Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction (Directions in Development)

146

DIRECTIONS IN DEVELOPMENT Poverty Making Work Pay in Nicaragua Employment, Growth, and Poverty Reduction Catalina Gutierrez, Pierella Paci, and Marco Ranzani

-

Upload

catalina-gutierrez -

Category

Documents

-

view

212 -

download

0

Transcript of Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction (Directions in Development)

D I R E C T I O N S I N D E V E L O P M E N T

Poverty

Making Work Pay in NicaraguaEmployment, Growth, and Poverty Reduction

Catalina Gutierrez, Pierella Paci, and Marco Ranzani

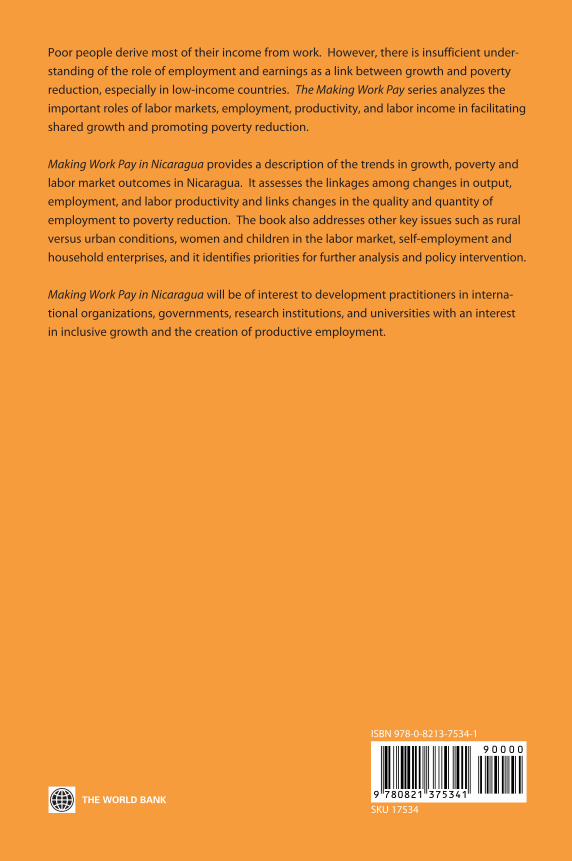

Poor people derive most of their income from work. However, there is insufficient under-standing of the role of employment and earnings as a link between growth and povertyreduction, especially in low-income countries. The Making Work Pay series analyzes theimportant roles of labor markets, employment, productivity, and labor income in facilitatingshared growth and promoting poverty reduction.

Making Work Pay in Nicaragua provides a description of the trends in growth, poverty andlabor market outcomes in Nicaragua. It assesses the linkages among changes in output,employment, and labor productivity and links changes in the quality and quantity ofemployment to poverty reduction. The book also addresses other key issues such as ruralversus urban conditions, women and children in the labor market, self-employment andhousehold enterprises, and it identifies priorities for further analysis and policy intervention.

Making Work Pay in Nicaragua will be of interest to development practitioners in interna-tional organizations, governments, research institutions, and universities with an interestin inclusive growth and the creation of productive employment.

ISBN 978-0-8213-7534-1

SKU 17534

Making Work Pay in Nicaragua

Making Work Pay in Nicaragua Employment, Growth, and Poverty ReductionCatalina GutierrezPierella PaciMarco Ranzani

© 2008 The International Bank for Reconstruction and Development/ The World Bank1818 H Street NWWashington DC 20433Telephone: 202-473-1000Internet: www.worldbank.orgE-mail: [email protected]

All rights reserved.

1 2 3 4 11 10 09 08

This volume is a product of the staff of the International Bank for Reconstructionand Development/The World Bank. The findings, interpretations, and conclusionsexpressed in this volume do not necessarily reflect the views of the ExecutiveDirectors of The World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in thiswork. The boundaries, colors, denominations, and other information shown on anymap in this work do not imply any judgment on the part of The World Bank con-cerning the legal status of any territory or the endorsement or acceptance of suchboundaries.

Rights and PermissionsThe material in this publication is copyrighted. Copying and/or transmitting por-tions or all of this work without permission may be a violation of applicable law. TheInternational Bank for Reconstruction and Development / The World Bank encour-ages dissemination of its work and will normally grant permission to reproduce por-tions of the work promptly.

For permission to photocopy or reprint any part of this work, please send arequest with complete information to the Copyright Clearance Center Inc., 222Rosewood Drive, Danvers, MA 01923, USA; telephone: 978-750-8400; fax: 978-750-4470; Internet: www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should beaddressed to the Office of the Publisher, The World Bank, 1818 H Street NW,Washington, DC 20433, USA; fax: 202-522-2422; e-mail: [email protected].

ISBN-13: 978-0-8213-7534-2eISBN: 978-0-8213-7535-8DOI: 10.1596/978-0-8213-7534-1

Library of Congress Cataloging-in-Publication Data

Making work pay in Nicaragua: employment, growth, and poverty reduction /edited by Catalina Gutiérrez, Pierella Paci, Marco Ranzani.

p. cm.Includes bibliographical references and index.ISBN 978-0-8213-7534-1 -- ISBN 978-0-8213-7535-8 (electronic)

1. Labor market--Nicaragua. 2. Wages--Nicaragua. 3. Poverty--Nicaragua. 4. Laborproductivity--Nicaragua. I. Gutiérrez, Catalina. II. Paci, Pierella, 1957- III. Ranzani,Marco, 1979- HD5737.A6M34 2008331.1097285--dc22

2008017702

Cover design: Candace Roberts, Quantum Think, Philadelphia, PA, United States

Acronyms and Abbreviations xiAcknowledgments xiii

Chapter 1 Introduction and Overview 1Objectives and Scope of this Task 2Structure of the Report 3

Chapter 2 Country Context 7Macroeconomic Context 7Labor Market Context 10Labor Regulation in Nicaragua 20

Chapter 3 Output, Population, Employment, and Poverty 27Main Trends in Output 27Main Trends in Population 28Main Trends in Employment 30Main Trends in Poverty 31Decomposition of Per Capita Income Growth 32

Contents

v

A Closer Look at the Manufacturing Sector 42Annex 3A. Decomposition of Per Capita 48

Value Added Growth

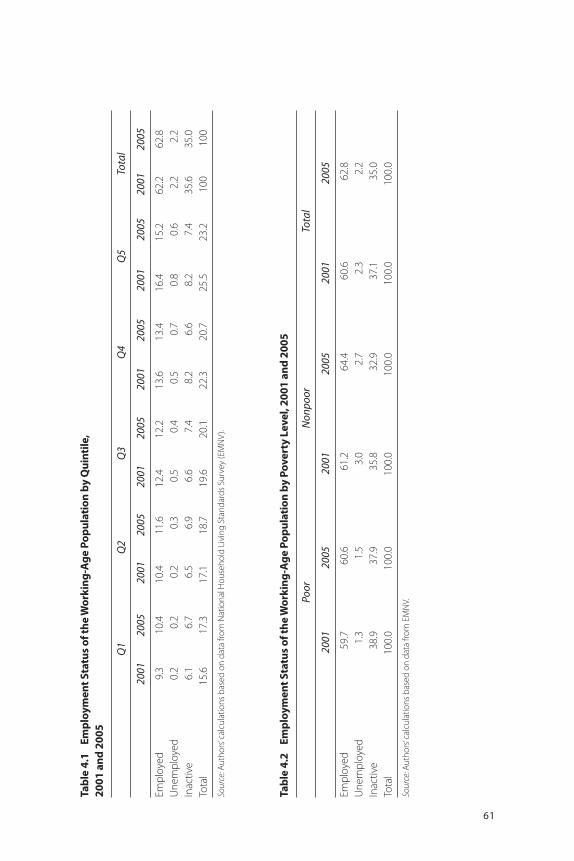

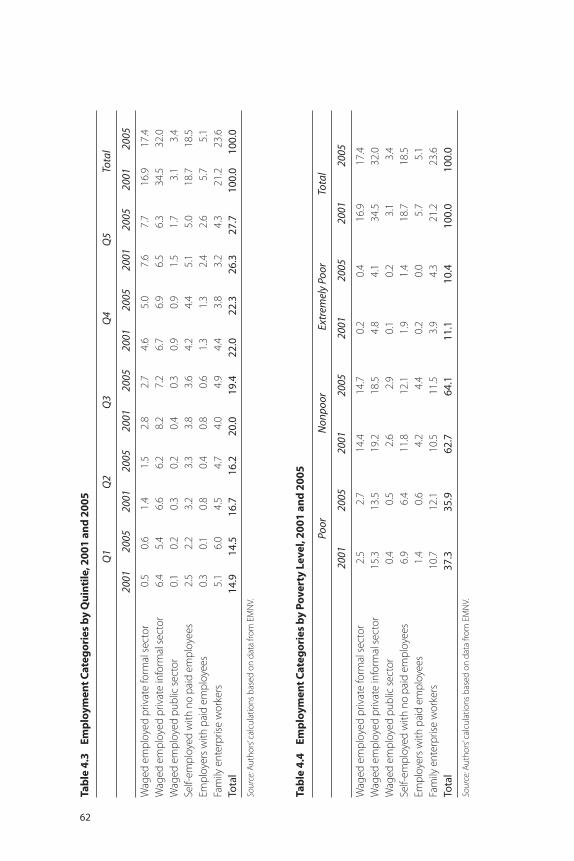

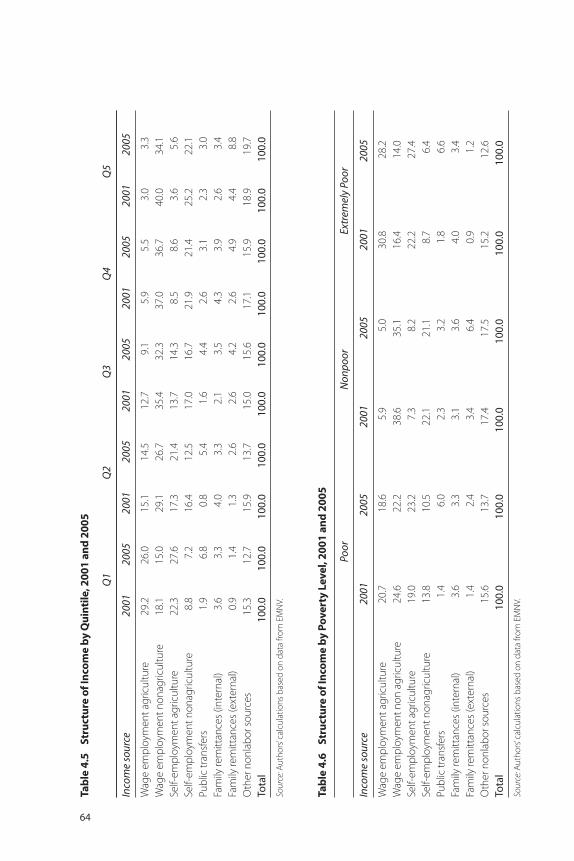

Chapter 4 Employment and Labor Income Profile 59of the PopulationIncome and Employment Profile 60Decomposition of Changes in Labor Income 63A Closer Look at Agriculture 69Annex 4A. Decomposition of Labor Income 78

GrowthAnnex 4B. Estimation Results 81

Chapter 5 Segmentation and Skill Mismatch 87Labor Market Segmentation: Basic Assumptions

and Literature Review 87Evidence of Segmentation across Different

Dimensions 90Segmentation and Barriers to Mobility:

A Qualitative Approach 103Skill Mismatch 107

Chapter 6 Policy Implications and Further Research 115

References 119Index 125

Figures2.1 Investment, Exports, and Growth, 1995–2005 92.2 Distribution of Wages by Sector and Formality, 2001 243.1 Change in Population Structure, 2001–05 293.2 Share of Employment by Sectors, 2001 and 2005 313.3 Aggregate Employment and Productivity Profile of 35

Growth, 2001–053.4 Decomposition of Changes in Output per Worker, 37

2001–054.1 Growth in Average Per Capita Income, by Quintile, 2001 684.2 Productivity of Sensitive Products by Yield per Hectare, 71

