Making the Case Developing Effective Business Cases 24 October 2011.

48

Making the Case Developing Effective Business Cases 24 October 2011

-

Upload

charleen-horn -

Category

Documents

-

view

216 -

download

1

Transcript of Making the Case Developing Effective Business Cases 24 October 2011.

Making the CaseDeveloping Effective Business Cases

24 October 2011

© 2011 Deloitte MCS Limited. Private and confidential

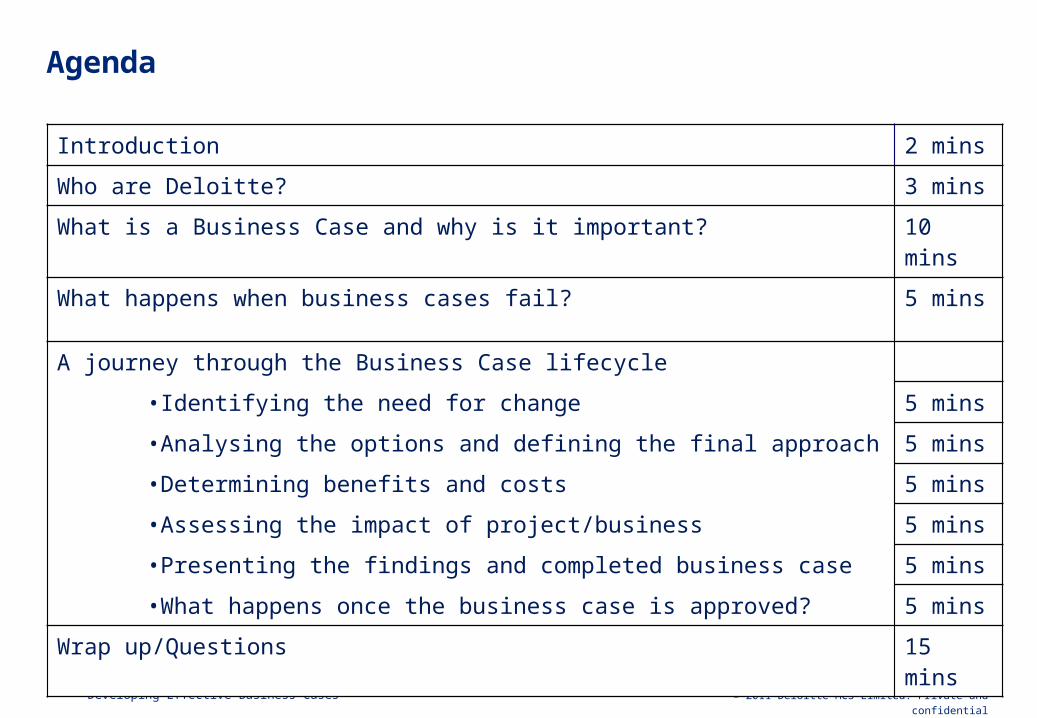

Agenda

2 Developing Effective Business Cases

Introduction 2 mins

Who are Deloitte? 3 mins

What is a Business Case and why is it important? 10 mins

What happens when business cases fail? 5 mins

A journey through the Business Case lifecycle

•Identifying the need for change 5 mins

•Analysing the options and defining the final approach 5 mins

•Determining benefits and costs 5 mins

•Assessing the impact of project/business 5 mins

•Presenting the findings and completed business case 5 mins

•What happens once the business case is approved? 5 mins

Wrap up/Questions 15 mins

© 2011 Deloitte MCS Limited. Private and confidential3

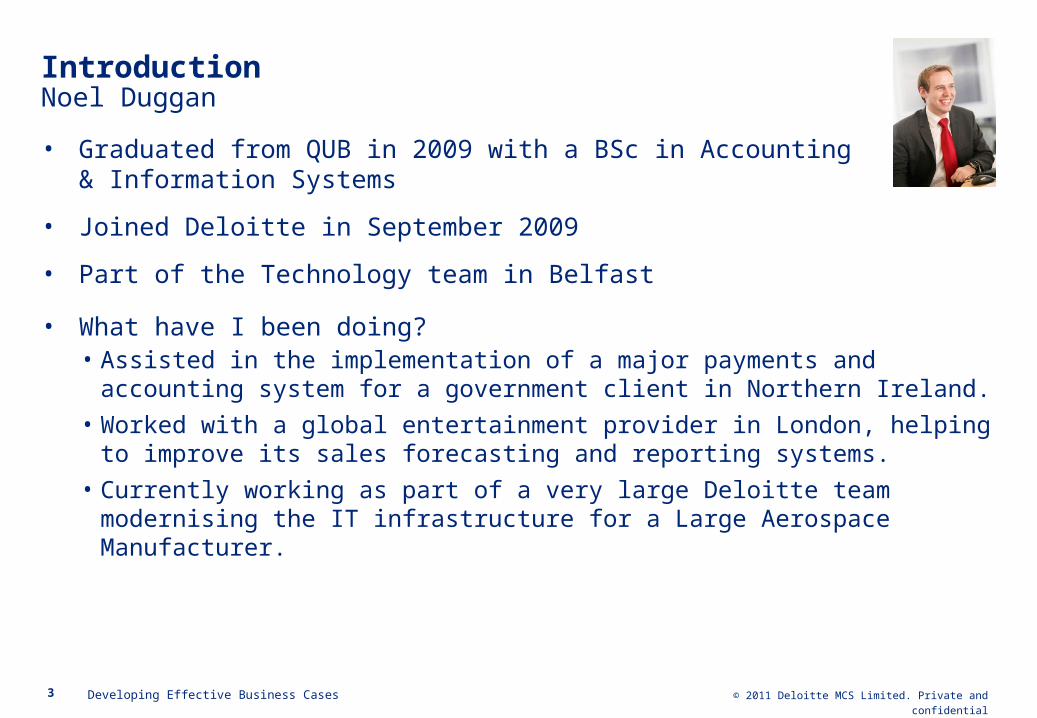

IntroductionNoel Duggan

• Graduated from QUB in 2009 with a BSc in Accounting & Information Systems

• Joined Deloitte in September 2009

• Part of the Technology team in Belfast

Developing Effective Business Cases

• What have I been doing?• Assisted in the implementation of a major payments and accounting system for a

government client in Northern Ireland.

• Worked with a global entertainment provider in London, helping to improve its sales forecasting and reporting systems.

• Currently working as part of a very large Deloitte team modernising the IT infrastructure for a Large Aerospace Manufacturer.

© 2011 Deloitte MCS Limited. Private and confidential4

Who are Deloitte?Some key facts

• Often referred to as one of the “Big 4” Professional Services firms

• Deloitte is an LLP with more than 690 Partners

• 23 recruiting offices in the UK, 140 globally

• Over 12,000 staff in the UK and 169,000 globally

• One of the largest private sector graduate recruiters in the UK, (1,100 recruits per year)

• Our clients are amongst the UK’s largest and best known companies (FTSE100 and

250)

• We came second in the Times Top 100 Graduate Employers 2011 for the 7th

consecutive year

• £1.95 billion revenue in 2010, of which consulting contributed 24%

• £10,000,000 contributed to community programmes in the UK in 2010

Careers in Consulting

What is a business case?

© 2011 Deloitte MCS Limited. Private and confidential

What is a business case?

6 Developing Effective Business Cases

Definitions of a Business Case“The business case presents clearly information necessary to support a series of decisions. These decisions, over time, increasingly commit an organisation to the achievement of the outcomes or benefits possible as a result of investment in business change” - Source OGC

“The business case is a management tool and is developed over time as a living document as the proposal develops. The Business Case keeps together and summarises the results of all the necessary research and analysis needed to support decision making in a transparent way. In its final form it becomes the key document of record for the proposal, also summarising objectives, the key features of implementation management and arrangements for post implementation evaluation” - Source HM Treasury Green Book

Attributes of an effective business case

Business cases serves to:

Act as a guide to future decision making.

Demonstrate and highlight the financial cost/benefit of a proposed project.

