Malaysia Industry Focus Malaysia Property - DBS PR1MA is set to complete 15,000 homes this year, ......

28

ed-TH / sa- WMT, PY Focus on emerging growth corridors • Rising supply in 2017 to dent market sentiment • Higher demand for public housing due to raised income ceiling could intensify competition in affordable housing • Demand at emerging growth corridors with huge population catchments remains healthy • BUY developers with niche expertise: Eco World, MKH and Matrix Concepts Subdued sentiment. Despite the recent share price recovery for property developers, we believe the property market will remain lacklustre in 2017, driven by persistently weak sentiment, low affordability and accelerating incoming supply. We believe more high-rise completions are expected this year due to the delivery of projects with developer interest-bearing scheme (DIBS) that developers capitalised on before it was banned effective January 2014. This could continue to dent the sentiment in the property market. Intensifying competition in affordable housing. The government has already prioritised the development of public housing. PR1MA is set to complete 15,000 homes this year, which is ~20% of recent year’s average completions. Also, 132,000 PR1MA houses are under construction now. The raised household income eligibility to RM15,000/month and reduced moratorium of five years will appeal to more middle- income households, indirectly posing more competition to private developers. Developers will have to revise their product offerings to incorporate more ‘value-buy’ properties with differentiating lifestyle amenities that will distinguish themselves from lower-priced public housing, which could come at the expense of margins. Flattish sales targets. Developers under our coverage have largely set flattish sales targets for 2017 in view of the still challenging property market, despite the healthy demand at certain emerging growth corridors with huge population catchments such as Kajang/Semenyih, Sungai Buloh/Denai Alam and Dengkil/Salak Tinggi. Selective picks. We like Eco World, MKH and Matrix which are township developers with niche expertise and established brand names within local communities. The trio has achieved their respective commendable sales targets in FY16 despite a fair share of downward revisions by their peers amidst the challenging environment. KLCI KLCI KLCI KLCI : : : : 1,725.54 1,725.54 1,725.54 1,725.54 Analyst QUAH He Wei, CFA +603 2604 3966 [email protected] STOCKS Source: AllianceDBS, Bloomberg Finance L.P. Closing price as of 8 Mar 2017 SP Setia SP Setia SP Setia SP Setia : Sector leader - largest residential property developer by market cap Sunway Bhd Sunway Bhd Sunway Bhd Sunway Bhd : Property and construction group with interests in quarrying, building materials manufacturing and trading. UEM Sunrise Bhd UEM Sunrise Bhd UEM Sunrise Bhd UEM Sunrise Bhd : Master developer of Nusajaya, high-end and commercial developer in Mont' Kiara and around KLCC Eco World Eco World Eco World Eco World : Township developer with 7,443 acres of land bank worth RM81bn GDV offering comprehensive range of products in Iskandar Malaysia, Klang Valley and Penang. Eastern & Oriental Bhd Eastern & Oriental Bhd Eastern & Oriental Bhd Eastern & Oriental Bhd : Largest niche high-end developer with exposure to prime landbank in Penang, KL & Iskandar Malaysia Matrix Concepts Holdings Bhd Matrix Concepts Holdings Bhd Matrix Concepts Holdings Bhd Matrix Concepts Holdings Bhd : Matrix Concepts is one of the largest developers in Negeri Sembilan, focusing on its flagship township development, Bandar Sri Sendayan which covers 2,350 acres MKH Berhad MKH Berhad MKH Berhad MKH Berhad : MKH is an established township developer in Kajang/Semenyih and Greater Klang Valley. Its 16k ha oil palm estates in Indonesia has started to contribute significantly Weak consumer sentiment Source: AllianceDBS, BNM, MIER -40% -30% -20% -10% 0% 10% 20% 30% 40% 50% 60% 70% 60 70 80 90 100 110 120 130 1Q10 3Q10 1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15 1Q16 3Q16 MIER consumer sentiment (LHS) Total approved property loan growth (RHS) DBS Group Research . Equity DBS Group Research . Equity DBS Group Research . Equity DBS Group Research . Equity 9 Mar 2017 Malaysia Industry Focus Malaysia Property Refer to important disclosures at the end of this report Price Price Price Price Mkt Cap Mkt Cap Mkt Cap Mkt Cap Target Price Target Price Target Price Target Price Performance (%) Performance (%) Performance (%) Performance (%) RM RM RM RM US$m US$m US$m US$m RM RM RM RM 3 mth 3 mth 3 mth 3 mth 12 mth 12 mth 12 mth 12 mth Rating Rating Rating Rating SP Setia 3.39 2,172 3.50 1.8 9.4 HOLD Sunway Bhd 3.16 1,436 3.00 6.8 3.6 HOLD UEM Sunrise Bhd 1.21 1,233 1.10 18.6 16.4 HOLD Eco World 1.55 823 1.80 12.3 20.2 BUY Eastern & Oriental Bhd 1.89 533 1.20 26.9 18.1 FV Matrix Concepts Holdings Bhd 2.51 322 3.10 2.5 4.2 BUY MKH Berhad 2.95 278 3.70 2.4 30.5 BUY

Transcript of Malaysia Industry Focus Malaysia Property - DBS PR1MA is set to complete 15,000 homes this year, ......

ed-TH / sa- WMT, PY

Focus on emerging growth corridors

• Rising supply in 2017 to dent market sentiment

• Higher demand for public housing due to raised

income ceiling could intensify competition in

affordable housing

• Demand at emerging growth corridors with huge

population catchments remains healthy

• BUY developers with niche expertise: Eco World,

MKH and Matrix Concepts

Subdued sentiment. Despite the recent share price recovery

for property developers, we believe the property market will

remain lacklustre in 2017, driven by persistently weak

sentiment, low affordability and accelerating incoming supply.

We believe more high-rise completions are expected this year

due to the delivery of projects with developer interest-bearing

scheme (DIBS) that developers capitalised on before it was

banned effective January 2014. This could continue to dent the

sentiment in the property market.

Intensifying competition in affordable housing. The

government has already prioritised the development of public

housing. PR1MA is set to complete 15,000 homes this year,

which is ~20% of recent year’s average completions. Also,

132,000 PR1MA houses are under construction now. The

raised household income eligibility to RM15,000/month and

reduced moratorium of five years will appeal to more middle-

income households, indirectly posing more competition to

private developers. Developers will have to revise their product

offerings to incorporate more ‘value-buy’ properties with

differentiating lifestyle amenities that will distinguish

themselves from lower-priced public housing, which could

come at the expense of margins.

Flattish sales targets. Developers under our coverage have

largely set flattish sales targets for 2017 in view of the still

challenging property market, despite the healthy demand at

certain emerging growth corridors with huge population

catchments such as Kajang/Semenyih, Sungai Buloh/Denai

Alam and Dengkil/Salak Tinggi.

Selective picks. We like Eco World, MKH and Matrix which

are township developers with niche expertise and established

brand names within local communities. The trio has achieved

their respective commendable sales targets in FY16 despite a

fair share of downward revisions by their peers amidst the

challenging environment.

KLCIKLCIKLCIKLCI : : : : 1,725.541,725.541,725.541,725.54

Analyst QUAH He Wei, CFA +603 2604 3966 [email protected]

STOCKS

Source: AllianceDBS, Bloomberg Finance L.P.

Closing price as of 8 Mar 2017

SP SetiaSP SetiaSP SetiaSP Setia :::: Sector leader - largest residential property developer by market cap

Sunway BhdSunway BhdSunway BhdSunway Bhd :::: Property and construction group with interests in quarrying, building materials manufacturing and trading.

UEM Sunrise BhdUEM Sunrise BhdUEM Sunrise BhdUEM Sunrise Bhd :::: Master developer of Nusajaya, high-end and commercial developer in Mont' Kiara and around KLCC

Eco WorldEco WorldEco WorldEco World :::: Township developer with 7,443 acres of land bank worth RM81bn GDV offering comprehensive range of products in Iskandar Malaysia, Klang Valley and Penang.

Eastern & Oriental BhdEastern & Oriental BhdEastern & Oriental BhdEastern & Oriental Bhd :::: Largest niche high-end developer with exposure to prime landbank in Penang, KL & Iskandar Malaysia

Matrix Concepts Holdings BhdMatrix Concepts Holdings BhdMatrix Concepts Holdings BhdMatrix Concepts Holdings Bhd :::: Matrix Concepts is one of the largest developers in Negeri Sembilan, focusing on its flagship township development, Bandar Sri Sendayan which covers 2,350 acres

MKH BerhadMKH BerhadMKH BerhadMKH Berhad :::: MKH is an established township developer in Kajang/Semenyih and Greater Klang Valley. Its 16k ha oil palm estates in Indonesia has started to contribute significantly

Weak consumer sentiment

Source: AllianceDBS, BNM, MIER

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

60

70

80

90

100

110

120

130

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

MIER consumer sentiment (LHS)

Total approved property loan growth (RHS)

DBS Group Research . Equity DBS Group Research . Equity DBS Group Research . Equity DBS Group Research . Equity

9 Mar 2017

Malaysia Industry Focus

Malaysia Property Refer to important disclosures at the end of this report

Price Price Price Price Mkt CapMkt CapMkt CapMkt Cap Target PriceTarget PriceTarget PriceTarget Price Performance (%)Performance (%)Performance (%)Performance (%)

RMRMRMRM US$mUS$mUS$mUS$m RMRMRMRM 3 mth3 mth3 mth3 mth 12 mth12 mth12 mth12 mth RatingRatingRatingRating

SP Setia 3.39 2,172 3.50 1.8 9.4 HOLD Sunway Bhd 3.16 1,436 3.00 6.8 3.6 HOLD UEM Sunrise Bhd 1.21 1,233 1.10 18.6 16.4 HOLD Eco World 1.55 823 1.80 12.3 20.2 BUY Eastern & Oriental Bhd

1.89 533 1.20 26.9 18.1 FV Matrix Concepts Holdings Bhd

2.51 322 3.10 2.5 4.2 BUY MKH Berhad 2.95 278 3.70 2.4 30.5 BUY

Industry Focus

Page 2

Down but not out

While the property market has been in a lull since 2015, it is

unlikely to improve in 2017 given the persistently weak

sentiment. It remains a buyer’s market given the huge

incoming supply which will cap property price appreciation.

Worse still, buyers may continue to adopt a wait-and-see

attitude in anticipation of lower selling prices. Low affordability

remains one of the most common issues voiced out by

property buyers as property prices remain stubbornly high

though appreciation growth has slowed down considerably.

