Lyndsey swift

34

Growing Rural Tourism in England: Our shared ambition Lyndsey Swift Head of Strategic Partnerships & Engagement

-

Upload

naaonb-landscapesforlife -

Category

Documents

-

view

796 -

download

0

Transcript of Lyndsey swift

Growing Rural Tourism in England: Our shared ambition

Lyndsey SwiftHead of Strategic Partnerships & Engagement

To lead and drive forward the quality, competiveness and

sustainable growth of England’s Visitor Economy

Our Mission

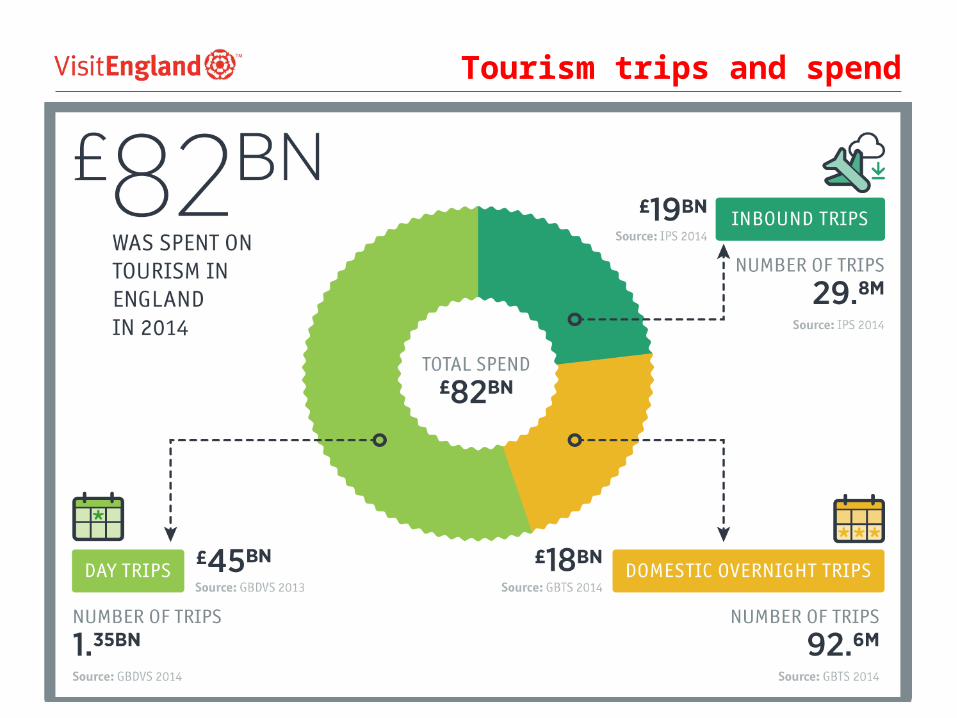

Economic impact of tourism

Tourism trips and spend

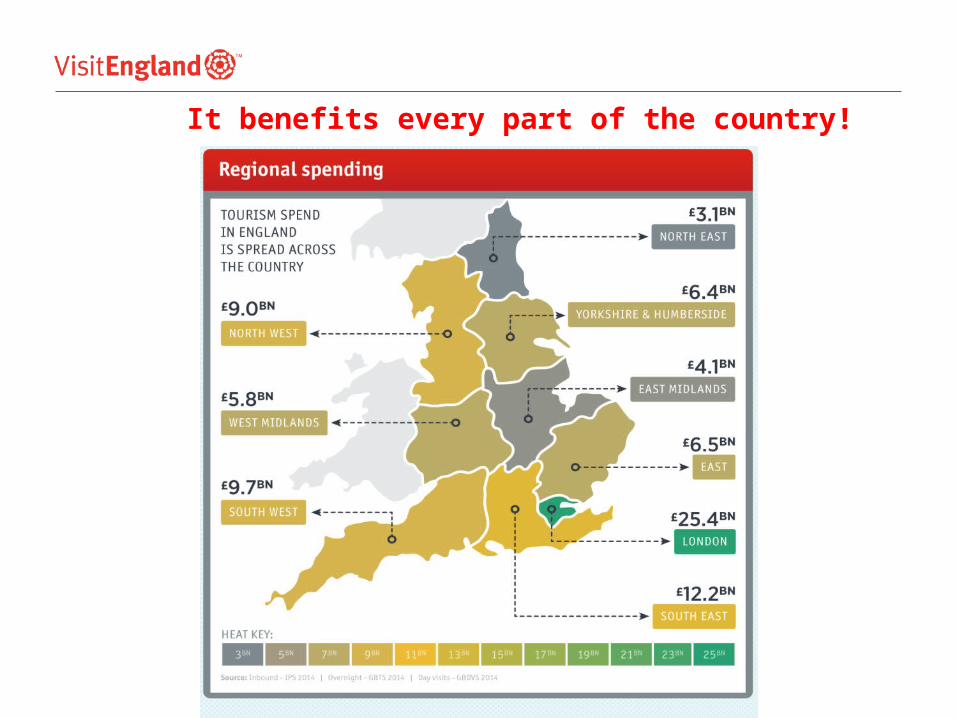

It benefits every part of the country!

Apr-06 Oct-06 Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-145

10

15

20

25

30

35

40

45

50

55Domestic Tourism in England – Rolling 12 Month Trend

Trips(m)

Domestic overnight trends vary by trip purpose – all declined in 2014, though early 2015 shows some recovery

Source: GBTS

Holiday

VFR

Business

Jan

'12

Feb

'12

Mar

'12

Apr

'12

May

'12

Jun

'12

Jul '

12

Aug

'12

Sep

'12

Oct

'12

Nov

'12

Dec

'12

Jan

'13

Feb

'13

Mar

' 13

Apr

'13

May

'13

Jun

'13

Jul '

13

Aug

'13

Sep

'13

Oct

'13

Nov

'13

Dec

'13

Jan

'14

Feb

'14

Mar

'14

Apr

'14

May

'14

Jun'

14

Jul'1

4

Aug

'14

Sep

'14

Oct

'14

Nov

'14

Dec

'14

1,3

46

.6

1,3

49

.3

1,3

56

.1

1,3

55

.6

1,3

70

.9

1,3

85

.7

1,3

90

.8

1,4

19

.1

1,4

40

.9

1,4

37

.7

1,4

39

.1

1,4

66

.5

1,4

53

.9

1,4

45

.7

