline is largelyattributable to a depressed global market forelectronic products. Given that electronics accountfor close to half of Malaysian manufactured

exports, the output performance of the electronicsindustry, which has deteriorated to 13.1% duringthe first seven months of 2001 (January-July2000: 15.1%), has impacted significantly on thegrowth of the manufacturing sector. While theexport-oriented industries have been adverselyaffected by weak external demand, the domestic-oriented industries have shown greater resilience,largely due to the expansion of output of industriesproducing construction-related materials, transportequipment and consumer products as well asresource-based industries. The growth in theseindustries has provided the support to growthand somewhat cushioned the contraction in themanufacturing sector. The overall decelerationin the sector’s growth has resulted in itscontribution to GDP declining sharply to 0.1percentage point to real GDP growth (2000: 6.3percentage points).

The agriculture, livestock, forestry and fishingsector is envisaged to expand at a higher rateof 1.2% (2000: 0.6%), largely on account ofhigher palm oil output. The output of rubber andsaw logs, however, continues to decline.

In the mining sector, the higher production ofnatural gas is expected to offset the decline incrude oil production. As such, the sector’s outputis projected to increase marginally by 0.9%(2000: 3.1%).

Value added of the construction sector, on theother hand, is expected to expand at a higherrate of 4.9% (2000: 1.0%), spurred by theGovernment’s fiscal expansion programme,particularly for infrastructure projects and theconstruction of low- and medium-cost residentialhousing.

The services sector is projected to continue tosustain its growth at 4.4% (2000: 4.8%). Whilethe electricity, gas and water, wholesale andretail trade and hotels and restaurants sub-sectorsare expected to record moderation in growth intandem with the slowdown in the manufacturingsector and the generally subdued consumersentiment, the finance, insurance, real estateand business services sub-sector is estimatedto achieve strong growth, mainly attributable tothe low interest rates which resulted in higherbank lending especially for housing and consumer

33

34

durables as well as higher demand for insuranceproducts. Given that the services sectoraccounts for 54.6% of GDP, the overall strongergrowth from the sector and the anticipated markeddeterioration in the contribution from themanufacturing sector will result in the servicessector providing the leading contribution to overallgrowth of 2.3 percentage points to GDP growth(2000: 2.6 percentage points).

Domestic Demand

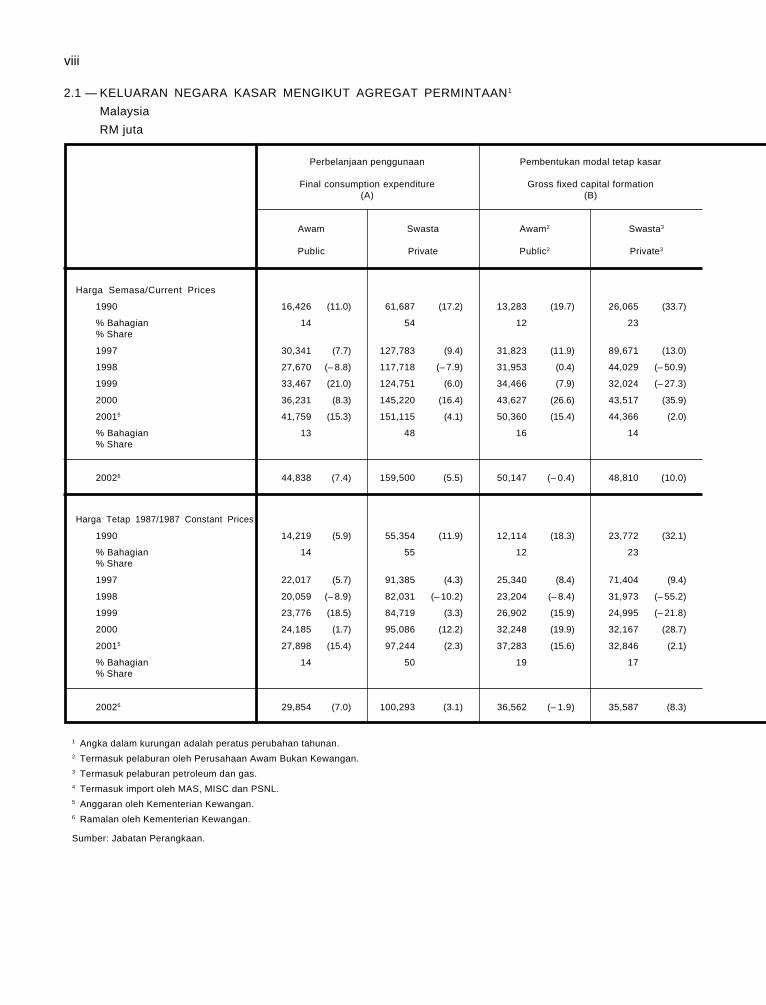

After registering a strong growth of 19.5% in2000, aggregate domestic demand (excludingchanges in stocks) is expected to moderatesignificantly to 7.1%. The relatively slower growthis attributable to weaker private sectorexpenditure, with growth deteriorating sharplyto 3.6% compared with 20.4% in the previousyear. The deterioration in private sector spendingwas somewhat offset by the large fiscal expansionof the public sector with public sectorexpenditure projected to expand strongly by15.4% (2000: 17.6%).

Public investment is envisaged to maintain itsdouble-digit growth of 15.4% (2000: 26.6%). TheFederal Government expenditure in Budget 2001was further augmented by the implementationof a pre-emptive package of RM3 billion in Marchas well as an additional RM4.3 billion inSeptember, in response to the anticipated growingdifficulties following the attack on the US. Apartfrom the Federal Government, the non-financialpublic enterprises (NFPEs), in particular PetroliamNasional Berhad, Tenaga Nasional Berhad andTelekom Malaysia Berhad, also expanded theirexpenditure in new investments for purposes ofupgrading services and capacity expansion. Theexpansion in public sector expenditure is expectedto result in the share of public sector investmentincreasing to 53.2% in 2001 from 50.1% in 2000of total investment, and accounting for 2.4percentage points of GDP growth (2000: 2.8percentage points).

Public consumption which accounts for 45.3%of total public expenditure is expected to registerhigher growth of 15.3% (2000: 8.3%) to supportthe expansion in public investment. The increase

is largely for supplies and services andemolument. The stronger growth in publicconsumption is expected to increase its shareof total consumption to 21.7% in 2001 (2000:20%).

Private sector investment has been adverselyaffected, particularly by the deterioration in theoutput growth of the manufacturing sector aswell as the continued reduction in investmentoutlay in the property sector, especially in officespace, hotels and retail outlets. Consequently,growth in private investment is expected todecelerate sharply to 2% from its strong double-digit growth of 35.9% in 2000. Its share of totalinvestment is, therefore, expected to decline to46.8% compared with 49.9% in 2000.

Private consumption spending is also expectedto expand by 4.1% (2000: 16.4%). This is onaccount of the slight contraction in private sector’sdisposable income attributable to the lowercorporate earnings of the export-orientedindustries and the negative wealth effect fromthe subdued stock market as well as greateruncertainties in employment prospects, whichhave led to more cautious consumer sentiment.To promote private consumption, the Governmenthas introduced several measures in Budget 2001,including providing higher tax rebates to individualtaxpayers, relaxing Government employees’eligibility for car loans, reducing employees’contribution to the Employees Provident Fund(EPF) as well as removing the RM50 charge oncredit cards.

External Demand

The performance of the nation’s external demandhas been severely affected by the markedslowdown in the industrialised economies,particularly by the sharper-than-expecteddownturn in the global electronics cycle. Exportof goods and non-factor services is expectedto contract sharply by 9.3% (2000: 17%), afterfifteen years of sustainable strong growth.Consequently, the share from external demandto GDP is expected to reduce to 112.3%(2000: 125.5%).

35

Export of goods is envisaged to decline by10.8% to RM333,464 million after a strong double-digit growth of 17% in 2000, led by a significantcontraction in the exports of manufactured goods,particularly electronics. The weak global demandfor electronics has led to sales of electronicsdeclining sharply, resulting in a large inventoryoverhang. The export performance of majorcommodities is also expected to remainunfavourable, primarily attributable to lower pricesfor all major commodities, including palm oiland crude oil. Export of non-factor services isexpected to decelerate to 1.7% compared with16.8% in 2000. This is in tandem with lowerexports of goods. Within the non-factor services,the stronger contribution from tourism has,however, continued to support the sector’s output.For the period January-August 2001, touristarrivals totalled 9.5 million, an increase of 44.1%over the same period in 2000.

