Management Report 2013 - Unicasa Móveis · Alexandre Grendene Bartelle Chairman Juvenil Antônio...

67

1 Management Report 2013

Transcript of Management Report 2013 - Unicasa Móveis · Alexandre Grendene Bartelle Chairman Juvenil Antônio...

1

Management Report

2013

BOARD OF DIRECTORS

Alexandre Grendene Bartelle Chairman

Juvenil Antônio Zietolie

Vice Chairman

Frank Zietolie Director

Hugo Antônio Jordão Bethlem

Independent Director

Renato Ochman Director

BOARD

Frank Zietolie President

Kelly Zietolie

Vice President

Paulo Eduardo Junqueira de Arantes Filho Financial and Investor Relations Officer

Thiago Proença Baisch

Commercial Officer

Ivanir Moro Accoutant

CRC/RS-053351/O-7

To The Shareholders,

In compliance with applicable laws and Bylaws of the company, the Management of Unicasa

Indústria de Móveis S.A. hereby presentes the Management Report and the Financial Statements

prepared according to the International Financial Reporting Standards (IFRS) issued by International

Accounting Standards Board (IASB), the generally accepted accounting principles in Brazil and the rules

issued by the Securities and Exchange Comission of Brazil (CVM). The Company adopted all the standars,

revisions of standards and interpretations issued by IASB and which are effective for the financial

statements ended on December 31, 2013.

The Financial Statements of Unicasa Indústria de Móveis S.A. as of December 31, 2013, were

prepared in accordance with the generally accepted accounting principles in Brazil and the rules issued

by the Securities and Exchange Comissions of Brazil (CVM), while also complying with the accounting

guidelines from corporate law (Law 6,404/76), which include the new provisions introduced, amended

and canceled by Law 11,638 of December 28, 2007 and Law 11,941 of May 27, 2009. These practices

differ from the IFRS applicable to separate financial statements only with regard to the valuation of

investments in subsidiaries, which are valued using the equity income method, whereas they would be

valued at cost or fair value according to IFRS.

MESSAGE FROM THE MANAGEMENT

In 2013, we began operations at five own stores, of which four were located in the city of São

Paulo and one in the city of Manaus. The opening of the sixth and final store planed in our own store

project should occur in the second half of 2014, in the city of São Paulo. Launched in 2012, the project

will help us acquire experience in the operation of stores to allow us to identify good practices and

efficiency gains to implement throughout our retail network. The direct relationship with final

consumers allows us to amass a great body of knowledge on the sales process, from the development of

project for environments to the final assembly of products.

This year, we launched operations for our new brand Casa Brasileira, which is marketed through

franchises and the multibrand stores. Inspired by the concept of Brazilianness and the country’s different

regions, the brand’s positioning is the product of a study on the Brazilian way of being and the country's

culture. The brand explores the need to create furniture that is especially designed for smaller

environments and faithful to the space currently available.

Over the course of the year, we made progress on repositioning the brands Dell Anno and Favorita,

which involved converting small stores with low sales and little impact on the Company’s results into

multibrand stores or shutting them down. Our objective is to make our chain more homogenous and

with our brands present in the markets best suited to their proposition.

The fourth quarter of 2013 brought signs of recovery in the revenue generated by the brands

Dell Anno and Favorita, signaling the end of the cycle of adverse revenue impacts related to the

comprehensive store repositioning carried out in 2012.

In 2013, we enjoyed strong cash generation, despite the lower-than-expected results. In the

year, we paid dividends and interest on equity, reduced our net debt, invested in CAPEX and settled our

tax liabilities by adhering to the REFIS tax amnesty program. However, despite this large volume of

expenditures, we ended the year with a cash position that, based on our projections, will enable us to

meet our investment obligations and working capital needs for 2014.

This year, we will consolidate part of our strategies, but we are cautious to project their effects

on the Company’s results, given the atypical year in 2014, with the World Cup and presidential elections,

which increases uncertainty on the country’s economic and political scenarios.

We thank you for your trust and support in this year marked by investments in our own store

operations and by the consolidation of our strategies. To our shareholders, dealers and their teams,

clients, suppliers and our employees, who are all steadfastly dedicated and committed to the Company’s

success, we say thank you.

SALES AND DISTRIBUTION CHANNELS

Continuing the process to reposition the brands Dell Anno and Favorita, as announced in 2Q13, which

basically consists of replacing stores located in markets with low acceptance of the brand proposition

and low revenue and results, we reduced the reseller base by 58 stores in 4Q13 and converted 27 of

these stores into Multibrand Casa Brasileira stores.

Our multibrand distribution channel reached 2,852 stores in 4Q13. We ended 4Q13 with 650 New and

Casa Brasileira multibrand stores and 2,202 points of sales in the retail chain under the Telasul Modular

brand.

Unicasa’s network of exclusive dealers reached 832 stores in the period, of which 381 were Dell Anno

and Favorita stores and 451 were New and Casa Brasileira franchise stores.

The evolution in our distribution channels is shown below:

Period 2012 1Q13 2Q13 3Q13 4Q13 ∆

Exclusive, Franchise and Own Stores 922 929 923 906 832 (74)

Dell Anno and Favorita 463 463 456 439 381 (58)

New and Casa Brasileira Franchise 459 466 467 467 451 (16)

Multibrand 2,131 2,161 2,761 2,820 2,852 32

New and Casa Brasileira Multibrand 576 576 594 618 650 32

Telasul Modular 1,555 1,585 2,167 2,202 2,202 -

SALES PERFORMANCE

Gross Revenue ex-IPI

Revenue information by brand is presented based on gross revenue excluding the IPI federal value-

added tax (Gross Revenue ex-IPI) from the comparison base, since this method improves the

comparability of sales information by brand. The rate of IPI tax was reduced from 5% to 0% from March

26, 2012 to January 31, 2013, after which it was raised to 2.5% as from February 1, to 3% as from July 1,

to 3.5% as from October 1, and to 4% as from January 1, 2014, with the return of a 5% rate expected on

July 1, 2014. Information on gross revenue, gross revenue ex-IPI and modules sold is available in

Attachment IV to this report.

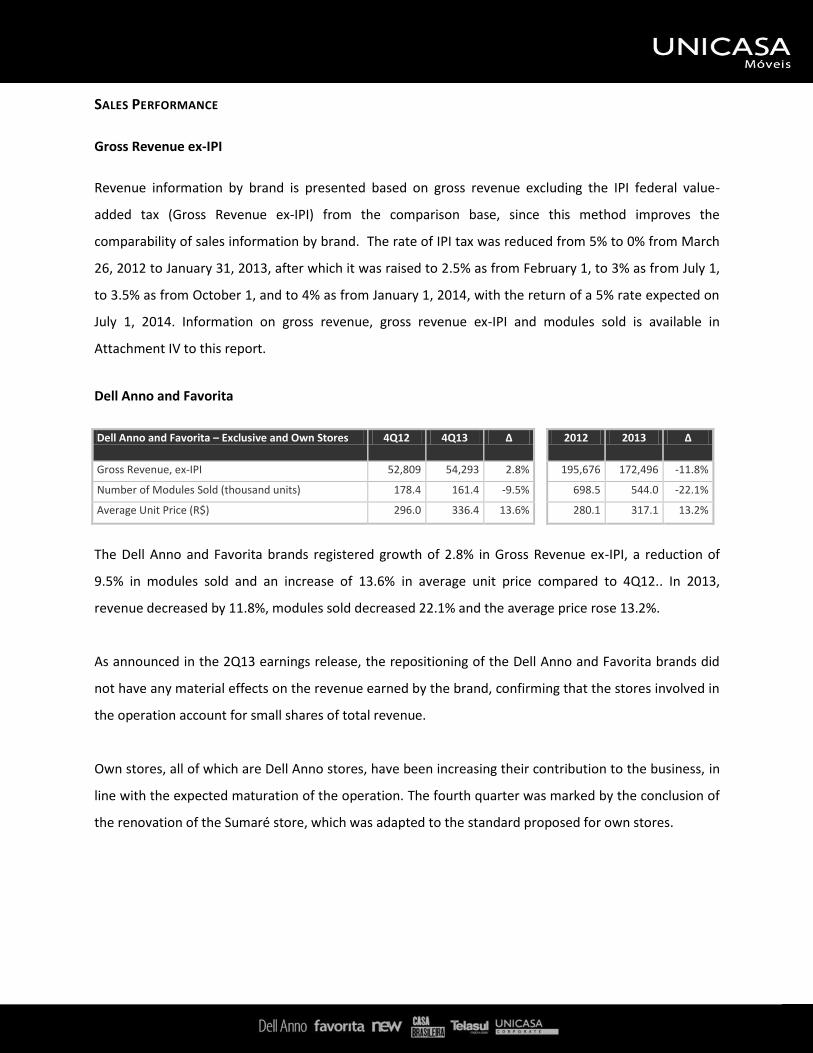

Dell Anno and Favorita

Dell Anno and Favorita – Exclusive and Own Stores 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 52,809 54,293 2.8% 195,676 172,496 -11.8%

Number of Modules Sold (thousand units) 178.4 161.4 -9.5% 698.5 544.0 -22.1%

Average Unit Price (R$) 296.0 336.4 13.6% 280.1 317.1 13.2%

The Dell Anno and Favorita brands registered growth of 2.8% in Gross Revenue ex-IPI, a reduction of

9.5% in modules sold and an increase of 13.6% in average unit price compared to 4Q12.. In 2013,

revenue decreased by 11.8%, modules sold decreased 22.1% and the average price rose 13.2%.

As announced in the 2Q13 earnings release, the repositioning of the Dell Anno and Favorita brands did

not have any material effects on the revenue earned by the brand, confirming that the stores involved in

the operation account for small shares of total revenue.

Own stores, all of which are Dell Anno stores, have been increasing their contribution to the business, in

line with the expected maturation of the operation. The fourth quarter was marked by the conclusion of

the renovation of the Sumaré store, which was adapted to the standard proposed for own stores.

New and Casa Brasileira

New Exclusive Dealers and Casa Brasileira Franchise Stores

4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 25,430 25,188 -1.0% 91,756 92,465 0.8%

Number of Modules Sold (thousand units) 138.0 125.2 -9.3% 488.0 474.1 -2.8%

Average Unit Price (R$) 184.3 201.2 9.2% 188.0 195.0 3.7%

Multibrands 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 10,271 9,750 -5.1% 38,159 37,093 -2.8%

Number of Modules Sold (thousand units) 66.9 61.8 -7.6% 241.7 232.8 -3.7%

Average Unit Price (R$) 153.5 157.8 2.8% 157.9 159.3 0.9%

Note: Revenue for 2012 refers to sales under the brand Telasul in the Exclusive and Multibrand channels, plus revenue from the New brand in

the Multibrand channel.

