Low quality coals key commercial ... - IEA Clean Coal Centre

24

Low quality coals – key commercial, environmental and plant considerations A report by Dr Stephen Mills IEA Clean Coal Centre, London, UK

Transcript of Low quality coals key commercial ... - IEA Clean Coal Centre

Low quality coals – key commercial, environmental and plant considerations

A report by Dr Stephen Mills

IEA Clean Coal Centre, London, UK

Background

• market has changed - the international

supply and demand situation for these

types of coal has evolved

• use in some economies has increased

significantly

• subbituminous coals and coals with

higher ash content introduced and

traded in increasing quantities

• several reasons – cost saving, depletion

of better quality reserves, security of

supply

• subbituminous and high-ash bituminous coals, and lignite

• important for power generation, cogeneration

• also residential, commercial and industrial applications

The market changes

• global coal demand and consumption increased

• most growth in Asia

• but quality and types of coals traded and utilised

has been changing

• steady decline in quality in some countries

• shift towards greater use of lower quality coals

• many countries rely on indigenous resources

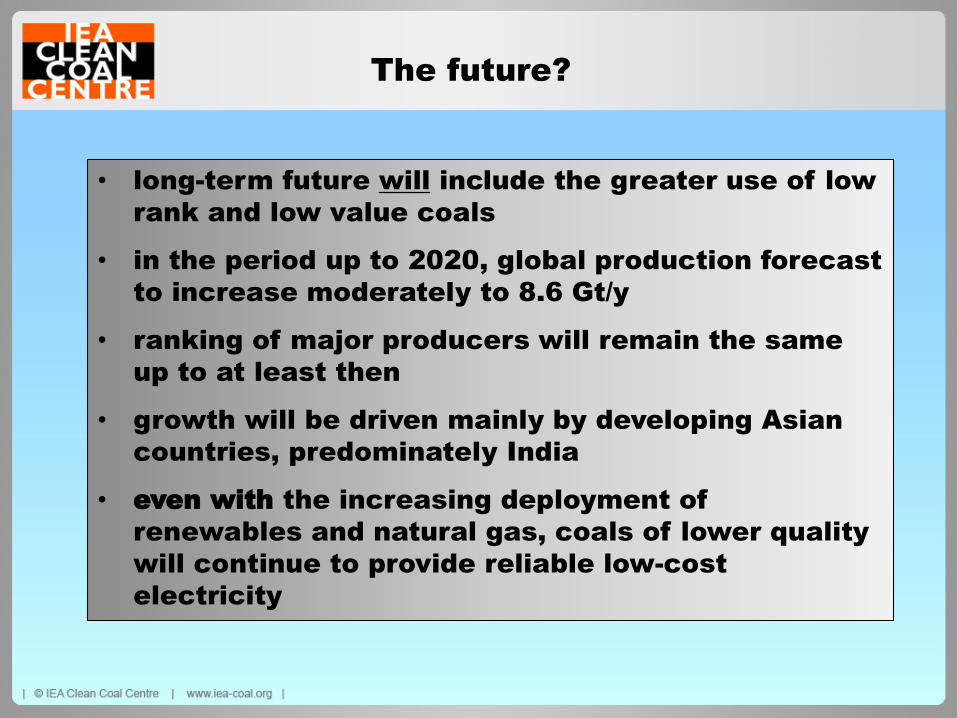

The future?