Property prices have not come down despite the much-talked

about gloom and doom in the market, largely driven by the

poor sentiment in the property market. According to National

Property Information Centre (NAPIC), 3Q16 property prices

grew 5.3% y-o-y which marks the slowest growth since 2010,

reflecting the weak sentiment in the Malaysian property

market. Nevertheless, demand from genuine homebuyers

remains robust, underpinned by relatively healthy economic

growth which is projected at 4.5% for 2017 while

unemployment rate stays at c.3.5%.

Weak sentiment since 2014

Source: AllianceDBS, BNM, MIER

We believe the outlook in 2017 will be similar to that of 2016

where developers continue to compete aggressively in a

subdued property market. Declining property sales is expected

to be the same key challenge for the sector though individual

developers with niche expertise and brand names could buck

the trend. Developers have been facing difficulties in

converting their initial high bookings into sales because of

stricter bank lending policies, as banks become more cautious

towards the property sector. This is despite the keen interest

shown by potential home buyers, especially genuine home-

occupiers who may be purchasing properties for the first time

or upgrading to better homes.

Quarterly house price index remains at elevated levels

Source: AllianceDBS, NAPIC

Slower growth of house price index

Source: AllianceDBS, NAPIC

In the near term, property price appreciation potential will be

capped given the stiff competition and rising incoming supply

which has been reflected in the slower growth over the past

few quarters. The healthy consolidation has resulted in

developers being more prudent and selective with their

launches as well as product offerings in the current buyers’

market. We believe property price growth will remain subdued

in 2017, converging towards its long-term average growth rate

of ~5%.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

60

70

80

90

100

110

120

130

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

MIER consumer sentiment (LHS)

Total approved property loan growth (RHS)

100

120

140

160

180

200

220

240

260

280

1Q00

4Q00

3Q01

2Q02

1Q03

4Q03

3Q04

2Q05

1Q06

4Q06

3Q07

2Q08

1Q09

4Q09

3Q10

2Q11

1Q12

4Q12

3Q13

2Q14

1Q15

4Q15

3Q16

2000=1002000=1002000=1002000=100

All Terraced High-rise

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1Q00

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

1Q09

1Q10

1Q11

1Q12

1Q13

1Q14

1Q15

1Q16

2000=1002000=1002000=1002000=100

All Terraced High-rise

Industry Focus

Page 3

Intensifying competition

Recall that the highly successful developer interest-bearing

scheme (DIBS) was banned effective January 2014, and

developers had capitalised on the last window in 2013 to

launch more development projects with DIBS. We believe more

completions will be expected in 2017 especially for high-rise

units which typically take between three to four years before

delivery.

Potential property buyers may not be willing to actively look

for their choice units in view of the relatively soft sentiment.

Also, investors could be discouraged by the subdued capital

appreciation in recent years, despite the generous freebies

offered by developers for newly launched projects. We

understand that a 10%-15% discount to the listed selling price

has increasingly become the norm in the property market as

take-up remains uninspiring, compared to the good years back

in 2011-2013.

Meanwhile, the federal government has been stepping up its

efforts in accelerating supply of affordable housing to the

masses, especially under the 1Malaysia People’s Housing

Programme (PR1MA). Recently, the monthly income eligibility

to purchase PR1MA houses was increased from RM10,000 to

RM15,000 while the moratorium has been cut to five years

from ten years previously.

Therefore, more middle-income households will be eligible to

purchase these houses in key urban centres which are sold at

between RM100,000 and RM400,000. This will indirectly pose

more competition to private developers as they will have to

revise their product offerings to incorporate more ‘value-buy’

properties with differentiating lifestyle amenities that will

distinguish themselves from lower-priced public housing,

which could come at the expense of margins.

The government has also come out with a special end-

financing scheme named Skim Pembiayaan Fleksibel (SPEF)

which is created exclusively for PR1MA buyers in collaboration

with Bank Negara Malaysia, Employees Provident Fund and

four local banks, namely Maybank, CIMB, RHB and AmBank.

SPEF allows borrowers to only service their interest in the first

five years, and the principal amount only kicks in from year six

onwards.

New supply coming on stream

*HPI – House Price Index

Source: AllianceDBS, NAPIC

Comple tionsComple tionsComple tionsComple tions

% of % of % of % of

stoc kstoc kstoc kstoc k

Incoming Incoming Incoming Incoming

supp lysupp lysupp lysupp ly

% of % of % of % of

s tocks tocks tocks tock Exis ting s tockExi s ting s tockExi s ting s tockExi s ting s tock HPIHPIHPIHPI

HPI HPI HPI HPI

growthgrowthgrowthgrowth

2002 156,042 5.1% 605,566 19.9% 3,050,421 104

2003 192,490 5.9% 627,028 19.1% 3,287,733 108 4.0%

2004 165,964 4.8% 641,771 18.5% 3,467,812 113 4.8%

2005 180,600 4.9% 637,208 17.3% 3,680,462 116 2.4%

2006 171,448 4.4% 619,583 16.0% 3,864,432 118 1.9%

2007 181,123 4.5% 573,716 14.1% 4,063,167 124 5.3%

2008 136,881 3.2% 557,502 13.2% 4,220,510 130 4.7%

2009 103,335 2.4% 538,894 12.4% 4,338,609 132 1.5%

2010 99,866 2.2% 533,605 12.0% 4,446,085 141 6.8%

2011 65,866 1.4% 533,844 11.7% 4,547,971 155 9.9%

2012 72,247 1.6% 628,655 13.5% 4,640,269 173 11.8%

2013 78,265 1.7% 696,557 14.8% 4,718,534 193 11.6%

2014 107,747 2.2% 769,788 15.9% 4,848,030 211 9.4%

2015 80,850 1.6% 892,099 18.1% 4,928,883 227 7.4%

9M16 39,791 0.8% 837,251 17.1% 4,906,722 242 6.6%

Industry Focus

Page 4

Developers remain cautious

Developers have also been guiding for relatively flattish sales

target in FY17, in tandem with our view that the property

market remains subdued this year. We believe the property

market will remain lacklustre in 2017, driven by persistently

weak sentiment, low affordability and accelerating incoming

supply despite the recent share price recovery for property

developers.

Sales target for developers under our coverage

Source: AllianceDBS, Companies

Developers’ priority lies in sustaining their property sales

momentum which is increasingly challenged by the soft

market. Therefore, attractive product offerings with strong

value propositions are critical to replenish unbilled sales. We

believe larger developers with diversified geographical

concentration and township exposure will be in a better

position to weather the market downturn. This is especially so

for those with large land banks acquired years ago at much

lower prices which will enable them to price their products

competitively.

Market share of property transactions by price range

Source: AllianceDBS, NAPIC

While the property market has been rather lacklustre compared

to the past few years, the overall house price index remains on

the uptrend, albeit at a slower pace. Affordable landed

properties with ready infrastructure and amenities remain in

demand, as attested by some of the recent launches.

Developments that are integrated with current or planned public

rail stations continue to be sought after. Property buyers have

been increasingly seeking value-adding properties as more

affluent buyers continue to upgrade their lifestyle.

We believe the bulk of launches from developers this year will

still be affordable housing priced below RM700,000 which

remains the most sellable products under this subdued

property market. Also, demand for affordable housing

remains healthy, especially at certain emerging growth

corridors with huge population catchments such as

Kajang/Semenyih, Sungai Buloh/Denai Alam and

Dengkil/Salak Tinggi.

Meanwhile, the difficulties faced by developers in converting

their initial high bookings to sales will remain unchanged this

year as banks stay cautious towards the property sector. Despite

the keen interest shown by potential home buyers, especially

genuine home-occupiers who may be purchasing properties for

the first time or upgrading to better homes, banks are most

likely to continue adopting strict lending policies.

Property s a le sProperty s a le sProperty s a le sProperty s a le s

RMmRMmRMmRMm FY14AFY14AFY14AFY14A FY15AFY15AFY15AFY15A FY16AFY16AFY16AFY16A FY17FY17FY17FY17

UEM Sunrise 2,443 2,357 1,369 1,200

SP Setia 4,623 *4320 3,823 4,000

Sunway 1,711 1,210 1,173 1,100

E&O 730 940 1,101 n.a.

MKH 820 835 776 700-900

Eco World 3,186 3,016 3,820 4,000

Matrix 630 ~974.2 n.a. 1,000

*14-month period ended Dec15

~15-month period ended Mar16

87% 85% 83% 83% 81% 78% 75% 72%

60%53%

61%

9% 11% 12% 12% 14% 15% 16% 18%

27%31%

25%

2% 3% 3% 4% 4% 5% 6% 7% 9% 11% 11%

0%

20%

40%

60%

80%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

<250k 250-500k 500k-1m

Industry Focus

Page 5

Investment strategy

Our key property picks in 2017 are Eco World, MKHEco World, MKHEco World, MKHEco World, MKH and

MatrixMatrixMatrixMatrix which are township developers with niche expertise

and established brand names within local communities. The

trio has achieved their respective commendable sales targets

in FY16 despite a fair share of downward revisions by their

peers amidst the challenging environment.

Eco World (Eco World (Eco World (Eco World (BUYBUYBUYBUY, RM1.80 TP), RM1.80 TP), RM1.80 TP), RM1.80 TP). Eco World remains the one-of-

its-kind premium developer with aggressive expansion plans

despite being a relatively new property developer with only

three years of history. It has been able to sell properties at an

unprecedented pace, reflecting property buyers’ confidence in

the group’s strong brand name.

After booking RM3.2bn/RM3.0bn/RM3.8bn gross sales in

FY14 -FY16, respectively, ECW is targeting RM4bn gross sales

in FY17 (including JV portion) despite the relatively weak

property market where most of its peers are having slower

sales performance. ECW has clearly been gaining more

market share at the expense of its competitors.

We are projecting an explosive 3-year earnings CAGR of 33%

over FY16-19F, due to its relatively smaller profit base at this

juncture. This is supported by its all-time high unbilled sales of

RM4.9bn as at end-October 2016 which will underpin

earnings up to FY19.

MKH (MKH (MKH (MKH (BUYBUYBUYBUY, RM3., RM3., RM3., RM3.77770 TP)0 TP)0 TP)0 TP). The company will be the largest

beneficiary of the upcoming MRT connectivity given its high

exposure to the booming Kajang/Semenyih growth corridor.

MKH has an unrivalled competitive advantage in

Kajang/Semenyih property development because of their low

land cost of RM10psf (vs peers’ >RM20psf).

Affordable homes - MKH’s stronghold - remains the key

theme for the property sector. The company's large tract of

property land bank in Kajang/Semenyih (490 acres) makes it

the prime beneficiary of rising land prices there. Scarcity of

land within Kajang also provides a distinct advantage for

MKH’s future launches, which are expected to see strong

demand and fetch premium pricing.

