M01 gitm5253 12_pp_c01

60

Copyright © 2009 Pearson Prentice Hall. All rights reserved. Chapter 1 The Role and Environment of Managerial Finance

-

Upload

cambodian-mekong-university -

Category

Documents

-

view

74 -

download

0

Transcript of M01 gitm5253 12_pp_c01

Copyright © 2009 Pearson Prentice Hall. All rights reserved.

Chapter 1

The Role and Environment of Managerial Finance

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-2

Learning Goals

1. Define finance, its major areas and opportunities available in this field, and the legal forms of business organization.

2. Describe the managerial finance function and its relationship to economics and accounting.

3. Identify the primary activities of the financial manager.

4. Explain the goal of the firm, corporate governance, the role of ethics, and the agency issue.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-3

Learning Goals (cont.)

5. Understand financial institutions and markets, and the role they play in managerial finance.

6. Discuss business taxes and their importance in financial decisions.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-4

What is Finance?

• Finance can be defined as the art and science of managing money.

• Finance is concerned with the process, institutions, markets, and instruments involved in the transfer of money among individuals, businesses, and governments.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-5

Major Areas & Opportunities in Finance: Financial Services

• Financial Services is the area of finance concerned with the design and delivery of advice and financial products to individuals, businesses, and government.

• Career opportunities include banking, personal financial planning, investments, real estate, and insurance.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-6

Major Areas & Opportunities in Finance: Managerial Finance

• Managerial finance is concerned with the duties of the financial manager in the business firm.

• The financial manager actively manages the financial affairs of any type of business, whether private or public, large or small, profit-seeking or not-for-profit.

• They are also more involved in developing corporate strategy and improving the firm’s competitive position.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-7

Major Areas & Opportunities in Finance: Managerial Finance (cont.)

• Increasing globalization has complicated the financial management function by requiring them to be proficient in managing cash flows in different currencies and protecting against the risks inherent in international transactions.

• Changing economic and regulatory conditions also complicate the financial management function.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-8

Table 1.1 Strengths and Weaknesses of the Common Legal Forms of Business Organization

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-9

Figure 1.1 Corporate Organization

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-10

Table 1.2 Other Limited Liability Organizations

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-11

Table 1.3 Career Opportunities in Managerial Finance

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-12

The Managerial Finance Function

• The size and importance of the managerial finance function depends on the size of the firm.

• In small companies, the finance function may be performed by the company president or accounting department.

• As the business expands, finance typically evolves into a separate department linked to the president as was previously described in Figure 1.1.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-13

The Managerial Finance Function: Relationship to Economics

• The field of finance is actually an outgrowth of economics.

• In fact, finance is sometimes referred to as financial economics.

• Financial managers must understand the economic framework within which they operate in order to react or anticipate to changes in conditions.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-14

The Managerial Finance Function: Relationship to Economics (cont.)

• The primary economic principal used by financial managers is marginal cost-benefit analysis which says that financial decisions should be implemented only when added benefits exceed added costs.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-15

The Managerial Finance Function: Relationship to Accounting

• The firm’s finance (treasurer) and accounting (controller) functions are closely-related and overlapping.

• In smaller firms, the financial manager generally performs both functions.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-16

The Managerial Finance Function: Relationship to Accounting (cont.)

• One major difference in perspective and emphasis between finance and accounting is that accountants generally use the accrual method while in finance, the focus is on cash flows.

• The significance of this difference can be illustrated using the following simple example.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-17

Sales $100,000 (1 yacht sold, 100% still uncollected)

Costs $ 80,000 (all paid in full under supplier terms)

The Managerial Finance Function: Relationship to Accounting (cont.)

• The Nassau Corporation experienced the following activity last year:

• Now contrast the differences in performance under the accounting method versus the cash method.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-18

INCOME STATEMENT SUMMARY

ACCRUAL CASH

Sales $100,000 $ 0

Less: Costs (80,000) (80,000)

Net Profit/(Loss) $ 20,000 $(80,000)

The Managerial Finance Function: Relationship to Accounting (cont.)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-19

The Managerial Finance Function: Relationship to Accounting (cont.)

• Finance and accounting also differ with respect to decision-making.