Inform those concerned of project possibilities and ensure they are streamlined with overall business strategy. Set out a guide for project fulfilment and best-practice guide

© 2011 Deloitte MCS Limited. Private and confidential

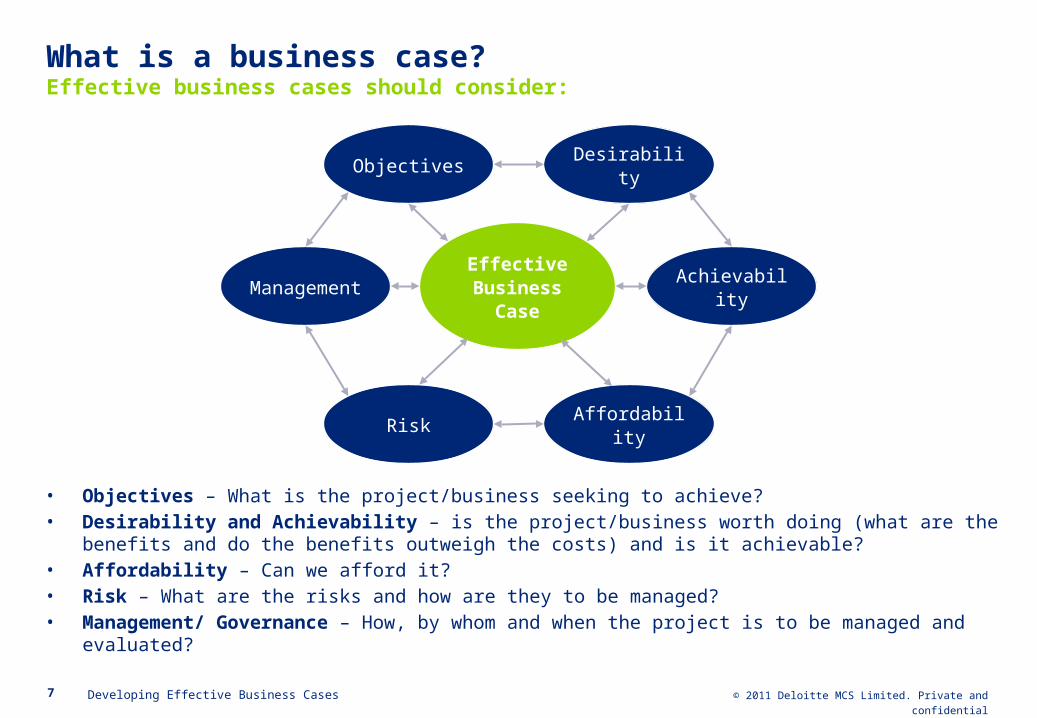

What is a business case?Effective business cases should consider:

• Objectives – What is the project/business seeking to achieve?• Desirability and Achievability – is the project/business worth doing (what are the benefits and do the benefits

outweigh the costs) and is it achievable?• Affordability – Can we afford it?• Risk – What are the risks and how are they to be managed?• Management/ Governance – How, by whom and when the project is to be managed and evaluated?

7 Developing Effective Business Cases

Achievability

Risk Affordability

Effective Business

Case

Objectives Desirability

Management

© 2011 Deloitte MCS Limited. Private and confidential

Why is a business case necessary?

8 Developing Effective Business Cases

Advantages of a Business Case

Creates

Discipline

Provides Control

Minimizes

Risk

Establish

Direction

•Creates a climate for idea creation and analysis•Outlines the issues and risk of a project before implementation • Identifies financial and business owners of a project; establishes accountability for results

•Provides a benchmark against which project performance, benefits and costs can be tracked.

•Provides a step-by-step approach

•Details future vision post project implementation

•Highlights the operational changes necessary to implement a project

• Identifies the financial impact of the project/business•Assesses the impact of the risks and rewards associated with the project/business

© 2011 Deloitte MCS Limited. Private and confidential

Who uses business cases?

9 Developing Effective Business Cases

Government Industry/Businesses Individuals

• Central• Local• QUANGO’s• Public services;

Schools, Healthcare, Police

• Business Improvements

• New Ventures

• Investment decision• Personal

opportunities e.g. Education (choosing your degree!), Career decisions.

Everyone!

What happens if business cases fail?

© 2011 Deloitte MCS Limited. Private and confidential

Public spending watchdogs attacked spiralling costs and delays in the National Offender Management information system (C-Nomis) 12 March 2009

Officials in charge of the scheme - abandoned after costs trebled - lacked even a "minimum level of competence", the Public Accounts Committee found. It highlighted a "culture of over-optimism" and lack of "rigorous" scrutiny of the scheme.

C-Nomis was treated as an IT project and not a business-change programme, project management was poor, and contracts with suppliers were weak.

3 Nov 2009

A £234m “C-Nomis” IT system for Prisons failed in almost every possible way... 12 March 2009

12 March 2009

Example 1: C-NOMIS

© 2011 Deloitte MCS Limited. Private and confidential

“The main cause of [these] difficulties is the failure to achieve the visitor numbers and income required. The targets were highly ambitious and inherently risky leading to a significant degree of financial exposure on the project. In addition, the task of managing the project has been complicated by the complex organisational arrangements put in place from the outset, and by the failure to establish sufficiently robust financial management.”- Sir John Bourn, Comptroller and Auditor General, NAO commenting on the factors contributing to the financial failure of the Millennium Dome project – Nov 2000

The bankrupt Dome 30/05/2002

Will the last person to leave the Dome turn off the lights? 01 January 2001

Duds all round: where the millennium millions sankOctober 29, 2006

Example 2: The Millennium Dome

© 2011 Deloitte MCS Limited. Private and confidential

‘The project has not delivered in line with the original intent as targets on dates, functionality, usage and levels of benefit have been delayed and reduced’

22 September 2011

£12bn NHS computer system is scrapped... and it's all YOUR money that

Labour poured down the drain!

22 September 2011

22 September 2011

A review of the National Programme for IT has decided

there is no confidence its plans will be delivered.

Example 3: National Programme for IT

22 September 2011

IT programme let down the NHS and wasted taxpayers' money by

imposing a top-down IT system on the local NHS, which didn't fit

their needs.

Journey through the business case lifecycle.

© 2011 Deloitte MCS Limited. Private and confidential

Business case development approachFollowing a stage-by-stage process enables you to create an inclusive, more effective business case ensuring you cover all the relative and important considerations

15 Developing Effective Business Cases

Stage 1

Identify need

Stage 2

Evaluate Options

Stage 3

Calculate Costs & Benefits

Stage 4

Conduct Impact Assessment

Stage 5

Present Findings

© 2011 Deloitte MCS Limited. Private and confidential

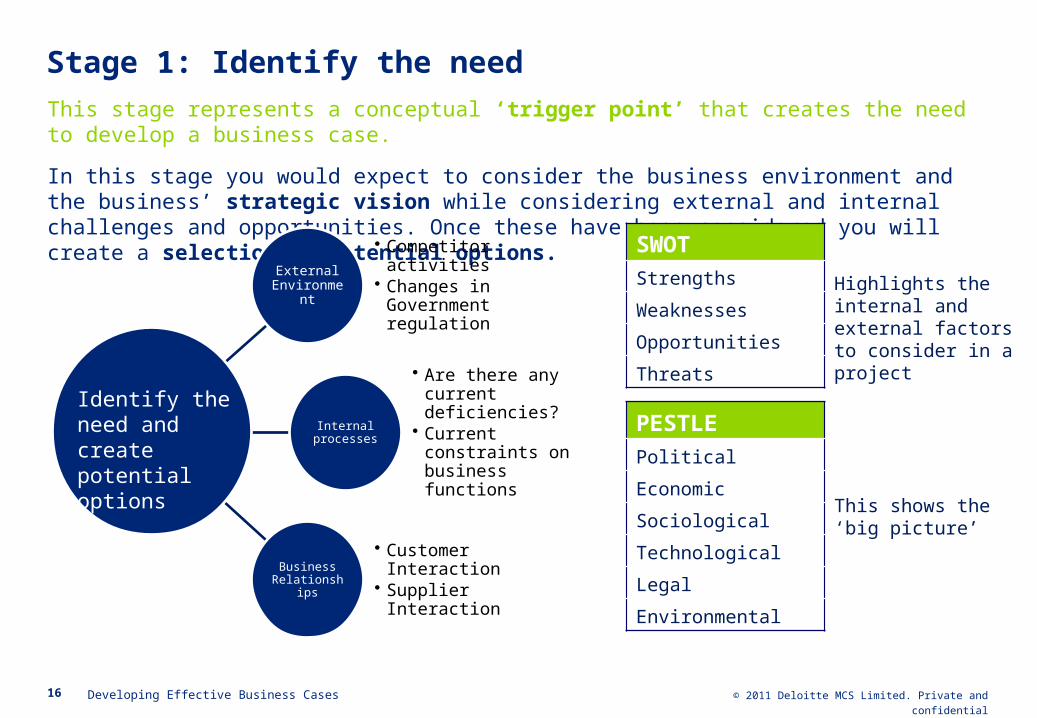

Stage 1: Identify the need

16 Developing Effective Business Cases

This stage represents a conceptual ‘trigger point’ that creates the need to develop a business case.

In this stage you would expect to consider the business environment and the business’ strategic vision while considering external and internal challenges and opportunities. Once these have been considered you will create a selection of potential options.

External Environment

• Competitor activities• Changes in

Government regulation

Internal processes

• Are there any current deficiencies?