Gross revenue ex-IPI from the Exclusive channels of the New brand and the franchise stores of the Casa

Brasileira brand decreased by 1.0% compared to 4Q12, with modules sold decreasing 9.3% and the

average unit price increasing 9.2%. In the year, revenue and average price of modules increased 0.8%

and 3.7%, respectively, while sales volume decreased 2.8%.

The Multibrand channel (New, Casa Brasileira and other) recorded a decrease in Gross Revenue ex-IPI of

5.1% in 4Q13 and 2.8% in the year, while the number of modules sold fell 7.6% in 4Q13 and 3.7% in the

year and average unit price increased 2.8% in 4Q13 and 0.9% in the year.

Telasul Modular

The Telasul brand was marketed through the Exclusive, Multibrand and Department Store channels and

was reported on a consolidated basis. With the creation of the Casa Brasileira brand in March 2013, the

former Telasul Exclusive and Multibrand channels of Telasul were transformed into Casa Brasileira

Multibrand, which began to be reported together with New Multibrand. The Department Store channel

continues to be served by the Telasul Modulados brand, which offers modular furniture to retail chains.

Telasul Modular 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 5,606 3,870 -31.0% 18,568 13,945 -24.9%

Number of Modules Sold (thousand units) 46.0 36.1 -21.5% 155.3 120.0 -22.7%

Average Unit Price (R$) 121.9 107.2 -12.1% 119.6 116.2 -2.8%

The performance of the Telasul Modulados brand was marked by reductions of 31.0% in Gross Revenue

ex-IPI, 21.5% in sales volume and 12.1% in average price.

Unicasa Corporate

This segment registered growth in Gross Revenue ex-IPI of 90.7%, with sales volume growing 169.0% and

average unit price decreasing 29.1%.

Unicasa Corporate 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 1,189 2,267 90.7% 4,868 5,793 19.0%

Number of Modules Sold (thousand units) 2.9 7.8 169.0% 19.7 19.7 0.0%

Average Unit Price (R$) 410.0 290.6 -29.1% 247.1 294.1 19.0%

Other Revenues

Other revenues are derived from sales to employees, suppliers, freight operators and other.

Other Revenues 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 1,435 1,451 1.1% 6,112 4,973 -18.6%

Number of Modules Sold (thousand units) 11.8 14.2 20.3% 27.8 56.9 104.7%

Average Unit Price (R$) 121.6 102.2 -16.0% 219.9 87.4 -60.3%

Export Market

Exports registered increases of 17.1% in revenue and 43.8% in sales volume, and a decrease of 18.5% in

the average price.

Export Market 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 1,753 2,052 17.1% 8,063 8,970 11.2%

Number of Modules Sold (thousand units) 11.2 16.1 43.8% 66.1 124.6 88.5%

Average Unit Price (R$) 156.5 127.5 -18.5% 122.0 72.0 -41.0%

Consolidated Indicators Unicasa

Unicasa Indústria de Móveis 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 98,493 98,871 0.4% 363,202 335,735 -7.6%

Number of Modules Sold (thousand units) 455.2 422.6 -7.2% 1,697.0 1,572.1 -7.4%

Average Unit Price (R$) 216.4 234.0 8.1% 214.0 213.6 -0.2%

Domestic Market 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 96,740 96,819 0.1% 355,139 326,765 -8.0%

Number of Modules Sold (thousand units) 444.0 406.5 -8.4% 1,630.9 1,447.5 -11.2%

Average Unit Price (R$) 217.9 238.2 9.3% 217.8 225.7 3.6%

Export Market 4Q12 4Q13 Δ 2012 2013 Δ

Gross Revenue, ex-IPI 1,753 2,052 17.1% 8,063 8,970 11.2%

Number of Modules Sold (thousand units) 11.2 16.1 43.8% 66.1 124.6 88.5%

Average Unit Price (R$) 156.5 127.5 -18.5% 122.0 72.0 -41.0%

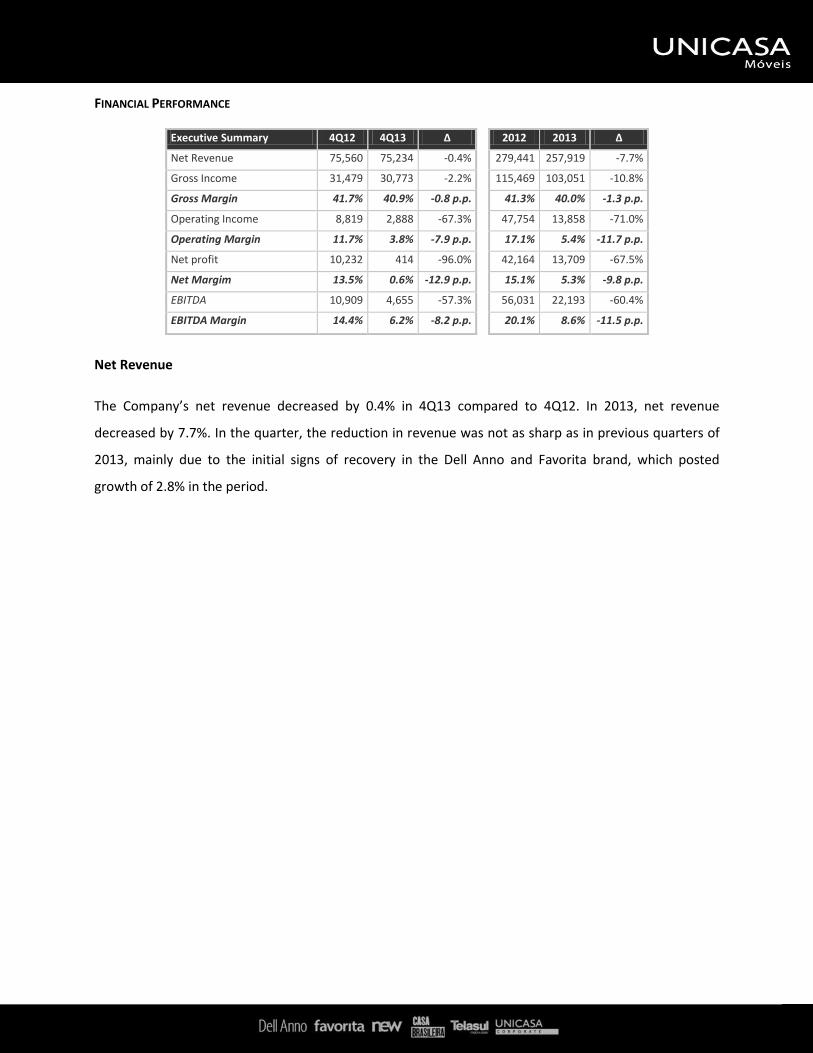

FINANCIAL PERFORMANCE

Executive Summary 4Q12 4Q13 Δ 2012 2013 Δ

Net Revenue 75,560 75,234 -0.4% 279,441 257,919 -7.7%

Gross Income 31,479 30,773 -2.2% 115,469 103,051 -10.8%

Gross Margin 41.7% 40.9% -0.8 p.p. 41.3% 40.0% -1.3 p.p.

Operating Income 8,819 2,888 -67.3% 47,754 13,858 -71.0%

Operating Margin 11.7% 3.8% -7.9 p.p. 17.1% 5.4% -11.7 p.p.

Net profit 10,232 414 -96.0% 42,164 13,709 -67.5%

Net Margim 13.5% 0.6% -12.9 p.p. 15.1% 5.3% -9.8 p.p.

EBITDA 10,909 4,655 -57.3% 56,031 22,193 -60.4%

EBITDA Margin 14.4% 6.2% -8.2 p.p. 20.1% 8.6% -11.5 p.p.

Net Revenue

The Company’s net revenue decreased by 0.4% in 4Q13 compared to 4Q12. In 2013, net revenue

decreased by 7.7%. In the quarter, the reduction in revenue was not as sharp as in previous quarters of

2013, mainly due to the initial signs of recovery in the Dell Anno and Favorita brand, which posted

growth of 2.8% in the period.

Cost of Goods Sold (COGS)

Cost per module sold increased 8.6%, from R$96.84 in 4Q12 to R$105.21 in 4Q13, mainly due to the

higher personnel expenses in the period. The nominal increase in COGS between 4Q12 and 4Q13 was

R$0.4 million, or 0.9%. Some of the main factors contributing to this result were:

i) the R$1.0 million increase in personnel expenses driven mainly by the growth in headcount a) in

the flexible production line, which was in the ramp-up phase in 4Q12; and b) in the painting line, and

also by the wage increases under the collective bargaining agreement;

ii) the R$0.9 million reduction in depreciation due to the revision in the useful life of property, plant

and equipment, which was partially offset by the depreciation of assets acquired for painting and flexible

production;

iii) the improvements obtained in our inventory control enabled us to reverse in 4Q12 the amount

provisioned for stock obsolescence. As a result, the reversal made in 2012 did not recur in 2013,

resulting in an increase of R$0.3 million in the provision for this expense in the comparison period.

The following chart presents the reconciliation of Cost of Goods Sold in 4Q12 and 4Q13(¹):

(1) In R$ million.

In 2013, cost of goods sold corresponded to 60.0% of net revenue from sales, compared to 58.7% in

2012. The increase was mainly due to the higher unit cost per module sold, which increased from

R$96.63 in 2012 to R$98.51 in 2013. This increase is explained by:

(i) primarily by personnel expenses. In 2012, the Flexible Production line was in the pre-operational

stage, while in 2013 the lacquer painting line started operations, therefore the impacts from these lines

combined represented an additional expense of R$3.48 million in 2013. Meanwhile, the wage increases

under the collective bargaining agreement resulted in a R$1.03 million increase in personnel expenses;

44.1 44.5

1.0 0.9 0.3

COGS4Q12 Personnel Depreciation Provision

COGS4Q13

(ii) the lower Net Revenue and change in the sales mix, which supported a reduction in costs of around

R$12.57 million;

(iii) the R$0.80 million reduction in depreciation expenses due to the new estimates for useful life of

assets adopted as of September 2013;

(iv) the R$0.24 million increase in other general manufacturing expenses.

The following chart presents a reconciliation of Cost of Goods Sold in 2012 and 2013(¹):

(1) In R$ million.

