LUXURY SENTIMENT SURVEY REPORT - Amazon...

18

LUXURY SENTIMENT SURVEY REPORT WEALTH-X INSTITUTE SPECIAL REPORT Q1 2015: A NEW YEAR – LOOKING AHEAD TO 2015 WWW.WEALTHX.COM

Transcript of LUXURY SENTIMENT SURVEY REPORT - Amazon...

LUXURY SENTIMENT SURVEY REPORT

WEALTH-X INSTITUTE SPECIAL REPORT

Q1 2015: A NEW YEAR – LOOKING AHEAD TO 2015

WWW.WEALTHX.COM

We at Wealth-X are proud to present the first instalment of the Wealth-X Luxury Sentiment Survey Report for 2015. This report is essential reading for those who want to gauge the level of optimism in the luxury industry with regards to the future of its relationship with ultra high net worth (UHNW) individuals, and understand the reasons behind this sentiment. The level of optimism at the end of Q4 2014, although lower than it was prior to the holiday shopping season, is almost one point higher than it was at the beginning of 2014. More than 70% of all respondents to our Luxury Sentiment Survey expect that their total revenue and their engagement with UHNW individuals will grow over the coming quarter, although the majority of respondents are more optimistic in their outlook for all of 2015 than they are for just the first quarter of the year.

Responses to Wealth-X’s previous Luxury Sentiment Surveys showed that events and experiential marketing are key strategies for engaging UHNW clients. For 72% of respondents, affinity partnerships

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 2

A NOTE TO THE READER

David S. FriedmanPresident

Mykolas D. RambusChief Executive Officer

are an important aspect of such engagement. In this survey, we asked respondents specific questions regarding their use of such partnerships: evaluating their advantages and disadvantages, length of partnerships, usefulness of partners and expectations for the future. 68% of respondents plan on increasing their use of affinity partnerships as a means of engaging their UHNW clients.

Affinity, passions, hobbies and interests are the key to engaging the ultra affluent audience. Brands often make the mistake of designing a marketing strategy that imposes their content rather than allowing the individual life narratives of their target audience to shape their approach. The brands that are successfully engaging this audience start with what’s important to their clients and build a “bespoke marketing strategy” that customises the nature of the content presented — often by working with affinity partners to maximise their clients’ engagement.

KEY FINDINGS

• The Luxury Industry Sentiment Index (LISI) stands at 100.6, almost the same level as it was at the start of 2014.

• Competition was the biggest obstacle in Q4 2014, followed by personnel issues, particularly in the traditional luxury subsector. Despite these constraints, respondents were still optimistic regarding their long-term performance and prospects.

• Outlook for 2015 as a whole was more optimistic than for the first quarter of the year, with 92% of respondents expecting to see growth in total revenue in 2015, up from below 75% for the first quarter.

• Fast revenue growth is expected in the luxury industry this year, with 40% and 50% of respondents expecting to see revenue increase by more than 10% in the first quarter of 2015 and the whole of 2015 respectively.

• Only 10% of respondents have no expansion plans in either Q1 2015 or throughout 2015. For the other 90% of respondents, new product launches were particularly significant, with around 40% of respondents expecting to launch new products either during Q1 2015 or at some point during the year.

• Respondents from the hospitality and services industry were the most likely to have expansion plans in Q1 2015, with more respondents planning on opening new stores, launching new products and increasing their digital presence in the first quarter of the year, rather than later in the year.

• Despite a growing number of respondents targeting specific geographical regions, 36% of respondents reported that the majority of their clients were from North America — and not all of these respondents were solely responsible for that region.

• 72% of respondents used affinity partnerships as one of their marketing strategies for targeting UHNW clients. Although this was a common practice across the industry, providers of big luxury items such as yachts, planes and motor cars had the highest proportion of respondents (37%) stating that affinity partnerships were not part of their marketing strategies.

