Management Presentation 27 th September 2002. Corporate Strategy Andrew Lindberg Managing Director...

91

Management Presentation 27 th September 2002

-

Upload

angel-dorsey -

Category

Documents

-

view

215 -

download

0

Transcript of Management Presentation 27 th September 2002. Corporate Strategy Andrew Lindberg Managing Director...

Management Presentation27th September 2002

Corporate Strategy

Andrew LindbergManaging Director

27th September 2002

Our financial objectives are clear

Target:

• 15% ROE

• Consistent trend EPS growth

• Stable dividend

• Improve quality of earnings

• Efficient capital management

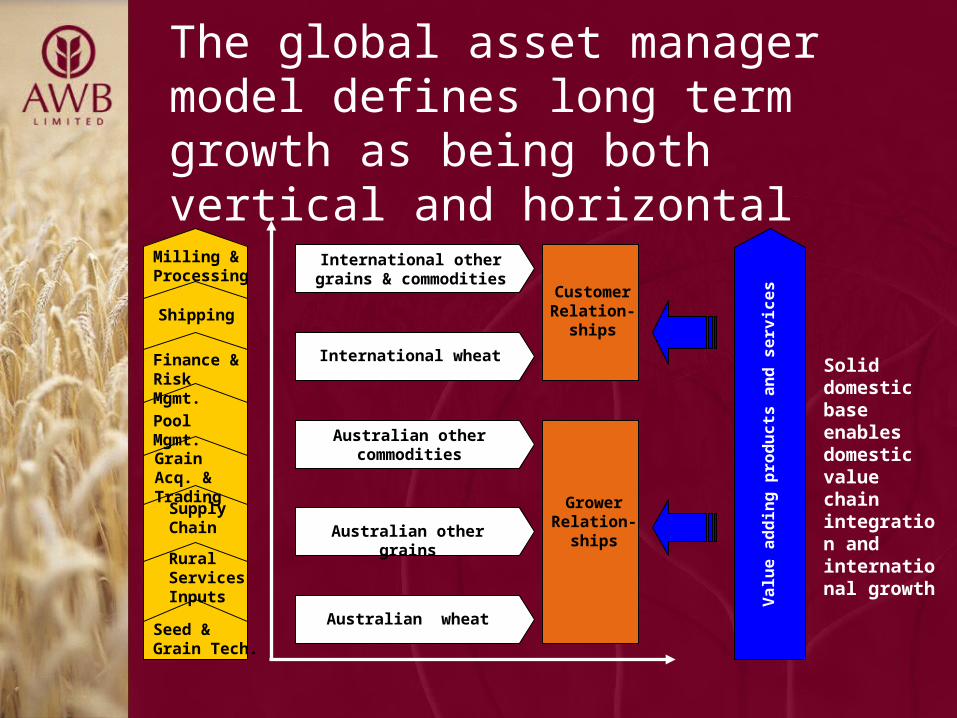

The global asset manager model defines long term growth as being both vertical and horizontal

Australian other grains

Australian other commodities

Australian wheat

International wheat

International other grains & commodities

Solid domestic base enables domestic value chain integration and international growth

Grower Relation-

ships

Customer Relation-

ships

Va

lue

ad

din

g p

rod

uc

ts a

nd

se

rvic

es

Rural Services Inputs

Seed & Grain Tech.

Shipping

Finance & Risk Mgmt.

Grain Acq. & Trading

Supply Chain

Milling & Processing

Pool Mgmt.

Maximise value for growers, customers & shareholders

In order to achieve our objectives, AWB has clearly defined strategies

• Win grower mandates• Create value through supply

chain efficiencies

• Sustain trading out performance • Lead in grain technology

• Maintain growth and diversify revenue streams

• Strengthen stakeholder support

• Secure end user demand• Strengthen organisational

capability and performance

Specific near term initiatives will support our strategies

• Diversify domestically and offshore

– Expand finance & risk management offerings

– Strengthen position in Asia and Middle East and develop global trading business (Geneva)

– Step up investigation of M&A opportunities

• Increase grains under management

• Strengthen our rural services base

• Supply chain investments that provide commercial returns

• Active capital management

• Ensure effective cost control

In 2001/02 AWB strengthened its core business …

Strengthen core business to sustain performance

• Further improvement to a key under-performing business area - Chartering

• Strengthening of the performance of the Single Desk and implementation of new performance based remuneration model

• Broaden financial and risk services to growers and customers

• Strengthen grower/rural services and financial advisory networks

• Development of AWB supply chain network with capacity of around 3mt

• Development of superior grain varieties through a JV with Syngenta

• Establishment of new business processes, systems and product development capability

Diversification … through acquisitions, other grain trading, non-pool chartering and global trading will result in a lower reliance on Australian wheat receivals

0%

20%

40%

60%

80%

100%

2001-02 (f) 2002-03 (p) 2003-04(p)

(f) = AWB forecast (p) = AWB Plan

Other grain and non-Aust wheat & Diversification

Wheat related

NPAT Diversification ($m)

97% 90% 80%

3%10%

20%

M&A activity is important to assist diversification

• Less than 80% reliant on wheat by 2004/05

• 15% ROE target

• Establishment of platforms for further growth and diversification

• Efficient capital management

• Further pursue and review opportunities in the value chain, other grains, other commodities

