Macroenomic Policy Coordination: Beyond Stability

31

M. Chatib Basri Anggota Dewan Kehormatan Bank Indonesia Instiute Bank Indonesia, Aug 24, 2017 Macroeconomic Policy Coordination: beyond stability

-

Upload

abdul-hadi-ilman -

Category

Economy & Finance

-

view

149 -

download

1

Transcript of Macroenomic Policy Coordination: Beyond Stability

M. Chatib Basri

Anggota Dewan Kehormatan

Bank Indonesia Instiute

Bank Indonesia, Aug 24, 2017

Macroeconomic

Policy

Coordination: beyond stability

The macroeconomic impact of the

global volatility

2

capital

inflow

Risks of assets

re pricing

Exchange rate

?

Trade balance/ current account

deficit

commodity

price (?)Trump Effect

Economic

growth

Government

Revenue

Negative

interest

rate

The opportunities Quah (2015), the bad news about China maybe not too bad

2005: China’s GDP was $2.3 tn

China grew by 12%, its market place will increase by $274 bn

2015: China’s GDP was around $ 11.3 tn

China grew by 7%, its market place will increase by $790 bn

So China still generate economic growth in absolute magnitude 3 times larger than 2005

ASEAN still grow and remains robust

ASEAN countries can also take some market opportunities

From 2002 to its high point in 2014 Vietnam manufactured exports increased 13-fold, India nearly 6-fold and Bangladesh 5 times.

3

Indonesian economy

4

Source: CEIC (2017)

4.94 4.93

5.05

4.82

4.744.77

5.17

4.92

5.18

5.01

4.94

5.01 5.01

Jun-14 Jun-15 Jun-16 Jun-17

Indonesian GDP Growth

(% of GDP)

-10

-8

-6

-4

-2

0

2

4

6

8

10

Jun-14 Jun-15 Jun-16 Jun-17

GDP Growth by Expenditure

(yoy growth, percent)

Gross… Export

Import

InvestmentHouseholdconsumption

gov't spending

-4

-2

0

2

4

6

8

Jun-14 Jun-15 Jun-16 Jun-17

Contribution to GDP Expenditure

(Contribution to real GDP Growth yoy, percent)Household Expenditure

Government SpendingInvestment

Statistic Discrepancy

-1

3

7

Jun-14 Jun-15 Jun-16 Jun-17

Contribution to GDP by Industrial Origin

(Contribution to real GDP Growth yoy, percent)ServicesFinansial, Ownership, and BusinessTransportation and CommunicationTrade, Hotel & RestaurantConstruction

Source: IHS Markit, BI, CEIC (2017)

0

100

200

300

400

500

Jun-14 Jun-15 Jun-16 Jun-17

Retail Sales Index(2010=100)

Retail Sales Index

Stationery & Communication

Food, Drinks, and Tobacco

Other Goods: Apparel

Other Goods

Household Appliances

Spare Parts & Accessories

Cultural & Recreation

Fuels

Other Goods

-10

0

10

20

43

44

45

46

47

48

49

50

51

52

53

54

Jun-14 Jun-15 Jun-16 Jun-17

Industrial production indicators

(PMI diffusion index; industrial production

growth yoy, percent)

Industrial production, RHS

Manufacturing PMI

(35)

(30)

(25)

(20)

(15)

(10)

(5)

-

5

10

15

20

Jun-14 Jun-15 Jun-16 Jun-17

Motor vehicle sales

(seasonally-adjusted sales growth yoy,

percent)

Motor Vehicle Sales

Motorcycle sales

80

90

100

110

120

130

140

Jul-14 Jul-15 Jul-16 Jul-17

Consumer Confidence Index(Index, Weighted average of 18 cities)

Consumer ConfidenceIndex

Current Economic Condition Index

Consumer Expectation Index

Growth of real average

monthly expenditure per

capita

7

0

5

10

15

20

25

01/2011 01/2012 01/2013 01/2014 01/2015 01/2016

AverageMonthlyExpenditurepercapita

AverageMonthlyExpenditureperCapita:Urban(UR)

AverageMonthlyExpenditureperCapita:Rural(RL)

Many of the Indonesian

poor are worse off than they

were 3 years ago

8

88

90

92

94

96

98

100

102

104

106

MonthlyRealWagesIndexforFarm,Construction,Barbershop,Housekeepers

LabourWages:Farmer:perDay:Real LabourWages:ConstructionWorker:perDay:Real

LabourWages:BarbershopWoman:perPerson:Real LabourWages:Housekeeper:perMonth:Real

Can we grow more than 6%? ICOR=6.4 (ratio Investment/GDP)

1% GDP growth will require Investment/GDP 6.4%

S=I

The Indonesia Gross Domestic Savings/GDP 34.8% (World Bank)

Thus GDP Growth more or less 5-5.5%

If Indonesia wants to achieve 6% GDP growth:

I/GDP should be 6%x6.4%=38.4 %

S/GDP=35% S-I= 3.4% (current account deficit).