• Current constraints on business functions

Business Relationships

• Customer Interaction

• Supplier Interaction

Identify the need and create potential options

PESTLE

Political

Economic

Sociological

Technological

Legal

Environmental

SWOT

Strengths

Weaknesses

Opportunities

Threats

This shows the ‘big picture’

Highlights the internal and external factors to consider in a project

© 2011 Deloitte MCS Limited. Private and confidential

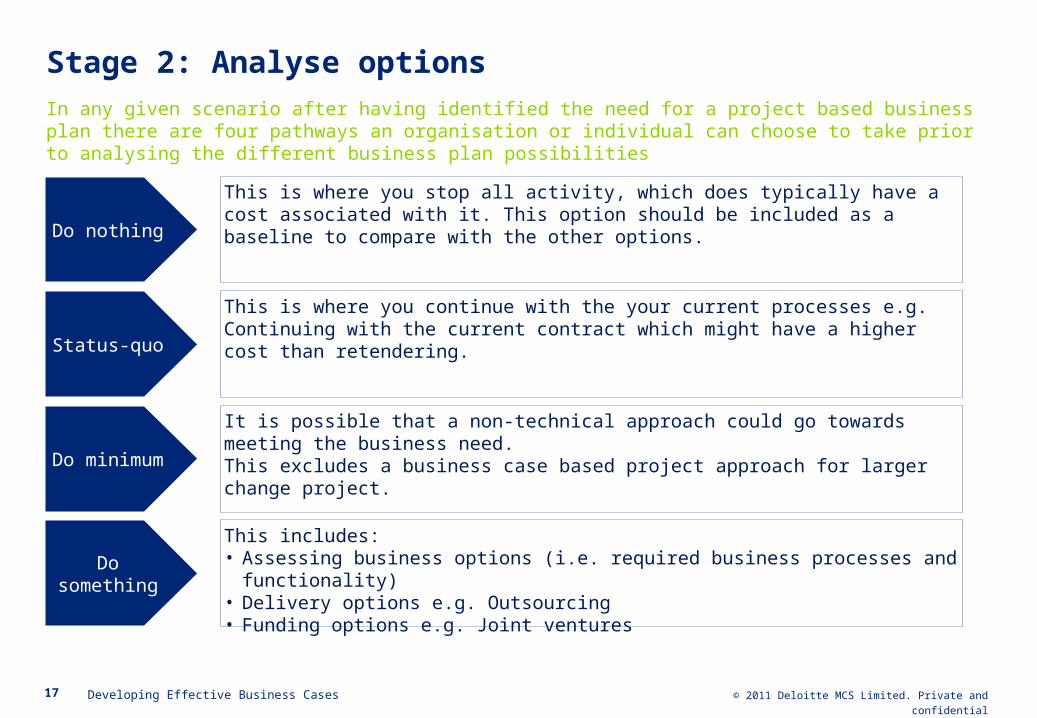

Stage 2: Analyse optionsIn any given scenario after having identified the need for a project based business plan there are four pathways an organisation or individual can choose to take prior to analysing the different business plan possibilities

17 Developing Effective Business Cases

Do nothing

Do minimum

Status-quo

Do something

This is where you stop all activity, which does typically have a cost associated with it. This option should be included as a baseline to compare with the other options.

This is where you continue with the your current processes e.g. Continuing with the current contract which might have a higher cost than retendering.

It is possible that a non-technical approach could go towards meeting the business need.This excludes a business case based project approach for larger change project.

This includes:• Assessing business options (i.e. required business processes and functionality)• Delivery options e.g. Outsourcing• Funding options e.g. Joint ventures

© 2011 Deloitte MCS Limited. Private and confidential

Stage 2: Analyse options

A number of options were identified in the Identify Need stage. In this section an initial analysis of these options will be carried out. This may reduce the need to develop a business case for each option.

Developing Effective Business Cases

Feasibility? Acceptance?Suitable?

Financial ProjectMarket

Filter and streamline ideas removing those which are obviously unfeasible

Cost benefit analysis?Ranking and scoring Cost of doing nothing?

Initial Cost?Business targets and

responsibilitiesIn-line with business

strategy?

Create a detailed shortlist of options and select a preferred option

Risks

Budgetary consideration

Financial methods

Evaluation techniques

Conclusion

Brainstorm workshop

© 2011 Deloitte MCS Limited. Private and confidential

Stage 2: Determine approach

19 Developing Effective Business Cases

Opportunity Assessment /Outline Business Case (OBC)

Full Business Case (FBC)Option Analysis

Establishes the scope and scale of potential opportunities by:

• Comparing to benchmarks of other organisations, best practice, industry body research, e.g. CIPFA, SOCITM, etc

• Agreeing the size of the prize as a range. Usually done at a high level using overall numbers rather than detailed analysis, e.g. total staffing numbers rather than detailed analysis of work done by each team.

Suitable when:

• The scope/opportunity is not well understood, i.e. the project is very early in it’s inception and indicative cost/benefit is required

• The project is similar in nature to one carried out before

• The financial benefits are likely to be low (i.e. the project has non-financial drivers

Establishes the scope and scale of potential opportunities by:

• Outlining all sensible options agreed with the client and providing a summary analysis of each (as for opportunity assessment)

• Defining the recommended option and providing a more detailed analysis of this option (closer to full business case).

Suitable when:

• Either an Opportunity Assessment or Full Business Case may be required

• A range of potential options need to be assessed to determine the way forward.

• Recommended option is derived from scoring against agreed criteria, e.g. financial case, political priorities, service improvement

Establishes the scope and scale of potential opportunities by:

• Producing a financial analysis of the current and future positions to provide a detailed picture of the costs / benefits, e.g. activity based costing or an analysis of work done by each team compared with future work following new system implementation.

• Producing a phased benefits case and implementation plan

Suitable when:

• The size of investment is high• The cost/benefit of different options needs to

be well understood• The viability of carrying out the project is in

question

An Outline Business Case document can be as long as or longer than a Full Business Case!

When considering the options you have selected during the Analysis stage you can then choose to approach your business case project through three methods.

Business case stage 3:Calculate costs and benefits

© 2011 Deloitte MCS Limited. Private and confidential

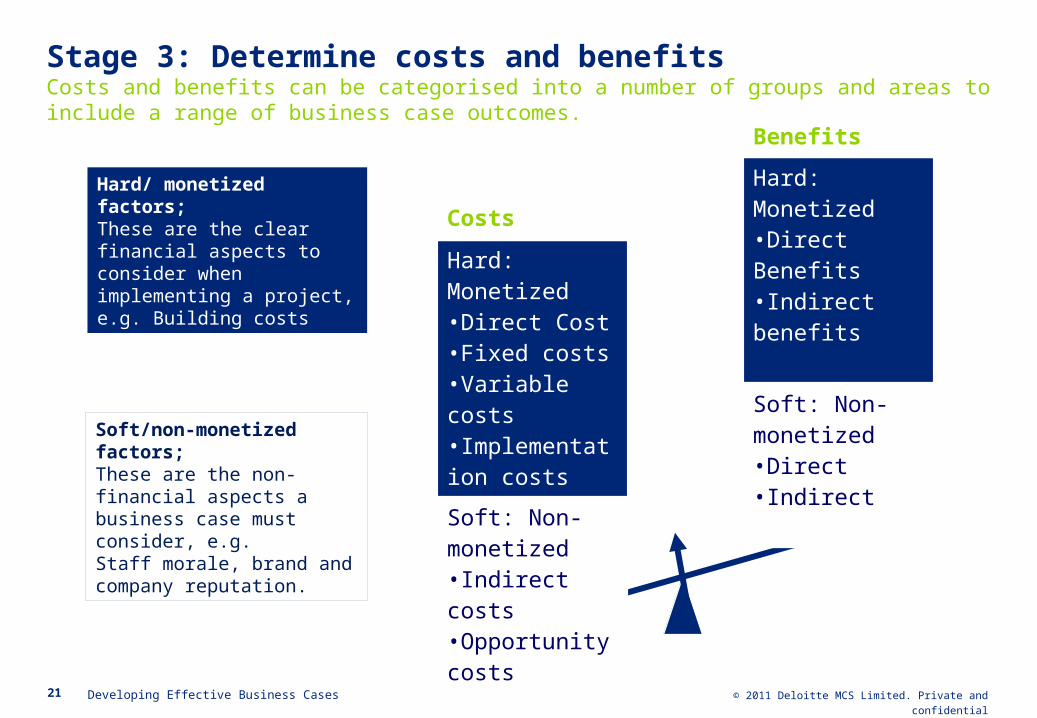

Stage 3: Determine costs and benefitsCosts and benefits can be categorised into a number of groups and areas to include a range of business case outcomes.