• Assess other opportunities for strategic fit as they become available

• Continue to manage current overseas investments

• Review of management of Single Desk in 2004

• Increased competition from domestic and global players

• Rationalisation of domestic supply chain

• Opportunities in other commodities, other grains

• Offshore opportunities

Planned Outcomes

InitiativesEnvironment

Investment highlights

• Significant expertise and scale in global wheat marketing

• One of the largest integrated global wheat managers

• Large existing customer base

• Manager of the Single Desk

• Potential to broaden range of products, services and

customers in Australia and overseas

• Strong balance sheet and dividend paying capacity

QUESTIONS

Corporate Strategy

Capital Management, Risk Management & Financial Services

Paul InglebyChief Financial Officer

27th September 2002

Efficient capital management

01/02

Shareholders’ funds (average) $772m

PAT (midpoint of range) $105m

ROE 13.6%

EPS 38 cps

DPS 25-28 cps

Capital allocation

Capital is allocated (notionally to businesses)

• Main businesses that use capital are:

- Finance & Risk Management Products

- Grain Acquisition & Trading

- Supply Chain & Other Investments

• Other business streams include:

- Grain Technology

- Pool Management Services

Capital management

• We allocate capital using a top-down and bottom-up approach

• We consider a range of factors such as targeted credit rating, value at risk and the universe of agricultural operations and product companies

• As an indication, for 2001/02 we allocated:

- Finance & Risk Management Products $150m

- Grain Acquisition & Trading $200m

- Supply Chain & Other Investments $100m

• Other main capital uses include corporate assets

• As we diversify we will allocate capital accordingly

Capital management (cont)

• Capital management means getting maximum value from

capital through leverage within risk range

• We target rating levels and to some extent this will

determine if we have excess capital

• We are continually looking at ways to grow the business

- Organically

- Investments in end use assets

- Investments in supply chain

- Acquisitions

Capital management (cont)

Commercial Paper

• We fund the company and therefore businesses through 3 commercial paper (CP) programs – AUD, US & EURO

• We have a relationship bank panel of 16 throughout the world. These banks provide liquidity support i.e. ability to fund company at all times even when markets are tight

• Last year AWB issued over $US5b in CP

• We are an active participant in the FX, Options and Swaps markets

Capital management (cont)

• We are constantly looking at the mix of capital and debt in relation to the opportunities available to us

• Depending on the range and size of these opportunities we will consider the structure of the balance sheet for maximum value to shareholders

• This will include raising some long term debt (none currently) which could take the form of medium term notes, private placement, or hybrid securities.

• We will consider a share buy back if this makes sense for shareholder value

Risk management

AWB comprises of a range of businesses with a range of risk profiles.

AWB has a focus on risk management:- Corporate Risk Board Committee (CRBC)

- Corporate Risk Review Committee (CRRC)

- Corporate Risk Unit (CRU)

Key factors are:- Physical sales

- Foreign exchange management

- Wheat price management

- Administration

- Governance

Financial services product range has been

expanded to provide more flexibility to growers

• Pool payment options take-up above 65%

• Enhanced relationship with growers from more flexible product suite

• Improved skill set and product knowledge of staff in marketing financial services

• Improve ‘time to market’

• Wealth creation pilot program

• New Group GM of Financial Services, Marcus Kennedy

• Expand loan products:- Harvest Loan- Flexible Drawdown Loan

- Pre Delivery Loan

• New payment products:- Advanced Payment- Deferred Payment

• Strengthening of grower services network

• 6 new Regional Financial Services Managers as on-ground product experts

• Reliant on value of national wheat export crop

• Increase in cash purchases decreases market available for loans

• Increased competition from banks, particularly NAB, ANZ and CBA

• Expand financial services to offer more cashflow choices for grain marketing decisions

• Opportunity to introduce wealth creation products and strategies to growers

Planned OutcomesInitiativesEnvironment

QUESTIONS

Capital Management, Risk Management & Financial Services

Grower Interface

Tim GoodacreGroup General Manager Corporate

27th September 2002

Grower profile

• 35,000 grain growers

• Average wheat yield = 1.91* tonnes per hectare

• Average wheat grower cash income = $113,503*

• Average size of grain cropping per farm = 500ha

• Average wheat tonnage produced per grower = 600t

• Average wheat delivered to AWB per grower = 480t

• Grower attitudes**

- 88% support the Single Desk

- 88% support AWB’s management of the Single Desk

*Average over 3 years to 2001-02, source = ABARE ** Independent Survey, 2002

The relationship with growers will be enhanced by a stronger rural presence

• Continue to

enhance existing

deep relationship

with growers

• Maximise market

penetration

• Retention of Single

Desk beyond 2010

• Expanded grower

services network

- 63 AWB

regional staff

(plus 6 financial

advisers)

- 25 AWB

regional offices

- 10 agencies

• Increased

competition by banks

and bulk handlers

• New more flexible

suite of AWB

products

• Growers perceive

AWB is heading in

the right direction

• 88% grower support

for Single Desk

marketing

Planned Outcomes

InitiativesEnvironment

Strategy to further enhance grower relations

Formation of Grower Relations Division with mission to:

