Managing Suburban Growth in China’s Metropolitan...

35

1 0. intro slide Managing Suburban Growth in China’s Metropolitan Regions: Trends and Options Edward Leman, President, Chreod Group Inc. Fourth World Bank Urban Research Symposium Washington, D.C. 16 May 2007

Transcript of Managing Suburban Growth in China’s Metropolitan...

1

0. intro slide

Managing Suburban Growth in China’s Metropolitan Regions:

Trends and Options

Edward Leman,President, Chreod Group Inc.

Fourth World Bank Urban Research SymposiumWashington, D.C.

16 May 2007

2

Outline

1.Context1. China’s Metropolitan Regions2. Shanghai as Case Study

2.Research Issue + Methodologies3. Key (interim) Findings

1. Drivers of suburbanization in China2. Emerging Outcomes3. Institutional Causes

4.Consequences5.Further Analytical and Policy Work

3

1. Context – national urbanization trends

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

urba

n po

pula

tion

(thou

sand

s)

China India United States of America BrazilIndonesia Pakistan Nigeria MexicoRussian Federation Japan Philippines BangladeshIran (Islamic Republic of) Germany Turkey United KingdomEgypt Dem. Rep. of the Congo France Colombia

China

India

USA

Brazil

Indonesia

from 1975 - 2010, China's urbanpopulation will have grown by 281 %

168 %

60 %

153 %

388 %

0

10

20

30

40

50

60

70

80

90

100

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

urba

n as

per

cen

t of t

otal

pop

ulat

ion

China India Indonesia Brazil USA

Brazil

USA

Indonesia

China

India

United States

United Kingdom

Russian Federation

Korea, Rep.

Japan

India

Germany France

China

Canada

Burundi

Brazil

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0 10 20 30 40 50 60 70 80 90 100urban pop (% of total)

GD

P pe

r cap

ita, U

S $

PPP,

cur

rent

by 2030?

4

1. Context – Yangtze Delta Megalopolis

5

1. Context – Largest Metropolitan Regions in 2015

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

popu

latio

n (m

illio

ns)

Shanghai Tokyo Mexico City New York-Newark Mumbai Delhi Buenos Aires Sao Paolo

Tokyo: 36.2

Mumbai: 22.6Shanghai: 21.3Delhi: 20.9Mexico: 20.6Sao Paolo: 20New York: 19.7

Buenos Aires:14.6

6

1. Context – Shanghai’s Existing Metropolitan Structure

7

Shanghai MR Population Densities, 2000 (inh/km2)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

80 77 74 71 68 65 62 59 56 53 50 47 44 41 38 35 32 29 26 23 20 17 14 11 8 5 2 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79

kilometers

resi

dent

s/km

2

People's Square

JiadingChuansha

Huinan

Taicang

Kunshan

Outer Ring RoadOuter Ring Road

KUNSHANCORRIDOR

TAICANG CLUSTER

JIADING CORRIDOR

CHUANSHA CLUSTER

SOUTHEASTERN CORRIDOR

8

Guangzhou MR Population Densities, 2000 (inh/km2)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

80 77 74 71 68 65 62 59 56 53 50 47 44 41 38 35 32 29 26 23 20 17 14 11 8 5 2 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79

kilometers

resi

dent

s/km

2

Guangzhou

Inner Ring Road

ShundeCity

Ronggui T.

Xiaolan T.

JiangmenCity

ConghuaCity

Inner Ring Road

9

Tokyo MR Population Densities, 2000 (inh/km2)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

80 77 74 71 68 65 62 59 56 53 50 47 44 41 38 35 32 29 26 23 20 17 14 11 8 5 2 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79

kilometers

resi

dent

s/km

2

Hatogaya Saitama

Hiratsuka

Fujisawa Minami Kohuku

Setagaya

Adachi

Gyoda

Kumagaya

10

London MR Population Densities, 1999 (inh/km2)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