Matrix Concepts (Matrix Concepts (Matrix Concepts (Matrix Concepts (BUY, RM3.1BUY, RM3.1BUY, RM3.1BUY, RM3.10 TP)0 TP)0 TP)0 TP). Matrix has bucked the

trend with record-high property sales at its two flagship

projects, Bandar Sri Sendayan (BSS) in Seremban and Bandar

Sri Impian (BSI) in Kluang, despite the relatively weak market

sentiment. The majority of its launches are priced below the

RM600k/unit mark, leveraging on the robust demand for

affordable homes. The sales momentum going forward is

likely to remain on the uptrend as Matrix still has a large

pipeline of affordable homes which are ready for launch.

BSS remains its jewel in the crown given the low average land

cost of RM7psf (with infrastructure in place) when its

affordably-priced properties are already selling at ~RM200psf,

leading to significantly higher-than-average profit margins.

It is on track to hit management’s target of RM1bn in FY17. This

reinforces our view that the strong sales momentum for its

flagship projects in BSS, Seremban and BSI, Kluang. Unbilled

sales stood at an all-time high of RM903m as at end-December

2016 which will provide strong earnings visibility over the next

two years

Industry Focus

Page 6

Risk

ForeclosuresForeclosuresForeclosuresForeclosures. This would be largely driven by several

completed schemes entering the market, for which the units

were purchased with small down payments a few years ago.

Buyers may not be able to flip at the high margins they had

expected earlier, and they may not want to go ahead with the

mortgage payments. Foreclosures could also arise from

incidences of rentals not being able to cover mortgage

payments. Buyers with weak holding power will face

foreclosure risk.

Margin compression. Margin compression. Margin compression. Margin compression. Developers may not be able to pass on

incremental land and construction costs to property buyers, as

the market may not be receptive to higher selling prices amid

record-high house prices. Also, the steep depreciation of the

MYR could result in higher cost of imported materials for

some projects.

Slowing salesSlowing salesSlowing salesSlowing sales. Property sales may slow down in some

locations as property buyers may be deterred by the high

entry price and tightening measures, with banks adopting

more cautious lending practices for mortgage loans.

Rising household debtRising household debtRising household debtRising household debt. The currently elevated household debt

level could strain purchasing power and the demand for

future properties, in view of the rising inflationary pressure

and unaffordability.

Peer comparison

Market Market Market Market capcapcapcap

RNAV RNAV RNAV RNAV discountdiscountdiscountdiscount

PEPEPEPE

PBPBPBPB

ROEROEROEROE CompanyCompanyCompanyCompany FYEFYEFYEFYE RatingRatingRatingRating PricePricePricePrice TPTPTPTP FFFFY1Y1Y1Y17777 FFFFY1Y1Y1Y18888 FFFFY1Y1Y1Y17777 FFFFY1Y1Y1Y18888 FFFFY1Y1Y1Y17777 FFFFY1Y1Y1Y18888

(RM)(RM)(RM)(RM) (RM)(RM)(RM)(RM) ((((RMmRMmRMmRMm))))

SP Setia Dec Hold 3.40 3.50 9,702 42% 12.4 14.3 1.0 1.0 8% 7%

Sunway Dec Hold 3.16 3.00 6,401 27% 10.3 9.8 0.8 0.7 7% 7%

UEM Sunrise Dec Hold 1.23 1.10 5,581 66% 27.5 19.4 0.9 0.8 3% 4%

Eco World Oct Buy 1.50 1.80 4,417 33% 31.2 20.0 1.1 1.0 3% 5%

E&O Mar FV 1.91 1.20 2,401 51% 49.5 45.4 1.4 1.4 3% 3%

Matrix Concepts Nar Buy 2.51 3.10 1,437 43% 6.9 6.1 1.5 1.3 14% 14%

MKH Sep Buy 2.99 3.70 1,259 48% 6.8 7.2 0.9 0.9 13% 12%

AverageAverageAverageAverage 44%44%44%44% 20.7 20.7 20.7 20.7 17.5 17.5 17.5 17.5 1.1 1.1 1.1 1.1 1.0 1.0 1.0 1.0 7%7%7%7% 7%7%7%7%

Source: AllianceDBS, Bloomberg Finance L.P.

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:BC, PY

BUYBUYBUYBUY Last Traded PriceLast Traded PriceLast Traded PriceLast Traded Price (((( 8 Mar 20178 Mar 20178 Mar 20178 Mar 2017)))): : : : RM1.55 (KLCIKLCIKLCIKLCI : : : : 1,725.54) Price TaPrice TaPrice TaPrice Target rget rget rget 12121212----mthmthmthmth:::: RM1.80 (16% upside) (Prev RM1.80)

Potential Catalyst: Potential Catalyst: Potential Catalyst: Potential Catalyst: Stronger-than-expected sales and profit margins

Where we differ:Where we differ:Where we differ:Where we differ: Among highest TP, bullish on company prospects

Analyst QUAH He Wei, CFA +603 2604 3966 [email protected]

What’s New • FY16 record profit met expectations

• Overwhelming demand with RM3.8bn sales

(Malaysian projects only) achieved in FY16

• Revise FY17-18F earnings by -28%/-22% to

account for initial losses from JVs/associates

• Maintain BUY and RM1.80 TP

Price Relative

Forecasts and Valuation FY FY FY FY OctOctOctOct ((((RMRMRMRM m) m) m) m) 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF

Revenue 2,546 2,995 3,303 3,656 EBITDA 247 360 513 645 Pre-tax Profit 193 206 322 435 Net Profit 129 142 222 300 Net Pft (Pre Ex.) 129 142 222 300 Net Pft Gth (Pre-ex) (%) 194.1 10.0 56.2 35.2 EPS (sen) 5.47 4.81 7.52 10.2 EPS Pre Ex. (sen) 5.47 4.81 7.52 10.2 EPS Gth Pre Ex (%) 194 (12) 56 35 Diluted EPS (sen) 5.47 4.81 7.52 10.2 Net DPS (sen) 0.0 0.0 0.0 0.0 BV Per Share (sen) 160 142 150 160 PE (X) 25.2 28.7 18.4 13.6 PE Pre Ex. (X) 25.2 28.7 18.4 13.6 P/Cash Flow (X) 13.6 5.5 14.5 18.3 EV/EBITDA (X) 22.5 17.7 13.0 10.9 Net Div Yield (%) 0.0 0.0 0.0 0.0 P/Book Value (X) 0.9 1.0 0.9 0.9 Net Debt/Equity (X) 0.6 0.5 0.6 0.6 ROAE (%) 3.7 3.6 5.2 6.6 Earnings Rev (%):Earnings Rev (%):Earnings Rev (%):Earnings Rev (%): (28) (22) N/A Consensus EPS Consensus EPS Consensus EPS Consensus EPS (sensensensen):::: 9.00 11.0 N/A Other Broker Recs:Other Broker Recs:Other Broker Recs:Other Broker Recs: B: 7 S: 0 H: 2

Source of all data on this page: Company, AllianceDBS, Bloomberg Finance L.P

In a class of its own The undisputed industry leader. The undisputed industry leader. The undisputed industry leader. The undisputed industry leader. A relatively new property developer with only three years of history, Eco World Development (ECW) has been able to sell properties at an unprecedented pace, reflecting property buyers’ confidence in the group’s strong brand name. After booking RM3.2bn/RM3.0bn/RM3.8bn gross sales in FY14 -FY16, respectively, ECW is targeting RM4bn gross sales in FY17 (including JV portion) despite the relatively weak property market where most of its peers are having slower sales performance. ECW has clearly been gaining more market share at the expense of its competitors. Explosive growth aheadExplosive growth aheadExplosive growth aheadExplosive growth ahead. We are projecting an explosive 3-year earnings CAGR of 33% over FY16-19F, due to its relatively smaller profit base at this juncture. This is supported by its all-time high unbilled sales of RM4.9bn as at end-Oct 16 which will underpin earnings up to FY19. In anticipation of better cashflow with the hand-over of completed units as well as the completion of a proposed private placement by 1QCY17, ECW’s balance sheet is expected to remain healthy and accommodative for its aggressive expansion plans. Listing of Eco World International by 1QCY17. Listing of Eco World International by 1QCY17. Listing of Eco World International by 1QCY17. Listing of Eco World International by 1QCY17. ECW is looking to venture overseas via a proposed subscription of a 27% stake in Eco World International (EWI) which has significant exposure to London and Sydney. This will further cement its earnings growth from FY18 onwards upon completion of projects, though EWI will incur losses in FY17.

Valuation:

We maintain our TP of RM1.80, based on a 20% discount to

our RNAV. We believe ECW deserves to trade at a lower

discount relative to its peers given its prominence as the

bellwether of the Malaysian property sector with ongoing

outperformance in a weak market. We continue to like ECW

for the proven and impeccable track record of its key senior

executives, who have helped the developer to establish strong

brand recognition among property buyers.

Key Risks to Our View:

Relatively weaker property sentiment. Relatively weaker property sentiment. Relatively weaker property sentiment. Relatively weaker property sentiment. The surge in property

prices over the last few years could weaken property sales as

buyers turn more cautious.

At A Glance Issued Capital (m shrs) 2,364

Mkt. Cap (RMm/US$m) 3,263 / 737

Major Shareholders (%)

Sinarmas Harta Sdn Bhd 33.0

Liew Tian Xiong 18.3

Eco World Development Holdings Sdn Bhd 15.7

Free Float (%) 26.2

3m Avg. Daily Val (US$m) 0.46

ICB IndustryICB IndustryICB IndustryICB Industry : Financials / Real Estate Investment & Services

DBS Group Research . Equity

9 Mar 2017

Malaysia Company Guide

Eco World Development Version 6 | Bloomberg: ECW MK | Reuters: ECOW.KL Refer to important disclosures at the end of this report

ASIAN INSIGHTS VICKERS SECURITIES

Page 8

Company Guide

Eco World Development

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

Sustainable sales momentum. Sustainable sales momentum. Sustainable sales momentum. Sustainable sales momentum. Eco World Development (ECW) is

projected to continue recording strong sales for its well-planned

township developments, as evidenced by its strong FY16 sales

of RM3.8bn. This underscores the strong market confidence

that buyers have in its brand name which continues to garner

impressive sales despite the weaker sentiment on the property

market.

