Malaysia The Administration of Selected Export...

68

Report No. 6278-MA Malaysia The Administration of Selected Export Incentives January 12,1987 East Asiaand Pacific Country Programs Department FOR OFFICIALUSE ONLY 7 Documert of the World Bank This document has a restricted distribution and may beused byrecipients onlyin the prformance of theirofficial duties. Its contents may nototherwise be disclosed without World Bank authorization. -3.. .. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Malaysia The Administration of Selected Export...

Report No. 6278-MA

MalaysiaThe Administration of Selected Export IncentivesJanuary 12,1987

East Asia and PacificCountry Programs Department

FOR OFFICIAL USE ONLY

7

Documert of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the prformance of their official duties. Its contents may nototherwisebe disclosed without World Bank authorization.

-3.. ..

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

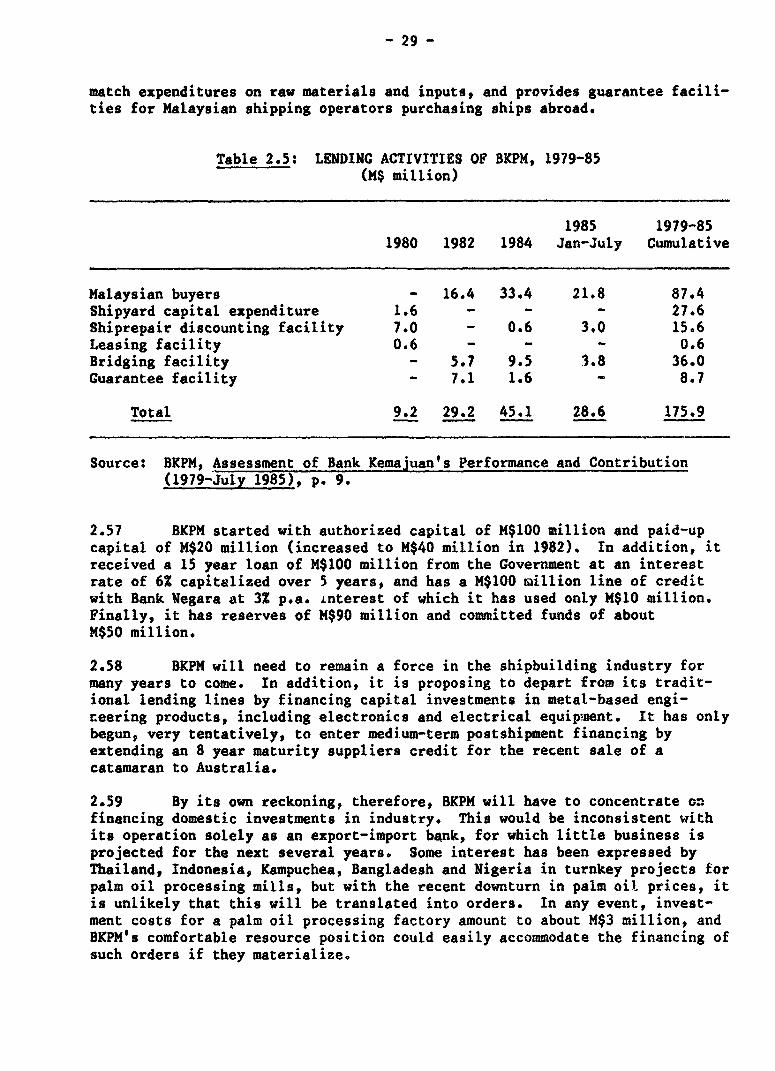

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

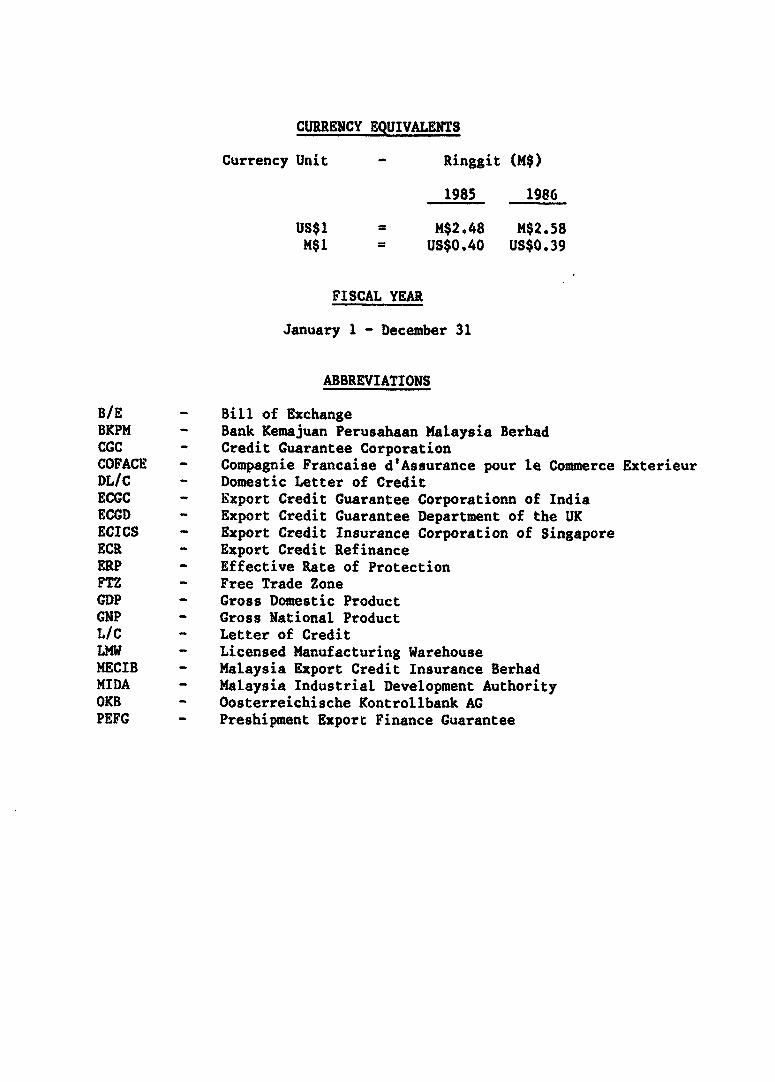

CURRENCY EQUIVALENTS

Currency Unit - Ringgit (M$)

1985 1986

US$ I M$2e48 M$2.58M$1 = US$0.40 US$0.39

FISCAL YEAR

January 1 - December 31

ABBREVIATIONS

B/E - Bill of ExchangeBKPM - Bank Kemajuan Perusahaan Malaysia BerhadCCC - Credit Guarantee CorporationCOFACE - Compagnie Francaise d'Assurance pour le Commerce ExterieurDL/C - Domestic Letter of CreditECGC - Export Credit Guarantee Corporationn of IndiaECGD - Export Credit Guarantee Department of the UKECICS - Export Credit Insurance Corporation of SingaporeECR - Export Credit RefinanceERP - Effective Rate of ProtectionFTZ - Free Trade ZoneGDP - Gross Domestic ProductGNP - Gross National ProductL/C - Letter of CreditLMW - Licensed Manufacturing WarehouseMECIB - Malaysia Export Credit Insurance BerhadMIDA - Malaysia Industrial Development AuthorityOKB - Oosterreichische Kontrollbank AGPEFG - Preshipment Export Finance Guarantee

FOR OMCIAL USE ONLY

MALAYSIA

THE ADMINISTRATION OF SELECTED EXPORT INCRNTIVES

Table of Contents

Page No.

SUMMARY AND RECOMMENDATIONS ... i..................... viii - vi

I* AN VRIW...... 1

A. Setting the Cont e x t 1

B. The Role of Export Incentives in Industrial andTrade Strategy... 3

C. Issues in the Administration of Selected Export6

The Export Credit Refinancing S chmeem e................. 6Import Duty Drawback and Tariff Exemption............... 9

II. PRIORITY TASKS IN POSTSHIPMENT FINANCE ADMINISTRATION......... 10

A. Weaknesses in the Existing Postshipment CreditInsurance Scee11MECIB's Operations are too S m al l 11MECIB's Insurance Coverage is Limited.m i t ed*** ,... 13Exporters and l3ankers do not Regard MECIB Highly........ 14

B. Measures to Improve the Postshipment CreditInsurance System 15Change the Organizational Structure***,********,,***,*,* 16Strengthen Institutional Links........................ 17Introduce New In6urance Instru ments...............,..... 19Develop MECIB Eprie25

C. Moving to a Market-Based Interest Rate.....o............... 26

D. Issues in Medium- and Long-term Export Financeanc..,.e..... 27

This report is based on the findings of a mission tti#-. v:sited Malaysia inMarch-April 1986. The mission consisted of Vikram Nehru (Mission Leader),Y. W. Rhee and Robert Martin (Consultant). The missiua benefitted greatlyfrom generous assistance provided by the staff of Bank Negara and MECIB.

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

III. PMIORITY TASKS IN PRESHIPtENT FINANCE ADKISTRATIONI .......... .31

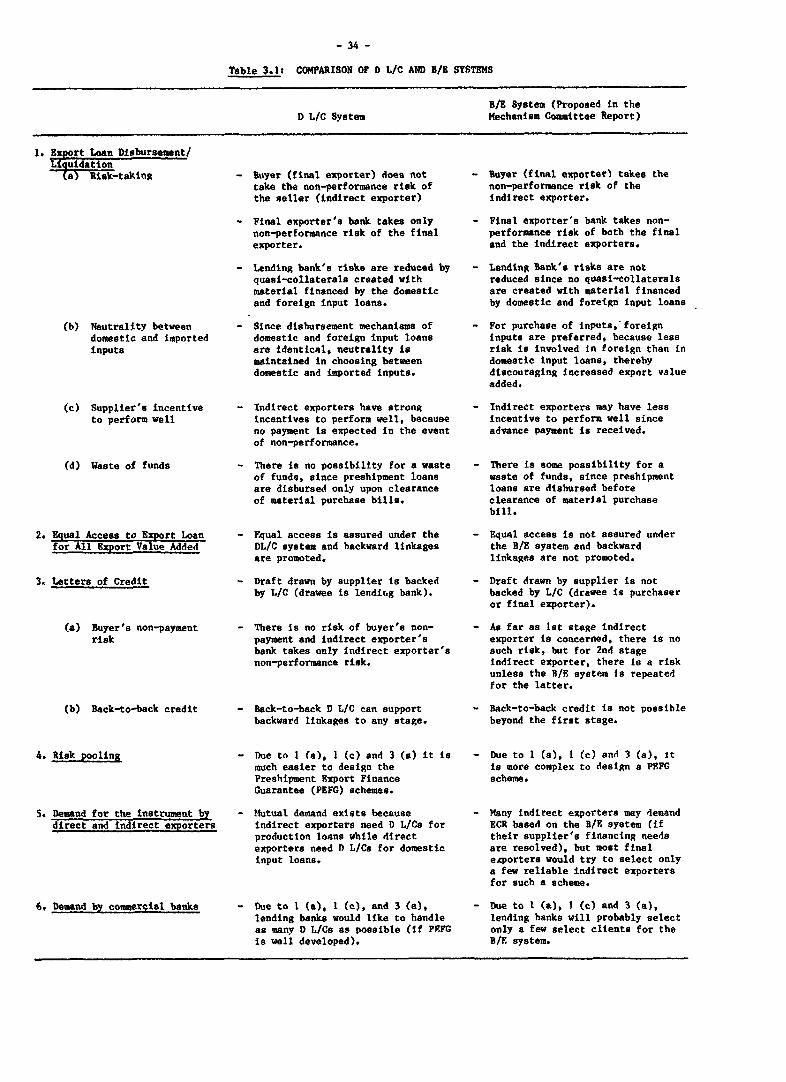

A. Administrative Mechanisms for Preshipmnt Finace.......... .31Disbursement and Liquidation Mechanisms.................. 32On the Choice Between the B/E and DL/C Systems.......... 33The Certificate of Performance Systemo.................... ?

