Managing financial reporting in times of uncertainty

23

Managing Financial Reporting in an Uncertain Environment 6th Controlling, Performance & Reporting Forum Amsterdam, 20 Mar 2015

-

Upload

xavier-sanso -

Category

Business

-

view

70 -

download

0

Transcript of Managing financial reporting in times of uncertainty

Managing Financial Reporting

in an Uncertain Environment

6th Controlling, Performance & Reporting Forum

Amsterdam, 20 Mar 2015

Your speaker today

Partner, finance services

Equity partner & mentor

Visiting professor

I have also had

mainstream jobs

SCIEX (Life Sciences)

FP&A EMEA 2007-2013

UppTalk (mobile messaging)

CFO 2013-2015

Outline

• 10:00 to 10:45 20 Mar 2015

• From internally produced to externally observed: business metrics in a digital environment

• Dealing with the pressure to perform with less resources and limited budgets. Low cost, low maintenance reporting systems

• Cross-functional leadership - expanding the reach and influence of the finance team

• The era of ever-growing expectations in a weak economy: how finance can help deal with human conflict

The Framework

The role of forward-looking assessments in dealing with complexity and uncertainty (Source adapted

from Zurek and Henrichs, 2007)

The Framework (2). McKinsey management under

uncertainty model

Hugh Courtney “20/20 Foresight: Crafting Strategy in an Uncertain World”

• Rare situations that tend to

migrate to other levels over

time

• Qualitative analysis mostly

• Still – don’t throw your hands

in the air, stay systematic

even if it is only to gain

perspective or identify

variables

• Eg: 2008 financial meltdown

in a capital equipment

industry

Paradigm 1

• Organizations increasingly recognize the

ability of analytics to give them a

competitive cutting edge, in a world where

all products and services become

commoditized

BI/Reporting projects,

a historical overviewCloud based

and external

Client server

&

Propietary

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

20

11

2012

2013

2014

2015

“I want to move from business

intelligence to business analytics”

0

10

20

30

40

50

60

70

80

90

100

business intelligence business analytics

Source: Google trends

Side by side

Biz Intelligence Biz Analytics

Runs the business, focuses on operational

efficiency

Changes the business, seeks to

understand the information that can drive

biz change

Understanding the past Anticipating the future (predictive analytics)

Reporting Self-Service analytics

Refers to the data platform as a whole A subset

A noun – umbrella term for the overall

scope of the activity

A verb – the act of discovering insights. Not

so much limited by the infrastructure

“Intelligence without analysis is a waste of

time”

“Analysis without intelligence can’t be

done”

Business Intelligence vs. Business Analytics: What’s The Difference?. BI Software

insight

“And the winner is…”

( Where are

salesforce.com

and Wave? )

The question remains…

• How do we become a data-driven

organization?

• (We will respond later on in the

presentation)

Paradigm 2

• From internally produced, internally

defined business metrics…

• … To industry standardized, externally

observed ones…

• … (bonus track – often public!)

New company, old metrics

• In its IPO filing, Twitter claimed that “through the eyes of management” the company had made a profit of $21MM in the semester

• Even though the accounting loss had been $69MM

• The difference is an unorthodox “adjusted EBITDA” which excluded non-cash compensation and other items

• Another example would be Groupon

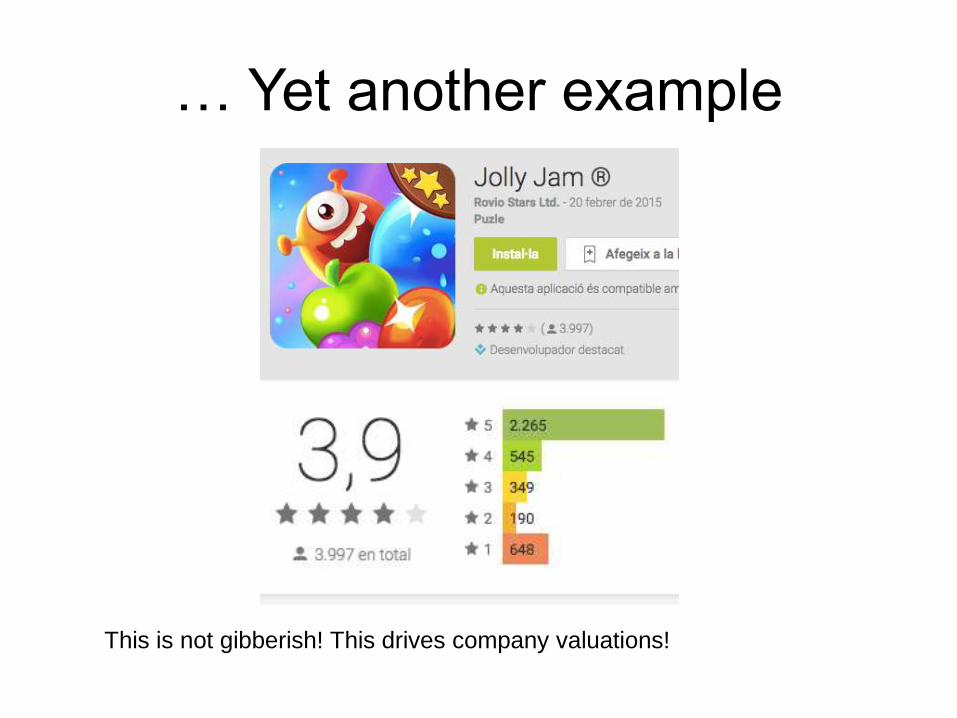

New company, new metrics

• In mobile apps, Localytics sets the standard about usage… both how you define usage and how many users you have

• There is no tolerance whatsoever for deviations from this standard, and companies have little capacity to influence the metric or to define an internal one

• And the info is semi-public

… Yet another example

This is not gibberish! This drives company valuations!

Paradigm 3

• “Process is everything”

• Choose the right metrics

• Communicate and disseminate

• Follow them consistently

• Do variance analysis

• Reiterate into model

• Finance is the key stakeholder that should own the operational cadence

“We are what we repeatedly do. Excellence, then, is not an act,

but a habit” (Aristotle)

Common sense rigorously applied

W1 W2 W3 W4

L1 Metric: Units

ordered new

product “XY78”

EMEA

Owner:

Roger

Penrose

AC 70 80 15

FC 71 76 56

LY 55 63 46

L2 Metric: Units

ordered new

product “XY78”

Italy

Owner:

Ruggiero la

Rosa

AC 11 16 1

FC 13 15 15

LY 12 11 8

• Consistent strategy deployment over different organization levels

• Visual management tools

• Robust process

• Focus on problem solving: Pareto analysis, etc. (This is a science, not an art!)

Corollary

• Finance is uniquely positioned to partner with

the general management

• And influence other parts of the organization

through cross functional leadership

• Avoiding human conflict by staying factual

• And being a true business driver

From reporting to

self service analytics

(also as a company

philosophy)

Become data centric,

improve the

organization and

make it cohesive

through process

The democratization

of information: your

metrics are not your

metrics, and you

don’t own them

anymore

( thank you! )