Aggressive marketing campaigns as the group gears up for Aggressive marketing campaigns as the group gears up for Aggressive marketing campaigns as the group gears up for Aggressive marketing campaigns as the group gears up for

more launches. more launches. more launches. more launches. Over the past two years, ECW has been

ramping up marketing efforts by opening more sales galleries at

its various township projects to better service prospective

buyers. Infrastructure has improved at project sites as we

understand the group is gearing itself towards the successful

launches of its new township projects. This has resulted in a

relatively weak pretax margin of 4.3% in FY15 but it improved

to 7.6% in FY16. It is most likely to further improve going

forward as most of its township projects have only been

launched over the past two years.

RM4bn FY17RM4bn FY17RM4bn FY17RM4bn FY17 sales target. sales target. sales target. sales target. Given the overwhelming response for

ECW’s launches in FY15-16, the group has set an FY17 gross

sales target of RM4bn. This will be anchored by 15 ongoing

projects in Malaysia. Its focus on township projects with gated-

and-guarded strata-titled homes will offer healthy and

sustainable long-term demand as the township matures. Eco-

friendly amenities and impressive landscaping features

commonly found in ECW’s townships will continue to attract

overwhelming response to its properties.

Strong earnings visibilityStrong earnings visibilityStrong earnings visibilityStrong earnings visibility. As at end-Oct 16, ECW had RM4.9bn

in unbilled sales which will support earnings visibility for the

next three years. After the aggressive launches over the past

two years, the group is now the leading developer in Malaysia.

Its established brand name has become a household name with

a strong following by both investors and home-occupiers.

Brighter longBrighter longBrighter longBrighter long----term prospects.term prospects.term prospects.term prospects. As ECW is still a relatively young

developer, its near-term earnings may not be exciting given the

upfront cost to be incurred for its marketing campaigns as well

as infrastructure improvements for its township projects.

Nevertheless, once its projects go into full swing over the

coming years, the townships can turn into self-sustaining

developments which will generate even stronger interest among

property buyers.

Property sales

Revenue (RMm)

EBIT (RMm)

EBIT Margin %

Pretax margin %

Source: Company, AllianceDBS

ASIAN INSIGHTS VICKERS SECURITIES

Page 9

Company Guide

Eco World Development

Balance Sheet:

Healthy balance sheet. Healthy balance sheet. Healthy balance sheet. Healthy balance sheet. ECW’s massive corporate exercise to

raise RM2.8bn total proceeds was completed on 19 May 2015.

We estimate that ECW’s net gearing will remain healthy at 0.5x

by end-FY17, taking into consideration its aggressive

acquisitions over the past two years. With its unbilled sales of

RM4.9bn, gearing is likely to improve further as the projects are

delivered progressively.

Share Price Drivers:

Earnings delivery a key reEarnings delivery a key reEarnings delivery a key reEarnings delivery a key re----rating catalyst. rating catalyst. rating catalyst. rating catalyst. While ECW has done

well with its strong property sales in FY14-16, the relatively

young company has yet to deliver on earnings. We believe that

investors will have more confidence in the company as ECW

continues to deliver on earnings growth. Given the strong brand

name and innovative township developments, ECW is poised to

deliver strong earnings CAGR of 33% over FY16-19F. While

margins may appear low at this juncture as its townships are still

at the infancy stages of development, looking ahead, we expect

increased profitability and margin expansion for future launch

phases as these projects mature.

Listing of Eco World International (EWI). Listing of Eco World International (EWI). Listing of Eco World International (EWI). Listing of Eco World International (EWI). ECW will also venture

into the overseas market via a proposed 27% participation in

Eco World International which will be floated on Bursa Malaysia

to raise RM2bn proceeds by 1QCY17. EWI has a 75% stake in

three projects in the UK with an estimated GDV of £2.257bn

(~RM13.2bn) and a mixed development project in Sydney worth

A$300m. The listing will help to raise ECW’s profile as a

successful international developer.

Key Risks:

Weaker property sentiment. Weaker property sentiment. Weaker property sentiment. Weaker property sentiment. The surge in property prices over

the last few years, coupled with recent tightening measures,

could weaken property sales as buyers turn more cautious.

Tighter bank lending. Tighter bank lending. Tighter bank lending. Tighter bank lending. Stricter lending guidelines by banks as a

result of rising household debt could lead to softer sales.

Company Background

ECW (formerly known as Focal Aims) is a relatively new

property developer, helmed by the former top executives of SP

Setia. Since the takeover by Eco World Development Holdings

Sdn Bhd (EWH) and Liew Tian Xiong (eldest son of Tan Sri Liew

Kee Sin – founder of SP Setia) in Nov 13, ECW has acquired

development rights of eight subsidiaries from Eco World

Development Sdn Bhd (EWSB; 50% owned by EWH) that has

positioned the group as the fastest-rising property developer in

Malaysia. ECW currently owns 8,052 acres of landbank across

property hotspots in the Klang Valley, Iskandar Malaysia and

Penang which are worth RM87bn GDV.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, AllianceDBS

ASIAN INSIGHTS VICKERS SECURITIES

Page 10

Company Guide

Eco World Development

Key Assumptions

FY FY FY FY OctOctOctOct 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF

Property sales 3,016 3,820 4,084 4,398 5,107

Revenue (RMm) 1,712 2,546 2,995 3,303 3,656

EBIT (RMm) 96.3 231 366 472 562

EBIT Margin % 5.63 9.08 12.2 14.3 15.4

Pretax margin % 4.32 7.59 6.88 9.75 11.9 Income Statement (RMm)

FY FY FY FY OctOctOctOct 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF Revenue 1,712 2,546 2,995 3,303 3,656

Cost of Goods Sold (1,300) (1,951) (2,180) (2,336) (2,546)

Gross ProfitGross ProfitGross ProfitGross Profit 412412412412 595595595595 815815815815 967967967967 1,1101,1101,1101,110 Other Opng (Exp)/Inc (316) (364) (449) (495) (548)

Operating ProfitOperating ProfitOperating ProfitOperating Profit 96.396.396.396.3 231231231231 366366366366 472472472472 562562562562 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0

Associates & JV Inc (2.1) (7.1) (30.7) 13.4 53.0

Net Interest (Exp)/Inc (20.3) (31.0) (129) (163) (179)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

PrePrePrePre----tax Profittax Profittax Profittax Profit 73.973.973.973.9 193193193193 206206206206 322322322322 435435435435 Tax (30.1) (63.9) (63.9) (99.8) (135)

Minority Interest 0.10 0.0 0.0 0.0 0.0

Preference Dividend 0.0 0.0 0.0 0.0 0.0

Net ProfitNet ProfitNet ProfitNet Profit 44.044.044.044.0 129129129129 142142142142 222222222222 300300300300 Net Profit before Except. 44.0 129 142 222 300

EBITDA 111 247 360 513 645

Growth

Revenue Gth (%) 1,053.7 48.7 17.6 10.3 10.7

EBITDA Gth (%) 639.9 121.7 45.8 42.4 25.8

Opg Profit Gth (%) 539.3 140.1 58.1 29.0 19.1

Net Profit Gth (Pre-ex) (%) 512.1 194.1 10.0 56.2 35.2

Margins & Ratio

Gross Margins (%) 24.1 23.4 27.2 29.3 30.4

Opg Profit Margin (%) 5.6 9.1 12.2 14.3 15.4

Net Profit Margin (%) 2.6 5.1 4.7 6.7 8.2

ROAE (%) 2.5 3.7 3.6 5.2 6.6

ROA (%) 1.2 1.6 1.5 2.3 3.0

ROCE (%) 1.9 2.5 3.5 4.2 4.8

Div Payout Ratio (%) 0.0 0.0 0.0 0.0 0.0

Net Interest Cover (x) 4.7 7.5 2.8 2.9 3.1

Source: Company, AllianceDBS

Dragged by initial losses from JVs/associates

In line with management’s target of RM4bn

ASIAN INSIGHTS VICKERS SECURITIES

Page 11

Company Guide

Eco World Development

Quarterly / Interim Income Statement (RMm)

FY FY FY FY OctOctOctOct 4Q4Q4Q4Q2015201520152015 1Q1Q1Q1Q2016201620162016 2Q2Q2Q2Q2016201620162016 3Q3Q3Q3Q2016201620162016 4Q4Q4Q4Q2016201620162016 Revenue 682 464 615 727 741

Cost of Goods Sold (513) (354) (467) (571) (559)

Gross ProfitGross ProfitGross ProfitGross Profit 169169169169 110110110110 148148148148 156156156156 182182182182 Other Oper. (Exp)/Inc (132) (73.5) (87.4) (79.7) (118)

Operating ProfitOperating ProfitOperating ProfitOperating Profit 37.037.037.037.0 36.236.236.236.2 60.260.260.260.2 76.376.376.376.3 64.164.164.164.1 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0

Associates & JV Inc 0.0 (1.9) (1.7) (2.1) (7.1)

Net Interest (Exp)/Inc (2.2) (3.1) (6.7) (7.5) (13.6)

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0

PrePrePrePre----tax Profittax Profittax Profittax Profit 34.934.934.934.9 31.231.231.231.2 51.951.951.951.9 66.866.866.866.8 43.443.443.443.4 Tax (15.2) (10.5) (17.2) (22.2) (14.0)

Minority Interest 0.0 0.0 0.0 0.0 0.0

Net ProfitNet ProfitNet ProfitNet Profit 19.719.719.719.7 20.720.720.720.7 34.734.734.734.7 44.644.644.644.6 29.329.329.329.3 Net profit bef Except. 19.7 20.7 34.7 44.6 29.3

EBITDA 37.0 34.3 58.5 74.3 57.0

Growth

Revenue Gth (%) 50.1 (32.0) 32.6 18.3 1.9

EBITDA Gth (%) 79.5 (7.4) 70.6 26.9 (23.3)

Opg Profit Gth (%) 79.5 (2.2) 66.2 26.8 (16.1)

Net Profit Gth (Pre-ex) (%) 109.7 5.0 67.8 28.6 (34.2)

Margins

Gross Margins (%) 24.7 23.7 24.0 21.4 24.5

Opg Profit Margins (%) 5.4 7.8 9.8 10.5 8.6

Net Profit Margins (%) 2.9 4.5 5.6 6.1 4.0 Balance Sheet (RMm)

FY FY FY FY OctOctOctOct 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF Net Fixed Assets 176 213 287 360 429

Invts in Associates & JVs 0.0 486 455 469 522

Other LT Assets 3,774 4,245 5,145 5,645 6,145

Cash & ST Invts 517 573 981 663 286

Inventory 25.4 24.9 99.8 110 122

Debtors 735 965 749 826 914

Other Current Assets 1,709 2,336 2,027 1,768 1,954

Total AssetsTotal AssetsTotal AssetsTotal Assets 6,9376,9376,9376,937 8,8428,8428,8428,842 9,7449,7449,7449,744 9,8409,8409,8409,840 10,37110,37110,37110,371