B. Introducing a Preshipmeit Export FinanceGuarantee (PEFG) ............................. .. **** 37Which Institution Should Handle PEFG?................... 38Some Features of a PEFG System.......................... 38Elements of an Action Program........................... 39

C. Other Issues in Preshipment FinanceAdministration ............... o.o...........o.o...e....o. 41

Domestic Value Added and Local Content Requirements..... 41Number of Production Stages with Access to ECRB.......... 41Definition of Confirmed Export Ordero................... 41Maximum Loan Periods for Preshipent CCR................ 42Interest Rate Spread for Preshipment ECRo............... 42

IV. THE ADMINISTRATION OF DUTY-FREE IMPORT SCHEMSo................ 43

A. Import Licensing for Exporters.o......................o.... 43

Bo The Duty Drawback Scheme . ........................ 44

CS The Prior Exemption S c h e m e 45

D. Some Recommendations for Reformf......orm....o..o.....e.... 46

TABLES IN THE TEXT

Table 1.1 Selected Macroeconomic Indicators.....o..oooeo....o....oo. 2Table 1.2 Projections of Growth Rates for Merchandise Exports

by Major Categories, 1986-90............................ 3Table 1.3 Interest Rates and Discount Rates Under the ECR Scheme.... 6Table 2.1 MECIBs Number of Policyholders and Value of

Exports Insured...............o..............o. .***00 OOo. 12

Table 2.2 MECIB: Financial Results, 1978-85.......................o 12Tabie 2.3 Some Potential Markets for Malaysian Exports with Little

or no Cover Provided by MECIB..oo.................o..... 13Table 2.4 MECIB: Suggestions on Premium Rates and Percentage of

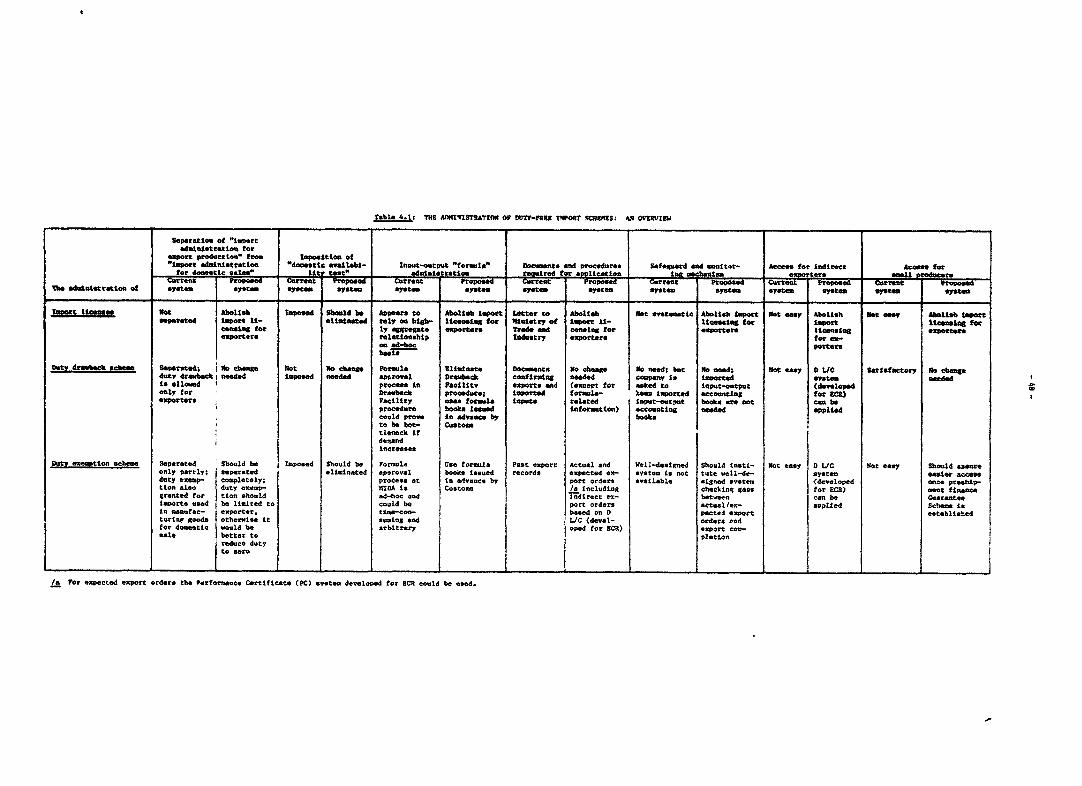

Cover for Bankers' Insurance Policiesoicies..o.o.o..o.o. 22Table 2.5 Lending Activities of BKPM, 1979-85.7 9 - 8S................. 29Table 3.1 Comp&rison of DL/C and B/E Systems.o..ooo......o...... 34Table 4.1 The Administration of Duty-Free tI:art Schemes:

An ........................................... 48

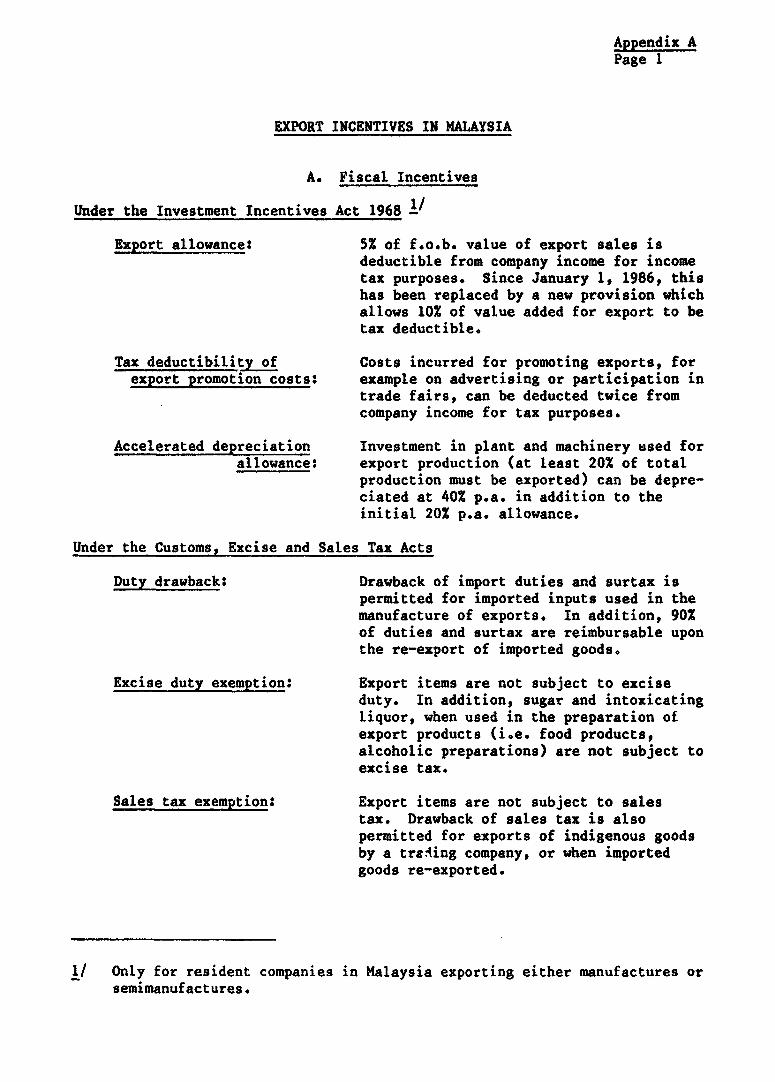

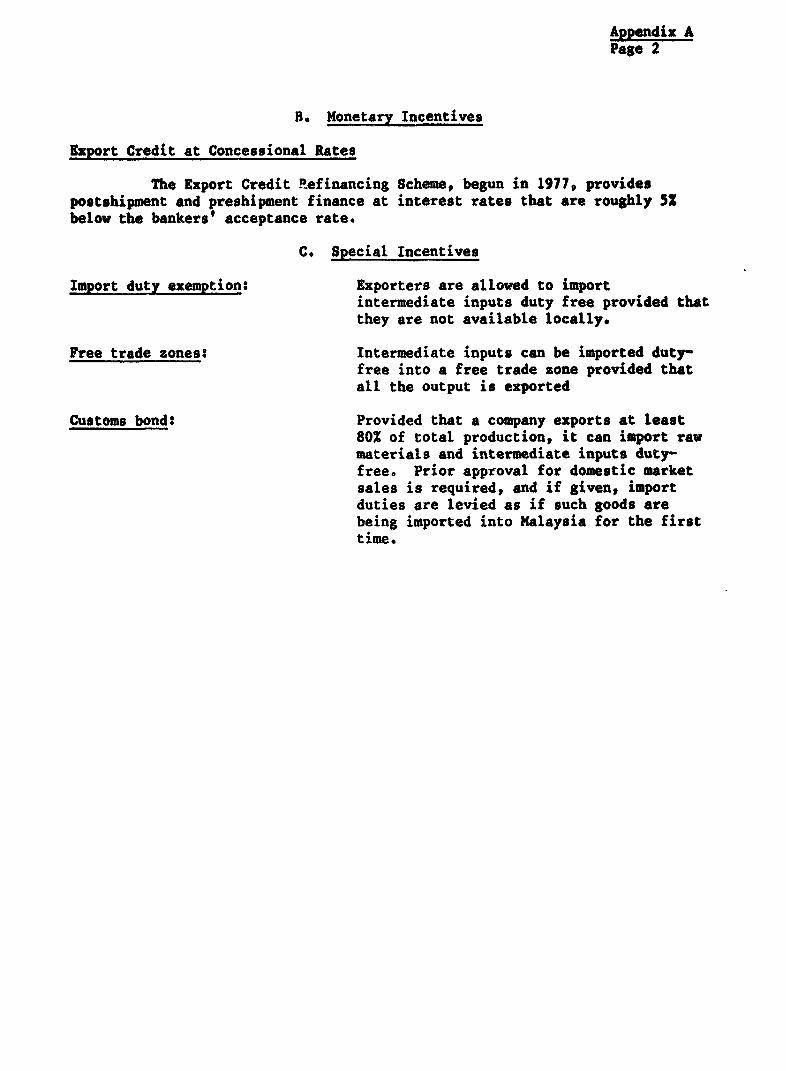

APPENDICES

A. Export Incentives in MalaysiaB. The Establishment and Structure of MECIBC. Further Thoughts on the Organization of MECIB

- iii -

SUMMARY AND RECOMMENDATIONS

i. Malaysia's future performance in exporting manufactures will provecritical in developing a strong manufacturing sector, providing employmentopportuniti8es and earning sufficient foreign exchange to maintain an externalbalance consistent with healthy growth. The rapid expansion of manufacturedexports in the past depended heavily on foreign investment in free trade zones(FTZs) and licensed manufacturing warehouse (LMIs) which have developed onlylimited backward linkages with the rest of the economy. Outside FTZs andLMW., the pro4'iction of exportables is encouraged less than the production ofimport substitutes. Tariff and nontariff barriers make it more attractive tosell in the domestic market than abroad. Furthermore, the internationalcompetitiveness of exports tends to suffer to the extent that direct andindirect exporters do not have quick and easy access to preshipment andpostahipuent export finance and duty free imports of intermediate and rawmaterial inputs. Provision of these facilities constitutes a critic2l firststep in reducing the antiexport bias in the incentive structure. As impor-tant, it supports backward linvages and contributes towards strengthening anddeepening Malaysian manufacturing industry. This report, prepared at thebehest of the Malaysian Government, reviews recent proposals to improveMalaysia's pre- and postshipment export finance administration. It also makessome preliminary observations on existing administrative mechanisms throughwhich exporters can import inputs duty free.

Issues in Pre- and Postshipment Finance Administration

ii. Pre- and postshipment export finance is available to Malaysianexporters at preferential interest rates through the Export Credit Refinancing(ICR) scheme. An ECR Task Force proposed that the Government reform thescheme in two phases. Phase I, already implemented by the Covernmenc inJanuary 1986, liberalizes the criteria for product eligibility and the maximumand administrative limits to outstanding export credits to a single exporter(see the Summary Table). Under Phase II, to be introduced in October 1986,the ECR Task Force proposes to: (a) improve upon the existing postshipmentcredit insurance scheme to support the postshipment finance mechanism; and (b)overhaul the preshipment ECR system with the objective of assuring quick andequal access to all firms that generate export value added.

Postshipment Finance Administration

iii. The most important issue with regard to postshipment finance admin-istration is the need to make the postshipment credit insurance system moreeffective. Malaysia Export Credit Insurance Berhad (MECIB) is the onlyorganization in Malaysia that provides postshipment export credit insurance,yets its operations are too small in relation to the value of manufacturesexported by Malaysia; it either does not provide coverage, or provides onlylimited coverage, for several countries that are usually covered by othercredit insurers abroad; and it is not considered "gilt-edged" by the exportingand banking community as credit insurers are in other parts of the world.Most of these weaknesses can be traced to one very important shortcoming inMECIB's organizational structure -- it does not enjoy full government backing.

- iv -

In this respect it is unlike any other credit insurer in the world, with theexceptioni of the Export Credit Insurance Corporation of Singapore. Theminimum portfolio size necessary to achieve an appropriate diversification ofrisk is usually so large in relation to the equity base of a credit insurer asto discourage most private sector organizations from entering the field. Theabsence of the Government as the guarantor of last resort in Malaysia leads totwo implications. First, MECIB cannot fulfill its export promotional rolebecause its limited capital base forces it to be very conservative whencovering buyer and transfer risks. Second, exporters and bankers are notsufficiently convinced of MECIB's financial ability to absorb large risks:this apprehension is reinforced each time MECIB declines to offer cover ongrounds that the Xransaction is too large or the country is off-cover.

iv. The report, therefore, recommends that MECIB should underwrite allrisks, commercial and political, in the name and on behalf of the MalaysianGovernment. An appealing feature of this recommendation is that it neitherinterferes with MECIB's existing company structure nor discards MECIB's exper-tise built painstakingly over the years. The role of the Government as theguarantor of last resort should not preclude MECIB from operating on commer-cial principles and setting premium rates high enough to cover claims and addto the claim reserve fund over a period of several years. A GuardianAuthority could represent the Government, and set broad policies through anExport Credit Insurance Council composeJ of representatives from relevantministries and Banh: Negara. It could de1egate underwriting authority foramounts above certain limits co a committee comprising government officialsand bankers. In addition, greater use of the assianment mechanism, wherebyMECIB assigns the proceeds of successful claims to the handling bank ratherthan the exporter, could strengthen institutional links significantly. At thesame time, Bank Negara may need to use its persuasive powers to encouragecommercial banks to ease the collateral terms of postshipment lending if MECIBprovides security against buyer default through the assignment mechanism.MECIB could also reinforce its links with commercial banks by offeringbanker's insurance policies that provide indemnity on their recourse toexporters and, if needed, offer unconditional guarantees to banks for buyers'bills purchased from exporters. Finally, MECIB will need to train staff indesigning and implementing these new insurance mechanisms.

v. The report also discusses two other aspects of postshipment finance.First, it suggests that rediscount facilities at preferential rates ofinterest and the low intermediation margin enjoyed by banks under the ECRcould inhibit the growth of the scheme. Instead, the Government may zonsiderallowing greater play by market forces in determining the interest rate struc-ture of postshipment export finance. Second, the report comments on theadvisability of setting up an export-import bank in Malaysia. It concludesthat the scale of capital goods exports from Malaysia does not justify this,but Bank Kemajuan can meet the demand for medium-term postshipment finance ifneed be, and MECIB could further support this effort by providing exportcredit insurance.