Similarly, the import of goods and non-factorservices is expected to reduce by 9.2% comparedwith a strong double-digit of 23.9% in 2000. Thedecline reflects mainly moderation in domesticdemand conditions as well as the reduction inimports of intermediate inputs for themanufacturing sector. The slower growth in privateinvestment also resulted in lower imports forcapital goods, while the more cautious consumersentiment has led to a more subdued import ofconsumption goods. The import of intermediategoods is expected to register a significantcontraction of 11.4%, while the import of capitaland consumption goods are anticipated to registera relatively smaller decline of 1% and 5.3%,respectively.

Balance of Payments

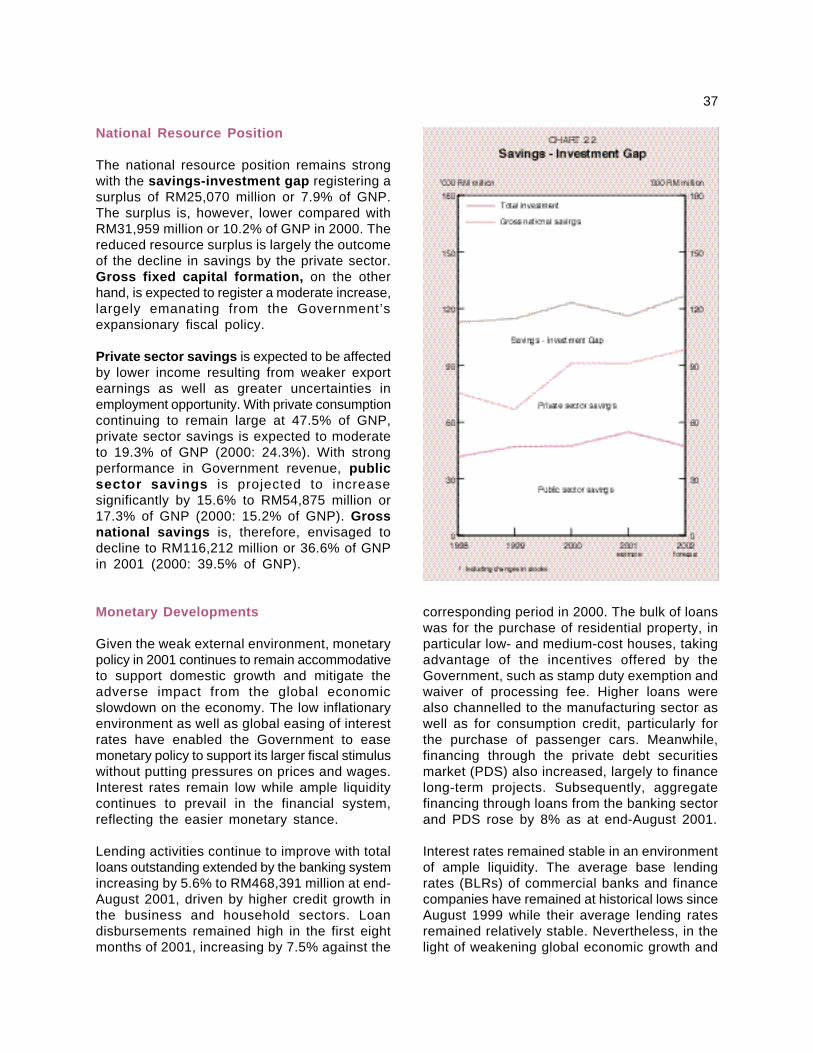

Malaysia’s balance of payments position isenvisaged to remain strong despite continuedweakening in the external environment. Thesurplus in the current account remains large atRM25,070 million or 7.9% of GNP (2000: 10.2%of GNP), registering the fourth consecutive surplussince 1998. The smaller surplus is partly dueto a lower net inflow in the goods account andthe continued larger net outflow in the transfersaccount.

The goods account is expected to continue toregister a surplus of RM69,175 million, albeitsmaller than RM79,247 million in 2000. Thesmaller surplus is attributable to the sharperdecline in exports (10.8%) relative to imports(10.3%). In the services account, lower importsas well as the contraction in exports are expectedto reduce the outflow in transportation and otherservices. At the same time, the higher receiptfrom travel, largely from the significant increasein the number of incoming tourists, is expectedto contribute to the significant narrowing of thedeficit in the services account to RM7,694 million(2000: -RM11,212 million).

With lower corporate earnings arising from weakerexports, especially of multinational companiesin the electronics industries, the income account(mainly investment income) is expected to registera smaller deficit of RM27,627 million (2000:-RM28,554 mill ion) on account of lowerrepatriation of profits. The deficit in the transfersaccount is, however, envisaged to increase toRM8,784 million (2000: -RM7,522 million),following higher remittances abroad by foreignworkers.

The financial account, which comprises direct,portfolio and other investments, including loans,trade credits and bank deposits, is expected toperform better with a smaller net outflow ofRM17,948 million (2000: -RM23,848 million). Thebetter outcome is attributable to continuing netinflows of direct investment (RM5,642 million)as well as the lower net outflows of portfolioinvestment (-RM3,329 million) and otherinvestment (-RM20,261 million). The net inflowof direct investment reflects continuing investmentcommitment by foreign investors as well as foreignequity acquisition in selected services sub-sectors,such as shipping and transportation industries.As for other investment, the smaller net outflowis partly due to narrowing interest differentialsbetween domestic and international rates,particularly in the US, thus reducing the incentivefor Malaysians to retain funds abroad over alonger period. Reverse investment by Malaysiancompanies is expected to decline due to thestringent approval criteria by Bank NegaraMalaysia (BNM) as well as liquidation of businessoverseas, following corporate restructuringexercises undertaken by Malaysian companies.

36

The overall position of the balance of paymentsis expected to improve slightly to register a surplusof RM459 million after experiencing a large deficitof RM3,703 million in 2000. This surplus issignificant considering that net outflows due toerrors and omissions, which included foreignexchange revaluation loss, amounted to RM6,663million (2000: -RM11,814 million). Thus, the netinternational reserves is expected to remain strongduring the year. As at 29 September 2001, thelevel of reserves amounted to RM112,934 millionor USD29,720 million, a significant increase fromits lowest level in May 2001 (RM98,536 millionor USD25,931 million). The current reservesposition is adequate to finance 4.6 months ofretained imports and is 6.2 times the short-termexternal debt.