• While accounting is primarily concerned with the presentation of financial data, the financial manager is primarily concerned with analyzing and interpreting this information for decision-making purposes.

• The financial manager uses this data as a vital tool for making decisions about the financial aspects of the firm.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-20

Figure 1.2 Financial Activities

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-21

Investment Year 1 Year 2 Year 3 Total (years 1-3)

Rotor 1.40$ 1.00$ 0.40$ 2.80$

Valve 0.60$ 1.00$ 1.40$ 3.00$

Earnings per share (EPS)

Which Investment is Preferred?

Goal of the Firm: Maximize Profit???

• Profit maximization fails to account for differences in the level of cash flows (as opposed to profits), the timing of these cash flows, and the risk of these cash flows.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-22

Share Price = Future Dividends Required Return

level & timing of cash flows

risk of cash flows

Goal of the Firm: Maximize Shareholder Wealth!!!

• Why?• Because maximizing shareholder wealth properly considers cash

flows, the timing of these cash flows, and the risk of these cash flows.

• This can be illustrated using the following simple stock valuation equation:

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-23

Goal of the Firm: Maximize Shareholder Wealth!!! (cont.)

• The process of shareholder wealth maximization can be described using the following flow chart:

Figure 1.3 Share Price Maximization

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-24

Goal of the Firm: What About Other Stakeholders?

• Stakeholders include all groups of individuals who have a direct economic link to the firm including employees, customers, suppliers, creditors, owners, and others who have a direct economic link to the firm.

• The "Stakeholder View" prescribes that the firm make a conscious effort to avoid actions that could be detrimental to the wealth position of its stakeholders.

• Such a view is considered to be "socially responsible."

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-25

Corporate Governance

• Corporate Governance is the system used to direct and control a corporation.

• It defines the rights and responsibilities of key corporate participants such as shareholders, the board of directors, officers and managers, and other stakeholders.

• The structure of corporate governance was previously described in Figure 1.1.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-26

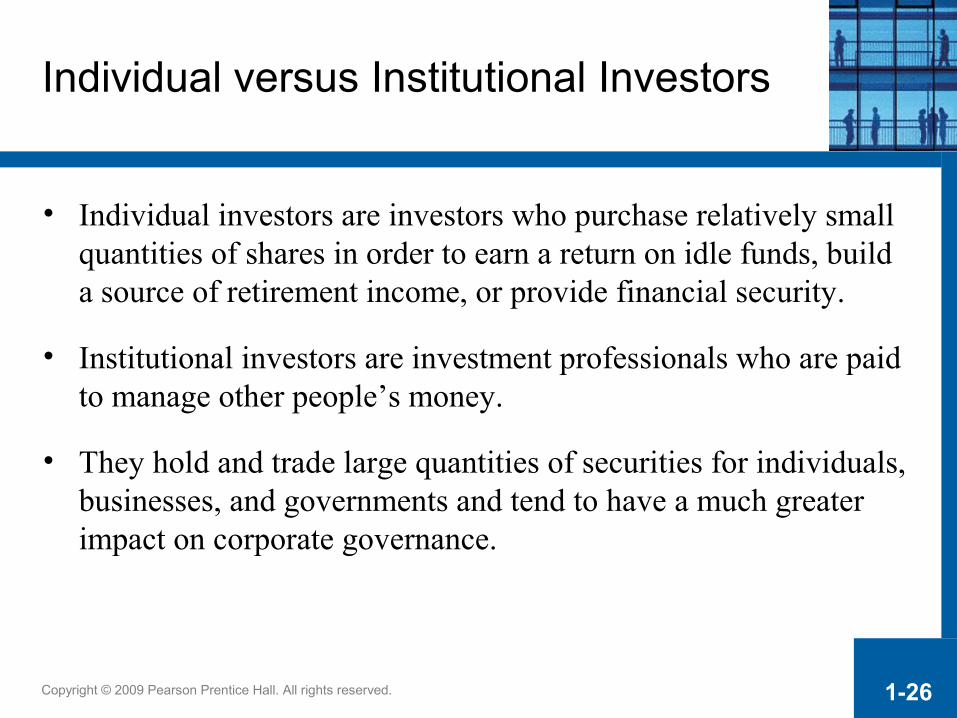

Individual versus Institutional Investors

• Individual investors are investors who purchase relatively small quantities of shares in order to earn a return on idle funds, build a source of retirement income, or provide financial security.