To get higher growth: we should increase S or lower ICOR (improve productivity and efficiency)

9

-12

-8

-4

0

4

8

Sep-13 Sep-14 Sep-15 Sep-16

Current Account

(USD billion)GoodsServicesPrimary IncomeTransferCurrent Account

The limit of monetary

policy?

10

Credit growth, consumption and

interest rate (Zahro, 2016, Basri

2016)

Consumption positively affect credit growth

Investment does not significantly affect credit growth.

BI rate does not significantly affect credit growth.

Fed fund rate significantly affects credit growth. When the fed fund rate goes up, credit growth falls. This also explains the role of liquidity inflow.

The short term problem is on the demand side

11

Undisbursed loan 12

Macroeconomic

coordination

Govt budget/ fiscal policy

Will fiscal policy promote growth?

13

Crowding out14

When a government needs to borrow money to pay for its deficit, private savers (represented by Slf above) will find lending money to the government more attractive than saving in private banks. When OJK peg the deposit rate, the government bonds is more attractive than deposit rate.

This should reduce the supply of loanable funds in the private sector, making them more scarce and driving up borrowing costs to households and firms.

Source: CEIC (2017)*from Aug 2016 Bank Indonesia adopt 7-days repo rate as new benchmark of monetary tool

-1

0

1

2

3

4

5

6

7

8

9

Jun-14 Jun-15 Jun-16 Jun-17

Policy Rate

(percent)

Indonesia

China

United Stated

EU

Japan

0

1

2

3

4

5

0

20

40

60

80

100

May-14 May-15 May-16 May-17

Banking sector indicators

(Monthly, percent)

Non performing loans (RHS)

Return on assets (RHS)

Capital adeqacy ratio

Loan to deposit ratio

0

5

10

15

20

25

30

35

May-14 May-15 May-16 May-17

Credit Growth

(yoy growth, percent)

total credit

Consumption

Investment

Working Capital

(5)

-

5

10

15

20

25

30

May-14 May-15 May-16 May-17

Deposit Growth

(yoy growth, percent)

Third Party…

Demand Deposit

Saving DepositTime Deposit

Growth of Domestic Savings, Deposit, and

Government Bond

-

5

10

15

20

25

30

35

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2011 2012 2013 2014 2015 20162017

Domestic Savings, Deposit, &

Government Bond Growth (%)

Domestic Savings

Deposit

Central Govt Debt: Government Securities

-

5

10

15

20

25

30

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2012 2013 2014 2015 2016 2017

Domestic Savings, Deposit, &

Government Bond Growth –

Moving Average (%)

Domestic Savings

Deposit

Central Govt Debt: Government Securities

Source: IMF

Simulation: Deposit vs bonds

Sjuib (2015) reinforces the same results

Crowding‐out effect exists in Indonesia: increasing public debt reduces the amount of credit given to economic agents (quantity channel) and increases the lending rate (price channel).

17

-200

-100

0

100

200

300

400

500

600

0 5 10 15 20 25 30 35

DEP

Budget: more realistic, but conservative

*outlook kementerian keuangan as of Agustus 2017

Realisasi APBN APBNP

Δ% dari

realisasi

2016

Outlook

realisasi*

Δ% dari

realisasi

2016

RAPBN

Δ% dari

outlook

2017

A. Pendapatan dan Hibah 1,555.8 1,750.3 1,736.0 11.6 1,736.1 11.6 1,878.4 8.2

1. Penerimaan Perpajakan 1,284.9 1,498.9 1,472.7 14.6 1,472.7 14.6 1,609.4 9.3

a. Pajak Dalam Negeri 1,249.4 1,464.8 1,436.8 15.0 1,436.7 15.0 1,570.7 9.3

i. Pajak Penghasilan 657.2 787.7 783.9 19.3 784.0 19.3 852.9 8.8

-Migas 36.1 35.9 41.8 15.7 41.8 15.7 35.9 (14.0)