Gross Profit and Gross Margin

Gross Profit in the quarter amounted to R$30.8 million, with Gross Margin of 40.9%. Gross margin

contracted by 0.8 p.p. from 4Q12, driven mainly by higher personnel expenses, which were partially

offset by the improvement in the sales mix in the period. Compared to 3Q13, gross margin expanded by

1.9%, mainly due to the better sales mix and the higher revenue in the period, which helped dilute fixed

costs.

Selling, General and Administrative Expenses (SG&A)

Selling, general and administrative expenses amounted to R$29.1 million in 4Q13, increasing 21.9%

compared to 4Q12 and corresponding to 38.7% of Net Revenue.

Selling General and Administrative Expenses 4Q12 4Q13 Δ 2012 2013 Δ

Total (23,875) (29,113) 21.9% (77,059) (93,543) 21.4%

Selling Expenses (18,192) (19,501) 7.2% (57,422) (69,148) 20.4%

% of Net Revenue 24.1% 25.9% 1.8 p.p. 20.5% 26.8% 6.3 p.p.

Administrative Expenses (5,683) (9,612) 69.14% (19,637) (24,395) 24.2%

% of Net Revenue 7.5% 12.8% 5.3 p.p. 7.0% 9.5% 2.5 p.p.

SG&A % of Net Revenue 31.6% 38.7% 7.1 p.p. 27.5% 36.3% 8.8 p.p.

163.4 154.9

12.6 0.8 4.5 0.3

COGS2012 Volume Depreciation Personnel Others

COGS2013

Expenses with Own Stores and the Service Center increased R$4.4 million in the quarter, led mainly by

personnel and rental expenses. In 2013, these expenses increased by R$13.0 million. Note that in 2012,

these expenses were less relevant, since own stores were starting their pre-operational cycle.

Expenses with clients increased by R$0.5 million from 4Q12 and by R$3.4 million from 2012. These

expenses are related to the expenses with services rendered to final consumers at the closed stores.

The amortization of commercial points, which began in 3Q13, increased operating expenses by R$0.6

million in 4Q13 and by R$0.8 million in 2013.

The participation in the Refis tax amnesty program, which was announced in the Material Fact notice

dated December 16, 2013, affected administrative expenses, net of provisions by R$2.2 million.

Expenses with provisions decreased by R$2.3 million compared to 4Q12, mainly due to the lower

allowance for doubtful accounts recorded in 4Q13. In 2013, the R$3.78 million decrease was mainly due

to the accrual of nonrecurring provisions in 2Q12.

Marketing and other expenses net of the abovementioned effects decreased by R$0.2 million compared

to 4Q12, mainly due to the decrease in marketing expenses in the period, which, in turn, is mainly

explained by the annualized deferment in 2013 of the recovery in marketing expenses In 2013, other

expenses reached R$0.8 million, mainly due to the consulting services contracted in the period.

The following chart presents the reconciliation of Selling, General and Administrative Expenses in 4Q12

and 4Q13(1):

(1) In R$ million.

23.9

29.1

4.4 0.5 0.6 2.2

2.3 0.2

SG&A4Q13

Own stores andshared service

centerExpenses with

clientsDepreciation and

amortization Refis ProvisionsMarketing and

othersSG&A4Q13

The following chart presents the reconciliation of Selling, General and Administrative Expenses in 2012

and 2013(1):

(1) In R$ million.

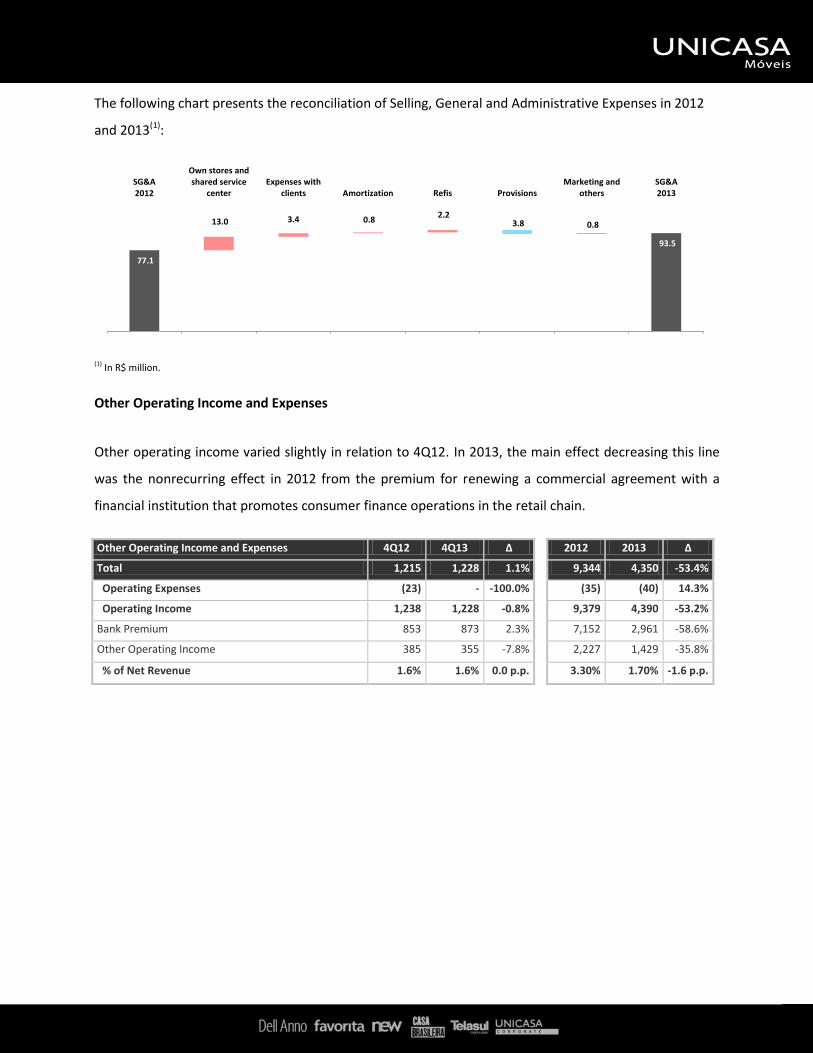

Other Operating Income and Expenses

Other operating income varied slightly in relation to 4Q12. In 2013, the main effect decreasing this line

was the nonrecurring effect in 2012 from the premium for renewing a commercial agreement with a

financial institution that promotes consumer finance operations in the retail chain.

Other Operating Income and Expenses 4Q12 4Q13 Δ 2012 2013 Δ

Total 1,215 1,228 1.1% 9,344 4,350 -53.4%

Operating Expenses (23) - -100.0% (35) (40) 14.3%

Operating Income 1,238 1,228 -0.8% 9,379 4,390 -53.2%

Bank Premium 853 873 2.3% 7,152 2,961 -58.6%

Other Operating Income 385 355 -7.8% 2,227 1,429 -35.8%

% of Net Revenue 1.6% 1.6% 0.0 p.p. 3.30% 1.70% -1.6 p.p.

77.1

93.5

13.0 3.4 0.8 2.2

3.8 0.8

SG&A2012

Own stores andshared service

centerExpenses with

clients Amortization Refis ProvisionsMarketing and

othersSG&A2013

Net Financial Result

The net financial result decreased 247.0% compared to 4Q12. The net financial result is presented

below:

Financial Result 4Q12 4Q13 Δ 2012 2013 Δ

Net Financial Result 1,846 (2,714) -247.0% 9,192 1,553 -83.1%

Financial Expenses (909) (5,365) 490.2% (3,075) (8,505) 176.6%

IOF charge and bank fees (119) (181) 52.1% (622) (686) 10.3%

Loans and financing expenses (128) (15) -88.3% (547) (259) -52.7%

Exchange variation expenses (104) (34) -67.3% (413) (414) 0.2%

Present value adjustment - AVP - (206) n/a (342) (365) 6.7%

Other financial expenses (558) (4,929) 783.3% (1,151) (6,781) 489%

Financial Income 2,755 2,651 -3.8% 12,267 10,058 -18.0%

Interest income 819 594 -27.5% 3,346 2,399 -28.3%

Discounts 67 47 -29.9% 516 156 -69.8%

Yield from short-term investments 465 567 21.9% 2,487 1,858 -25.3%

Exchange variation income 103 281 172.8% 314 645 105.4%

Present value adjustment - AVP 1,139 1,023 -10.2% 5,033 4,533 -9.9%

Other financial income 162 139 -14.2% 571 467 -18.2%

The participation in the Refis tax amnesty program, as announced through the Material Fact notice dated

December 16, 2013, affected the item “other financial expenses” in the amount of R$2.2 million related

to the interest paid in the process. The same item recorded financial discounts of R$2.8 million in 4Q13

arising from negotiations with dealers that resulted in the recovery of receivables and involved the

incorporation of assets. Note that both of these effects are nonrecurring.

The main factors impacting the result in the year were: (i) the R$3.5 million increase in discounts granted

to clients; (ii) the amount of R$2.2 million related to the Refis tax amnesty program, as commented

above; (iii) the lower interest income due to the lower balance related to contracts, R$0.9 million; (iv)

the lower yield from financial investments, since in 2012 the Company held cash arising from the sale of

shares up to the date of the effective payment of dividends to partners, R$0.6 million.

Net Income Net income declined by 96.0% from 4Q12, mainly due to the nonrecurring effects from Refis and the

discounts granted, as well as the higher expenses with own stores and with services rendered to final

consumers. In the year, the 67.5% decrease is explained by, in addition to the same factors that

impacted net income in the quarter augmented in the year, the accounting of the nonrecurring other

operating income recorded in 2012.

EBITDA and EBITDA Margin

EBITDA decreased by 57.3%, from R$10.9 million in 4Q12 to R$4.7 million in 4Q13. In the year, EBITDA

decreased by 60.4%, from R$56.0 million in 2012 to R$22.2 million in 2013. EBITDA margin was 6.2% in

the quarter and 8.6% in the year. The decline is explained by the same reasons that affected net income.

EBITDA 4Q12 4Q13 Δ 2012 2013 Δ

Net Income for the Period 10,232 414 -96.0% 42,164 13,709 -67.5%

(-) Income Tax and Social Contribution (433) 240 -155.4% (14,782) (1,702) -88.5%

(-) Financial Result 1,846 (2,714) -247.0% 9,192 1,553 -83.1%

EBIT 8,819 2,888 -67.3% 47,754 13,858 -71.0%

(-) Depreciation and Amortization (2,090) (1,767) -15.5% (8,277) (8,335) 0.7%

EBITDA 10,909 4,655 -57.3% 56,031 22,193 -60.4%

EBITDA Margin 14.4% 6.2% -8.2 p.p. 20.1% 8.6% -11.5 p.p.