1,4

36

.3

1,4

28

.7

1,4

22

.7

1,4

22

.3

1,4

24

.5

1,4

08

.4

1,3

87

.4

1,3

83

.2

1,3

81

.0

1,3

70

.0

1,3

62

.4

1,3

59

.7

1,3

68

.2

1,3

71

.9

1,3

68

.6

1,3

55

.1

1,3

44

.9

1,3

44

.1

1,3

42

.3

1,3

40

.0

1,3

49

.6

1,3

45

.1

Tourism Day Visits in England – Rolling 12 Month Totals

Volume of visits (millions)

Jan

'12

Feb

'12

Mar

'12

Apr

'12

May

'12

Jun

'12

Jul '

12

Aug

'12

Sep

'12

Oct

'12

Nov

'12

Dec

'12

Jan

'13

Feb

'13

Mar

' 13

Apr

'13

May

'13

Jun

'13

Jul '

13

Aug

'13

Sep

'13

Oct

'13

Nov

'13

Dec

'13

Jan

'14

Feb

'14

Mar

'14

Apr

'14

May

'14

Jun'

14

Jul'1

4

Aug

'14

Sep

'14

Oct

'14

Nov

'14

Dec

'14

£4

4,4

29

£4

4,0

41

£4

4,0

53

£4

4,1

85

£4

5,0

79

£4

4,5

40

£4

3,7

50

£4

4,8

18

£4

6,1

25

£4

7,2

94

£4

8,1

97

£4

8,4

59

£4

7,5

15

£4

7,4

52

£4

7,7

43

£4

8,0

71

£4

8,1

42

£4

9,3

98

£4

9,6

19

£4

9,9

71

£4

7,9

59

£4

6,5

57

£4

6,0

69

£4

6,0

24

£4

5,8

70

£4

5,7

65

£4

6,6

95

£4

6,1

57

£4

6,0

67

£4

4,7

77

£4

4,6

20

£4

4,1

33

£4

4,7

22

£4

4,6

17

£4

5,3

05

£4

5,1

01

Value of visits (£millions)

Domestic tourism day visits are a significant – and relatively stable – part of the market

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

24.2 24.727.8

3032.7 32.8 31.9

29.9 29.8 30.8 31.132.7

34.4

7.7 89.3 9.7 10.6 10.8 10.9 11.4 11.7 12 12 12.7 13.6

UK Inbound Visits (Millions)