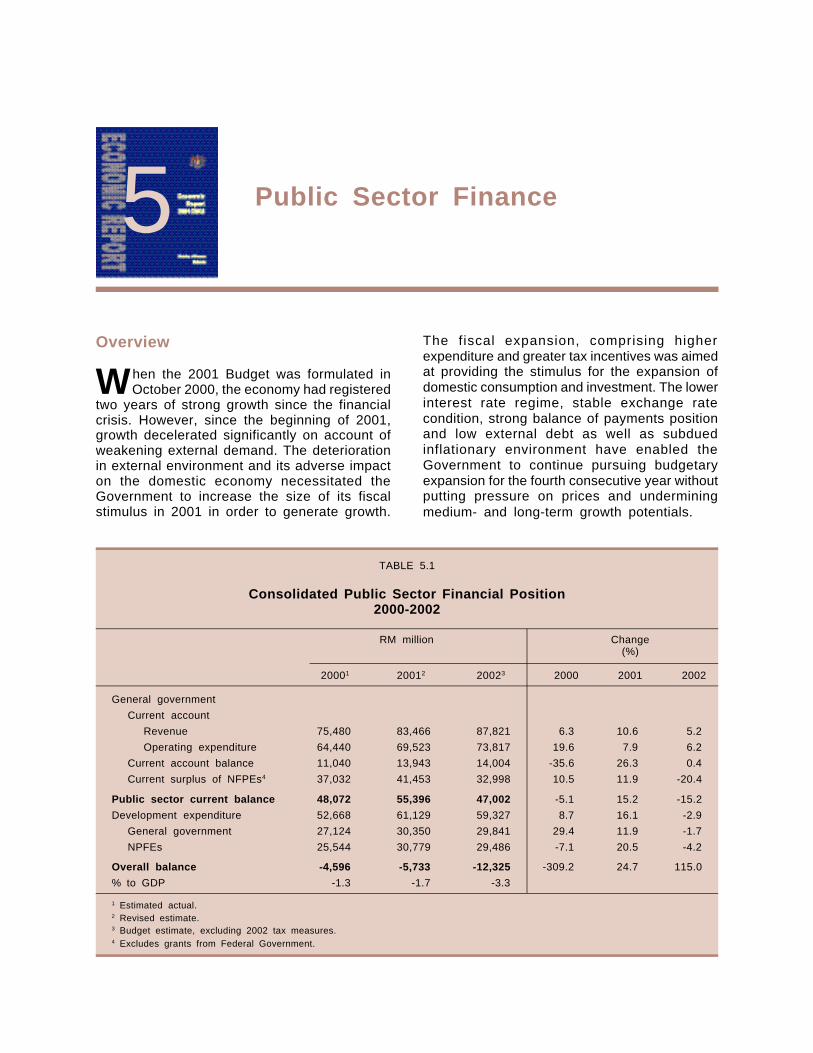

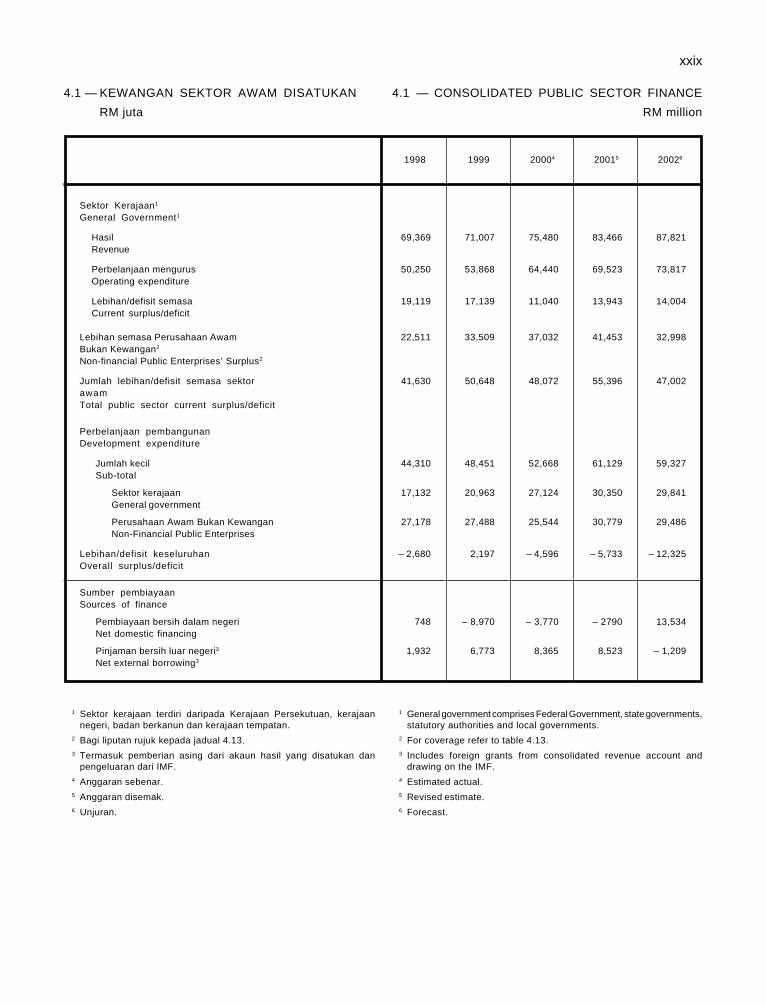

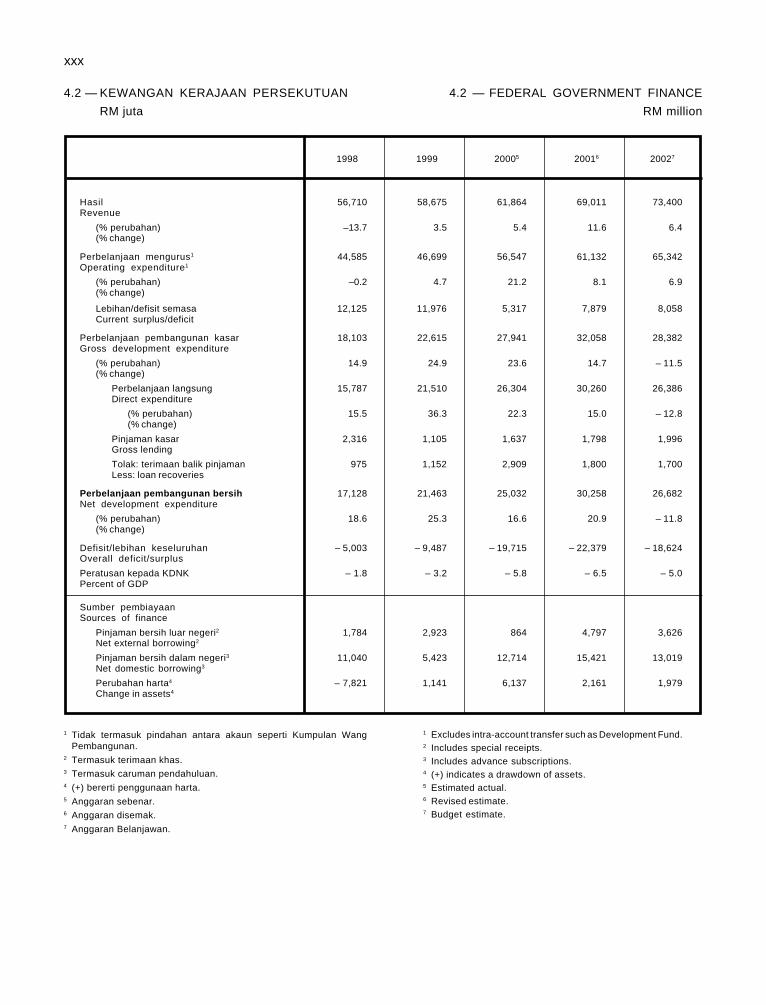

Federal Government Financial Position

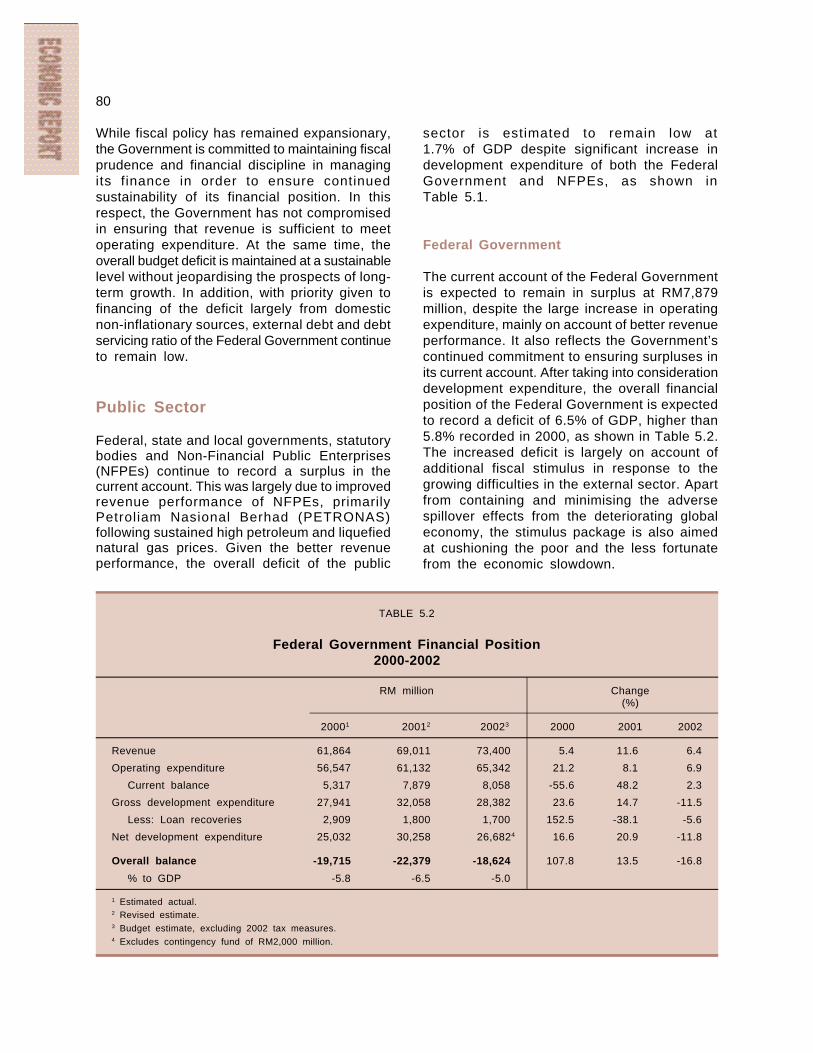

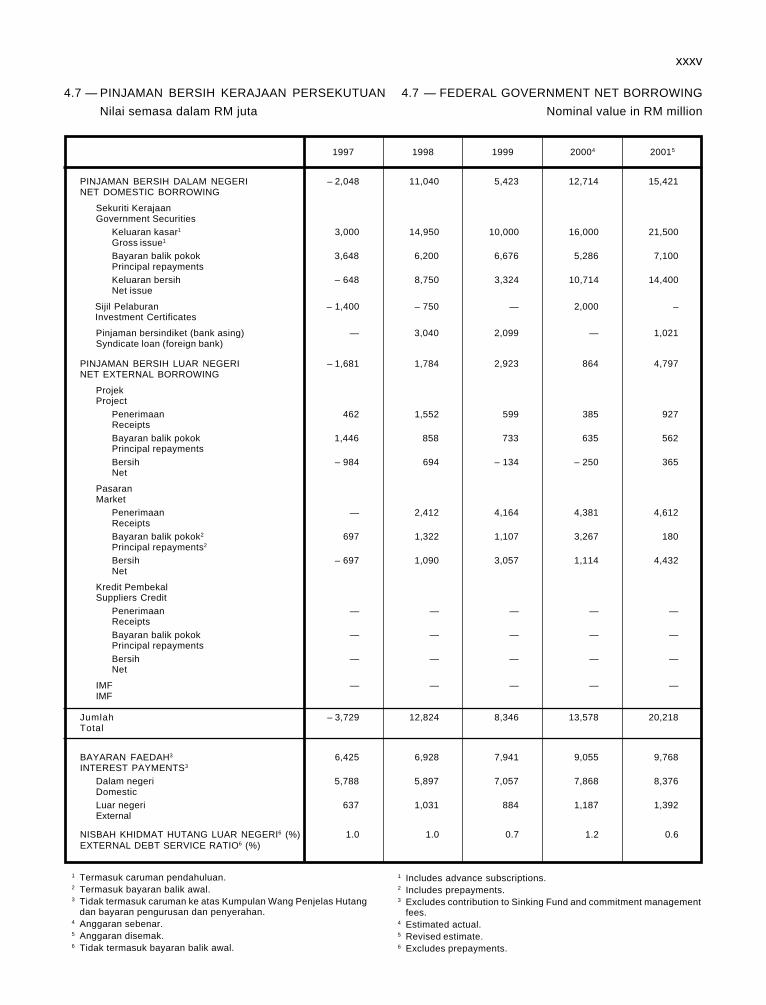

The continued weakening in the externalenvironment and its adverse impact on domesticprivate demand necessitated the Governmentto pursue a stronger expansionary fiscal stimulusto revive domestic economic activit ies.Consequently, the overall deficit of the FederalGovernment is estimated to register a largerdeficit of RM22,379 million or 6.5% of GDP,compared with RM19,715 million or 5.8% of GDPin 2000. Despite the larger deficit, the Governmentremains prudent and ensures financial disciplinein managing its financial resources. The deficitis still manageable and sustainable, given thatit is mainly financed from non-inflationary domesticsources and, hence, external debt and debtservicing ratio remain low.