• Maintain and build grower support for AWB and AWB

managed Single Desk

• Further align AWB with the commercial needs of

growers

QUESTIONS

Grower Interface

National Pool and the Pool Services Management Model

Sarah ScalesGeneral Manager National Pool

27th September 2002

AWB

Growers

Business services

Pool payments

Wheat deliveries

AWBI Export markets

Wheat

marketing

Monitor

performance of

AWBI

Wheat Export

Authority

Relationship of the WEA, AWB & AWBI

Performance Based Remuneration

• Retention of Single

Desk beyond 2010

• Performance based

remuneration system

fully integrated into

business

• Continued

maximisation of

returns to growers

through pool out-

performance

• Focus on performance

improvement

• Management of the

relationship with the

WEA

• OPI implementation

• About 50% decreased

crop value in 2002/03

compared to 2001/02

• 2002-03, second year

of OPI arrangements

- First year of OPI

entitlement from

previous year

• Review of management

of Single Desk in 2004

Planned Outcomes

InitiativesEnvironment

Note: OPI = Out Performance Incentive

AWB(I)’s Mandate

Maximise net returns to National Pool Growers

• Maximise USD FOB price obtained

• Minimise USD/AUD rate

• Minimise domestic supply chain costs deducted from growers

Actively manage the main harvest risk exposures

• Management of wheat price, currency and domestic supply chain cost exposures

Total harvest coverage

• Accept delivery of all grades of Australian wheat (subject to minimum quality standards)

• Sell all Australian wheat delivered to the National Pool in the pool period

AWB(I)’s Pool Management Performance Benchmark - WIB

1. USD Wheat PriceSub-

benchmark

2. FX (AUD/USD)

Sub- benchmark

3. Domestic Supply Chain

Sub- benchmark

• WIB designed to measure AWBI performance consistent with mandate

• Integrated nature of risk and return

- Price

- FX

- Supply Chain costs

• Applicable to market:

- World/Competitor prices

- Liquidity, demand, capacity constraints.

• Seasonal pool basis – applicable to management and growers

WIB Pool Benchmark

A performance hurdle is necessary to reconcile AWB(L) decision making ability with the full AWB(I) mandate

Hurdle Components

Freight advantage:

• Reflect price advantages/ disadvantages available to any Australian wheat exporter

Single Desk Advantage:

• Reflect the market power available to any manager of the Single Desk System

Performance Based Remuneration Model

1. Base Fee

• 1.5% of Gross Pool Value(GPV)

• Subject to a cap of AUD$60m and a floor of AUD$45m (CPI indexed)

• Effectively covers operating costs to provide services to AWB(I)

• Reduces risk to both AWB(I) and AWB(L)

2. Out-Performance Incentive (OPI)

• Calculated as 20% of revenue generated above the WIB plus hurdle: = [GPV – {WIB + HURDLE}] x 20%

Total cap of 3% of GPV, limiting risk to AWB(I)

The performance based remuneration model has a two-

tiered payment system consisting of:

Conclusion

• Consistent with the Pool mandate:

- Strives for out-performance within defined risk parameters - balancing grower risk and grower rewards (Pool Returns)

- Does not strive for maximum returns regardless of risk

• Transparent, objective, auditable

• Provides incentive to the manager to maximise grower returns

• Grower preference: reflects main revenue and cost drivers for the National Pool & links AWB(L) remuneration to Pool Performance

• Practically applicable to the business & consistent with industry standards

• Quantifies and limits remuneration risk to AWB(I) and AWB(L)

• Encourages AWB(L) to invest in achieving out-performance

QUESTIONS

National Pool and the Pool Services

Management Model

Grain Acquisition & Trading

Peter GearyGroup General Manager Trading

27th September 2002

Domestic and global trading

Grain Acquisition & Trading

Domestic Global

• Establish global trading

business in Geneva

• Establishing new trade flows

with new customers

• 02/03 opportunity to supply

existing customers other origin

wheat

• Global trading to trade 1.5

million tonnes in 2002/03

•Contract Acquisition Products

- 70 Regional based representatives

- 2 million tonnes committed prior to harvest 2001/02

•Domestic Trading

- Wheat and other grains

- 50 domestic customers

- Grain traders

- Pool transfers

- Normally trade 4.5 to 5 million tonnes

•Non Wheat exports

- Canola, sorghum, barley

Our domestic trading strategy

• Grain is predominately

accumulated incrementally from

growers

• Grain is physically priced with

customers or priced in the

derivatives market leaving a basis

position to trade

• AWB also trades with other grain

companies which increases the

volume of grain trade and liquidity

to close physical positions

• Positions will be built and

transferred to the Pool in the

appropriate circumstances

Major factors impacting

trading strategy for

growers in 02/03

• Domestic regional

shortages in high

domestic demand areas

Mix of traded grain

0

1

2

3

4

5

6

99/

00

00/

01

01/

02

02/

03(p

)

Pool wheat Trading Wheat

Other Grain Fwd Contract

2002/03 we could see:

• Forward contracting

approaching 2000/01 levels

• East coast cash prices are

outstripping national pool

returns and will be primarily

trade for cash

• Transfers to the pool, (other

than on east coast) but at

reduced levels

(p) = AWB projection

mt

Trading risks and how we manage them

• Local production – volume traded

• Price volatility – production in exporters &

importer

• Foreign exchange exposure – active

management

• Hedging is used to price physical

exposures (not to speculate)

• Basis trading – requires correctly

positioning physical product in line with

movements in basis

Drought conditions result in contract

washouts

• replacement cost to protect position

• credit risk of collecting washout settlement

Grower demand for risk products increasing

• Increased take-up

of Riskassist

• Stronger

relationship with

growers

• Contribution to

securing end user

demand through

solution selling

• Expanded range of risk

management products:

- Basis Pool

- Riskassist – Basis

Pool Products

- Riskassist – Fixed

Basis Contracts

- Riskassist –

Consumer Risk

Services

• Grower demand for

risk products

increasing

• Opportunity to expand

the range of contract

alternatives to

growers

• Opportunity, as part of

trading group, to

provide solution

selling to end users

Planned Outcomes

InitiativesEnvironment

QUESTIONS

Grain Acquisition & Trading

Supply Chain Investments & Chartering

Jill GillinghamChief Operating Officer

27th September 2002

Agenda

• Objectives for supply chain

• Outline of supply chain strategy

• Examples of returns

• Chartering

Objectives for supply chain

• Reduce costs

• Improve efficiency

• Secure grain for the long-term

• Commercial return on capital invested

East Coast:Compete

West Coast:Collaborate

Strategy

Domestic supply chain strategy

•Supply chain optimisation

•Deliver a return on investment above weighted average cost of capital

•OPI for supply chain sub-benchmark

• Increase AWB’s ability to access the wheat flow

•Strategic hedge against deregulation

• New grain centres built

• On farm storage pilot being conducted during the 2002/03 harvest in Southern NSW

• Investment in NSW rail and grain handling infrastructure via joint rail freight agreement with FreightCorp

• Purchase of rail wagons – leased to Freight Australia

• Port options being investigated

• JV / Merger options being investigated with CBH and Grain Pool of WA

• Supply chain costs of $1.4b

• Domestic supply chain inefficient

• Old infrastructure BHCs have geographic monopolies and employ traditional uniform pricing structures

• Freight companies with traditional monopolies have also employed uniform pricing structures

• Susceptible to competition from new entrants with modern infrastructure and differential pricing

Planned OutcomesInitiativesEnvironment

Expenditure on AWB grain centres*

Number of Sites (Cumulative)

Capacity Location Capital Cost (Cumulative)

1999/00 1 200k VIC $11M

2001/02 7 1m4 VIC

3 NSW$58M

2002/03 16 2.9m

4 VIC

9 NSW

3 SA

$130M

2003/04 Up to 22 4.0m TBA Up to $175m

* 17 Grain centres have been announced

Grain Centres – Dimboola Grain Centre

1999/00 2000/01 2001/02f

Tonnes Received (kt) 89 203 232

EBITDA ($m) 0.6 1.4 1.9

EBIT ($m) (0.1) 0.5 1.0

Asset WDV $10.5m $9.7m $8.9m

ROI (1.0%) 5.0% 11.0%

• Investment of $11.3m in 1999

Note: WDV = written down value

Grain Centres – Standard new site

Year 1 Year 2 Year 3 Year 4 Year 5

Tonnes Received (kt) 100 125 168 168 168

EBITDA ($m) 0.4 0.8 1.2 1.2 1.2

EBIT ($m) (0.2) 0.2 0.7 0.7 0.7

Asset WDV $6.7m $6.1m $5.5m $5.0m $4.5m

ROI (3.0%) 3.3% 12.7% 14.0% 15.6%

• Investment of $7.3m for each site

Current Investments – Melbourne Port Terminal

Note: AWB’s financial year differs from the contract period. High payment rates for initial tonnages are spread between alternate years leading to the variation in financial results shown above.

2000/01 2001/02f

Tonnes Received (kt) 1,257 1,222

EBITDA ($m) 3.9 3.1

EBIT ($m) 3.1 2.3

Asset WDV $17.8m $17.0m

ROI 17.0% 13.5%

• Investment of $18.6m in 2000

Current Investments – Rail Wagons

Year 1 Year 2 Year 3

EBITDA ($m) 1.15 1.15 1.15

EBIT ($m) 0.8 0.8 0.8

Asset WDV $4.8m $4.4m $4.0m

ROI 16.8% 18.2% 19.8%

• Investment of $5.4m in 2001

Customer

Chartering

National Pool/Trading

External

CFR or FOB+FR

FR

FR

One Parcel of Grain

Three AWB Contracts

Freight offer by

Chartering

“Market on the Day”• No margin • Net of Adcom

Chartering

Position Takers

plus Success Fee

1

2

3

Chartering contract flow

Objective is to increase non-pool chartering

• Increase tonnes

sold CFR to around

55% by 2004/05

• Triple non pool

chartering tonnes

by 2004/05 (to

1.6mt)

• Charter 2.0 million

tonnes from

Geneva office by

2003/04

• Increase pool tonnes

sold CFR

• Build a chartering

program to achieve

economies of scale

thereby enabling

globally competitive

rates for non pool

chartering

• Develop freight

function in Geneva to

complement Global

Trading

• Pool chartering

dependent on size of

export crop

• Market conditions

putting pressure on

trading margins

• Opportunity to expand

non pool business

• Opportunity to increase

market penetration of

chartering through

global trading

Planned Outcomes

InitiativesEnvironment

Summary

• Reduce costs

• Improve efficiency

• Secure grain for the long-term

• Commercial return on capital invested

QUESTIONS

Supply Chain Investments &

Chartering

Presentation Supplement

Finance & Risk Management Products

Wheat receivals currently have significant impact on profit

Sensitivity Analysis

Key DriversIncremental

changeImpact on

2002-03 NPAT

National Wheat Crop (mt) +/- 1mt

USD Wheat Price (US$) +/- US$5.00

USD/AUD Exchange Rate -/+ $0.05

Domestic Interest Rate (%) +/- 1.0%

+/- $6 - 7m

+/- $1m

+/- $3m - 4m

+/- $2m - 3m

Opportunity to introduce wealth creation products and strategies to growers

• $3.5-$5B in gross pool value per annum

• Each crop farm has $70,000 in liquid assets ($31k shares, $17k deposits)