The following chart presents the reconciliation of EBITDA in 4Q12 and 4Q13(1):

(1) In R$ million.

The following chart presents the reconciliation of EBITDA in 2012 and 2013(1):

(1) In R$ million

10.9

4.7

0.3

0.4 1.3

3.9

0.3

EBITDA4Q12

Netrevenue COGS

Salesexpenses

Admnistrativeexpenses Depreciation

EBITDA4Q13

56.0

22.1

21.5

9.1 11.7

4.8 5.0

EBITDA2012

Netrevenue COGS

Salesexpenses

Admnistrativeexpenses

Other non-recuringincome

EBITDA2013

Net Cash

On December 31, 2013, the Company held a cash balance of R$11.0 million, or 51.9% lower than in the

same period last year. In 2013, the Company paid dividends and interest on equity related to fiscal year

2012 in the amount of R$34.0 million, decreased its net debt by R$5.0 million, paid R$4.9 million related

to tax liabilities under the Refis tax amnesty program and effected an advance for CAPEX investments of

R$6.8 million.

Net Cash 12/31/2012 12/31/2013 Δ 12/31/2012 Δ(1)

Short Term Debt 5,128 557 -89.1% 5,128 -89.1%

Long Term Debt 557 - -100.0% 557 -100.0%

Gross Debt 5,685 557 -90.2% 5,685 -90.2%

Cash and Cash Equivalents 28,719 11,629 -59.5% 28,719 -59.5%

Net Cash 23,034 11,072 -51.9% 23,034 -51.9%

Return on Invested Capital (ROIC)

The Company’s net ROIC in the last twelve months (LTM) to 4Q13 was 6.1%, down 11.2 p.p. from the

same period last year.

Return on Invested Capital (ROIC) 4Q12 4Q13 Δ

EBIT (LTM) 47,754 13,858 -71.0%

Average of Operating Assets 203,713 204,615 0.4%

ROIC 23.4% 6.8% -16.6 p.p.

Effective IR + CSLL rate (LTM) 26.0% 11.0% -15.0 p.p.

ROIC, Net 17.3% 6.1% -11.2 p.p.

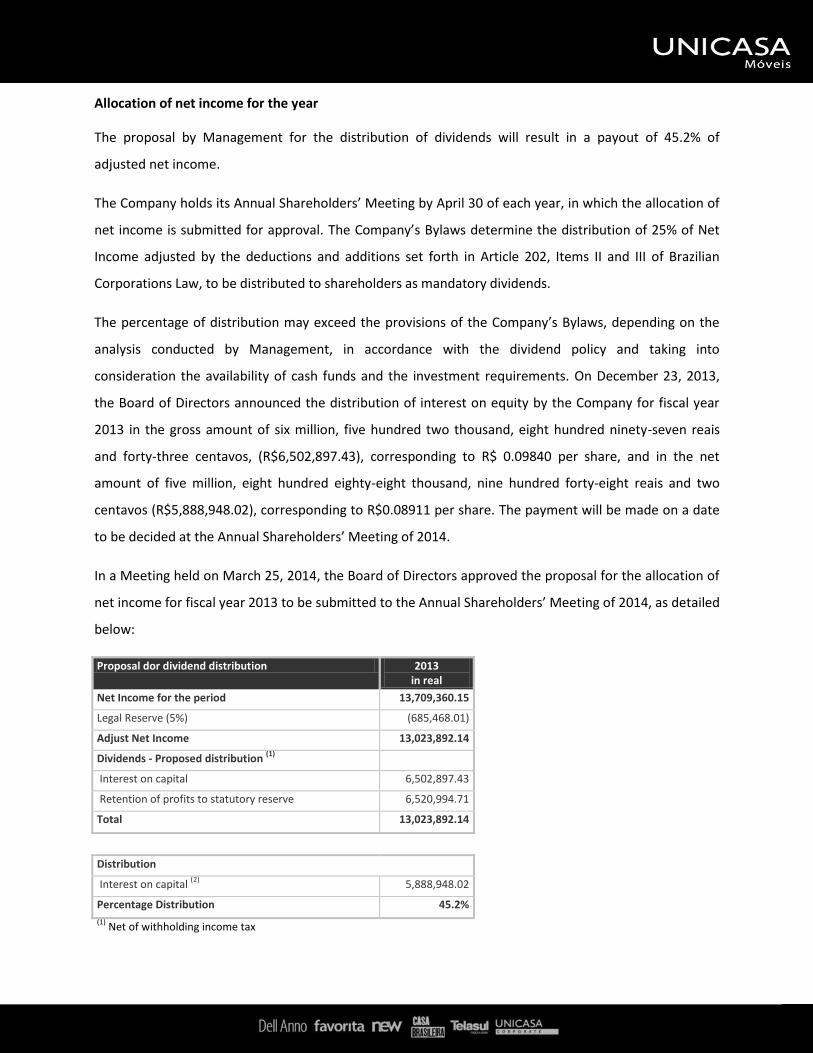

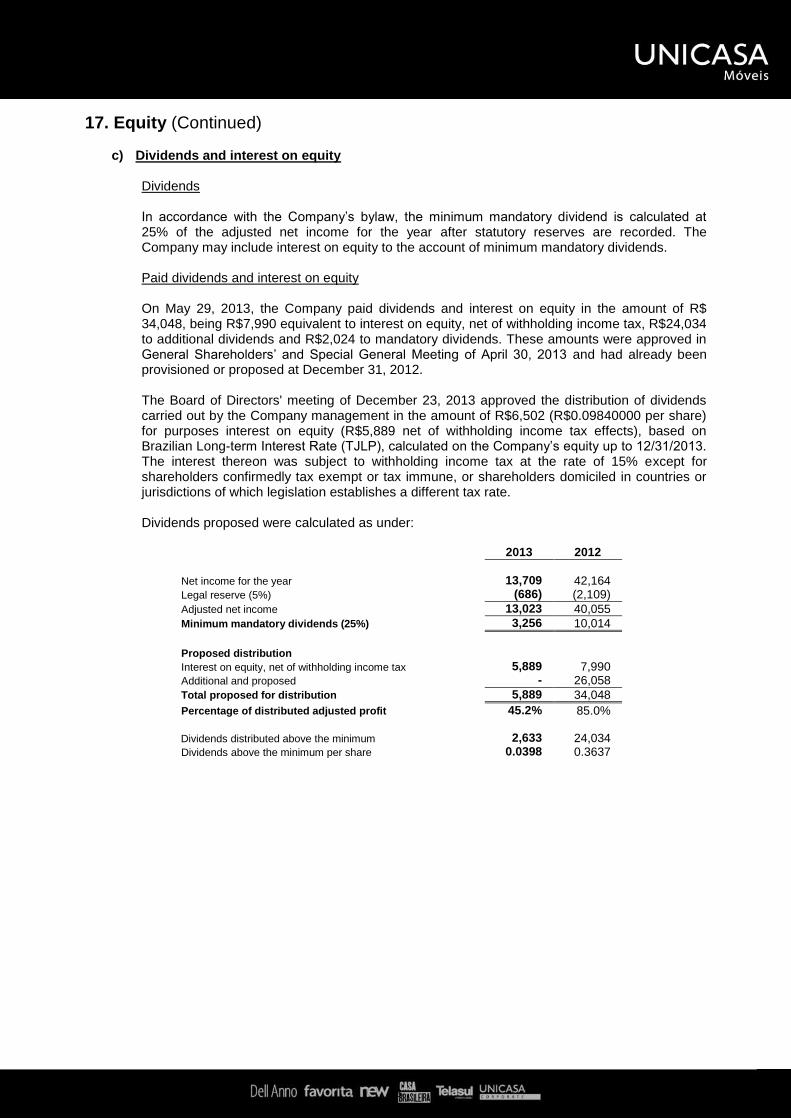

Allocation of net income for the year

The proposal by Management for the distribution of dividends will result in a payout of 45.2% of

adjusted net income.

The Company holds its Annual Shareholders’ Meeting by April 30 of each year, in which the allocation of

net income is submitted for approval. The Company’s Bylaws determine the distribution of 25% of Net

Income adjusted by the deductions and additions set forth in Article 202, Items II and III of Brazilian

Corporations Law, to be distributed to shareholders as mandatory dividends.

The percentage of distribution may exceed the provisions of the Company’s Bylaws, depending on the

analysis conducted by Management, in accordance with the dividend policy and taking into

consideration the availability of cash funds and the investment requirements. On December 23, 2013,

the Board of Directors announced the distribution of interest on equity by the Company for fiscal year

2013 in the gross amount of six million, five hundred two thousand, eight hundred ninety-seven reais

and forty-three centavos, (R$6,502,897.43), corresponding to R$ 0.09840 per share, and in the net

amount of five million, eight hundred eighty-eight thousand, nine hundred forty-eight reais and two

centavos (R$5,888,948.02), corresponding to R$0.08911 per share. The payment will be made on a date

to be decided at the Annual Shareholders’ Meeting of 2014.

In a Meeting held on March 25, 2014, the Board of Directors approved the proposal for the allocation of

net income for fiscal year 2013 to be submitted to the Annual Shareholders’ Meeting of 2014, as detailed

below:

Proposal dor dividend distribution 2013 in real

Net Income for the period 13,709,360.15

Legal Reserve (5%) (685,468.01)

Adjust Net Income 13,023,892.14

Dividends - Proposed distribution (1)

Interest on capital 6,502,897.43

Retention of profits to statutory reserve 6,520,994.71

Total 13,023,892.14

Distribution

Interest on capital (2)

5,888,948.02

Percentage Distribution 45.2%

(1) Net of withholding income tax

Capital budget

The following table presents the capital budget for fiscal year 2014, in compliance with Instruction

480/09 issued by the Securities and Exchange Commission of Brazil (CVM) on December 7, 2009.

The business projections and outlook presented in the proposed capital budget involve risks,

uncertainties and assumptions, and therefore depend on circumstances that may or may not occur.

The conditions of the general economy and the industry and other operational factors could affect the

projected amounts for the allocation to fixed assets.

To ensure the financial feasibility of the investments planned for the Company’s expansion plan,

Management proposes the retention of 47.57% of net income for fiscal year 2013, in the amount of

R$6,521 thousand, bringing the aggregate balance of the Profit Reserve for Investment and Expansion on

December 31, 2013 to R$11,518 thousand.