-Non Migas 621.1 751.8 742.2 19.5 742.2 19.5 817.0 10.1

ii. Pajak Pertambahan Nilai 412.2 493.9 475.4 15.3 475.5 15.4 535.3 12.6

iii. Pajak Bumi dan Bangunan 19.4 17.3 15.4 (20.6) 15.4 (20.6) 17.4 12.7

iv. Cukai 143.5 157.2 153.4 6.9 153.2 6.7 155.4 1.5

v. Pajak Lainnya 17.2 8.7 8.7 (49.3) 8.7 (49.3) 9.7 11.4

b. Pajak Perdagangan Internasional 35.5 34.1 35.9 1.1 36.0 1.3 38.7 7.6

2. Penerimaan Bukan Pajak 261.9 250.0 260.2 (0.6) 260.2 (0.6) 267.9 2.9

a. Penerimaan Sumber Daya Alam 65.0 87.0 95.6 47.2 95.6 47.2 99.3 3.8

b. Bagian Laba BUMN 37.1 41.0 41.0 10.5 41.0 10.5 43.7 6.6

c. PNBP Lainnya 118.0 84.4 85.1 (27.9) 85.1 (27.9) 82.0 (3.7)

d. Pendapatan BLU 41.9 37.6 38.5 (8.1) 38.5 (8.1) 43.0 11.5

Hibah 9.0 1.4 3.1 (65.5) 3.1 (65.4) 1.2 (61.5)

B. Belanja Negara 1,864.3 2,080.5 2,133.2 14.4 2,098.9 12.6 2,204.4 5.0

I. Belanja Pemerintah Pusat 1,154.0 1,315.5 1,366.8 18.4 1,343.1 16.4 1,443.3 7.5

Belanja K/L 684.2 763.6 798.5 16.7 769.2 12.4 814.1 5.8

Belanja Non-K/L 469.8 552.0 568.3 21.0 573.9 22.1 629.2 9.6

a. 1. Pembayaran Kewajiban Utang 182.8 221.2 219.2 19.9 218.6 19.6 247.6 13.3

2.. Subsidi 174.2 160.1 168.9 (3.1) 168.9 (3.1) 172.4 2.1

a. Subsidi Energi 106.8 77.3 89.9 (15.9) 89.9 (15.9) 103.4 15.0

b. Subsidi Non Energi 67.4 82.7 79.0 17.2 79.0 17.2 69.0 (12.6)

II. Transfer ke Daerah 710.3 764.9 766.4 7.9 755.9 6.4 761.1 0.7

C. Keseimbangan Primer (308.5) (109.0) (178.0) (42.3) (144.3) (53.2) (78.4) (45.7)

D. Surplus/Defist (308.5) (330.2) (397.2) 28.8 (362.9) 17.6 (325.9) (10.2)

% of gdp (2.46) (2.41) (2.92) (2.67) (2.19)

E. Pembiayaan 331.0 330.2 397.2 20.0 362.9 9.6 325.9 (10.2)

2017 2018

URAIAN

2016

Monetary expansion in RAPBN 2018 is slightly smaller than

APBN-P 2017

Oil and commodity prices

-

01

01

02

02

03

03

04

04

05

05

0

50

100

150

200

250

2012 2013 2014 2015 2016 2017P 2018P

PertumbuhanVolumePerdaganganDunia(%,yoy)

BrentCrudeOil(US$perbarrel)

CommodityAgriculturalRawMaterialsIndex(2005=100)

CommodityMetalsPriceindex(2005=100)

Proyeksi pergerakan harga komoditas dan tingkatpertumbuhan volumeperdagangan dunia

2017 2018

%

- RHS

Sumber:IMF,WEOApril 2017

Source2017 2018

WTI Brent WTI Brent

Bloomberg*** 56,23 56,14 61,07 62,23

EIA** 52,50 53,50 55,18 56,18

ConsensusForecast 52,97 54,92 57,67 59,80

IMF* 54,42 56,31 54,51 55,90

WorldBank* 55,20 55,20 59,90 59,90

Rerata 54,26 55,21 57,67 58,80

19

60.00

112.7

105.8

96.510

49.210

40.160

50.00

30

40

50

60

70

80

90

100

110

120

2012 2013 2014 2015 2016 2017F 2018F

Commodity prices, export and

GDPThe Movement of Commodity Prices, Exports Growth, and GDP Growth in Indonesia

-40

-20

0

20

40

60

80

020406080

100120140160180200

Jan

-94

Ap

r-9

5

Jul-

96

Oct

-97

Jan

-99

Ap

r-0

0

Jul-

01

Oct

-02

Jan

-04

Ap

r-0

5

Jul-

06

Oct

-07

Jan

-09

Ap

r-1

0

Jul-

11

Oct

-12

Jan

-14

Ap

r-1

5

Jul-

16

Commodity Prices and Indonesian Exports Growth (Monthly Data)