Preshipment Finance Administration

vi. Proposals in Phase II center on two critical areas: (a) the intro-duction of new administrative arrangements for preshipment export finance thatwill improve the disbursement mechanism and allow direct access to indirectexporters; and (b) the establishment of a new preshipment export finance gua-rantee (PEFG) scheme to overcome the collateral-based behavior of commercialbanks by covering potential nonperformance risks of exporters.

vii. New Administrative Arrangements. The new administrative arrange-ments for preshipment export finance proposed by the ECR Task Force includethree important innovations: (i) disaggregating preshipment export loans intofour categories to cover value added, and the purchase of imported inputs,domestic inputs and final output, and specifying a disbursement mechanism foreach; (ii) offering a choice between the bill of exchange (B/E) and thedomestic letter of credit (DL/C) as two alternative instruments foradministering access by indirect exporters to preshipment loans under the ECR;and (iii) allowing preshipment loans under the ECR in parallel on an expectedorder basis using export performance certificates.

viii. The report notes that any effective preshipment finance administra-tive mechanism must have two features without which the entire objective ofthe scheme could be jeopardized. First, at all stages of production, loandisbursements must be tied to the clearance of the material purchase bill andloan liquidation to the clearance of the products sales bill. These tie-upsare critical if a preshipment export finance guarantee scheme is to be intro-duced; they also prevent abuse of the scheme, conserve the financial resourcesof commercial banks and simplify administration. Second, indirect exportersat all stages who contribute to value added for export must have equal accessto preshipment loans under the ECR. This feature is especially helpful inpromoting backward linkages and exploiting the country's full export poten-tial. The report notes that the B/E system does not passess these two criti-cal features, whereas the DL/C system does and therefore recommends that theTask Force consider redesigning the B/E system to include them before offeringit as an alternative to the DL/C system. The report also suggests that theTask Force take into account the administrative requirements of other exportincentives (e.g., duty-free imports or the income tax abatement scheme -- seebelow) before coming to any firm conclusions on the relative merits of the B/Eand the DL/C system as administrative mechanism for preshipment exportlending.

ix. Preshipment Export Finance Guarantee. The second important Phase IIproposal is to set up a preshipment export finance guarantee (PEFG) schemethat will encourage commercial banks to lend preshipment funds to small andinfant exporters. MECIB appears to be the most suitable agency to initiatesuch a scheme, though it will need to keep the administration of the PEFGscheme separate from its other activities related to conventional creditinsurance. Its short-term tasks will include: (i) designing PEFG policiesbased on the new ECR; (ii) conducting a survey of direct and indirect expor-ters; and (iii) organizing overseas study and training programs. In themedium-terms it will need actively to reduce nonperformance risks associatedwith its client firms by providing technical assistance and other development

- vi -

services. This is a new area for MECIB, and it will need to display abundantcaution and considerable patience. Ultimately, it should aim to become both amature credit guarantee institution and a dynamic development agency that canplay a catalytic role in implementing Malaysia's new outward-orienteddevelopment strategy.

x. The report also makes other suggestions that may assist in clari-fying or rationalizing several Phase II proposals and thus make them morecoasistent with the objectives of the ECR reform. These are mentioned in theSummary Table.

The Administration of Duty-Free Import Schemes

xi. Malaysia has four separate schemes that permit duty-free imports forexport production, but this report focuses on only two of them - the priorexemption and the duty drawback schemes. These two schemes tend to sufferfrom two imporrant shortcomings: first, obtaining access to them oftenresults in delays and requires considerable effort on the part of exporters;and second, in practice these schemes are available only to final exporters.The inability of direct and indirect exporters to gain eay and quick accessto duty-free imports affects competitiveness and inhibits the formation ofbackward linkages arising frome. export production. In addition, the "domesticavailability test" under the prior exemption scheme (or to obtain an importlicense for products subject to quantitative restrictions) complicates theprocess of obtaining duty free imports. Finally, the monitoring mechanismunder the two schemes appears to be slack and probably does not act as adeterrent for abuse of the system.

xii. The report suggests that the DL/C mechanism can be used as theappropriate vehicle to administer and monitor the prior exemption and dutyfree import schemes for indirect exporters. Those who abuse the system shouldbe prosecuted and prohibited from access to ICR facilities. In addition,other key tasks for reforming the administration of duty-free import schemeswould include: (a) pretabulating input-output coefficients in a book whichwould then become applicable to all exporters; (b) eliminating the "4zomesticavailability test;" (c) abolishing the import licensing requirement; and(d) considering use of the proposed DL/C system to improve the administrationof a range of other export incentives for indirect exporters.

A Postscript

xiii. Since this study was completed in June of 1986, Bank Negara launched thepilot test of the phase II revisions of the ICR scheme on October 15, 1986.Many of the recomendations made in this study were adopted for the pilottest, including the use of the domestic letter of credit (DL/C) for conven-tional preshipment finance and the use of the certificate of performancesystem for preshipment finance based on expected orders.

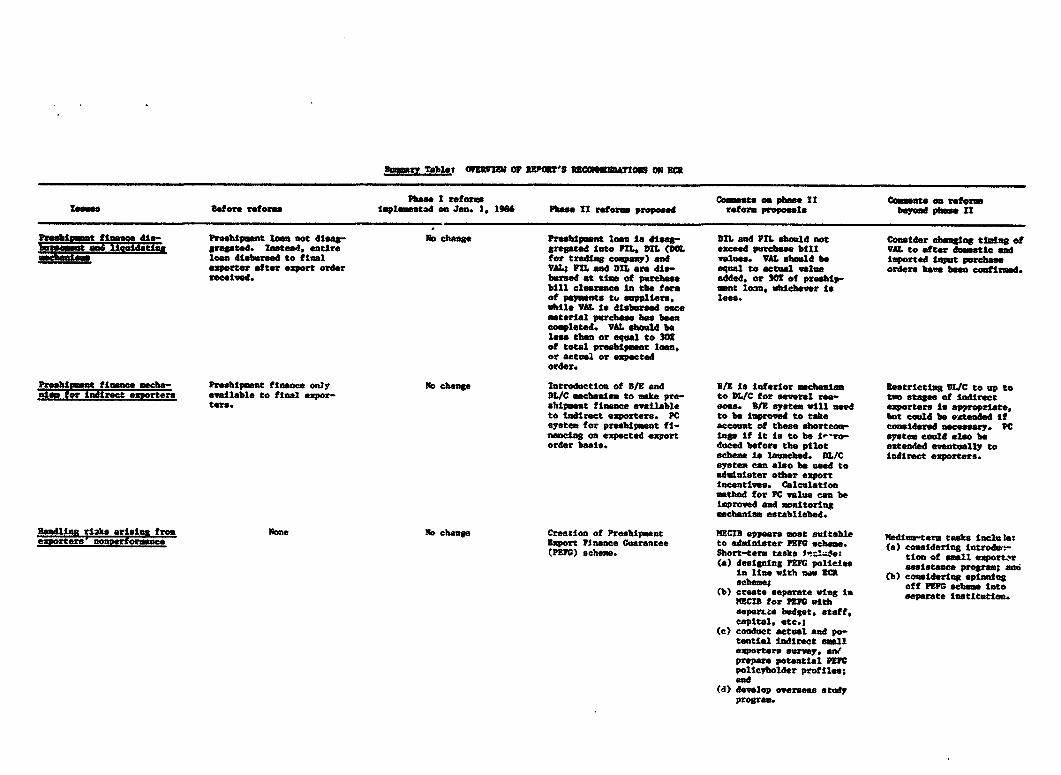

_mry Tables OWIE3 OIP RZFPWRS RZCWNDSAT1IONS ON XCI

Phas I refogma Coents oa pbhJe II Cooate on retornSam" _t fore refor_ impl m_tad on Jan. 1, 1986 Phse I reforms proposed reform propoSal beyond pba It

Preebi_ t finance dli- Preehipuant loon cot disag- RD change Presbipent loon io dis- DIL and P 1 should not Consider changing tutung of_ at *nd lieid tift Sregotod. Instead. entire gregatd Into iZL. DMI (DOL exceed purchsee bill VAL to ofter do_etic end

_A___S__ loan didbursed to final for tredlng company) nd values. VAL shcold be Iported input purebaeexporter ofter export order VAL; M1 and DIL ore die- equml to aetud value orders baov been eoufirmad.recev1d. bursed at tima of pureba added, or 302 of presbip-

bill clearance In the form must loan, whichever isof peyments tu suppliers, le"s.while VAL Is disbursed oncematerial purcebse bas beencompleted. VAL should beles tban or equal to 305of total preebipa_t lo"n.or actual or expectedorder.

Preebiument finance macba- Preebipm_nt finance only No c¢a_ Introduction of B/S and Btt is Inferior mcbanIsm Restriettag DIJC to up toa"a for fidirect exporters available to final exWor- DL/C mechanis to make pre- to DL.C for several rea- two stages o indirect

ter. shpment finance available eon. B/t systea will need exportrs is apPropriste,to indirect exportere. PC to be improved to take bht celd be extended Ifsystem for prebipuent fi- account of he"e shortecr- considered uece sery. PCnaniung on expected export tags If It Is to be 1--ro- Sytem could *1 o beorder beais. duced before the pilot extended eventually to

cheme is launched. 1/C indirect exporters.system can alao be used toadminister other exportincenttves. Calculationmethod for PC value can beimproved and monitoringmcehaniam establisbed.

Dandlnag riak arisin from None No ehange Creation of Preah1pment MECrB appears moat suitable Nediu,m-tor tasks mneb o:exporters nonperformance Expert Fiane Guarantee to administer PE scea (a) considering introdai-

(PMP) scheme. Short-term taskts 9,t1.Le tion of smell emport..(a) designang PEFC policies assistance program; s ni

In lime with row WM (b) considering spinningschbne; of f P110 scebma into

(b) create sepsrate wing In separte instituiton.5301 for Me1 withsepartce budget, staff.capital. etc.;

(c) coaduct actual and po-tential Indirect smellexportere surve, oneprepare potential PE10policybolder profiles;and

(d) develop overseas studyprogram.

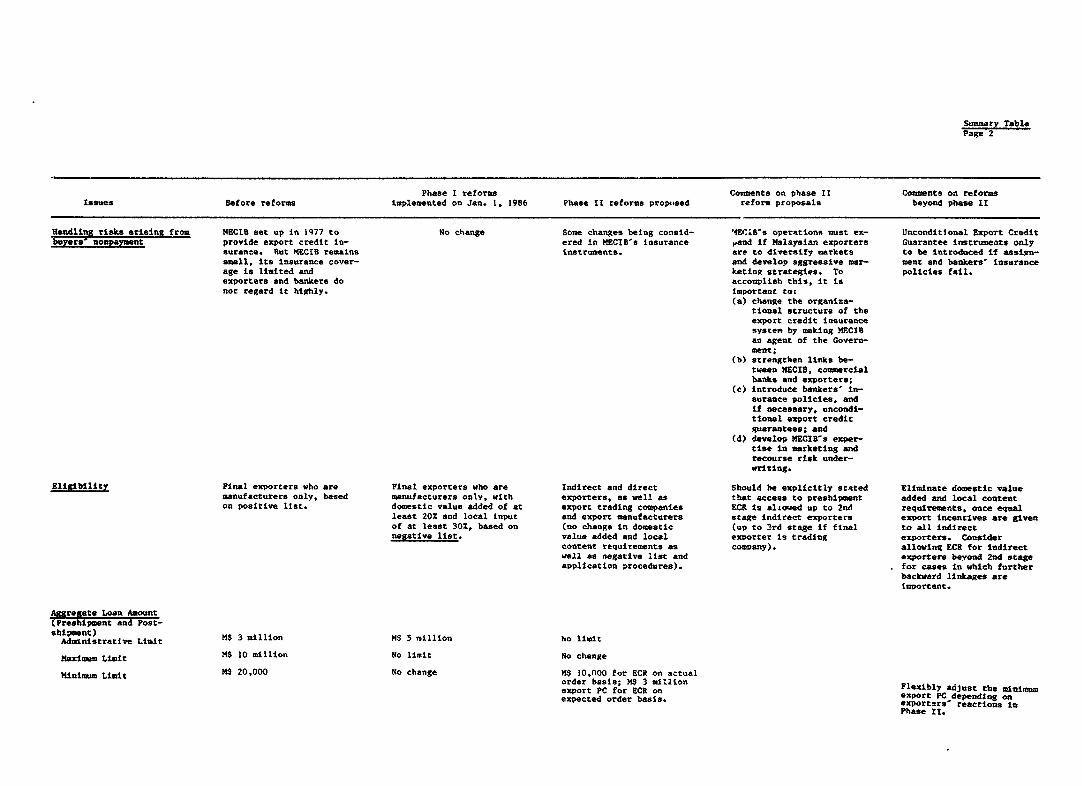

Suary TablePage 2

Phase I reforms Comments on phase 11 Comments on reformsIssues Before reforms implemented on Jan. 1, 1986 Phase II reforms proposed reform proposals beyond phase II

llandling risks arising from NECIS set up in 1977 to No change Some changes being consid- M4ECB's operations must ex- Unconditional Export Creditbuvers nonpayment provide export credit in- ered in MECIB's insurance ,and if Malaysian exporters Guarantee instrumeAts only

surance. Rut MECIS remains instruments. are to diversify markets to be Introduced if assign-small, Its insurance cover- and develop aggressive mar- ment and bankers' insuranceage is limited and keting strategies. To policies fail.exporters and bankers do accomplish this, it isnot regard It highly. important to:

(a) cheane the organiza-tional structure of theexport credit insurancesystem by making MFCIBan agent of the Govern-ment;

(b) strengthen litnks be-tween NECIS, commercialbanks and exporters;

(c) introduce bankers' in-surance policies, andif necessary, uncondi-tional export creditguarantees; and

(d) develop NECI8's exper-tise In marketing andrecourse risk under-writing.