Sources of finance R$ mil

Retained Profits in Profits Reserve for Investment and Expansion 11,518

Own resources (generated from operational activities during the year) 1,867

Total sources of finance 13,385

Capital expenditures budget – Investment of resources 2014

Forecast

Property, plant and equipment (13,385)

Machinery and Equipment (8,113)

Equipment and IT programs (2,944)

Leasehold improvements (1,180)

Others (1,148)

Total of capital expenditure (13,385)

The Company's Management believes it is necessary to maintain the Profit Reserve for Expansion at

current levels, which will be augmented by the retained profits for fiscal year 2013 and operating cash

flow in 2014 to support the expansion plan to be implemented over the course of the year.

Responsibility and Social and Environment Protection Projects

Unicasa complies with all environmental laws applicable to its industrial segment. Following are the

practices aimed at protecting the environment:

Separation and disposal of solid waste generated in the manufacturing process;

Treatment of industrial effluents;

Rouse of 100% of the water used in our plants;

Reuse of by-products generated during the production process, such as sawdust, wood, plastic,

and cardboard, which are used by other sectors of economy;

Substitution of diesel oil by LPG (liquefed petroleum gas);

Use of packaging made of recycable plastic to transport the furniture we produce;

Use of raw material acquired only from companie, that adopt na economically viable,

ecologically correct and socially just system, certified ISO 14001, which guarantees that the

impacts of their activities are controlled and that they undertake to use the wood from certified

planted forests, owned by the Company or by third parties, or acquired from controlled sources,

in accordance with the principles and criteria of the Forest Stewardship Council (FSC). This wood

is employed in the production of reconstituted wood boards and could also be used to produce;

Air Pollution Control System.

Independent Auditors

In compliance with Article 2 of CVM Instruction 381/03, the Company informs that Ernst& Young Terco

Auditores Independentes S.S. (“Ernst”) was engaged by the Company in the following services:

Full audit conducted in accordance with Brazilian and international audit standards of the parent

company and consolidated financial statements of the Company, prepared in accordance with the

accounting practices adopted in Brazil (parent company and consolidated) and with IFRS

(consolidated), for the fiscal year ended December 31, 2013, and the review of the Company’s Interim

Quarterly Financial Information of March 31, June 30, and September 30, 2013, for total fees of

R$156,970.00. Date of contract: April 25, 2013, duration until: April 24, 2014;

Translation of the parent company and consolidated financial statements of the Company, prepared

in accordance with the accounting practices adopted in Brazil (parent company and consolidated) and

with IFRS (consolidated), for the fiscal year ended December 31, 2013, and of the Company’s

Quarterly Financial Information as of March 31, June 30, and September 30, 2013, for total fees of

R$7,030.00, representing 4.5% of the fees paid for the audit of the financial statements. Date of

contract: April 25, 2013, duration until: April 24, 2014;

Review of the valuation reports of the market value of the store use rights (“key money”) acquired by

the Company, prepared by an expert company, for total fees of R$12,250.00, representing 7.8% of

the fees paid for the audit of the financial statements;

Tax advisory services on the review of the fiscal impact on the operations conducted by the Company

in the incorporation of the Commercial Unit (Unicasa Comércio de Móveis Ltda.) and analysis of the

compliance of the tax procedures adopted with state and federal law and with judicial and

administrative jurisprudence, with the assessment of any risks related to the present operation, with

fees based exclusively on the hours effectively worked, multiplied by the average rate of R$250.00,

with total fees in 2013 of R$12,000.00, representing 7.6% of the fees paid for the audit of the

financial statements. Date of contract: May 20, 2013, duration until: May 19, 2014;

The Company’s policy in hiring any services unrelated to the external audit from the independent auditor

is based on principles that preserve the independence of the auditor, which are: (a) auditors should not

audit their own work; (b) auditors should not perform managerial functions at their client; and (c)

auditors should not promote the interests of their client.

The Company declares that it has received a letter from Ernst on the services it provided to the Company

stating that they do not compromise the principle of independence of Ernst in relation to the external

audit services rendered to the Company.

Statement by Executive Officers

Pursuant to CVM Instruction 480/09, the executive officers hereby declare that they have reviewed,

discused and agree with financial statements for the fiscal year ended December 31, 2013 and the

opinions contained in the independent auditors’ report.

Financial Statements

Unicasa Indústria de Móveis S.A.

December 31, 2013 and 2012 with independent auditor’s report on financial statements

UNICASA INDÚSTRIA DE MÓVEIS S.A. Financial Statements December 31, 2013 and 2012 Contents Independent auditor’s report on financial statements ......................................................... 1 Audited Financial Statements Balance sheets .................................................................................................................. 3 Statements of income ....................................................................................................... 5 Statements of comprehensive income .............................................................................. 6 Statements of changes in equity ......................................... ................................................7 Statements of cash flow .................................................................................................... 8 Statements of value added ................................................................................................ 9 Notes to the financial statements .................................................................................... 10

1

A free translation from Portuguese into English of Independent Auditor’s Report on Individual Financial Statements in accordance with accounting practices adopted in Brazil and on Consolidated Financial Statements in accordance with International Financial Reporting Standards (IFRS) and also with accounting practices adopted in Brazil.

Independent auditor’s report on financial statements The Shareholders, Board of Directors and Officers

Unicasa Indústria de Móveis S.A. Bento Gonçalves – RS We have audited the accompanying individual and consolidated financial statements of Unicasa Indústria de Móveis S.A. (“Company”), identified as Company and Consolidated, respectively, which comprise the balance sheet as at December 31, 2013 and the related statement of income, comprehensive income, changes in equity and cash flow for the year then ended, and a summary of significant accounting practices and other explanatory information. Management's responsibility for the financial statements Management is responsible for the preparation and fair presentation of the individual financial statements in accordance with accounting practices adopted in Brazil and of the consolidated financial statements in accordance with the International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB), and in conformity with the accounting practices adopted in Brazil, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with the Brazilian and international standards on auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatements. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Company’s preparation and fair presentation of the Company’s financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control. An audit also includes evaluating the appropriateness of accounting practices used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion on the individual financial statements In our opinion, the individual financial statements referred to above present fairly, in all material respects, the financial position of Unicasa Indústria de Móveis S.A. at December 31, 2013, and its financial performance and its cash flows for the year then ended in accordance with the accounting practices adopted in Brazil.

2

Opinion on the consolidated financial statements In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of Unicasa Indústria de Móveis S.A. as at December 31, 2013, and its consolidated financial performance and its consolidated cash flows for the year then ended, in accordance with the International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB) and with the accounting practices adopted in Brazil. Emphasis of a matter As described in Note 2.1, the individual financial statements were prepared in accordance with accounting practices adopted in Brazil. In the case of Unicasa Indústria de Móveis S.A., these practices differ from IFRS, applicable to the separate financial statements, solely with respect to the measurement of investments in subsidiaries under the equity method, while such investments would be measured at cost or fair value for IFRS purposes. Our opinion is not qualified in respect of this matter. Other matters Statements of value added We have also audited the individual and consolidated statement of value added for the year ended December 31, 2013, prepared under the Company’s Management responsibility, the presentation of which is required by the Brazilian Corporation Law for publicly held companies, and an supplementary information under the IFRS, whereby no statement of value added presentation is required. These statements have been subject to the same auditing procedures previously described and, in our opinion, are presented fairly, in all material respects, in relation to the overall financial statements. Porto Alegre, March 10, 2014. ERNST & YOUNG Auditores Independentes S.S. CRC-2SP015199/O-6/F/RS

Américo F. Ferreira Neto Accountant CRC-1SP192685/O-9

3

A free translation from Portuguese into English of Individual Financial Statements in accordance with accounting practices adopted in Brazil and on Consolidated Financial Statements in accordance with International Financial Reporting Standards (IFRS), and also with accounting practices adopted in Brazil.

UNICASA INDÚSTRIA DE MÓVEIS S.A. Balance sheets Years ended December 31, 2013 and 2012 (In thousands of reais)

Company Consolidated

Note 2013 2012 2013

Assets

Current assets

Cash and cash equivalents 4 11,316 28,719 11,629

Trade accounts receivable 5 64,308 77,732 65,342

Inventories 6 21,875 19,296 23,304

Advances and prepayments 1,449 1,038 1,559

Loans granted 8 1,287 1,971 1,287

Prepaid expenses 2,361 1,868 2,386

Taxes recoverable 6,220 3,104 6,230

Other assets 12 2,612 2,377 2,648

Total current assets 111,428 136,105 114,385

Noncurrent

Long-term receivables

Trade accounts receivable 5 9,369 15,476 9,369

Loans granted 8 2,387 5,547 2,387

Noncurrent asset held for sale 7 12,668 8,848 12,668

Deferred income and social contribution taxes 15 6,489 6,734 9,481 Taxes recoverable 18 25 18

Prepaid expenses 88 251 88

Judicial deposits 16 3,555 2,140 3,555

Other assets 12 1,975 2,004 1,975

36,549 41,025 39,541

Investments 9 784 404 82

Property, plant and equipment (PP&E) 10 80,119 78,373 81,758

Intangible assets 11 21,117 18,312 21,120

102,020 97,089 102,960

Total noncurrent assets 138,569 138,114 142,501

Total assets 249,997 274,219 256,886

4

Company Consolidated

Note 2013 2012 2013

Liabilities

Current liabilities

Loans and financing 13 557 5,128 557

Trade accounts payable 14 6,245 6,698 6,311

Tax obligations 4,196 4,961 4,636

Interest on equity payable 17.c 5,889 7,990 5,889

Salaries and social charges 4,826 4,507 5,983

Advances from customers 16,840 14,002 22,037

Mandatory dividends to be distributed 17.c - 2,024 -

Other current liabilities 985 1,057 1,014

Total current liabilities 39,538 46,367 46,427

Noncurrent

Loans and financing 13 - 557 -

Provision for tax, civil and labor contingencies 16 5,156 5,165 5,156

Total noncurrent liabilities 5,156 5,722 5,156

Equity 17

Capital 187,709 187,709 187,709

Capital reserves (2,658) (2,658) (2,658)

Income reserves 20,252 13,045 20,252

Proposed additional dividends - 24,034 -

Total equity 205,303 222,130 205,303

Total liabilities and equity 249,997 274,219 256,886

See accompanying notes.