• Only 47% of respondents agree or strongly agree that “marketing strategies with affinity partnerships have higher ROI than those without affinity partners”.

• 82% of respondents who have affinity partnerships use them for targeted and bespoke events.

• 78% of respondents felt that affinity partners were particularly helpful in expanding customer base, and 68% think that these partners help to increase the prestige/awareness of their companies.

• 61% respondents only had one or two partners at any one time, and 53% of respondents focused on long-term partnerships of one year or longer. This enabled them to remove the perceived risk of incompatibility with their partners, which ranked as the main disadvantage when using affinity partners.

• 78% of respondents plan on increasing their use of affinity partners in the future.

92%expect to see their total

revenue grow in 2015

90%have plans to expand

throughout 2015

72%have used affinity

partnerships to target UHNW clients

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 3

THE LUXURY INDUSTRY & UHNW INDIVIDUALS

Only 11% of respondents said they did not specifically define UHNW individuals, confirming the trend we have identified in previous surveys: UHNW individuals are crucial to the luxury industry. Even those 11% who do not specifically qualify UHNW individuals still categorise

61% of respondents said that 75% to 100% of their revenue was derived from UHNW clients. In this edition of the Luxury Sentiment Survey, this breakdown held true across types of luxury — from jewellery and watches to art, yachts and services.

N/B: This breakdown varies per survey, but the Luxury Industry Sentiment Index (LISI) is weighted so as to provide comparable results.

Proportion of Total Revenue Derived from UHNW Clients1

1 This graph is representative of the respondents in the

survey and may not apply to the entire luxury industry.

75%–100%

25%–50%

50%–75%

0%–25%

No Differentiation

11% 10%

5%

13%

61%

themselves as providers of luxury services/goods to UHNW clients. For many providers of luxury goods and/or services, while there may not be a specific definition for a type of individual based on his or her net worth, classifications do remain important.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 4