1990–2005

vi Contents

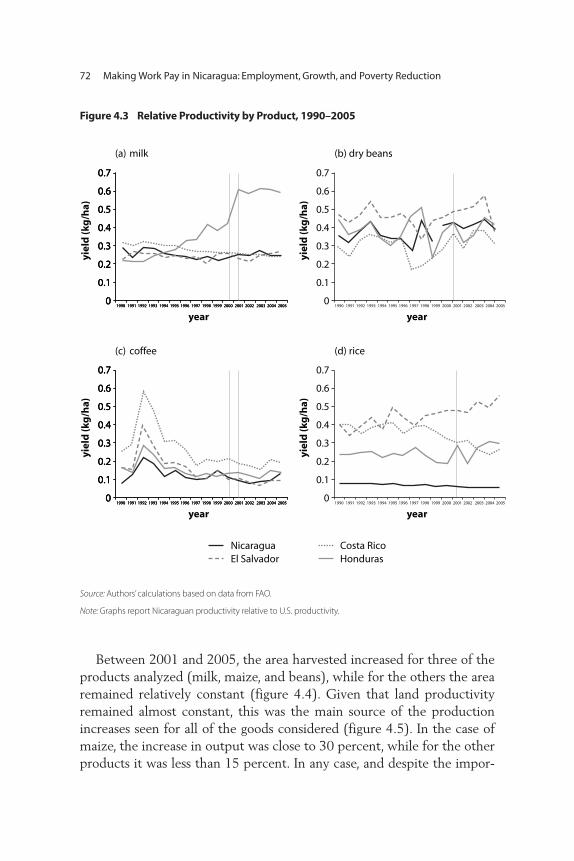

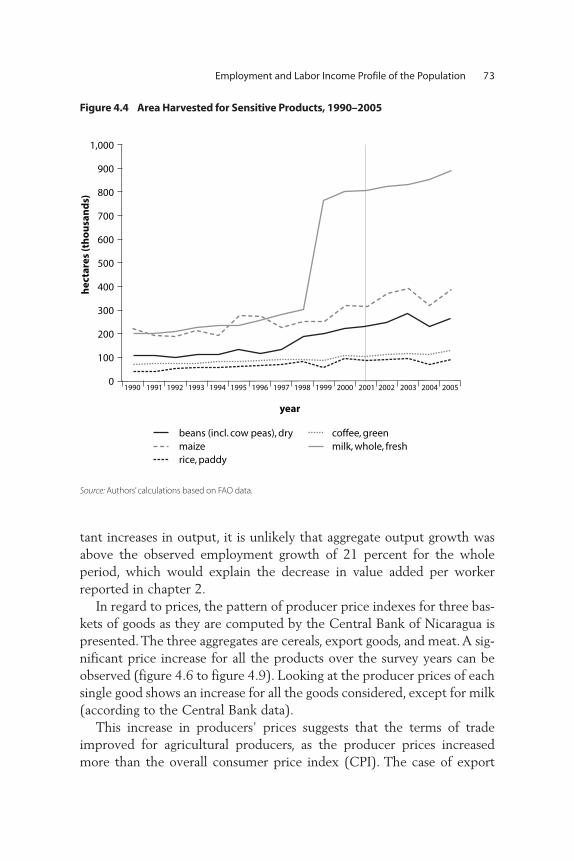

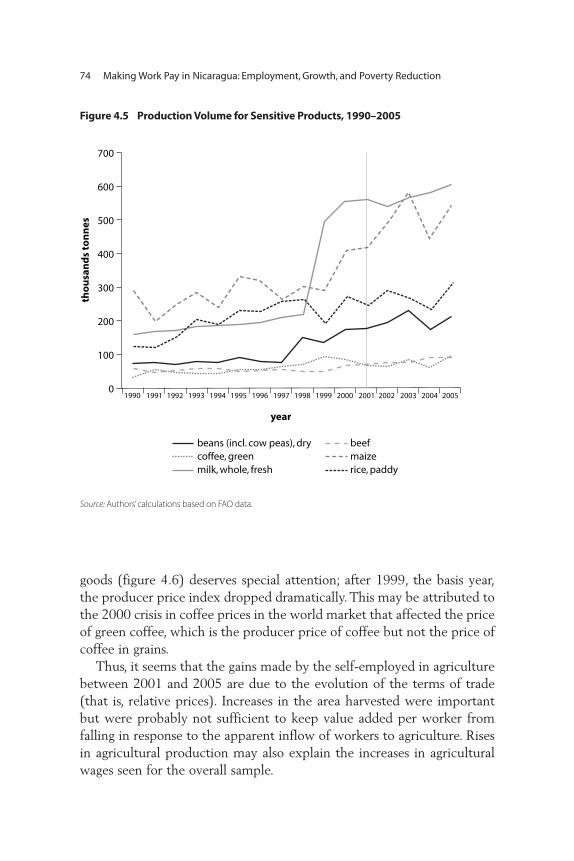

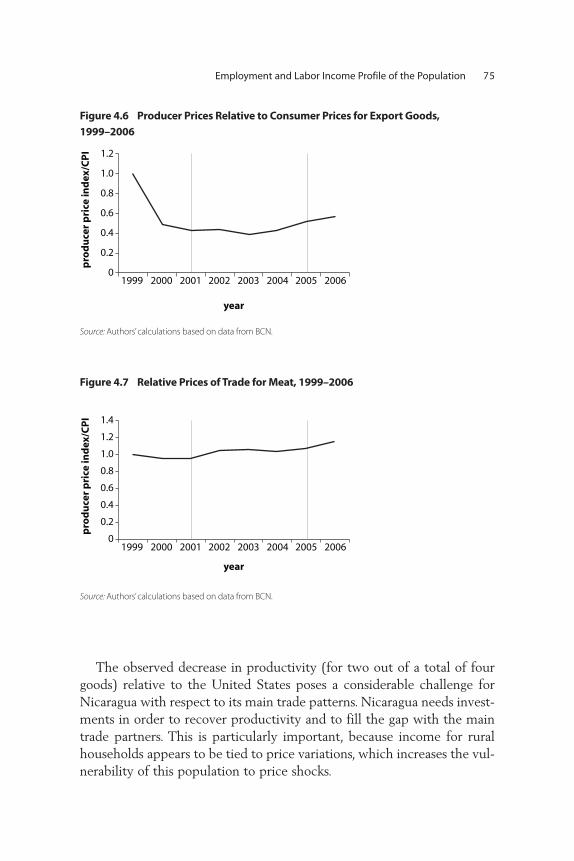

4.3 Relative Productivity by Product, 1990–2005 724.4 Area Harvested for Sensitive Products, 1990–2005 734.5 Production Volume for Sensitive Products, 1990–2005 744.6 Producer Prices Relative to Consumer Prices for 75

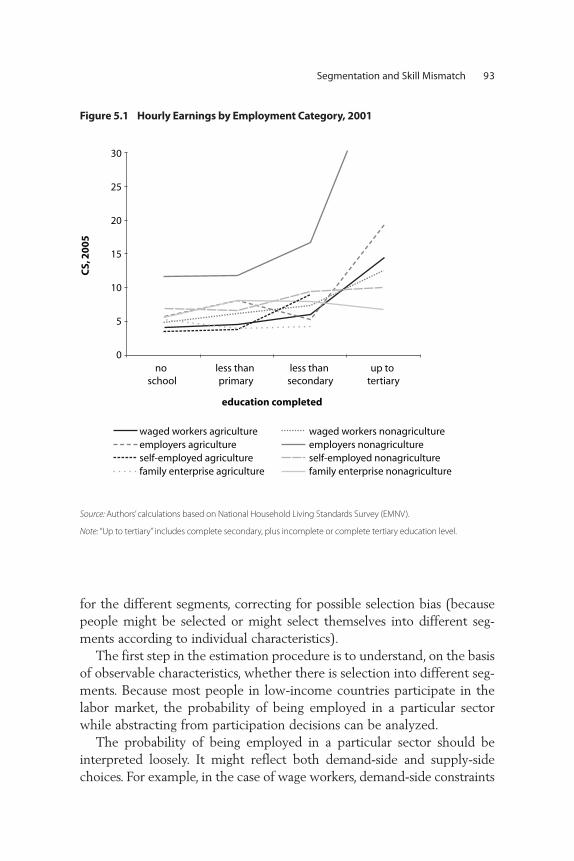

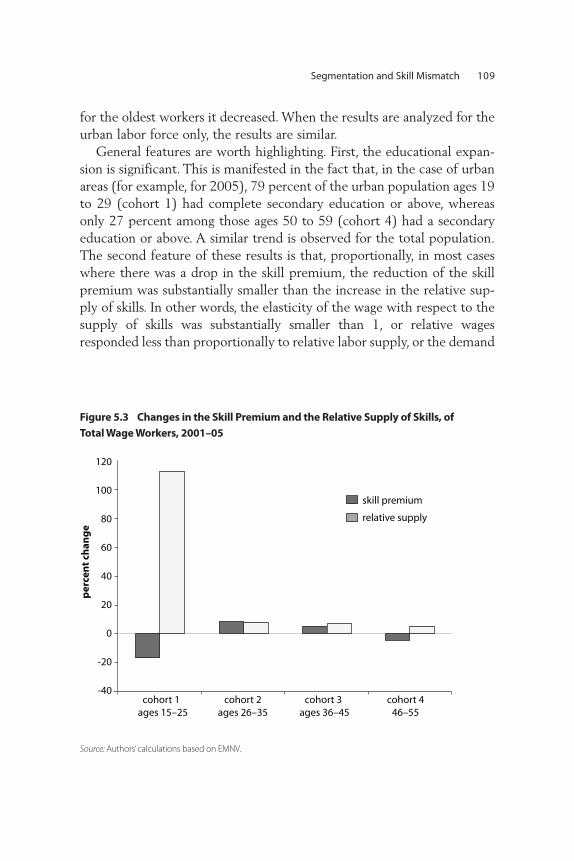

Export Goods, 1999–20064.7 Relative Prices of Trade for Meat, 1999–2006 754.8 Relative Prices for Cereals, 1999–2006 764.9 Relative Prices for Sensitive Products, 2001–06 765.1 Hourly Earnings by Employment Category, 2001 935.2 Hourly Earnings by Broad Sector and Informality, 2001 945.3 Changes in the Skill Premium and the Relative Supply 109

of Skills, of Total Wage Workers, 2001–055.4 Changes in the Skill Premium and the Relative Supply 110

of Skills, of Urban Wage Workers, 2001–05

Tables2.1 Main Macroeconomic Indicators, 1998–2005 112.2 Main Indicators of the Labor Market, 2001 and 2005 132.3 Earnings and Income by Employment Category, 14

2001 and 20052.4 Hierarchical Description of the Population Six Years 16

of Age and Above, 2001 and 20052.5 Other Characteristics of the Employed, 2001 and 2005 182.6 Labor Market Flexibility, Comparative Performance 212.7 Issues Affecting the Investment Climate 222.8 Minimum Wage and Lowest Wage Paid as a Proportion 23

of Minimum Wage, 2001 and 20053.1 Sectoral Growth, 1998–2005 283.2 Average Level of Education of Population Ages 25 to 64 303.3 Evolution of Employment by Sectors, 2001 and 2005 323.4 Headcount Poverty Rates of the Working-Age Population 33

by Employment Status, 2001–053.5 Employment by Sector and Poverty Level, Shares of 34

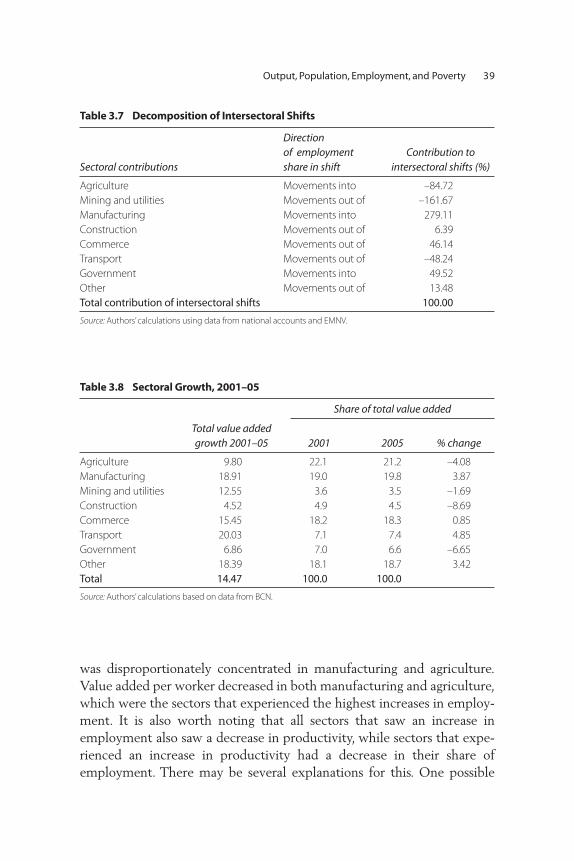

Total Employment, 2001 and 20053.6 Percentage Change in Selected Variables, 2001–05 353.7 Decomposition of Intersectoral Shifts 393.8 Sectoral Growth, 2001–05 39

Contents vii

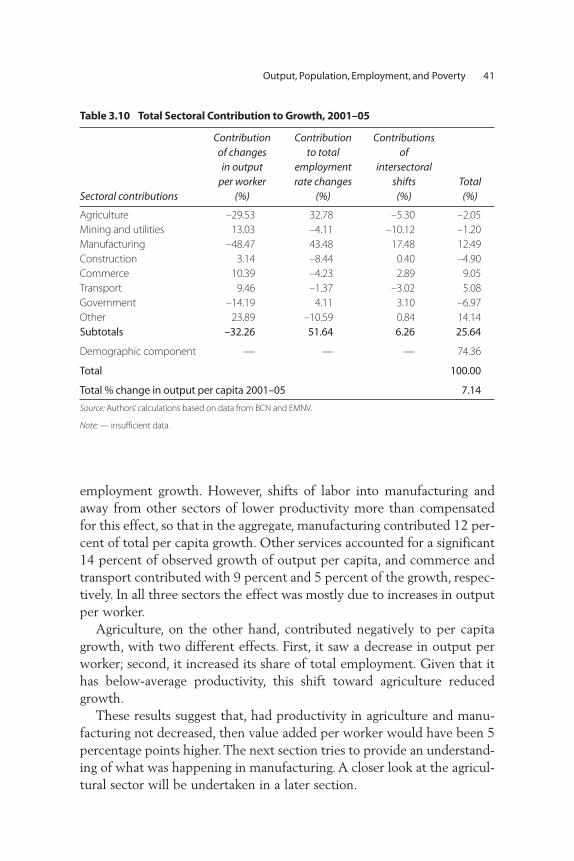

3.9 Employment Shares and Productivity, by Sectors of 40Economic Activity, 2001–05

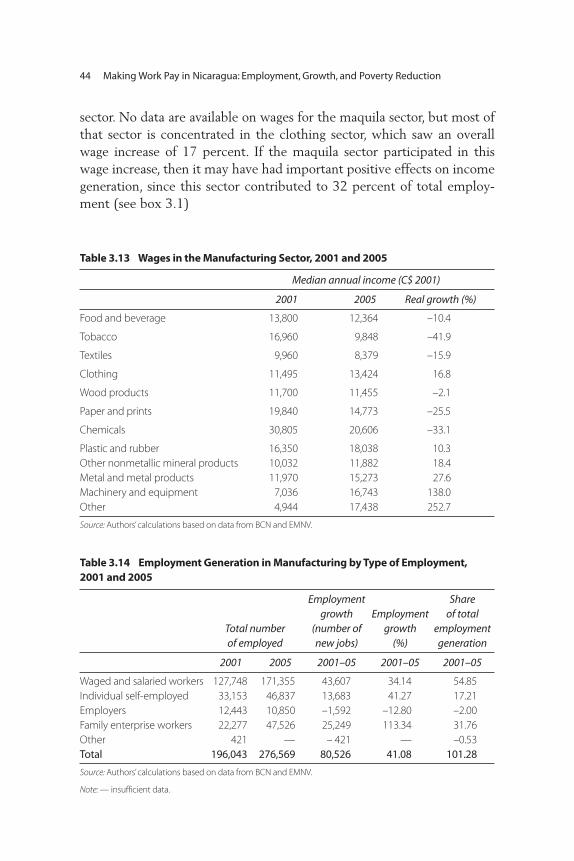

3.10 Total Sectoral Contribution to Growth, 2001–05 413.11 Wages by Sector of Economic Activity, 2001 and 2005 423.12 Employment Generation by Subsector, 2001 and 2005 433.13 Wages in the Manufacturing Sector, 2001 and 2005 443.14 Employment Generation in Manufacturing by Type 44

of Employment, 2001 and 20054.1 Employment Status of the Working-Age Population 61

by Quintile, 2001 and 20054.2 Employment Status of the Working-Age Population by 61