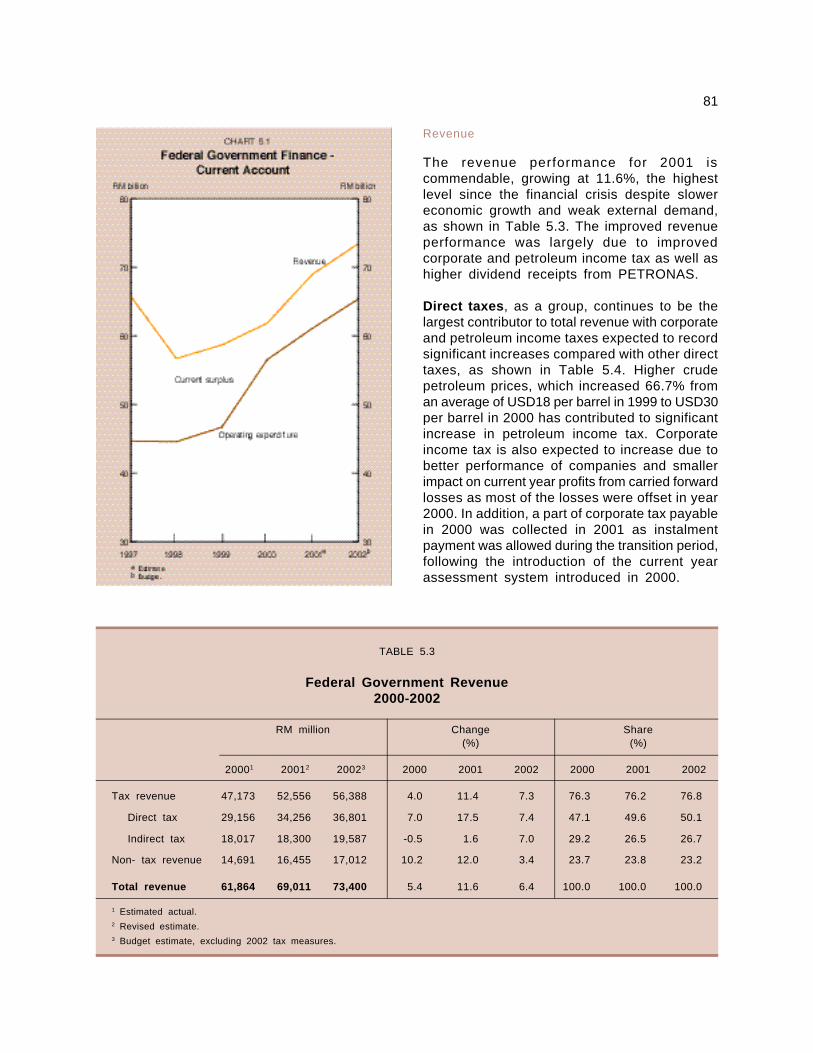

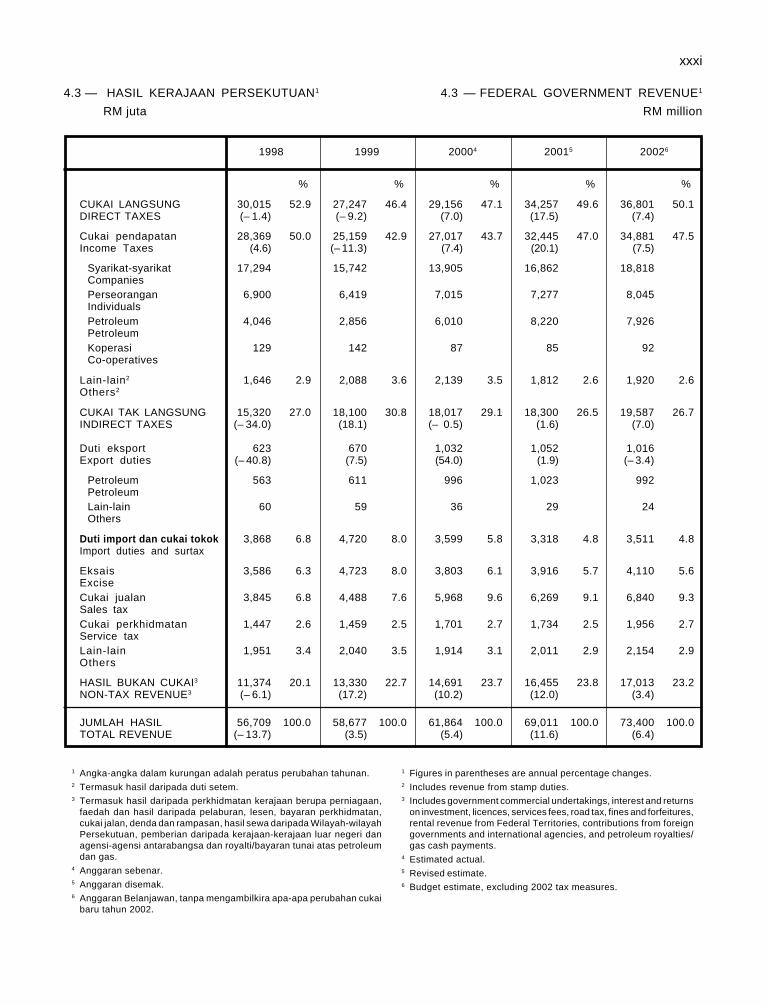

Federal Government revenue is expected toregister a strong performance of 11.6% to reachRM69,011 million, the highest growth achievedsince 1998, mainly attributable to higher collectionof corporate and petroleum income taxes. Thehigher corporate income tax is due to fewerlosses carried forward from previous years tooffset current year profits, while the highercollection from petroleum income tax is on accountof better petroleum prices, which increased fromUSD18 per barrel in 1999 to USD30 per barrelin 2000. Other major revenue sources include

sales tax, excise duties and service tax are alsoexpected to increase moderately. Non-taxrevenue, which includes investment income andfees from licenses and permits, is expected toperform well given the improved performance ofgovernment companies and buoyant sales ofmotor vehicles.

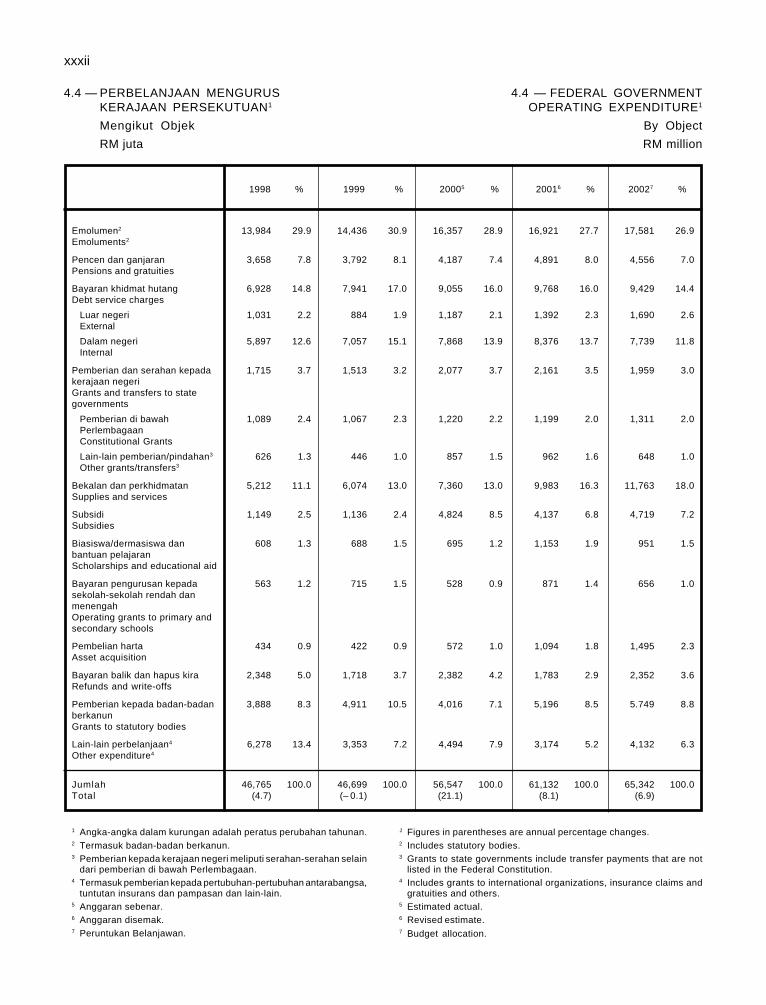

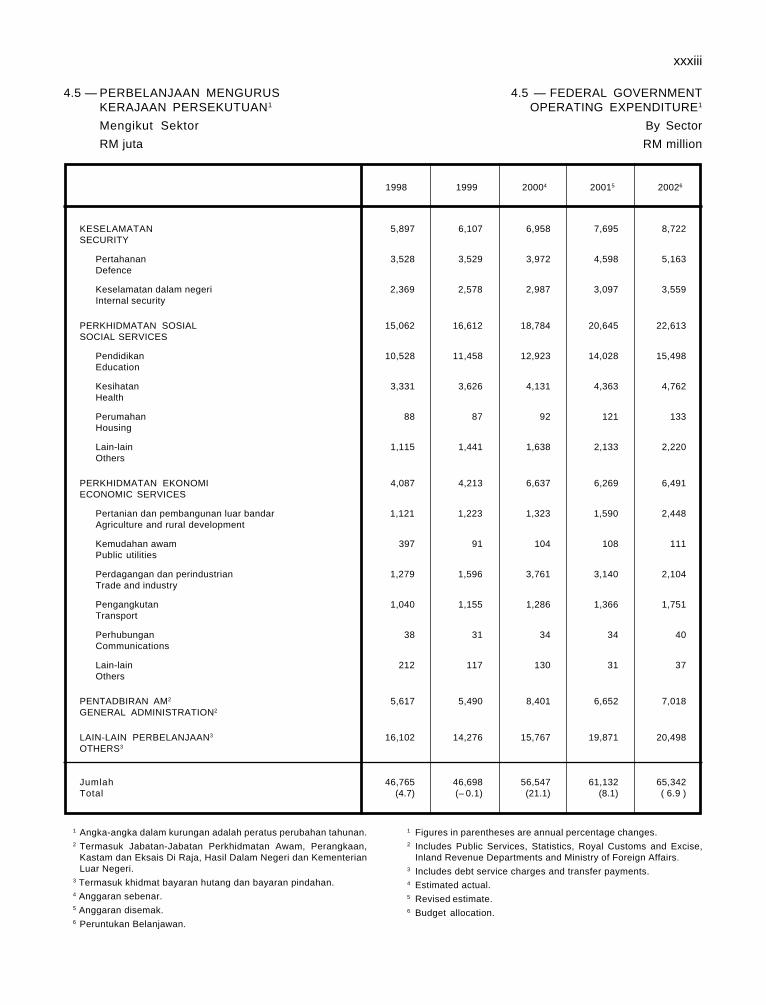

Operating expenditure is expected to increaseby 8.1% (2000: 21.2%), largely for emoluments,debt service charges and supplies and services.The bulk of expenditure is for supplies andservices as well as the increase in emolumentresulting from increased allowances, particularlyfor the police and armed forces personnel aswell as nurses, doctors and headmasters. Theexpenditure for debt service charges remainslow, mainly for domestic interest payments. Giventhe stronger performance in revenue and thesmaller increase in operating expenditure, thecurrent account of the Federal Government is,therefore, expected to record a higher surplusof RM7,879 million (2000: RM5,317 million). TheFederal Government has always maintained asurplus in its current account, reflecting continuedfiscal prudence and discipline in the managementof its finance.