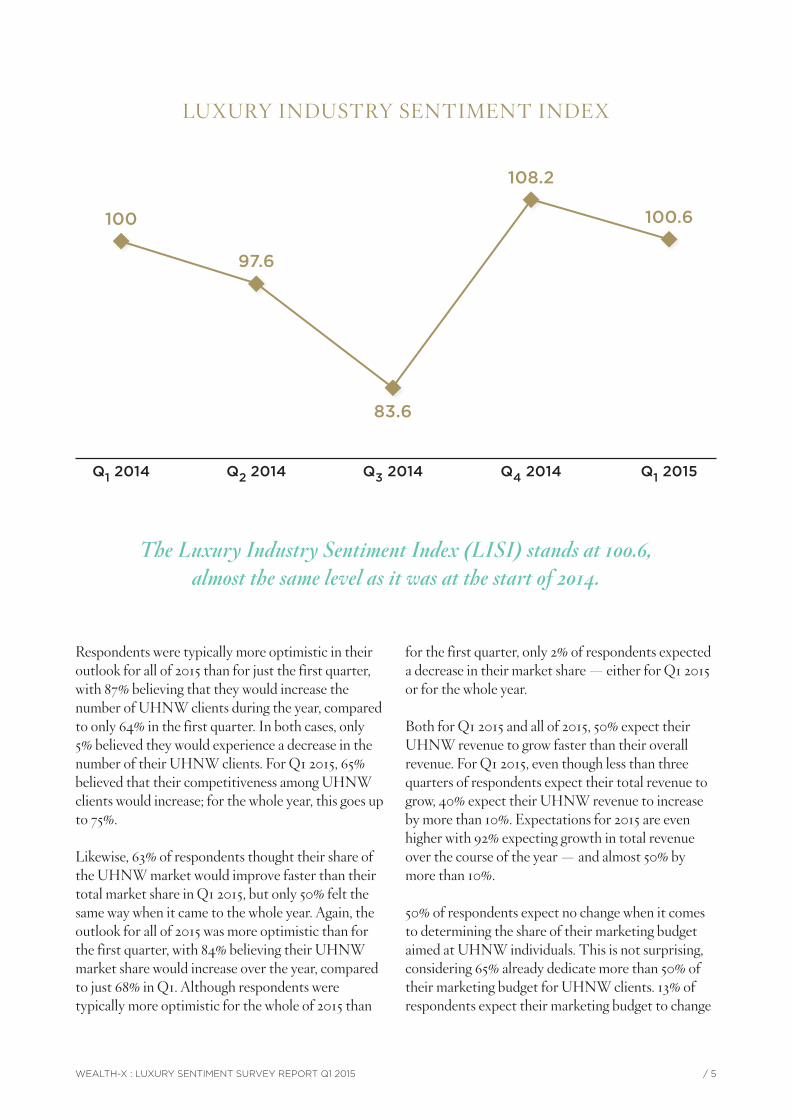

LUXURY INDUSTRY SENTIMENT INDEX

The Luxury Industry Sentiment Index (LISI) stands at 100.6, almost the same level as it was at the start of 2014.

Respondents were typically more optimistic in their outlook for all of 2015 than for just the first quarter, with 87% believing that they would increase the number of UHNW clients during the year, compared to only 64% in the first quarter. In both cases, only 5% believed they would experience a decrease in the number of their UHNW clients. For Q1 2015, 65% believed that their competitiveness among UHNW clients would increase; for the whole year, this goes up to 75%.

Likewise, 63% of respondents thought their share of the UHNW market would improve faster than their total market share in Q1 2015, but only 50% felt the same way when it came to the whole year. Again, the outlook for all of 2015 was more optimistic than for the first quarter, with 84% believing their UHNW market share would increase over the year, compared to just 68% in Q1. Although respondents were typically more optimistic for the whole of 2015 than

Q1 2014 Q2 2014 Q4 2014

100

97.6

83.6

Q3 2014

108.2

for the first quarter, only 2% of respondents expected a decrease in their market share — either for Q1 2015 or for the whole year.

Both for Q1 2015 and all of 2015, 50% expect their UHNW revenue to grow faster than their overall revenue. For Q1 2015, even though less than three quarters of respondents expect their total revenue to grow, 40% expect their UHNW revenue to increase by more than 10%. Expectations for 2015 are even higher with 92% expecting growth in total revenue over the course of the year — and almost 50% by more than 10%.

50% of respondents expect no change when it comes to determining the share of their marketing budget aimed at UHNW individuals. This is not surprising, considering 65% already dedicate more than 50% of their marketing budget for UHNW clients. 13% of respondents expect their marketing budget to change

Q1 2015

100.6

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 5

Challenges in Q4 2014

For 29% of respondents, the biggest challenge in Q4 2014 was competition. Personnel issues and demand constraints were also significant obstacles to performance. Within the “other” types of challenges category, customer expectations registered a number of entries.

29%

Competition

Decreased Demand

Lack of Inventory

Personnel

throughout 2015, with 87% of these expecting to increase their marketing budget targeting UHNW clients specifically only after Q1.

Along the same lines, only 10% of respondents have no expansion plans for either Q1 2015 or for the whole of 2015. The most common plan during both time periods is new product launches — with 43% and 39% of respondents expecting to proceed with product launch plans in Q1 2015 or at some point in 2015 respectively. 35% of respondents expect to increase their digital presence during the year and 16% expect to open new stores in 2015, though only 10% expect to do so during Q1 2015.

A greater number of respondents in this quarter’s survey were from more niche markets, and the median

number of regions respondents were in charge of dropped from two to one. Consequently, we found that many respondents this time had a majority of clients from their core region — whether it be Africa, the Middle East, Asia... Nonetheless, North America — as the region that is home to largest population of UHNW individuals in the world, and the most valuable market for the luxury industry — has continued to dominate the luxury industry landscape, with 36% of all respondents stating that the majority of their clients came from North America. Europe and Asia were the next two most significant markets for the luxury industry, though both of their proportions declined from over 20% of respondents stating that the majority of their clients came from these two regions in the last quarter to 17% and 13% respectively.