• Institutional investors are investment professionals who are paid to manage other people’s money.

• They hold and trade large quantities of securities for individuals, businesses, and governments and tend to have a much greater impact on corporate governance.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-27

The Sarbanes-Oxley Act of 2002

• The Sarbanes-Oxley Act of 2002 (commonly called SOX) eliminated many disclosure and conflict of interest problems that surfaced during the early 2000s.

• SOX: – established an oversight board to monitor the accounting industry;

– tightened audit regulations and controls;

– toughened penalties against executives who commit corporate fraud;

– strengthened accounting disclosure requirements;

– established corporate board structure guidelines.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-28

The Role of Ethics: Ethics Defined

• Ethics is the standards of conduct or moral judgment—have become an overriding issue in both our society and the financial community

• Ethical violations attract widespread publicity

• Negative publicity often leads to negative impacts on a firm

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-29

The Role of Ethics: Considering Ethics

• Robert A. Cooke, a noted ethicist, suggests that the following questions be used to assess the ethical viability of a proposed action:– Does the action unfairly single out an individual

or group?– Does the action affect the morals, or legal rights of any

individual or group?– Does the action conform to accepted moral standards?– Are there alternative courses of action that are less likely to

cause actual or potential harm?

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-30

The Role of Ethics: Considering Ethics (cont.)

• Cooke suggests that the impact of a proposed decision should be evaluated from a number of perspectives:

– Are the rights of any stakeholder being violated?

– Does the firm have any overriding duties to any stakeholder?

– Will the decision benefit any stakeholder to the detriment of another stakeholder?

– If there is a detriment to any stakeholder, how should it be remedied, if at all?

– What is the relationship between stockholders and stakeholders?

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-31

The Role of Ethics: Ethics & Share Price

• Ethics programs seek to:– reduce litigation and judgment costs

– maintain a positive corporate image– build shareholder confidence– gain the loyalty and respect of all stakeholders

• The expected result of such programs is to positively affect the firm's share price.

• Home work & Presentation

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-32

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-33

The Agency Issue: The Agency Problem

• Whenever a manager owns less than 100% of the firm’s equity, a potential agency problem exists.

• In theory, managers would agree with shareholder wealth maximization.

• However, managers are also concerned with their personal wealth, job security, fringe benefits, and lifestyle.

• This would cause managers to act in ways that do not always benefit the firm shareholders.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-34

The Agency Issue: Resolving the Problem

• Market Forces such as major shareholders and the threat of a hostile takeover act to keep managers in check.

• Agency Costs are the costs borne by stockholders to maintain a corporate governance structure that minimizes agency problems and contributes to the maximization of shareholder wealth.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-35

The Agency Issue: Resolving the Problem (cont.)

• Examples would include bonding or monitoring management behavior, and structuring management compensation to make shareholders interests their own.

• A stock option is an incentive allowing managers to purchase stock at the market price set at the time of the grant.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-36

The Agency Issue: Resolving the Problem (cont.)

• Performance plans tie management compensation to measures such as EPS growth; performance shares and/or cash bonuses are used as compensation under these plans.

• Recent studies have failed to find a strong relationship between CEO compensation and share price.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-37