All Visits Holiday Visits

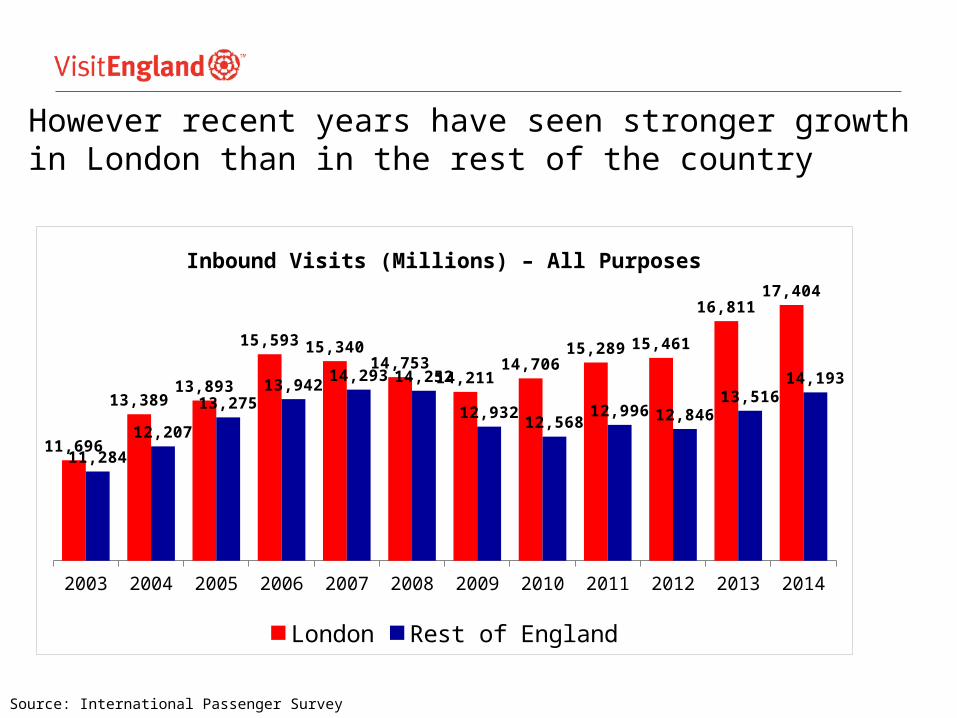

Inbound visits to the UK reached record levels in 2014

Source: International Passenger Survey

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

11,696

13,389 13,893

15,593 15,340 14,753

14,211 14,706

15,289 15,461

16,811 17,404

11,284

12,207

13,27513,942

14,293 14,252

12,93212,568

12,996 12,84613,516

14,193

Inbound Visits (Millions) – All Purposes

London Rest of England

However recent years have seen stronger growth in London than in the rest of the country