• long-term future will include the greater use of low

rank and low value coals

• in the period up to 2020, global production forecast

to increase moderately to 8.6 Gt/y

• ranking of major producers will remain the same

up to at least then

• growth will be driven mainly by developing Asian

countries, predominately India

• even with the increasing deployment of

renewables and natural gas, coals of lower quality

will continue to provide reliable low-cost

electricity

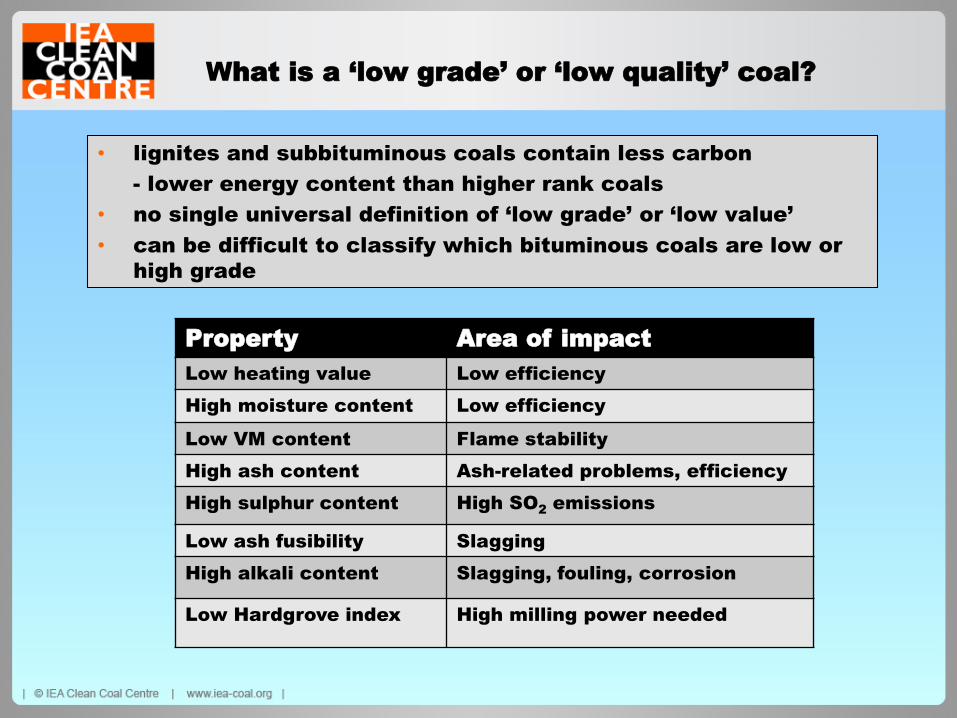

What is a ‘low grade’ or ‘low quality’ coal?

• lignites and subbituminous coals contain less carbon

- lower energy content than higher rank coals

• no single universal definition of ‘low grade’ or ‘low value’

• can be difficult to classify which bituminous coals are low or

high grade

Property Area of impact

Low heating value Low efficiency

High moisture content Low efficiency

Low VM content Flame stability

High ash content Ash-related problems, efficiency

High sulphur content High SO2 emissions

Low ash fusibility Slagging

High alkali content Slagging, fouling, corrosion

Low Hardgrove index High milling power needed

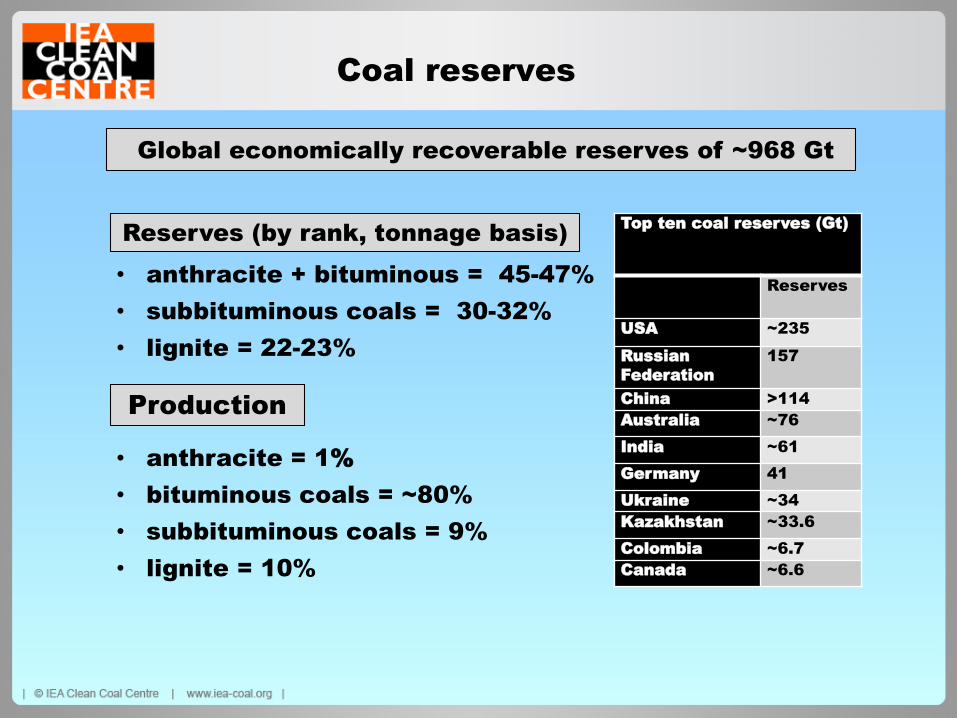

Coal reserves

Top ten coal reserves (Gt)

Reserves

USA ~235

Russian

Federation

157

China >114

Australia ~76

India ~61

Germany 41

Ukraine ~34

Kazakhstan ~33.6

Colombia ~6.7

Canada ~6.6

• anthracite + bituminous = 45-47%

• subbituminous coals = 30-32%

• lignite = 22-23%

• anthracite = 1%

• bituminous coals = ~80%

• subbituminous coals = 9%

• lignite = 10%

Global economically recoverable reserves of ~968 Gt

Reserves (by rank, tonnage basis)

