Looking for Shelter from the Storm - wiiw

25

Wiener Institut für Internationale Wirtschaftsvergleiche The Vienna Institute for International Economic Studies wiiw.ac.at Looking for Shelter from the Storm Richard Grieveson Mario Holzner Webinar, May 6 th 2020 New wiiw forecast for Central, East and Southeast Europe, 2020-2021

Transcript of Looking for Shelter from the Storm - wiiw

Wiener Institut für Internationale Wirtschaftsvergleiche

The Vienna Institute forInternational EconomicStudies

wiiw.ac.at

Looking for Shelter from the Storm

Richard Grieveson

Mario Holzner

Webinar, May 6th 2020

New wiiw forecast for Central, East and Southeast Europe, 2020-2021

Ó 2

1. Global overview and assumptions

2. New wiiw forecasts for Eastern Europe

3. Tracking COVID-19 cases and deaths in Eastern Europe

4. Initial economic impact

5. Areas of resilience and vulnerability

6. How this crisis will change Eastern Europe in the medium and long term

Overview

Ó 3

1. Global overview: Worst crisis since the 1930s

Ó 4Source: IMF April WEO.

Real GDP growth, %

Global overview: Worst crisis since the 1930s

-10

-8

-6

-4

-2

0

2

4

6

8

10

Austria Germany Italy US China

2009 2020 2021

Ó 5

2. New wiiw forecasts for CESEE

Ó 6Note: Current forecast and revisions relative to the wiiw Spring forecast 2020. Colour scale variation from the minimum (red) to the maximum (green). Source: wiiw forecast.