Eligibility Final exporters who are Final exporters who are Indirect and direct Should be explicitly stated Eliminate domestic valuemanufacturers only. based manufacturers only, with exporters, as well as that access to preshipment added and local contenton positive list. domestic value added of at export trading companies ECR is sliowed up to 2nd requirements, once equal

least 20X and local Input and export manufacturers stage indirect exporters export Incentives are givenof at least 30%, based on (no change in domestic (up to 3rd stage if final to all indirectnegative list, value added and local exporter is trading exporters. Consider

content requirements as company). allowing ECR for indirectwell as negative Ilst and exporters beyond 2nd stageapplication procedures), for cases in which further

backward linkages areimportant.

Agregate LanAmountftreahipmen and Post-

shipment) rS 3 million HS 5 million ho limit

Maximum Limit KS 10 million No limit No change

Minimum Limit M$ 20,000 No change MS 10,000 for ECR on actualorder basis; MS 3 million Flexibly adjust the minimexport PC for ECRI on export PC depending onexpected order basis. export2rs' reactions in

Phase It.

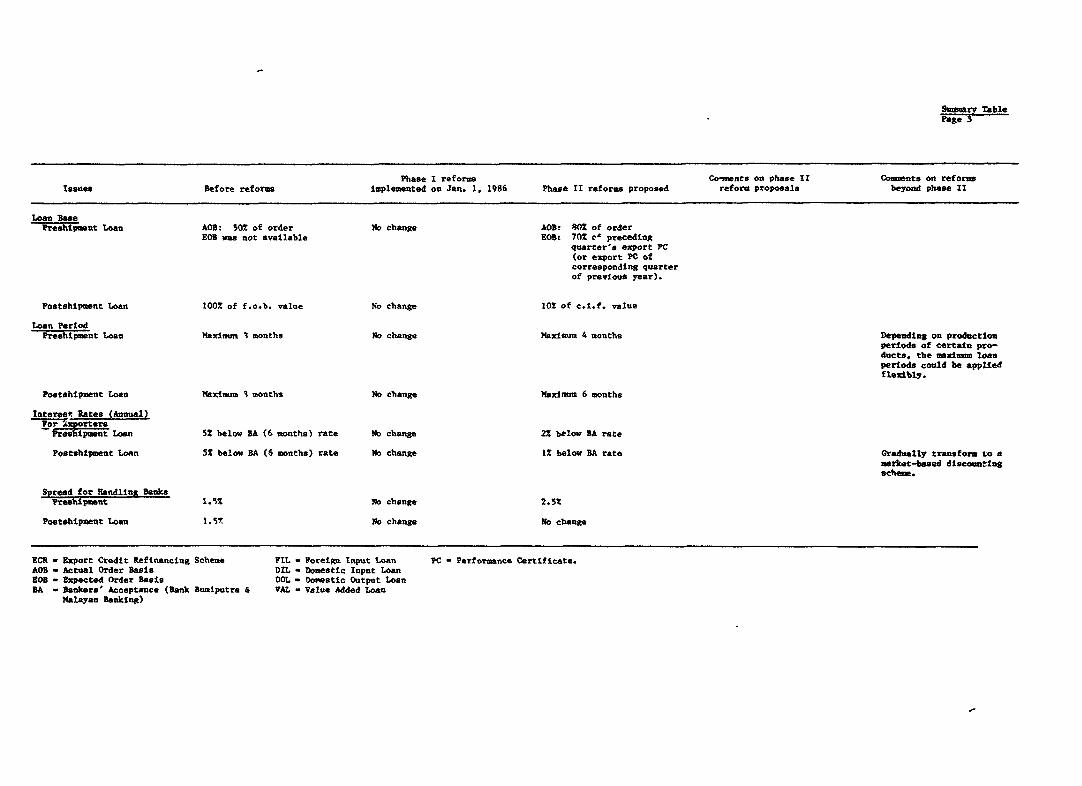

S- Tble

Phase I reforms Co.aencs on phase Ir C0nents on reformsIssues Before reforms implemented on Jan. 1, 1986 Phase II reforms proposed reform proposals beyond phase II

Loan BasePreshipient Loan AOP: 50S of order No change AOB: 80? of order

BOB was not available EOB: 70% c' precedingquarter's export PC(or export PC ofcorresponding quarterof prevIous year).

Postshipment Loan 100% of f.o.b. value No change 102 of c.i.f. value

Loan PeriodPreshtipment Loan. Maximum 1 months Nto change maximum 4 moneths Depending on production

periods of eertain pro-ducts, the maximm loanperiods could be appliedflexibly.

Postehipuent Loan M4aximmI 3 months No change Naximum 6 months

Interest Bates (Annual)Porxporters

Preshipment Loan 5S helow BA (6 months) rate No change 2% below BA rate

Postshipment Loan 5X below BA (6 months) rate No change 1% below BA rate Gradually transform to amrket-based discountingscheme.

Spread for Handlins BanksFreahipment 1.5? No cbange 2.5%

Postehipment Loan 1.521 No change No change

ECR - Export Credit Refinancing Scheme PtL - Foretgn Input Loan PC - Performance Certificate.AOS - Actual Order Basis DIL - Domestic Input LoanEOB - Expected Order Basis DOL - Dopestic Output LoanBA - Bankers' Acceptance (Bank Bumiputra & VAL - Value Added Loan

Malayan Banking)

MALAYSIA

THE ADMINISTRATION OF SELECTED EXPORT INCENTIVES

;. AN OVERVIEW

1.01 The pressure on Malaysia to expand its exports, particularly ofmanufactures, is greater than ever before. The Covernment unveiled recentlyan Industrial Master Plan for 1986-90 which emphasizes an outward-orienteddevelopment strategy. The overall thrust of the plan is to promote exports byencouraging resource-based and other manufacturing industries with extensivebackward linkages. To support this recent shift in emphasis towardsencouraging manufactured exports, the Government is also keen to improve andstrengthen the administration of export incentives. This report, prepared atthe request of the Government, reviews recent proposals to improve uponMalaysia's existing pre- and postshipment export finance administration. Italso makes some preliminary observations on existing administrative mechanismsthrough which exporters can import intermediate inputs and raw materials dutyfree.

1.02 This chapter places the discussion of export finance administrationand duty-free import administration in the context of Malaysia's overallstrategic imperatives. Section A of this chapter, therefore, sets the contestof the report by describing briefl' Malaysia's present economic situation andits strategic options for the future. Section B notes the role of export pro-motion and the administration of export incentives in the context of an over-all trade and industrial development strategy for the medium term. Finally,Section C indicates some important issues in the administration of selectedexport incentives and sets the stage for the discussion in the remainingchapters of this report.

A. Setting the Context

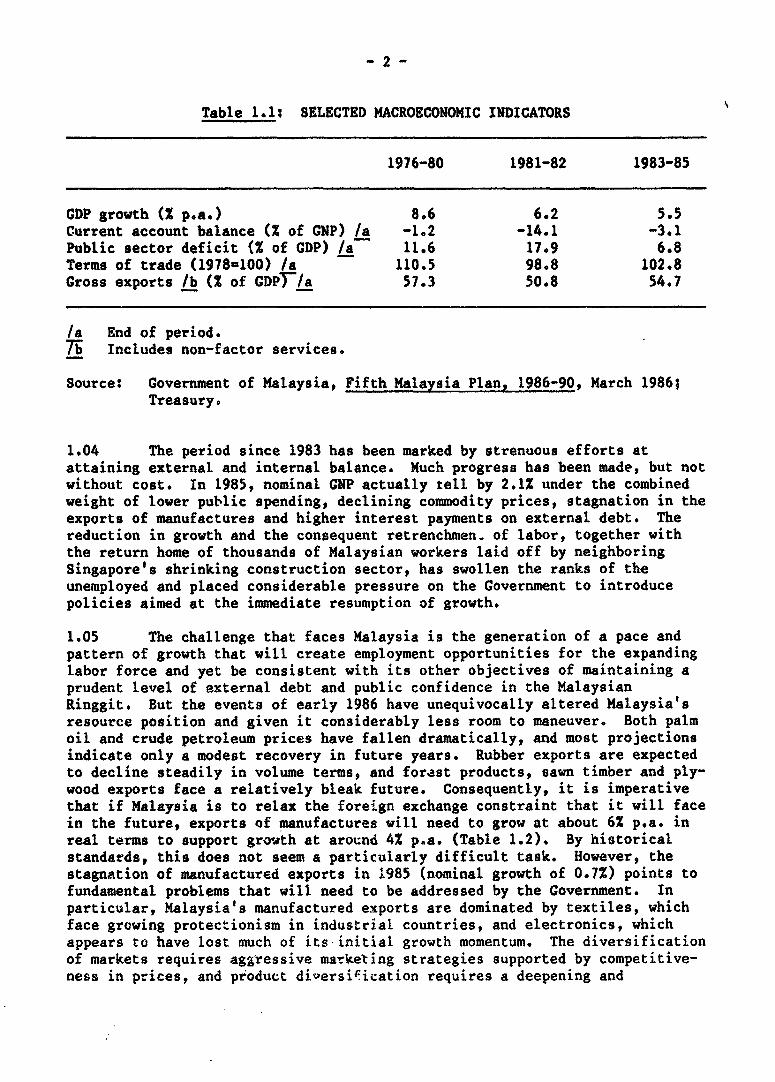

1.03 Malaysia, with its small population, rich natural resources, andstrategic location, is heavily dependent on international trade for itseconomic well-being. Exports account for more than half of total GDP, and lodo imports. The importance of international trade and the attraction of thecountry's relatively free foreign exchange markets to foreign investors have,over the years, proved to be of enormous benefit to the economy. During the1970s, when commodity prices fared well and international trade grew at Ahealthy pace, Malaysia enjoyed a growth rate of over 8X p.a., amongst thehighest in the developing world. By the same token, however, the economy isvery sensitive to downturns in international economic activity and trade. In1981-82 the terms of trade fell by over 10%t, but growth was maintained bycountercyclical fiscal policies which culminated in unsustainably large publicsector and external current account deficits (Table 1.1).

Table 1.1: SELECTED MACROECONOMIC INDICATORS

1976-80 1981-82 1983-85

CDP growth (% p.a.) 8.6 6.2 5.5Current account balance (% of GNP) /a -1.2 -14.1 -3.1Public sector deficit (X of GDP) /a 11.6 17.9 6.8Terms of trade (1978=100) /a 110.5 98.8 102.8Gross exports /b (Z of GDPF/a 57.3 50.8 54.7

/a End of period.Th Includes non-factor services.

Source: Government of Malaysia, Fifth Malaysia Plan, 1986-90, March 1986;Treasury.

1.04 The period since 1983 has been marked by strenuous efforts atattaining external and internal balance. Much progress has been made, but notwithout cost. In 1985, nominal GNP actually tell by 2.1% under the combinedweight of lower public spending, declining commodity prices, stagnation in theexports of manufactures and higher interest payments on external debt. Thereduction in growth and the consequent retrenchmen- of labor, together withthe return home of thousands of Malaysian workers laid off by neighboringSingapore's shrinking construction sector, has swollen the ranks of theunemployed and placed considerable pressure on the Government to introducepolicies aimed at the immediate resumption of growth.

