Macroeconomic Policy and Aggregate Demand and Supply Analysis · PDF fileMacroeconomic Policy...

37

Macroeconomic Policy and Aggregate Demand and Supply Analysis Reference : Mishkin, Macroeconomics: Policy and Practice, Chapter 12-13

Transcript of Macroeconomic Policy and Aggregate Demand and Supply Analysis · PDF fileMacroeconomic Policy...

MacroeconomicPolicyand

AggregateDemandandSupplyAnalysis

Reference:Mishkin,Macroeconomics:PolicyandPractice,Chapter12-13

TheObjectivesofMacroeconomic Policy

• Twoprimaryobjectivesofmacroeconomicpolicy:

– Stabilizingeconomicactivity

– Stabilizinginflationaroundalowlevel

StabilizingEconomicActivity• Economic activity is commonly gauged by theunemployment rate because high unemployment:– causes human misery– leaves workers and other resources idle, reducing output

• Instead of a zero rate of unemployment, policymakerstarget the nature rate of unemployment that isconsistent with the maximum sustainable level ofemployment at which there is no tendency for inflationto increase

StabilizingEconomicActivity(cont’d)

• The natural rate of unemployment includes:

• Frictional unemployment—exists when workers and firms needtime to make suitablematchups

• Structural unemployment—exists as a mismatch between jobskill requirements and worker availability

• At the natural rate of unemployment, output movestowards potential output, so the output gap (Y-YP) is zero

StabilizingEconomicActivity(cont’d)

• Inpractice,identifyingthenaturalrateofunemploymentisnotstraightforward

• Currently,mosteconomistsbelievethenaturalrateofunemploymentisaround5%,butstillitissubjecttomuchuncertaintyanddisagreement

StabilizingInflation:PriceStability

• High inflation is always accompanied by high variability ofinflation, so it reduces economic growth

• So central banks pursue a policy goal of price stability—low and stable inflation

• Monetary policy is to maintain inflation, π , close to aninflation target, πT—a target level that is slightly abovezero, so that the inflation gap (π - πT) is minimized

EstablishingHierarchicalVersusDualMandates

• A hierarchical mandate requires stable prices as acondition of pursuing other goals– Adopted by the European Central Bank (through the

Masstricht Treaty), the Bank of England, the Bank of Canada,and the Reserve Bank of New Zealand

• A dual mandate requires co-equal objectives of pricestability and other objectives– The Federal Reserve the dual mandate of “stable prices and

maximum sustainable employment”

TheRelationshipBetweenStabilizingInflationandStabilizingEconomicActivity

• What is a central bank’s appropriate policy response toan economic shock?

• In the case of a demand shock or a temporary supplyshock, the central bank can simultaneously pursuestability in both the price level and economic output

• In the case of a permanent supply shock, however,policymakers can achieve either stable prices or stableoutput, but not both—a tradeoff for a central bank withdual mandates

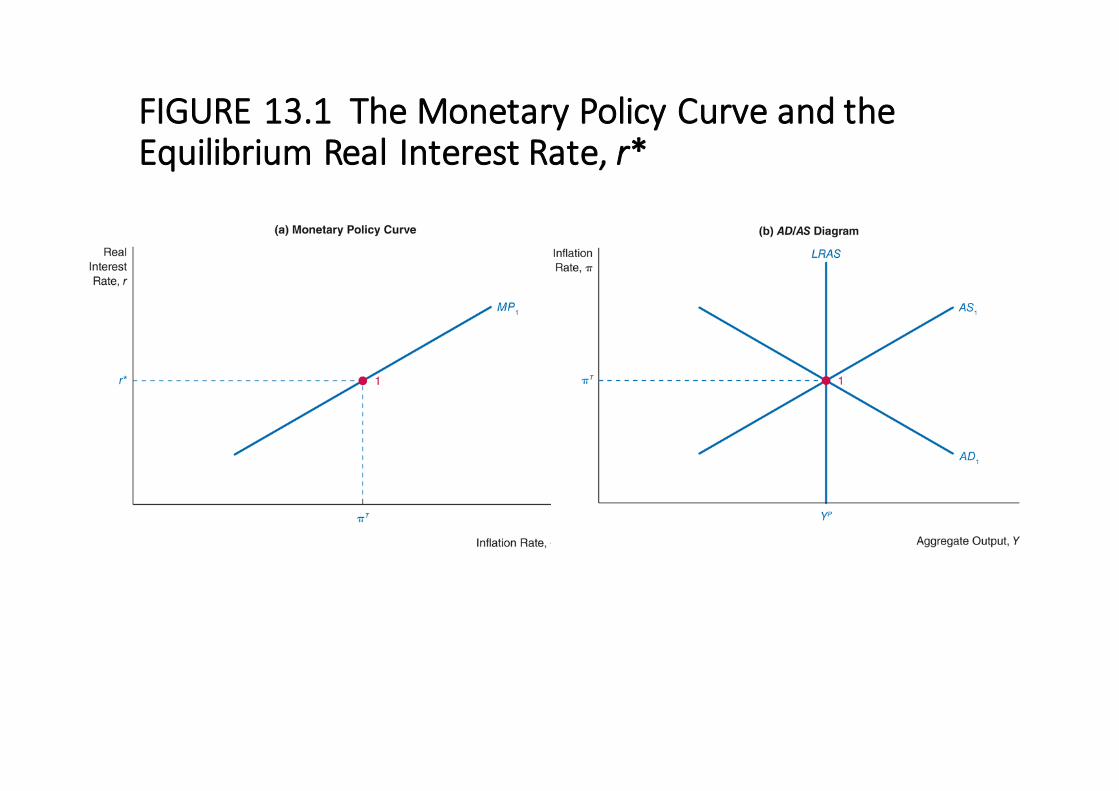

MonetaryPolicyandtheEquilibriumRealInterestRate

• At long-run equilibrium, the real interest rate is theequilibrium real interest rate, r*:

– It is the rate of interest that maintains the quantity ofaggregate output demanded equal to potential output,or (Y-YP)=0