Other

16%

22%

24%

9%

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 6

TRADITIONAL LUXURY*

In the traditional luxury subsector, the most significant obstacle that respondents faced in Q4 2014 was personnel issues, with 43% of respondents stating that this was the single greatest problem of the last quarter. Competition ranked as the second biggest obstacle, with 29%. Despite these issues, 60% of respondents stated they received an increase in enquiries during Q4 2014.

64% expect to gain new UHNW clients in the next quarter and an even higher proportion, 69%, expect to gain new UHNW clients over the year 2015 — showing greater optimism for prospects in the later parts of the year. Despite such an optimistic view, the UHNW segment of the traditional luxury sector is expected to perform less well than the entire industry: 92% of these same respondents expect to see an increase in their total clients (including UHNW clients) over the coming year — much higher than the 58% that expect to see increase in Q1 2015 for total clients. 50% of respondents expect to see total revenue increase by over 10% in the coming quarter and for the whole of 2015.

Only 19% of respondents have no expansion plans in 2015 at all — showing the strong optimism of this subsector. 46% of respondents plan on opening new stores in Q1 2015, compared to 69% over the whole year. The most likely plan for expansion, however, is not new stores, but rather new product launches: with 85% of respondents planning to do so over the year and 56% over the first quarter of 2015.

Only 19% of respondents from the traditional luxury subsector do not make use of affinity partnerships —compared to 28% in the whole industry. The majority of respondents make use of these partnerships during exclusive product launches — often through bespoke events. This is considered the ultimate use of such partnerships because it helps increase a company’s brand prestige/awareness, cultivates expertise in hosting events, and serves to expand the customer basis. For respondents in this subsector, choosing a partner was dependent on various criteria including compatibility in branding, followed by experience and potential for future collaboration.

* Traditional Luxury include Apparel, Shoes & Leather Goods, Jewellery & Timepieces.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 7

BIG LUXURY ITEMS*

In the big luxury items subsector, 50% of respondents indicated that both personnel and competition were significant hurdles during the last quarter of 2014. Despite these issues, 56% of respondents saw increased enquiries for their products in Q4 2014.

59% of respondents to this quarter’s Luxury Sentiment Survey expect to increase the number of their UHNW clients in Q1 2015 — and an even larger proportion expect to do so over the year: 83%. A further indication of optimism in this industry is shown by the fact that 48% of respondents expect growth in excess of 10% in total revenue for both Q1 2015 and for the entire year of 2015. As a way to ensure that such expectations are met, 62% of respondents indicated that new products launches would be the main expansion plan for their businesses over the coming quarter and year, while only 8% have no expansion plan for either periods.

Affinity partnerships were least prevalent in this subsector of the luxury industry, with 37% stating they do not engage in such marketing initiatives. The other 63% used prior contacts and referrals with external brands in their exclusive product launches and/or targeted/bespoke events. The crucial added value that such partnerships provided was in the expansion of the respondent’s customer base and guest list, and increasing brand prestige/awareness.

Expertise in an industry other than the respondent’s was highlighted by respondents as one of their top three priorities when it came to evaluating the value of a partner, with 24% of respondents stating that the chance of increased competition was the most significant risk when it came to establishing such affinity partnerships. Nonetheless, 65% of respondents in this subsector stated that, typically, their partnerships lasted a year or longer.

* Big Luxury Items include planes, helicopters, yachts and motor vehicles.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 8

HOSPITALITY & SERVICES

Only 8% of respondents in this industry felt that competition was their most significant obstacle at the end of Q4 2014. Instead, personnel issues and regulations were considered to be the most important barriers to performance, according to over 50% of respondents.