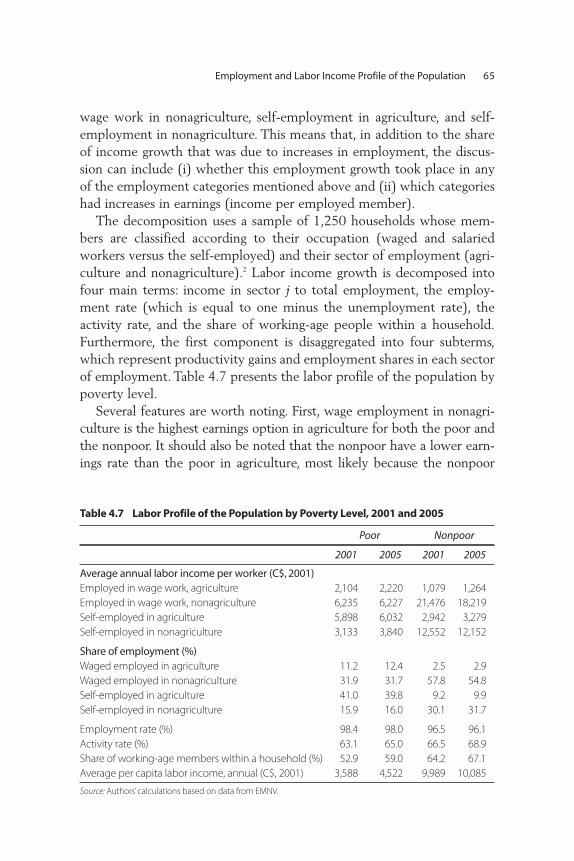

Poverty Level, 2001 and 20054.3 Employment Categories by Quintile, 2001 and 2005 624.4 Employment Categories by Poverty Level, 2001 and 2005 624.5 Structure of Income by Quintile, 2001 and 2005 644.6 Structure of Income by Poverty Level, 2001 and 2005 644.7 Labor Profile of the Population by Poverty Level,

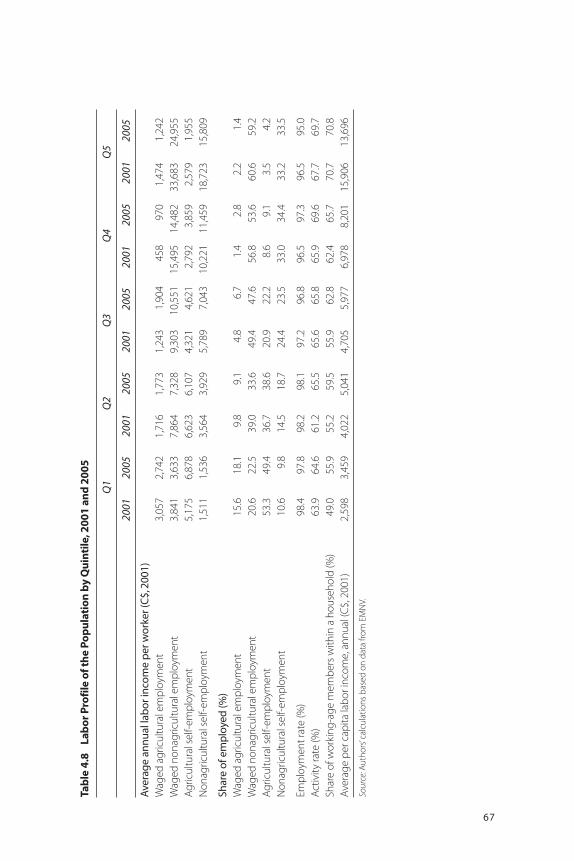

2001 and 2005 654.8 Labor Profile of the Population by Quintile, 67

2001 and 20054.9 Per Capita Household Income Changes, by Quintile, 68

2001–054.10 Shapley Decomposition of Per Capita Labor Income, 70

by Quintile4.11 Number of Farms, by Sensitive Product, according to 71

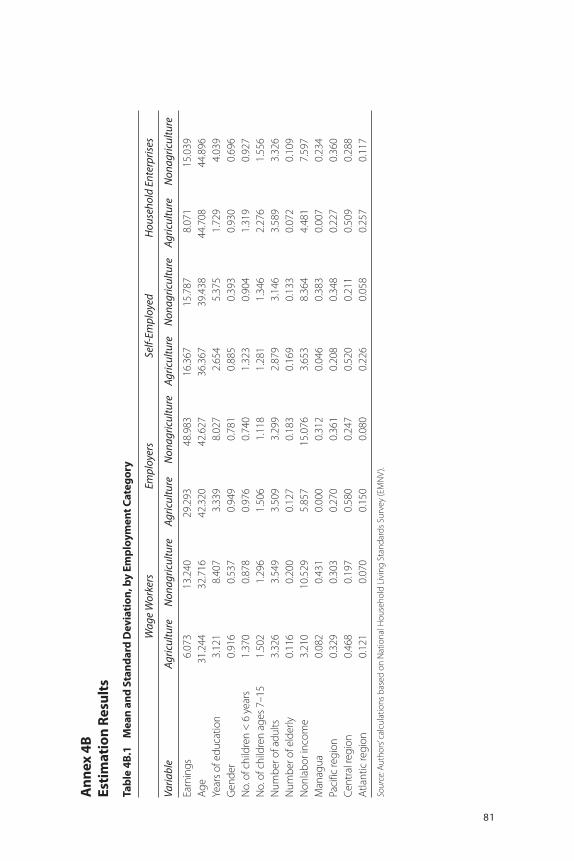

Farm Size, 20014B.1 Mean and Standard Deviation, by Employment 81

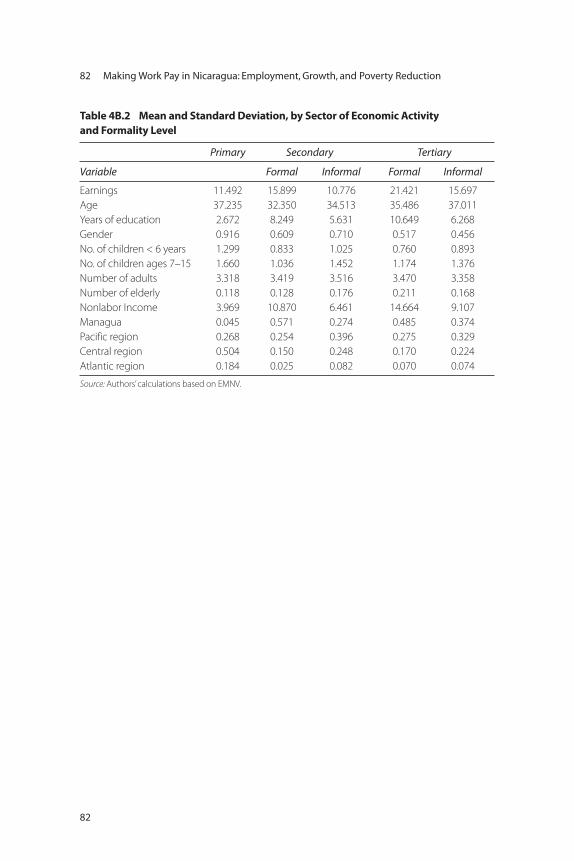

Category4B.2 Mean and Standard Deviation, by Sector of Economic 82

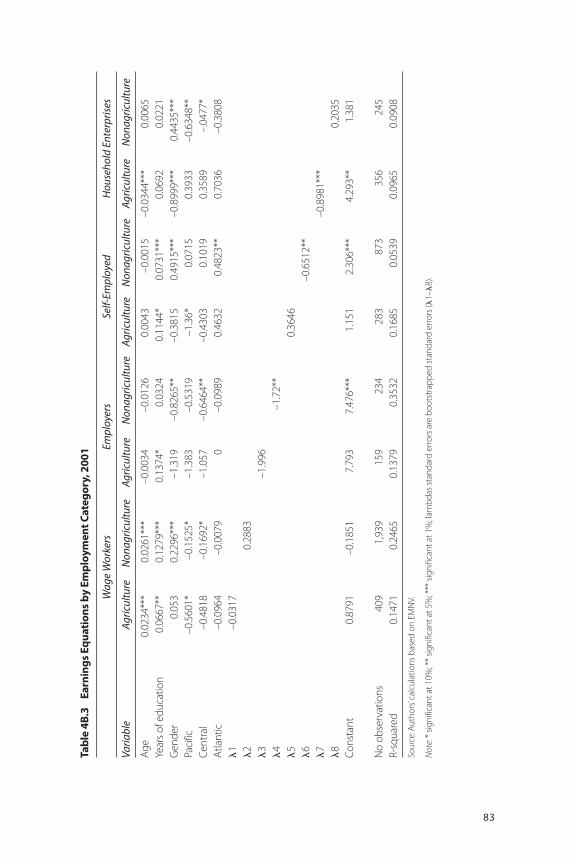

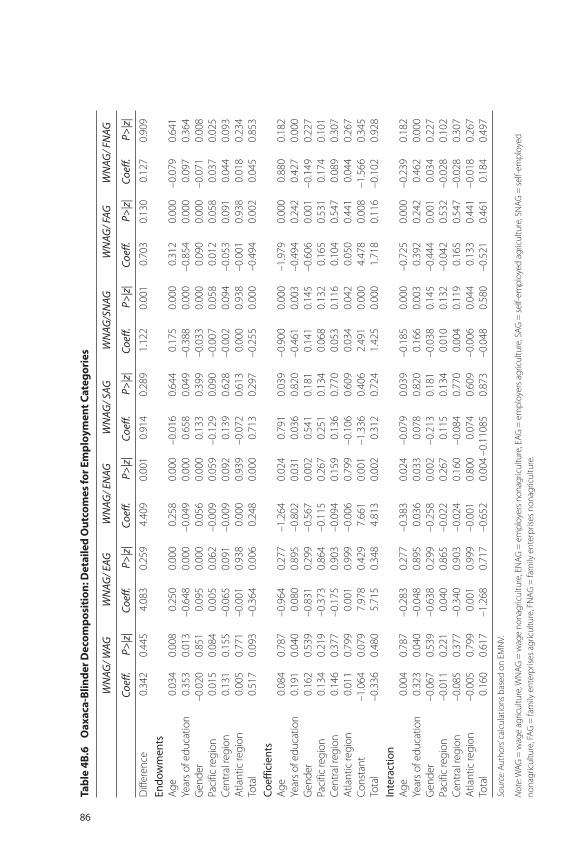

Activity and Formality Level4B.3 Earnings Equations by Employment Category, 2001 834B.4 Earnings Equations by Sector of Employment, 2001 844B.5 Oaxaca-Blinder Decomposition: Detailed Outcomes 85

for Sector and Informality4B.6 Oaxaca-Blinder Decomposition: Detailed Outcomes 86

for Employment Categories

viii Contents

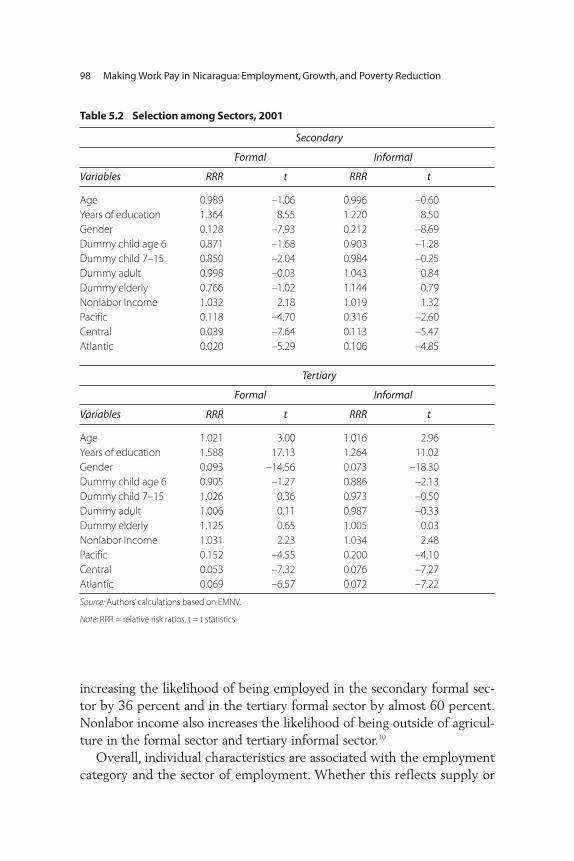

5.1 Selection among Employment Categories, 2001 975.2 Selection among Sectors, 2001 985.3 Oaxaca-Blinder Decomposition by Employment 100

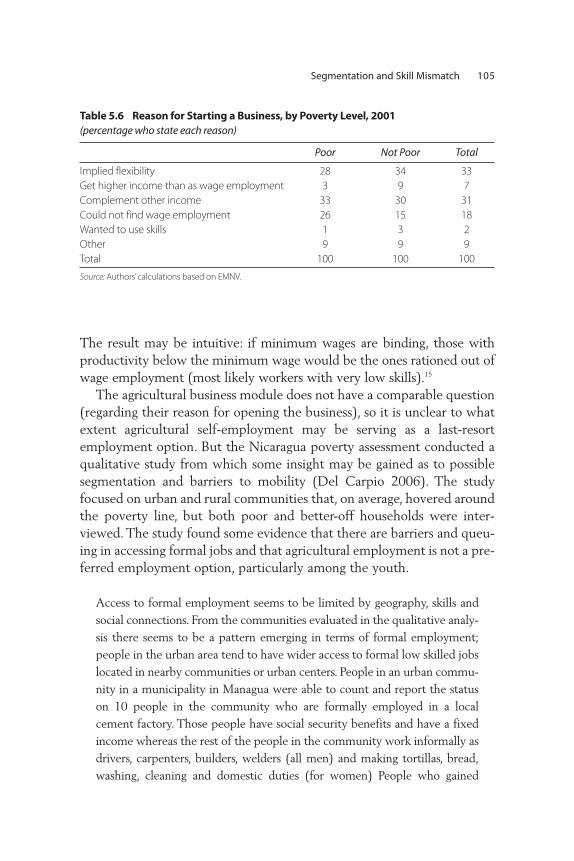

Category5.4 Oaxaca-Blinder Decomposition by Employment Sector 1015.5 Reason for Starting a Business, by Level of Education, 104

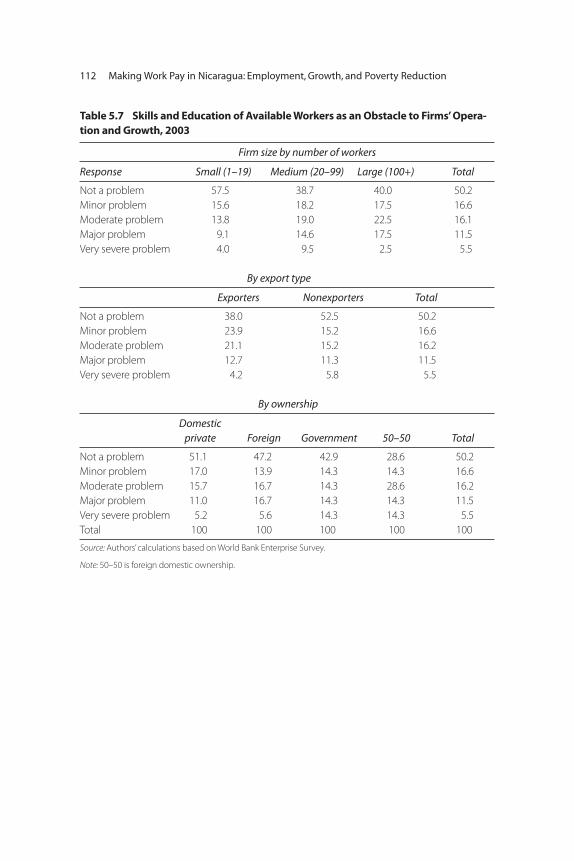

20015.6 Reason for Starting a Business, by Poverty Level, 2001 1055.7 Skills and Education of Available Workers as an 112

Obstacle to Firms’ Operation and Growth, 2003

Boxes1.1 Definitions 42.1 Urban versus Rural Population: Possible Data Problems 193.1 Evolution of the Maquila Sector and Its Importance in 45

the Employment Growth in Manufacturing

Contents ix

BCN Central Bank of NicaraguaCAFTA Central American Free Trade Agreement CEPAL Economic Commission for Latin America and

the CaribbeanCPI consumer price indexEMNV National Household Living Standards Survey

(Encuesta de Medición del Nivel de Vida) EPZ export processing zoneFAO Food and Agriculture Organization of the United NationsGDP gross domestic productHIPC heavily indebted poor countriesIFC International Finance CorporationILO International Labour OrganizationIMF International Monetary FundINATEC National Technology Institute

(Instituto Nacional Tecnológico)INEC National Institute of Statistics and Census

(Instituto National de Estadísticas y Censos)

Acronyms and Abbreviations

xi

xii Acronyms and Abbreviations

INIDE National Institute for Development InformationMITRAB Ministry of Labor PRGF Poverty Reduction and Growth FacilityRAAS Autonomous Region of the Atlantic South

(Región Autónoma del Atlántico Sur)RRR relative risk ratio

This report was prepared by Catalina Gutierrez, Pierella Paci and MarcoRanzani in the Jobs and Migration cluster in the Poverty Reduction andDevelopment Effectiveness Group at the World Bank as part of a multi-year program on the role of employment for inclusive growth. It also pro-vided background information for the Poverty Assessment of Nicaraguaproduced by the World Bank.