Production

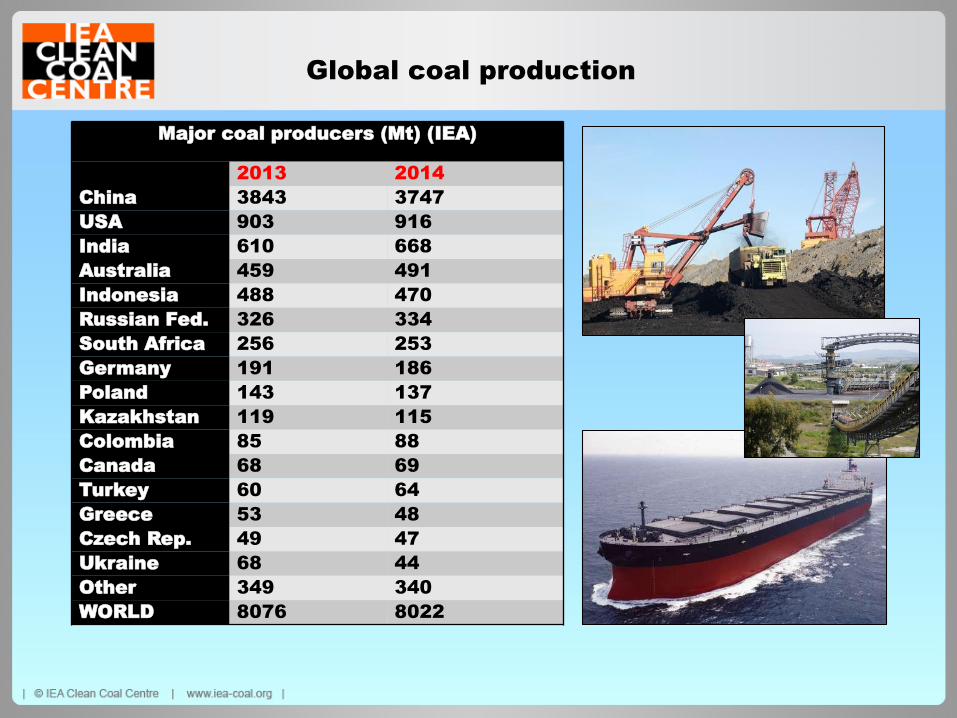

Global coal production

Major coal producers (Mt) (IEA)