The fact that competition is an apparently limited issue for these respondents helps explain why 57% of them experienced an increase in the number of enquiries for their products/services in Q4 2014, as well as why the industry was particularly optimistic with no respondents expecting a decrease in the number of their UHNW clients. Only 6% of respondents expect a decrease in total clients over the year, while 50% of respondents expect to see total revenue in the first quarter grow by more than 10%, and 64% expect growth of more than 10% over the whole of 2015. Their outlook is even more bullish with regards to UHNW clients, with 68% and 78% expecting growth of more than 10% in revenue from UHNW clients alone over the first quarter of 2015 and the whole year, respectively.

Respondents typically seemed more enthusiastic in their expansion plans in the first quarter of the year than over the rest of the year, with 57% planning new products, 21% planning new stores and 50% planning an increase in digital presence in the first quarter of 2015, each percentage higher than for the rest of the year. Nonetheless, 36% and 21% of respondents were not planning on any expansion in Q1 2015 and all of 2015 respectively.

Only 14% of respondents in this subsector did not engage in affinity partnerships as a marketing strategy. For the other 86% of respondents, expanding the customer base and increasing the guest list for any bespoke/targeted event was the main added value affinity partners provided, although for almost 50% of respondents, cost reduction was also considered important. In terms of selection criteria, experience and compatibility in branding were considered the most important characteristics for potential affinity partners, although risk of incompatibility was deemed the most likely adverse effect of affinity partnerships.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 9

ALTERNATIVE LUXURY*

43% of respondents in this subsector felt competition was their single biggest obstacle in the last quarter of 2014. This subsector of the luxury industry was also the most likely to be pessimistic when it came for its future performance, with 13% of the subsector’s respondents experiencing a decrease in the number of enquiries they received during Q4 2014 and 19% of respondents having no expansion plans. Despite this, 67% of respondents expect to see an increase in number of clients and none expect a decrease in this coming quarter. These respondents were even more optimistic for the whole of 2015, with 87% expecting an increase in UHNW clients.

Although 33% of respondents expect no change in total revenue this quarter, all expect an increase over the year and 45% expect an increase of more than 10% in 2015 — in terms of total revenue and UHNW revenue. For most respondents in this subsector, increased digital presence is the main expansion plan,

with 69% of respondents expecting to increase this aspect of their marketing strategy over the year.

88% of respondents engaged in affinity partnerships when it comes to marketing to the UHNW population - particularly through targeted and bespoke events for 80% of respondents. The prospect of an expanded customer basis was the most significant factor when it came to the usefulness of such partnerships, and the main criterion was compatibility in branding. On the other hand, the main fear was that events or marketing strategies done in conjunction with a partner would have an appeal considered too broad for the respondent’s clients. Despite this concern or perhaps because of this, 67% of respondents used affinity partnerships for longer than one year and only one or two partners were typically used at any one time.

* Alternative luxury includes spirits & wines, art & collectibles.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 10

ENGAGING WITH UHNW INDIVIDUALS:AFFINITY PARTNERSHIPS

Prior relationship

Partner Selection

Referral Other

80% 70%

20%

Cold contact

72% of respondents use affinity partnerships when it comes to engaging with UHNW clients, but only 47% agree that “marketing strategies with affinity

partnerships have higher ROI than those without affinity partners”.

As with connecting and engaging with UHNW clients, the selection of affinity partners is rarely done through cold calling — with only 20% of respondents using such a technique to form these relationships.

Exclusive products

Use of Affinity Partners

Large public events (conferences, road

shows, etc.)

Other

61%

29%

82%

Targeted and bespoke events

11%

5%

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 11

Affinity Partner Contribution

Guest list

Venue selection

Cost reduction in event hosting

Expanded customer base

Prestige / Awareness

Expertise in hosting events

59%

35%

41%

78%

68%

46%

Previous editions of the Wealth-X Luxury Sentiment Survey Report suggested that events and bespoke marketing were particularly important methods of engaging with UHNW clients. This remains the case, with the use of affinity partners being particularly important for targeted and bespoke events.