80 77 74 71 68 65 62 59 56 53 50 47 44 41 38 35 32 29 26 23 20 17 14 11 8 5 2 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79

kilometers

resi

dent

s/km

2

ReadingRichmond

Upon Thames

NewhamKensington

Tower

Basildon

Southend-on-Sea

11

New York MR Population Densities, 1999 (inh/km2)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

80 77 74 71 68 65 62 59 56 53 50 47 44 41 38 35 32 29 26 23 20 17 14 11 8 5 2 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79

kilometers

resi

dent

s/km

2

NorwalkStamford

NewBrunswick Elizabeth

Manhattan

12

Toronto MR Population Densities, 2000 (inh/km2)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

80 77 74 71 68 65 62 59 56 53 50 47 44 41 38 35 32 29 26 23 20 17 14 11 8 5 2 1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79

kilometers

resi

dent

s/km

2

Toronto

Hamilton

Burlington Oakville

Mississauga

OshawaPickering

13

2. Research Issue + Methodologies

Patterns of both structured and unstructured suburbanization are constraining the emergence of potential agglomeration benefits across China’s metropolitan regions.

• Not a systematic program of research (yet).• Analytic work on consulting projects in 9 MRs in China

for World Bank: investment projects and AAA• GIS-based spatial analysis of demographic and

economic trends• Satellite image-based, change analysis of builtup land• Fiscal and institutional assessments * Caveat: big danger in making generalizations in China

given huge regional differences

14

2. Research Issue + Methodologies

Maximizing potential agglomerationbenefits requires:

1. (almost) sufficient serviced land and building stock to affordably meet locational, quantitative, and qualitative demands of all households (including the poor and near-poor)

2. transport systems to affordably, safely, and predictably meet household and worker demands for accessibility to services and places of work

3. infrastructure services to affordably, safely, and predictably meet quantitative and qualitative demands of households and firms for power, communication, water, sanitation where needed

4. affordable options to facilitate the proximate location of firms, service providers, and innovation partners

5. least-effort (time and cost), safe, and predictable accessibility to firms’ supply and output markets, and to innovation partners

6. minimum of agglomeration diseconomies

15

3. Findings: Patterns of Suburbanization

16

Intensity of Land Use Change, 1987-2002

17

Emergence of Suburban Corridors and Clusters

18

Growing at Varying Speeds

Chuansha Cluster

Zhoupu Cluster

Duhang Corridor

Baoshan Corridor

Luodian CorridorJiading CorridorAnting Corridor

Qingpu Corridor

Minhang Cluster

Songjiang Corridor

Southeastern Corridor

Nanqiao Corridor

Jinshanwei Cluster

Chongming Corridor

Kunshan Corridor

Taicang Cluster

R2 = 0.5616

0

50

100

150

200

250

300

350

400

0 10 20 30 40 50 60growth in urban land (km2), 1988-2002

per c

ent c

hang

e in

urb

an la

nd u

se, 1

988-

2002

19

3. Findings - Key Drivers of Suburbanization

Key Drivers of Suburbanization:1. Economic restructuring:

• Shift of manufacturing to suburbs• Strong growth in consumer and producer services in

high-density core area• Global trade hub function for central China and

Yangze Basin2. In-migration: 5 million migrants in Shanghai 3. Land Values:

• Price incentives for enterprises• Forced industrial and residential relocations• Housing inflation in core areas• Subsidization of suburban industrial land

4. Physical Accessibility Improvements (for firms, not households)5. Competition for investment among governments: municipal and

district; between districts

20

3. Key Drivers of Suburbanization – economic restructuring

0

10

20

30

40

50

60

70

80

47 45 43 41 39 37 35 33 31 29 27 25 23 21 19 17 15 13 11 9 7 5 3 1 1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73