Source: International Passenger Survey

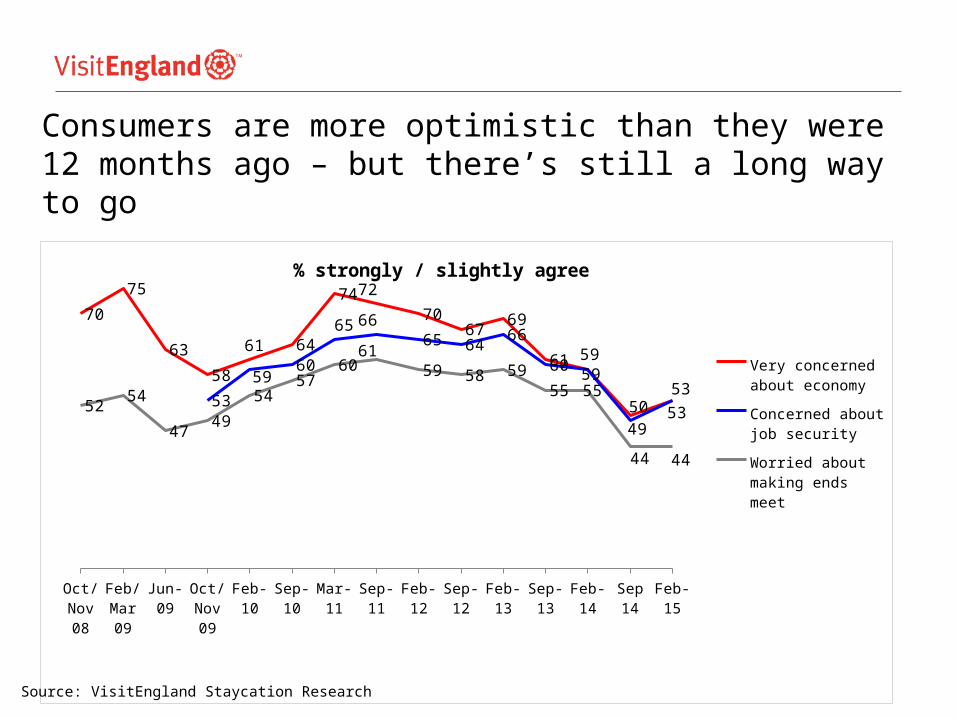

Oct/Nov 08

Feb/Mar 09

Jun-09

Oct/Nov 09

Feb-10

Sep-10

Mar-11

Sep-11

Feb-12

Sep-12

Feb-13

Sep-13

Feb-14

Sep 14

Feb-15

70

75

63

58

61 64

7472

7067

69

6159

50 5353

5960

65 6665 64

66

6059

49

5352

54

4749

5457

6061

59 58 5955 55

44 44

% strongly / slightly agree

Very concerned about economy

Concerned about job security

Worried about mak-ing ends meet

Consumers are more optimistic than they were 12 months ago – but there’s still a long way to go