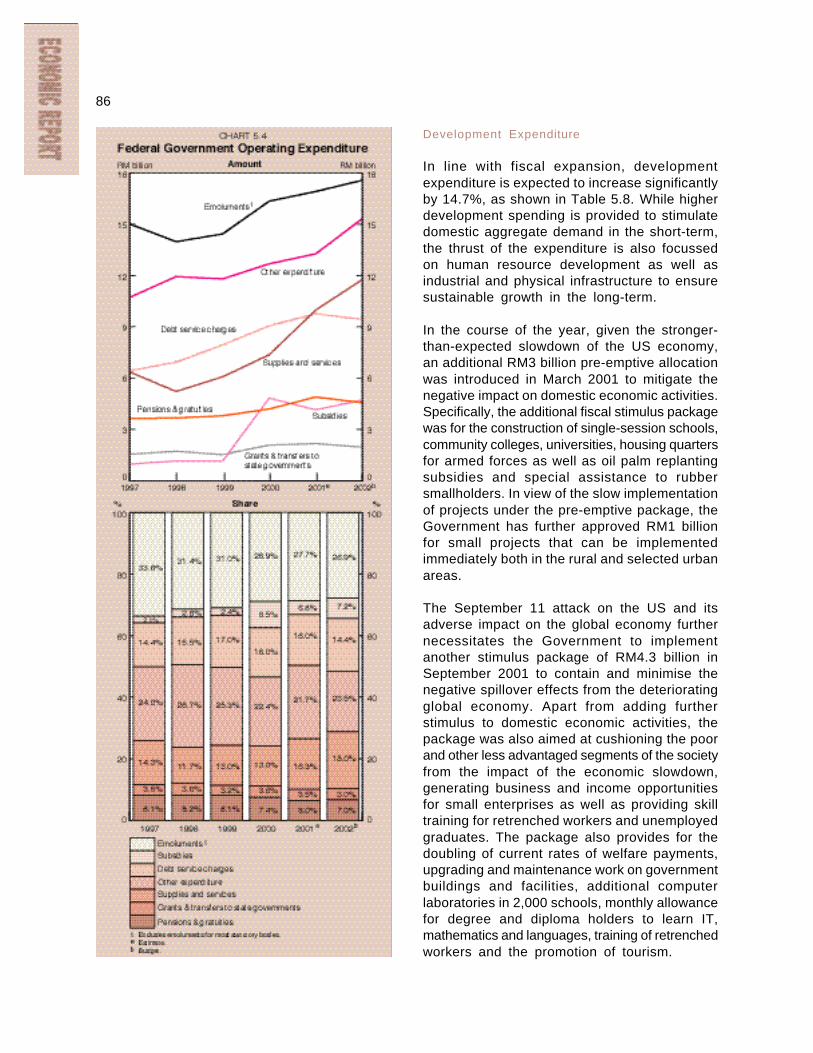

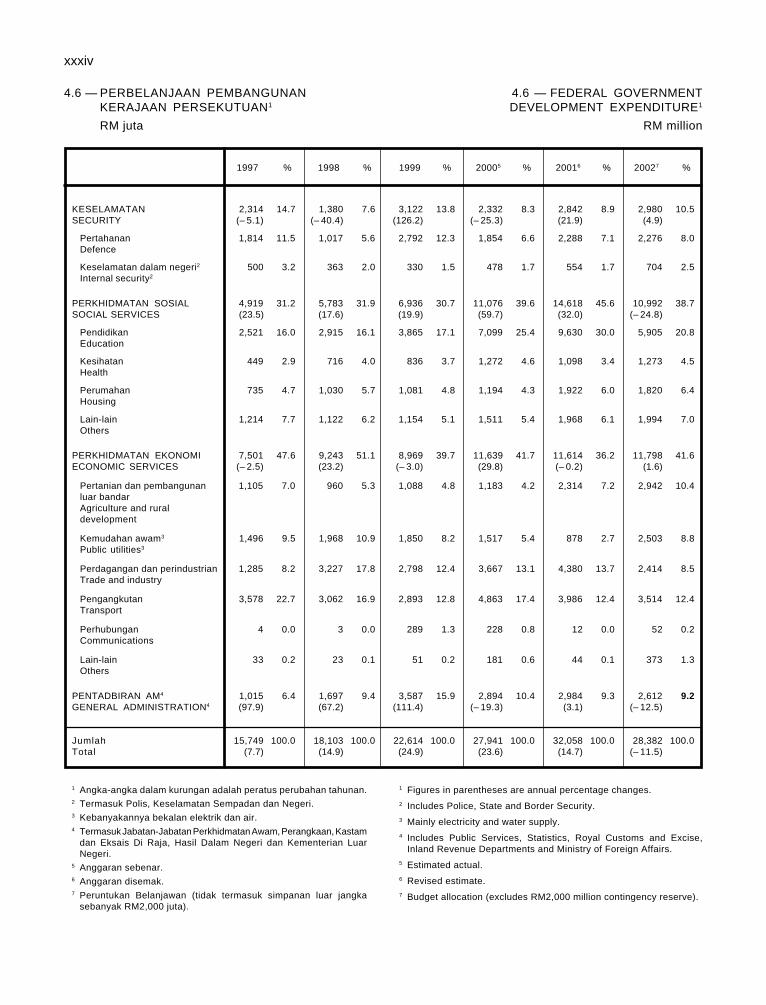

Arising from the additional stimulus packagesimplemented by the Government, developmentexpenditure is expected to increase significantlyby 14.7% to RM32,058 million (2000: 23.6%,RM 27,941 million). The Government announcedthe first pre-emptive package in March of RM3billion for enhancing training capacity throughbuilding universities, community colleges andsingle-session schools as well as topping upfunds for the development of small- and medium-scale enterprises. In September, an additionalpackage of RM4.3 billion was announced, largelyfor rural and selected urban development projectsand training of unemployed graduates andretrenched workers. After taking into accountthe higher expenditure, the overall deficit isexpected to increase to 6.5% of GDP. Given theample liquidity in the financial system, about82.2% of the deficit will be financed from domesticsources, largely Malaysian Government Securities(MGS) and Government Investment Issues (GII),with the balance from external borrowings.

37

National Resource Position

The national resource position remains strongwith the savings-investment gap registering asurplus of RM25,070 million or 7.9% of GNP.The surplus is, however, lower compared withRM31,959 million or 10.2% of GNP in 2000. Thereduced resource surplus is largely the outcomeof the decline in savings by the private sector.Gross fixed capital formation, on the otherhand, is expected to register a moderate increase,largely emanating from the Government’sexpansionary fiscal policy.

Private sector savings is expected to be affectedby lower income resulting from weaker exportearnings as well as greater uncertainties inemployment opportunity. With private consumptioncontinuing to remain large at 47.5% of GNP,private sector savings is expected to moderateto 19.3% of GNP (2000: 24.3%). With strongperformance in Government revenue, publicsector savings is projected to increasesignificantly by 15.6% to RM54,875 million or17.3% of GNP (2000: 15.2% of GNP). Grossnational savings is, therefore, envisaged todecline to RM116,212 million or 36.6% of GNPin 2001 (2000: 39.5% of GNP).

Monetary Developments

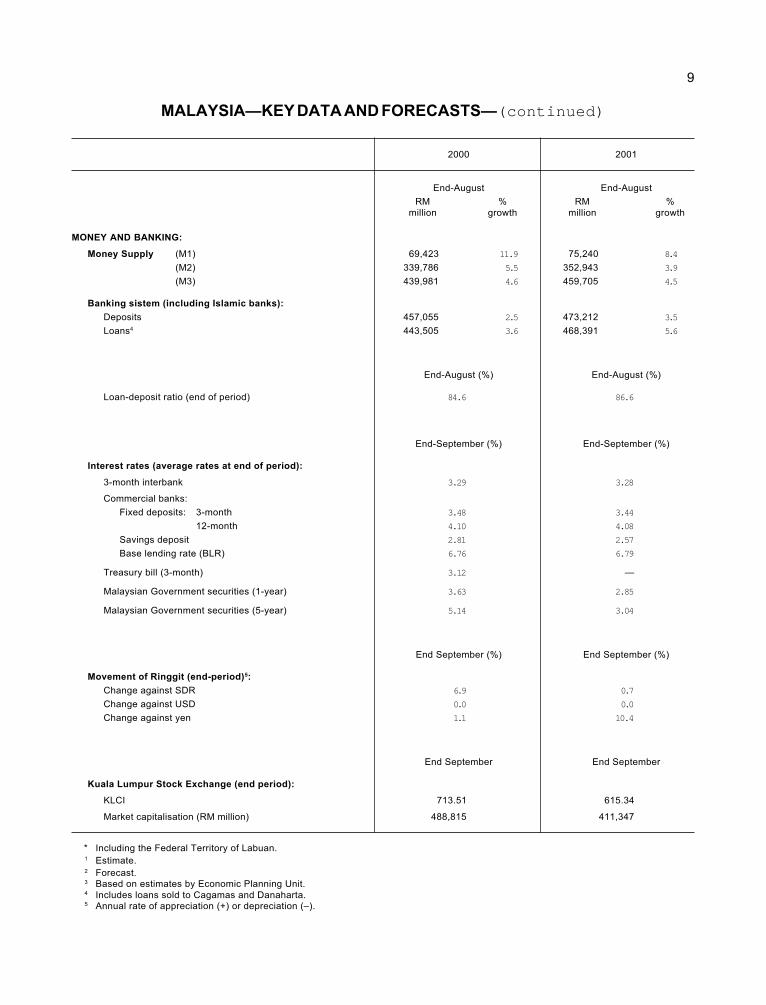

Given the weak external environment, monetarypolicy in 2001 continues to remain accommodativeto support domestic growth and mitigate theadverse impact from the global economicslowdown on the economy. The low inflationaryenvironment as well as global easing of interestrates have enabled the Government to easemonetary policy to support its larger fiscal stimuluswithout putting pressures on prices and wages.Interest rates remain low while ample liquiditycontinues to prevail in the financial system,reflecting the easier monetary stance.