– The inflation rate is consistentwith price stability, or π = πT

– It is also the long-run real interest rate for the economy

FIGURE13.1TheMonetaryPolicyCurveandtheEquilibriumReal InterestRate,r*

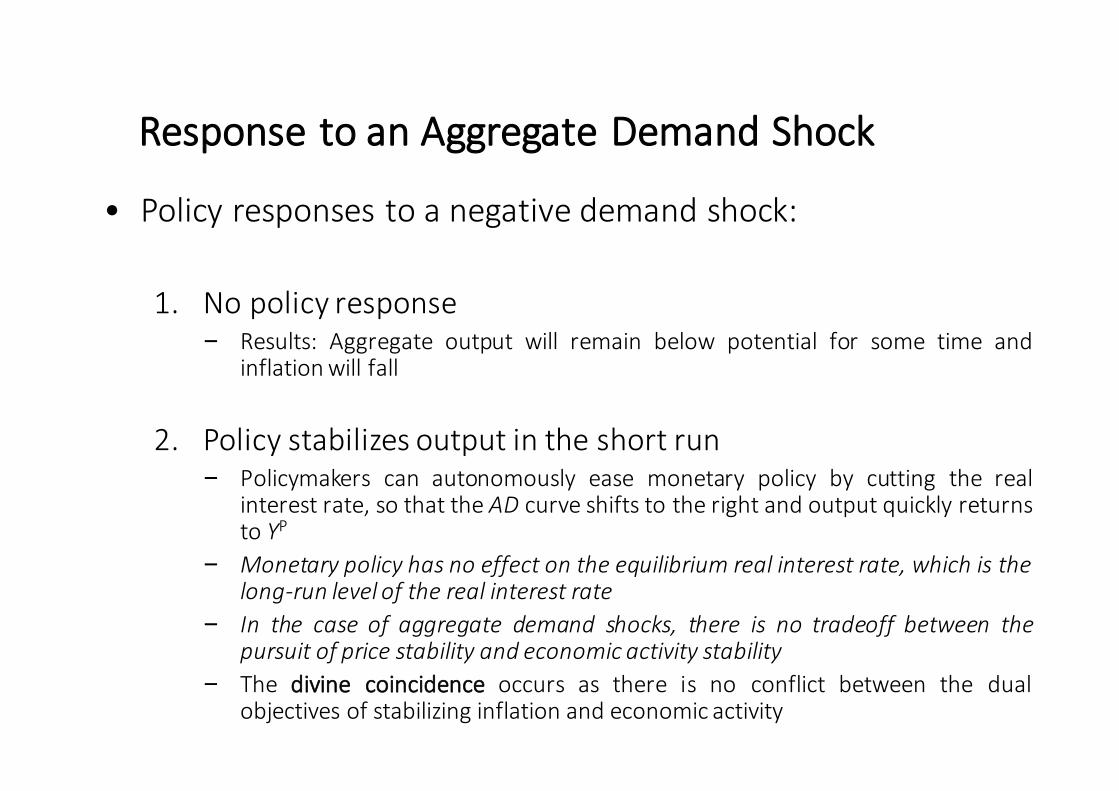

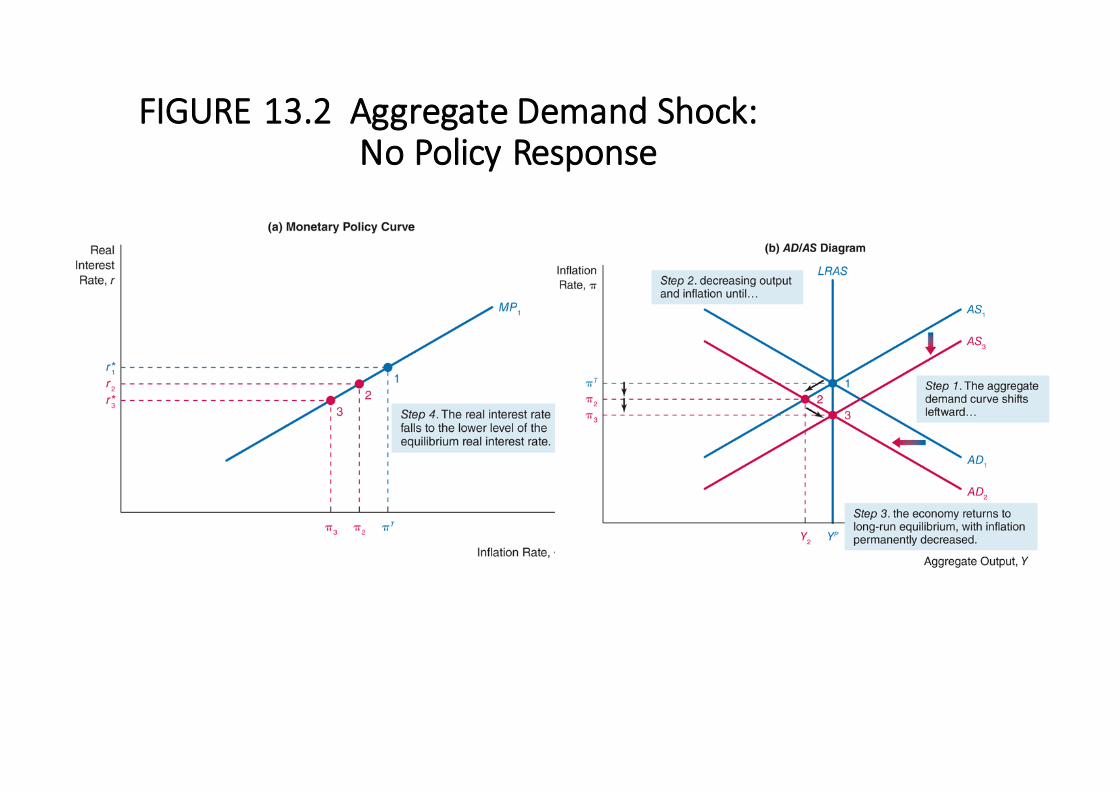

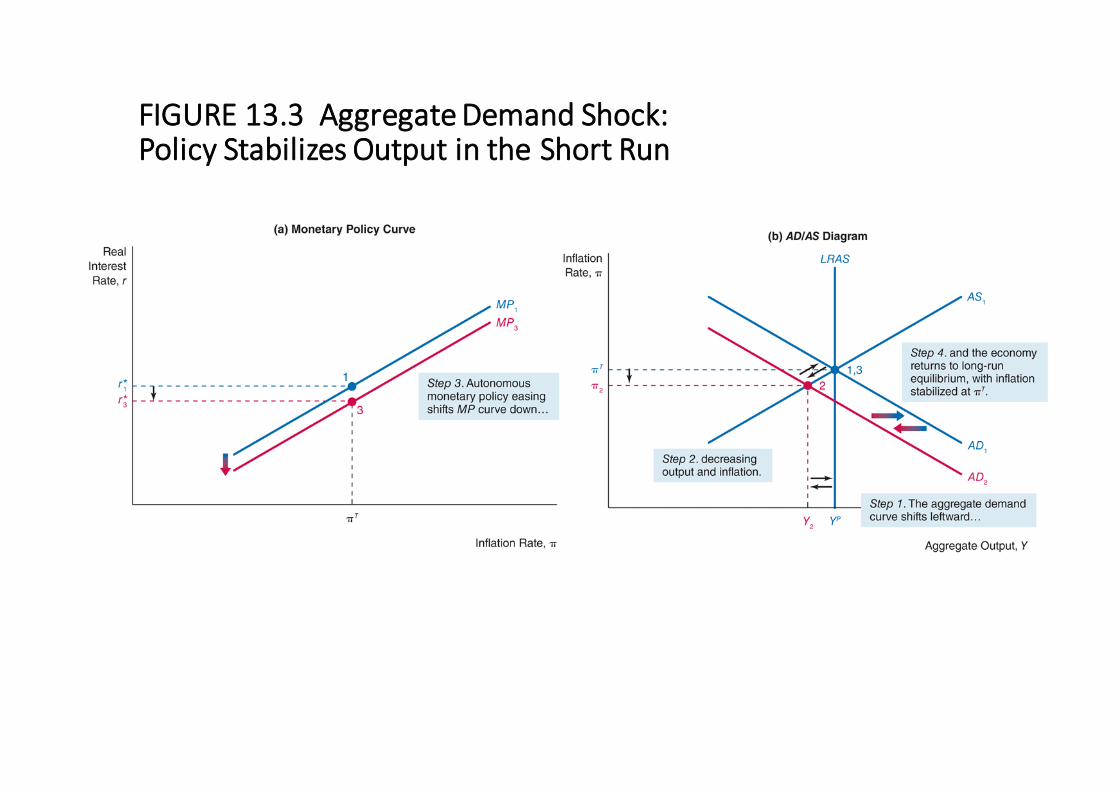

ResponsetoanAggregateDemandShock

• Policy responses to a negative demand shock:

1. No policy response– Results: Aggregate output will remain below potential for some time and

inflationwill fall

2. Policy stabilizes output in the short run– Policymakers can autonomously ease monetary policy by cutting the real

interest rate, so that the AD curve shifts to the right and output quickly returnsto YP

– Monetary policy has no effect on the equilibrium real interest rate, which is thelong-run level of the real interest rate

– In the case of aggregate demand shocks, there is no tradeoff between thepursuit of price stability and economic activity stability

– The divine coincidence occurs as there is no conflict between the dualobjectives of stabilizing inflation and economic activity