21 Developing Effective Business Cases

Costs

Hard: Monetized•Direct Cost•Fixed costs•Variable costs•Implementation costs

Soft: Non-monetized•Indirect costs•Opportunity costs

Benefits

Hard: Monetized•Direct Benefits•Indirect benefits

Soft: Non-monetized•Direct•Indirect

Hard/ monetized factors;These are the clear financial aspects to consider when implementing a project, e.g. Building costs

Soft/non-monetized factors;These are the non-financial aspects a business case must consider, e.g.Staff morale, brand and company reputation.

© 2011 Deloitte MCS Limited. Private and confidential

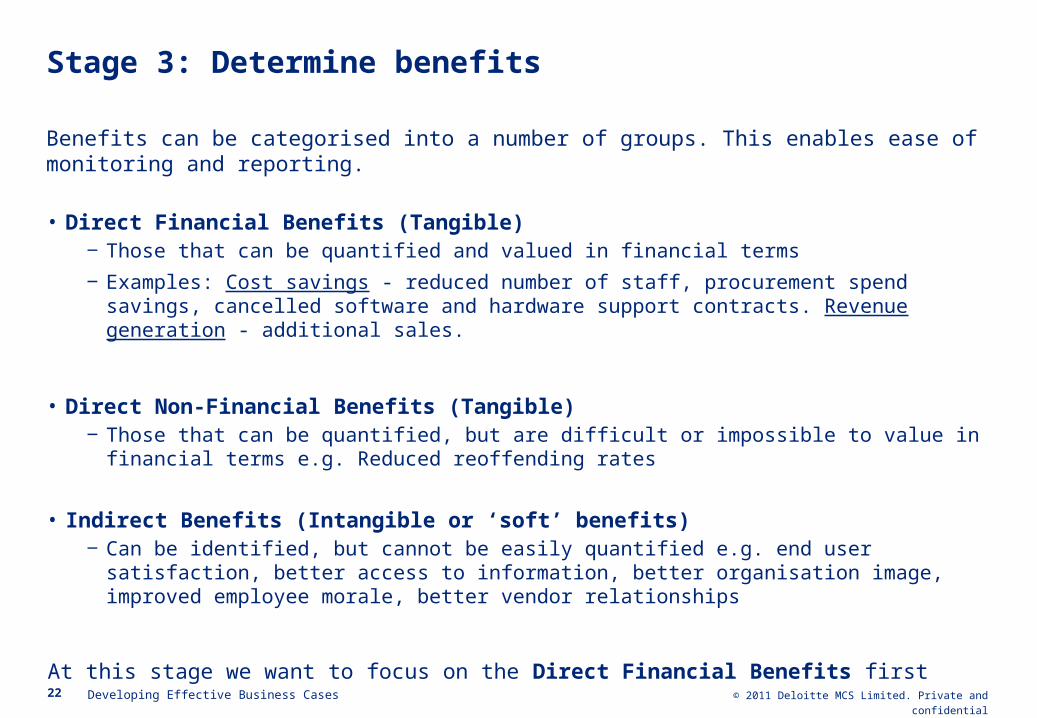

Stage 3: Determine benefits

Benefits can be categorised into a number of groups. This enables ease of monitoring and reporting.

• Direct Financial Benefits (Tangible)‒ Those that can be quantified and valued in financial terms

‒ Examples: Cost savings - reduced number of staff, procurement spend savings, cancelled software and hardware support contracts. Revenue generation - additional sales.

• Direct Non-Financial Benefits (Tangible)‒ Those that can be quantified, but are difficult or impossible to value in financial terms e.g. Reduced

reoffending rates

• Indirect Benefits (Intangible or ‘soft’ benefits)‒ Can be identified, but cannot be easily quantified e.g. end user satisfaction, better access to

information, better organisation image, improved employee morale, better vendor relationships

At this stage we want to focus on the Direct Financial Benefits first

22 Developing Effective Business Cases

© 2011 Deloitte MCS Limited. Private and confidential

Stage 3: Determine costs

23 Developing Effective Business Cases

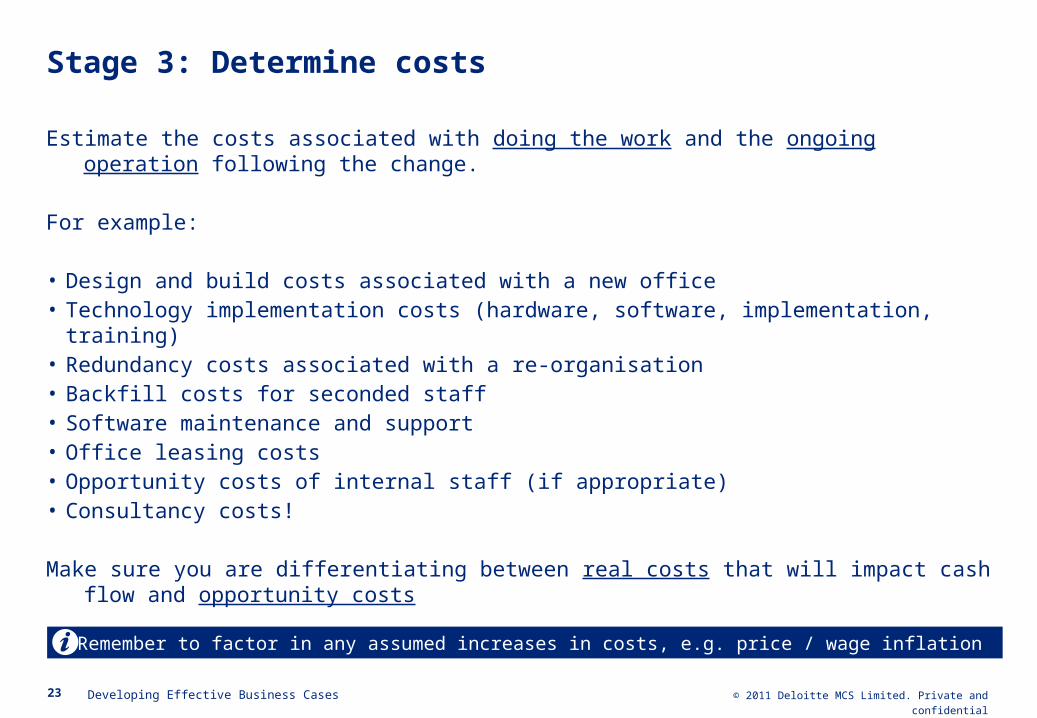

Estimate the costs associated with doing the work and the ongoing operation following the change.

For example:

• Design and build costs associated with a new office• Technology implementation costs (hardware, software, implementation, training)• Redundancy costs associated with a re-organisation• Backfill costs for seconded staff• Software maintenance and support• Office leasing costs• Opportunity costs of internal staff (if appropriate)• Consultancy costs!

Make sure you are differentiating between real costs that will impact cash flow and opportunity costs

Remember to factor in any assumed increases in costs, e.g. price / wage inflation

© 2011 Deloitte MCS Limited. Private and confidential

Stage 3: Determine costs

24 Developing Effective Business Cases

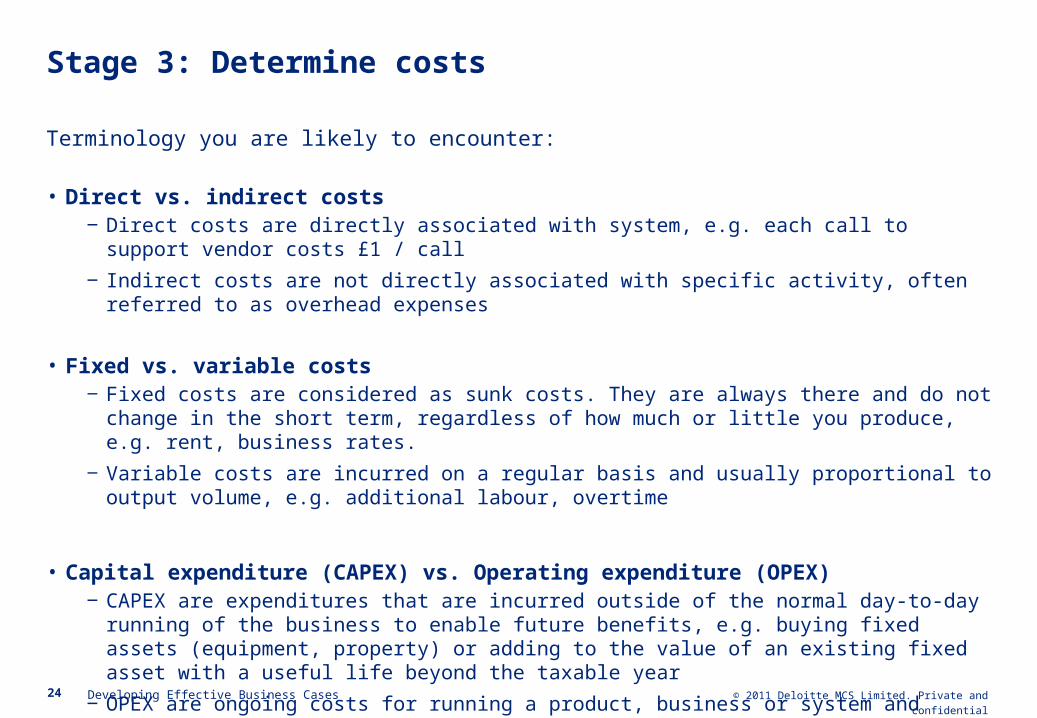

Terminology you are likely to encounter:

• Direct vs. indirect costs ‒ Direct costs are directly associated with system, e.g. each call to support vendor costs £1 / call

‒ Indirect costs are not directly associated with specific activity, often referred to as overhead expenses

• Fixed vs. variable costs ‒ Fixed costs are considered as sunk costs. They are always there and do not change in the short

term, regardless of how much or little you produce, e.g. rent, business rates.