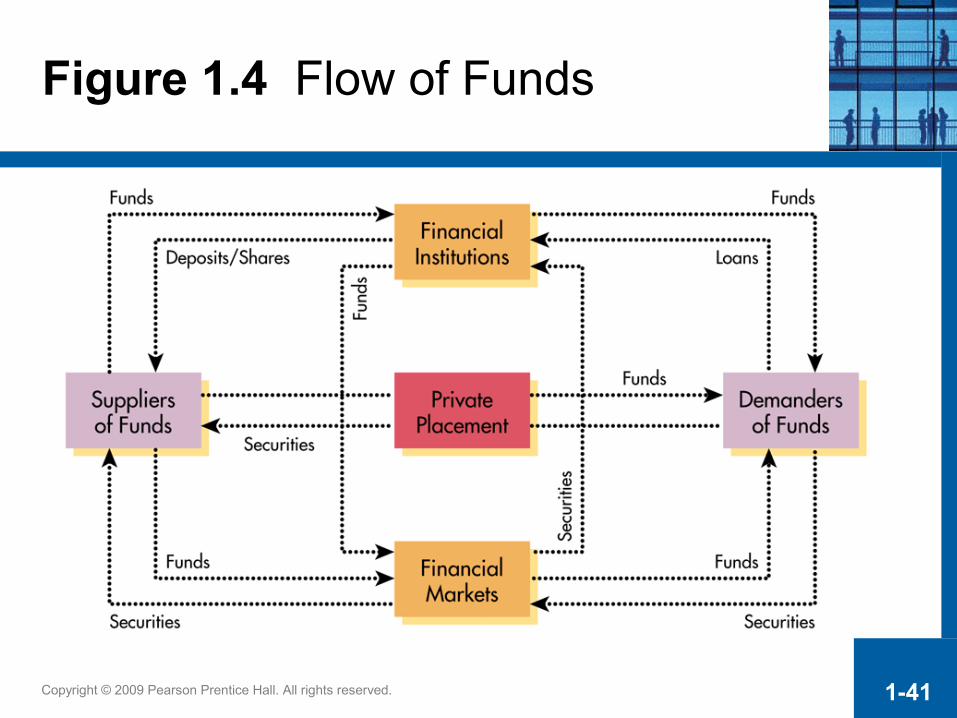

Financial Institutions & Markets

• Firms that require funds from external sources can obtain them in three ways:

– through a bank or other financial institution

– through financial markets

– through private placements

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-38

Financial Institutions & Markets: Financial Institutions

• Financial institutions are intermediaries that channel the savings of individuals, businesses, and governments into loans or investments.

• The key suppliers and demanders of funds are individuals, businesses, and governments.

• In general, individuals are net suppliers of funds, while businesses and governments are net demanders of funds.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-39

Financial Institutions & Markets: Financial Markets

• Financial markets provide a forum in which suppliers of funds and demanders of funds can transact business directly.

• The two key financial markets are the money market and the capital market.

• Transactions in short term marketable securities take place in the money market while transactions in long-term securities take place in the capital market.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-40

Financial Institutions & Markets: Financial Markets (cont.)

• Whether subsequently traded in the money or capital market, securities are first issued through the primary market.

• The primary market is the only one in which a corporation or government is directly involved in and receives the proceeds from the transaction.

• Once issued, securities then trade on the secondary markets such as the New York Stock Exchange or NASDAQ.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-41

Figure 1.4 Flow of Funds

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-42

The Money Market

• The money market exists as a result of the interaction between the suppliers and demanders of short-term funds (those having a maturity of a year or less).

• Most money market transactions are made in marketable securities which are short-term debt instruments such as T-bills and commercial paper.

• Money market transactions can be executed directly or through an intermediary.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-43

The Money Market (cont.)

• The international equivalent of the domestic (U.S.) money market is the Eurocurrency market.

• The Eurocurrency market is a market for short-term bank deposits denominated in U.S. dollars or other marketable currencies.

• The Eurocurrency market has grown rapidly mainly because it is unregulated and because it meets the needs of international borrowers and lenders.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-44

The Capital Market

• The capital market is a market that enables suppliers and demanders of long-term funds to make transactions.

• The key capital market securities are bonds (long-term debt) and both common and preferred stock (equity).

• Bonds are long-term debt instruments used by businesses and government to raise large sums of money or capital.

• Common stock are units of ownership interest or equity in a corporation.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-45

Broker Markets and Dealer Markets

• Broker markets consists of national and regional securities exchanges, which are organizations that provide a marketplace in which firms can raise funds the sale of new securities and purchasers can resell securities

• Dealer markets consist of both the Nasdaq market and the over-the-counter (OTC) market, where the (unlisted) shares of smaller firm shares are sold and traded.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-46

• The key difference between broker and dealer markets is a technical point dealing with the way trades are executed.

• When a trade occurs in a broker market, buyers and sellers are brought together and the trade takes place on the floor of the exchange.

• In contrast, buyers and sellers are never actually brought together in a dealer – transactions are executed by securities dealers that make markets in certain securities.