FIGURE13.2AggregateDemandShock:NoPolicyResponse

FIGURE13.3AggregateDemandShock:PolicyStabilizesOutputintheShortRun

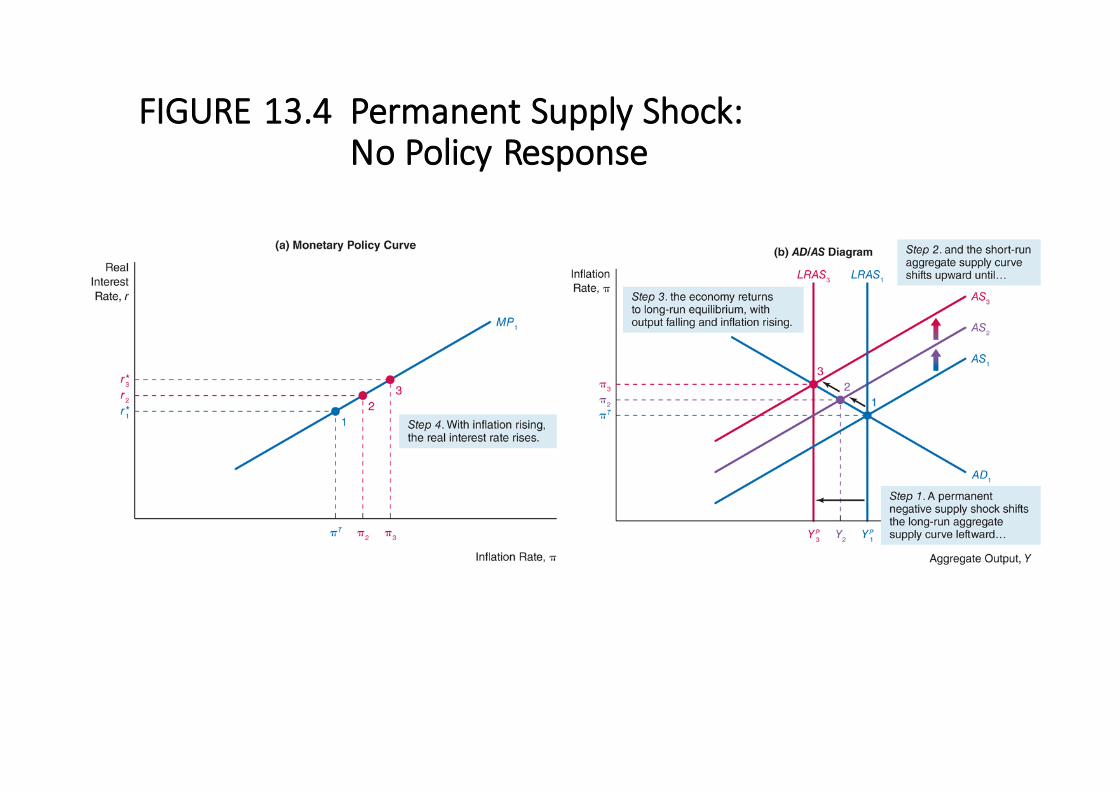

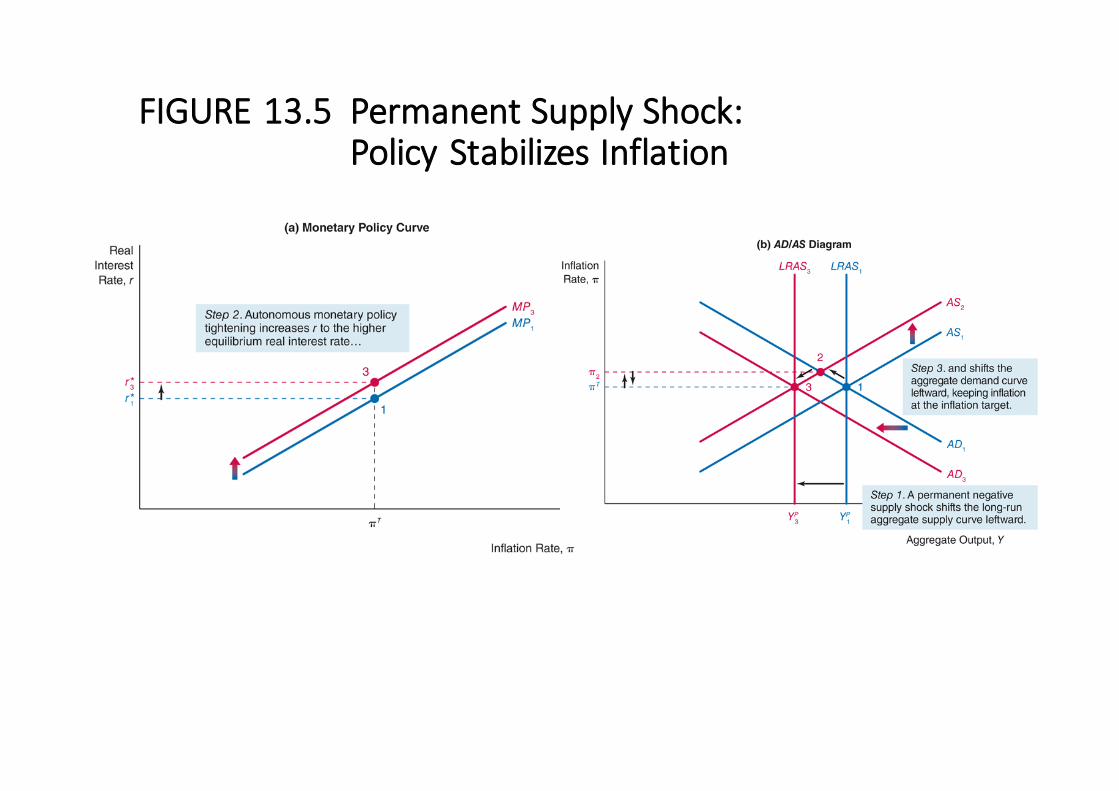

ResponsetoaPermanentSupplyShock

• Policy responses to a negative permanent supply shock(reducing YP):

1. No policy response

– Results: The short-run AS curve keeps shifting up, so that both inflation and thereal interest rate are higher

FIGURE13.4PermanentSupplyShock:NoPolicyResponse

ResponsetoaPermanentSupplyShock

• Policy responses to a negative permanent supply shock(reducing YP):

2. Policy stabilizes inflation

– Policymakers can autonomously tighten monetary policy by raising the realinterest rate, so that the output gap becomes zero, inflation is at πT, and thereal interest rate finally falls

– The divine coincidence still remains true when there is a permanent supplyshock: there is no tradeoff between the dual objectives of stabilizing inflationand economic activity