5

UNICASA INDÚSTRIA DE MÓVEIS S.A. Statement of income Years ended December 31, 2013 and 2012 (In thousands of reais, except earnings per share)

Company Consolidated

Note 2013 2012 2013

Net sales revenue 22 256,706 279,441 257,919 Cost of sales (156,159) (163,972) (154,868)

Gross profit 100,547 115,469 103,051

Operating income (expenses)

Selling expenses (61,868) (57,422) (69,148) Administrative expenses (19,830) (19,637) (24,395)

Other operating revenues, net 19 4,020 9,344 4,350 Equity pickup 9 (6,098) - -

(83,776) (67,715) (89,193)

Income before profit or loss 16,771 47,754 13,858

Financial income (expenses), net

Financial expenses 20 (8,423) (3,075) (8,505)

Financial income 20 10,055 12,267 10,058

1,632 9,192 1,553

Income before income and social contribution taxes 18,403 56,946 15,411

Income and social contribution tax expenses 15

Current (4,449) (15,719) (4,449) Deferred (245) 937 2,747

(4,694) (14,782) (1,702)

Net income for the year 13,709 42,164 13,709

Basic and diluted earnings per share (R$) 18 0.21 0.67 0.21

See accompanying notes.

6

UNICASA INDÚSTRIA DE MÓVEIS S.A. Statements of comprehensive income Years ended December 31, 2013 and 2012 (In thousands of reais)

Company Consolidated

2013 2012 2013

Net income for the year 13,709 42,164 13,709

Other comprehensive income - - -

Total comprehensive income for the year, net of taxes 13,709 42,164 13,709

See accompanying notes.

]

7

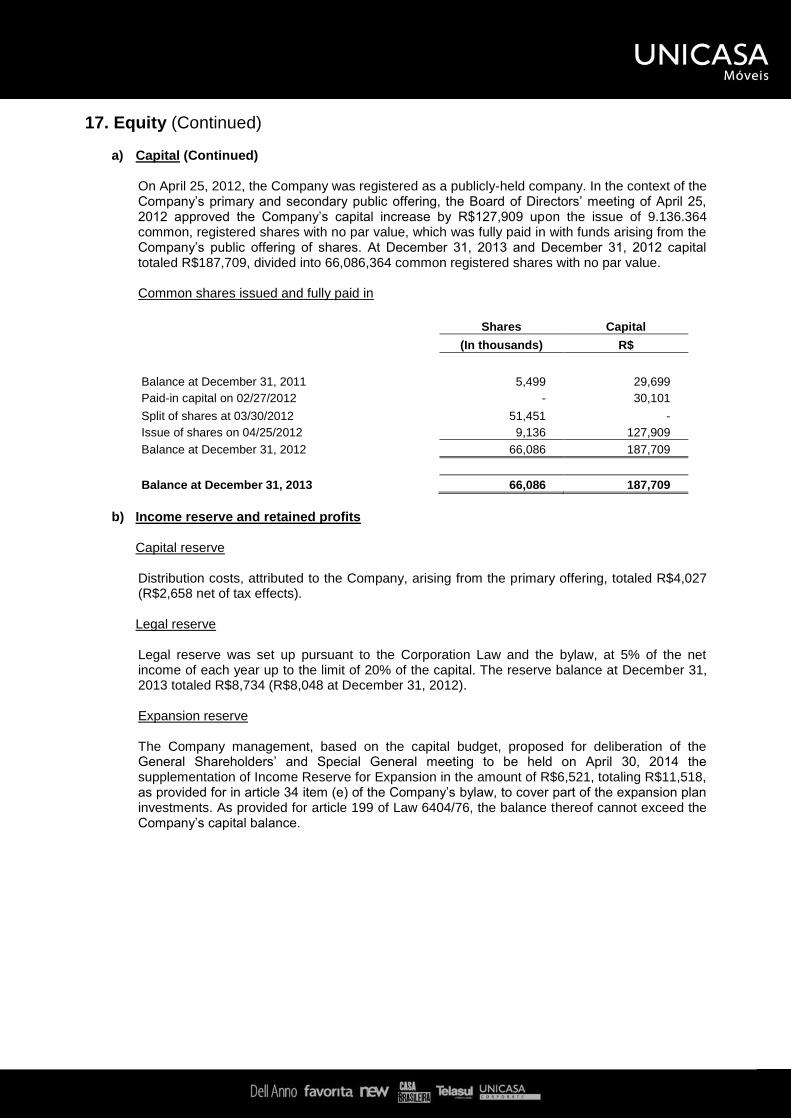

UNICASA INDÚSTRIA DE MÓVEIS S.A. Statements of changes in equity Years ended December 31, 2013 and 2012 (In thousands of reais)

Income reserves

Paid in capital

Capital reserve

Legal reserve

Reserve for expansion

Proposed additional dividends Retained earnings Total

Balances at December 31, 2011 29,699 - 5,939 - 160,101 - 195,739 Capital increase (Note 17.a) 158,010 - - - (30,101) - 127,909 Share issuance expenses (Note 17.b) - (2,658) - - - - (2,658) Distributed dividends (Note 17.c) - - - - (130,000) - (130,000) Net income for the year - - - - - 42,164 42,164 Allocation of income:

Interest on equity (Note 17.c) - - - - - (9,000) (9,000) Mandatory minimum dividends - - - - - (2,024) (2,024) Additional dividends proposed (Note 17.c) - - - - 24,034 (24,034) - Retained earnings (Note 17.b) - - 2,109 4,997 - (7,106) -

Balances at December 31, 2012 187,709 (2,658) 8,048 4,997 24,034 - 222,130 Distributed dividends (Note 17.c) - - - - (24,034) - (24,034) Net income for the year - - - - - 13,709 13,709 Allocation of income:

Interest on equity (Note 17.c) - - - - - (6,502) (6,502) Retained earnings (Note 17.b) - - 686 6,521 - (7,207) -

Balances at December 31, 2013 187,709 (2,658) 8,734 11,518 - - 205,303

See accompanying notes.

]

8

UNICASA INDÚSTRIA DE MÓVEIS S.A. Statement of cash flow Years ended December 31, 2013 and 2012 (In thousands of reais)

Company Consolidated

2013 2012 2013

Income before income and social contribution taxes 18,403 56,946 15,411 Adjustments to reconcile net income to cash and cash equivalents:

Depreciation and amortization 8,286 8,277 8,335 Foreign exchange variation - customers (87) 73 (87) Exchange variation - Suppliers (57) (15) (57) Interest appropriation 259 547 259 Provision for labor, tax and civil risks (9) 1,776 (9) Provision for obsolescence (27) (694) (27) Allowance for doubtful accounts 3,420 4,123 3,420 Provision for losses with sureties - 2,468 - Write-offs of PP&E 442 122 442 Equity pickup 6,098 - -

36,728 73,623 27,687 Changes in assets and liabilities:

Trade accounts receivable 12,987 (369) 11,953 Inventories (2,552) 3,542 (3,981) Taxes recoverable 1,591 (178) 1,581 Restricted short-term investments - 323 - Loans granted 3,844 3,184 3,844 Prepaid expenses (330) 4,081 (355) Judicial deposits (1,415) (721) (1,415) Other current or noncurrent assets (616) (4,444) (762) Noncurrent assets held for sale (3,820) (2,097) (3,820) Trade accounts payable 497 (784) 563 Advance from customers 2,838 (267) 8,035 Tax obligations (1,379) (2,831) (939) Other current and noncurrent liabilities 247 (49) 1,433 Payment of income and social contribution taxes (9,149) (26,395) (9,149)

Net cash provided by operating activities 39,471 46,618 34,675

Cash flow from investing activities:

In investments (6,800) - - In PP&E (10,106) (11,205) (11,794) In intangible assets (533) (3,137) (536)

Cash flow used in investing activities (17,439) (14,342) (12,330)

Cash flow from financing activities

Capital increase – issue of shares - 127,909 - Share issue expenses - (4,027) - Loan repayments (5,387) (1,665) (5,387) Payment of interest on equity (7,990) (7,905) (7,990) Dividend paid (26,058) (130,000) (26,058)

Cash flow used in financing activities (39,435) (15,688) (39,435)

Increase/(decrease) in cash and cash equivalents (17,403) 16,588 (17,090)

Statement of changes in cash and cash equivalents

At beginning of year 28,719 12,131 28,719 At the end of year 11,316 28,719 11,629

Increase/(decrease) in cash and cash equivalents (17,403) 16,588 (17,090)

See accompanying notes.

]

9

UNICASA INDÚSTRIA DE MÓVEIS S.A. Statements of value added Years ended December 31, 2013 and 2012 (In thousands of reais)

Company Consolidated

2013 2012 2013

Revenue from product sale, net of returns and adjustment to present value

335,831 357,958

338,337

Other revenues 3,773 8,955 4,103 Allowance for doubtful accounts (3,420) (4,123) (3,420)

336,184 362,790 339,020 Inputs acquired from third parties Cost of products and goods sold (163,567) (174,153) (163,024) Materials, energy, third-party services (47,122) (41,619) (49,595) Other (9,586) (14,448) (9,630)

(220,275) (230,220) (222,249) Gross value added 115,909 132,570 116,771 Depreciation and amortization (8,286) (8,277) (8,335)

Gross value added generated by the Company 107,623 124,293 108,436

Value added received in transfer Equity pickup (6,098) - - Financial income 10,055 12,267 10,058

3,957 12,267 10,058

Total unpaid value added 111,580 136,560 118,494

Personnel

Direct compensation 31,705 27,597 37,889 Benefits 3,547 5,251 3,949 Unemployment Compensation Fund (FGTS) 2,734 2,017 3,289

37,986 34,865 45,127 Taxes, fees and contributions Federal 28,257 34,121 25,998 State 19,723 21,830 20,071 Municipal 96 61 126

48,076 56,012 46,195 Debt remuneration Rent 3,589 444 5,161 Interest 259 547 259 Other 7,961 2,528 8,043

11,809 3,519 13,463 Equity remuneration Dividends and interest on equity 6,502 35,058 6,502 Retained profits 7,207 7,106 7,207

13,709 42,164 13,709

Total value added distributed 111,580 136,560 118,494

See accompanying notes.