• Average balance of Farm Management Deposit account is $40,000 (medium/long term investment product)

• Succession planning issues for growers

• AWB has strong brand name with growers

• Pilot program in 2003

Source: ABARE, Australian Farm Surveys Report 2001. Dept of Fisheries, Agriculture and Forestry Australia

Strengthening our financial services manufacturing and distribution capability

• Marcus Kennedy, new Group General Manager Financial Services

- Strong financial services background

• Grower Services Division

- 63 regional staff, 25 regional offices and 10 agencies

• 6 new Regional Financial Services Managers

- On-ground product experts

• Product Development Division

- Improving ‘time to market’ capability

• New SAP system which enables products to be built in-house rapidly

AWB business sensitivities

Climate -Impact on domestic and offshore crop production

International prices

& exchange rates

-Wheat price impacts

-AUD relative to USD

-Increase in US and European farm subsidies

Global Markets-Instability in Iraq

-Increasing role of minor exporters

Regulatory-Review of management of Single Desk in 2004 by WEA

-ACCC

Competitive

-Rationalisation of domestic supply chain

-Banks and bulk handlers providing financial services

-Global traders entering domestic market

Pool management services risk profile

Operation Risk Control / Risk Mitigator

National Pool

• OPI Fee Return

• Price Risk (Flat & Basis)*

• FX Risk*

• Interest rate risk*

• Sales risk*

• Crop size*

• Logistics risk*

• Credit risk*

• Hedge Policies & Benchmarks

• Board Committees Oversight

• Position Reporting

• Mgt Risk Committee Monitoring

• Credit Limits on Counter-Parties

• Internal/External Audit Reviews

• Credit Risk Transfer

• Insurance

* Grower risks

Finance & risk management products risk profile

Operation Risk Control / Risk Mitigator

Financial services products

• Underwriting Risk

• Size of Pool

• Margin on Loans

• Underwriting Fees

• Reduced Take-up of Harvest Payment Products

• Loan Book Interest Rate

• Competition

• Underwriting risk model mgt

• Grower Services relationship management

• Interest Rate risk management policies

• Product design flexibility and speed to market

Basis Pool Management

• Basis Pool Receival Tonnes

• Management & underwriting fee

• Grower Services relationship mgt

Discretionary Treasury Trading

•Market risk• FX & IR risk limits

• Mgt Risk Committee Monitoring

Riskassist

•Tonnes Managed by Risk Assist

•Risk Assist Fee

•Grower credit risk

• Contracting policy limits

• Grower Services relationship mgt

• Insurance to mitigate potential

Grain acquisition & trading risk profile

Operation Risk Control / Risk Mitigator

Domestic Trading

• Trade Execution Management

• Credit Risk

• Market Risk

• VAR & Trading Limits

• Board Committee oversight

• Position reporting

• Mgt Risk Committee Monitoring

Grain Contract Acquisition Products

• Credit Risk

• Grower Services relationship management

• Grower Services "Almanac" Policies

Grain technology risk profile

Operation Risk Control / Risk Mitigator

Agrifood Technology

•Testing result inaccuracies

•Business Risk

•OH&S Risk

• ISO accreditation

• Insurance

• Governmental Regulation

AWB Seeds •Business Risk• Commercial protocol maintenance

R&D

•Unrewarding research

•Intellectual Property risk

•Non commercial development

•Customer services

• Investment and mgt of skills

• Identifying opportunities

Quality Assurance & Hygiene

•Grain value reduction and quality

•GMO Risk

•Customer service risk

• Receival standards

• Care custody and Control Standards

• Governmental Regulation

• AWB GMO Policy

Supply chain & other investments risk profile

Operation Risk Control / Risk Mitigator

Chartering • Pool Receival Tonnes

• Chartering Price risk

• National Pool service

• FX and Chartering Price Risk Limits

• Insurance

Domestic Investments (Grain Centres)

• Tonnes Handled/Received

• OH&S Risk

• Operational Risk

• Business/Grower relationship management

• O,H&S Risk management strategy

• Insurance

Offshore Investments

•Country/Political Risk

•Market Risk

•Business Risk

• Active Board Management and Oversight

• Risk limits and policies

Pool Management Services

AWB National Pool

AWB Pool Management Services

International Sales & Marketing

Managing the Wheat Supply Chain

Risk Management Services

Research & Development

Grower Services

AWB Limited manages AWB National Pool to maximise net pool returns to growers and provide Pool Management Services

AWB National Pool

National Pool

AWB Limited

Customers Growers

Receival & BulkHandling Freight Port

Maintains “paddock to

plate”

Integrated value chain

Increases competition &

drives cost savings

Managing to achieve AWB(I)’s Mandate

Management behaviour consistent with mandate:

• Maximise Pool Returns within defined risk parameters

• Performance Monitoring Models drives behaviour

• Performance Monitoring Models consistent with mandate

• Remuneration also drives behaviour

• Remuneration therefore consistent with mandate and

performance assessment of achieving mandate

Management of “paddock to plate” marketing

• National Pool generates value for growers through managing the value chain from farm-gate to end user

• “Line of sight” is maintained between customer and grower to ensure customers get the product they want and growers are rewarded for providing the product

• National Pool shapes the quality profile of the crop by:

• Setting receival standards

• Developing binning and segregation strategies

• Operating payment programs like Golden Rewards

• National Pool meets customers’ growing requirements through sophisticated site selection of cargoes based on specific quality attributes of the grain from a region or even receival point.