The team would like to thank very much a number of people withoutwhom this report would not have been possible. First, the Minister ofLabor of Nicaragua, Janeth Chavéz Gómez, for taking time to provide uswith detailed explanations of the characteristics and peculiarities of theNicaraguan labor market and for sharing with us her view on priorityissues. Second, the staff of the Central Bank of Nicaragua, who havealways responded positively to our many data and information requests.The team is particularly indebted to the Director of the ResearchDepartment, Mario Alemán, and, among his staff, Hiparco Loaisiga, JesusRojas, Ligia Miranda, Miguel Aguilar, and Lisbeth Laguna, who sharedtheir knowledge and views with us in addition to providing us withinvaluable data and information. The team is also grateful to Juan Rocha

Acknowledgments

xiii

xiv Acknowledgments

of the Statistical and Census Office in Nicaragua for his help with house-hold surveys and to Alejandro Martinéz Cuenca in FundaciónInternacional para el Desafío Económico Global (FIDEG), who was kindenough to share his views on the challenges faced by the Nicaraguaneconomy. Finally, special thanks go to Nydia Betanco in the NicaraguaWorld Bank Country Office for all her help and support while on missionin Nicaragua.

The report benefited greatly from the comments received from themembers of the Nicaragua Poverty Assessment Team, led by FlorenciaCastro-Leal, and from the participants to the seminar held in Managua,March 16–17, 2007. We are particularly grateful to Florencia, NormanHicks, Gabriel Demombynes, Diego Angel-Urdinola, Ximena Del Carpio,and José Ramón Laguna for helpful comments and advice. The manyinputs of the members of the Employment and Migration team in thePoverty Reduction and Debt Effectiveness Unit at the World Bank werealso invaluable. The team is extremely grateful for these inputs.

The degree to which growth is able to translate into poverty reductiondepends on how its benefits are distributed among different segments ofsociety. There is little doubt that growth—measured by changes in aver-age income—contributes significantly to poverty reduction.1 However, itis also clear that countries differ in the degree to which income growthspells have translated into poverty reduction. Although differences in theresponsiveness of poverty to income growth account for a small fractionof the overall differences in poverty changes across countries, from thepoint of view of an individual country, these differences may have signif-icant implications for poverty reduction, especially in the short term.2

There is a general consensus that the availability of employmentopportunities and their characteristics constitute an essential transmis-sion channel from growth to poverty reduction and, in this way, play akey role in poverty’s response to growth. For one thing, the poor derivemost of their income from work, either as self-employed or as employees,so what happens to their income and employment status seems tautolog-ically relevant. In addition, the ease with which the poor may take up theopportunities afforded by growth may depend crucially on (i) the struc-ture of employment, (ii) the returns to labor and their distribution, and

C H A P T E R 1

Introduction and Overview

1

(iii) the existence of imperfections and frictions in the labor markets. Forexample, one may be inclined to believe that when the poor face flexiblelabor markets and low barriers to mobility across labor market segments,geographic regions, or sectors of production, they are in a better positionto take the opportunities generated by growth, by moving more easily tothe growing sectors. Similarly, the effectiveness of growth in reducingpoverty may also depend on whether growth is unskilled labor–intensiveand whether the poor have or can easily acquire the skills required by thegrowing sectors. Moreover, there is some evidence of strong links betweenlabor market regulations, such as minimum wages, and the incidence ofpoverty in developing countries.

The concern that employment, returns to labor, and imperfections orrigidities in the labor markets play a crucial role in the poverty impact ofgrowth has been reflected in the emphasis in the policy debate on theidea that jobless growth has been responsible for the disappointing resultsseen by some countries in the effectiveness of growth in reducing pover-ty. As a result, debates addressing how to foster employment-intensivegrowth have followed.3 However, it is also often recognized that povertyis less an outcome of open unemployment than of adequate levels ofincome, and as such, emphasis should be placed not on increasingemployment levels but on increasing the productivity of the workingpoor (ILO 2003). The debate has also been concerned with whether pol-icy interventions should concentrate on increasing earnings in the sectorswhere the poor are found (such as agriculture), or whether they shouldbe targeted to sectors where the poor are not found, so that more of thepoor can be drawn into the higher-earning sectors (Fields 2006). To date,there is very little evidence to illuminate the debate. Moreover, the ques-tions are hard to address, because there is lack of clarity on how to achievethe alternative objectives and because it is inherently difficult to identifythe costs and benefits of the possible policy alternatives.

Objectives and Scope of this Task

The objective of this report is to shed light on some of the issues dis-cussed above in the case of Nicaragua, and to provide some policy guide-lines for the fight against poverty. In particular, it hopes to be able to iden-tify the growing sectors, as well as the constraints faced by the poor inbenefiting from this growth.

2 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

Introduction and Overview 3

The report is part of a series of studies conducted within the PRMPRto foster understanding of the role of employment earnings and labormarkets in shared growth. In addition, it is intended to function as a back-ground document for the World Bank’s Nicaragua Poverty Assessment2007.

Structure of the Report

The report is structured in six chapters. Chapter 2 briefly describes theevolution of the Nicaraguan economy, in terms of its macroeconomicindicators, employment, and poverty. The third chapter analyzes the pro-file of growth and the way in which it helps explain the observed behav-ior of poverty, using data from national accounts and employment datafrom household surveys. It describes growth and employment by the sec-tor of economic activity and its employment productivity profile. Thechapter goes more deeply into the evolution of the manufacturing sectorand the maquila production. Chapter 4 looks at the income profile of thepopulation, using household surveys. Segmentation and skill mismatchare explored in chapter 5, and chapter 6 provides a brief statement onpolicy implications and further research.

Definitions of terms used throughout the report are presented below.Workers have been classified into four occupational categories: waged andsalaried workers, individual self-employed workers, family enterpriseworkers, and employers. These are considered qualitatively distinct typesof labor. Each might constitute a segment within the labor market, withdifferent rules for earnings determination and different employment poli-cies for individuals of identical productivity, and workers’ mobilitybetween these employment categories might be limited. The nonwageworkers are divided into the above-mentioned categories for several rea-sons. First, employers (those who employ paid labor) receive substantial-ly higher income than other nonwage workers and are better educated.They often have assets that other nonwage workers do not. Second,returns to labor for family enterprise workers and the self-employed whoare not working with other members of the family need differentmethodologies of calculation. While the income reported by the self-employed working alone is the return for labor for his or her individualwork, reported income for self-employed workers working with other

4 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

Box 1.1

Definitions

Employment

Child labor A child between 6 and 14 years of age who performed market activities for at least one hour in the week prior to the survey, or who has a permanent job.

Employed An individual who performed market activities for at least one hour in the week prior to the survey, or who has a permanent job.

Formal Employment for which social security contributions are paid employment by workers and firms.

Household A self-declared self-employed person living in a household enterprise worker, with other self-employed or unpaid family workers.family enterprise worker

Inactive A person who is neither employed nor actively looking for work.

Labor force The sum of the working-age employed and unemployed.

Labor market The place where labor services are bought, sold, and exchanged. The labor market comprises wage and salaried workers and their employers, but also nonwage family enterprise workers and the self-employed, who make up the largest share of workers in Nicaragua.

Maquila sector The maquila sector comprises all production units located in the special export processing zones (EPZs), which are clearly defined zones, often within a wired complex. Produc-tion is undertaken with mostly imported materials using local labor, and all output is destined for export markets. Employment in the maquila sector is referred to as maquila employment.

Self-employed A self-declared self-employed person, living in a household in which there are no other self-employed or unpaid family workers.

Unemployed A working-age individual who is not employed but is actively looking for work.

(continued)

Introduction and Overview 5

Box 1.1

(continued)Wage worker A worker who has declared being salaried for his or her work.

It includes those self-reported as jornaleros and peones, who work for a daily or per job rate in manual agricultural labor, often only during the harvest season.

Working-age The population between 15 and 64 years of age.population

Earnings

Earnings, labor All cash payments, payments in kind, and benefits received income in exchange for labor services in wage and salaried employ-

ment, self-employment, and other forms of labor exchange. Earnings and labor income are used interchangeably, although the latter is more often used when referring to the labor income of a household rather than of an individual. Depending on the context, earnings include only primary job earnings (for example, when comparing earnings in the different sectors) or the sum of earnings in all reported jobs.

Earnings of the For nonagricultural work, it is calculated as declared in the self-employed survey. For agricultural work, it is calculated as net profits and employers using the survey’s agricultural enterprise module.

Household For nonagricultural work, earnings for each individual are enterprise calculated as a proportion of the sum of earnings declared earnings in the survey of all the workers employed in the household

enterprise. For 2001, each worker is assigned a portion of earnings proportional to reported hours of work. For 2005, total enterprise income is divided equally among total number of adult workers. For agricultural work, earnings are derived from the survey’s agricultural enterprise module and divided by the number of adult household members reported as working in the enterprise.

Low earner An employed individual whose earnings are below the national poverty line.

Wage earnings Total cash and in-kind earnings as declared in the survey.

6 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

unpaid family members is the income earned by all the family members,and a methodology has to be devised to assign a proportion of householdincome to each member of the family. Finally, individual self-employedare more prevalent in urban areas, whereas family household enterpriseworkers are more prevalent in rural agricultural work.

Notes

1. Kraay (2006) finds that in the short and medium terms income growthaccounts for 70 percent of the variation in headcount poverty, and in the longrun, it accounts for as much as 97 percent.

2. For evidence on heterogeneity in the poverty impact of growth, see for exam-ple Bourguignon (2002); Kakwani, Khandker, and Son (2006); Lucas andTimmer (2005); and Ravallion (2004). See Ravallion (2004) for a discussion ofthe relevance of this heterogeneity from the perspective of a country. A 1 per-cent increase in income levels could result in a poverty reduction of as muchas 4.3 percent or as little as 0.6 percent.

3. One of the core elements of the global employment agenda, MacroeconomicPolicies for Growth and Employment, calls for addressing four key questions,one of which is: How can the employment intensity of growth be increased?(ILO 2003).

This chapter briefly describes the main features of the Nicaraguan econ-omy and its labor market. It summarizes the recent evolution of the mainmacroeconomic indicators, presents a broad picture of the labor marketand how its structure compares with that of other countries, and discuss-es in some detail labor market regulation and its effects on employmentgeneration and investment.

Macroeconomic Context

Over the past 12 years, Nicaragua has witnessed a very significant trans-formation: from a nation torn by war, political instability, and natural dis-asters with its economy plunged into chaos, it has reemerged as an inclu-sive democracy where the foundations for economic growth andsustainable development are being laid. Notwithstanding this progress,Nicaragua still remains among the poorest countries in the western hemisphere. It is classified as a lower-middle-income economy with a percapita gross national income of US$1,000 in 2005, which is a third of theaverage value for Latin America and the Caribbean region and half theaverage of all lower-middle-income countries. It has a population of 5.1million, with a life expectancy at birth of 70 years.

C H A P T E R 2

Country Context

7

8 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

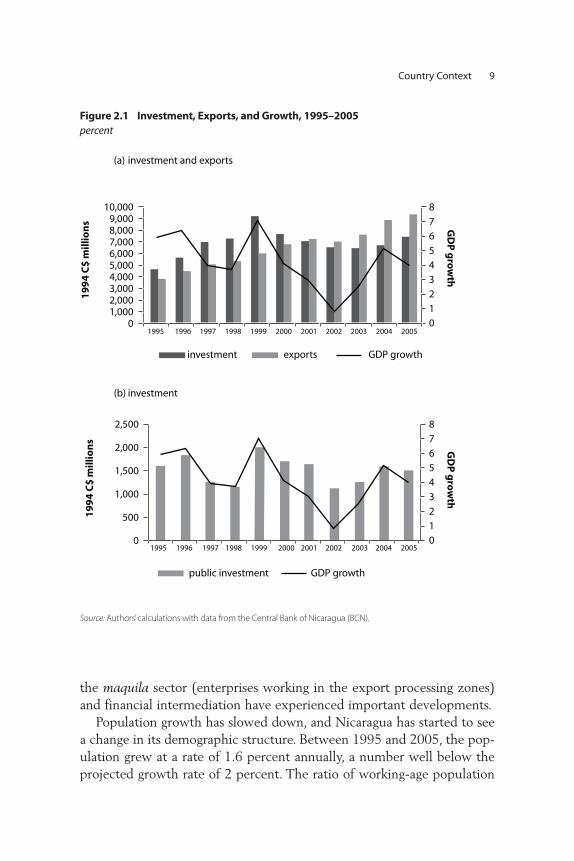

During the past 10 years Nicaragua has experienced modest growthrates, averaging 3.8 percent between 1998 and 2005. The country hasconsolidated its structural adjustment programs and completed therequirements for benefiting from the Heavily Indebted Poor Countries(HIPC) Initiative, thereby freeing the country from a debt service thatamounted to 9.5 percent of GDP in 2001.

Between 1998 and 2001, GDP per capita grew at an average rate of3.8 percent and then decelerated, averaging a per capita growth rate of1.7 percent between 2001 and 2005. This growth has been closely tied toinvestment and exports (see figure 2.1). Investment has been fueled byforeign assistance. In 1998, after Hurricane Mitch struck the country,massive reconstruction efforts were undertaken. The country receivedUS$250 million in emergency assistance, and a further US$1.4 billion waspledged by the international community. Until 2001, recovering from theaftermath of the hurricane was a prime policy objective, which, togetherwith important flows of foreign assistance, led to an increase in publicinvestment of 27 percent in 1999.