kilometers

per c

ent

within Outer Ring Road

People's SquareJiading Chuansha Huinan

21

3. Key Drivers of Suburbanization – inmigration

1,300,700 1,302,600

2,570,500

3,685,300

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

2000 2003

9 urban districts suburban districts + county

22

3. Key Drivers - inmigration

23

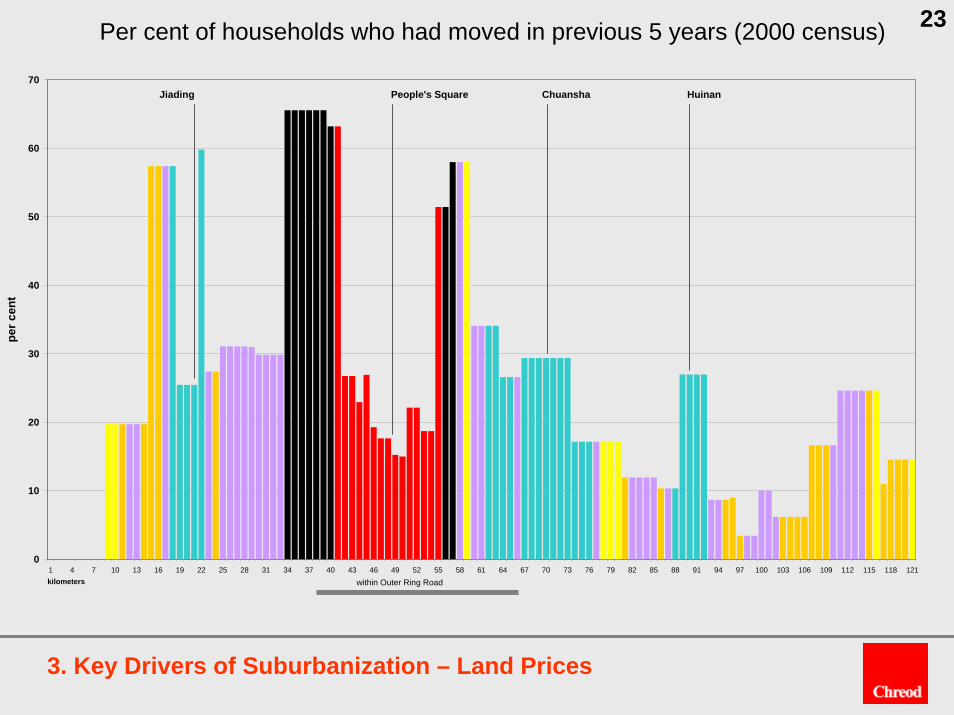

3. Key Drivers of Suburbanization – Land Prices

0

10

20

30

40

50

60

70

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 100 103 106 109 112 115 118 121kilometers

per c

ent

within Outer Ring Road

People's SquareJiading Chuansha Huinan

Per cent of households who had moved in previous 5 years (2000 census)

24

3. Key Drivers of Suburbanization – Land Prices [apartment sale prices]

5000/m2

15000/m2 40000/m2

7500/m2

25

3. Drivers: Physical Accessibility Improvements (for firms)

26

3. Drivers: Physical Accessibility Improvements (for firms)

27

3. Drivers: Physical Accessibility Improvements (for firms)

28

3. Drivers: Physical Accessibility Improvements (for firms)

29

3. Key Drivers – competition for investment among governments

30

4. Policy Consequences – emerging outcomes

Emerging Outcomes:1. Over-consumption of agricultural land2. Shortage of serviced land to required standards in

demand locations3. Growing core-area -- and inner suburban – traffic

congestion, increasing transactions costs 4. Misalignment between metropolitan transport and

residential land use patterns increasing travel costs to households

5. Inaccessibility of suburban residents to metropolitan labour markets

6. Dissipation of pollution sources across the metropolitan region

31

4. Policy Consequences: Institutional Causes

Causes are Institutional:1. Mis-alignment of functional responsibilities, revenue

assignments, and expenditure responsibilities among municipal, district, and town governments

2. Perverse fiscal incentives: declining fiscal capacities of sub-municipal governments forces one-time sales of land use lease rights; no land-based recurring revenues