ST Debt

436 817 817 817 817

Creditor 1,533 1,954 1,997 1,835 2,031

Other Current Liab 12.0 14.8 63.9 99.8 135

LT Debt 1,264 2,045 2,445 2,445 2,445

Other LT Liabilities 534 224 224 224 224

Shareholder’s Equity 3,157 3,787 4,197 4,419 4,719

Minority Interests 0.0 0.0 0.0 0.0 0.0

Total Cap. & Liab.Total Cap. & Liab.Total Cap. & Liab.Total Cap. & Liab. 6,9376,9376,9376,937 8,8428,8428,8428,842 9,7449,7449,7449,744 9,8409,8409,8409,840 10,37110,37110,37110,371

Non-Cash Wkg. Capital 924 1,356 815 769 824

Net Cash/(Debt) (1,183) (2,288) (2,281) (2,599) (2,976)

Debtors Turn (avg days) 103.1 121.8 104.4 87.0 86.8

Creditors Turn (avg days) 225.1 330.0 334.6 303.0 280.5

Inventory Turn (avg days) 10.7 4.8 10.6 16.6 16.8

Asset Turnover (x) 0.4 0.3 0.3 0.3 0.4

Current Ratio (x) 1.5 1.4 1.3 1.2 1.1

Quick Ratio (x) 0.6 0.6 0.6 0.5 0.4

Net Debt/Equity (X) 0.4 0.6 0.5 0.6 0.6

Net Debt/Equity ex MI (X) 0.4 0.6 0.5 0.6 0.6

Capex to Debt (%) 4.1 1.7 3.1 3.1 3.1

Z-Score (X) 1.0 0.9 1.1 1.2 1.2

Source: Company, AllianceDBS

4QFY16 results in line

Healthy balance sheet

ASIAN INSIGHTS VICKERS SECURITIES

Page 12

Company Guide

Eco World Development

Cash Flow Statement (RMm)

FY FY FY FY OctOctOctOct 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF Pre-Tax Profit 73.9 193 206 322 435

Dep. & Amort. 17.2 22.9 25.2 27.7 30.5

Tax Paid (64.0) (112) (14.8) (63.9) (99.8)

Assoc. & JV Inc/(loss) 2.06 7.07 30.7 (13.4) (53.0)

Chg in Wkg.Cap. 224 199 492 9.46 (89.7)

Other Operating CF (56.5) (69.9) 0.0 0.0 0.0

Net Operating CFNet Operating CFNet Operating CFNet Operating CF 197197197197 240240240240 740740740740 282282282282 223223223223 Capital Exp.(net) (69.0) (47.8) (100.0) (100.0) (100.0)

Other Invts.(net) (2,990) (1,409) (900) (500) (500)

Invts in Assoc. & JV 0.0 (466) 0.0 0.0 0.0

Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0

Other Investing CF (438) 70.3 0.0 0.0 0.0

Net Investing CFNet Investing CFNet Investing CFNet Investing CF (3,498)(3,498)(3,498)(3,498) (1,853)(1,853)(1,853)(1,853) (1,000)(1,000)(1,000)(1,000) (600)(600)(600)(600) (600)(600)(600)(600) Div Paid 0.0 0.0 0.0 0.0 0.0

Chg in Gross Debt 914 1,151 400 0.0 0.0

Capital Issues 2,798 501 268 0.0 0.0

Other Financing CF (11.9) (0.3) 0.0 0.0 0.0

Net Financing CFNet Financing CFNet Financing CFNet Financing CF 3,7013,7013,7013,701 1,6521,6521,6521,652 668668668668 0.00.00.00.0 0.00.00.00.0

Currency Adjustments 73.8 17.6 0.0 0.0 0.0

Chg in Cash 474 56.3 407 (318) (377)

Opg CFPS (sen) (1.2) 1.73 8.36 9.21 10.6

Free CFPS (sen) 5.41 8.14 21.6 6.15 4.17

Source: Company, AllianceDBS

Target Price & Ratings History

Source: AllianceDBS

Analyst: QUAH He Wei, CFA

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:BC, PY

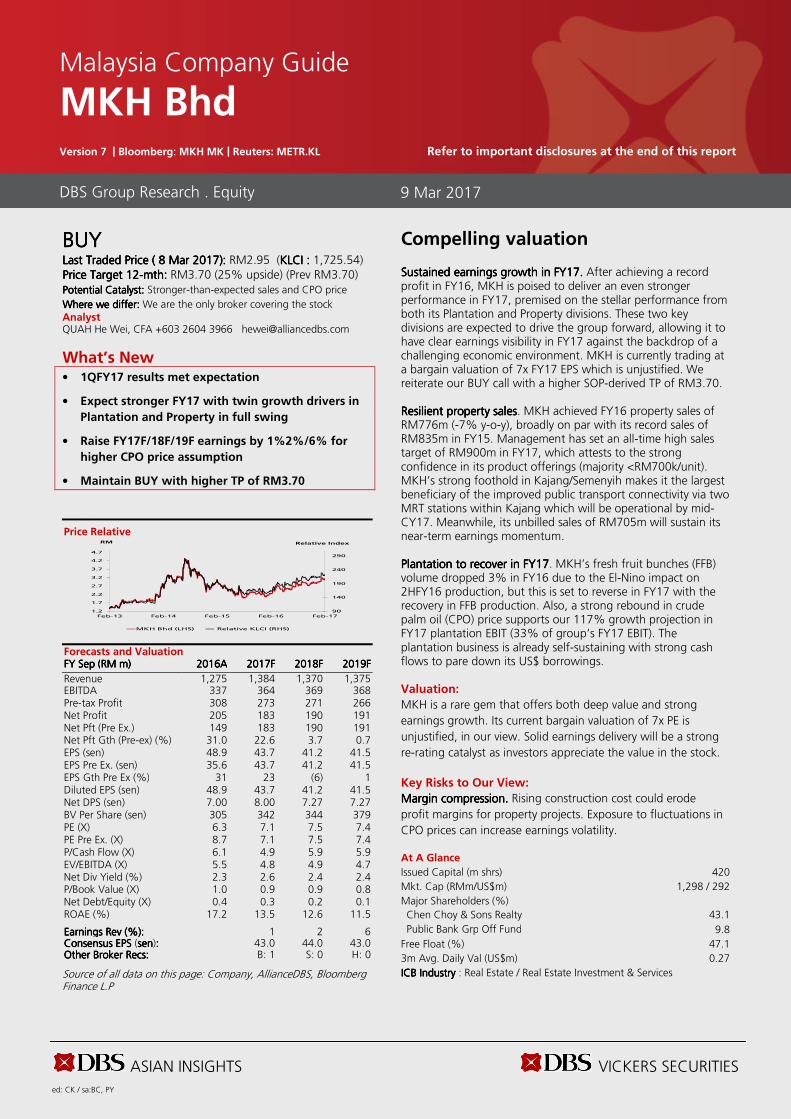

BUYBUYBUYBUY Last Traded PriceLast Traded PriceLast Traded PriceLast Traded Price (((( 8 Mar 20178 Mar 20178 Mar 20178 Mar 2017)))): : : : RM2.95 (KLCIKLCIKLCIKLCI : : : : 1,725.54) Price Target Price Target Price Target Price Target 12121212----mthmthmthmth:::: RM3.70 (25% upside) (Prev RM3.70) Potential Catalyst: Potential Catalyst: Potential Catalyst: Potential Catalyst: Stronger-than-expected sales and CPO price

Where we differ:Where we differ:Where we differ:Where we differ: We are the only broker covering the stock Analyst QUAH He Wei, CFA +603 2604 3966 [email protected]

What’s New • 1QFY17 results met expectation

• Expect stronger FY17 with twin growth drivers in

Plantation and Property in full swing

• Raise FY17F/18F/19F earnings by 1%2%/6% for

higher CPO price assumption

• Maintain BUY with higher TP of RM3.70

Price Relative

Forecasts and Valuation FY FY FY FY SepSepSepSep ((((RMRMRMRM m) m) m) m) 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF

Revenue 1,275 1,384 1,370 1,375 EBITDA 337 364 369 368 Pre-tax Profit 308 273 271 266 Net Profit 205 183 190 191 Net Pft (Pre Ex.) 149 183 190 191 Net Pft Gth (Pre-ex) (%) 31.0 22.6 3.7 0.7 EPS (sen) 48.9 43.7 41.2 41.5 EPS Pre Ex. (sen) 35.6 43.7 41.2 41.5 EPS Gth Pre Ex (%) 31 23 (6) 1 Diluted EPS (sen) 48.9 43.7 41.2 41.5 Net DPS (sen) 7.00 8.00 7.27 7.27 BV Per Share (sen) 305 342 344 379 PE (X) 6.3 7.1 7.5 7.4 PE Pre Ex. (X) 8.7 7.1 7.5 7.4 P/Cash Flow (X) 6.1 4.9 5.9 5.9 EV/EBITDA (X) 5.5 4.8 4.9 4.7 Net Div Yield (%) 2.3 2.6 2.4 2.4 P/Book Value (X) 1.0 0.9 0.9 0.8 Net Debt/Equity (X) 0.4 0.3 0.2 0.1 ROAE (%) 17.2 13.5 12.6 11.5 Earnings Rev (%):Earnings Rev (%):Earnings Rev (%):Earnings Rev (%): 1 2 6 Consensus EPS Consensus EPS Consensus EPS Consensus EPS (sensensensen):::: 43.0 44.0 43.0 Other Broker Recs:Other Broker Recs:Other Broker Recs:Other Broker Recs: B: 1 S: 0 H: 0

Source of all data on this page: Company, AllianceDBS, Bloomberg Finance L.P

Compelling valuation Sustained earnings growth in FY17. Sustained earnings growth in FY17. Sustained earnings growth in FY17. Sustained earnings growth in FY17. After achieving a record profit in FY16, MKH is poised to deliver an even stronger performance in FY17, premised on the stellar performance from both its Plantation and Property divisions. These two key divisions are expected to drive the group forward, allowing it to have clear earnings visibility in FY17 against the backdrop of a challenging economic environment. MKH is currently trading at a bargain valuation of 7x FY17 EPS which is unjustified. We reiterate our BUY call with a higher SOP-derived TP of RM3.70. ResilientResilientResilientResilient property salesproperty salesproperty salesproperty sales. MKH achieved FY16 property sales of RM776m (-7% y-o-y), broadly on par with its record sales of RM835m in FY15. Management has set an all-time high sales target of RM900m in FY17, which attests to the strong confidence in its product offerings (majority <RM700k/unit). MKH’s strong foothold in Kajang/Semenyih makes it the largest beneficiary of the improved public transport connectivity via two MRT stations within Kajang which will be operational by mid-CY17. Meanwhile, its unbilled sales of RM705m will sustain its near-term earnings momentum. Plantation to recover in FY17Plantation to recover in FY17Plantation to recover in FY17Plantation to recover in FY17. MKH’s fresh fruit bunches (FFB) volume dropped 3% in FY16 due to the El-Nino impact on 2HFY16 production, but this is set to reverse in FY17 with the recovery in FFB production. Also, a strong rebound in crude palm oil (CPO) price supports our 117% growth projection in FY17 plantation EBIT (33% of group’s FY17 EBIT). The plantation business is already self-sustaining with strong cash flows to pare down its US$ borrowings.