Energy Price Index (USD) - LHS Non-Energy Price Index (USD) - LHS

Exports Growth (Yearly, %) - RHS

-20

-15

-10

-5

0

5

10

15

0

50

100

150

200

Mar

-94

Jun

-95

Sep

-96

Dec

-97

Mar

-99

Jun

-00

Sep

-01

Dec

-02

Mar

-04

Jun

-05

Sep

-06

Dec

-07

Mar

-09

Jun

-10

Sep

-11

Dec

-12

Mar

-14

Jun

-15

Sep

-16

Commodity Prices and Indonesian GDP Growth (Quarterly Data)

Energy Price Index (USD) - LHS Non-Energy Price Index (USD) - LHS

GDP Growth (Yearly, %) - RHS

The Movement of Commodity Prices, Exports Growth, and GDP Growth in Indonesia

-40

-20

0

20

40

60

80

020406080

100120140160180200

Jan

-94

Ap

r-9

5

Jul-

96

Oct

-97

Jan

-99

Ap

r-0

0

Jul-

01

Oct

-02

Jan

-04

Ap

r-0

5

Jul-

06

Oct

-07

Jan

-09

Ap

r-1

0

Jul-

11

Oct

-12

Jan

-14

Ap

r-1

5

Jul-

16

Commodity Prices and Indonesian Exports Growth (Monthly Data)

Energy Price Index (USD) - LHS Non-Energy Price Index (USD) - LHS

Exports Growth (Yearly, %) - RHS

-20

-15

-10

-5

0

5

10

15

0

50

100

150

200

Mar

-94

Jun

-95

Sep

-96

Dec

-97

Mar

-99

Jun

-00

Sep

-01

Dec

-02

Mar

-04

Jun

-05

Sep

-06

Dec

-07

Mar

-09

Jun

-10

Sep

-11

Dec

-12

Mar

-14

Jun

-15

Sep

-16

Commodity Prices and Indonesian GDP Growth (Quarterly Data)