Although there is no doubt that there are numerous advantages to having affinity partners, two stand out: the ability to expand one’s client base and the ability to increase brand prestige or awareness. This is crucial to the value of an affinity partnership: for

RANK

1

2

3

4

5

MOST IMPORTANT CHARACTERISTICS OF PARTNERS

Experience in similar events

Potential for future collaboration

Domain expertise (in same industry)

Domain expertise (in other industry)

Compatibility in branding

most brands, VIP clients are already aware of the value of their goods/services — a partner will help promote this reputation, while enhancing its own reputation at the same time. Furthermore, a partner can help in organising successful marketing strategies:

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 12

5% of respondents specified there were no disadvantages to affinity partnerships, with some of these respondents specifying this to be the case when the partnership was well planned.

RANK

1

2

3

MAIN DISADVANTAGES WITH AFFINITY PARTNERSHIPS

Risk of incompatible affinity partnership

Appeal too broad

Risk of increased competition

One

Number of Partners (at any one time)

Two More than Five

31% 30% 27%

Three to Five

12%

78% of respondents plan on increasing their use of affinity partnerships in the future.

Despite the numerous advantages of affinity partnerships, it is clear that too many can be counterproductive. In fact, for over 60% of respondents, two or less affinity partners were used at any one time, and the majority — 53% — of such partnerships lasted for a year or longer.

Length of Partnership

Other

Longer than one year

One year

One season

One event

5%

14%

16%

16%

49%

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 13

THE SURVEY: METHODOLOGY

Respondents to our survey come from various sectors within the luxury industry including Clothing, Shoes & Leather; Watches & Jewellery; Household Furnishings; Electronics; Spirits & Wines; Antique, Art & Collectibles; Hospitality & Services; Planes

& Helicopters; Yachting & Boating and Motor Vehicles. The survey was conducted between January 13th 2015 and January 24th 2015. The survey was sent to over a thousand different brands across all sectors of the luxury industry as listed above.

Asia

Proportion of RespondentsResponsible for Specific Regions*

Europe

42%

* Respondents could choose more than one region, hence the percentages add up to more than 100%.

41% 45%

28%19% 16% 17%

NorthAmerica

MiddleEast

Latin America

Oceania Africa

These respondents, in their positions at their respective firms, are typically responsible for numerous regions. On average, each respondent’s role was responsible for almost three regions, a constant throughout the last four surveys. The resulting diversity in our results enabled us to draw unique, global insights into where revenue in the

luxury industry was generated in Q4 2014, where growth is more likely to come from in the future and what the luxury industry expects for 2015, both during Q1 and throughout the year, as well as how the industry regards and makes use of affinity partnerships.

The sixth edition of Wealth-X Luxury Sentiment Survey will be conducted between March 17th and March 29th 2015. If you would like to take part in the next Luxury Sentiment Survey, please email [email protected].

Alternatively, an invitation link will be distributed through the Wealth-X newsletter on March 18th and March 25th 2015.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 14

WEALTH-X SOLUTIONS

Wealth-X is the first organisation to focus exclusively on UHNW intelligence, research and insights to support financial institutions, not-for-profit organisations and luxury brands working with the ultra affluent.

Wealth-X’s team has a passion for partnering with our clients to develop successful strategies to connect with UHNW individuals.

PROFESSIONAL

Wealth-X Professional is an online collection of global UHNW individual dossiers, highlighting their financial profiles, passions and interests, known associates, affiliations, family members, biographies, news and much more.

Designed to help expand our client’s business, Wealth-X Pro enables private bankers, business development professionals, fundraisers and luxury brand marketers to spend less time researching prospects and more time developing business relationships.

INTEGRATION

The full integration of Wealth-X data within our clients’ CRM systems enables the big data automation of new UHNW client identification and business development.