FIGURE13.5PermanentSupplyShock:PolicyStabilizesInflation

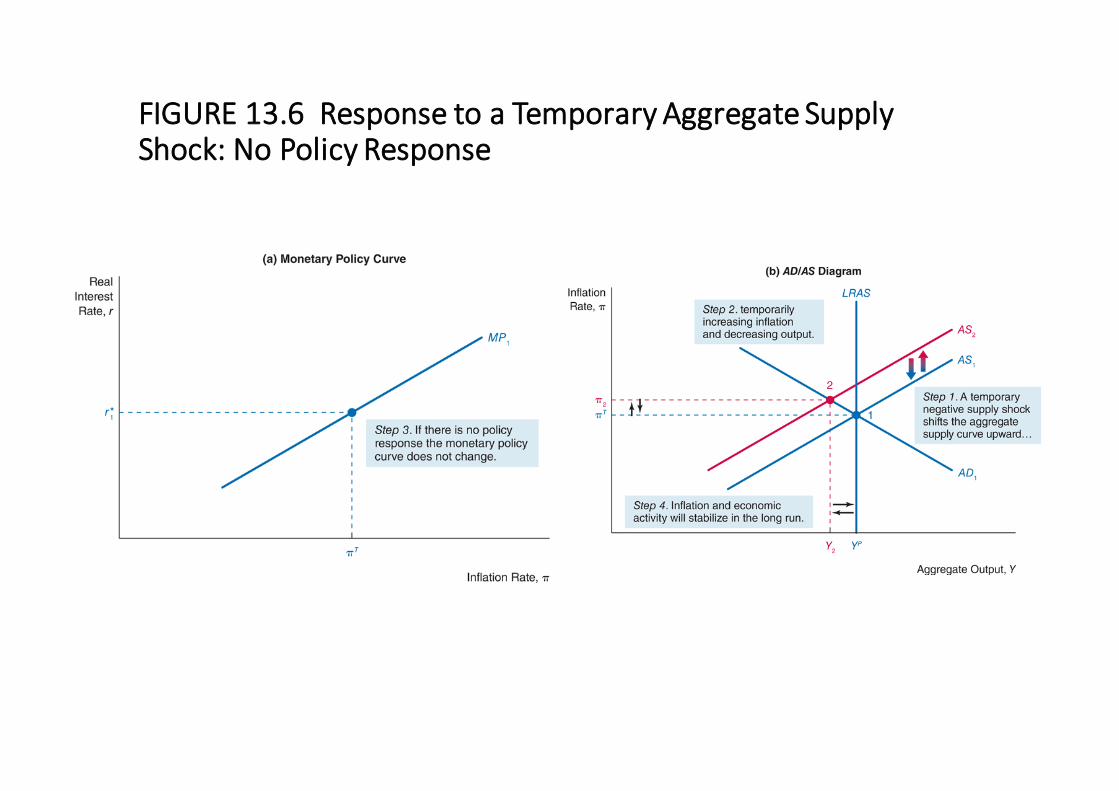

ResponsetoaTemporarySupplyShock

• Policy responses to a negative temporary supply shock (e.g.,oil price surges) that shifts the short-run AS curve but not theLRAS curve:

1. No policy response

– Results: The short-run AS curve shifts back to the initial position, so that outputreturns to their initial levels.

– In the long run, there is no tradeoff between the two objectives, and the divinecoincidence holds

FIGURE13.6ResponsetoaTemporaryAggregateSupplyShock:NoPolicyResponse

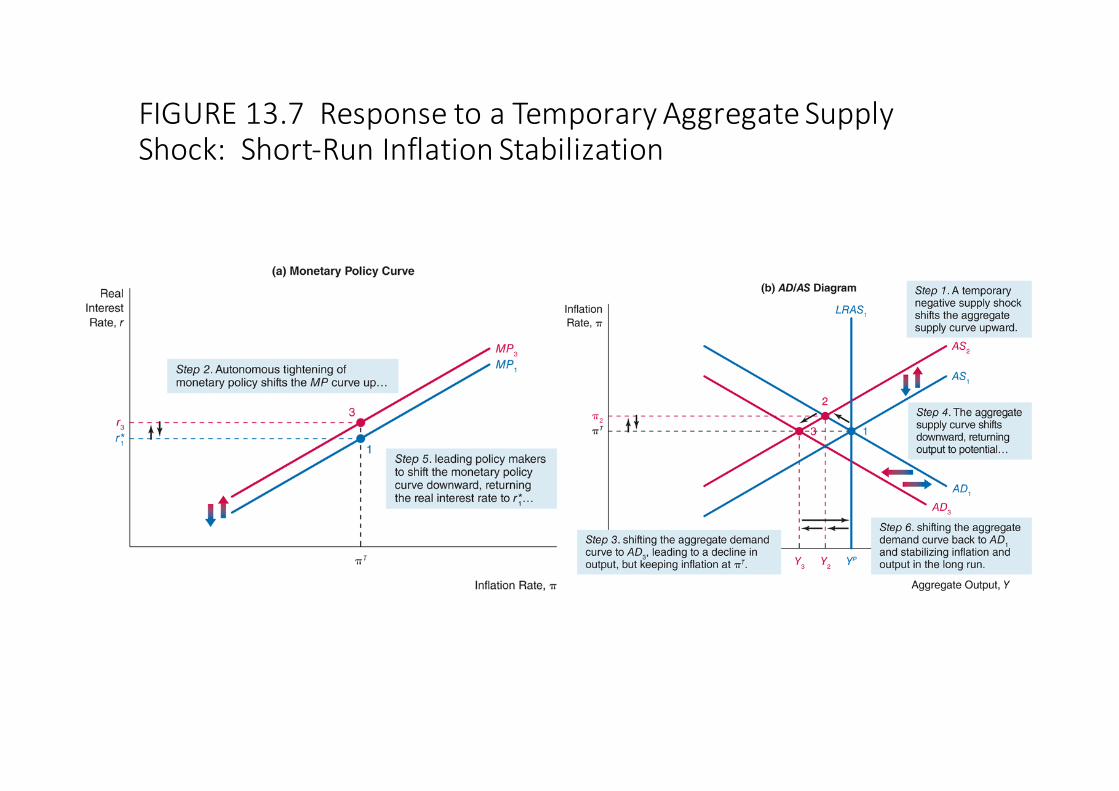

ResponsetoaTemporarySupplyShock(cont’d)2. Policy stabilizes inflation in the short run

– Policymakers can autonomously tighten monetary policy by raising the realinterest rate, which lowers output further below its potential level, but inorder to keep inflation at πT, policymakers need to subsequently reverse theautonomous tightening monetarypolicy

– Stabilizing inflation in response to a temporary supply shock has led to alarger deviation of aggregate output from potential, so this action has notstabilized economic activity