2013 2014

China 3843 3747

USA 903 916

India 610 668

Australia 459 491

Indonesia 488 470

Russian Fed. 326 334

South Africa 256 253

Germany 191 186

Poland 143 137

Kazakhstan 119 115

Colombia 85 88

Canada 68 69

Turkey 60 64

Greece 53 48

Czech Rep. 49 47

Ukraine 68 44

Other 349 340

WORLD 8076 8022

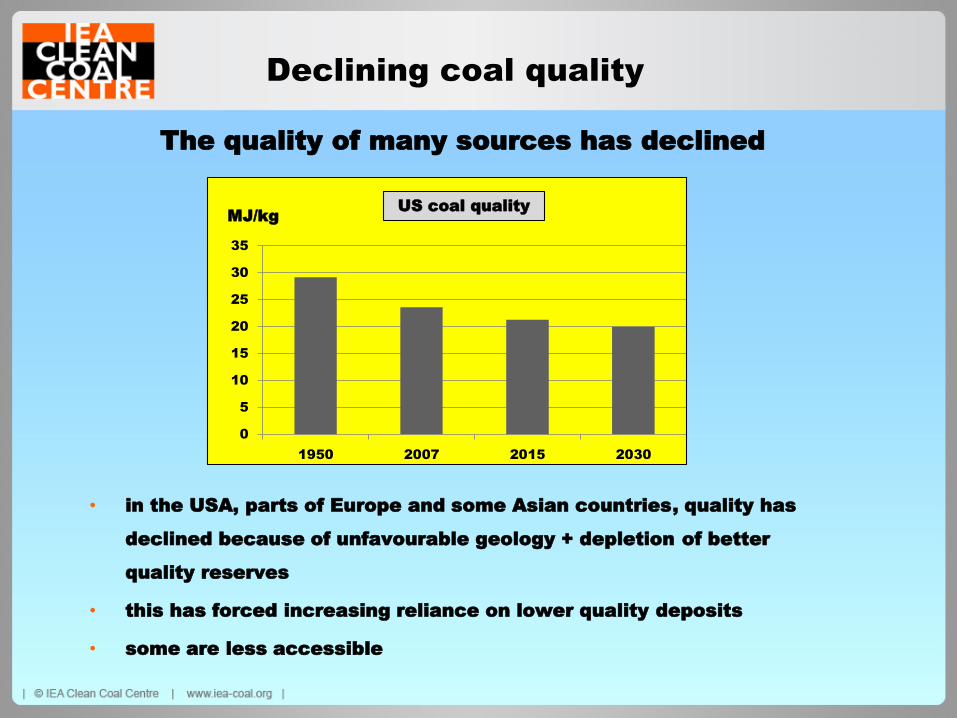

Declining coal quality

The quality of many sources has declined

• in the USA, parts of Europe and some Asian countries, quality has

declined because of unfavourable geology + depletion of better

quality reserves

• this has forced increasing reliance on lower quality deposits

• some are less accessible

0

5

10

15

20

25

30

35

1950 2007 2015 2030

MJ/kgUS coal quality

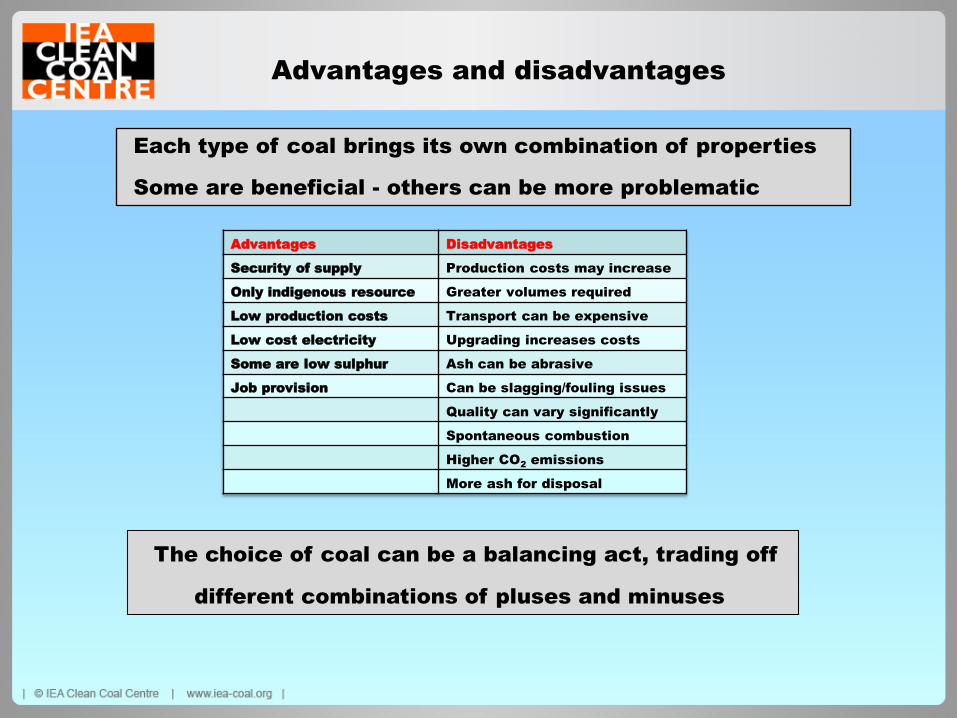

Advantages and disadvantages

Each type of coal brings its own combination of properties

Some are beneficial - others can be more problematic

Advantages Disadvantages

Security of supply Production costs may increase

Only indigenous resource Greater volumes required

Low production costs Transport can be expensive

Low cost electricity Upgrading increases costs

Some are low sulphur Ash can be abrasive

Job provision Can be slagging/fouling issues

Quality can vary significantly

Spontaneous combustion

Higher CO2 emissions

More ash for disposal

The choice of coal can be a balancing act, trading off