Energy Price Index (USD) - LHS Non-Energy Price Index (USD) - LHS

GDP Growth (Yearly, %) - RHS

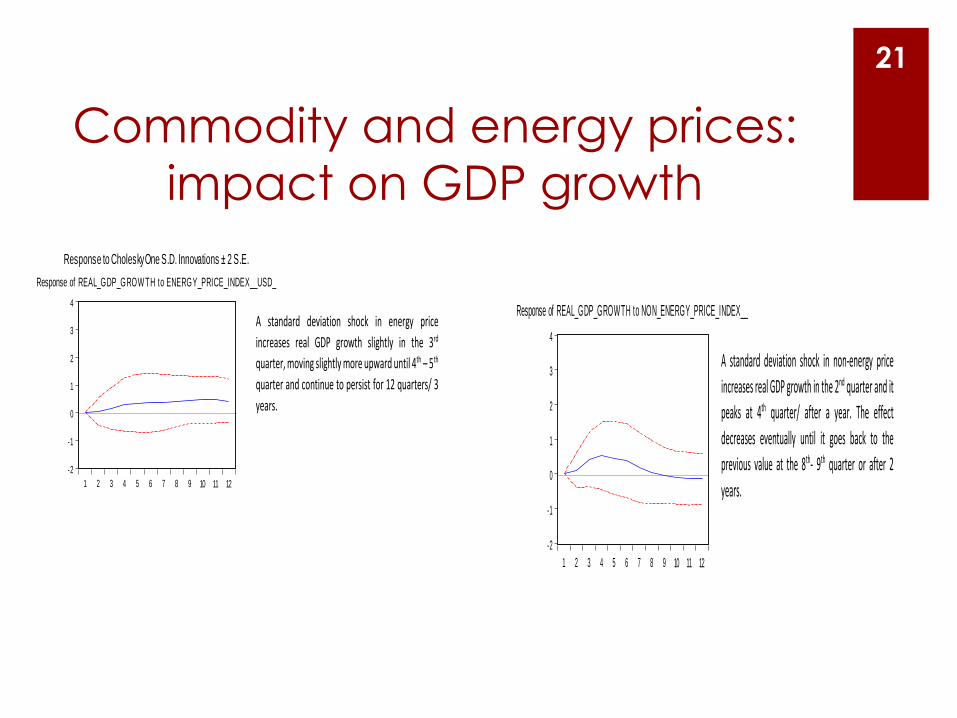

20

Commodity and energy prices:

impact on GDP growth

-2

-1

0

1

2

3

4

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP_GROW TH to REAL_GDP_GROW TH

-2

-1

0

1

2

3

4

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP_GROW TH to ENERGY_PRICE_INDEX__USD_

-2

-1

0

1

2

3

4

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP_GROWTH to NON_ENERGY_PRICE_INDEX__

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to REAL_GDP_GROW TH

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to ENERGY_PRICE_INDEX__USD_

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to NON_ENERGY_PRICE_INDEX__

-4

0

4

8

12

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to REAL_GDP_GROW TH

-4

0

4

8

12

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to ENERGY_PRICE_INDEX__USD_

-4

0

4

8

12

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to NON_ENERGY_PRICE_INDEX__

Response to Cholesky One S.D. Innovations ± 2 S.E.

IV. Impulse Response Function of Commodity Prices to Real GDP

Variables: Index of Energy and Non-Energy Price, and GDP in Constant Price (Quarterly Data)

IV. Impulse Response Function of Commodity Prices to Real GDP Growth

Variables: Index of Energy and Non-Energy Price, and Real GDP Growth (Quarterly Data)

-20,000

0

20,000

40,000

60,000

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP to REAL_GDP

-20,000

0

20,000

40,000

60,000

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP to ENERGY_PRICE_INDEX__USD_

-20,000

0

20,000

40,000

60,000

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP to NON_ENERGY_PRICE_INDEX__

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to REAL_GDP

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to ENERGY_PRICE_INDEX__USD_

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to NON_ENERGY_PRICE_INDEX__

-2

0

2

4

6

8

10

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to REAL_GDP

-2

0

2

4

6

8

10

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to ENERGY_PRICE_INDEX__USD_

-2

0

2

4

6

8

10

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to NON_ENERGY_PRICE_INDEX__

Response to Cholesky One S.D. Innovations ± 2 S.E.

-20,000

0

20,000

40,000

60,000

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP to REAL_GDP

-20,000

0

20,000

40,000

60,000

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP to ENERGY_PRICE_INDEX__USD_

-20,000

0

20,000

40,000

60,000

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP to NON_ENERGY_PRICE_INDEX__

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to REAL_GDP

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to ENERGY_PRICE_INDEX__USD_

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to NON_ENERGY_PRICE_INDEX__

-2

0

2

4

6

8

10

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to REAL_GDP

-2

0

2

4

6

8

10

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to ENERGY_PRICE_INDEX__USD_

-2

0

2

4

6

8

10

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to NON_ENERGY_PRICE_INDEX__

Response to Cholesky One S.D. Innovations ± 2 S.E.

A standard deviation shock in energy price

increases real GDP in the second quarter and the

effect continue to increase until more than 12

quarters/ 3 years.

A standard deviation shock in non-energy price

increases real GDP in the third quarter and the

same effect persists until the 12th quarter/ for 3

years.

A standard deviation shock in energy price

increases real GDP growth slightly in the 3rd

quarter, moving slightly more upward until 4th – 5th

quarter and continue to persist for 12 quarters/ 3

years.

-2

-1

0

1

2

3

4

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP_GROWTH to REAL_GDP_GROWTH

-2

-1

0

1

2

3

4

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP_GROWTH to ENERGY_PRICE_INDEX__USD_

-2

-1

0

1

2

3

4

1 2 3 4 5 6 7 8 9 10 11 12

Response of REAL_GDP_GROWTH to NON_ENERGY_PRICE_INDEX__

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to REAL_GDP_GROWTH

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to ENERGY_PRICE_INDEX__USD_

-10

-5

0

5

10

15

20

1 2 3 4 5 6 7 8 9 10 11 12

Response of ENERGY_PRICE_INDEX__USD_ to NON_ENERGY_PRICE_INDEX__

-4

0

4

8

12

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to REAL_GDP_GROWTH

-4

0

4

8

12

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to ENERGY_PRICE_INDEX__USD_

-4

0

4

8

12

1 2 3 4 5 6 7 8 9 10 11 12

Response of NON_ENERGY_PRICE_INDEX__ to NON_ENERGY_PRICE_INDEX__

Response to Cholesky One S.D. Innovations ± 2 S.E.