The past 10 years have also seen a consolidation in the InternationalMonetary Fund (IMF)-led stabilization policies adopted in the early1990s, which were concentrated in controlling hyperinflation, reducingthe fiscal deficit, and privatizing public utility companies. A second waveof reforms was initiated in 2002 with the signature of the PovertyReduction and Growth Facility (PRGF) with the IMF. Its aim was toachieve fiscal sustainability through the broadening of the tax base, theelimination of tax exemptions, improved revenue collection, more effec-tive budgeting, and the improvement of the financial position of theCentral Bank. The government also sought access to a HIPC Initiative togain foreign debt relief. In 2004, Nicaragua reached the completion pointunder HIPC, and bilateral and multilateral debt relief was granted fordebt incurred prior to 2005. On the international front Nicaragua hassigned several trade and integration agreements with its CentralAmerican partners, and trade with El Salvador, Guatemala, andHonduras is gaining in importance, although the United States remainsthe main trading partner.

There have been no major changes in the sectoral structure of produc-tion and in the urban versus rural composition of the population.However, Nicaragua has experienced an important demographic transi-tion: the share of working-age population (15–64 years) has increasedfaster than other age ranges, reducing the dependency ratio.1 In addition,

Country Context 9

the maquila sector (enterprises working in the export processing zones)and financial intermediation have experienced important developments.

Population growth has slowed down, and Nicaragua has started to seea change in its demographic structure. Between 1995 and 2005, the pop-ulation grew at a rate of 1.6 percent annually, a number well below theprojected growth rate of 2 percent. The ratio of working-age population

public investment GDP growth

investment exports GDP growth

8

7

6

5

4

3

2

1

0

8

7

6

5

4

3

2

1

0

2,500

2,000

1,500

1,000

500

0

10,0009,0008,0007,0006,0005,0004,0003,0002,0001,000

0 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

(a) investment and exports

(b) investment

GD

P g

row

thG

DP

gro

wth

19

94

C$

mill

ion

s1

99

4 C

$ m

illio

ns

Figure 2.1 Investment, Exports, and Growth, 1995–2005percent

Source: Authors’calculations with data from the Central Bank of Nicaragua (BCN).

10 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

(15–64 years) to total population increased from 53 percent in 1998 to55 percent in 2001 and 58 percent in 2005, significantly reducing thedependency ratio. Despite this overall demographic change, there was lit-tle gain in the share of urban population, which increased its share in totalpopulation by 1 percentage point in the past 10 years (table 2.1).

The sectoral structure of GDP remained relatively constant duringthese 10 years, with the secondary sector gaining only a 1-percentage-point share during the whole period. Although there were no majorchanges in the structure of production, within the secondary and tertiarysectors there were some important developments, namely the growth ofthe maquila sector and an important surge in financial intermediation.

Financial intermediation has grown at an average annual rate of 9 per-cent. This increase in intermediation is an important development, asNicaragua has the smallest banking system in Central America and as it isthe main source of credit for the private sector. Still, financial intermedi-ation is weak and accounts for only 3.6 percent of GDP.

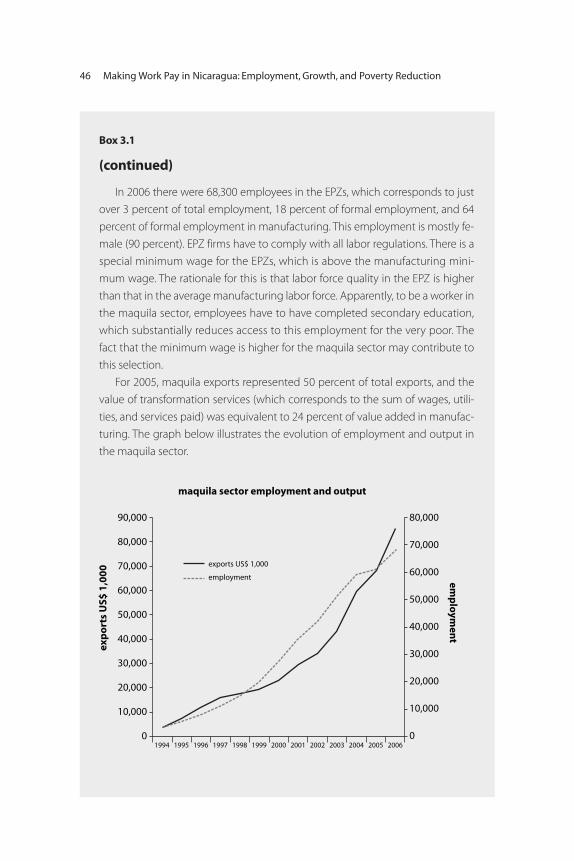

Growth in the maquila sector has had important implications in termsof the availability of foreign reserves and employment. The maquila sec-tor, which started in the early 1990s with the development of the firstpublic free trade zone, has experienced an amazing dynamism. Between2001 and 2005, the share of maquila exports in total exports jumpedfrom 32 percent to 50 percent, and the sector generated just over 53,000new jobs during these four years. The value of transformation services inthe maquila, which measure, the value of domestic inputs used in theprocess, reached 5.5 percent of total value added in 2005.2

Labor Market Context

The labor market profile of Nicaragua is very similar to that of low-incomeand low-middle-income countries and is characterized by low unemploy-ment rates,3 low formality and wage employment rates, high shares of pop-ulation working in agriculture, and relatively high child labor.

This structure of employment is mainly a reflection of the stage ofindustrialization of these countries. Low- and middle-income countriesstill have a large agricultural sector in which productivity is generally lowand workers are mostly self-employed. Most of the population has verylow incomes, so they cannot afford to be unemployed. Instead, an impor-tant fraction of the working-age population is self-employed in informalactivities, many in agriculture. As industrialization progresses, the share of

Table 2.1 Main Macroeconomic Indicators, 1998–2005

1998 1999 2000 2001 2002 2003 2004 2005

GDP real growth (%) 3.7 7.0 4.1 3.0 0.8 2.5 5.1 4.0Real GDP per capita growth (%) 2.0 5.3 2.4 1.3 –0.9 0.8 3.4 2.2Share of value added in 21.3 20.8 22.3 22.1 21.8 21.6 21.3 21.2

primary sector (%) Share of value added in 26.7 27.5 27.1 27.5 27.1 26.8 27.6 27.8

secondary sector (%)Private consumption per 3.0 4.1 3.5 3.1 2.7 0.1 1.9 1.8

capita real growth (%)Gross fixed investment 4.3 27.1 –16.8 –8.4 –7.1 –1.0 4.2 10.1

real growth (%)Consumer price inflation 13.04 11.22 11.55 7.36 3.99 5.15 8.44 9.42

(year-to-year % change)Real effective exchange rate 98.9 96.9 100.0 100.9 96.9 91.2 89.0 88.7

(year 2000 = 100)Urban population as a share 54.9 55.0 55.2 55.3 55.5 55.6 55.8 55.9

of total populationTotal population (thousands) 4,579 4,655 4,733 4,812 4,892 4,974 5,057 5,142

Sources: National Statistical Institute (INEC), BCN, and World Bank.

Country Context 11

employment in the modern sectors, mainly manufacturing and services,rises. Industrialization spreads predominantly in urban areas, which leadsto a process of urbanization, as rural workers leave low-productivity jobsin agriculture in search of higher paying jobs outside of agriculture.

As urbanization progresses, urban self-employment in low-productivi-ty jobs (in many cases informal) increases.The reason behind this increaseis still a matter of debate and may depend on the particulars of the labormarket structure and regulation. In many cases workers who are search-ing or queuing for good jobs are still too poor to afford to be unemployedand must engage in self-employment “survival activities” while they seeka job. In other cases, monopsonistic behavior by firms leads to very lowwages for the unskilled, so that many low-skilled migrant workers findself-employment as attractive as wage employment. With urbanization,unemployment begins to be noticeable, as higher incomes resulting fromhigher productivity permit the luxury of shopping for good jobs.

The development of a modern sector also comes with a rise in formal-ization and in the share of wage and salary employment, as modern firmsgrow and demand labor. The growth of the modern sector is usually alsoaccompanied by a rise in agricultural productivity, although the links and

12 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

causalities for this are less clear. In many cases purposeful investment inagriculture frees rural labor, as more productive techniques mean thatfewer workers are needed to exploit the available land. This surplus labormigrates to urban markets, providing new labor that feeds the process ofurbanization and industrialization. In other cases, migration to nonagri-cultural jobs with higher productivity and higher pay allows householdsto generate savings that can translate into new investments that raise agri-cultural productivity.

As industrialization progresses child labor may decrease, as higherincomes mean lower opportunity costs of sending children to school.Additionally, as the demand for skill increases, so do its returns, and thebenefits of acquiring an education become more evident. Thus, it is cost-lier not to send children to school.

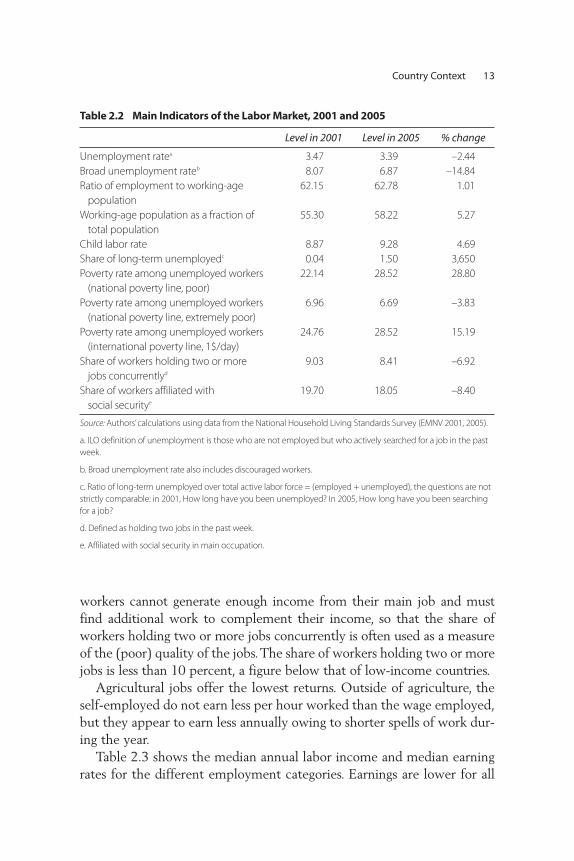

In Nicaragua, unemployment as defined by the International LabourOrganization (ILO) is low, slightly less than 4 percent (see table 2.2).Most of the employed work in the informal sector (82 percent), wageemployment accounts for half of the employed, agriculture absorbs a highshare of employment (37 percent), and child labor is relatively high (9percent). Agriculture is still a sector with low returns, and productivityhas been declining, suggesting that employment in this sector still acts asa “last resort” option for the working population. In the discussion thatfollows, the labor market structure is described in more detail.

Table 2.2 presents the main indicators of the labor market. It showsthat unemployment rates according to the ILO definition are very lowand that they remained almost constant during the period under analysis.The broad unemployment rate, which also includes discouraged workers,is slightly higher but is still low compared with other countries (less than10 percent). The working-age population, defined as those ages 15–64, asa proportion of the total population increased 5 percent (or 3 percentagepoints). The number of employed as a fraction of the total working-agepopulation also rose slightly. Child labor saw a small increase, from 8.7percent to 9.2 percent. The poverty rate among unemployed workersstands out, at half the overall poverty rate, which suggests that unemploy-ment is not strongly correlated with poverty.

The table also shows the number of workers affiliated with social secu-rity, which is often a measure for formalization. In Nicaragua only some 19percent of the labor force has social security, and this ratio decreasedslightly in 2005. Finally, the table shows the number of workers holdingmore than one job concurrently. It has been pointed out that in many cases

workers cannot generate enough income from their main job and mustfind additional work to complement their income, so that the share ofworkers holding two or more jobs concurrently is often used as a measureof the (poor) quality of the jobs.The share of workers holding two or morejobs is less than 10 percent, a figure below that of low-income countries.

Agricultural jobs offer the lowest returns. Outside of agriculture, theself-employed do not earn less per hour worked than the wage employed,but they appear to earn less annually owing to shorter spells of work dur-ing the year.

Table 2.3 shows the median annual labor income and median earningrates for the different employment categories. Earnings are lower for all

Country Context 13

Table 2.2 Main Indicators of the Labor Market, 2001 and 2005

Level in 2001 Level in 2005 % change

Unemployment ratea 3.47 3.39 –2.44Broad unemployment rateb 8.07 6.87 –14.84Ratio of employment to working-age 62.15 62.78 1.01

populationWorking-age population as a fraction of 55.30 58.22 5.27

total populationChild labor rate 8.87 9.28 4.69Share of long-term unemployedc 0.04 1.50 3,650Poverty rate among unemployed workers 22.14 28.52 28.80

(national poverty line, poor)Poverty rate among unemployed workers 6.96 6.69 –3.83

(national poverty line, extremely poor)Poverty rate among unemployed workers 24.76 28.52 15.19

(international poverty line, 1$/day)Share of workers holding two or more 9.03 8.41 –6.92

jobs concurrentlyd

Share of workers affiliated with 19.70 18.05 –8.40social securitye

Source: Authors’calculations using data from the National Household Living Standards Survey (EMNV 2001, 2005).

a. ILO definition of unemployment is those who are not employed but who actively searched for a job in the pastweek.

b. Broad unemployment rate also includes discouraged workers.

c. Ratio of long-term unemployed over total active labor force = (employed + unemployed), the questions are notstrictly comparable: in 2001, How long have you been unemployed? In 2005, How long have you been searchingfor a job?

d. Defined as holding two jobs in the past week.

e. Affiliated with social security in main occupation.

14 Making Work Pay in Nicaragua: Employment, Growth, and Poverty ReductionTa

ble

2.3

Earn

ings

and

Inco

me

by E

mpl

oym

ent C

ateg

ory,

200

1 an

d 20

05

Leve

l in

2001

Leve

l in

2005

% c

hang

e

Non

agric

ultu

reAg

ricul

ture

Non

agric

ultu

reAg

ricul

ture

Non

agric

ultu

reAg

ricul

ture

Wag

e an

d s

alar

y w

orke

rsM

edia

n an

nual

labo

r inc

ome

21,0

64.3

610

,532

.18

20,8

44.0

011

,700

.00

–1.0

511

.09

Med

ian

hour

ly e

arni

ngs

rate

8.32

4.22

8.52

5.06

2.41

20.0

1Lo

w e

arni

ngs

rate

20.5

737

.76

17.6

624

.86

–14.

17–3

4.16

Ind

ivid

ual

sel

f-em

plo

yed

wor

kers

Med

ian

annu

al la

bor i

ncom

e13

,374

.20

6,42

3.42

12,0

00.0

06,

319.