Valuation:

MKH is a rare gem that offers both deep value and strong

earnings growth. Its current bargain valuation of 7x PE is

unjustified, in our view. Solid earnings delivery will be a strong

re-rating catalyst as investors appreciate the value in the stock.

Key Risks to Our View:

Margin compression. Margin compression. Margin compression. Margin compression. Rising construction cost could erode

profit margins for property projects. Exposure to fluctuations in

CPO prices can increase earnings volatility. At A Glance Issued Capital (m shrs) 420

Mkt. Cap (RMm/US$m) 1,298 / 292

Major Shareholders (%)

Chen Choy & Sons Realty 43.1

Public Bank Grp Off Fund 9.8

Free Float (%) 47.1

3m Avg. Daily Val (US$m) 0.27

ICB IndustryICB IndustryICB IndustryICB Industry : Real Estate / Real Estate Investment & Services

DBS Group Research . Equity

9 Mar 2017

Malaysia Company Guide

MKH Bhd Version 7 | Bloomberg: MKH MK | Reuters: METR.KL Refer to important disclosures at the end of this report

90

140

190

240

290

1.2

1.7

2.2

2.7

3.2

3.7

4.2

4.7

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

Relative IndexRM

MKH Bhd (LHS) Relative KLCI (RHS)

ASIAN INSIGHTS VICKERS SECURITIES

Page 14

Company Guide

MKH Bhd

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

FirstFirstFirstFirst----mover advantage. mover advantage. mover advantage. mover advantage. We expect MKH to do well in property

development, given its entrenched brand name in the Kajang-

Semenyih growth corridor and stronghold in the affordable

housing segment. This has placed the company in an enviable

position with property sales and unbilled sales continuing to

chalk new highs. Strong unbilled sales of RM705m imply clear

earnings visibility in the near term.

Healthy sales of affordable housingHealthy sales of affordable housingHealthy sales of affordable housingHealthy sales of affordable housing. MKH’s projects continue to

be well-received in this challenging market because of its focus

on affordable housing. MKH’s FY16 property sales came in at

RM776m (-7% y-o-y) which is a commendable performance.

The completion of MRT Line 1 by 2017 that will link the

Kajang/Semenyih growth corridor will be a strong catalyst for

MKH, given its 490-acre property land bank in that area.

Scarcity of land in Kajang also offers an advantage for MKH for

its future launches – they are expected to fetch premium

pricing, supported by strong demand.

Cheapest plantation proxyCheapest plantation proxyCheapest plantation proxyCheapest plantation proxy. MKH’s 16k-ha fully planted oil palm

estate in East Kalimantan has continued to register strong FFB

production because of the young age profile, though it was

slightly affected by the dry weather in early CY16. FY16 FFB

volume dropped 3% after surging by 36% in FY15. We project

FFB production will recover in FY17 (+16%) with an expected

yield of 29MT/ha which is impressive given that the average age

of the oil palms at its estate is seven years.

Growing plantation contributionGrowing plantation contributionGrowing plantation contributionGrowing plantation contribution. Plantation EBIT contribution

made up ~16% of MKH’s FY16 EBIT, and this is likely to

continue to increase in tandem with rising FFB production. Also,

as the plantation estates mature, MKH will benefit significantly

from a CPO price recovery. The plantation business will

underpin the strong recurring earnings base for MKH going

forward, thus complementing its property business which is

project-based.

CPO ASP (RM/MT)

FFB production (MT)

property sales (RMm)

EBIT margin (%)

Source: Company, AllianceDBS

2014 2056

2649 2729 2687

0.0

393.8

787.6

1181.4

1575.2

1969.0

2362.8

2756.5

2015A 2016A 2017F 2018F 2019F

370000 357674

413262431858 442447

0.0

90259.2

180518.3

270777.5

361036.7

451295.9

2015A 2016A 2017F 2018F 2019F

835776

746 750795

0.00

170.40

340.80

511.20

681.60

852.01

2015A 2016A 2017F 2018F 2019F

20.5

23.9 23.7 24.1 23.6

0.0

4.9

9.7

14.6

19.5

24.3

2015A 2016A 2017F 2018F 2019F

ASIAN INSIGHTS VICKERS SECURITIES

Page 15

Company Guide

MKH Bhd

Balance Sheet:

Gearing for expansion. Gearing for expansion. Gearing for expansion. Gearing for expansion. MKH’s net gearing stood at 47% as at

end-Dec 16. It may appear relatively high as ~34% of its

borrowings are used for its Indonesian plantation business

which started back in 2008. The estate is fully planted, and self-

sustaining and contributing earnings, enabling the group to

service borrowings. Meanwhile, its property business is still in

expansion mode with aggressive launches in recent years, as

MKH tries to ride on the booming property market in the

Kajang-Semenyih growth corridor.

Share Price Drivers:

Strong property sales. Strong property sales. Strong property sales. Strong property sales. The weak sentiment towards the property

market has dampened interest in MKH. Therefore, it is critical

for MKH to deliver strong property sales to entrench its pole

position in Kajang/Semenyih. Its focus on affordable homes will

help the group to attract more buyers.

CPO price recovery. CPO price recovery. CPO price recovery. CPO price recovery. Given rising contribution from the

Plantation business, a sustained recovery in CPO price remains a

key catalyst for MKH. With the tighter supply due to El Nino

phenomenon, CPO price strength may hold. It may be a

blessing in disguise as the group’s maturing oil palms could reap

the benefits of improving CPO price when production peaks.

Key Risks:

Margin compression. Margin compression. Margin compression. Margin compression. Rising construction cost could erode

profit margins for property projects. Exposure to fluctuations in

CPO prices can increase earnings volatility.

Weaker property sales. Weaker property sales. Weaker property sales. Weaker property sales. Rising household debt and softer

consumer sentiment may lead to lower property sales. The

hurdles that potential buyers are facing in getting bank

financing have also resulted in generally lower sales.

Company Background

MKH is an established township developer in Kajang/Semenyih

and Greater Klang Valley with an uninterrupted 25-year profit

track record. It also has a plantation business with 16k ha of oil

palm estates in Indonesia, which has started to contribute

significantly.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, AllianceDBS

0.3

0.3

0.3

0.4

0.4

0.4

0.4

0.4

0.5

0.5

0.5

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

2015A 2016A 2017F 2018F 2019F

Gross Debt to Equity (LHS) Asset Turnover (RHS)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

2015A 2016A 2017F 2018F 2019F

Capital Expenditure (-)

RMm

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2015A 2016A 2017F 2018F 2019F

Avg: 8.2x

+1sd: 10.7x

+2sd: 13.3x

-1sd: 5.6x

-2sd: 3x2.7

4.7

6.7

8.7

10.7

12.7

14.7

16.7

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Avg: 0.94x

+1sd: 1.19x

+2sd: 1.44x

-1sd: 0.69x

-2sd: 0.44x

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

ASIAN INSIGHTS VICKERS SECURITIES

Page 16

Company Guide

MKH Bhd

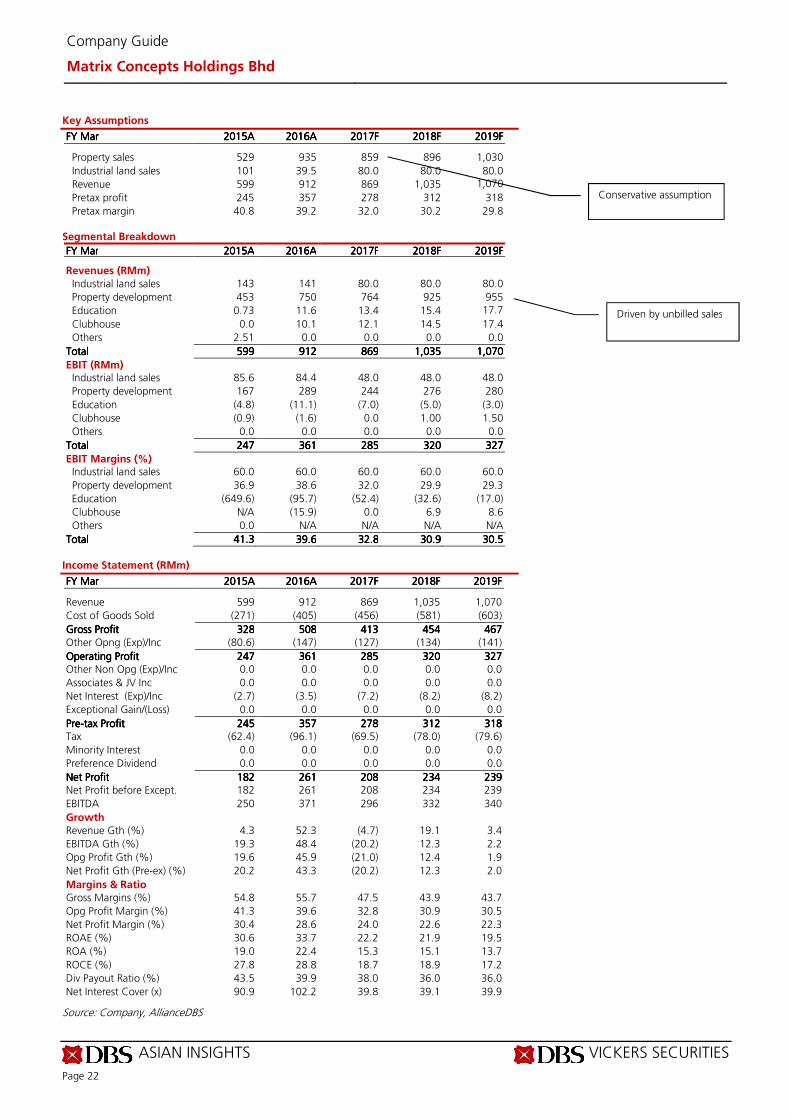

Key Assumptions

FY FY FY FY SepSepSepSep 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF

CPO ASP (RM/MT) 2,014 2,056 2,649 2,729 2,687

FFB production (MT) 370,000 357,674 413,262 431,858 442,447

property sales (RMm) 835 776 746 750 795

EBIT margin (%) 20.5 23.9 23.7 24.1 23.6

Segmental Breakdown

FY FY FY FY SepSepSepSep 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF Revenues (RMm) Property development & construction