• Uses its customer relationships, its marketing ability and its confidence to back up the quality of the product to extract premiums and maintain and enhance market share

• In an effort to achieve cost reductions, the National Pool is becoming involved in tactical management of the supply chain

• Strategic management of grain flows

• Direct negotiation with service providers

• Coordinating interface between storage and handling, freight and port services

• Tactical management is increasingly allowing the National Pool to manage logistics and select most efficient distribution channels for specific parcels of grain

• National Pool returns all value generated back to growers in full – efficiency gains, blending and swap revenues

Integrated management of the value chain

Driving competition in the supply chain• National Pool involvement at the tactical level critical to it carrying out its

marketing program today and into the future.

• New players prepared to invest in new assets eg. AWB, ABA, movement across borders

• Incumbents investing in up grades and new sites to maintain their market position

• Similar reductions have been seen where competition has been introduced in rail freight services

• In NSW, have witnessed savings of between 8.3% and 17.5% depending on the level of competition on freight routes

• These are real savings being passed on to growers in the form of lower costs

• A more efficient industry will benefit all participants

• The benchmark aims to represent average USD price achieved for a passively managed portfolio of Australian Wheat (of known grade mix and volume) sold into global markets (of known global demand)

• It has three core elements:

- an expected price for Australian wheat based on the market prices of world traded wheat grades that can be related to Australian wheat prices

- a sell-down (allocation to market) profile which takes account of capacity and demand constraints

- a return from wheat price hedging in accordance with the Hedging Policy

USD Wheat Price Sub-benchmark

FX Sub-Benchmark:

• The FX benchmark aims to represent the currency outcome a passive manager could expect to achieve given the AWB(I) FX mandate and a passively managed $US wheat price exposure

Supply Chain Sub-Benchmark:

• The Supply Chain benchmark, unlike export wheat and FX, there is no ‘market’ in supply chain services. AWB is the price maker.

• The benchmark index aims to reflect the expected/passive outcome for supply chain costs,

• It adjusts for cost changes outside the control of the pool manager, such as those caused by different harvest sizes.

• It has three main components, Freight Costs, Bulk Handling costs & Port Costs

FX (AUD/USD) and Supply Chain Sub-benchmarks

Grain Acquisition & Trading

AWB Geneva office established

Business activities

• Australian wheat sales

• Non Australian wheat and feed-grain sales

• Freight

• Structured finance products/services

• Risk management products/services

Investment structure

• 100% AWBL ownership

• US$20m capital investment via AWBL

Tonnes traded 1.5mt in 2003

Management

• Skill and capability of core team is strong

• Office of 12

Supply Chain & Other Investments

Supply chain history in Australia

• Established more than 60 years ago yet remains remarkably unchanged

• Minor cost savings, competition and efficiency gains achieved in this time

• Competition in the supply chain has historically been limited – only small number of new entrants

• Incumbents still enjoy monopoly or near monopoly positions in their markets

• Incumbents enjoy high profit margins on storage and handling business – up to 50%

• BHC’s charge uniform prices across storage facilities leads to inefficient use of infrastructure