Source: VisitEngland Staycation Research

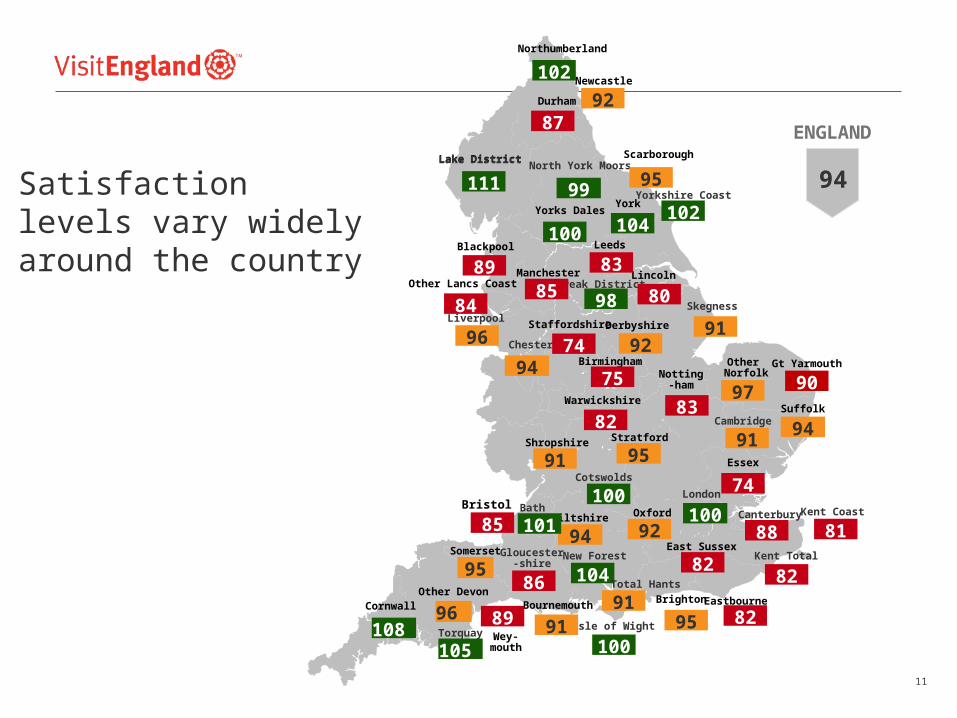

94

ENGLAND

Cornwall

Lake District

xNorthumberland

Yorks DalesYork

Bristol

Manchester

Gt Yarmouth

Essex

Leeds

East Sussex

ScarboroughLake DistrictNorth York Moors

Liverpool

Bath

Cotswolds

London

New Forest

Isle of WightTorquay

Yorkshire Coast

97

x

x

Kent Coast

Durham

Warwickshire

Gloucester-shire

Staffordshire

Lincoln

Eastbourne

Peak District

Skegness

Notting-ham

SuffolkCambridge

Newcastle

Blackpool

Chester

Bournemouth

Wey-mouth

Somerset

Oxford

StratfordShropshire

Brighton

Wiltshire

Derbyshire

Other Devon

Birmingham Other Norfolk

x

x

Canterbury

11

95

96

105108

94

90

95100

81

82

100

74

75

92

74

100102

104

111

85

91

87

102

100

101

10486

88

91

92

83

8389

91

95

96

97

80

91

94

99

82

85

Total Hants

91

95

Kent Total

8282

94

92

89

98

Satisfaction levels vary widely around the country

Other Lancs Coast

x84

Rural tourism growth: Responding to the consumer

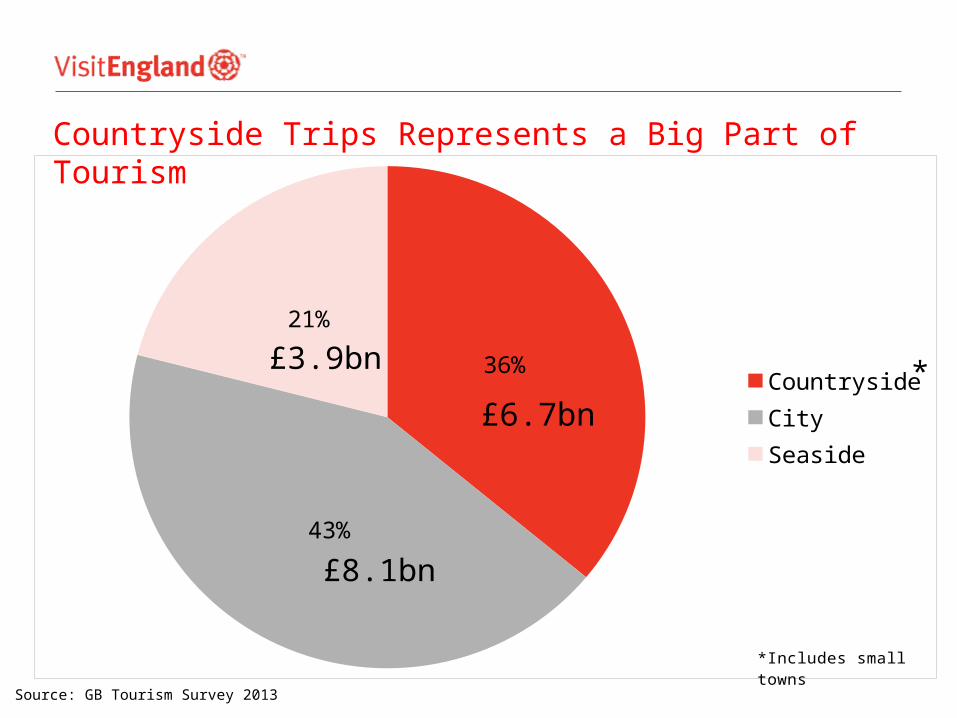

Countryside Trips Represents a Big Part of Tourism

36%

43%

21%

CountrysideCitySeaside

£8.1bn

£3.9bn *

*Includes small towns

£6.7bn

Source: GB Tourism Survey 2013

City and countryside breaks are two of the key drivers of the staycation trend

2006 2007 2008 2009 2010 2011 2012 20130

2

4

6

8

10

12

14

16

18

Domestic Holidays by Social Grade 2006-2013

Seaside Countryside/ village Large city/ large town

Trips (m)

-6%+26%

+16%

-20%

2006 vs 2013

Seaside

City / Large Town

Countryside

Source: GB Tourism Survey 2013

• If the consumer is king, we need to understand how his (or her) needs and wants are changing

• Spending on culture and leisure has grown

• Work-life balance remains a challenge

The world is changing fast starting & ending with the customer

• Access• Fear of unknown• Perceptions• Seasonality• Weather• Quality of product and

experience

Barriers

Easy to get to by public transport

Ease of getting around by public transport

Reasonably priced car parking

Availability of independent local shops

Wide range of attractions and things to do

Doesn't take too long to get to

27%

28%

43%

51%

56%

57%

39%

40%

40%

50%

58%

57%

All English Destinations Countryside Destinations

% Describing Destination as Excellent or Very Good

Access issues relate to public transport rather than time / distance

Source: VisitEngland Brand & Satisfaction Tracker

The unknown countryside.• A blurred picture despite evocative

perceptions

• Holidaymakers can imagine appealing countryside images (when asked to visualise)

• Don’t always have a clear image of what they can do

• Pre-family most likely to feel it’s boring

• They’re also often unsure where to find this appealing countryside

“The countryside is just green and boring.”(London: Pre-family)

A few words about the weather

• Most people know the weather can be changeable

• The English know you can’t count on the weather!