different combinations of pluses and minuses

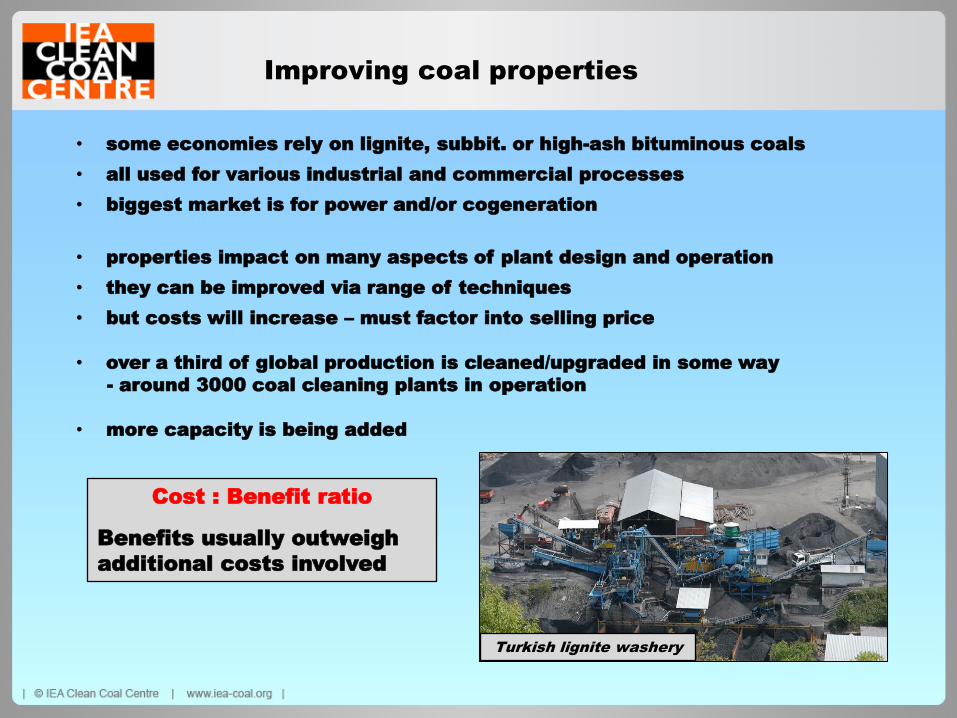

Improving coal properties

Cost : Benefit ratio

Benefits usually outweigh

additional costs involved

• some economies rely on lignite, subbit. or high-ash bituminous coals

• all used for various industrial and commercial processes

• biggest market is for power and/or cogeneration

• properties impact on many aspects of plant design and operation

• they can be improved via range of techniques

• but costs will increase – must factor into selling price

• over a third of global production is cleaned/upgraded in some way

- around 3000 coal cleaning plants in operation

• more capacity is being added

Turkish lignite washery

Coal blending

• in some countries, blending indigenous and imported coals

has increased significantly

• often done to improve the characteristics of poor quality

domestic supplies

Power plants blend for a number of reasons:

• cost saving

• improving plant efficiency and operation

• achieving environmental goals

Blending - a process where two or more different coals are

combined in order to achieve certain quality attributes

A significant proportion of low quality coal output is blended to

produce end-products capable of meeting necessary

specifications at an affordable price

Technologies using low quality coals

Current uses

Biggest market is power generation:

• subcritical PCC

• supercritical/ultrasupercritical PCC

• fluidized bed combustion

Lower quality coals can be used in most conventional

and clean coal utilisation technologies

Technologies using low quality coals

Gasification and IGCC

• a variety of lower quality coals have been gasified

• a number of different technologies have been developed

and deployed

• various end-products produced

• plants operational in the USA, China, and parts of Europe

and Asia

• others in development or under construction

Vresova Great Plains Kemper County

Technologies using low quality coals

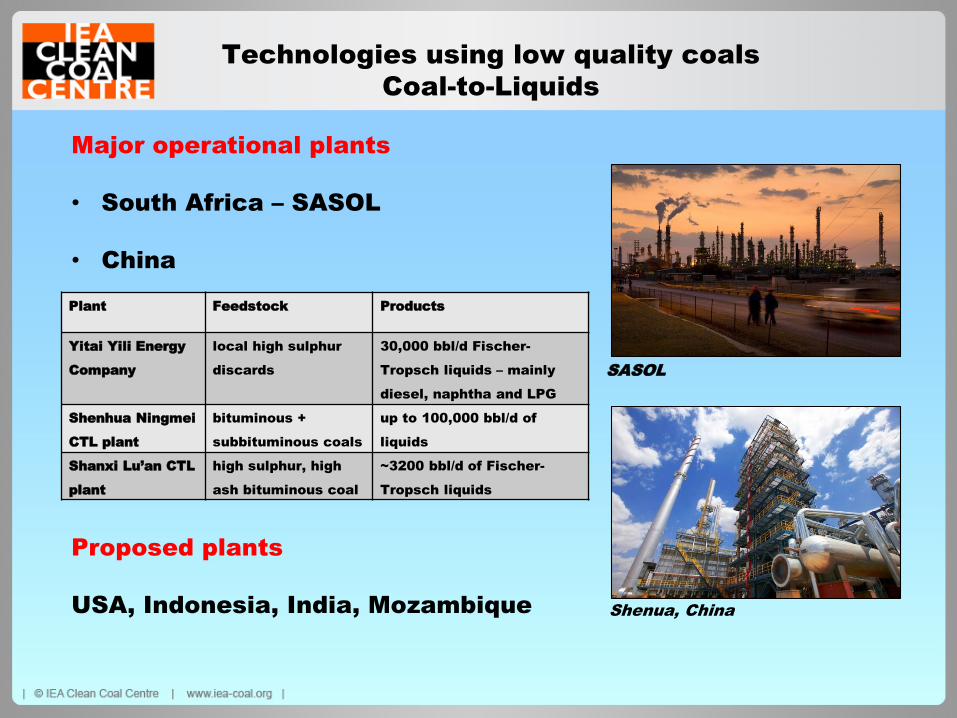

Coal-to-Liquids

Plant Feedstock Products

Yitai Yili Energy

Company

local high sulphur

discards

30,000 bbl/d Fischer-

Tropsch liquids – mainly

diesel, naphtha and LPG

Shenhua Ningmei

CTL plant

bituminous +

subbituminous coals

up to 100,000 bbl/d of

liquids

Shanxi Lu’an CTL

plant

high sulphur, high

ash bituminous coal

~3200 bbl/d of Fischer-

Tropsch liquids

Major operational plants

• South Africa – SASOL

• China

Proposed plants

USA, Indonesia, India, Mozambique

SASOL

Shenua, China

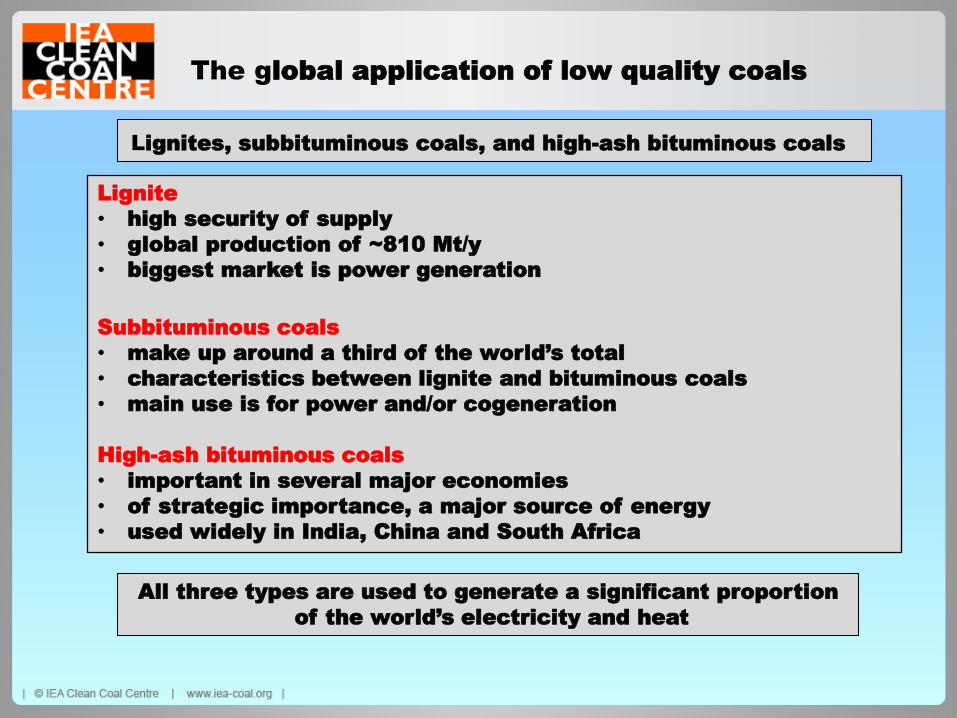

The global application of low quality coals

Lignite

• high security of supply

• global production of ~810 Mt/y

• biggest market is power generation

Subbituminous coals

• make up around a third of the world’s total

• characteristics between lignite and bituminous coals

• main use is for power and/or cogeneration

High-ash bituminous coals

• important in several major economies

• of strategic importance, a major source of energy