‒ Variable costs are incurred on a regular basis and usually proportional to output volume, e.g. additional labour, overtime

• Capital expenditure (CAPEX) vs. Operating expenditure (OPEX)‒ CAPEX are expenditures that are incurred outside of the normal day-to-day running of the business

to enable future benefits, e.g. buying fixed assets (equipment, property) or adding to the value of an existing fixed asset with a useful life beyond the taxable year

‒ OPEX are ongoing costs for running a product, business or system and include the cost of workers and facility expenses such as rent and utilities

© 2011 Deloitte MCS Limited. Private and confidential

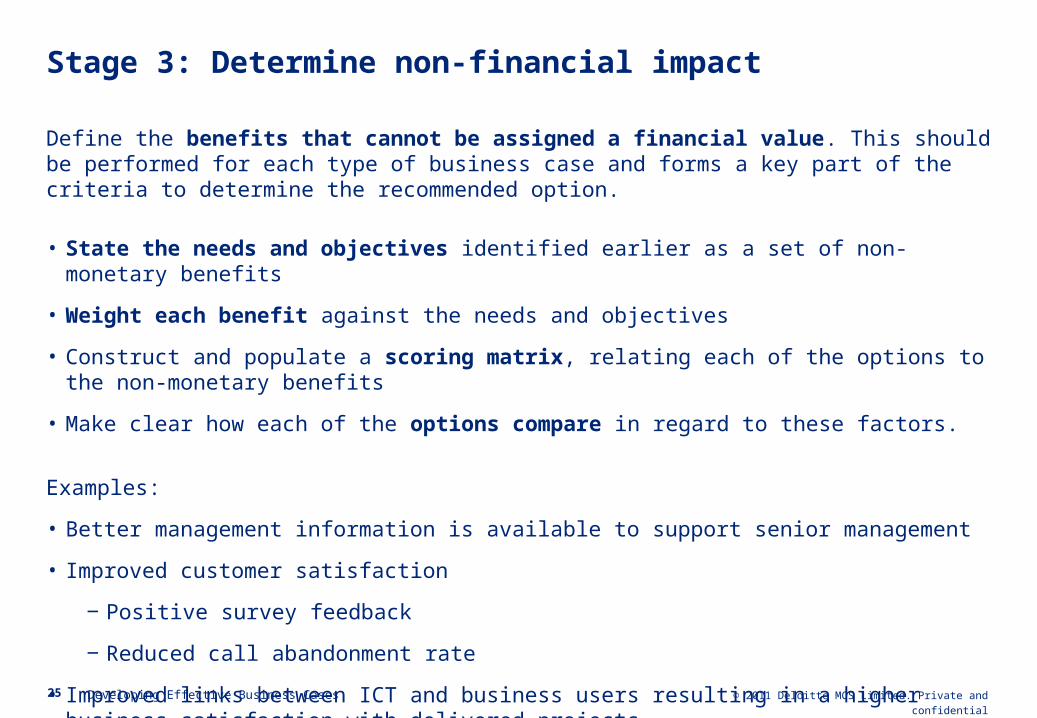

Stage 3: Determine non-financial impact

25 Developing Effective Business Cases

Define the benefits that cannot be assigned a financial value. This should be performed for each type of business case and forms a key part of the criteria to determine the recommended option.

• State the needs and objectives identified earlier as a set of non-monetary benefits

• Weight each benefit against the needs and objectives

• Construct and populate a scoring matrix, relating each of the options to the non-monetary benefits

• Make clear how each of the options compare in regard to these factors.

Examples:

• Better management information is available to support senior management

• Improved customer satisfaction

‒ Positive survey feedback

‒ Reduced call abandonment rate

• Improved links between ICT and business users resulting in a higher business satisfaction with delivered projects

Business case stage 4:Conduct impact assessment

© 2011 Deloitte MCS Limited. Private and confidential

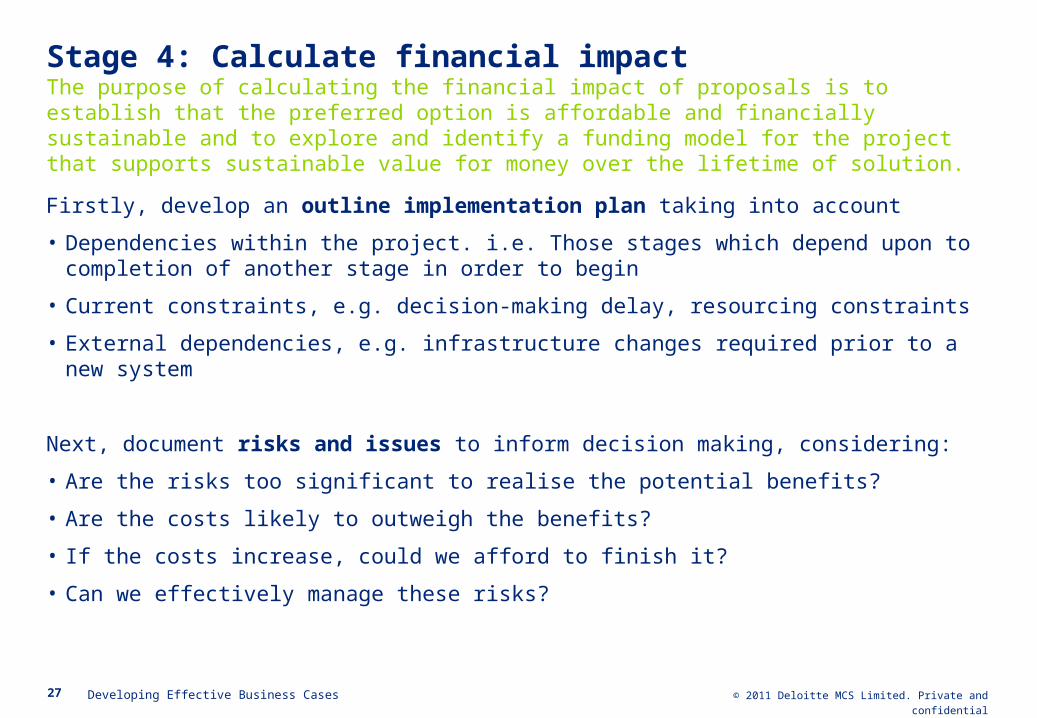

Stage 4: Calculate financial impactThe purpose of calculating the financial impact of proposals is to establish that the preferred option is affordable and financially sustainable and to explore and identify a funding model for the project that supports sustainable value for money over the lifetime of solution.

27 Developing Effective Business Cases

Firstly, develop an outline implementation plan taking into account

• Dependencies within the project. i.e. Those stages which depend upon to completion of another stage in order to begin

• Current constraints, e.g. decision-making delay, resourcing constraints

• External dependencies, e.g. infrastructure changes required prior to a new system

Next, document risks and issues to inform decision making, considering:

• Are the risks too significant to realise the potential benefits?

• Are the costs likely to outweigh the benefits?

• If the costs increase, could we afford to finish it?

• Can we effectively manage these risks?

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Calculate financial impactThe purpose of calculating the financial impact of proposals is to establish that the preferred option is affordable and financially sustainable and to explore and identify a funding model for the project that supports sustainable value for money over the lifetime of solution.