25–1

0.28

–1.6

2M

edia

n ho

urly

ear

ning

s ra

te11

.20

3.88

6.22

—–4

4.43

—Lo

w e

arni

ngs

rate

28.3

255

.96

34.1

351

.59

20.5

0–7

.81

Emp

loye

rsM

edia

n an

nual

labo

r inc

ome

46,8

09.7

09,

298.

0045

,000

.00

31,7

51.1

9–3

.87

241.

48M

edia

n ho

urly

ear

ning

s ra

te26

.87

5.87

19.7

8—

–26.

39—

Low

ear

ning

s ra

te3.

4045

.72

6.83

9.72

100.

85–7

8.74

Hou

seh

old

en

terp

rise

wor

kers

Med

ian

annu

al la

bor i

ncom

e10

,532

.18

5,19

0.74

16,0

53.4

55,

891.

4452

.42

13.5

0M

edia

n ho

urly

ear

ning

s ra

te10

.75

4.12

8.40

——

—Lo

w e

arni

ngs

rate

23.4

064

.36

56.9

557

.70

143.

36–1

0.34

Sour

ce: A

utho

rs’c

alcu

latio

ns w

ith d

ata

from

EM

NV

2001

and

200

5.

Not

e: —

indi

cate

s in

suffi

cien

t or m

issin

g da

ta. M

edia

n an

nual

labo

r inc

ome

refe

rs to

all

the

occu

patio

ns a

nd in

clud

es m

onet

ary,

nonm

onet

ary,

and

in-k

ind

earn

ings

. The

med

ian

hour

ly e

arn-

ings

rate

is c

alcu

late

d fro

m th

e m

ain

occu

patio

n on

ly, e

xcep

t for

the

agric

ultu

ral s

elf-e

mpl

oyed

, agr

icul

tura

l em

ploy

ers,

and

agric

ultu

ral f

amily

ent

erpr

ises,

for w

hich

it is

cal

cula

ted

as p

rofit

spe

r hou

r wor

ked

usin

g th

e ag

ricul

tura

l ent

erpr

ise m

odul

e. In

200

5, th

e ag

ricul

tura

l ent

erpr

ise m

odul

e di

d no

t rep

ort h

ours

wor

ked,

and

ther

efor

e th

e ho

urly

ear

ning

s ra

te c

anno

t be

calc

ulat

-ed

for t

he s

elf-e

mpl

oyed

in a

gric

ultu

re.

agricultural categories, and among agricultural workers the lowest incomeis obtained by household enterprise workers and the individually self-employed. It is also obvious that wages decreased for nonagriculturalemployment while they increased for agricultural workers. The self-employed in nonagricultural work have similar earning rates to the wageemployed, which suggests that wage employment is not necessarily a bet-ter earning option. However, yearly earnings among the self-employed arelower, which suggests that they are employed for shorter periods or workfewer hours.

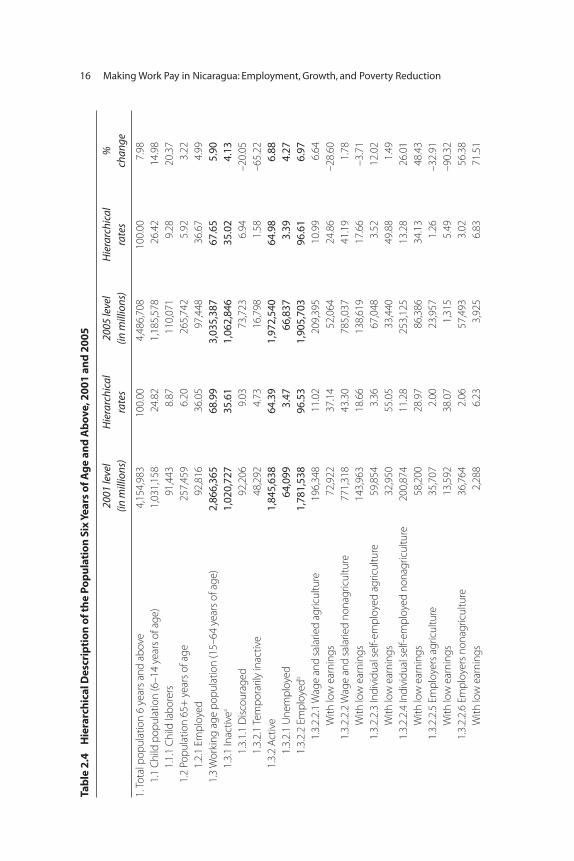

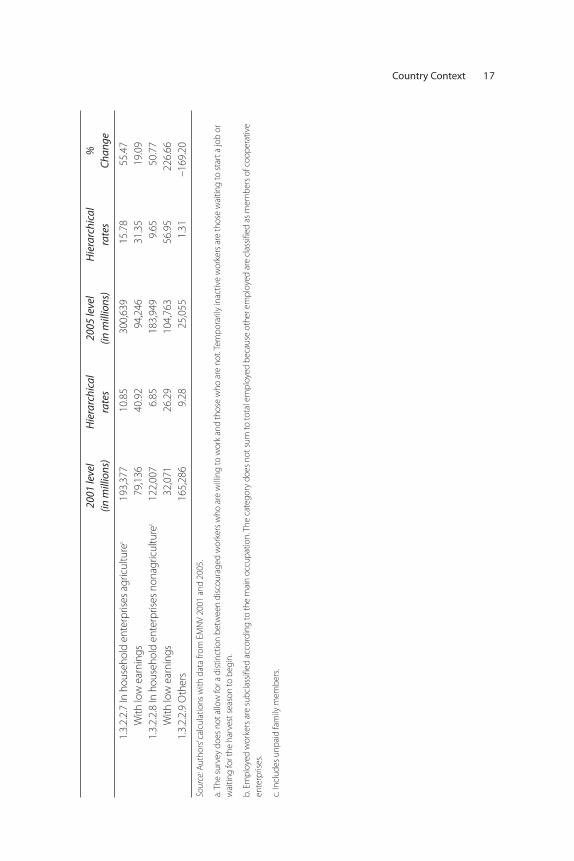

The first column lists the tiers, meaning the group and subgroup oflabor force categories. The second column shows the number of personsunder each tier for 2001. The third column shows the hierarchical rates,meaning the percentage of people in the subcategory (or tier) for 2001.The fourth and fifth columns show the equivalent numbers and rates for2005. The last column gives the percent change.

The first three tiers (child population, population age 65 and above,and working-age population) illustrate the basic population structure ofthose 6 years of age and older. It is very evident that the share of the pop-ulation between ages 6 and 14 increased its participation among thegroup.This has important implications for the evolution of the labor mar-ket in the coming decade, as the cohort between 6 and 14, which repre-sents the largest fraction of the population, will enter the labor market inthe coming years. The population 65 and older and the working-age pop-ulation reduced their shares in the total population. The table further dis-aggregates the working-age population (15–64) into active and inactive.The rate of inactivity has remained almost constant at 35 percent. Theinactive include the discouraged workers and the seasonally inactive. Theproportion of discouraged workers as a fraction of the active populationhas decreased. But this is also true for the seasonally inactive (from 5 per-cent to 1.6 percent). Among the active population, 96 percent areemployed, with very little change from 2001 to 2005.

The employed population (tier 1.3.2.2) is disaggregated into differentemployment categories. The bulk of the nonagricultural population isemployed as wage and salary workers (43 percent in 2001). In the agri-cultural sector, the bulk of employment is evenly distributed betweenthose employed in agricultural family enterprises and the wage and salaryworkers (11 percent each in 2001).4 There has been little change in thisstructure. Under each employment category, the share of low earners isshown. These are the workers who earn incomes below the poverty line.

Country Context 15

Tabl

e 2.

4H

iera

rchi

cal D

escr

iptio

n of

the

Popu

latio

n Si

x Ye

ars o

f Age

and

Abo

ve, 2

001

and

2005

2001

leve

l H

iera

rchi

cal

2005

leve

l H

iera

rchi

cal

%

(in m

illio

ns)

rate

s(in

mill

ions

)ra

tes

chan

ge

1. To

tal p

opul

atio

n 6

year

s an

d ab

ove

4,15

4,98

310

0.00

4,48

6,70

810

0.00

7.98

1.1

Child

pop

ulat

ion

(6–1

4 ye

ars

of a

ge)

1,03

1,15

824

.82

1,18

5,57

826

.42

14.9

81.

1.1

Child

labo

rers

91,4

438.

8711

0,07

19.

2820

.37

1.2

Popu

latio

n 65

+ y

ears

of a

ge25

7,45

96.

2026

5,74

25.

923.

221.

2.1

Empl

oyed

92,8

1636

.05

97,4

4836

.67

4.99

1.3

Wor

king

age

pop

ulat

ion

(15–

64 y

ears

of a

ge)

2,86

6,36

568

.99

3,03

5,38

767

.65

5.90

1.3.

1 In

activ

ea1,

020,

727

35.6

11,

062,

846

35.0

24.

131.

3.1.

1 D

iscou

rage

d92

,206

9.03

73,7

236.

94–2

0.05

1.3.

2.1

Tem

pora

rily

inac

tive

48,2

924.

7316

,798

1.58

–65.

221.

3.2

Activ

e1,

845,

638

64.3

91,

972,

540

64.9

86.

881.

3.2.

1 U

nem

ploy

ed64

,099

3.47

66,8

373.

394.

271.

3.2.

2 Em

ploy

edb

1,78

1,53

896

.53

1,90

5,70

396

.61

6.97

1.3.

2.2.

1 W

age

and

sala

ried

agric

ultu

re

196,

348

11.0

220

9,39

510

.99

6.64

With

low

ear

ning

s72

,922

37.1

452

,064

24.8

6–2

8.60

1.3.

2.2.

2 W

age

and

sala

ried

nona

gric

ultu

re77

1,31

843

.30

785,

037

41.1

91.

78W

ith lo

w e

arni

ngs

143,

963

18.6

613

8,61

917

.66

–3.7

11.

3.2.

2.3

Indi

vidu

al s

elf-e

mpl

oyed

agr

icul

ture

59,8

543.

3667

,048

3.52

12.0

2W

ith lo

w e

arni

ngs

32,9

5055

.05

33,4

4049

.88

1.49

1.3.

2.2.

4 In

divi

dual

sel

f-em

ploy

ed n

onag

ricul

ture

200,

874

11.2

825

3,12

513

.28

26.0

1W

ith lo

w e

arni

ngs

58,2

0028

.97

86,3

8634

.13

48.4

31.

3.2.

2.5

Empl

oyer

s ag

ricul

ture

35,7

072.

0023

,957

1.26

–32.

91W

ith lo

w e

arni

ngs

13,5

9238

.07

1,31

55.

49–9

0.32

1.3.

2.2.

6 Em

ploy

ers

nona

gric

ultu

re36

,764

2.06

57,4

933.

0256

.38

With

low

ear

ning

s2,

288

6.23

3,92

56.

8371

.51

16 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

Country Context 1720

01 le

vel

Hie

rarc

hica

l 20

05 le

vel

Hie

rarc

hica

l %

(in

mill

ions

)ra

tes

(in m

illio

ns)

rate

sCh

ange

1.3.

2.2.

7 In

hou

seho

ld e

nter

prise

s ag

ricul

ture

c19

3,37

710

.85

300,

639

15.7

855

.47

With

low

ear

ning

s79

,136

40.9

294

,246

31.3

519

.09

1.3.

2.2.

8 In

hou

seho

ld e

nter

prise

s no

nagr

icul

ture

c12

2,00

76.

8518

3,94

99.

6550

.77

With

low

ear

ning

s32

,071

26.2

910

4,76

356

.95

226.

661.

3.2.

2.9

Oth

ers

165,

286

9.28

25,0

551.

31–1

69.2

0

Sour

ce: A

utho

rs’c

alcu

latio

ns w

ith d

ata

from

EM

NV

2001

and

200

5.

a. T

he s

urve

y do

es n

ot a

llow

for a

dist

inct

ion

betw

een

disc

oura

ged

wor

kers

who

are

will

ing

to w

ork

and

thos

e w

ho a

re n

ot. T

empo

raril

y in

activ

e w

orke

rs a

re th

ose

wai

ting

to s

tart

a jo

b or

wai

ting

for t

he h

arve

st s

easo

n to

beg

in.

b. E

mpl

oyed

wor

kers

are

sub

clas

sifie

d ac

cord

ing

to th

e m

ain

occu

patio

n. T

he c

ateg

ory

does

not

sum

to to

tal e

mpl

oyed

bec

ause

oth

er e

mpl

oyed

are

cla

ssifi

ed a

s m

embe

rs o

f coo

pera

tive

ente

rpris

es.

c. In

clud

es u

npai

d fa

mily

mem

bers

.

The highest number of low earners can be found among those individu-ally self-employed in agriculture (55 percent have low earnings) andthose that work in household family enterprises in agriculture (40 per-cent have low earnings). Employment in all agricultural categories hasincreased. As will be discussed further, it is unclear how much of thisincrease might be due to errors in the urban-rural weights of the 2001survey.

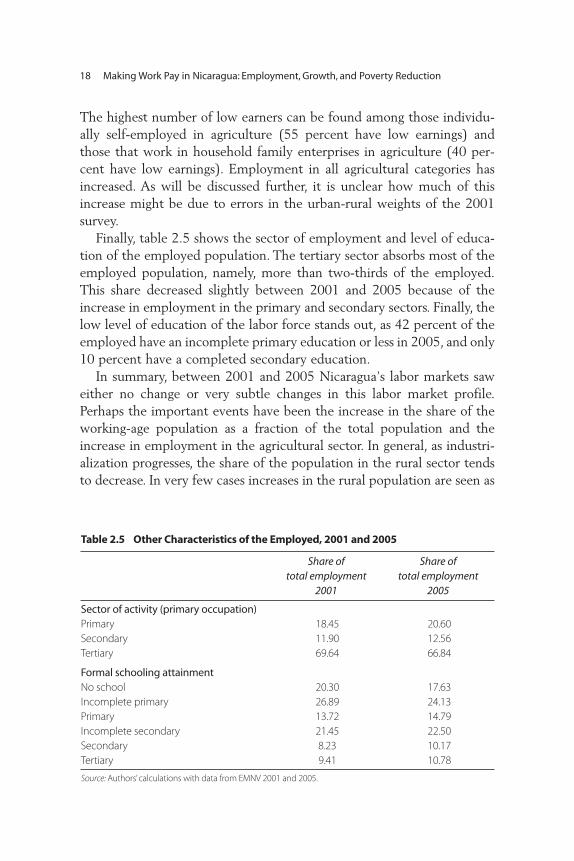

Finally, table 2.5 shows the sector of employment and level of educa-tion of the employed population. The tertiary sector absorbs most of theemployed population, namely, more than two-thirds of the employed.This share decreased slightly between 2001 and 2005 because of theincrease in employment in the primary and secondary sectors. Finally, thelow level of education of the labor force stands out, as 42 percent of theemployed have an incomplete primary education or less in 2005, and only10 percent have a completed secondary education.