721 941 971 932 931 Hotel & property investment

34.8 39.1 40.2 41.4 42.7

Trading 65.0 71.8 74.0 76.2 78.5

Plantation 210 206 282 304 306

Others 10.4 16.1 16.1 16.1 16.1

TotalTotalTotalTotal 1,0421,0421,0421,042 1,2751,2751,2751,275 1,3841,3841,3841,384 1,3701,3701,3701,370 1,3751,3751,3751,375

EBIT (RMm) Property development & construction

153 228 203 191 191 Hotel & property investment

16.1 20.4 19.3 19.9 20.5

Trading 5.60 5.35 5.18 5.34 5.50

Plantation 32.4 49.4 107 121 115

Others 5.98 (3.4) (7.2) (7.2) (7.2)

TotalTotalTotalTotal 214214214214 299299299299 328328328328 330330330330 324324324324

EBIT Margins (%) Property development & construction

21.3 24.2 20.9 20.5 20.5 Hotel & property investment

46.2 52.2 48.0 48.0 48.0

Trading 8.6 7.4 7.0 7.0 7.0

Plantation 15.5 23.9 38.0 39.7 37.5

Others 57.3 (20.8) (44.8) (44.8) (44.8)

TotalTotalTotalTotal 20.520.520.520.5 23.523.523.523.5 23.723.723.723.7 24.124.124.124.1 23.623.623.623.6

Income Statement (RMm)

FY FY FY FY SepSepSepSep 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF Revenue 1,042 1,275 1,384 1,370 1,375

Cost of Goods Sold (720) (848) (922) (895) (892)

Gross ProfitGross ProfitGross ProfitGross Profit 322322322322 428428428428 461461461461 475475475475 482482482482

Other Opng (Exp)/Inc (108) (122) (133) (145) (158)

Operating ProfitOperating ProfitOperating ProfitOperating Profit 214214214214 305305305305 328328328328 330330330330 324324324324 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0

Associates & JV Inc 0.07 (1.0) 0.0 0.0 0.0

Net Interest (Exp)/Inc (49.1) (51.9) (54.4) (58.6) (58.6)

Exceptional Gain/(Loss) (27.7) 55.7 0.0 0.0 0.0

PrePrePrePre----tax Profittax Profittax Profittax Profit 137137137137 308308308308 273273273273 271271271271 266266266266 Tax (41.2) (94.0) (79.3) (70.6) (63.8)

Minority Interest (9.3) (9.0) (10.9) (10.9) (10.6)

Preference Dividend 0.0 0.0 0.0 0.0 0.0

Net ProfitNet ProfitNet ProfitNet Profit 86.386.386.386.3 205205205205 183183183183 190190190190 191191191191 Net Profit before Except. 114 149 183 190 191

EBITDA 238 337 364 369 368

Growth

Revenue Gth (%) 29.2 22.4 8.5 (1.0) 0.4

EBITDA Gth (%) 10.4 41.4 8.0 1.6 (0.5)

Opg Profit Gth (%) 10.2 42.9 7.4 0.7 (1.7)

Net Profit Gth (Pre-ex) (%) 16.4 31.0 22.6 3.7 0.7

Margins & Ratio

Gross Margins (%) 30.9 33.5 33.3 34.7 35.1

Opg Profit Margin (%) 20.5 23.9 23.7 24.1 23.6

Net Profit Margin (%) 8.3 16.1 13.2 13.9 13.9

ROAE (%) 8.1 17.2 13.5 12.6 11.5

ROA (%) 3.6 7.0 5.4 5.3 5.1

ROCE (%) 7.5 8.9 8.6 8.5 8.1

Div Payout Ratio (%) 34.0 14.3 18.3 17.6 17.5

Net Interest Cover (x) 4.3 5.9 6.0 5.6 5.5

Source: Company, AllianceDBS

Lower than management’s target of RM900m

Driven by unbilled sales

ASIAN INSIGHTS VICKERS SECURITIES

Page 17

Company Guide

MKH Bhd

Quarterly / Interim Income Statement (RMm)

FY FY FY FY SepSepSepSep 4Q4Q4Q4Q2015201520152015 1Q1Q1Q1Q2016201620162016 2Q2Q2Q2Q2016201620162016 3Q3Q3Q3Q2016201620162016 4Q4Q4Q4Q2016201620162016 Revenue 349 266 322 282 404

Cost of Goods Sold (248) (179) (214) (177) (278)

Gross ProfitGross ProfitGross ProfitGross Profit 101101101101 87.887.887.887.8 109109109109 105105105105 126126126126 Other Oper. (Exp)/Inc (31.3) (22.8) (32.7) (36.5) (30.3)

Operating ProfitOperating ProfitOperating ProfitOperating Profit 69.769.769.769.7 65.165.165.165.1 75.875.875.875.8 68.668.668.668.6 95.895.895.895.8 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0

Associates & JV Inc (0.1) 0.17 0.32 (1.1) (0.4)

Net Interest (Exp)/Inc (22.0) (9.7) (9.6) (9.8) (22.8)

Exceptional Gain/(Loss) (8.7) 34.7 8.67 4.92 7.43

PrePrePrePre----tax Profittax Profittax Profittax Profit 38.938.938.938.9 90.390.390.390.3 75.275.275.275.2 62.662.662.662.6 80.080.080.080.0 Tax (15.3) (23.2) (18.1) (22.6) (30.1)

Minority Interest 0.81 (5.5) (1.8) (2.4) 0.57

Net ProfitNet ProfitNet ProfitNet Profit 24.424.424.424.4 61.661.661.661.6 55.355.355.355.3 37.737.737.737.7 50.450.450.450.4 Net profit bef Except. 33.1 26.9 46.6 32.8 43.0

EBITDA 75.5 73.4 83.8 75.5 104

Growth

Revenue Gth (%) 36.3 (23.6) 21.0 (12.5) 43.4

EBITDA Gth (%) 43.8 (2.8) 14.1 (9.9) 38.1

Opg Profit Gth (%) 51.7 (6.7) 16.5 (9.5) 39.5

Net Profit Gth (Pre-ex) (%) 25.8 (18.9) 73.6 (29.7) 31.1

Margins

Gross Margins (%) 29.0 33.0 33.7 37.3 31.2

Opg Profit Margins (%) 20.0 24.4 23.5 24.3 23.7

Net Profit Margins (%) 7.0 23.1 17.2 13.4 12.5 Balance Sheet (RMm)

FY FY FY FY SepSepSepSep 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF Net Fixed Assets 211 218 282 343 399

Invts in Associates & JVs 12.5 14.0 14.0 14.0 14.0

Other LT Assets 1,201 1,739 1,762 1,785 1,809

Cash & ST Invts 269 301 414 500 583

Inventory 68.9 93.5 101 100 101

Debtors 211 223 242 239 240

Other Current Assets 621 656 693 679 678

Total AssetsTotal AssetsTotal AssetsTotal Assets 2,5942,5942,5942,594 3,2453,2453,2453,245 3,5083,5083,5083,508 3,6613,6613,6613,661 3,8253,8253,8253,825

ST Debt

287 264 264 264 264

Creditor 365 554 601 595 597

Other Current Liab 100 53.8 105 96.7 90.0

LT Debt 514 573 573 573 573

Other LT Liabilities 205 488 488 488 488

Shareholder’s Equity 1,102 1,278 1,432 1,588 1,746

Minority Interests 21.4 34.2 45.1 56.0 66.6

Total Cap. & Liab.Total Cap. & Liab.Total Cap. & Liab.Total Cap. & Liab. 2,5942,5942,5942,594 3,2453,2453,2453,245 3,5083,5083,5083,508 3,6613,6613,6613,661 3,8253,8253,8253,825

Non-Cash Wkg. Capital 435 365 330 327 332

Net Cash/(Debt) (532) (536) (423) (337) (254)

Debtors Turn (avg days) 63.1 62.0 61.3 64.1 63.7

Creditors Turn (avg days) 164.5 205.9 237.8 255.2 256.3

Inventory Turn (avg days) 28.0 36.4 40.1 43.1 43.3

Asset Turnover (x) 0.4 0.4 0.4 0.4 0.4

Current Ratio (x) 1.6 1.5 1.5 1.6 1.7

Quick Ratio (x) 0.6 0.6 0.7 0.8 0.9

Net Debt/Equity (X) 0.5 0.4 0.3 0.2 0.1

Net Debt/Equity ex MI (X) 0.5 0.4 0.3 0.2 0.1

Capex to Debt (%) 23.3 11.3 11.9 11.9 11.9

Z-Score (X) 1.8 1.7 1.7 1.7 1.7

Source: Company, AllianceDBS

Within expectations

Steady margins

Healthy balance sheet

ASIAN INSIGHTS VICKERS SECURITIES

Page 18

Company Guide

MKH Bhd

Cash Flow Statement (RMm)

FY FY FY FY SepSepSepSep 2015201520152015AAAA 2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF Pre-Tax Profit 137 308 273 271 266

Dep. & Amort. 24.5 32.6 35.8 39.4 43.4

Tax Paid (49.1) (78.6) (27.6) (79.3) (70.6)

Assoc. & JV Inc/(loss) (0.1) 1.00 0.0 0.0 0.0

Chg in Wkg.Cap. (49.0) (15.7) (16.5) 11.0 2.05

Other Operating CF 141 (34.0) 0.0 0.0 0.0

Net Operating CFNet Operating CFNet Operating CFNet Operating CF 205205205205 213213213213 265265265265 243243243243 241241241241 Capital Exp.(net) (187) (94.5) (100.0) (100.0) (100.0)

Other Invts.(net) (4.0) (4.6) (22.9) (22.9) (24.0)

Invts in Assoc. & JV 0.0 0.0 0.0 0.0 0.0

Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0

Other Investing CF (5.2) (7.8) 0.0 0.0 0.0

Net Investing CFNet Investing CFNet Investing CFNet Investing CF (196)(196)(196)(196) (107)(107)(107)(107) (123)(123)(123)(123) (123)(123)(123)(123) (124)(124)(124)(124) Div Paid (33.6) (29.4) (29.3) (33.5) (33.5)