10

1. Operations Unicasa Indústria de Móveis S.A. (the “Company”) was established in 1985 and is primarily engaged in manufacturing, importing and exporting furniture made of wood, iron, steel and aluminum, kitchen furniture and other commercial and residential furniture items. The Company is a publicly-held company, headquartered in the city of Bento Gonçalves, state of Rio Grande do Sul. Its shares have been traded in the New Market segment of Brazilian Securities, Commodities and Futures Exchange (BM&FBovespa S.A.), under the stock ticker symbol UCAS3 since April 27, 2012. The Company has a broad chain of exclusive retailers and multi-brand stores in Brazil and abroad selling products of the following brands: “Dell Anno”, “Favorita”, “New”, “Telasul Modulados” and “Casa Brasileira”. The Company’s modern manufacturing plant has state-of-the-art technology, developing, manufacturing, distributing and selling furniture and other products for all types of residential and commercial environments, reaching all consumption segments. Following is the Company’s subsidiary included in the consolidated quarterly information: Unicasa Comércio de Móveis Ltda. Unicasa Comércio de Móveis Ltda. was incorporated on October 8, 2012 and is engaged in the retail sale of planned furniture, with stores in operation in the city of São Paulo and Manaus. Unicasa Comércio de Móveis Ltda. started operations in April 2013.

2. Summary of significant accounting practices

2.1 Basis for preparation and presentation of financial statements The financial statements were prepared in accordance with accounting practices adopted in Brazil, which comprise the rules and regulations issued by the Brazilian Securities Commission (CVM) and the pronouncements, interpretations and guidance issued by the Brazilian Accounting Standards Committee (CPC), and in accordance with the International Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board (IASB). The Board of Directors’ meeting held on March 5, 2014 authorized the issue of the Company’s financial statements (Company and consolidated) for the year ended December 31, 2013. The preparation of these financial statements requires the use of certain accounting estimates and judgment by the Company management, the most significant of which are disclosed in Note 3. The Company reviewed and adopted all standards, revisions and interpretations issued by IASB and CPC that are effective for the financial statements for year ended December 31, 2013 and 2012.

11

2. Summary of significant accounting practices (Continued)

2.2 Basis of consolidation The subsidiary Unicasa Comércio de Móveis Ltda. is fully consolidated as of the establishment date, on which the Company acquired the control thereof and will continued to be consolidated until this control ceases to exist. The financial statements of the subsidiary are prepared for the same reporting period as that of the Company, using consistent accounting practices. All intragroup balances, revenue and expenses and unrealized gains and losses, arising from companies’ transactions are fully eliminated. The change in interest equity on a subsidiary that does not result in loss of control is accounted for as a transaction between shareholders under equity.

2.3 Investments in subsidiaries The investment in the subsidiary is assessed at the equity method, in accordance with CPC 18.

Based on the equity method, investments in subsidiaries are recorded in the Company’s balance sheets at cost, plus changes after acquisition of equity interest in the subsidiary. The equity interest in the subsidiary will be demonstrated in the Company’s income statement as equity pickup, representing the net income attributable to Company’s shareholders. After the equity method is applied for disclosure of the Company’s financial statements, the Company determines whether it is necessary to recognize additional impairment losses on its investments in subsidiaries. The Company determines, at each balance sheet date, whether there is objective evidence of impairment in the subsidiaries’ investments. If such evidence is identified, the Company calculates impairment as the difference between the recoverable and book value of the subsidiary, and recognizes the resulting amount in the Company’s income statement.

2.4 Revenue recognition Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Company and can be reliably measured. Revenue is measured based on fair value of the consideration received, net of discounts, rebates and taxes or charges on sales. The Company assesses revenue transactions in accordance with specific criteria to determine if it is the agent or principal and thus concluded it has been acting as the principal in all its sales contracts. The following specific criteria must also be satisfied before revenue recognition: Sale of products Sales revenue is recognized when significant risks and rewards of ownership of the products are transferred to the buyer, which generally occurs upon delivery thereof.

12

2. Summary of significant accounting practices (Continued)

2.4 Revenue recognition (Continued) Financial income For all financial instruments stated at amortized cost, interest income or expense is recorded at the effective interest rate, discounting exactly the payments or estimated future receipts of cash during the estimated life of the financial instruments or in a shorter period of time, where applicable, at net book value of financial assets or liabilities. Interest income is recognized under “Financial income”, in the income statement.

2.5 Translation of foreign currency denominated balances These financial statements are presented in Brazilian reais (R$), which is the Company’s functional currency. Transactions in foreign currency are initially recorded at the foreign currency exchange rate on the transaction date. Monetary assets and liabilities stated in foreign currency are translated at the foreign exchange rate effective on the balance sheet date. All differences are recorded in the income statement.

2.6 Cash and cash equivalents Cash and cash equivalents include cash, balances in bank account, short-term investments redeemable up to three months as of the date of acquisition and with insignificant risk of change in their market value

2.7 Trade accounts receivable Trade accounts receivable are recorded at billed amount, adjusted at present value when applicable, including the corresponding direct taxes incumbent upon the Company. Trade accounts receivable from foreign customers are updated as disclosed in Note 25. If the receipt period corresponds to one year or less, these accounts receivable will be classified as current assets. Otherwise, these will be classified under non-current assets. Allowance for doubtful accounts was recorded in an amount considered sufficient by the Company’s management to cover any losses arising from the realization of credits, based on the analysis of balances of customers with default risk.

13

2. Summary of significant accounting practices (Continued)

2.8 Inventories Inventories are stated at cost or net realizable value, whichever is lower. Costs incurred in bringing each product to its current location and conditions are accounted as follows: (i) Raw-materials – acquisition cost based on average cost. (ii) Finished products and work in process – cost of direct materials and labor and a

proportional portion of overhead costs, based on regular operating capacity. Net realizable value corresponds to sales price in the normal course of business, less estimated conclusion costs and estimated selling costs. Provisions for slow-moving or obsolete inventories are recognized when deemed necessary by Company management.

2.9 Noncurrent assets held for sale Noncurrent assets classified as held for sale are measured based on the lower amount between book value and fair value, deducted of cost to sell. Noncurrent assets are classified as held for sale when the related book values are recovered by means of a sale transaction, rather than through continuous use. This condition is only met when the sale is highly probable and the group of assets/assets for sale is available for immediate sale in their current condition. Management should be committed the sale. Once classified as held for sale, the assets are not depreciated or amortized.

2.10 Property, plant and equipment These are recorded at acquisition or construction cost. Depreciation is calculated on a straight-line basis at rates considering the estimated useful life of assets as described in Note 10. PP&E is stated net of Social Contribution Tax on Gross Revenue for Social Integration Program (PIS)/Social Contribution Tax on Gross Revenue for Social Security Financing (COFINS) and State VAT (ICMS) credits, recorded against taxes recoverable. An item of property, plant and equipment is derecognized on disposal or when no future economic benefits are expected from its use or sale. Possible gains or losses from assets written off - calculated as the difference between net sales and book value of assets - are included in the income statement in the year in which the asset is written off. Repair and maintenance costs are recognized in the income statement, when incurred. The net book value and useful life of assets and depreciation methods are reviewed at each year-end, and prospectively adjusted, if so necessary.

14

2. Summary of significant accounting practices (Continued)

2.11 Intangible assets Intangible assets acquired separately are measured on initial recognition at cost. Following initial recognition, intangible assets are carried at cost less accumulated amortization, when applicable. Intangible assets internally generated are not capitalized, being recognized in the income statement in the year as incurred. The useful life of intangible assets is evaluated as finite and indefinite. Intangible assets with finite lives are amortized over the useful economic life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortization period and method for an intangible asset with a finite useful life are reviewed at least at the each financial year-end. Changes in the estimated useful life or the expected pattern of consumption of future economic benefits embodied in the asset are accounted for by changing the amortization period or method, as appropriate, and treated as changes in accounting estimates. The amortization charges on finite-lived intangible assets are recognized in the income statement in the expense category consistent with the use of the intangible asset. Intangible assets with indefinite useful lives are not amortized; however they are annually tested to determine impairment losses, individually or in relation to cash-generating unit. The useful life of an intangible asset having indefinite life is reviewed annually to determine whether indefinite life assessment remains supportable. Otherwise, change in the useful life assessment from indefinite to finite shall be performed on prospective basis.

2.12 Impairment of non-financial assets Management regularly reviews the net book value of assets in order to evaluate events or changes in the operating or technological economic circumstances that may indicate deterioration or impairment. When such evidence is identified and the net book value exceeds the recoverable amount, a valuation allowance is set up by adjusting the net book value at recoverable amount The recoverable amount of an asset or a cash-generating unit is defined as the higher of value in use and fair value less costs to sell. In order to estimate the asset’s value in use, estimated future cash flows are discounted to present value by using a discount rate before taxes that reflects the weighted average cost of capital for the industry in which the cash-generating unit operates. The net sale price is determined, whenever possible, considering firm sale contracts on an arm’s length basis, between knowledgeable, willing parties, adjusted by costs to sell the asset, or, in the absence of firm sale contracts, based on the observable market price in an active market, or on the most recent transaction price involving similar assets. At December 31, 2013, no impairment risks were identified; accordingly, no provision for impairment losses was required.

15

2. Summary of significant accounting practices (Continued)

2.13 Present value adjustment of assets and liabilities Current and noncurrent monetary assets and liabilities are adjusted to present value, when the effect is considered significant in relation to the overall accompanying overall financial statements. At December 31, 2013 and 2012, only trade accounts receivable and loans granted to customers were considered significant and subject to present value adjustment. There were no other current or noncurrent assets and liabilities, which required present value adjustment. The present value is calculated at the interest rate reflecting term and risk of each transaction, also considering contractual cash flows and explicit and sometimes implicit interest rate, interest rate of the respective assets and liabilities. For forward transactions, the Company uses Selic rate variation, since this is the benchmark rate used in this type of transaction. Present value adjustment of trade accounts receivable is recorded against gross revenue in P&L and the difference between present value of a transaction and face value of billing is considered as a financial income and will be allocated based on amortized cost.

2.14 Provisions General Provisions are recognized when the Company has a present, legal or not formalized obligation arising from a past event, the settlement of which is likely to require an outflow of economic benefits, and such obligation amount may be reliably estimated. Provisions for tax, civil and labor risks The Company is party to various lawsuits and administrative proceedings. Provisions are set up for all contingencies related to lawsuits for which an outflow of resources is probable to settle the contingency/obligation and when its amount may be reasonably estimated. The assessment of the chances of loss includes analysis of available evidence, hierarchy of laws, available case law, recent court decisions and their relevance in the legal system, as well as the opinion of the Company’s outside legal counsel. Provisions are reviewed and adjusted so as to consider changes in circumstances, such as applicable prescription period, tax inspection conclusions or additional exposures identified based on new matters or court decisions.