New wiiw real GDP forecasts and revisions

2019 2020 2021 2019 2020 2021

BG 3.4 -6.3 1.7 -0.1 -9.1 -0.6

CZ 2.6 -4.8 2.5 0.2 -7.0 0.1

EE 4.3 -7.0 4.0 0.4 -9.7 1.4

HR 2.9 -11.0 4.0 -0.1 -13.7 1.3

HU 4.9 -5.5 2.0 0.0 -8.8 -0.6

LT 3.9 -6.5 4.3 0.0 -9.3 1.7

LV 2.2 -8.0 4.5 0.0 -10.0 2.2

PL 4.1 -4.0 3.0 0.1 -7.6 -0.3

RO 4.1 -7.0 3.0 0.0 -10.2 0.2

SI 2.4 -9.5 4.0 -0.2 -12.1 1.3

SK 2.3 -9.0 4.6 0.0 -11.0 2.2

AL 2.2 -5.0 3.8 -0.4 -8.2 0.4

BA 2.6 -5.0 3.0 -0.1 -7.5 0.2

ME 3.6 -8.0 5.0 0.3 -10.8 2.1

MK 3.6 -5.0 4.0 0.2 -8.3 0.7

RS 4.2 -4.0 4.0 0.2 -7.7 0.5

XK 4.2 -4.4 4.0 0.1 -8.7 -0.2

Turkey TR 0.9 -6.0 5.5 0.4 -9.9 1.4

BY 1.2 -5.3 -0.7 0.0 -6.3 -2.0

KZ 4.5 -3.0 2.0 0.0 -6.7 -1.8

MD 3.6 -3.0 3.0 -1.0 -7.0 -1.0

RU 1.3 -7.0 1.5 0.0 -9.1 -0.8

UA 3.2 -6.0 2.5 -0.1 -9.6 -1.7

Forecast, % Revisions, pp

EU-CEE11

WB6

CIS4+UA

Ó 7

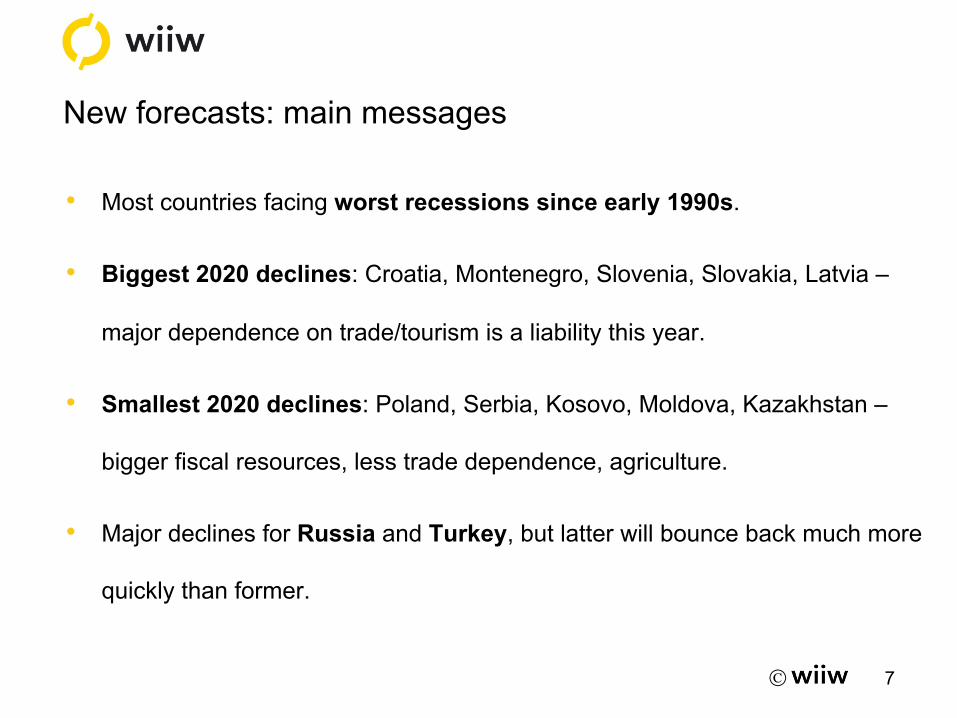

New forecasts: main messages

• Most countries facing worst recessions since early 1990s.

• Biggest 2020 declines: Croatia, Montenegro, Slovenia, Slovakia, Latvia –

major dependence on trade/tourism is a liability this year.

• Smallest 2020 declines: Poland, Serbia, Kosovo, Moldova, Kazakhstan –

bigger fiscal resources, less trade dependence, agriculture.

• Major declines for Russia and Turkey, but latter will bounce back much more

quickly than former.

Ó 8

3. Tracking cases and deaths in CESEE

Ó 9

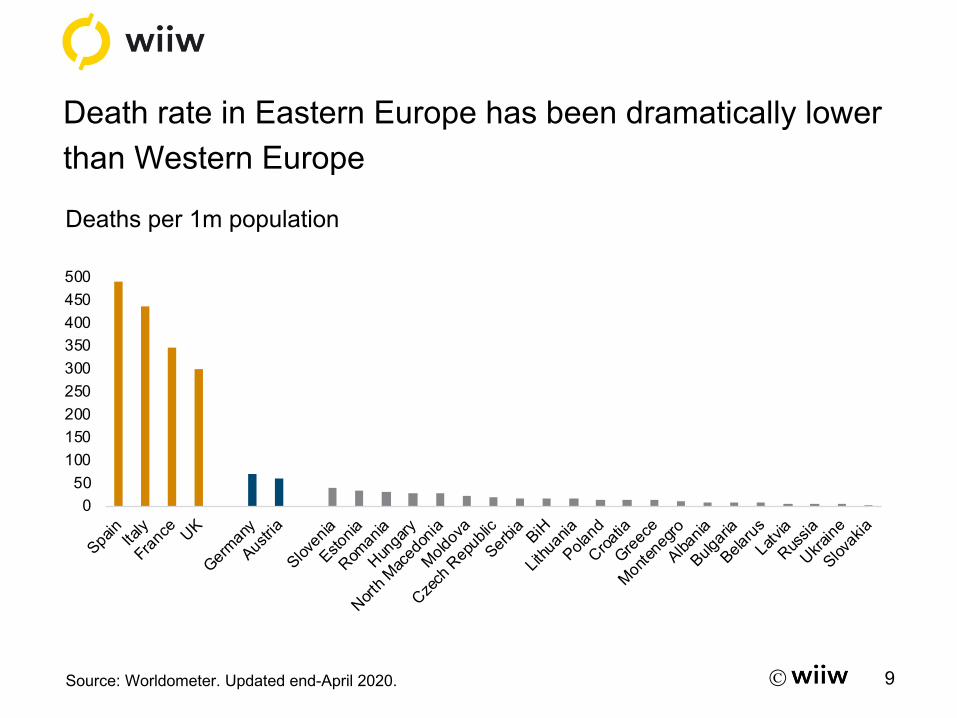

Death rate in Eastern Europe has been dramatically lower

than Western Europe

Source: Worldometer. Updated end-April 2020.

0

50

100

150

200

250

300

350

400

450

500

Spain

Italy

Fran

ce UK

Ger

man

y

Austri

a

Slove

nia

Eston

ia

Rom

ania

Hun

gary

Nor

th M

aced

onia

Moldo

va

Cze

ch R

epub

lic

Serbia

BiH

Lith

uania

Polan

d

Cro

atia

Gre

ece

Mon

tene

gro

Alban

ia

Bulga

ria

Belar

us

Latv

ia

Rus

sia

Ukr

aine

Slova

kia

Deaths per 1m population

Ó 10

Eastern European countries imposed major restrictions at a much lower level of confirmed cases

Source: Blavatnik School of Government, Oxford University.