• used widely in India, China and South Africa

Lignites, subbituminous coals, and high-ash bituminous coals

All three types are used to generate a significant proportion

of the world’s electricity and heat

Country reports

The report reviews individual countries that rely heavily on one or

more of these types of coal + the type and scale of their application

USA

Russia

China

Australia

India

Germany

Ukraine

Kazakhstan

South Africa

Indonesia

Turkey

Canada

Poland

Greece

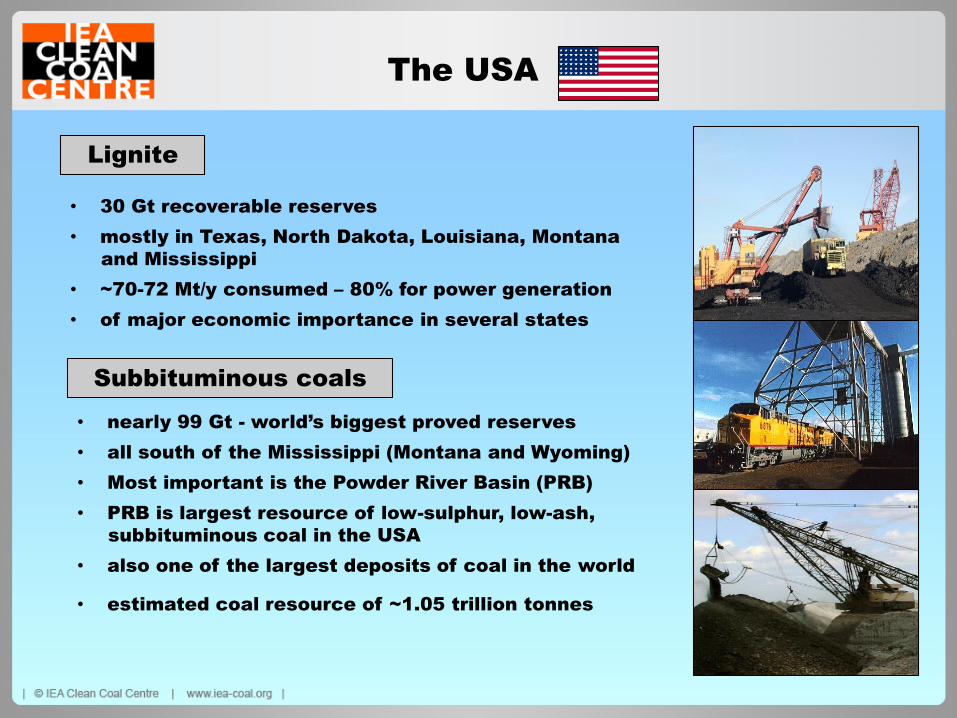

The USA

Lignite

Subbituminous coals

• 30 Gt recoverable reserves

• mostly in Texas, North Dakota, Louisiana, Montana

and Mississippi

• ~70-72 Mt/y consumed – 80% for power generation

• of major economic importance in several states

• nearly 99 Gt - world’s biggest proved reserves

• all south of the Mississippi (Montana and Wyoming)

• Most important is the Powder River Basin (PRB)

• PRB is largest resource of low-sulphur, low-ash,

subbituminous coal in the USA

• also one of the largest deposits of coal in the world

• estimated coal resource of ~1.05 trillion tonnes

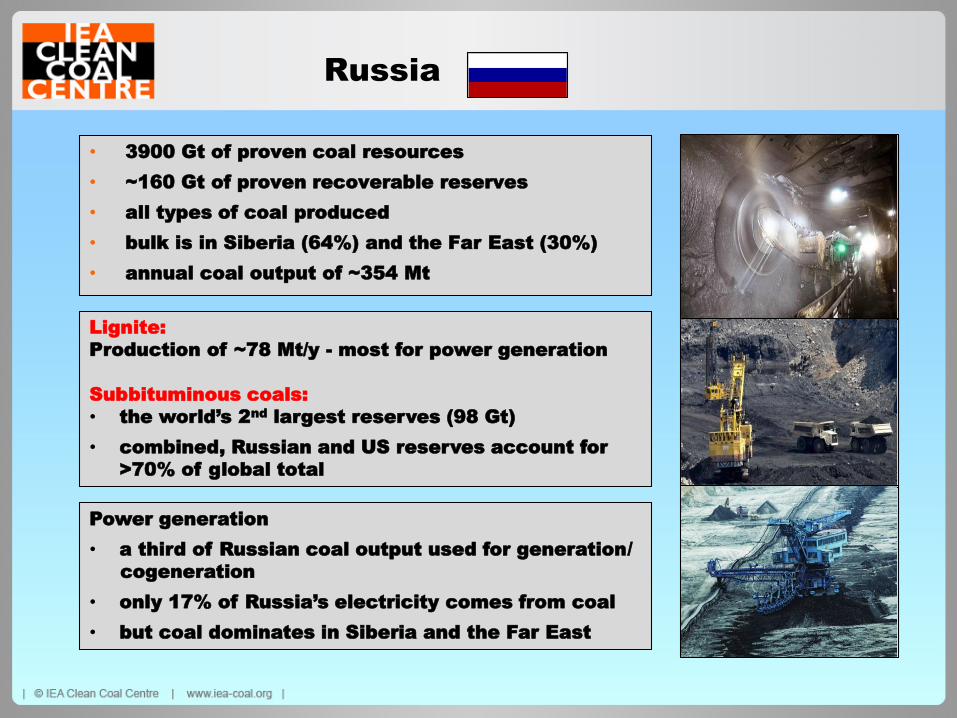

Russia

• 3900 Gt of proven coal resources

• ~160 Gt of proven recoverable reserves

• all types of coal produced

• bulk is in Siberia (64%) and the Far East (30%)

• annual coal output of ~354 Mt

Power generation

• a third of Russian coal output used for generation/

cogeneration

• only 17% of Russia’s electricity comes from coal

• but coal dominates in Siberia and the Far East

Lignite:

Production of ~78 Mt/y - most for power generation

Subbituminous coals:

• the world’s 2nd largest reserves (98 Gt)