28 Developing Effective Business Cases

Create financial schedule

Identify funding model

Assign benefits and

costs to project phases

Document risks and

issues

Outline implementation

plan

© 2011 Deloitte MCS Limited. Private and confidential

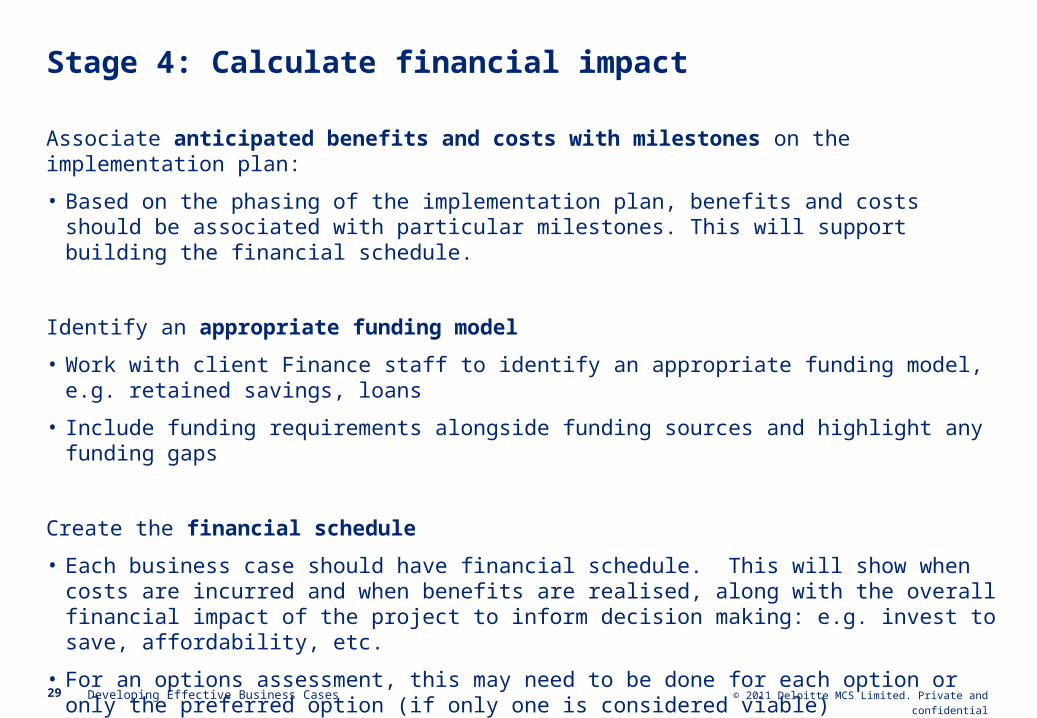

Stage 4: Calculate financial impact

29 Developing Effective Business Cases

Associate anticipated benefits and costs with milestones on the implementation plan:

• Based on the phasing of the implementation plan, benefits and costs should be associated with particular milestones. This will support building the financial schedule.

Identify an appropriate funding model

• Work with client Finance staff to identify an appropriate funding model, e.g. retained savings, loans

• Include funding requirements alongside funding sources and highlight any funding gaps

Create the financial schedule

• Each business case should have financial schedule. This will show when costs are incurred and when benefits are realised, along with the overall financial impact of the project to inform decision making: e.g. invest to save, affordability, etc.

• For an options assessment, this may need to be done for each option or only the preferred option (if only one is considered viable)

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Calculate financial impact

30 Developing Effective Business Cases

Some typical financial analysis methods include:

• Payback period

• Net Present Value

• Break-even point

• Unadjusted or 'Accounting' Rate of Return (ARR)

• Internal Rate of Return (IRR)

• Discount Rate of Return or Yield

• Benefit/ Cost Ratio

© 2011 Deloitte MCS Limited. Private and confidential

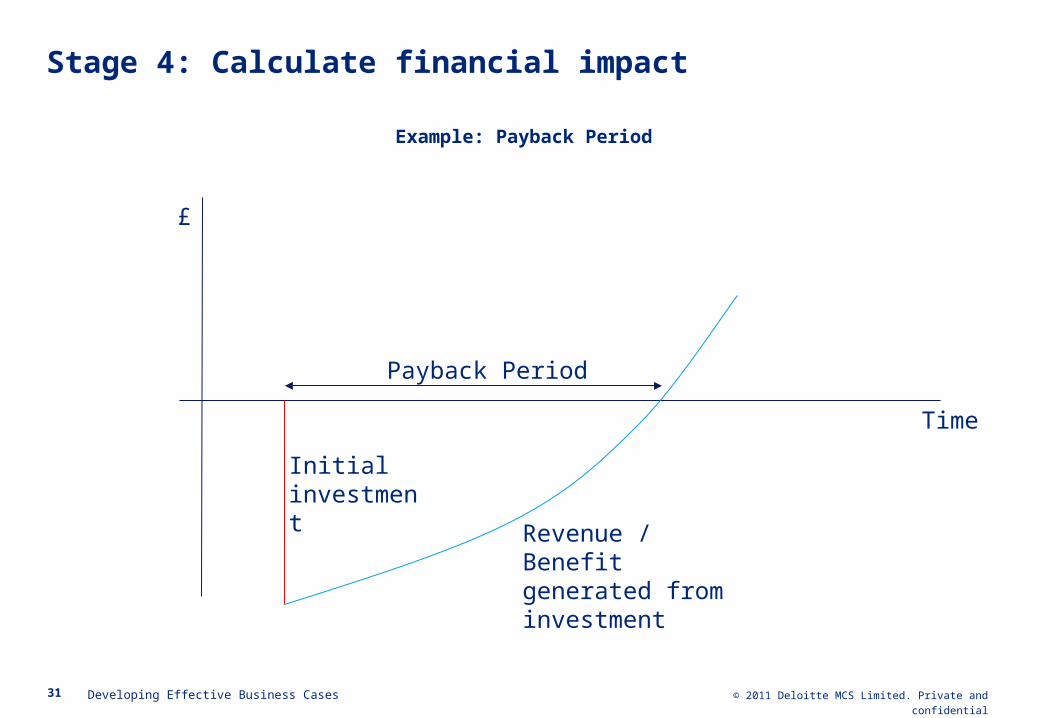

Stage 4: Calculate financial impact

31 Developing Effective Business Cases

Example: Payback Period

Time

Initial investment

Revenue / Benefit generated from investment

Payback Period

£

© 2011 Deloitte MCS Limited. Private and confidential

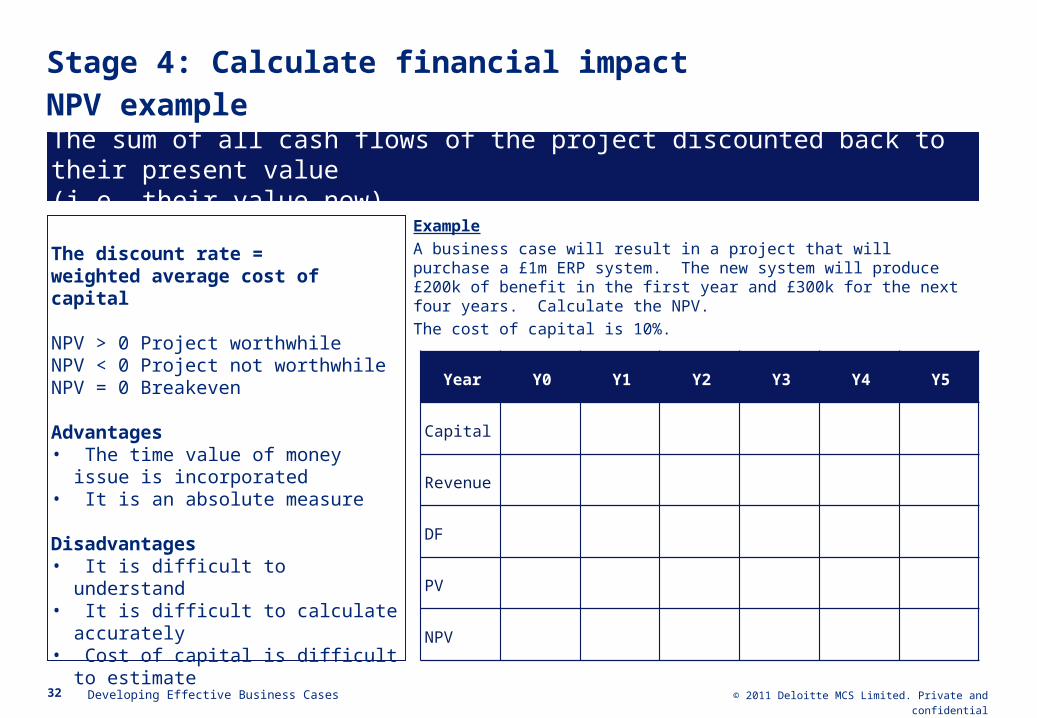

Stage 4: Calculate financial impactNPV example

32 Developing Effective Business Cases

Example

A business case will result in a project that will purchase a £1m ERP system. The new system will produce £200k of benefit in the first year and £300k for the next four years. Calculate the NPV.