1.05 The challenge that faces Malaysia is the generation of a pace andpattern of growth that will create employment opportunities for the expandinglabor force and yet be consistent with its other objectives of maintaining aprudent level of external debt and public confidence in the MalaysianRinggit. But the events of early 1986 have unequivocally altered Malaysia'sresource position and given it considerably less room to maneuver. Both palmoil and crude petroleum prices have fallen dramatically, and most projectionsindicate only a modest recovery in future years. Rubber exports are expectedto decline steadily in volume terms, and forest products, sawn timber and ply-wood exports face a relatively bleak future. Consequently, it is imperativethat if Malaysia is to relax the foreign exchange constraint that it will facein the future, exports of manufactures will need to grow at about 6% p.a. inreal terms to support growth at around 4% p.a. (Table 1.2). By historicalstandards, this does not seem a particularly difficult task. However, thestagnation of manufactured exports in 1985 (nominal growth of 0.7%) points tofundamental problems that will need to be addressed by the Government. Inparticular, Malaysia's manufactured exports are dominated by textiles, whichface growing protectionism in industrial countries, and electronics, whichappears to have lost much of its initial growth momentum. The diversificationof markets requires ag2ressive martketing strategies supported by competitive-ness in prices, and product diversification requires a deepening and

- 3 -

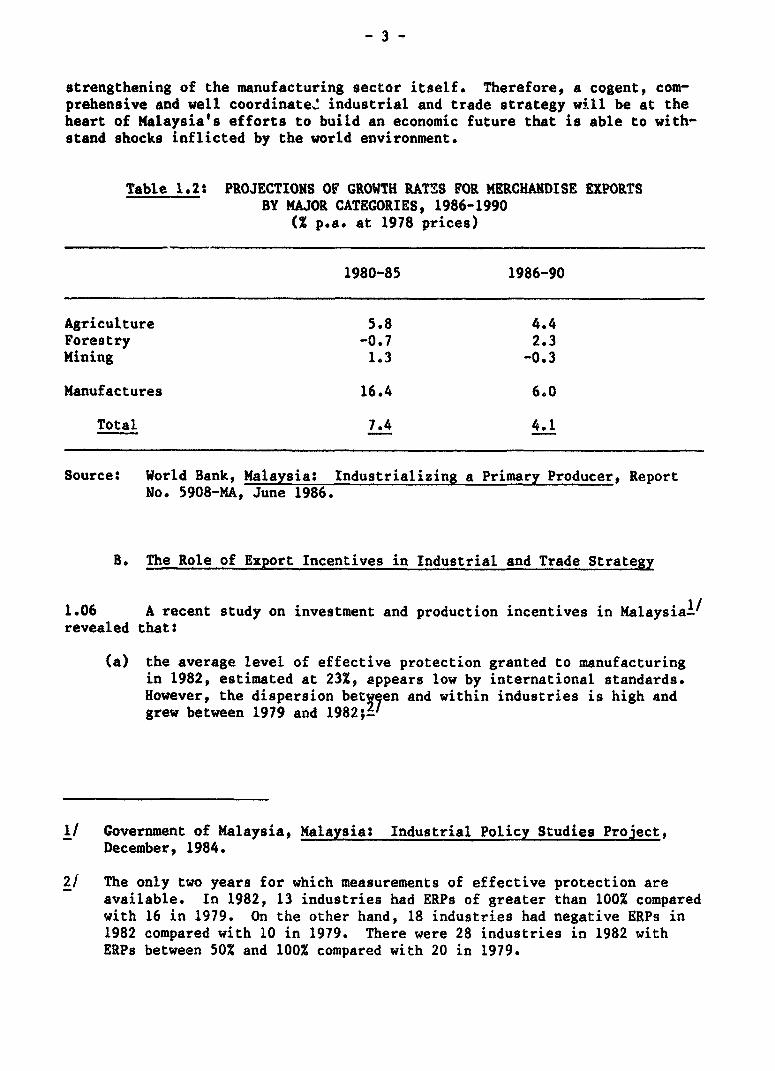

strengthening of the manufacturing sector itself. Therefore, a cogent, com-prehensive and well coordinate' industrial and trade strategy will be at theheart of Malaysia's efforts to build an economic future that is able to with-stand shocks inflicted by the world environment.

Table 1.2: PROJECTIONS OF GROWTH RATES FOR MERCHANDISE EXPORTSBY MAJOR CATEGORIES, 1986-1990

(X p.a. at 1978 prices)

1980-85 1986-90

Agriculture 5.8 4.4Forestry -0.7 2.3Mining 1.3 -0.3

Manufactures 16.4 6.0

Total 7.4 4.1

Source: World Bank, Malaysia: Industrializing a Primary Producer, ReportNo. 5908-MA, June 1986.

B. The Role of Export Incentives in Industrial and Trade Strategy

1.06 A recent study on investment and production incentives in MalaysiaY1revealed that:

(a) the average level of effective protection granted to manufacturingin 1982, estimated at 23%, appears low by international standards.However, the dispersion between and within industries is high andgrew between 1979 and 1982;-V

1/ Government of Malaysia, Malaysia: Industrial Policy Studies Project,December, 1984.

21 The only two years for which measurements of effective protection areavailable. In 1982, 13 industries had ERPs of greater than 100% comparedwith 16 in 1979. On the other hand, 18 industries had negative ERPs in1982 compared with 10 in 1979. There were 28 industries in 1982 withERPs between 50% and 100% compared with 20 in 1979.

(b) in addition, there is a significant antiexport bias in the incentivestructure -- the average ERP for exporting and import-competingactivities in 1982 was 12X and 24%1 respectively;

(c) the structure of protection incentives appears to discriminateagainst small firms and non-FTZ (free trade zone) activities; and

(d) several trade and investment policy incentives combine to produce anadministratively complex, and sometimes inefficient, system.

1.07 The implications of th se incentives have already been analysed in arecent report of the World Bank._ Both tariff and nontariff policy instru-ments are responsiblg,for shaping the present structure of incentives in themanufacturing sector"/. Relatively inefficient and high cost domesticindustries hdve sprung up where protective barriers have been particularlyhigh, such as tires and tubes, automobiles and automotive parts, rubber foot-wear, confectionery, etc. These industries have drawn investment resourcesaway from potentially efficient, export-oriented industries which receivelittle encouragement through the incentive system. The bulk of Malaysia'sexports of manufactures are produced by firms located in its free trade zones(QTZs) or operated as licensed manufacturing warehouses (LMWs) which areunaffected by import barriers. These firms have been able to establish few,if any, backward linkages with the rest of the economy. Outside these freetrade areas, most industries (except for textiles) have geared theirproduction for the domestic market. Exports that do originate from outsidePTZs and LMWs are dominated by a small number of final stage manufactures.Protection from the forces of international competition has been complementedby an industrial licensing system which has tended to blunt the cost-reducingand efficiency-enhancing effects of free entry by domestic entrepreneurs, allof which ultimately affects the export competitiveness of Malaysian productsin the international market.

1.08 As a matter of priority, therefore, the Government will need toreduce the fairly large disincentives to export that affect production andinvestment decisions outside FTZs and LMWs. To achieve this, policies willneed to be introduced that lower trade barriers, increase manufacturingefficiency and reduce the antiexport bias implicit in the incentive system.The Government took a few steps recently in this direction: import duties onraw materials and components were reduced uniformly to 21; 101 of value addedin export production was made tax deductible and the export allowance was

3/ World Bank, Malaysia: Industrializing a Primary Producer, Report No.5908-MA, June 1986.

4/ Nontariff policy instruments include import quotas (prohibitive in thecase of some iron and steel products, automobiles and sugar, andimportant in timber and cement); local content programs in the automobileindustry; price controls on some manufactured items which tend to have aprotection effect; government purchasing guidelines and tax relatedincentives.

abolished; and double deduction for tax purposes was permitted for exportcredit insurance premiums. In addition the Industrial Coordination Act wasliberalized somewhat and a new set of investment promoti measures is to beintroduced soon. But the two reports referred to above - recommend reformsthat go beyond these recent changes. In substance these studies haverecommended replacing quotas with tariffs, eliminating local contentrestrictions, reviewing price controls, reconsidering the "buy Malaysia"policy, increasing the neutrality of tax and tax-related intentives betweendifferent industries, and liberalizing the licensing system beyond the recentchanges in the Industrial Coordinatioa Act.

1.09 The introduction of these policies will alter the present structureof incentives, inevitab'.y reducing the level of implicit subsidies granted tosome existing industries, and increasing it for others. This, in turn, willrequire individual firms to invest in new machinery, initiate new managementpractices, seek new markets, improve production efficiency or alter productmix. To give existing industries sufficient time to adjust to the new policyenvironment, change will have to be introduced gradually and according to apreannounced timetable.

1.10 The first step to lowering the antiexport bias would include givingexporters the opportunity of purchasing their intermediate inputs and rawmaterials at internationally competitive prices and allowing them access *.oexport finance. This could be achieved by providing automatic and duty freeaccess to imported inputs, access to credit for both direct and indirectexporters, and export credit guarantee facilities for pre- and postshipmentloans. Korea's example has shown that these incentives, aimed specifically aCpromoting the generation of export value added, can make a material differenceto a country's overall export performance. Introducing these new incentivesrequires building institutions, creating new systems and changing existingpractices and modes of thinking. It is a time-consuming task, requiringpatience and perseverance. Only by starting immediately will Malaysia havethe requisite administrative infrastructure to support its export efforts inthe 1990s and beyond. There is some evidence to suggest that existing exportincentives reach only between 100-200 manufacturers and contribute to theskewed distribution of exports in manufacturing. On the other hand, of the8,000-odd manufacturing establishments in Malaysia, 95% are small and mediumscale producers who have had only limited access to export incentives and haveconsequently,not had the opportunity to earn foreign exchange, directly orindirectly.- The task ahead is challenging, but as the experience ofsuccessful East Asian countries has demonstrated, small and mediummanufacturers can make important contributions to exports and growth, providedthey have equal access to export incentives.

5/ Government of Malaysia, 1984, op. cit.; World Bank, June 1986, op. cit.

6/ Out of a total of 8,343 manufacturing establishments in 1982, 6,205 weresmall (with less than 50 workers) and 1,688 were medium-sized (with 50-199 workers). See Lim, Chee Peng, Small Industry in Malaysia, BeritaPublishing, 1986, P. 17.

- 6 -

C. Issues in the Administration of Selected Export Incentives

1.11 Mal4sia already operates a large number of export promotion schemesand policies," but this report focuses primarily on issues related to exportfinancing facilities; to a lesser extent, and in a very preliminary fashion,the report also touches on issues concerning the administration of the importduty drawback and exemption schemes.

The Export Credit Refinancing Scheme

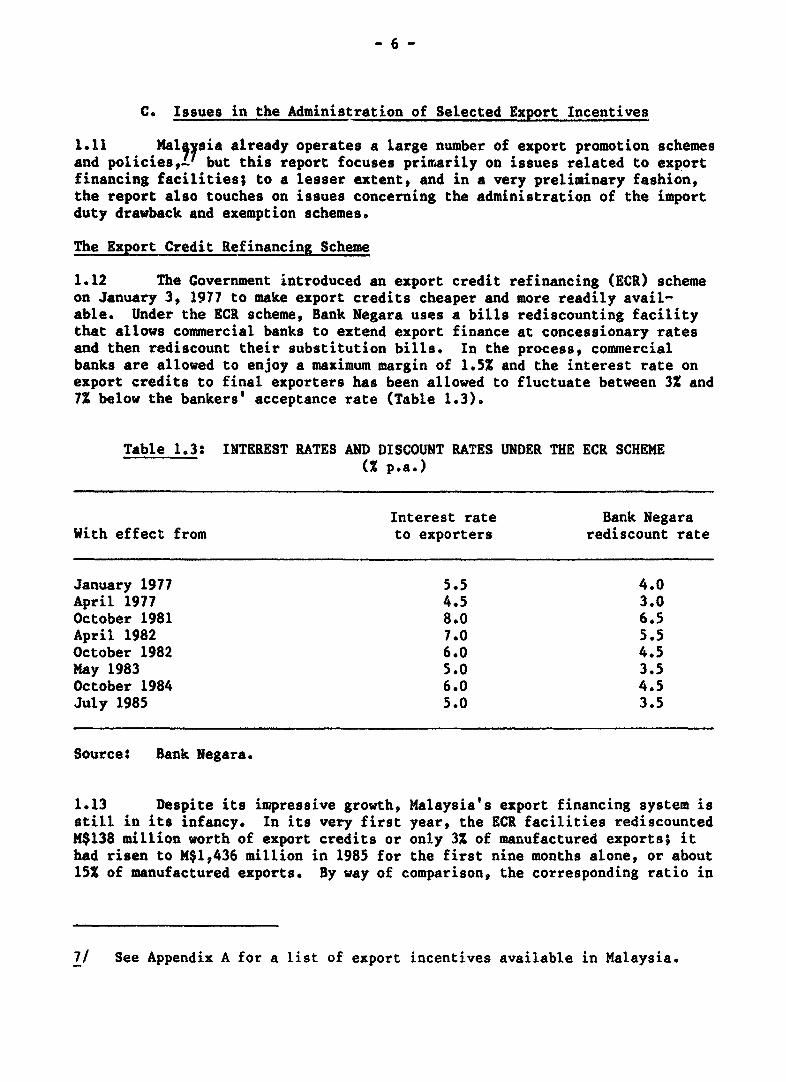

1.12 The Covernment introduced an export credit refinancing (ECR) schemeon January 3, 1977 to make export credits cheaper and more readily avail-able. Under the ECR scheme, Bank Negara uses a bills rediscounting facilitythat allows commercial banks to extend export finance at concessionary ratesand then rediscount their substitution bills. In the process, commercialbanks are allowed to enjoy a maximum margin of 1.51 and the interest rate onexport credits to final exporters has been allowed to fluctuate between 3Z and71 below the bankers' acceptance rate (Table 1.3).