• combined, Russian and US reserves account for

>70% of global total

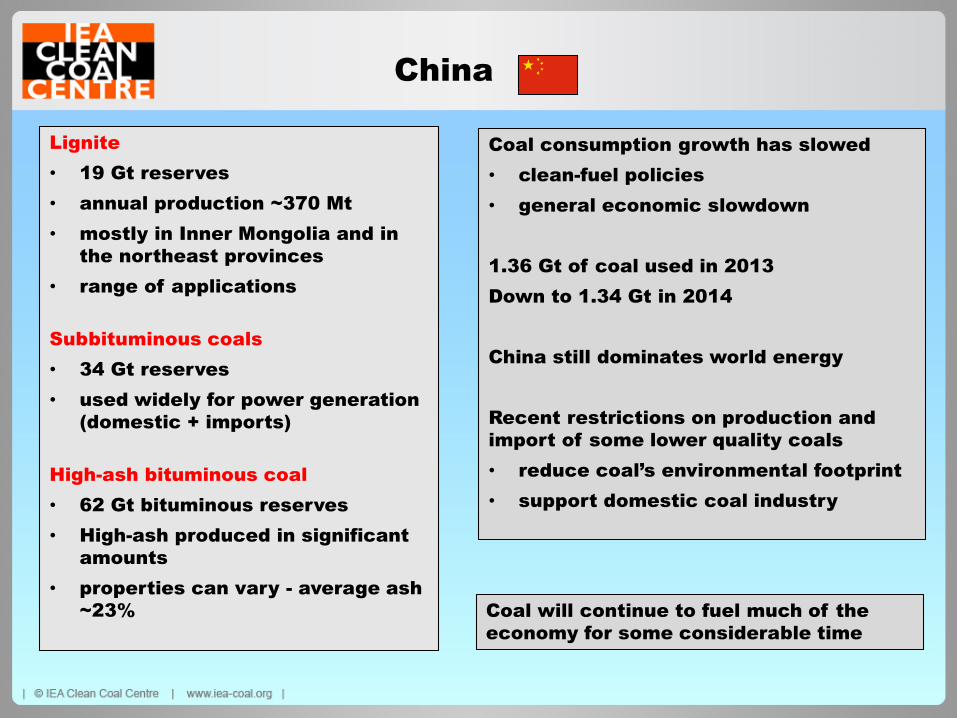

China

Lignite

• 19 Gt reserves

• annual production ~370 Mt

• mostly in Inner Mongolia and in

the northeast provinces

• range of applications

Subbituminous coals

• 34 Gt reserves

• used widely for power generation

(domestic + imports)

High-ash bituminous coal

• 62 Gt bituminous reserves

• High-ash produced in significant

amounts

• properties can vary - average ash

~23%

Coal consumption growth has slowed

• clean-fuel policies

• general economic slowdown

1.36 Gt of coal used in 2013

Down to 1.34 Gt in 2014

China still dominates world energy

Recent restrictions on production and

import of some lower quality coals

• reduce coal’s environmental footprint

• support domestic coal industry

Coal will continue to fuel much of the

economy for some considerable time

India

• world’s 3rd largest coal producer

• large deposits of bituminous coal + lignite

• coal resources of 213 Gt

• proven reserves of 87 Gt

• >70% of electricity from coal-fired plants

Indian coals

• high ash levels

• variable properties

• ash disposal

Coal quality has declined steadily

operational

challenges for

power plants

• increased use of renewables in the future

• some coal projects cancelled

• but 60 new coal mines planned

South Africa

High-ash bituminous coal

Provides more than three quarters of SA’s energy

Major coal consumers

Eskom

• 90 Mt/y of coal – 7th largest global generator

• generates 95% of SA’s electricity

• 90% from coal-fired stations

• building several new major stations

• but declining coal quality impacting on power plant

operations

Sasol

• largest global coal-to-liquids/chemicals producer

• 40 Mt/y coal

• a third of SA’s total liquid fuel production

Exports

• 25-30% of saleable coal is washed and exported

• Richard’s Bay - capacity of 91 Mt/y

• in 2015, exports increased by 5.7% to 75.4 Mt

• similar level expected for 2016

Future coal supply?

• previous decade saw sustained increase in

demand

• numerous new mining projects proposed

• global production could be increased significantly

• but many projects currently on hold

• future growth expected in some areas

• potential for significant global increase in output

• new resources often harder to access

- lack of transport infrastructure

- capital expenditure needed

- long payback time

- ongoing transport costs

Closing comments

• around half of the world’s estimated recoverable reserves comprise

coals of low quality/value

• mainly lignite, subbituminous and high-ash bituminous coals

• all used widely for power generation/cogeneration

• greater market acceptance in recent years

• may be only major energy resource available

• coal still important for baseload but increasingly flexible operation

often needed

• can be important backup for intermittent renewables

• a significant part of the global economy continues to rely on coal

• coal generates ~39% of the world’s electricity

• despite decline in some countries, overall, lower quality coals will retain

their importance for some considerable time

Contact details:

Dr Stephen Mills

IEA Clean Coal Centre, Park House, 14 Northfields,

London SW18 1DD, UK

email: [email protected]

Thank you for your attention