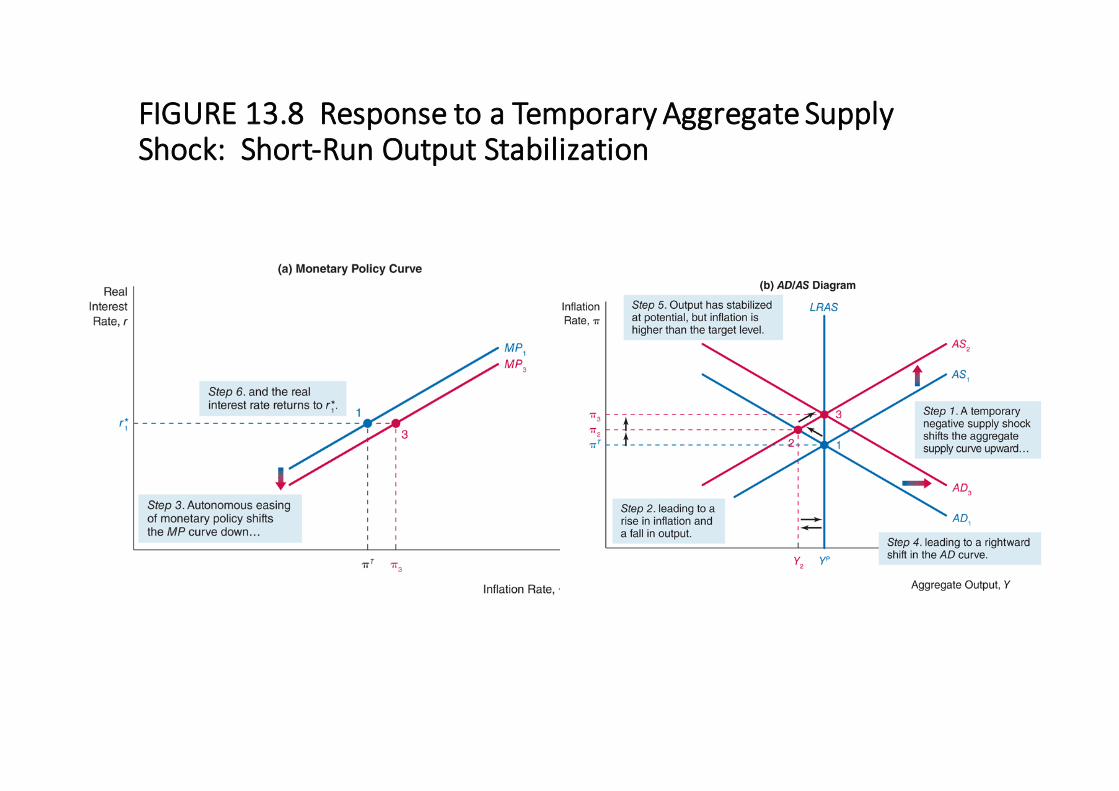

Response toaTemporarySupplyShock(cont’d)3. Policy stabilizes economic activity in the short run

– Policymakers can stabilize output rather than inflation in the short run byautonomously easing monetary policy, so that the output gap returns tozerowhile inflation rises

– Stabilizing output in response to a temporary supply shock has led to a risein inflation, so inflation hasnot been stabilized

FIGURE13.7ResponsetoaTemporaryAggregateSupplyShock:Short-RunInflationStabilization

FIGURE13.8ResponsetoaTemporaryAggregateSupplyShock:Short-RunOutputStabilization

The Bottom Line: The Relationship BetweenStabilizing Inflation and Stabilizing EconomicActivity

1. If most shocks to the macro economy are aggregate demandshocks or permanent aggregate supply shocks, then policythat stabilizes inflation will also stabilize economic activity,even in the short run.

2. If temporary supply shocks are more common, then a centralbank must choose between the two stabilization objectives inthe short run.

3. In the long run, however, there is no conflict betweenstabilizing inflation and economic activity in response totemporary supply shocks.

HowActivelyShouldPolicyMakersTrytoStabilizeEconomicActivity?

• Nonactivists believe that government action isunnecessary to stabilize economic activity becausewages and prices are very flexible and so the self-correcting mechanism quickly returns the economy tofull employment

• Activists, particularly Keynesians, argue that thegovernment should pursue active policy to eliminate highunemployment because wages and prices are sticky, andso it takes a long time for the self-correcting mechanismto reach the long run

LagsandPolicyImplementation

• LagsoccurinactivistpoliciesthatshifttheAD curve:

1. Datalag2. Recognitionlag3. Legislativelag4. Implementationlag5. Effectivenesslag

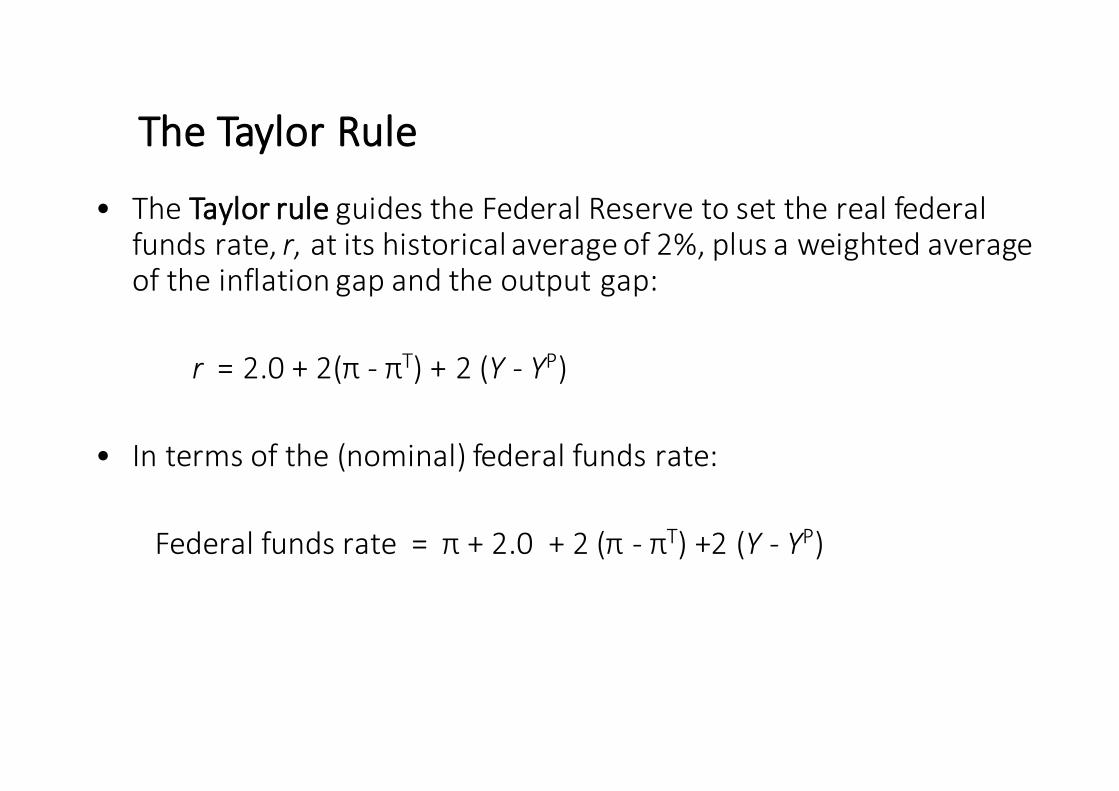

TheTaylorRule

• TheTaylorrule guidestheFederalReservetosettherealfederalfundsrate,r,atitshistoricalaverageof2%,plusaweightedaverageoftheinflationgapandtheoutputgap:

r =2.0+2(π- πT)+2 (Y- YP)