• Rural areas it is perhaps a greater barrier

• Messaging needs to focus on: Still lots to do and enjoy if it rains Lists/ reminders of wet weather activities If your dressed appropriately it’s still fun

to be outside Fun to be had inside “No such thing as bad

weather, just bad clothing.”(York: Family)

“Mention a pub and everyone's’ happy.”(York: Family)

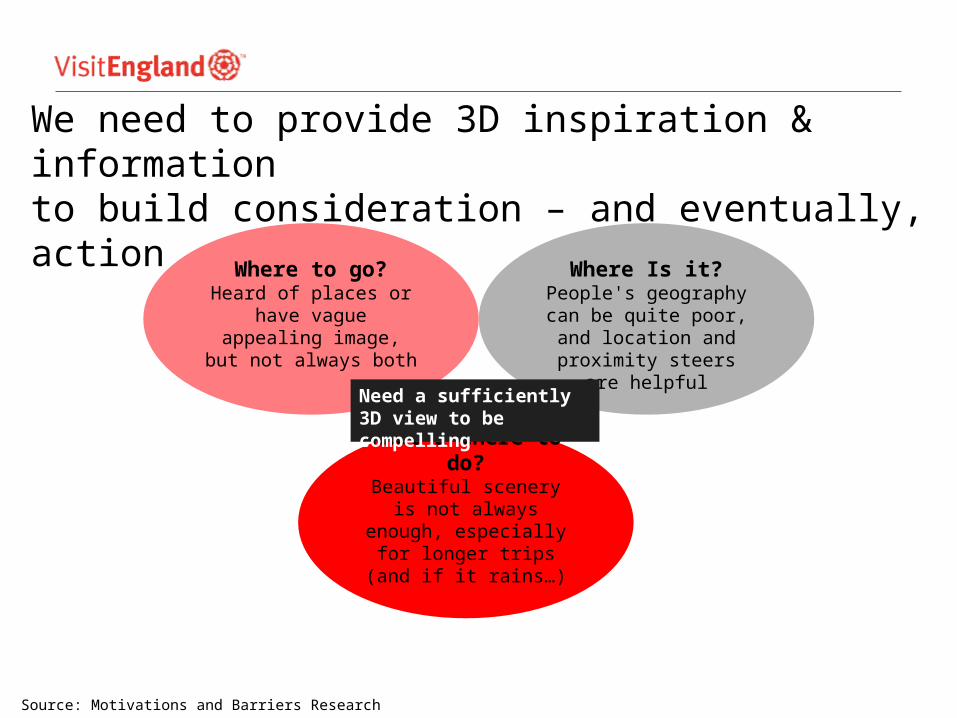

We need to provide 3D inspiration & information to build consideration – and eventually, action

Where to go?Heard of places or

have vague appealing image, but not always

both

Where Is it?People's geography

can be quite poor, and location and proximity

steers are helpful

What’s there to do?

Beautiful scenery is not always enough, especially for longer

trips (and if it rains…)

Need a sufficiently 3D view to be compelling

Source: Motivations and Barriers Research

Opportunities

EscapeExperience

ExerciseEnlightenment

Increasingly urbanised population keen to get away from towns and cities

80% Of the UK population live

in urban areas

Escape

Source: Trajectory Global Foresight

Sedentary lifestyles and sense that life is ‘too easy’ – driving

consumers to push themselves and seek adventure

43% Say that ‘adventure and

taking risks’ is important to them

54% Say that ‘trying new things’

is important to them

Experience

Source: Trajectory Global Foresight

Quality of the Experience: Distinctive and Local

• Tourism is more than just selling!• Need to ensure the visitor experience

excellentHigher spend, higher returns and more recommendations

• Creating destination distinctivenessLocal activities and eventsthings you can’t or wouldn’t do closer to homeMixing with the friendly localsIndependent shops, restaurants, etc.