Lending activities continue to improve with totalloans outstanding extended by the banking systemincreasing by 5.6% to RM468,391 million at end-August 2001, driven by higher credit growth inthe business and household sectors. Loandisbursements remained high in the first eightmonths of 2001, increasing by 7.5% against the

corresponding period in 2000. The bulk of loanswas for the purchase of residential property, inparticular low- and medium-cost houses, takingadvantage of the incentives offered by theGovernment, such as stamp duty exemption andwaiver of processing fee. Higher loans werealso channelled to the manufacturing sector aswell as for consumption credit, particularly forthe purchase of passenger cars. Meanwhile,financing through the private debt securitiesmarket (PDS) also increased, largely to financelong-term projects. Subsequently, aggregatefinancing through loans from the banking sectorand PDS rose by 8% as at end-August 2001.

Interest rates remained stable in an environmentof ample liquidity. The average base lendingrates (BLRs) of commercial banks and financecompanies have remained at historical lows sinceAugust 1999 while their average lending ratesremained relatively stable. Nevertheless, in thelight of weakening global economic growth and

38

in response to similar interest rate cuts by othercentral banks, BNM has reduced its 3-monthintervention rate by 50 basis points to 5% on 20September 2001. With the reduction, the BLRceiling of commercial banks and financecompanies will decline to 6.42% and 7.46%,respectively (from 6.83% and 7.98%). Thereduction is aimed at enhancing business andconsumer sentiment to support economicactivities.

Equity Market

In tandem with the developments in major worldand regional bourses, the performance of theKuala Lumpur Stock Exchange (KLSE) duringthe first nine months of 2001 was affected byweaker investor sentiment on concerns of theglobal economic slowdown. KLSE began the yearwith a Chinese New Year rally, with the KualaLumpur Composite Index (KLCI), closing at 727.73points at end-January. It trended downwardsfrom April before recovering to close at 659.40points at end-July, following several optimisticdevelopments in corporate mergers andacquisitions. The attack on the US, however,triggered a fall in share prices worldwide, includingthe KLCI, which declined to 615.34 points as atend-September. Nevertheless, the KLCI continuesto outperform other selected regional bourses.During the period end-2000 to end-September2001, the KLCI declined by 9.5% against thePhilippines Composite Index (-24.6%), the STI(-31.5%) and the Nikkei Index (-29.1%).