• Intermsofthe(nominal)federalfundsrate:

Federalfundsrate=π+2.0+2 (π- πT)+2(Y- YP)

TheTaylorRuleVersustheMonetaryPolicyCurve

• As for the monetary policy curve, the Taylor ruleincorporates the inflation gap and output gap:

– The Central Bank should raise the real federal funds rate withan increase in the inflation gap, and vice versa

– The Central should raise the real federal funds rate with anincrease in the output gap, and vice versa

Box:TheDifferenceBetweentheTaylorRuleandtheTaylorPrinciple

• The Taylor rule describes how the real interest rate is setin response to the output level and to inflation: It gives acomplete description of the conduct of monetary policy inany situation

• The Taylor principle describes only how the real interestrate is set in response to the level of inflation (ignoringthe output level): It gives only a partial description of theconduct of monetary policy

TheTaylorRuleVersustheMonetaryPolicyCurve(cont’d)

• In the case of aggregate demand shocks, the Taylor rulesuggests a positive relationship between the real federalfunds rate and the output gap (shifting the MP curve)

• In the case of a temporary aggregate supply shock, theTaylor rule requires the Fed to focus on economic activityin addition to inflation

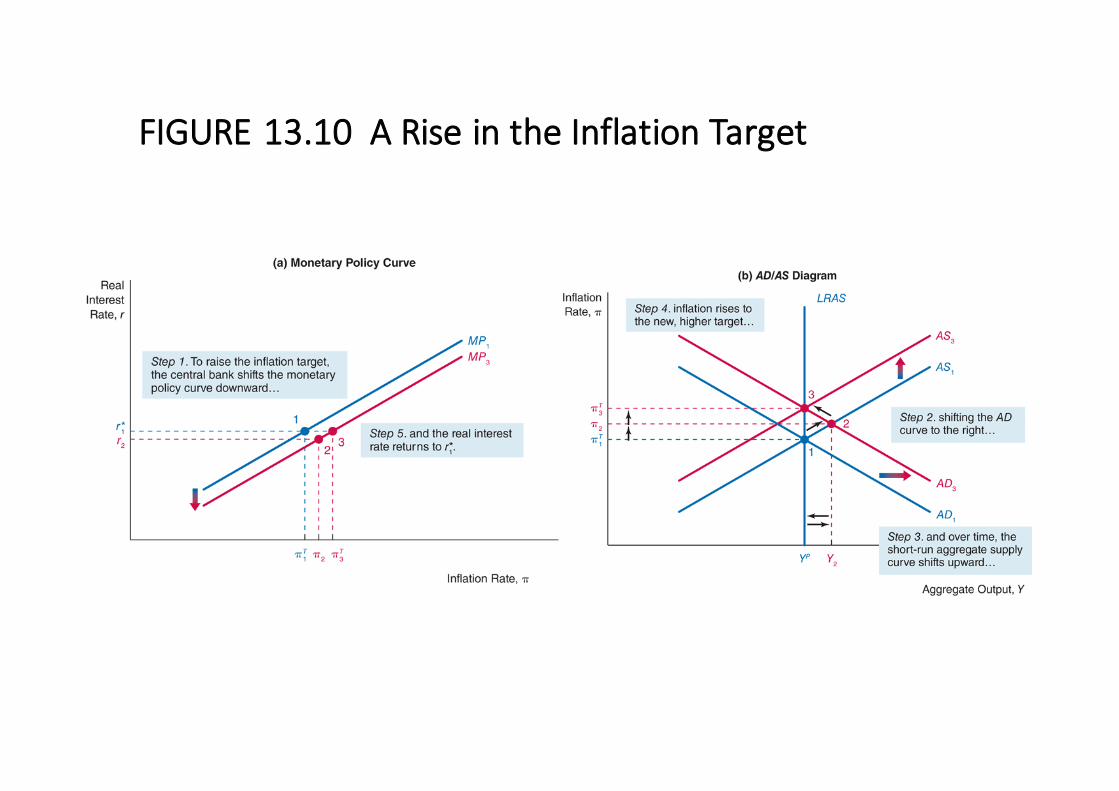

Inflation:AlwaysandEverywhereaMonetaryPhenomenon

• Our aggregate demand and supply analysis supports MiltonFriedman’s adage that in the long run, “Inflation is always andeverywhere a monetary phenomenon”

• Suppose the central bank chooses to raise the its inflation target,the results are:

– The monetary authorities can target any inflation rate in the long run withautonomousmonetarypolicy adjustments

– Although monetary policy controls inflation in the long run, it does notdetermine the equilibriumreal interest rate

– Potential output—and therefore the quantity of aggregate output producedin the long run—is independent ofmonetarypolicy

– The classical dichotomyandmonetary neutrality (Ch.5) hold

FIGURE13.10ARiseintheInflationTarget

HighEmploymentTargetsandInflation

• The primary goal of most governments is high employment but the pursuit ofthis goal canbring high inflation

• Activist stabilization policy to promote high employment can result in two typesof inflation:

– Cost-push inflation—results either from a temporary negative supply shockor wagehikes beyond what productivity gains can justify

– Demand-pull inflation—results from policymakers pursuing policies thatincrease aggregatedemand