The cost of capital is 10%.

The sum of all cash flows of the project discounted back to their present value (i.e. their value now)

The discount rate = weighted average cost of capital

NPV > 0 Project worthwhileNPV < 0 Project not worthwhileNPV = 0 Breakeven

Advantages• The time value of money issue is

incorporated• It is an absolute measure

Disadvantages• It is difficult to understand• It is difficult to calculate accurately• Cost of capital is difficult to estimate

Year Y0 Y1 Y2 Y3 Y4 Y5

Capital

Revenue

DF

PV

NPV

© 2011 Deloitte MCS Limited. Private and confidential

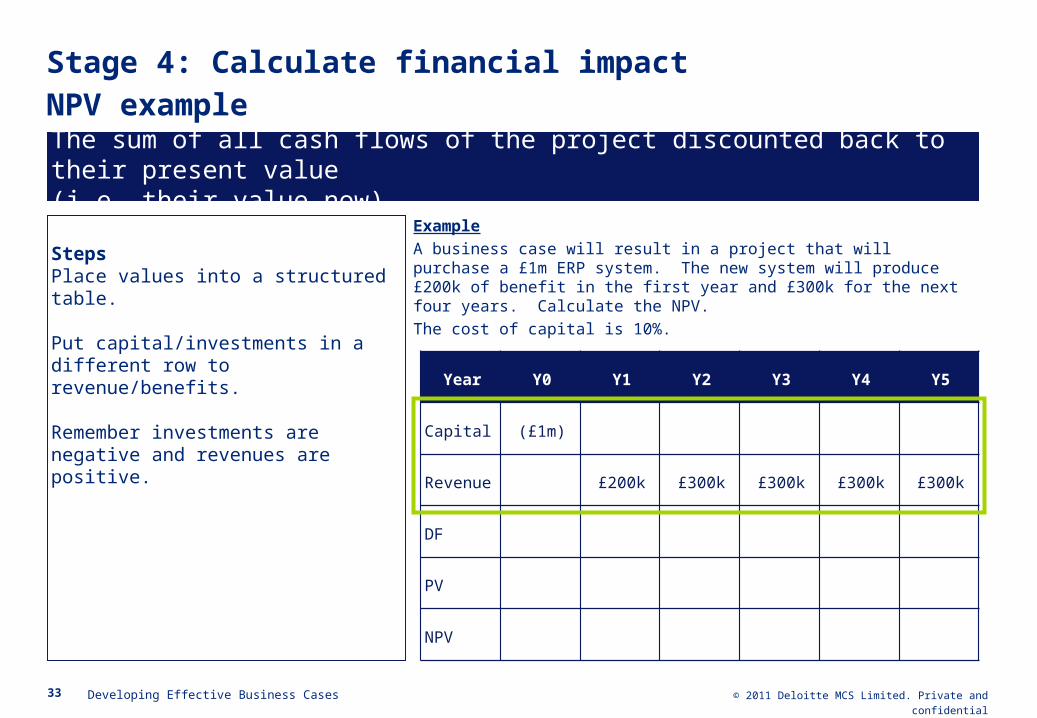

Stage 4: Calculate financial impactNPV example

33 Developing Effective Business Cases

Example

A business case will result in a project that will purchase a £1m ERP system. The new system will produce £200k of benefit in the first year and £300k for the next four years. Calculate the NPV.

The cost of capital is 10%.

The sum of all cash flows of the project discounted back to their present value (i.e. their value now)

StepsPlace values into a structured table.

Put capital/investments in a different row to revenue/benefits.

Remember investments are negative and revenues are positive.

Year Y0 Y1 Y2 Y3 Y4 Y5

Capital (£1m)

Revenue £200k £300k £300k £300k £300k

DF

PV

NPV

© 2011 Deloitte MCS Limited. Private and confidential34 Developing Effective Business Cases

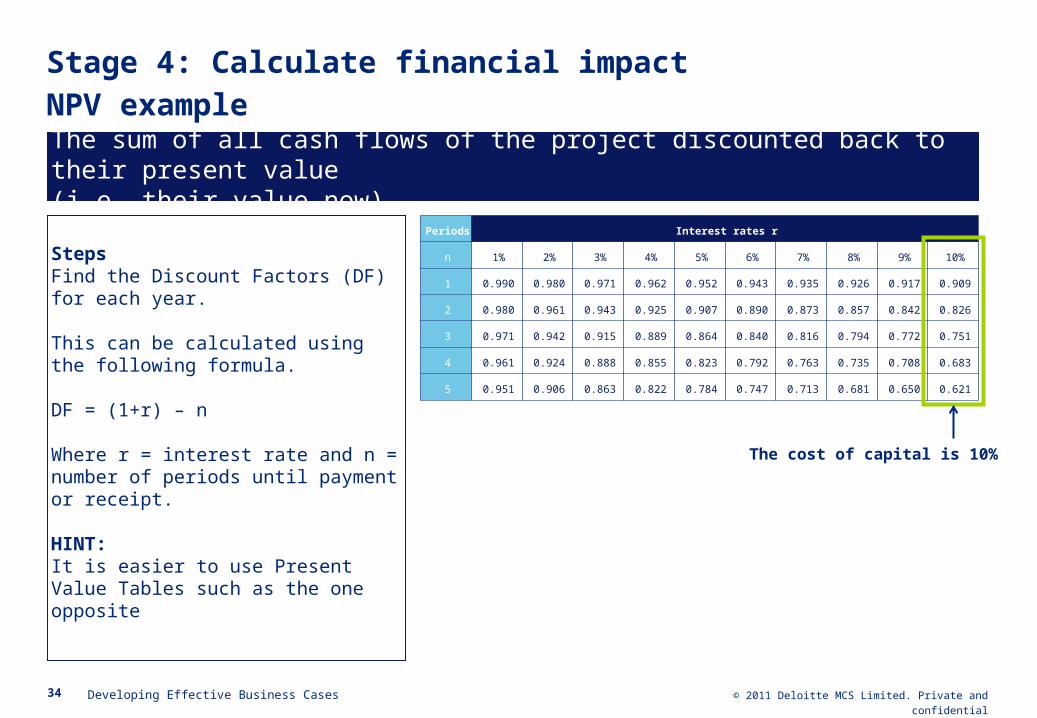

The sum of all cash flows of the project discounted back to their present value (i.e. their value now)

StepsFind the Discount Factors (DF) for each year.

This can be calculated using the following formula.

DF = (1+r) – n

Where r = interest rate and n = number of periods until payment or receipt.

HINT: It is easier to use Present Value Tables such as the one opposite

Periods Interest rates r

n 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909

2 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.857 0.842 0.826

3 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751

4 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683

5 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621

The cost of capital is 10%

Stage 4: Calculate financial impactNPV example

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Calculate financial impactNPV example

35 Developing Effective Business Cases

Example

A business case will result in a project that will purchase a £1m ERP system. The new system will produce £200k of benefit in the first year and £300k for the next four years. Calculate the NPV.

The cost of capital is 10%.

The sum of all cash flows of the project discounted back to their present value (i.e. their value now)

StepsTransfer the Discount Factors (DFs) into the table.

Year Y0 Y1 Y2 Y3 Y4 Y5

Capital (£1m)

Revenue £200k £300k £300k £300k £300k

DF 1 0.909 0.826 0.751 0.683 0.621

PV

NPV

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Calculate financial impactNPV example

36 Developing Effective Business Cases

Example

A business case will result in a project that will purchase a £1m ERP system. The new system will produce £200k of benefit in the first year and £300k for the next four years. Calculate the NPV.

The cost of capital is 10%.