Table 1.3: INTEREST RATES AND DISCOUNT RATES UNDER THE ECR SCHEME( p.a.)

Interest rate Bank NegaraWith effect from to exporters rediscount rate

January 1977 5.5 4.0April 1977 4.5 3.0October 1981 8.0 6.5April 1982 7.0 5.5October 1982 6.0 4.5May 1983 5.0 3.5October 1984 6.0 4.5July 1985 5.0 3.5

Source: Bank Negara.

1.13 Despite its impressive growth, Malaysia's export financing system isstill in its infancy. In its very first year, the ECR facilities rediscountedM$138 million worth of export credits or only 3% of manufactured exports; ithad risen to M$1,436 million in 1985 for the first nine months alone, or about151 of manufactured exports. By way of comparison, the corresponding ratio in

7/ See Appendix A for a list of export incentives available in Malaysia.

most advanced developing countries, with well developed export finance systemstends to be anywhere between 50% and 902.

1.14 A preliminary assessment of the ECR scheme by a World Bank team in198581 noted the following issues:

(a) that preshipment financing has been somewhat neglected, whereaspostshipment financing has been given too much emphasis. As aresult, the 802 share of postshipment financing in total exportcredits refinanced through the ECR scheme is extremely high, andcorrespondingly, the share of preshipment financing is very low;this appears to be contrary to the experience of most developingcountries, including advanced developing countries, where typicallythe ratios are just the reverse (80% for preshipment and 20% forpostshipment);

(b) that greater emphasis has been placed on providing compensatoryexport incentives through preferential interest rates, and insuffi-cient attention was paid to ensuring that exporters had quick andeasy access to financing; the report pointed out that access, andnot cost, is invariably the critical constraint in export finance;

(c) that the positive list system identifying goods eligible for ECRfacilities was inconsistent with the principle of treating equally,in terms of access to financing, all manufacturing and tradingactivities contributing to the export effort; and

(d) that tnough the ECR scheme met the production financing needs ofexporters, it did not meet the inventory financing needs of tradingcompanies.

1..15 As a consequence of the World Bank's preliminary assessment, theGovernment of Malaysia established a task force comprising officials from BankNegara and six leading commercial banks to review the ECR scheme and recorwMendmeasures for its improvemcat. The review was conducted in two phases. PhaseI was completed in early 1986 with the announcement of several revisions tothe ECR scheme beginning January 31, 1986:

(a) List of eligible goods. The "positive list" was replaced by a"negative list" listing only those goods not eligible for both post-shipment and preshipment financing under the ECR. The "negativelist" is composed of goods that are (i) excluded for strategicreasons (e.g., arms and ammunition); (ii) banned by law (e.g.,

8/ World Bank, Export Financing and Insurance in the Promot.on of Malaysia'sManufactured Exports, May 20, 1985.

-8 -

hallucinogenic drugs); and (iii) ined'le raw materials that havenot undergone significant processing._

(b) New refinancing limits. The administrative limit on totaloutstanding export credits available to a single exporter under theEOM scheme was raised from M$3 million to M$5 million. In addition,the maximum limit of M$10 million per exporter was abolishedaltogether; applications for loans in excess of M$5 million willneed to be approved by Bank Negara which will base its decision onthe financial position of the company, the value of exports sold oncredit terms and the destination of exports.

(c) Eligibility criteria. Only products with a domestic value added ofat least 20X and which use a minimum local raw material cntent of302 will be eligible for financing under the ECR scheme,

1.16 Under Phase II of the review, the Task Force set up three committeesto look into different aspects of the ECR scheme, namely the MechanismCommittee, Insurance Committee, and Procedures and Documentation Committee.The Mechanism Committee has already submitted a report, the InsuranceCommittee is now drafting its findings and the Procedures and DocumentationCommittee is expected to embark on its task only after the recommendations inthe mechanism and insurance reports are approved.

1.17 The mission was able to review the proposals of the MechanismCommittee and the preliminary findings of the Insurance Committee. Indeed,most of the remainder of this report contains the mission's views on thevarious recommendatjyls and suggestions expressed by both Committees. Amongstthe more important _ proposals for Phase II are:

(a) the introduction of a preshipment financing mechanism to improveindirect exporters' accessibility to working capital finance at thepreshipment stage;

(b) the improvement of existing postshipment insurance schemes tosupport the postshipment financing mechanism; and

(c) the introduction of a preshipment finance guarantee scheme toimprove access by exporters to the preshipment finance facility.

9/ The purpose of this last provision is consistent with the broadergovernmental objective of encouraging greater domestic value added inresource-based exportable manufactures.

10/ Comments on this aspect of the January 31st revisions are in para. 3.28of this report.

11/ The relatively less important proposals for Phase II such as periods andcoverage of financing are mentioned in the next two chapters.

The emphasis on preshipment finance in the Phase II proposal is entirelyappropriate, and reflects the enormous amount of institution building thatstill remains to be done in this area. However, for purposes of exposiFion,this report discusses issues in postshipment credit insurance in Chapter 2before it enters the more difficult and complex problems associated withpreshipment financing in Chapter 3.

Import Duty Drawback and Tariff Exemption

1.18 Under the import duty exemption scheme, the Minister of Finance isempowered by Section 14 of the Customs Act to exempt payments of import dutiesand surtax on imported inputs used in the production of goods destined foreither the export 'or the domestic market. Exporters are allowed full exemp-tion from import duty on imported components and raw materials that are notmanufactured locally, or, if manufactured locally, are not of acceptablequality or price. The duty drawback scheme, on the other hand, provides forduty drawback of both import and excise duties paid on inputs used in exportproduction. All imported inputs used in export production are eligible forduty drawback, and refunds are handled under an advanced payments basis.

1.19 The purpose of an import duty drawback or prior exemption scheme isto recompense exporters for any loss of competitiveness in internationalmarkets that may be caused by paying import duties on imported inputs. Tosome extent the schemes adopted in Malaysia tend to reduce the antiexport biasinherent in the incentive structure, but do not eliminate it altogether forseveral reasons. First, manufacturers tend to prefer selling to the domesticmarket because exports do not enjoy the same level of implicit subsidies as doimport substitutes. Second, these schemes as they are presently designed andadministered, do not recompense exporters who are forced to acquire inputs inthe domestic market at higher than c.i.f. import prices owing to theprevalence of import quotas, outright bans, or local content regulations.Third, these schemes do not benefit indirect exporters at all, and thereforedo not encourage or strengthen backward linkages. Finally, the full benefitof these schemes is reduced to the extent that it costs the exporters time andresources to obtain access to them.

1.20 It was noted earlier that introducing well designed and administeredduty drawback and prior exemption schemes would be a significant step towardsreducing the antiexport bias in the incentive structure. Furthermore, throughproper design and administration, these schemes can, and indeed should, reachindirect exporters, avoid any abuse of the system and yet remain costless tomanufacturers. This provides the focus of Chapter IV of this report. It mustbe emphasized here that the mission had insufficient time to analyze thedrawback and exemption schemes in detail, and therefore the findings in thisreport must be considered as only preliminary and tentative.

- 10 -

II. PRIORITY TASKS IN POSTSHIPMENT FINANCE ADMINISTRATION

2.01 Chapter 1 outlined the strategic options confronting Malaysia, theimportance of industry and trade policy to export prospects, and issues relat-ing to the ECR scheme and compensatory fiscal incentives to exporters. Thischapter delves into the specifics of the ECR scheme, and focuses on prioritytasks in postshipment finance administration. After a brief description ofthe Government's proposals on postshipment finance in this introduction, therest of the chapter concentrates mostly on postshipment credit insurance.

2.02 As noted earlier (para. 1.17), the ECR Task Force made a number ofreCommendations under Phase II of its deliberations. In regard to postship-ment finance, these also included proposals to:

(a) continue refinancing for 100% of the f.o.b. value of export orders,but include freight and insurance charges in the post-shipmentcoverage if such payments are made to Malaysian companies;

(b) increase the refinancing period from 90 to 180 days plus a standarden route period for each country of destination;

(c) reduce the minimum amount of postshipment finance for each exporterapplication from M$20,000 to M$1O,000, though applications forsmaller amounts can be entertained provided that refinancingrequests are bunched so as to exceed this minimum; and

(d) introduce an effective insurance and guarantee system to coveroverseas political and commercial risks so that access topostshipment finance is eased.

2.03 It is normal in many other developing countries to finance exportersfor freight and insurance charges in c.i.f. contracts, but restricting financeto goods shipped only by Malaysian carriers is unfortunate because thecompetitiveness of Malaysia's export products in international markets maysuffer unduly. Raising the maximum refinancing period would place Malaysianexporters on the same footing as their competitors who, increasingly often,are offering 180 day credit terms for consumer and light engineering goods.The postshipment ECR facility is not available for sales on sight draft termsor cash against documents and this is in line with the practice of manycountries offering postshipment credit schemes. The introduction of an effec-tive postshipment credit insurance scheme, however, is a difficult task and isthe focus of the next two sections in this chapter.

- 11 -

A. Weaknesses in the Existing Postshipment Credit Insurance Scheme

2.04 Export credit insurance promotes exports by:

(a) providing exporters an effective umbrella of protection against therisks of nonpayment by foreign buyers;

(b) encouraging exporters to:

(i) liberalize payment terms to traditional customers as a meansof increasing business;

(ii) seek new buyers in existing markets; and

(iii) diversify into new, unfamiliar and sometimes riskier markets;

(c) facilitating access to postshipment finance by sharing risks carriedby commercial banks.

The objectives of export credit insurance and those of the ECR scheme havemuch in common, but export credit insurance facilities are an important compo-nent of the institutional framework supporting Malaysian exporters irrespec-tive of whether financing is available through the ECR scheme or not.Malaysia Export Credit Insurance Berhad (MECIB) ' the only organization inMalaysia which provides export credit insurance.-/ An analysis of the short-comings of the export credit insurance scheme in Malaysia, therefore, inevit-ably becomes a discussion of MECIB's operations and experience.

MECIB's Operations are too Small

2.05 MECIB offers a whole turnover comprehensive export credit insurancepolicy, renewable annually, covering an exporter's sales worldwide and underwhich revolving credit limits are established for each of the exporter'sbuyers. There is a choice between a "contracts" policy which covers risks ofnon-payment by the buyer from date of contract and a "shipments" policy whichcovers risks from date of shipment. In addition, the exporter can choosebetween a global policy covering exports to all countries or a selectedmarkets policy which excludes some markets requested by the exporter.

2.06 Despite an impressive range of policies 131 offered by MECIB, itsoperations cover only a tiny fraction of Malaysia's manufactured exports(Table 2.1). Since 1982, the number of policies held with MECIB has stagnatedat around 106, a small figure in comparison to the number of firms in Malaysiainvolved in export activities. The total value of exports covered by

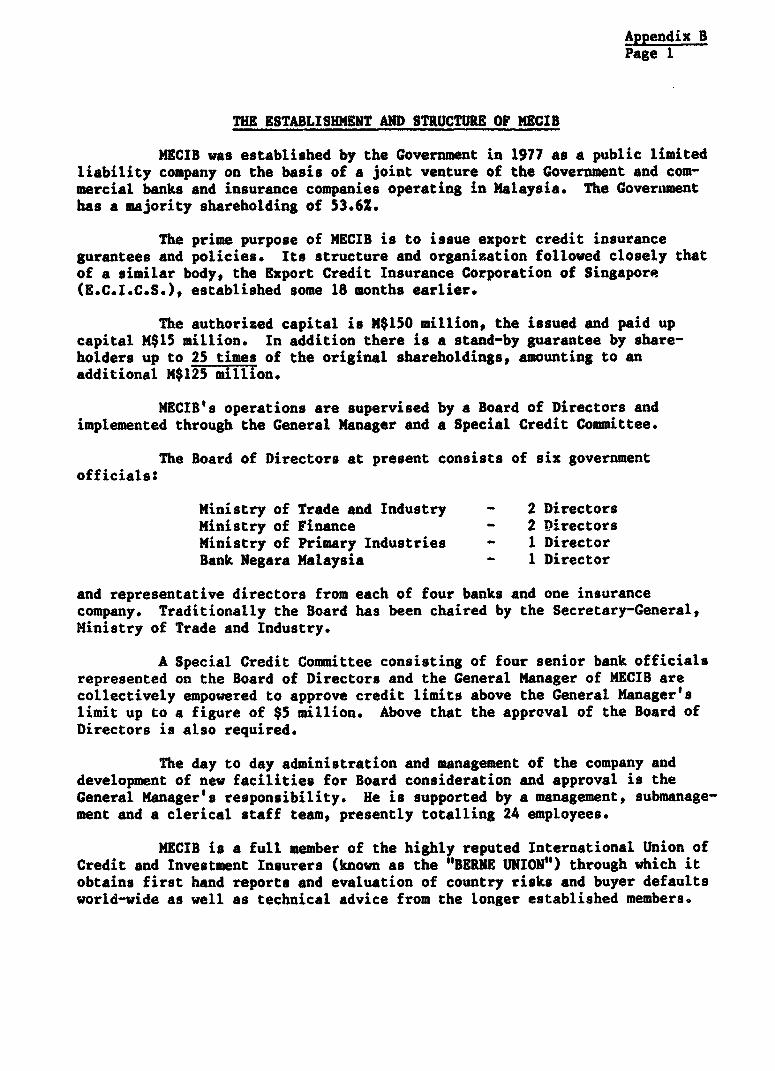

12/ For a brief description on the establishment and structure of MECIB, SeeAppendix B.