CausesofInflationaryMonetaryPolicy

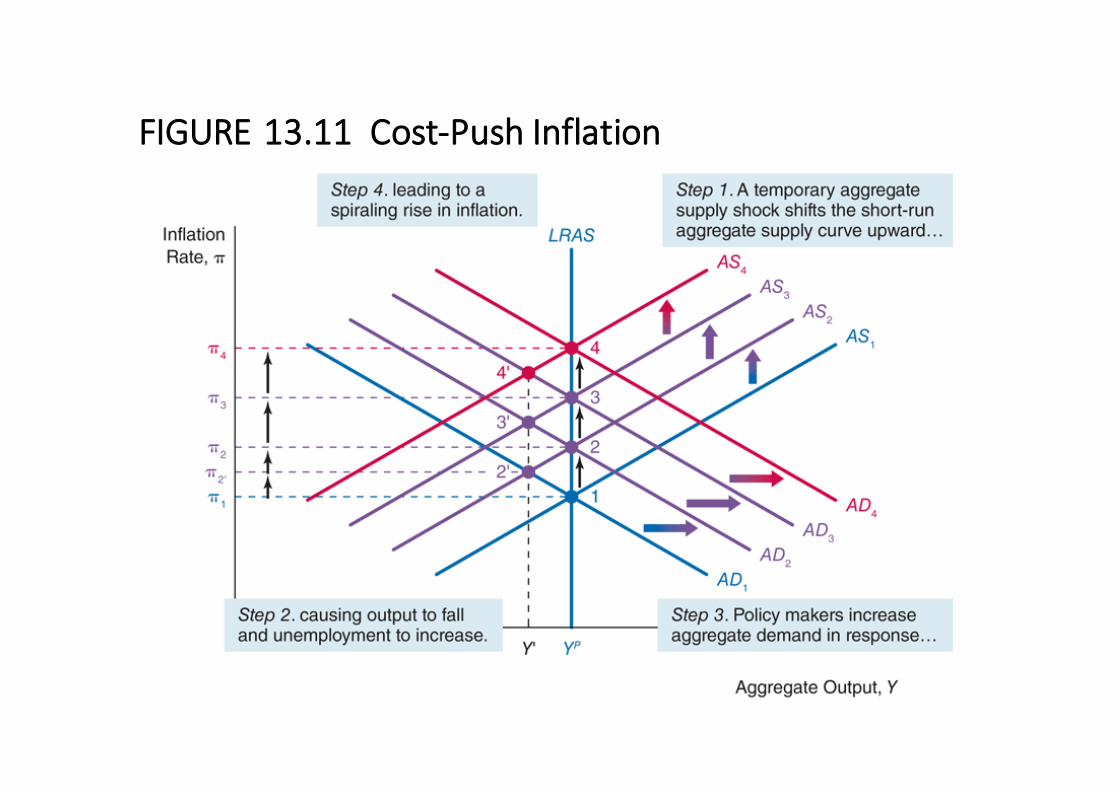

Cost-PushInflation

• Suppose a temporary negative supply (cost push) shockoccurs, so that the short-run AS curve shifts up and the left,then:

– Initially output will to a level below its potential, inflation will rise andunemploymentwill rise

– In response to an increase in the unemployment rate, activist policymakerswith a high employment target would implement expansionary policies toshift the AD curve to the right

– However, unemployment will rise again because the short-run AS curve willshift up and to the left as workers seek higher wages to keep their realwages from falling (due to higher inflation)

– This process continues and continuing inflationoccurs

FIGURE13.11Cost-PushInflation

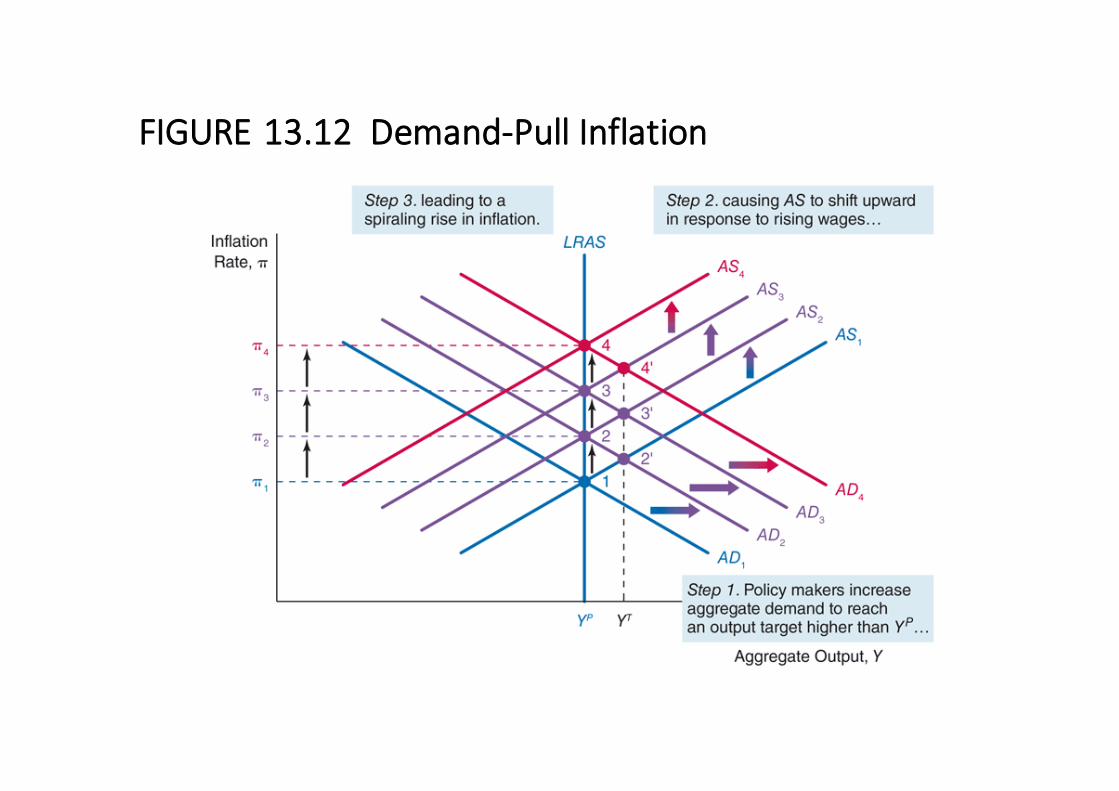

Demand-Pull Inflation

• Suppose policymakers set an unemployment target (4%)that is below the natural rate of unemployment (5%),resulting in expansionary fiscal policy or an autonomouseasing of monetary policy that shifts the AD curveupward, then:

– Policymakers would initially achieve the 4% unemployment ratetarget so that output is at its target YT

– However, wages would subsequently increase, shifting theshort-run AS curve up and to the left, resulting in a steadilyrising inflation rate

FIGURE13.12Demand-PullInflation