Supply chain costs demand attention

Export Customer

On-Farm Storage & Transport

$250m

Domestic Customer

Feed Wheat $40m

Milling Wheat $100m

Total supply chain

costs = $1.4

billion

Land-Based$750m

Sea-Freight$260m

Note: based on wheat production of 24 million

APW Pool Return

$189

$0

$50

$100

$150

$200

$250

NSW

port costs

rail freight

storage and handling

grower return

$50.45 supply chain cost

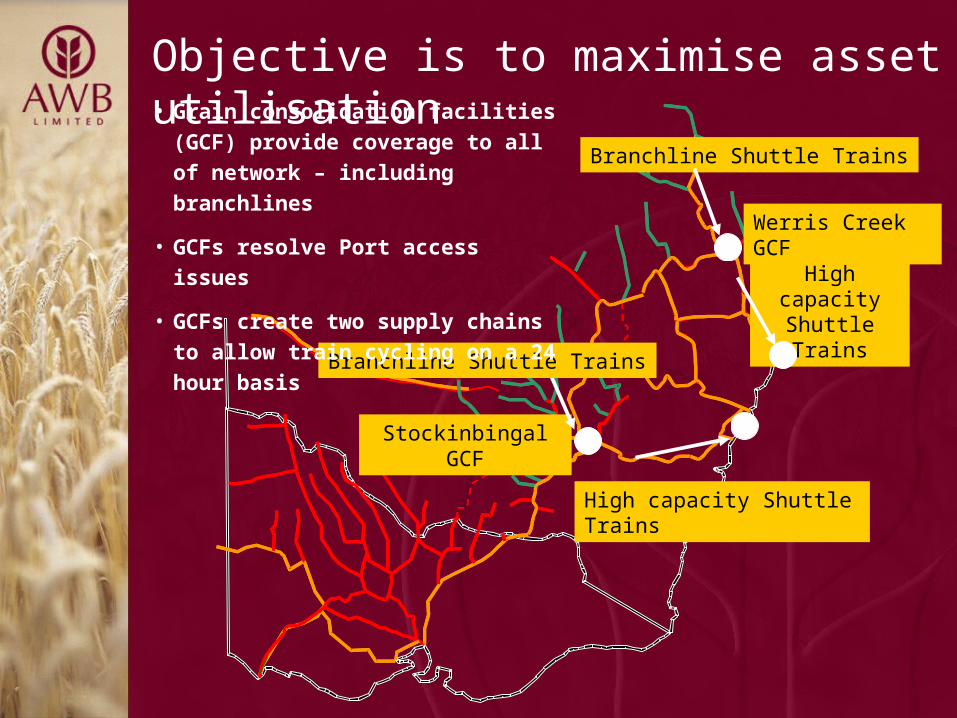

High capacity Shuttle Trains

Werris Creek GCF

Stockinbingal GCF

Branchline Shuttle Trains

Branchline Shuttle Trains

High capacity Shuttle Trains

Objective is to maximise asset utilisation• Grain consolidation facilities (GCF)

provide coverage to all of network –

including branchlines

• GCFs resolve Port access issues

• GCFs create two supply chains to

allow train cycling on a 24 hour basis

Typical efficiency drivers for grain train transport

Characteristics Efficient Operators Traditional

Silo load rate 1,000 t/hr 200 t/hr

Sliding length 42 wagons 15 wagons

Operating hours 24hrs / 7 days 8 hrs / 5 days

Track 23t axle loads15t – 19t axle

loads

Track speed 80km/hr 30km/hr

Wagon capacity 67t – 72t <50t

*AWB grain centre sites designed for optimal interface with rail transport providers

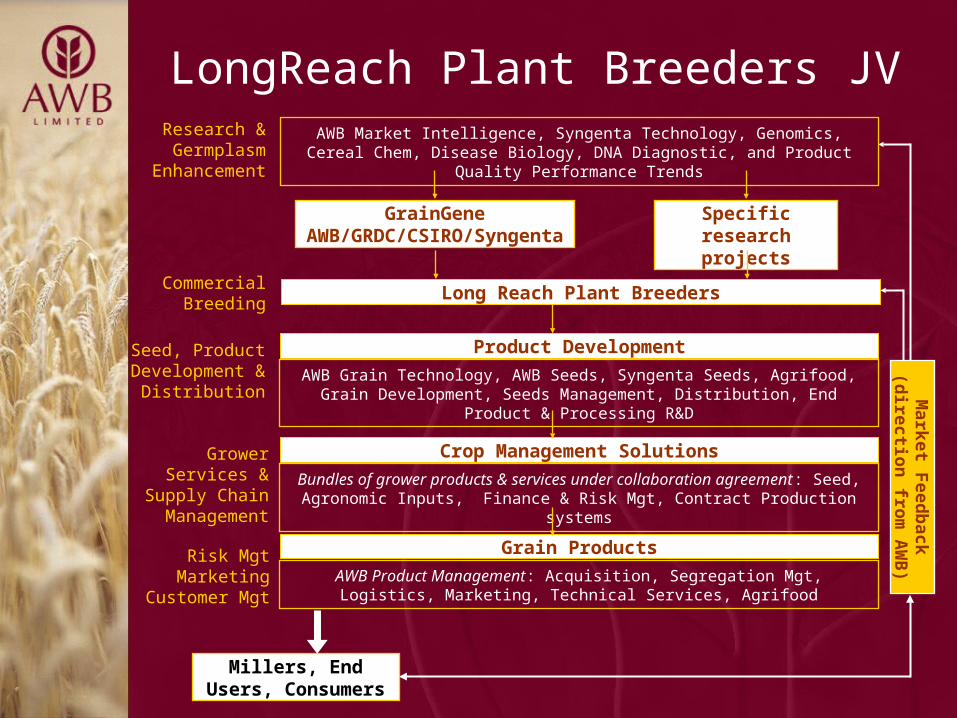

Grain Technology

LongReach Plant Breeders JVResearch & Germplasm

Enhancement

Commercial Breeding

Seed, Product Development &

Distribution

Grower Services & Supply Chain

Management

Risk Mgt Marketing

Customer Mgt

Specific research projects

Bundles of grower products & services under collaboration agreement: Seed, Agronomic Inputs, Finance & Risk Mgt, Contract Production systems

Crop Management Solutions

Millers, End Users, Consumers

AWB Product Management: Acquisition, Segregation Mgt, Logistics, Marketing, Technical Services, Agrifood

Grain Products

AWB Grain Technology, AWB Seeds, Syngenta Seeds, Agrifood, Grain Development, Seeds Management, Distribution, End Product & Processing R&D

Product Development

Long Reach Plant Breeders

AWB Market Intelligence, Syngenta Technology, Genomics, Cereal Chem, Disease Biology, DNA Diagnostic, and Product Quality Performance Trends

Market F

eedb

ack (d

irection

from

AW

B)

GrainGene AWB/GRDC/CSIRO/Syngenta

Measuring efficiency & effectiveness of AWB R&D processes

Product/Market Development View

Discovery Implementation Commercialisation

•No. of successful discoveries

•No. of usable suggestions from the user groups

•Effectiveness of R&D alliances

•Return on development investments

•No. of registered patents

•Success and/or quota of outcomes

•Time-to-market

•No. of marketing partners

•Market shares

•Innovation revenues (revenues of products younger than 2 years)