Our intelligence is delivered directly into our clients’ IT infrastructure through a bespoke API, Salesforce or Pythagoras interface. Customer and prospect data never leaves the local environment, providing clients with all the benefits and functionality of Wealth-X Professional to multiple users through a single access point.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 15

DILIGENCE

Wealth-X Diligence provides in-depth intelligence on UHNW individuals, combining wealth intelligence and Know Your Customer (KYC) solutions for financial institutions and not-for-profit organisations to meet their regulatory requirements and mitigate reputational and commercial risk.

Wealth-X Diligence provides clients with enhanced dossiers on UHNW individuals, detailing their source of wealth, significant litigation or sanctions, political inclinations and connections, wealth breakdown and analysis, business activities and asset holdings.

SCREENING

Wealth screening unlocks the potential in your customer or prospect data using our unparalleled coverage on UHNW individuals and expertise in matching and identity resolution.

Wealth-X Screening complements your knowledge of the ultra-wealthy and their relationship networks and provides powerful client analytics for new UHNW client or donor initiatives.

Assess market and wallet share; Drive new business cases; Leverage market segmentation through UHNW characteristics; Perform statistical analyses on UHNW consumer spend or philanthropic giving.

ADVISORY

Wealth-X offers bespoke advisory services that provide intelligence on evolving global wealth creation trends and dynamics through advisory projects and reports for our clients, generated by our Institute. The Institute supports leaders in the banking, luxury, and non-profit sectors in making informed decisions.

Our advisory has produced dozens of high profile reports including the World Ultra Wealth Report and the Billionaire Census in partnership with UBS, Around the World in Dollars and Cents with Savills, the Wealth Report 2013 with Knight Frank and several others.

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 16

ABOUT WEALTH-X INSTITUTE

Using the wealth of data collected by Wealth-X’s team of researchers, Wealth-X Institute quantitatively analyses the UHNW population. Variables that can be used in determining clusters and market size include asset analysis, wealth source, net worth, liquid assets, source of wealth, education, interests, age, gender, marital status, and location. This analysis provides valuable insights that can then be identified and explored for a variety of purposes.

Wealth-X Institute provides leaders and decision makers in the private banking, luxury, and philanthropy sectors with data and insights to help them make informed decisions. By bringing internal and external thought leaders together, the Wealth-X Institute illuminates issues that matter to these stakeholders today, as well as those that will in the future.

For the last three years, Wealth-X has published an annual report: the World Ultra Wealth Report. Since 2013, this report has been published in partnership with UBS. 2013 also saw the publication of the inaugural UBS and Wealth-X Billionaire Census Report.

In 2014, Wealth-X partnered with Arton Capital to launch the inaugural Philanthropy Report, while 2015 has seen the launch of The Global Luxury Residential Real Estate Report with Sotheby’s International Realty and the Family Wealth Transfers Report in partnership with NFP.

In addition to these reports, Wealth-X institute publishes insights on UHNW individuals across the financial services, luxury and non-profit sectors.

PARTNERSHIPS

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 17

ABOUT WEALTH-X

Wealth-X is the world’s leading ultra high net worth (UHNW) intelligence and prospecting firm with the largest collection of curated research on UHNW individuals, defined as those with net assets of US$30 million and above. The firm’s Wealth-X Professional solution is the standard for financial institutions, not-for-profit organisations and luxury brands working with the ultra affluent.

Headquartered in Singapore, Wealth-X has 13 offices on five continents.

WWW.WEALTHX.COM

For more information, contact [email protected]

WEALTH-X AND UBS BILLIONAIRE CENSUS 2014http://www.billionairecensus.com

WEALTH-X AND UBS WORLD ULTRA WEALTH REPORT 2014http://www.worldultrawealthreport.com

CONNECT WITH US

WEALTH-X : LUXURY SENTIMENT SURVEY REPORT Q1 2015 / 18