13/ Which includes policies for special requirements such as capital goodscontracts on a medium- or long-term basis, construction contracts etc.

- 12 -

MECIB 141 has never exceeded 2X of manufactured exports from Malaysia. Thiscompares very unfavorably with other developing countries using similarschemes.

Table 2.1s MECIB: NUMBER OF POLICYHOLDERS AND VALUE OF EXPORTS INSURED,1978-85

1978 1980 1982 1984 1985

Number of policyholders 21 80 103 107 106Exports declared (1M$ millions) 11 97 119 153 119Share in exports of manufactures (X) 0.3 1.5 1.6 1.3 1.0

Source: MECIB.

2.07 As a consequence of its small operation, MECIB is unable to coverits operating costs. Ignoring investment income derived from the initialpaid-up capital, the insurance account after seven years' operations shows nosigns of breaking even (Table 2.2). Annual premium income is only just overhalf of administration expenses, leaving noihing for claims. The investmentincome, however, has been more than sufficient to create a surplus in mostyears and has increased the capitalization of MECIB.

Table 2.2: MECIB: FINANCIAL RESULTS, 1978-85(in M$ '000) /a

1978 1980 1982 1984 1985

Premium income 56 422 430 760 457Claims - 72 2,169 233 216Administration expenses 367 707 786 833 801

Net operational deficit 311 357 2,446 306 560Investment income n.a. n.a. 1,718 1,420 1,577

Net surplus n.a. n.a. (728)/b 1,114 1,017

/a Rounded to nearest thousand.7i Brackets indicate net loss.

Source: MECIB.

14/ i.e., the value of exports declared by the policyholders.

- 13 -

MECIB's Insurance Coverage is Limited

2.08 The global schedule of markets In MECIB's comprehensive policycomprises a list of 199 countries with no less than 44 totally off cover, anda further 30 with low monetary ceilings. Other credit insurers appear to bemore liberal in several of these markets (Table 2.3), and many continue tocover new business even in the face of transfer delays. MECIB provided a listto the mission of some 40 credit limit applications amounting to M$27 millionand 6 enquiries for medium term contracts amounting to X$138 million for whichcover had been rejected or, in the case of some revolving credit limits, can-celled as a result of the suspension of cover on various countries sinceAugust 1984.

Table 2.3: SOME POTENTIAL MARKETS FOR MALAYSIAN EXPORTSWITH LITTLE OR NO COVER PROVIDED BY MECIB

Destination MECIB Attitude of Berne Union memberscountry current Number Number providing Number

ceilings reporting full or off cove,(M$ million) restrictive cover

Bangladesh 1 5 4 1Egypt 2 20 20 -Iran 5 18 17 1Pakistan 2 15 14 1Romania 2 17 16 1Yemen AR 1 15 15 -fugoslavia 10 20 20 -Brazil off cover 21 21 -Ethiopia off cover 16 14 2Iraq off cover 19 18 1Nigeria off cover 19 9 10North Korea off cover 8 3 5El Salvador off cover 10 6 4Syria off cover 13 12 1Yemen DR off cover 11 11 -

Source: MECIB; Berne Union.

2.09 Declining cover for so much business feeds exporters' and bankers'disillusionment with MECIB's credit insurance scheme (see para. 2.12).MECIB's basic principle of cover on a whole turnover basis to create a largepool of risk end an adequate underwr;ting reserve cannot flourish if too muchrisky business is declined. It tends to lose policyholders and spreads anegative impression about the usefulness of the credit insurance scheme.

- 14 -

2.10 MECIB's prudence stems from its private company structure. MECIB'spaid-up capital structure does not permit it to take on too many risks. As aconsequence it tries to generate a cash surplus every year even if it meansnot offering cover on a large number of potential markets. This runs contraryto the needs and purpose of a national export credit insurance scheme for thepromotion of exports.

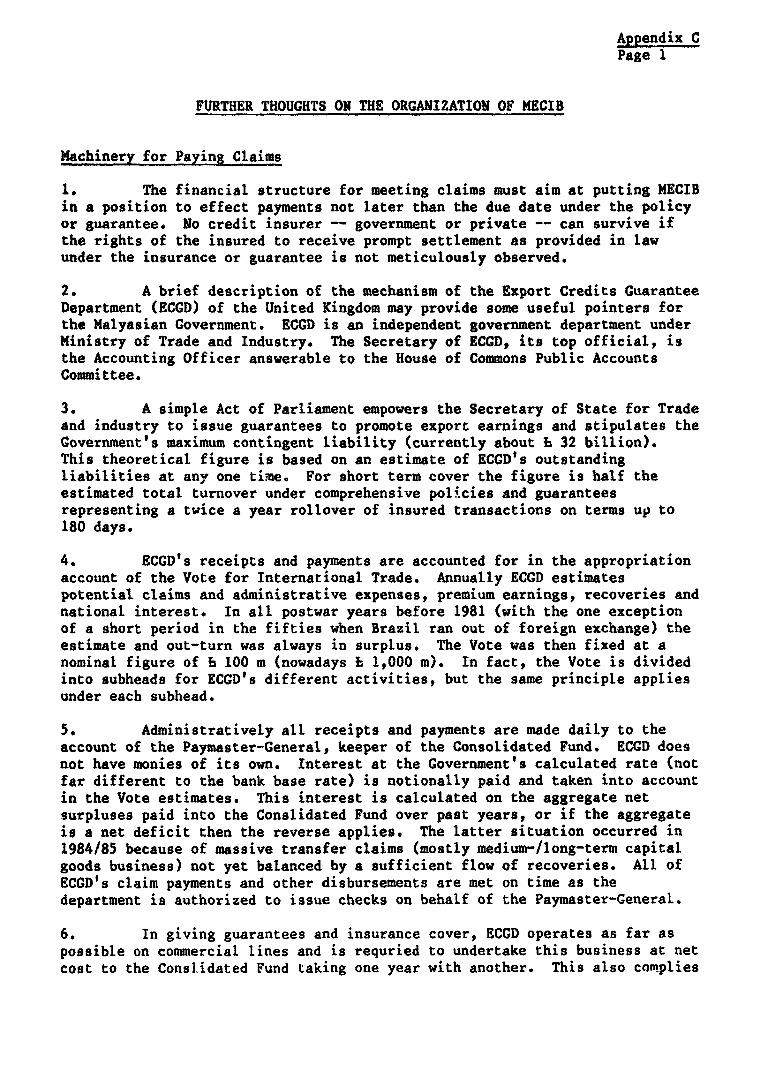

2.11 Declining cover on buyer creditworthiness grounds makes for prudentcommercial practice since the potential for recoveries on insolvencies anddefaults is low. However, cover for political risks is altogether differentfrom cover for buyer risk. Losses stemming from political risk arise mainlyfrom transfer delays. Upon a transfer claim, the credit insurer suffers onlya loss of interest. Risks stemming from transfer delays cannot be estimatedby standard actuarial methods and cannot generally be covered by the privateinsurance market. The world's officially-backed credit insurarce institutionsowe their existence to covering transfer risks, but sometimes when transferdelays do take place, losses are incurred. However, official credit insurersare expected to conduct their business at no net cost to the taxp ,-er over aperiod of several years. The cycle of transfer losses and recoveries makesthis possible. In the U.K., the Export Credits Guarantee Department (ECGD)transfers annual surpluses into the Government's consolidated fund and earnsinterest at market rates on the accumulated balance; in times of deficit itpays interest, also at market rates.

Exporters and Bankers do not Regard MECIB Highly

2.12 Discussions with exporters and bankers revealed that they did notregard MECIB as capable financially of honoring claims made by its clients.MECIB's track record on claims payments does not justify this pegception,though improvements can be made in claims payments procedures. Theperception that MECIB will not honor claims made by its policyholders stemspartly from the reputation of another credit guarantee organization, CreditGuarantee Corporation (CGC), which does not have a particularly good record ofmeeting claims promptly. In addition, MECIB is vi'wed as a private organiz-ation and without official government backing, which places narrow limits onits financial strength.

2.13 Large exporters displayed little interest in credit insurancebecause they either continue to command secured terms from their buyers underletters of credit or sell to long established customers. They demonstratedlittle awareness that credit insurance could make new exporting opportunitiesless risky, and appeared satis£ied with selling to traditional markets andbuyers. In the few instances that they had approached MECIB for cover oflarge orders, MECIB had declired because of its limited insurance coverage and

15/ See Appendix C.

- 15 -

prudent country limits.161 This merely tended to reinforce the negativeimpressions that they already held of MECIB.

2.14 Small exportersp on the other hand, appeared to be more conscious ofthe need for credit insurance protection, particularly if new at exporting.But like their larger brethren, they found MECIB's long list of closed andrestricted markets very frustrating. In addition, several complained of beingunable to obtain adequate postshipment finance because of collateral demandsby commercial banks who either failed to advise their client, of the roleMECIB could play to ease their situation, or advised them that a MEC[B policywas an inadequate substitute for a collateral.

2.15 Bankers clearly did not consider MECIB gilt-edged in the way bankersin other countries regard their official credit insurance institutions. Theprivate company structure of MECIB and limited paid-up capital did not inspiresufficient confidence. Bankers would not accord a MECIB insurance policy thesame standing as a letter of credit from a wAl known overseas bank, thusdiscouraging any move away from letters of credit to win new business.

2.16 But even more disturbing is the banking practice of grantingpostshipment finance on the strength of an exporter's collateral securityrather than on "buyer paper". It follows that even the full acceptance of aMECIB i;.surance policy as subst.tute for a first-class irrevocable letter ofcredit will not alter the basic collateral approach of bankers. The prefer-ence for collateral security to buyer paper appeared to be strongest amongstMalaysian banks. In contrast, the two international banks interviewed by themission prided themselves on being trade banks and claimed that they evaluatedpostshipment financing on a project basis with due regard to the standing ofthe buyer whose paper secured the debt. However, in practice, MECIB has notfound the international banks any more receptive to credit insurance thanMalaysian banks.

B. Measures to Improve the Postshipment Credit Insurance System

2.17 The previous section noted that the existing postshipment creditinsurance system is weak because MECIB's operations are small in relation tothe country's exports, its insurance coveragp is limited, and it is not highlyregarded by the exporting and banking community. Rectifying these short-comings will require the joint efforts of the Government, MECIB, exporters andcommercial banks. In particular, it will be necessary to: (a) change theorganizational structure of MECIB; (b) strengthen institutional links;(c) introduce new insurance instruments; and (d) develop MECIB expertise.

16/ For example, MECIB was unable to cover a M$12 m single order to Iraqbecause it was off cover. The exporter concerned stated that they couldsignificantly increase their M$75 m export business if MECIB covered itssales to Iraq and other Middle-East buyers.

- 16 -

Change the Organ(wational Structure

2.18 The export credit insurance scheme in Malaysia was !g up alongsimilar lines to its contemporary sister in Singapore, ECICS, - and togetherthey are unique in the world in providing export credit insurance withoutgovernment financial backLng'. All the other export credit insurance schemes,both in developed and in developiug countries, have been unable to fulfilltheir role of promoting exports w'thout their Governments standing asguarantors of last resort. MECIR's various shortcomings, described in theprevious section, stem primarily from its lack of government backing. EvenECICS has failed to fulfill,its. 'proper national role despite much highercapitalization; however, wit'hin 12 months of its formation the SingaporeGovernment acknowledged this by supporting the insurance of contractsindividually too large in relation to ECICS' paid-up capital.

2.19 Providing exporterp with the opportunity to obtain an all-riskinsurance, -policy, and covering exports to most (if not all) countries andbuyers within certain prudent underwriting limits, is a practice to bestrongly recommended. This practice, consistently applied, will attract alarge number of exporters and thus create the broad premium base and largerisk pool so necessary for successful underwriting.

2.20 There are five possible ways in which the Government can back exportcredit insurance facilities: (i) through a government department or govern-ment agency; (ii) through a private sectcr insurance company or financialinstitution acting as a commission agent in the name and for the account ofthe Government; (iii) through an organizationally autonomous but whollygovernment-owned corporate entity or public ,und; (iv) through a government-controlled corporate entity which is jointly owned by the Government andprivate sector insurance and banking entities; and (v) in cooperation withprivate sector insurance entities which assume, for their own account, someagreed-upon percentage of the commercial and political risk.

2.21 This report does not discuss the pros and cons of each option inrespect of Malaysia's requirements. However, a recent report prepared byconsultant from the official Austrian credit insurance institution, OKB, -

looked specifically into this issue and redowmended strongly that MECIB shouldunderwrite all risks, commercial and political, in the name and on behalf ofthe Malaysian Government. In other words, the OKB report suggested that MECIBshould act as the "sole agent of th Malaysian Governmept" in the field ofexport credit insurance. This system has featured succ ssfully for decades inthe Federal Republic of Germany as well aa in Austria, but the OKB reportadapts it well to Malaysia's needs.