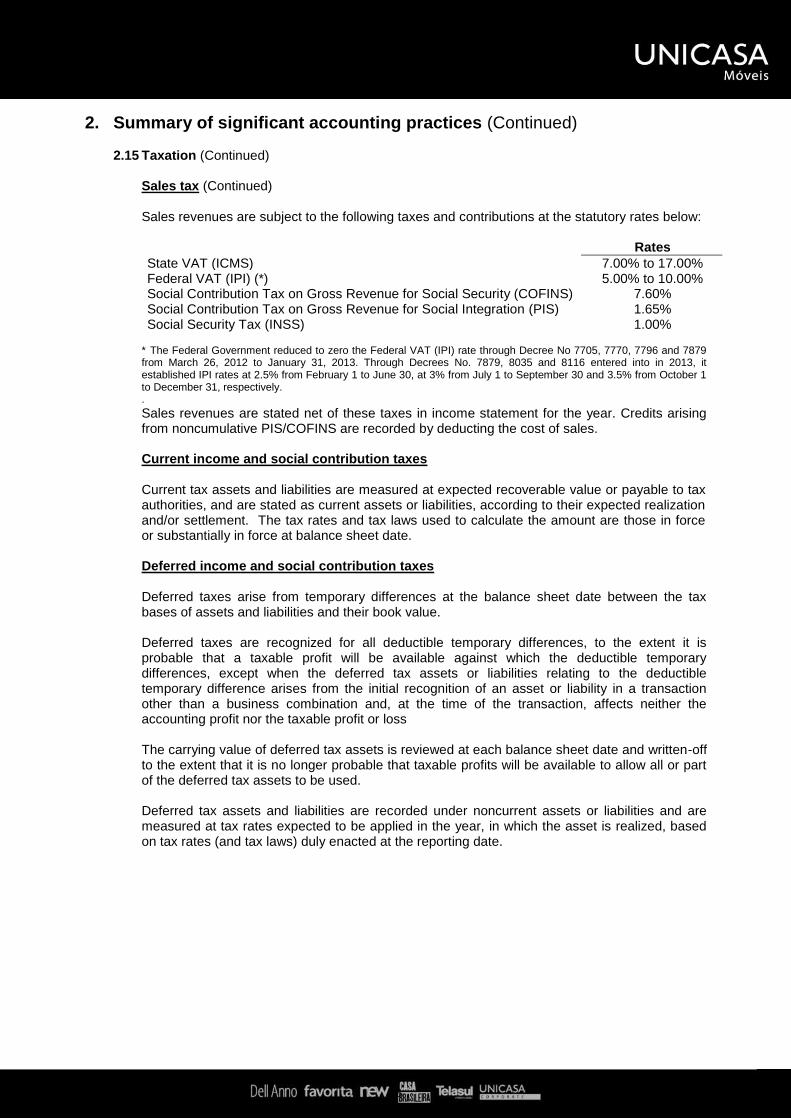

2.15 Taxation Sales tax Revenues, expenses and assets are recognized net of sales tax, except:

when taxes on sales incurred on the purchase of goods or services are not recoverable with the tax authorities, case in which taxes on sales are recognized as part of the acquisition cost or of expense item, as follows;

when amounts receivable and payable are presented together with sales tax.

when net sales taxes, either recoverable or payable, are included as a component of amounts receivable or payable in the balance sheet.

16

2. Summary of significant accounting practices (Continued)

2.15 Taxation (Continued) Sales tax (Continued) Sales revenues are subject to the following taxes and contributions at the statutory rates below:

Rates

State VAT (ICMS) 7.00% to 17.00% Federal VAT (IPI) (*) 5.00% to 10.00% Social Contribution Tax on Gross Revenue for Social Security (COFINS) 7.60% Social Contribution Tax on Gross Revenue for Social Integration (PIS) 1.65% Social Security Tax (INSS) 1.00%

* The Federal Government reduced to zero the Federal VAT (IPI) rate through Decree No 7705, 7770, 7796 and 7879 from March 26, 2012 to January 31, 2013. Through Decrees No. 7879, 8035 and 8116 entered into in 2013, it established IPI rates at 2.5% from February 1 to June 30, at 3% from July 1 to September 30 and 3.5% from October 1 to December 31, respectively. . Sales revenues are stated net of these taxes in income statement for the year. Credits arising from noncumulative PIS/COFINS are recorded by deducting the cost of sales. Current income and social contribution taxes Current tax assets and liabilities are measured at expected recoverable value or payable to tax authorities, and are stated as current assets or liabilities, according to their expected realization and/or settlement. The tax rates and tax laws used to calculate the amount are those in force or substantially in force at balance sheet date. Deferred income and social contribution taxes Deferred taxes arise from temporary differences at the balance sheet date between the tax bases of assets and liabilities and their book value. Deferred taxes are recognized for all deductible temporary differences, to the extent it is probable that a taxable profit will be available against which the deductible temporary differences, except when the deferred tax assets or liabilities relating to the deductible temporary difference arises from the initial recognition of an asset or liability in a transaction other than a business combination and, at the time of the transaction, affects neither the accounting profit nor the taxable profit or loss The carrying value of deferred tax assets is reviewed at each balance sheet date and written-off to the extent that it is no longer probable that taxable profits will be available to allow all or part of the deferred tax assets to be used. Deferred tax assets and liabilities are recorded under noncurrent assets or liabilities and are measured at tax rates expected to be applied in the year, in which the asset is realized, based on tax rates (and tax laws) duly enacted at the reporting date.

17

2. Summary of significant accounting practices (Continued)

2.16 Other employee benefits Benefits granted to Company’s employees and managing officers include, in addition to fixed compensation (salaries and social security contributions, vacation pay and 13th monthly salary pay), variable compensation, such as profit sharing, health care plan and education allowance. These benefits are recorded in the income statement for the year when the Company has an obligation on an accrual basis, as incurred.

2.17 Earnings per share The Company calculates its basic and diluted earnings per share using the weighted average number of common shares outstanding over the corresponding period.

2.18 Cash flow statement and statement of value added

The cash flow statements were prepared under the indirect method and are presented in accordance with CPC 03 R2 (IAS 7) - Cash Flow Statement issued by the Brazilian Accounting Standards Committee (CPC). The statement of value added was prepared in accordance with CPC 09.

2.19 Financial instruments - Initial recognition and subsequent measurement

Initial recognition and measurement Financial instruments are initially recognized at fair value plus transaction costs directly attributable to their acquisition or issue, except for financial assets and liabilities classified at fair value through profit or loss, when such costs are directly charged to P&L for the year. The main financial assets recognized by the Company comprise; cash and cash equivalents, trade accounts receivable and loans granted to customers. These assets were classified under loans and receivable. The main financial liabilities comprise; trade accounts payable, other accounts payable and loans and financing. These instruments are classified as loans and financing and measured at amortized cost. Subsequent measurement The subsequent measurement of financial instruments is performed at each balance sheet date according to classification of financial asset and liability under the following categories: fair value through profit or loss, held-to-maturity investments, loans and receivables and loans and financing. The Company’s financial assets and liabilities were classified into the following categories:

18

2. Summary of significant accounting practices (Continued)

2.19 Financial instruments - Initial recognition and subsequent measurement (Continued) Subsequent measurement - (Continued) Loans and receivable Loans and receivables are non-derivative financial assets with fixed or determinable payments not quoted in an active market. After initial measurement, such financial assets are subsequently measured at amortized cost at the effective interest rate method less impairment. Amortized cost is calculated by taking into account any discount or premium upon acquisition and fees or costs incurred. The amortization of the effective interest rate method is recorded under financial income under P&L. Impairment losses are recognized as financial expenses under P&L. Loans and financing After initial recognition, interest bearing loans and financing are subsequently measured at amortized cost using the effective interest rate method. Gains and losses are recognized in P&L when the liabilities are written off, as well as upon amortization under the effective interest rate method.

2.20 Information by segment The Company’s operations involve developing, manufacturing, marketing and providing furniture-related services (modular and planned) for both the domestic and international markets, which are organized in a single operating segment. Although products are sold through specific sales channels, according to their category, the Company manages and controls its products on an integrated basis. The corresponding operating results are also monitored and assessed on an integrated basis

2.21 Lease agreements

Finance leases that transfer basically all the risks and rewards related to ownership of the leased item to the Company are capitalized at the inception of the lease at fair value of the leased asset or, if lower, the present value of minimum lease payments. Costs will be increased by the initial directed costs incurred in the transaction, where applicable. Payments of finance lease transactions are allocated to financial charges and reduction of liabilities of finance lease transactions in order to obtain a constant interest rate on the remaining balance of the liabilities. The financial charges are recognized in the income statement. The leased assets are depreciated over their useful lives. However, when there is no reasonable certainty that the Company will obtain ownership at the end of the lease term, the asset is depreciated over its estimated useful life or within the lease term, whichever is shorter. The operating lease payments are recognized as expense in the income statement at a straight-line method over the lease transaction term.

19

2. Summary of significant accounting practices (Continued)

2.22 IFRS standards not yet effective as of December 31, 2013

Standards issued but not yet effective Following are the standards and interpretations issued but not yet effective on this reporting date. The Company intends to adopt these pronouncements, if applicable, once they become effective. IAS 32 Offsetting of Financial Assets and Financial Liabilities – Amendments to IAS 32 These amendments explain the meaning of “currently have a legally enforceable right of set-off”. The amendments also explain the adoption of the offset criteria of IAS 32 for the settlement systems (such as the clearing house systems), which apply gross mechanisms of settlement that are not simultaneous. These amendments will not have an impact on the Company’s financial position, performance or disclosures effective for annual periods beginning on or after January 1, 2014. IFRS 9 — “Financial Instruments: Classification and measurement IFRS 9 Financial Instruments- Recognition and Measurement IFRS 9, as originally issued, reflects the first Phase 1 of IASB’s work to replace IAS 39 in its entirety. It is applicable to recognition and measurement of financial assets and financial liabilities, such as established in IAS 39. IFRS 9 was initially effective for periods beginning after January 1, 2013, however; Amendments to IFRS9 – Effective date of IFRS 9 and Transition Disclosures, issued in December 2011, amended the effective date of IFRS 9 to January 1, 2015. IASB will subsequently address the impairment methodology and hedge accounting of financial assets. The Company does not expect this amendment to affect its financial statements. IFRIC 21 Levies IFRIC 21 provides guidance on when to recognize a liability for a tax or levy when the obligating event occurs. For a levy that is triggered upon reaching a given metric, the interpretation indicates that no liability should be recognized before the specified metric is reached. IFRIC 21 is applicable for annual periods beginning on or after January 1, 2014. Management does not anticipate any material impact from IFRIC 21 on the financial statements of the Company. There are no other standards and interpretations issued but not yet adopted that may, in the management opinion, have a significant impact on the income or equity disclosed by the Company.

.

20