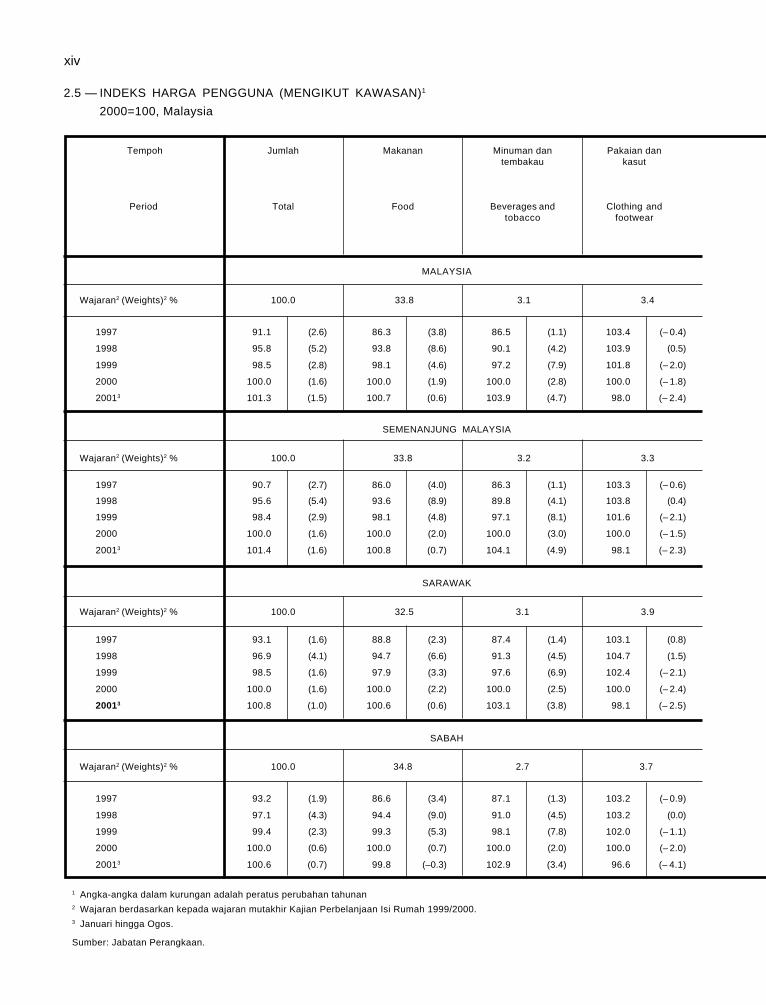

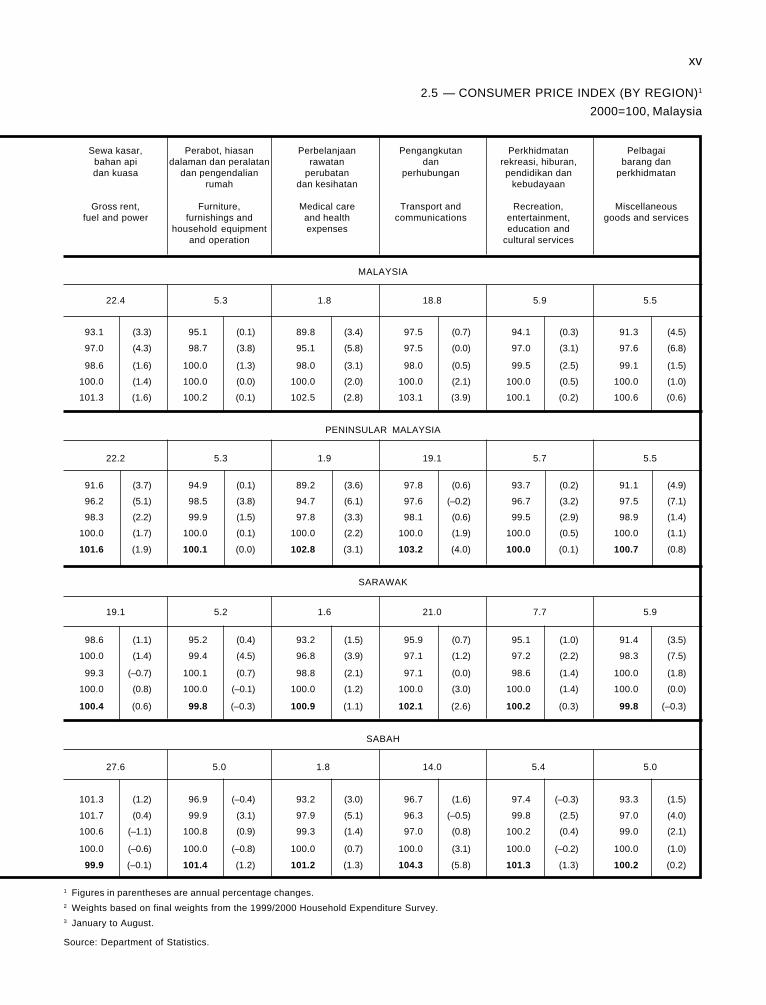

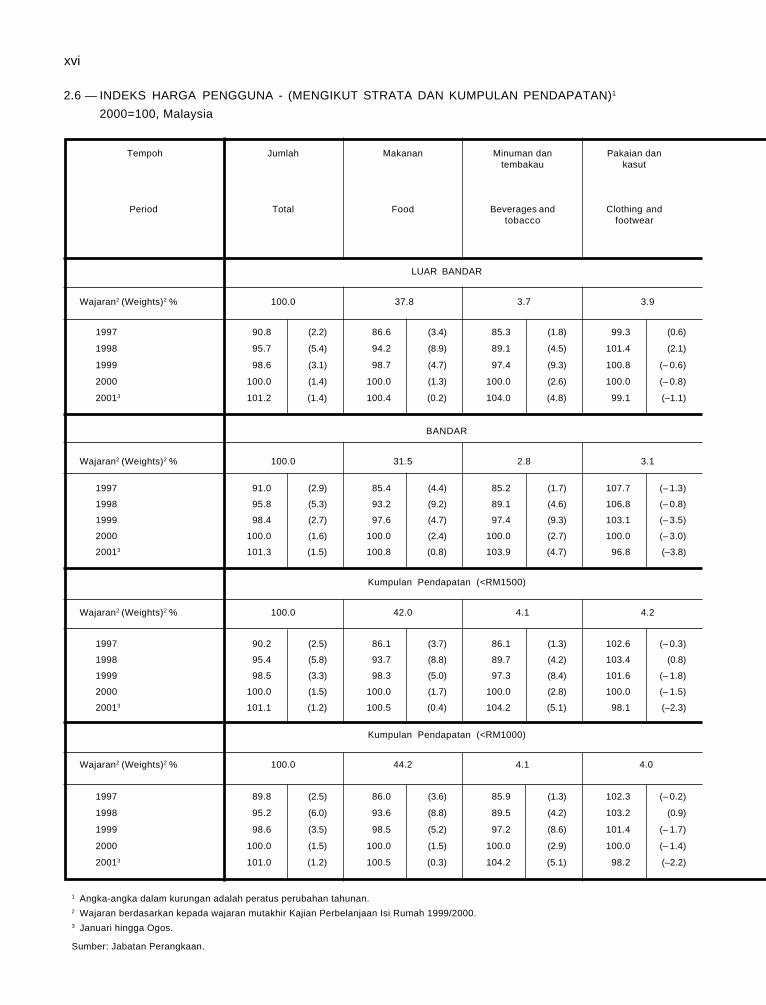

Inflation

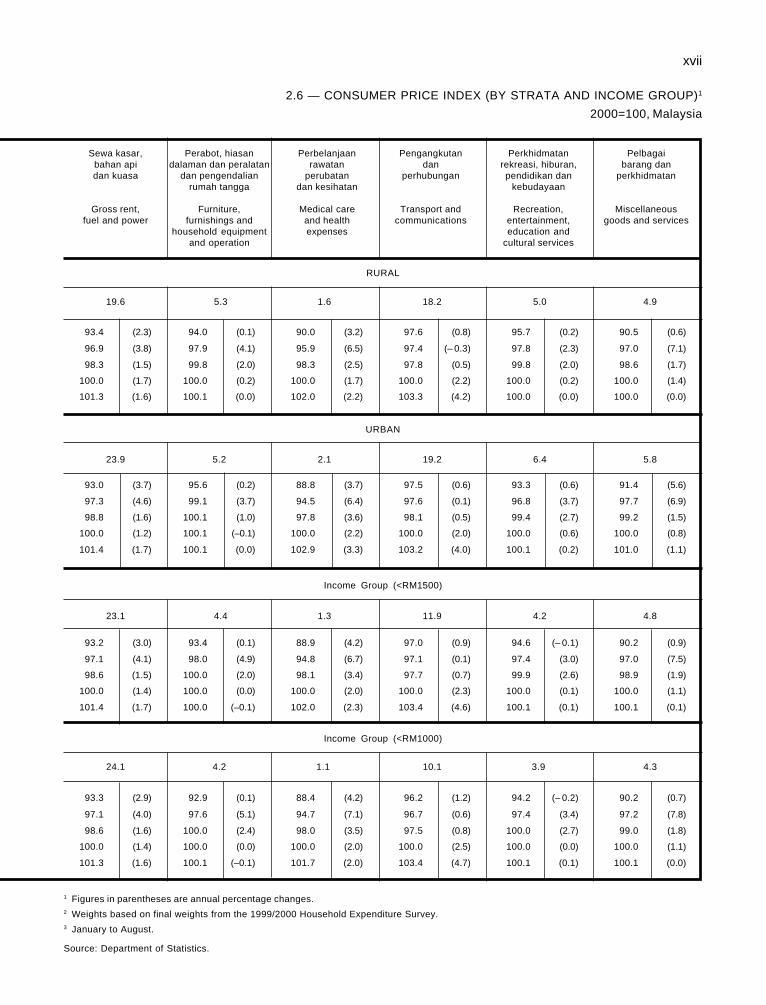

Inflation continues to remain subdued at below2% since 1999. The Consumer Price Index (CPI)registered a small increase of 1.5% during thefirst eight months of 2001, the lowest since 1999,attributable mainly to the relative stability of theexchange rate, low inflation abroad, lower oiland commodity prices as well as excess capacityin several sectors of the domestic economy.The expectation of continued moderation ineconomic activit ies, the less favourableemployment prospects and relatively weakerconsumer confidence will continue to have amoderating effect on domestic prices. As such,inflation is expected to decline to 1.3% in2001.

The moderation in CPI is reflected in most majorsub-indices, largely for food, which accounts formore than a third of the total weightage of theCPI. The food sub-index increased marginallyby 0.6% during the first eight months of 2001while that of gross rent, fuel and power by 1.6%.The marginal increase in food prices is largelyon account of favourable weather conditions aswell as the success of the Government’s measuresto contain price increases of essential goods,particularly food items.

Labour Market

The slower economic activities have somewhataffected labour market conditions. Withemployment creation projected to increase by1.5% and labour force rising by 2.4%, theunemployment rate is expected to increase to3.9% from 3.1% in 2000. Although higher, theunemployment rate is below 4% and as such,the nation is still at its full employment level.The number of workers retrenched stood at20,038, mainly in the electronics sub-sector.Notwithstanding these retrenchments, the nationcontinues to experience shortage of workers,reflecting skill mismatches, job preferences aswell as labour immobility in some regions.

The nation still continues to depend on foreignworkers with the number of registered foreignworkers increasing to 810,695 from 732,588 in2000. Reflecting the easier labour marketconditions, wage pressures were subdued, asreflected by the slower rate of increase in thewages of all categories of workers in themanufacturing sector.

Prospects for 2002

The outlook of the external sector in 2002 remainsuncertain, particularly in the light of the aftermathof the attack on the US. While it is generallyviewed that the US may avoid a recession, therecovery would be delayed with an upturn takingplace gradually in the later part of 2002. Theprospect for a growth in Japan continues to bediscouraging, with the economy not expected towitness a rapid growth. Given the weakerperformance of the US and Japan, world growth

39

has subsequently been revised downwards to2.6%, with the GDP growth for the majorindustrialised countries decelerating to 1.3%.

Taking cognisance of the uncertainties in theexternal environment, growth for the Malaysianeconomy will continue to be spearheaded bydomestic activities. In this regard, the Governmentwill continue to adopt an expansionary fiscalpolicy to further strengthen domestic demand togenerate growth. At the same time, to increasebusiness confidence and commitment, theGovernment will ensure a more conducivebusiness environment for the private sector’sexpansion and initiatives.

Sectoral Performance

The Malaysian economy is forecast to grow by4-5% in 2002, led by stronger performances inthe manufacturing and services sectors. Therecovery in global electronics demand willcontribute towards growth in the manufacturingsector while the pace of expansion in the servicessector will be driven by higher economic activitiesand the Government fiscal stimulus.