17/ Export Credit Insurance Corporation of Singapore.

18/ Oesterreichische Kontrollbank Aktiengesellschaft, Study on the Status andStructure of MECIB, April 1984.

- 17 -

2.22 The central recommendations of the OKB report are well conceived andcould suit Malaysia's requirements. An appealing feature of the recommenda-tions is that it does not interfere with MECIB's existing company structure,and it ensures that MECIB's export credit insurance expertise, built overyears, will continu-e to be used. MECIB will operate as the aget of theGovernment which will be represented by a Guardian Authority, The Guardianauthority, with powers conferred on it by parliamentary decree, should beresponsible for setting broad policies through an extort credit insurancecouncil composed of representatives from relevant ministries and BankNegara. Certain underwriting authority could be delegated further to asmaller "Export Credit Insurance Committee" comprising representatives of fourministries and, because underwriting is a matter of professional skill, atleast three bankers.

2.23 However, there are certain amplifications and modifications that canbe made to the OKB report. These, and other details of the proposed neworganiz.ational structure are given in Appendix C.

Strengthen Institutional Links

2.24 A successful export effort requires close and strong institutionallinks between exporters, banks and the export credit insurance agency. Therole of the export credit insurance agency is primarily to help exporters gainaccess to postshipment finance by reducing the risk of lending for exports bybanks. In considering how MECIB's credit insurance operations can fulfillthis function, it is well to remember that MECIB has already an assignmentmechanism available to banks which is not sufficiently used and appreciated toachieve its purpose. Since this mechanism exists and does not involve MECIBadopting new underwriting and operational techniques, it is important toconsider its operations and implications.

2.25 Exporters taking out export credit insurance with MECIB submitproposal forms outlining the anticipated volume of their exports worldwide forthe next 12 months, broken down by country of destination and by terms ofpayment. MECIB then issues a comprehensive contract policy or comprehensiveshipments policy according to whether the exporter requires to cover risksfrom date of contract or date of shipment. The policy describes veryprecisely the risks coveredj0 he revolving credit limit mechanism, thepercentage of loss covered,- the calculation of loss in case of a claim, themethod of declarations made and payment of premium. The policy definesvarious conditions that have to be observed by the exporter including the

19/ The Guardian Authority could be either the Ministry of Trade or theMinistry of Finance. The Ministry of Trade may be preferred for itsobvious interest in promoting exports The annual budget may need toinclude allocations to cover insurance liabilities incurred by theGovernment, as is the case for ECGD in the U.K.

20/ Eighty-five percent for all causes of loss other than buyer repudiationwhere there is a 20% first loss clause.

- 18 -

obligation to declare all exports globally for the 12 month period covered bythe policy. Exporters' claims may be declined in the event of a dispute withthe buyer which results in the loss of the case, or failure to resolve thedisputet or if they otherwise breach the terms of their policies or creditlimits.

2.26 The most commonly accepted method employed by a bank to protectitself when lending money against an exporter's extension of credit to aforeign buyer is for the bank to obtain from the exporter's credit insurer an"assignment of proceeds" of the exporter's credit insurance policy. However,irrespective of the assignment of proceeds to the bank, the credit insurerstill considers the exporter as the party responsible for providing theevidence, in the event of a claim, that the subject loss was not in any waydue to the policyholder's nonperformance under the contract of sale.Accordingly, if an exporter fails in a claim against the credit insurer, thesecurity of the assignment which the bank thought it obtained will not behonored. Claim failures are generally due to an exporter's non-performance,or the exporter's noncompliance with the terms and conditions of the insurancepolicy. A vital policy condition is the buyer credit limit approval. Thisarea of doubt for banks can be removed by MECIB copying all credit limitapprovals to the bank.

2.27 Banks throughout the world vary in their attitudes towards therelative collateral value of the proceeds of such an assignment, but forexport financing on short credit terms, the majority of countries operate onthe security afforded by assignment. Only a relatively few continue tooperate more advanced systems of direct insurance or guarantees to banks inrelation to the bulk of export credit insurance.

2.28 Banks usually place considerable trust in their government-backedexport credit insurance organizations and find that the majority of claims aremet. Indeed, many credit insurers tend to pay ex gratia where possible ratherthan decline a claim for the sake of their reputation and to prevent anydamage to the country's export effort. In France, for example, the onlysecurity provided by COFACE is assignment, yet it is understood that banksreduce their collateral requirements on their clients by an amount at leastequal to the COFACE cover. Nearer by, Hong Kong also operates only onassignments to banks.

2.29 Some countries, for example the United Kingdom and India, havereinforced their links with banks even for short-term postshipmentfinancing. In the UK the development of the short term comprehensiveguarantee to banks was aimed sp-cifically at persuading banks to reduce theirinterest rates on postshipment credits. Early in 1960 the ECCD concluded anagreement with the banks that in return for the protection of an ECGDguarantee, the banks would reduce their lending rates to 5/8% over the baserate. Since the charge imposed on the exporter for this facility (additionalto the premium on the underlying credit insurance) is 0.75%, this supplemen-

- 19 -

tary guarantee tends to attract medium an small size firms who would other-wise pay 3X or more above the base rate.21/

2.30 Neither assignment nor more sophisticated direct insurance orguarantee mechanisms (para. 2.35) will be sufficient to generate a minimumlevel of demand for credit insurance. It seems imperative that in introducingPhase II of the ECR scheme and establishing MECIB as a government agency, BankNegara will need to use its enormous persuasive powers to encourage commercialbanks to ease the collateral terms of postshipment lending depending upon theavailability of buyer or MECIB security. This will be of considerable benefitto small and medium exporters who experience collateral limitations.

2.31 However, the Government should resist the temptations to make theavailability of ECR facilities to exporters conditional upon obtaining exportcredit insurance from MECIB. Such an arrangement may be beneficial to MECIB,but it would run counter to the original objective of promoting exports andwould not provide MECIB an incentive to constantly improve its insuranceservices and provide better support to the export community. Instead, BankNegara will need to help MECIB on the initial stages to advertise its servicesand educate the banking and export communities on the advantage of the exportcredit insurance scheme.

Introduce New Insurance Instruments

2.32 Despite the value of assignments to banks, a direct form ofguarantee or insurance given by the credit insurer directly to a bank is moreeffective in ensuring adequate financial access for new and small exporters.There is an overwhelming case for a banker's guarantee or insurance where longcredit terms are involved becaum the financing burden can be considerableeven for the largest companies.-/

2.33 Though short-term credit is more easily borne by exporters andrelatively few countries have felt the need to develop bankers' guarantees,some countries have developed a form of direct guarantee or insurance to banksto overcome the resistance of commercial banks in easing their collateralrequirements. Some guarantees, such as that provided by ECGD in the U.K.,have induced banks to lend at less than market rates.

2.34 Two systems have been developed to provide comprehensive guarante13 /or insurance covering an exporter's entire sales on credit for over a year:-3

21/ The mechanics of this type of guarantee are explained in para. 2.39.

22/ It is interesting to note here that in France, the assignment systemoperates even in the medium term field; but this is possible becausemedium-term financing is provided by a government-sponsored bank, theBanque de Commerce Exterieure.

23/ In contrast, bankers' guarantees for medium term credit are usuallyspecific to each contract of sale.

- 20 -

(a) an indemnity to a bank against recourse loss arising from either theinsolvency; or protracted default by an exporter in which the creditinsurer shares a portion of such loss (System A); and

(b) a 100l unconditional guarantee to a bank relating to buyers' failureto pay a particular bill or bills (System B).

2.35 Insurance policy 24/ to banks against exporter recourse risk(System A). Under this system there are two parallel policies. One insurancepolicy protects the exporter against loss arising from nonpayment from thebuyer or the buyer's country. The other protects the bank should recoursehave to be taken against the exporter (Figure 1). For example in India thebanker's policy relates to one exporter only. Claim proceeds under theexporter's policy are assigned to the bank. If MECIB were to provide similarloss coverage, then from the bank's point of view the exporter's insuranceassignment would produce 85% of an unpaid bill plus 66-2/3% of the uninsuredamount of 15X if and when recourse proceedings against the exporter fail.Recourse by the bank would, however, be for 100% of the bill should theexporter's claim on MECIB fail, in which case cover to the bank would be lessoverall, namely only the 66-2/3% provided in the banker's insurance policy.

2.36 This system has the advantage that it can be installed with littledisturbance to existing banking procedures and that MECIB would rely largelyon banks, with considerable knowledge of their clients, continuing to appraisetheir recourseworthiness. Of course, if the banks do not sufficiently modifytheir recourse criteria to take account of the combined effect of the MECIBcredit insurance proceeds assignment and MECIB's recourse risk participation,then the system will produce only marginal benefit tv the smaller exporterswith little collateral to offer.

2.37 This system can also be modified to provide every encouragement tobanks and exporters to use MECIB. MECIB can provide an "all exporter" policyto banks on more generous terms as an alternative to the "individual exporter"policy. As exporters included in MECIB's bankers' insurance policy must takeout an underlying insurance policy, banks may find it difficult to persuadeall their client exporters to acce,'t the arrangement. A compromise negotiablebetween MECIB and the banks could be a policy covering all exporters in aparticular product group or homogeneous group. A suggestion on how premiumrates and percentage of cover c.,n differ between different types of bankers'insurance policies is given in Table 2.4. Of course, MECIB management will

24/ The terms "guarantee" and "insurance" are often used interchangeably, butin this report they have been used with a precise meaning in mind. An"insurance policy" provides indemnity against net loss arising fromcertain events taking into account savings, counter claims, etc., andsuch a policy is conditional upon performance or compliance with otherconditions. A guarantee, on the other hand, is an instrument whichguarantees that if a debtor does not pay at due date, the guarantor willstand unconditionally in his place.

- 21 -

FIGUtRE I

MECIB INSURANCE POLICY TO BANK PROVIDINGINDEMNITY ON ITS RECOURSE TO EXPORTER

| RPORTE 0 ODEBTBUER

4?~~~c

w

BIANt

1. Bankts pay premoium for their policies. Exporters pay for theirw#holeturnover credit insurance policies.

2.. Bankers' insurance policies art further "cured by an "ssigentof exporters' wholeturnover policy.

- 22 -

need to do considerable additional work to refine these preliminary estimates,taking into account cash flow projections, capital availability etc.

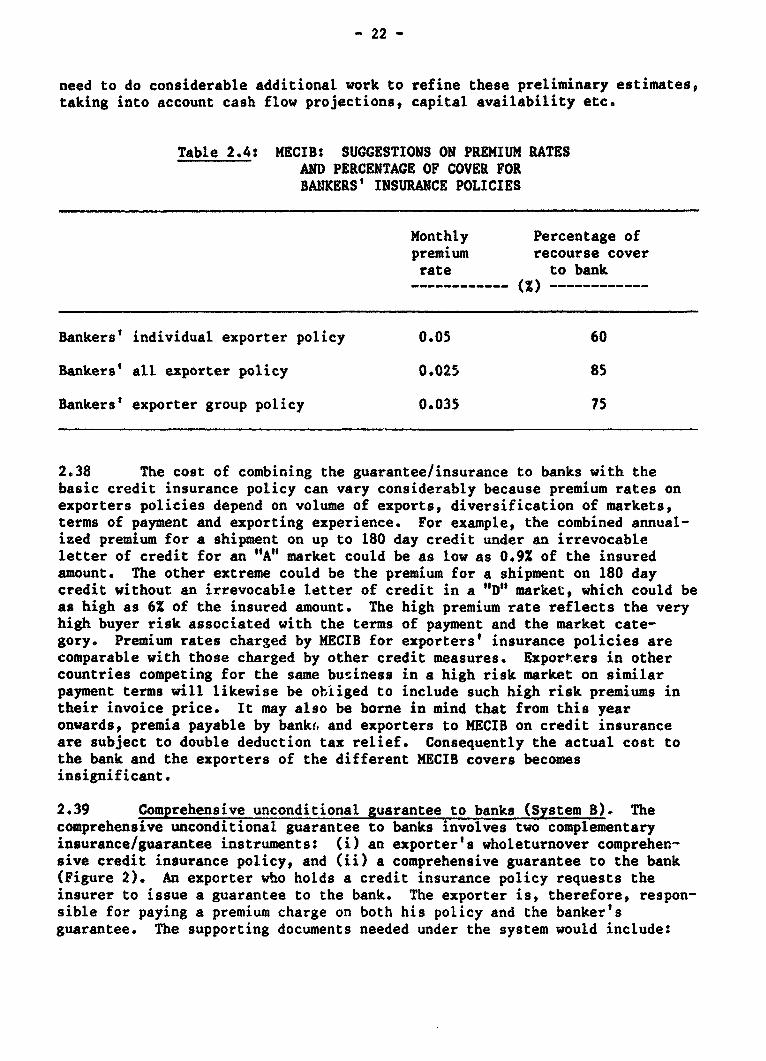

Table 2.4: MECIB: SUGGESTIONS ON PREMIUM RATESAND PERCENTAGE OF COVER FORBANKERS' INSURANCE POLICIES

Monthly Percentage ofpremium recourse coverrate to bank

…___________ (x) …-----------

Bankers' individual exporter policy 0.05 60

Bankers' all exporter policy 0.025 85

Bankers' exporter group policy 0.035 75