A standard deviation shock in non-energy price

increases real GDP growth in the 2nd quarter and it

peaks at 4th quarter/ after a year. The effect

decreases eventually until it goes back to the

previous value at the 8th- 9th quarter or after 2

years.

21

Challenges to the future

22

New normal growth?

Success story of East Asia: Industrialization and

trade

A world with creeping protectionism

Services is not a perfect substitute to

manufacturing

23

Why services are not like manufactures

Taken from Dani Rodrik (2014)

High-productivity (tradable) services

sector cannot absorb as much labor

Preimum skill-intensive

Requires good institution

Low productivity (non-tradable) services cannot

act as growth poles

since they cannot expand without turning their terms

of trade against themselves

continued expansion in one segment relies on

expansion on others

limited gains from sectoral “winners”

Indonesia: GDP growth and

terms of trade

2003

2004

20052006

2007

2008

2009

2010 20112012

2013

2014

4.0

4.5

5.0

5.5

6.0

6.5

20 30 40 50 60 70 80 90 100 110 120

GDPGrowth(%,Y)andOilPrice(USD/barrel,X):Indonesia

2003

2004

20052006

2007

2008

2009

2010 20112012

2013

2014

4.0

4.5

5.0

5.5

6.0

6.5

100 105 110 115 120 125 130 135 140

GDPGrowth(%,Y)andTermsofTrade(Index2000=100,X):Indonesia

Indonesia could do more in promoting new export

Basri and Rahardja (2011)

Growth of manufactured

exports, 2002-2016

Indon

esia

Vietn

amIndia Kenya

Bangl

adeshPeru

Thaila

nd

Growth 2002-2016 136% 1631% 558% 440% 525% 295% 262%

Value 2016, bn $69 $143 $198 $3 $35 $5 $181

0%250%500%750%

1000%1250%1500%

Taken from Papanek, 2017

High minimum wages make

Indonesia’s exports less

competitive Indonesia’s high minimum wages,

especially in Jakarta, make the country’s exports less competitive.

Indonesia’s competitors also have problems with infrastructure and over-regulation, but since wages are lower their firms are taking over Indonesia’s markets.

Raising the minimum wage does not help the poor, who earn much less than the minimum wage in the agricultural and informal sectors.

04080

120160200240

Monthly Minimum wages in

US$*2015

2016

*Monthly wage in most

expensive region

Taken from Papanek, 2017

Export volatility and

concentrationFigure 8: Export volatility and concentration in medium & high tech manufacturing

Figure 9: Export Volatility and concentration in resource based manufacturing

Development challenges are

beyond macro-stability

30

Brazil China India Indonesia Malaysia Philippines Thailand Vietnam

Characteristics (2013)

Population (person mn) 200.4 1,357.4

1,252.

1 249.9 29.7 98.4 67.0 89.7

GDP Per Capita (in PPP, USD) 5,823 3,583 1,165 1,810 6,998 1,581 3,438 1,029

Density (person/sq km) 24.0 144.6 421.1 137.9 90.4 330.0 131.2 289.3

Real Exchange Rate Movement (%)

2003-2013 (average 68.3 31.4 -0.3 6.4 2.5 39.2 25.0 50.9

PISA Test Score (2012)

Math 391 613 351* 375 421 427 511

Science 406 580 348* 382 420 438 528

Broadband Penetration

Fixed (wired)-broadband

subscriptions per 100 inhabitants

(2013)

10.08 13.36 1.16 1.3 8.22 9.12 7.36 5.62

Logistics Performance Index (2014) 2.94 3.53 3.08 3.08 3.59 3.00 3.43 3.15

Percentage of shipment met quality 82 76 67 70 97 71 83 76

Government effectiveness score -0.08 -0.03 -0.19 -0.24 1.10 0.06 0.21 -0.30* Tamil Nadu dan Himachal Pradesh Sources: World Bank, ITU, BIIS and others

Thank you

31