The sum of all cash flows of the project discounted back to their present value (i.e. their value now)

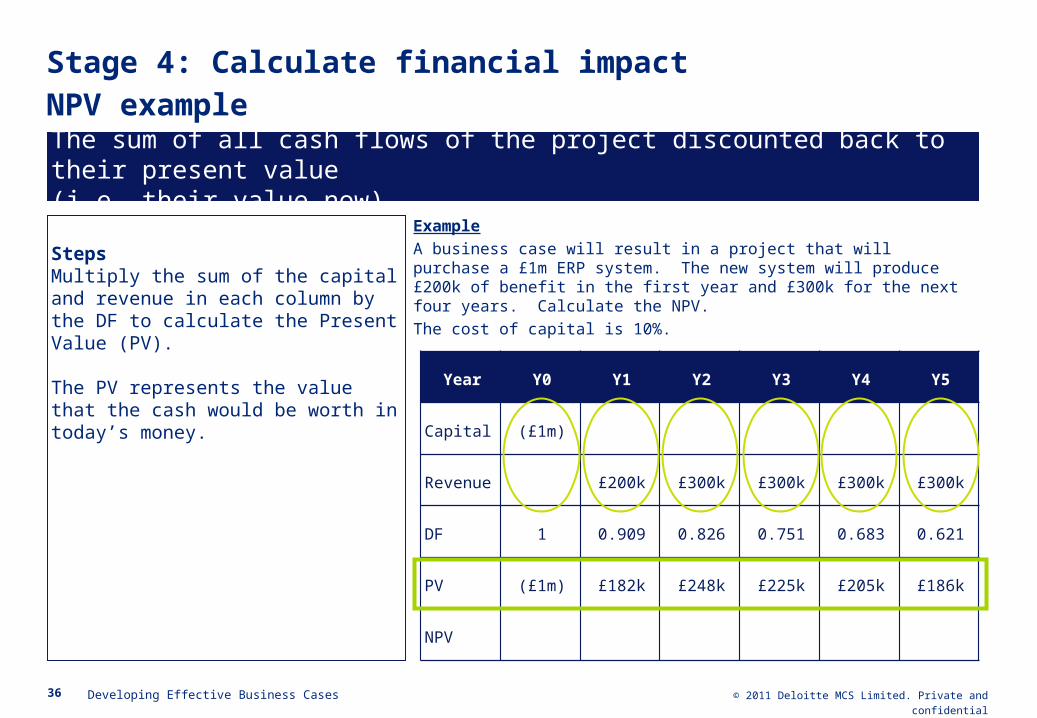

StepsMultiply the sum of the capital and revenue in each column by the DF to calculate the Present Value (PV).

The PV represents the value that the cash would be worth in today’s money. Year Y0 Y1 Y2 Y3 Y4 Y5

Capital (£1m)

Revenue £200k £300k £300k £300k £300k

DF 1 0.909 0.826 0.751 0.683 0.621

PV (£1m) £182k £248k £225k £205k £186k

NPV

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Calculate financial impactNPV example

37 Developing Effective Business Cases

Example

A business case will result in a project that will purchase a £1m ERP system. The new system will produce £200k of benefit in the first year and £300k for the next four years. Calculate the NPV.

The cost of capital is 10%.

The sum of all cash flows of the project discounted back to their present value (i.e. their value now)

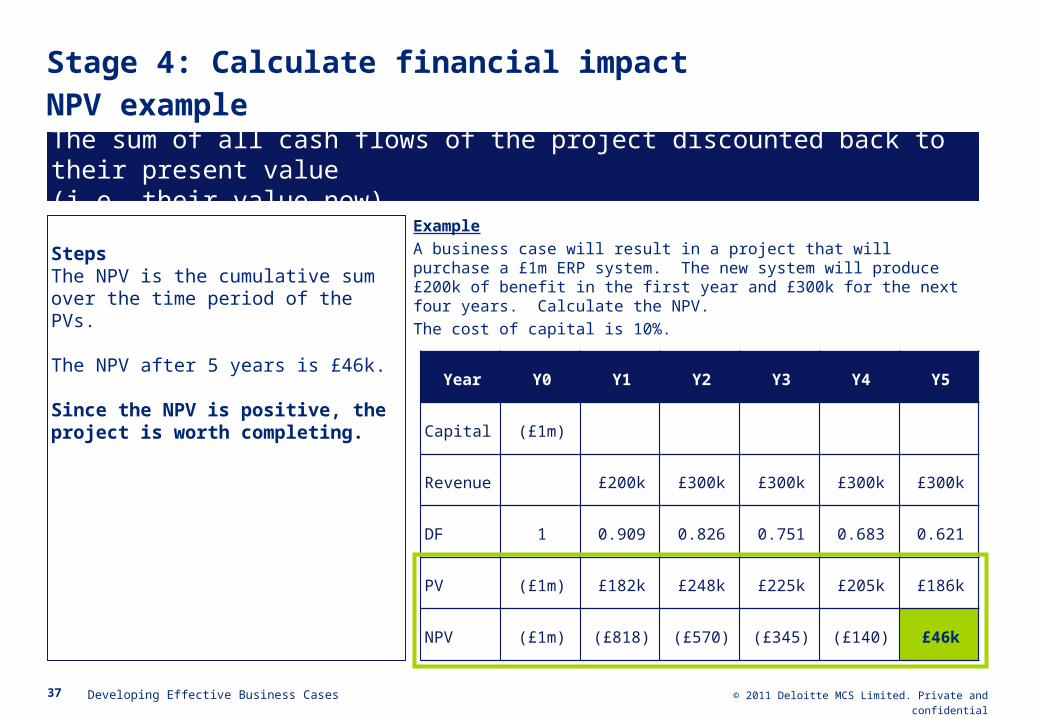

StepsThe NPV is the cumulative sum over the time period of the PVs.

The NPV after 5 years is £46k.

Since the NPV is positive, the project is worth completing.

Year Y0 Y1 Y2 Y3 Y4 Y5

Capital (£1m)

Revenue £200k £300k £300k £300k £300k

DF 1 0.909 0.826 0.751 0.683 0.621

PV (£1m) £182k £248k £225k £205k £186k

NPV (£1m) (£818) (£570) (£345) (£140) £46k

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Perform sensitivity analysis

38 Developing Effective Business Cases

Throughout the life of the project there are risks and uncertainties that can and will materialise.

Sensitivity analysis is a crucial part of a business case which:

• Tests the vulnerability of options to these uncertainties and

• Forecasts the potential impact on the costs / benefits of each option

When performing a sensitivity analysis you should consider and define:

Assumptions• Consider the assumptions that underpin the costs / benefits of each option

and what aspects of these would be sensitive to change

Scenarios• Define scenarios that represent events which could occur and cause a

deviation from plan

Mitigating actions

• For each scenario include mitigating actions that could be taken

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Perform sensitivity analysis

39 Developing Effective Business Cases

When conducted a sensitivity analysis you should consider the factors which may distort a realistic assessment of the current situation and the potential outcome of a project.

Optimism bias

Confirmation bias

Herd mentality

People expect positive future events despite lack of evidence

Optimism bias factors are expected to decrease as a project progresses

Searching/interpreting evidence in a selective manner to support pre-existing beliefs

Being influenced by peers to believe uncritically that something must be true

Be aware of accepted ‘norms’, culture and ingrained habits

© 2011 Deloitte MCS Limited. Private and confidential

Stage 4: Perform sensitivity analysis

40 Developing Effective Business Cases

Example: Corporate Jet Building Company

-200000

-100000

0

100000

200000

300000

400000

1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985Cu

mu

lati

ve C

ash

($0

00s)

Year

Fig.1 J Curve of Challenger Cash Flow Forecast with Varied Orders

Probable Cumulative Cash Flow Pessimistic Cumulative Cash Flow 40% reduction in sales Optimistic Cumulative Cash Flow 20% increase in sales

Business case stage 5:Present findings

© 2011 Deloitte MCS Limited. Private and confidential

Stage 5: Present findings

42 Developing Effective Business Cases

Document all elements produced in an easy to understand format. The format will differ depending on the type of business case.

Key sections would typically include:

• Executive Summary and Introduction

• Project Scope and Mandate

• Overview of Future Model or Options

• Benefits, both Qualitative and Quantitative

• Costs

• Project Plan / Milestones

• Financial Schedule

• Assumptions

• Risk Assessment

• Conclusions and Recommendations

© 2011 Deloitte MCS Limited. Private and confidential

Stage 5: Present findingsExamples

43 Developing Effective Business Cases

What happens once the business case is approved?

© 2011 Deloitte MCS Limited. Private and confidential

What happens next?

45 Developing Effective Business Cases

Approved business case

Benefits management

strategy & plan

Change control

Risk and issue log

Update business case

Project continues or stops

Project budget & funding

Are the costs in line with the

business case

Manage the delivery of project products / outputs

Project implementation &

plans

© 2011 Deloitte MCS Limited. Private and confidential

Business Cases – recap

What have we learned?

• The business case is a key tool used to ascertain whether a project should go ahead;

• It should also set the basis of targets to assess the performance of a project in terms of costs (budget), timescales and benefits.

• It sets a solid foundation upon which a successful project can be developed

46 Developing Effective Business Cases

© 2011 Deloitte MCS Limited. Private and confidential

Wrap up and close

47

Any further questions?

Developing Effective Business Cases

© 2011 Deloitte MCS Limited. Private and confidential

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte MCS Limited is a subsidiary of Deloitte LLP, the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte MCS Limited would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte MCS Limited accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2011 Deloitte MCS Limited. All rights reserved.

Registered office: Hill House, 1 Little New Street, London EC4A 3TR, United Kingdom. Registered in England No 3311052.

Member of Deloitte Touche Tohmatsu Limited