• Local produce, food and drink (specialties)

enjoying good produce and food is increasingly key to holidaymakers

Health conscious consumers look for breaks that exhilarate and

help them keep fit

Healthier older people means that consumers are active for

longer into retirement – not just for younger consumers

Exercise

Source: Trajectory Global Foresight

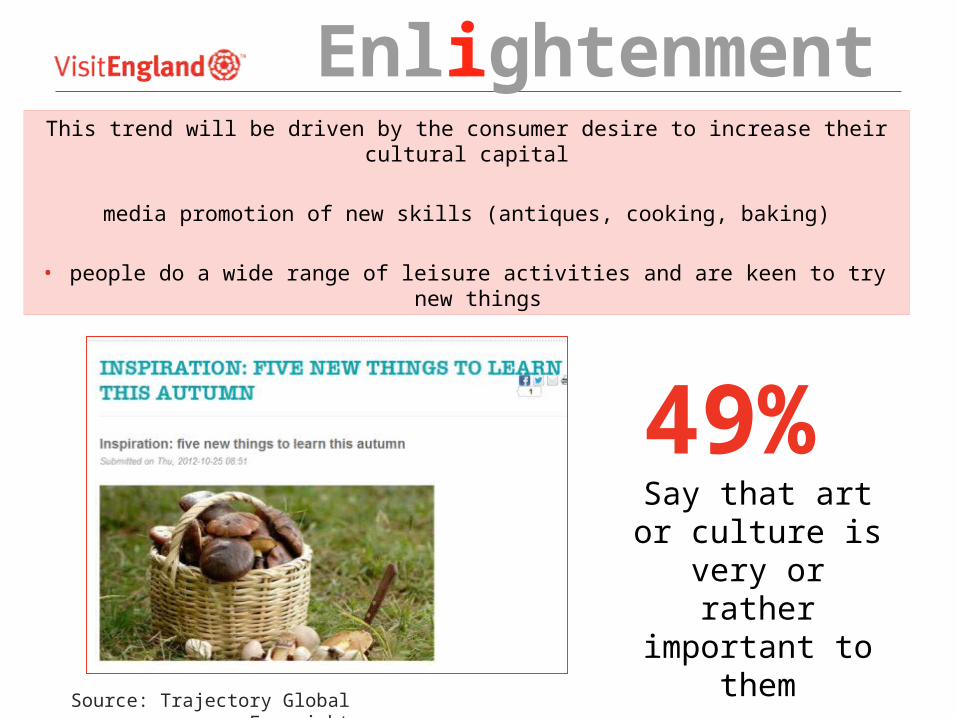

This trend will be driven by the consumer desire to increase their cultural capital

media promotion of new skills (antiques, cooking, baking)

• people do a wide range of leisure activities and are keen to try new things

49% Say that art or

culture is very or rather important

to them

Source: Trajectory Global Foresight

Enlightenment

Sustainable growth through partnership & collaboration

• Supports enterprise and jobs

• Drives investment through building image and brand

• Sustains local services e.g. transport

• Protects and preserves heritage & natural landscapes

• Attracts local spend for reinvestment

• Supports the wider local economy/supply-chain e.g. local food & drink

The case for sustainable growth

• Our shared growth ambition

• 5% average growth, year on year, in the value of tourism since 2010

• 7% uplift in jobs since 2010 = 178,000

• Circa 70% of actions completed

• Refreshed in 2015

Importance of local delivery• Local tourism bodies

- Promotion vs management - 200+ local tourism bodies- Circa 40 considered DMOs- Some operating within a larger entity- Most looking for engagement with VE

• New organisations becoming involved in tourism/visitor economy – Chambers of Commerce, Business Improvement Districts, LEPs

• 39 LEPs with a clearly identified interest in tourism

Crucial role of Destination Management

Common Vision• Partnership• Understanding destination SWOT• Destination Management Plan

Visitor Experience• Clean, tidy, safe, inviting and

welcoming places• Accessible destinations

Developing the destination• Understanding Performance• Product development and

investment

Selling the destination• Co-ordinated, holistic and focused

marketing• Information provision

Destination Management

●A new Government

●Northern & South West Funds

●Product development Fund

●UK GREAT Challenge Fund

●EU investment

But challenges ahead…• National balance• International competition• Public sector support• Tourism’s ‘perception’

Seizing the opportunity!

Working together – collaboration is key

Further information

Lyndsey SwiftHead of Strategic Partnerships020 7578 [email protected]

www.visitengland.com/biz

@visitenglandbiz