Chg in Gross Debt 88.5 (25.9) 0.0 0.0 0.0

Capital Issues 0.0 0.0 0.0 0.0 0.0

Other Financing CF (12.8) (4.7) 0.0 0.0 0.0

Net Financing CFNet Financing CFNet Financing CFNet Financing CF 42.242.242.242.2 (60.0)(60.0)(60.0)(60.0) (29.3)(29.3)(29.3)(29.3) (33.5)(33.5)(33.5)(33.5) (33.5)(33.5)(33.5)(33.5)

Currency Adjustments 21.7 (13.8) 0.0 0.0 0.0

Chg in Cash 72.6 32.7 113 86.1 83.0

Opg CFPS (sen) 60.5 54.7 67.2 50.2 51.7

Free CFPS (sen) 4.26 28.4 39.4 30.9 30.5

Source: Company, AllianceDBS

Target Price & Ratings History

Source: AllianceDBS

Analyst: QUAH He Wei, CFA

S.No.S.No.S.No.S.No.Date of Date of Date of Date of

ReportReportReportReport

Closing Closing Closing Closing

PricePricePricePrice

12-mth 12-mth 12-mth 12-mth

T arget T arget T arget T arget

PricePricePricePrice

Rat ing Rat ing Rat ing Rat ing

1: 08 Mar 16 2.26 2.80 BUY

2: 29 Mar 16 2.53 3.20 BUY

3: 12 Apr 16 2.75 3.20 BUY

4: 30 May 16 2.46 3.20 BUY

5: 10 Jun 16 2.51 3.20 BUY

6: 13 Jun 16 2.56 3.20 BUY

7: 14 Jul 16 2.50 3.20 BUY

8: 22 Aug 16 2.95 3.20 BUY

9: 26 Aug 16 2.82 3.20 BUY

10: 27 Sep 16 2.91 3.20 BUY

11: 22 Nov 16 2.85 3.20 BUY

12: 28 Nov 16 2.92 3.40 BUY

13: 07 Dec 16 2.88 3.40 BUY

14: 03 Jan 17 2.87 3.40 BUY

Note Note Note Note : Share price and Target price are adjusted for corporate actions.

1

23

4

5

6

7

8

9

10

11

12

13

14

2.12

2.32

2.52

2.72

2.92

3.12

3.32

Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16 Feb-17

RMRMRMRM

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:BC, PY

BUYBUYBUYBUY Last Traded PriceLast Traded PriceLast Traded PriceLast Traded Price (((( 8 Mar 20178 Mar 20178 Mar 20178 Mar 2017)))): : : : RM2.51 (KLCIKLCIKLCIKLCI : : : : 1,725.54) Price Target Price Target Price Target Price Target 12121212----mthmthmthmth:::: RM3.10 (24% upside) (Prev RM3.10) Potential Catalyst: Potential Catalyst: Potential Catalyst: Potential Catalyst: Stronger-than-expected property sales

Where we differ:Where we differ:Where we differ:Where we differ: We have the highest TP Analyst QUAH He Wei, CFA +603 2604 3966 [email protected]

What’s New • 3QFY17 results missed expectations due to ESOS

expenses

• Third interim DPS of 3.5 sen declared

• Record-high unbilled sales due to impressive new

sales in flagship townships

• Maintain BUY with a slightly lower TP of RM3.10

Price Relative

Forecasts and Valuation FY FY FY FY MarMarMarMar ((((RMRMRMRM m) m) m) m) ****2016201620162016AAAA 2017201720172017FFFF 2018201820182018FFFF 2019201920192019FFFF

Revenue 912 869 1,035 1,070 EBITDA 371 296 332 340 Pre-tax Profit 357 278 312 318 Net Profit 261 208 234 239 Net Pft (Pre Ex.) 261 208 234 239 Net Pft Gth (Pre-ex) (%) 43.3 (20.2) 12.3 2.0 EPS (sen) 46.3 36.4 40.9 41.7 EPS Pre Ex. (sen) 46.3 36.4 40.9 41.7 EPS Gth Pre Ex (%) 35 (21) 12 2 Diluted EPS (sen) 46.3 36.4 40.9 41.7 Net DPS (sen) 18.5 13.8 14.7 15.0 BV Per Share (sen) 157 173 200 227 PE (X) 5.3 6.7 6.0 5.9 PE Pre Ex. (X) 5.3 6.7 6.0 5.9 P/Cash Flow (X) nm 8.1 32.8 6.6 EV/EBITDA (X) 4.1 5.1 4.8 4.4 Net Div Yield (%) 7.5 5.7 6.0 6.1 P/Book Value (X) 1.6 1.4 1.2 1.1 Net Debt/Equity (X) 0.1 0.1 0.2 0.1 ROAE (%) 33.7 22.2 21.9 19.5 Earnings Rev (%):Earnings Rev (%):Earnings Rev (%):Earnings Rev (%): (9) (1) 0 Consensus EPS Consensus EPS Consensus EPS Consensus EPS (sensensensen):::: 39.7 41.3 48.5 Other Broker Recs:Other Broker Recs:Other Broker Recs:Other Broker Recs: B: 5 S: 0 H: 0

*15-month period due to FYE change from Dec15 to Mar16

Source of all data on this page: Company, AllianceDBS, Bloomberg Finance L.P

Proxy to affordable housing Sustainable townshipSustainable townshipSustainable townshipSustainable township. Matrix has bucked the trend with record- high property sales at its two flagship projects, Bandar Sri Sendayan (BSS) in Seremban and Bandar Sri Impian (BSI) in Kluang, despite the relatively weak market sentiment. The majority of its launches are priced below the RM600k/unit mark, leveraging on the robust demand for affordable homes. The sales momentum going forward is likely to remain on the uptrend as Matrix still has a large pipeline of affordable homes which are ready for launch. Ultimate winner.Ultimate winner.Ultimate winner.Ultimate winner. BSS remains its jewel in the crown given the low average land cost of RM7psf (with infrastructure in place) when its affordably-priced properties are already selling at ~RM200psf, leading to significantly higher-than-average profit margins. This unrivalled competitive advantage will make Matrix the best proxy to pure township developments which are set to outperform in this challenging market. The new air force training base at BSS is expected to be completed by mid-CY17 which will then accommodate an additional ~1,500 personnel, further improving the vibrancy of the sprawling township. Impressive dividend yieldImpressive dividend yieldImpressive dividend yieldImpressive dividend yield. Matrix has revised its dividend policy to a maximum of 40% payout from at least 40% previously, as management intends to preserve more cash for future developments. Nevertheless, its FY18 dividend yield of 6% is still the highest within our property sector coverage. Valuation:

We maintain our BUY rating but nudge down our TP to

RM3.10, based on a 30% discount to our fully-diluted RNAV

of RM4.43 after tweaking our future launch pipeline. Matrix is

currently trading at a bargain 6x FY18 PE, which is unjustified

given the strong earnings visibility for this township developer.

Key Risks to Our View:

Weak property salesWeak property salesWeak property salesWeak property sales. Rising household debt and softer

consumer sentiment may lead to lower property sales. At A Glance Issued Capital (m shrs) 572

Mkt. Cap (RMm/US$m) 1,402 / 315

Major Shareholders (%)

Hock Lee Tian 17.7

Shining Term Sdn Bhd 15.4

Free Float (%) 67.0

3m Avg. Daily Val (US$m) 0.21

ICB IndustryICB IndustryICB IndustryICB Industry : Financials / Real Estate Investment & Services

DBS Group Research . Equity %

9 Mar 2017

Malaysia Company Guide

Matrix Concepts Holdings Bhd Version 7 | Bloomberg: MCH MK | Reuters: MATR.KL Refer to important disclosures at the end of this report

90

110

130

150

170

190

210

230

250

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

May-13 May-14 May-15 May-16

Relative IndexRM

Matrix Concepts Holdings Bhd (LHS) Relative KLCI (RHS)

ASIAN INSIGHTS VICKERS SECURITIES

Page 20

Company Guide

Matrix Concepts Holdings Bhd

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

Focusing on township developmentFocusing on township developmentFocusing on township developmentFocusing on township development. Matrix’s flagship projects –

Bandar Sri Sendayan (BSS) in Seremban, Negeri Sembilan and

Bandar Seri Impian (BSI) in Kluang, Johor – continue to be well

received by property buyers despite the challenging property

market. BSS will continue to be the main earnings driver for

Matrix, as the township contributes more than 80% of its

revenue. Property sales at BSS have been growing from strength

to strength, largely attributable to the healthy demand for

landed properties within township developments which provide

a holistic living environment.

Strong property salesStrong property salesStrong property salesStrong property sales. The take-up for Matrix’s projects remains

encouraging despite the cautious sentiment. It secured

RM630m property sales in FY14 and RM974m for 15MFY15/16

(FYE changed to Mar 16 from Dec 15). While Matrix will delay

some of the new launches in BSS and BSI in view of the softer

sentiment, its property sales are expected to remain resilient. For

the trailing 12-month period in 15MFY15/16, Matrix achieved

RM817m property sales, far exceeding its initial target of

RM700m.

Riding on maturing townshipRiding on maturing townshipRiding on maturing townshipRiding on maturing township. BSS is the jewel in the crown due

to its attractive land cost despite heavy capex for the township

infrastructure over the years. Its blended land cost still stood at

a meagre RM7psf (based on annual report), which explains the

significantly higher profit margins fetched by Matrix vis-à-vis

other listed peers. Going by the current sales momentum in

BSS, the project is poised to be a resounding success as we

believe BSS has yet to hit critical mass. The new air-force

training base at BSS is expected to be completed by mid-CY17

which will then accommodate an additional ~1,500 personnel,

further improving the vibrancy of the sprawling township.

Affordable homes remain the mainstayAffordable homes remain the mainstayAffordable homes remain the mainstayAffordable homes remain the mainstay. Apart from BSS and

BSI, Matrix may launch its third flagship development, Kota

Gadong Perdana in Negeri Sembilan (next to BSS) spanning 295

acres and worth RM3.1bn GDV, in FY17. The project will boast

more than 3,000 units of affordable homes priced below

RM400k/unit. We estimate that Matrix still has about 2,000

acres of undeveloped land bank which will mainly cater to the

affordable housing segment.

Penetrating beyond Negeri SembilanPenetrating beyond Negeri SembilanPenetrating beyond Negeri SembilanPenetrating beyond Negeri Sembilan. Matrix has also

showcased its ambitious plan to venture into the property

market in Klang Valley via its two parcels of land in KL and

Puchong which are intended for high-rise developments. It

acquired a 1.1-acre land in KL and a 5.8-acre land in Puchong in

Aug 13 and Apr 15, respectively, as a strategic move to expand

its footprint beyond Negeri Sembilan to secure future earnings.