In summary, between 2001 and 2005 Nicaragua’s labor markets saweither no change or very subtle changes in this labor market profile.Perhaps the important events have been the increase in the share of theworking-age population as a fraction of the total population and theincrease in employment in the agricultural sector. In general, as industri-alization progresses, the share of the population in the rural sector tendsto decrease. In very few cases increases in the rural population are seen as

18 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

Table 2.5 Other Characteristics of the Employed, 2001 and 2005

Share of Share of total employment total employment

2001 2005

Sector of activity (primary occupation)Primary 18.45 20.60Secondary 11.90 12.56Tertiary 69.64 66.84

Formal schooling attainmentNo school 20.30 17.63Incomplete primary 26.89 24.13Primary 13.72 14.79Incomplete secondary 21.45 22.50Secondary 8.23 10.17Tertiary 9.41 10.78

Source: Authors’calculations with data from EMNV 2001 and 2005.

a response to urban crisis. However, this has not been the case inNicaragua; thus the reason for this increase is yet to be determined. Onepossible explanation is that the population weights used in the 2001 sur-vey were not in accordance with the census behavior of the population(see box 2.1). However, it is not clear to what extent this may be affect-ing the results.

Country Context 19

Box 2.1

Urban versus Rural Population: Possible Data Problems

The table below shows the population calculated from the census and the sur-

veys. According to the surveys, urban population increased substantially from

1998 to 2001, from 54 percent to 58 percent, and then decreased between 2001

and 2005, from 58 percent to 55 percent. It is hard to estimate whether the be-

havior in the surveys is actually true. It is surprising that urbanization increased

substantially and then reversed in such a short time. The available census infor-

mation suggests that there was an increase of 1 percentage point between 1995

and 2005, but there are no data points in between to illustrate the intercensus

behavior. Moreover, the 2001 population estimations used in the 2001 survey

overestimate the population growth. The present report corrects the weights for

this overestimation but makes no adjustments for regional or urban-rural com-

position, as no data were available to do that. It is unlikely that the population

overestimation was uniform across regions or urban and rural populations.

Percentage of regional populationCensus Survey

1995 2005 1998 2001 2005Managua 25.10 24.56 26.06 24.83 24.54

Pacific Urban 17.38 17.13 16.75 17.37 16.95

Pacific Rural 14.16 12.34 15.57 14.34 12.38

Central Urban 10.79 12.21 10.51 12.74 12.28

Central Rural 20.30 19.83 20.82 18.67 19.85

Atlantic Urban 3.89 4.37 5.05 5.50 4.39

Atlantic Rural 8.39 9.56 5.25 6.55 9.62

Overall Urban 54.41 55.92 54.35 58.33 55.83

Labor Regulation in Nicaragua

The largest share of nonlabor costs paid by employers corresponds tosocial security contributions, which amount to 15 percent of the wage.Workers contribute 6.25 percent of their wage for social security.Workersare entitled to one month of paid vacations and an annual bonus that isequivalent to one month of work. They are also entitled to senioritybonuses. In addition to these costs, employers have to pay 2 percent of thetotal payroll for INATEC, the technological training institute. Moreover,there are minimum wages, by sectors, and strong support for unioniza-tion. Firms are allowed to hire temporary workers and can extend thistype of contract indefinitely. The workweek consists of six days and it canbe extended up to 50 hours. Termination of the employment contract isauthorized with no third-party involvement, and workers are entitled toseverance pay upon termination, which varies with tenure.

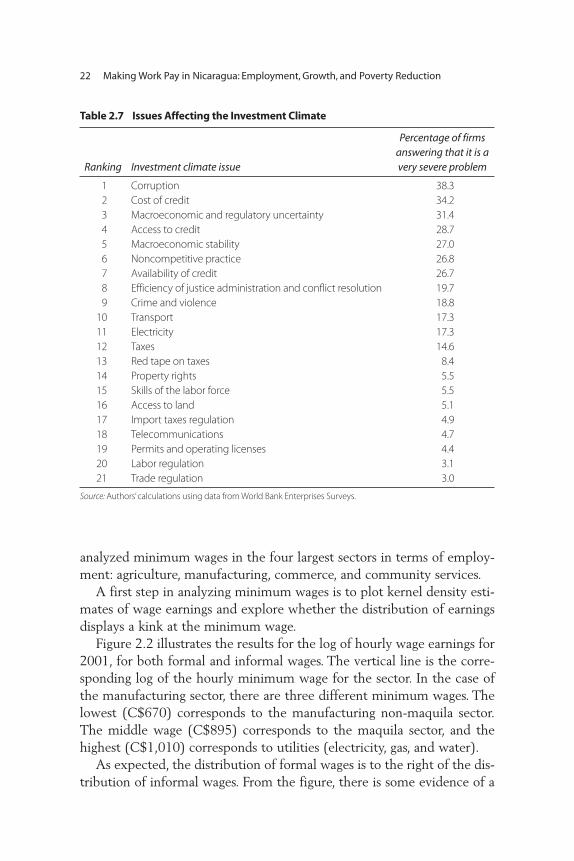

Nicaragua conducted an enterprise survey for 2003, in conjunctionwith the World Bank. Enterprise surveys collect information among firmsregarding constraints to growth and business activities.5 The informationis often used for the analysis of the investment climate in different coun-tries. Although a complete investment climate assessment is outside thescope of this report, the survey can be used to pinpoint the main bottle-necks that are present and that may be hampering growth and employ-ment generation.

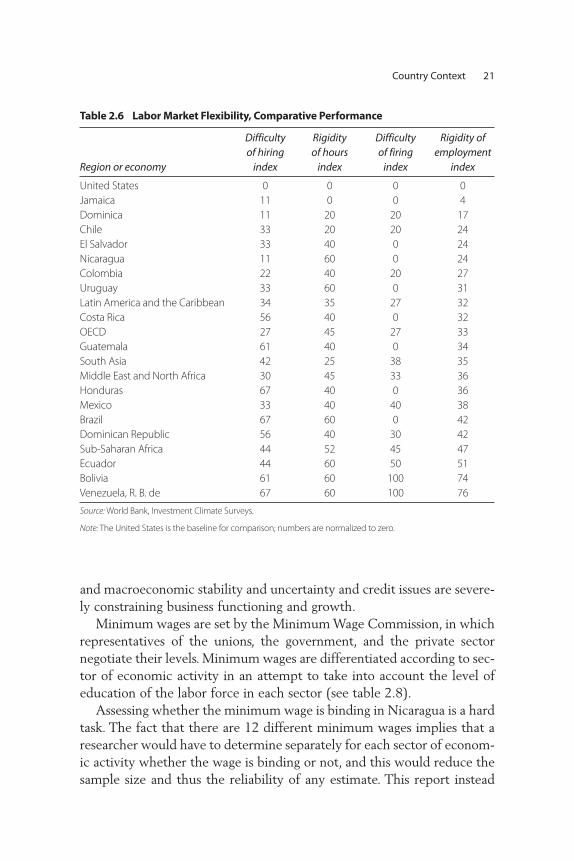

The information collected includes the level of nonwage labor costsand the perception among firms of the rigidity of labor regulation. Usingthis information, the Enterprise Survey Unit at the International FinanceCorporation constructs relative hiring and firing rigidity indexes. Table2.6 compares the results for Nicaragua with other countries in the region(and elsewhere) and with its main trading partners (shown in gray). Ascan be seen, Nicaragua does not appear particularly rigid when comparedwith other countries in the region. In fact, it appears to be one of the leastrigid economies, ranking only below Jamaica and the DominicanRepublic and having an overall performance equal to Chile’s and ElSalvador’s. It is relatively low compared with the United States, one of itsmain trading partners but also the most flexible economy in the world.

Other information collected can be used to asses the main constraintsto investment faced by different firms. Table 2.7 shows the percentage offirms responding that a particular constraint was severely hampering busi-ness functioning and growth. Responses show that labor regulation andthe skills of the labor force are among the least problematic constraints,

20 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

and macroeconomic stability and uncertainty and credit issues are severe-ly constraining business functioning and growth.

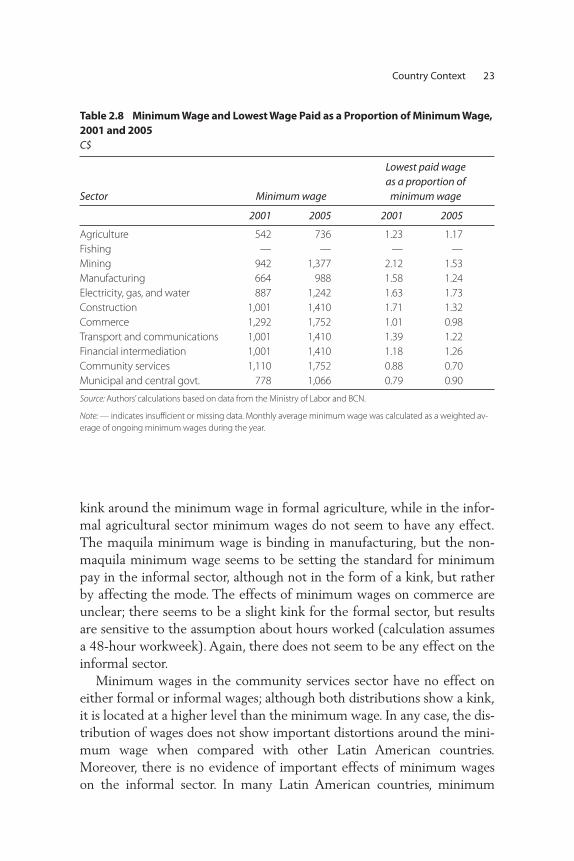

Minimum wages are set by the Minimum Wage Commission, in whichrepresentatives of the unions, the government, and the private sectornegotiate their levels. Minimum wages are differentiated according to sec-tor of economic activity in an attempt to take into account the level ofeducation of the labor force in each sector (see table 2.8).

Assessing whether the minimum wage is binding in Nicaragua is a hardtask. The fact that there are 12 different minimum wages implies that aresearcher would have to determine separately for each sector of econom-ic activity whether the wage is binding or not, and this would reduce thesample size and thus the reliability of any estimate. This report instead

Country Context 21

Table 2.6 Labor Market Flexibility, Comparative Performance

Difficulty Rigidity Difficulty Rigidity of of hiring of hours of firing employment

Region or economy index index index index

United States 0 0 0 0Jamaica 11 0 0 4Dominica 11 20 20 17Chile 33 20 20 24El Salvador 33 40 0 24Nicaragua 11 60 0 24Colombia 22 40 20 27Uruguay 33 60 0 31Latin America and the Caribbean 34 35 27 32Costa Rica 56 40 0 32OECD 27 45 27 33Guatemala 61 40 0 34South Asia 42 25 38 35Middle East and North Africa 30 45 33 36Honduras 67 40 0 36Mexico 33 40 40 38Brazil 67 60 0 42Dominican Republic 56 40 30 42Sub-Saharan Africa 44 52 45 47Ecuador 44 60 50 51Bolivia 61 60 100 74Venezuela, R. B. de 67 60 100 76

Source: World Bank, Investment Climate Surveys.

Note: The United States is the baseline for comparison; numbers are normalized to zero.

analyzed minimum wages in the four largest sectors in terms of employ-ment: agriculture, manufacturing, commerce, and community services.

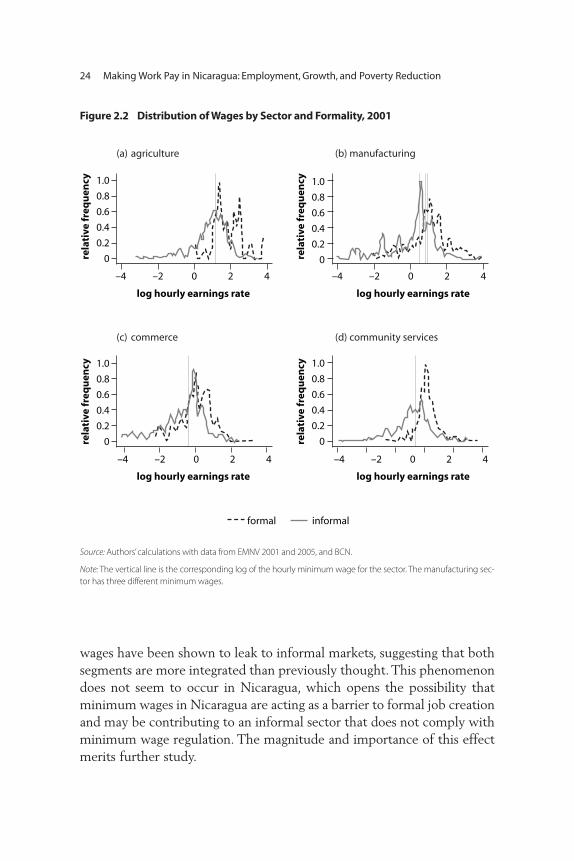

A first step in analyzing minimum wages is to plot kernel density esti-mates of wage earnings and explore whether the distribution of earningsdisplays a kink at the minimum wage.

Figure 2.2 illustrates the results for the log of hourly wage earnings for2001, for both formal and informal wages. The vertical line is the corre-sponding log of the hourly minimum wage for the sector. In the case ofthe manufacturing sector, there are three different minimum wages. Thelowest (C$670) corresponds to the manufacturing non-maquila sector.The middle wage (C$895) corresponds to the maquila sector, and thehighest (C$1,010) corresponds to utilities (electricity, gas, and water).

As expected, the distribution of formal wages is to the right of the dis-tribution of informal wages. From the figure, there is some evidence of a

22 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

Table 2.7 Issues Affecting the Investment Climate

Percentage of firms answering that it is a

Ranking Investment climate issue very severe problem

1 Corruption 38.32 Cost of credit 34.23 Macroeconomic and regulatory uncertainty 31.44 Access to credit 28.75 Macroeconomic stability 27.06 Noncompetitive practice 26.87 Availability of credit 26.78 Efficiency of justice administration and conflict resolution 19.79 Crime and violence 18.8

10 Transport 17.311 Electricity 17.312 Taxes 14.613 Red tape on taxes 8.414 Property rights 5.515 Skills of the labor force 5.516 Access to land 5.117 Import taxes regulation 4.918 Telecommunications 4.719 Permits and operating licenses 4.420 Labor regulation 3.121 Trade regulation 3.0

Source: Authors’calculations using data from World Bank Enterprises Surveys.

kink around the minimum wage in formal agriculture, while in the infor-mal agricultural sector minimum wages do not seem to have any effect.The maquila minimum wage is binding in manufacturing, but the non-maquila minimum wage seems to be setting the standard for minimumpay in the informal sector, although not in the form of a kink, but ratherby affecting the mode. The effects of minimum wages on commerce areunclear; there seems to be a slight kink for the formal sector, but resultsare sensitive to the assumption about hours worked (calculation assumesa 48-hour workweek). Again, there does not seem to be any effect on theinformal sector.