•Brand value

Key

dri

ver

s in

R&

D/G

rain

Tec

hn

olo

gy

Wheat Statistics

El Niño patterns generally last 12 & 18 months

0

5

10

15

20

25

3019

70-71

1971

-7219

72-73

1973

-7419

74-75

1975

-7619

76-77

1977

-7819

78-79

1979

-8019

80-81

1981

-8219

82-83

1983

-8419

84-85

1985

-8619

86-87

1987

-8819

88-89

1989

-90

1990

-9119

91-92

1992

-9319

93-94

1994

-9519

95-96

1996

-9719

97-98

1998

-9919

99-00

2000

-0120

01-02

2002

-03

0.0

50.0

100.0

150.0

200.0

250.0

300.0

Volume Price

Volume (mt)

Price ($AUD)

El NiñoEl Niño

El Niño El Niño

El Niño

Source: ABARE f = forecast. Note: 5 – 20 yr averages include 2002-03 forecast

Production: 5 yr ave = 21.1 mt 10 yr ave = 19.0 mt 20 yr ave = 17.3 mt

f

Area: 5 yr ave=11.8 m/ha 10 yr ave=10.7 m/ha 20 yr ave=10.4 m/ha

International supply & demand

•2002-03 world consumption

expected to again exceed world

production

•2002-03 carryover stocks

forecast to decline for the fourth

consecutive year

•EU is the only major exporting

country forecast to increase

production for 2002-03.

•Continued competition from

minor exporting countries

despite production forecast to be

slightly less than 2001-02.

500520540560580600620640

2001-02(f) 2002-03(z) 2003-04(z)100

105

110

115

120

125

130

Production

Consumption

Closing stocks

Prod & Cons (mt) Closing Stocks(mt)

Source: USDA June 2002 & ABARE March 2002 (mt) = million tonnes (f) = forecast (z) = Projection

2002-03 Global Prod 597mt, Cons 604mt

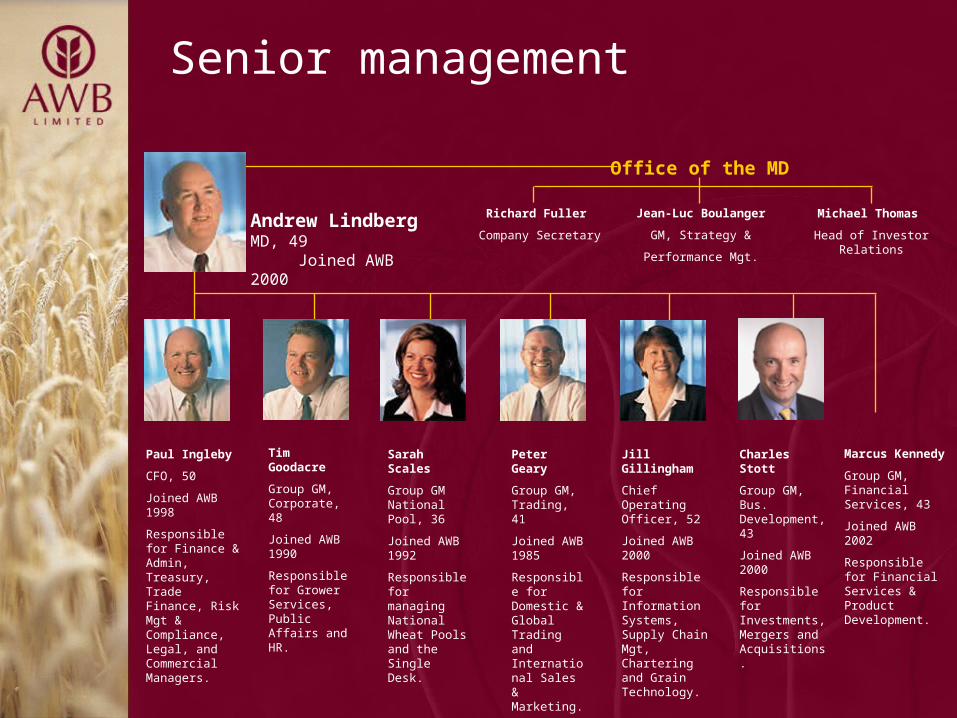

Senior Management

Senior management

Office of the MD

Richard Fuller

Company Secretary

Michael Thomas

Head of Investor Relations

Jean-Luc Boulanger

GM, Strategy &

Performance Mgt.

Paul Ingleby

CFO, 50

Joined AWB 1998

Responsible for Finance & Admin, Treasury, Trade Finance, Risk Mgt & Compliance, Legal, and Commercial Managers.

Tim Goodacre

Group GM, Corporate, 48

Joined AWB 1990

Responsible for Grower Services, Public Affairs and HR.

Sarah Scales

Group GM National Pool, 36

Joined AWB 1992

Responsible for managing National Wheat Pools and the Single Desk.

Peter Geary

Group GM, Trading, 41

Joined AWB 1985

Responsible for Domestic & Global Trading and International Sales & Marketing.

Jill Gillingham

Chief Operating Officer, 52

Joined AWB 2000

Responsible for Information Systems, Supply Chain Mgt, Chartering and Grain Technology.

Andrew Lindberg MD, 49 Joined AWB 2000

Charles Stott

Group GM, Bus. Development, 43

Joined AWB 2000

Responsible for Investments, Mergers and Acquisitions.

Marcus Kennedy

Group GM, Financial Services, 43

Joined AWB 2002

Responsible for Financial Services & Product Development.

For more information contact:

Michael Thomas

Head of Investor Relations

Ph: +61 3 9209 2064

Email: [email protected]