Broker Markets and Dealer Markets (continued)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-47

• The New York Stock Exchange (NYSE) is the most famous of all broker markets and accounts for about 60% of the value of shares traded in the U.S. stock markets.

• Trading is conducted through an auction process where specialists “make a market” in selected securities.

• As compensation for executing orders, specialists make money on the spread (bid price – ask price).

Broker Markets and Dealer Markets (cont.)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-48

• The over-the-counter (OTC) market is an intangible market for securities transactions.

• Unlike organized exchanges, the OTC is both a primary market and a secondary market.

• The OTC is a computer-based market where dealers make a market in selected securities and are linked to buyers and sellers through the NASDAQ System.

• Dealers also make money on the “spread.”

Broker Markets and Dealer Markets (cont.)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-49

International Capital Markets

• In the Eurobond market, corporations and governments typically issue bonds denominated in dollars and sell them to investors located outside the United States.

• The foreign bond market is a market for foreign bonds, which are bonds issued by a foreign corporation or government that is denominated in the investor’s home currency and sold in the investor’s home market.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-50

International Capital Markets (cont.)

• Finally, the international equity market allows corporations to sell blocks of shares to investors in a number of different countries simultaneously.

• This market enables corporations to raise far larger amounts of capital than they could raise in any single national market.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-51

The Role of Securities Exchanges

Figure 1.5 Supply and Demand

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-52

Business Taxes

• Both individuals and businesses must pay taxes on income.

• The income of sole proprietorships and partnerships is taxed as the income of the individual owners, whereas corporate income is subject to corporate taxes.

• Both individuals and businesses can earn two types of income—ordinary income and capital gains income.

• Under current law, tax treatment of ordinary income and capital gains income change frequently due frequently changing tax laws.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-53

Example

Calculate federal income taxes due if taxable income is $80,000.

Tax = .15 ($50,000) + .25 ($25,000) + .34 ($80,000 - $75,000)

Tax = $15,450

Business Taxes: Ordinary Income

• Ordinary income is earned through the sale of a firm’s goods or services and is taxed at the rates depicted in Table 1.4 on the following slide.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-54

Business Taxation: Ordinary Income

Table 1.4 Corporate Tax Rate Schedule

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-55

Example

What is the marginal and average tax rate for the previous example?

Marginal Tax Rate = 34%

Average Tax Rate = $15,450/$80,000 = 19.31%

Business Taxation: Average & Marginal Tax Rates

• A firm’s marginal tax rate represents the rate at which additional income is taxed.

• The average tax rate is the firm’s taxes divided by taxable income.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-56

Business Taxation: Tax on Interest & Dividend Income

• For corporations only, 70% of all dividend income received from an investment in the stock of another corporation in which the firm has less than 20% ownership is excluded from taxation.

• This exclusion is provided to avoid triple taxation for corporations.

• Unlike dividend income, all interest income received is fully taxed.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-57

ExampleTwo companies, Debt Co. and No Debt Co., both expect in the coming year to have EBIT of $200,000. During the year, Debt Co. will have to pay $30,000 in interest expenses. No Debt Co. has no debt and will pay not interest expenses.

Business Taxation (Tax Deductibility): Debt versus Equity Financing

• In calculating taxes, corporations may deduct operating expenses and interest expense but not dividends paid.

• This creates a built-in tax advantage for using debt financing as the following example will demonstrate.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-58

Business Taxation (Tax Deductibility): Debt versus Equity Financing (cont.)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-59

• As the example shows, the use of debt financing can increase cash flow and EPS, and decrease taxes paid.

• The tax deductibility of interest and other certain expenses reduces their actual (after-tax) cost to the profitable firm.

• It is the non-deductibility of dividends paid that results in double taxation under the corporate form of organization.

Business Taxation (Tax Deductibility): Debt versus Equity Financing (cont.)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 1-60

Business Taxation: Capital Gains

• A capital gain results when a firm sells an asset such as a stock held as an investment for more than its initial purchase price.

• The difference between the sales price and the purchase price is called a capital gain.

• For corporations, capital gains are added to ordinary income and taxed like ordinary income at the firm’s marginal tax rate.