3. Subsidization and land conversion controls distort real estate markets

4. System of Property Rights mitigates economies of scale and constricts land supply

5. Planning processes cannot keep up with pace of change6. No explicit, codified mandates for metropolitan

management, including suburban areas

32

4. Causes – master plan and actual development

33

5. Analytic and Policy Priorities

Central challenge: how to get governments to better manage land, transport, infrastructure, and environmental protection across metropolitan regions, including through inter-jurisdictional cooperation?• Top-down, command and control not sustainable• Incentives needed:

• Career: performance appraisals…not sustainable

• Equity: ‘do good’…not likely• Effectiveness: ‘do more, better…save farms, save

the environment’…dubious• Efficiencies: ‘do it at less cost’…maybe

• …ECONOMIC RETURNS to governments: job creation, inward investment, fiscal returns from taxes on economic activity

34

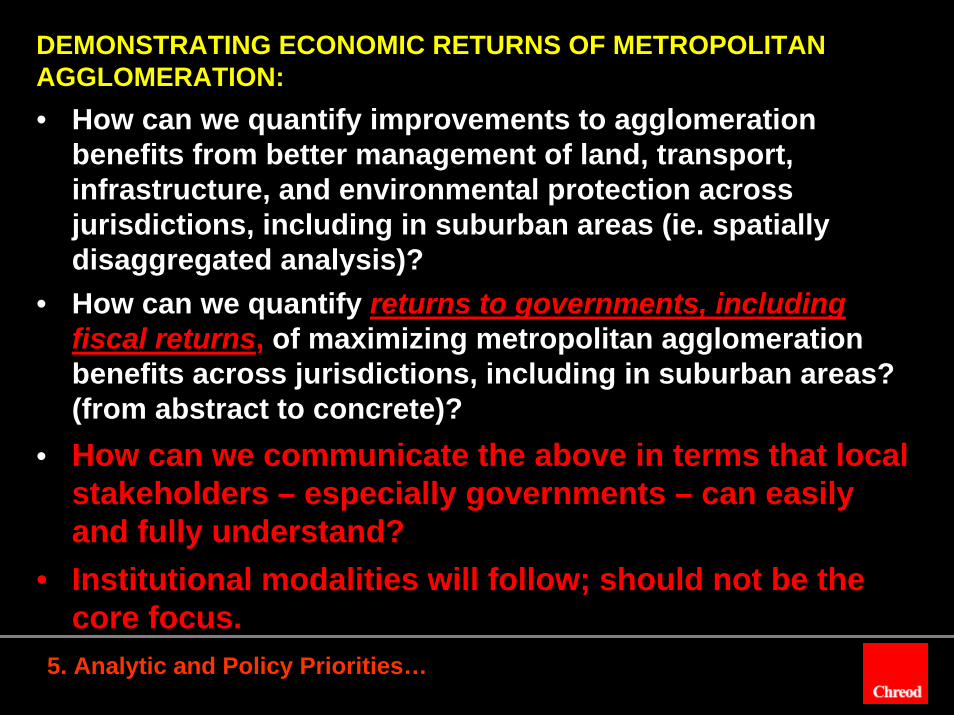

5. Analytic and Policy Priorities…

DEMONSTRATING ECONOMIC RETURNS OF METROPOLITAN AGGLOMERATION:• How can we quantify improvements to agglomeration

benefits from better management of land, transport, infrastructure, and environmental protection across jurisdictions, including in suburban areas (ie. spatially disaggregated analysis)?

• How can we quantify returns to governments, including fiscal returns, of maximizing metropolitan agglomeration benefits across jurisdictions, including in suburban areas? (from abstract to concrete)?

• How can we communicate the above in terms that local stakeholders – especially governments – can easily and fully understand?

• Institutional modalities will follow; should not be the core focus.

35

ChreodSuite 200,111 Sparks Street.Ottawa, Ontario,CANADA K1P 5B5

Shanghai 200030, China

www.Chreod.com

Shanghai Representative Office1301Suite A , Building A

527 Huai Hai Zhong Road

Tel: (86-21) 5306-3477Fax: (86-21) 5306-1358