Minimum wages in the community services sector have no effect oneither formal or informal wages; although both distributions show a kink,it is located at a higher level than the minimum wage. In any case, the dis-tribution of wages does not show important distortions around the mini-mum wage when compared with other Latin American countries.Moreover, there is no evidence of important effects of minimum wageson the informal sector. In many Latin American countries, minimum

Country Context 23

Table 2.8 Minimum Wage and Lowest Wage Paid as a Proportion of Minimum Wage,2001 and 2005C$

Lowest paid wage as a proportion of

Sector Minimum wage minimum wage

2001 2005 2001 2005

Agriculture 542 736 1.23 1.17Fishing — — — —Mining 942 1,377 2.12 1.53Manufacturing 664 988 1.58 1.24Electricity, gas, and water 887 1,242 1.63 1.73Construction 1,001 1,410 1.71 1.32Commerce 1,292 1,752 1.01 0.98Transport and communications 1,001 1,410 1.39 1.22Financial intermediation 1,001 1,410 1.18 1.26Community services 1,110 1,752 0.88 0.70Municipal and central govt. 778 1,066 0.79 0.90

Source: Authors’calculations based on data from the Ministry of Labor and BCN.

Note: — indicates insufficient or missing data. Monthly average minimum wage was calculated as a weighted av-erage of ongoing minimum wages during the year.

wages have been shown to leak to informal markets, suggesting that bothsegments are more integrated than previously thought. This phenomenondoes not seem to occur in Nicaragua, which opens the possibility thatminimum wages in Nicaragua are acting as a barrier to formal job creationand may be contributing to an informal sector that does not comply withminimum wage regulation. The magnitude and importance of this effectmerits further study.

24 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

formal informal

(a) agriculture

(c) commerce

(b) manufacturing

(d) community services

1.0

0.8

0.6

0.4

0.2

0

1.0

0.8

0.6

0.4

0.2

0

1.0

0.8

0.6

0.4

0.2

0

1.0

0.8

0.6

0.4

0.2

0

–4 –2 0 2 4 –4 –2 0 2 4

–4 –2 0 2 4 –4 –2 0 2 4

log hourly earnings rate log hourly earnings rate

log hourly earnings rate log hourly earnings rate

rela

tive

freq

uen

cyre

lati

ve fr

equ

ency

rela

tive

freq

uen

cyre

lati

ve fr

equ

ency

Figure 2.2 Distribution of Wages by Sector and Formality, 2001

Source: Authors’calculations with data from EMNV 2001 and 2005, and BCN.

Note: The vertical line is the corresponding log of the hourly minimum wage for the sector. The manufacturing sec-tor has three different minimum wages.

It is unclear whether the current structure of minimum wages pro-vides much benefit over a unique minimum wage. If the idea of sectoralminimum wages is to take into account the different average skill levelsof the labor force in each sector, it might be better to set a minimumwage by level of education (for the low skilled) rather than by sector.Thecurrent structure of the minimum wage might be introducing unneces-sary distortions into the labor market, and might be segmenting the mar-ket according to skills. This might explain the behavior of maquila facto-ries, which face a higher minimum wage than overall manufacturing and,as a response, may restrict employment to those with a secondary orhigher education. If the analysis assumes that more productive firmshave larger profits and a higher share of skills (as is often the case), thecurrent minimum wage–setting mechanism is acting more as a centralcollective bargaining mechanism to distribute profits between low-skilled workers and firms, rather than as a mechanism for setting thelowest paid wage. But even if this were the objective of having a differ-ential minimum wage by sectors, it is unclear what the advantages of thiscentralized bargaining system would be over a decentralized (firm level)bargaining system.

When firms make hiring decisions they compare the marginal cost oflabor, that is, the minimum wage, with the marginal product, that is, thevalue of output produced by one additional worker. More productivefirms are usually more competitive, account for larger shares of employ-ment, and grow faster. If firms differ in productivity, and minimum wagesare higher for the most productive firms, then low-skilled workers (forwhich minimum wages are binding) will be excluded from the mostdynamic and productive sectors of the economy. Instead, a minimumwage by skill level will mean that more productive firms will have anadvantage with respect to low-productivity firms when hiring low-skilledworkers. Relative to the marginal cost (that is, the minimum wage), themarginal benefit of having an unskilled worker is larger. Therefore, high-productivity firms might be more inclined to increase the use of unskilledlabor (that is, increase the unskilled-labor intensity of the productionprocess), while workers will be equally off (for a given level of education)in any sector or firm. Understanding the employment effects of minimumwages and the impact of its sectoral structure on employment, plus therelative demand for unskilled labor, is beyond the scope of this report. Butit is an area that merits further research.

Country Context 25

Notes

1. The dependency ratio is the ratio of total population to working age popula-tion, and it indicates, on average, how many people a working adult has to sup-port.

2. The value of transformation services corresponds to the difference betweenthe value of imported raw materials and the value of final exports and corre-sponds mostly with the cost of labor and utilities.

3. ILO defines unemployed as those who are not employed and who actuallylooked for a job in the past week.

4. The individually self-employed are the self-employed who do not work withother family members. The employers are those who are self-employed buthave paid workers. The household enterprise workers are the self-employedwho work with unpaid family members or unpaid helpers.

5. The International Finance Corporation of the World Bank Group providescomprehensive data for productivity analysis in emerging markets at itsEnterprise Surveys Web site: http://www.enterprisesurveys.org/.

26 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

This chapter describes the labor and productivity profile of growth andlinks it to poverty reduction. It also takes a closer look at the manufactur-ing sector and the maquila sector. The first section describes the maintrends in output, poverty, and employment; the second section decom-poses growth into sectoral employment and productivity changes; thefinal section takes a closer look at manufacturing.

Main Trends in Output

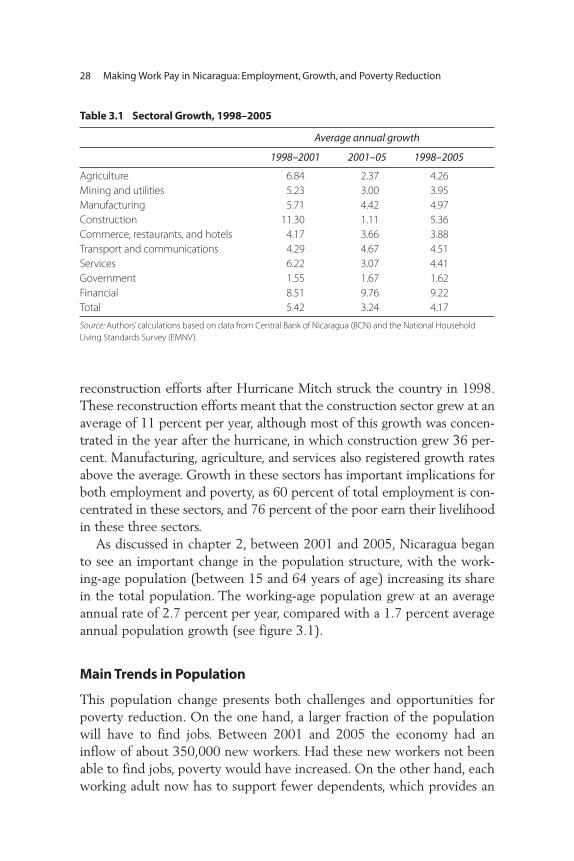

Value added grew at an average annual rate of 4.2 percent between 1998and 2005. Between 1998 and 2001 growth reached 5.42 percent. Growthdecelerated dramatically between 2001 and 2005, reaching an averageannual growth rate of 3.24 percent (table 3.1). Agriculture, construction,and services suffered the largest growth losses. Only transport and thefinancial sector kept their growth pace, but these sectors are small in termsof employment and output. Furthermore, the share of the poor employedin these two sectors is less than 4 percent. Despite this strong decelerationof economic activity, the manufacturing sector managed to grow at anaverage annual rate of 4.4 percent. This has important implications forpoverty reduction, as discussed later. Overall growth was fueled in part by

C H A P T E R 3

Output, Population, Employment, and Poverty

27

reconstruction efforts after Hurricane Mitch struck the country in 1998.These reconstruction efforts meant that the construction sector grew at anaverage of 11 percent per year, although most of this growth was concen-trated in the year after the hurricane, in which construction grew 36 per-cent. Manufacturing, agriculture, and services also registered growth ratesabove the average. Growth in these sectors has important implications forboth employment and poverty, as 60 percent of total employment is con-centrated in these sectors, and 76 percent of the poor earn their livelihoodin these three sectors.

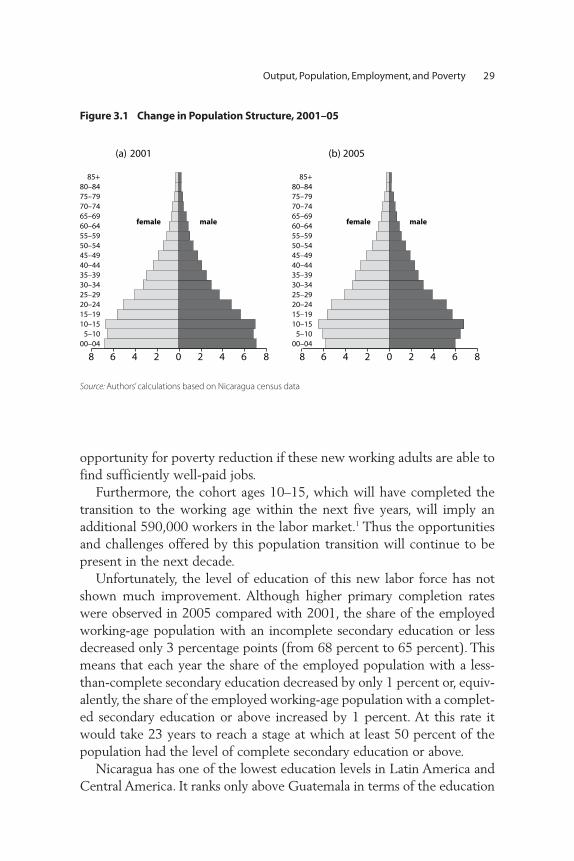

As discussed in chapter 2, between 2001 and 2005, Nicaragua beganto see an important change in the population structure, with the work-ing-age population (between 15 and 64 years of age) increasing its sharein the total population. The working-age population grew at an averageannual rate of 2.7 percent per year, compared with a 1.7 percent averageannual population growth (see figure 3.1).

Main Trends in Population

This population change presents both challenges and opportunities forpoverty reduction. On the one hand, a larger fraction of the populationwill have to find jobs. Between 2001 and 2005 the economy had aninflow of about 350,000 new workers. Had these new workers not beenable to find jobs, poverty would have increased. On the other hand, eachworking adult now has to support fewer dependents, which provides an

28 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

Table 3.1 Sectoral Growth, 1998–2005

Average annual growth

1998–2001 2001–05 1998–2005

Agriculture 6.84 2.37 4.26Mining and utilities 5.23 3.00 3.95Manufacturing 5.71 4.42 4.97Construction 11.30 1.11 5.36Commerce, restaurants, and hotels 4.17 3.66 3.88Transport and communications 4.29 4.67 4.51Services 6.22 3.07 4.41Government 1.55 1.67 1.62Financial 8.51 9.76 9.22Total 5.42 3.24 4.17

Source: Authors’calculations based on data from Central Bank of Nicaragua (BCN) and the National Household Living Standards Survey (EMNV).

opportunity for poverty reduction if these new working adults are able tofind sufficiently well-paid jobs.

Furthermore, the cohort ages 10–15, which will have completed thetransition to the working age within the next five years, will imply anadditional 590,000 workers in the labor market.1 Thus the opportunitiesand challenges offered by this population transition will continue to bepresent in the next decade.

Unfortunately, the level of education of this new labor force has notshown much improvement. Although higher primary completion rateswere observed in 2005 compared with 2001, the share of the employedworking-age population with an incomplete secondary education or lessdecreased only 3 percentage points (from 68 percent to 65 percent). Thismeans that each year the share of the employed population with a less-than-complete secondary education decreased by only 1 percent or, equiv-alently, the share of the employed working-age population with a complet-ed secondary education or above increased by 1 percent. At this rate itwould take 23 years to reach a stage at which at least 50 percent of thepopulation had the level of complete secondary education or above.

Nicaragua has one of the lowest education levels in Latin America andCentral America. It ranks only above Guatemala in terms of the education

Output, Population, Employment, and Poverty 29

(a) 2001 (b) 2005

8 6 4 2 0 2 4 6 8 8 6 4 2 0 2 4 6 8

85+80–8475–7970–7465–6960–6455–5950–5445–4940–4435–3930–3425–2920–2415–1910–15

5–1000–04

85+80–8475–7970–7465–6960–6455–5950–5445–4940–4435–3930–3425–2920–2415–1910–15

5–1000–04

female male female male

Figure 3.1 Change in Population Structure, 2001–05

Source: Authors’calculations based on Nicaragua census data

levels of its urban and rural populations (table 3.2). If the population tran-sition is to lead to poverty reduction, two policies will need to be at thefront of the agenda: increasing good employment opportunities and accel-erating educational achievement.

Main Trends in Employment

Using data from household surveys of 2001 and 2001, it is possible to ana-lyze the main trends in employment.All sectors, with the exception of themining and utilities sector and construction, experienced positive employ-ment growth. The average annual total employment growth was 4 per-cent. Moreover, the growth in employment was greater than the growth inthe labor force (3 percent).

Between 2001 and 2005, the growing labor force was absorbed by theagriculture, manufacturing, and commerce sectors.These sectors account-ed for about 67 percent of total employment, and they all experiencedaverage annual growth rates above 2.5 percent, thus accounting for 84percent of total employment growth (table 3.3). On the other hand, com-munity services, which is the other important sector in terms of its

30 Making Work Pay in Nicaragua: Employment, Growth, and Poverty Reduction

Table 3.2 Average Level of Education of Population Ages 25 to 64

Country Year Urban Rural

Guatemala 2004 6.5 2.4Nicaragua 2001 6.9 3.1Honduras 2003 7.5 3.5Brazil 2005 7.8 3.8El Salvador 2004 8.6 3.8Bolivia 2004 8.9 4.9Venezuela, R. B. de (national total) 2005 8.9 …Dominican Republic 2005 9.1 6.2Mexico 2005 9.6 6.0Costa Rica 2005 9.6 6.8Colombia 2005 9.7 ..Uruguay 2005 9.9 ..Ecuador 2005 10.4 5.6Peru 2003 10.6 5.3Panama 2005 11.1 7.0

Sources: Nicaragua: Authors’calculations based on 2005 survey. Other countries: Economic Commission for LatinAmerica and the Caribbean (CEPAL).

Note: .. indicates negligible value.

employment size, was stagnant, growing at an average annual rate of 1percent. This meant that its contribution to total employment generationwas 5 percent. Figure 3.2 illustrates the sectoral shares of employment for2001 and 2005.