Stringency index and number of confirmed cases, March 15th 2020

0

10

20

30

40

50

60

70

80

90

100

0 1000 2000 3000 4000 5000 6000

Strin

genc

y in

dex

Number of confirmed cases

Spain

FranceUS

UK

Albania and Kosovo

Poland

Bulgaria, Romania, Slovakia, Ukraine

Ó 11

4. Initial impact

Ó 12

Manufacturing PMIs at or close to all-time lows across Europe in April

Source: IHS Markit.

Manufacturing purchasing managers’ indices (PMIs); 50 = no change

0

5

10

15

20

25

30

35

40

45

50

Euro area CzechRepublic

Poland Turkey Kazakhstan Russia

March April

Ó 13

Lockdowns have had severe impact on normal economic life

Source: google. Average of data for grocery/pharmacy, retail/recreation and workplace activity

Google mobility data, change versus baseline (%), mid-April

-70

-60

-50

-40

-30

-20

-10

0

BY LV TR CZ HU EE LT SK PL MK MD HR SI BA BG KZ RO SE AT IT

Ó 14

5. Factors of resilience and vulnerability

Ó 15

5.a. Trade and tourism dependence leaves some countries particularly exposed to initial fallout

Sources: World Bank, national sources, wiiw.

Exposure to external trade, tourism and travel services

0

5

10

15

20

25

30

0 20 40 60 80 100 120 140 160 180 200

Trav

el a

nd to

uris

m, %

of G

DP

External trade, % of GDP

Least exposed

Most exposedAlbania Croatia Montenegro

Estonia

Slovenia

HungarySlovakia

RussiaKazakhstan

Turkey

Moldova

Romania Ukraine

Poland

Bosnia

Serbia

Ó 16

5.b. Fiscal space to react and room to recover differs widely across the region

Sources: Moody’s, Fitch, S&P. Average of available ratings.

Average credit rating; 1 (prime) to 7 (substantial risks)

0

1

2

3

4

5

6

7

Czech

Rep

ublic

Estonia

Latvi

a

Lithu

ania

Poland

Slovak

ia

Sloven

ia

Bulgari

a

Hunga

ry

Kazak

hstan

Roman

ia

Russia

Croatia

North M

aced

oniaSerb

ia

Turke

y

Albania

Belarus BiH

Moldov

a

Monten

egro

Ukraine

Sweden

Austria

Spain

Italy

Ó 17

5.c. Weak healthcare capacity required lockdowns at lower level of infections and could influence recovery

Source: World Bank. Data for 2016.

Public healthcare spending per capita, PPP, Austria = 100

0

10

20

30

40

50

60

Moldov

a

Ukraine

Kazak

hstan

Albania

North M

aced

onia

Serbia

Belarus

Russia BiH

Bulgari

a

Turke

yLa

tvia

Roman

ia

Poland

Hunga

ry

Lithu

ania

Croatia

Estonia

Slovak

ia

Sloven

ia

Czech

Rep

ublic

Ó 18

5.d. Reliance on capital flows a major area of exposure for much of Western Balkans, Moldova and Ukraine

Sources: World Bank, national sources, wiiw.

Selected capital inflows, % of GDP, average of last five available years

-10-505

101520253035

Sloven

ia

Russia

Hunga

ry

Estonia

Bulgari

a

Lithu

ania

Turke

y

Poland

Croatia

Kazak

hstan

Roman

iaLa

tvia

Belarus

Slovak

ia

North M

aced

onia

Czech

Rep

ublic

Ukraine

Serbia BiH

Albania

Kosov

o

Moldov

a

Monten

egro

Personal remittances received Net FDI inflows Net hot money inflows

Ó 19

6. First thoughts on the medium and long-term implications

Ó 20

1. Consumer caution could outlast acute phase of crisis.

2. Interest rates and inflation lower for longer.

3. Higher (and maybe more progressive) taxes.

4. A bigger role for the state in economic life.

5. Opportunities from near-shoring, services out-sourcing and digitalisation.

6. After a pause, labour shortages and automation will return.

7. Ever greater gulf within Eastern Europe.

8. China’s economic role in the region will remain important.

The next decade in Eastern Europe

Ó 21

• Worst year for global economy since 1930s.

• Many CESEE countries face worst recession since early 1990s.

• Short-term: those with major trade and tourism exposure will suffer most.

• But advantages for those with better healthcare and bigger fiscal capacity.

• Many will face difficulties with sharp reduction in capital flows, and are going

to need outside help.

• Longer-term: A lot of things are going to change.

• Negative: Consumer caution, higher debt, non-EU falling further

behind.

• Positive: Near-shoring, outsourcing of services, digitalisation, further

automation.

Conclusions

Ó 22

Wiener Institut für Internationale Wirtschaftsvergleiche

The Vienna Institute forInternational EconomicStudies

www.wiiw.ac.at

Thank you for your attention!

Follow us:www.wiiw.ac.at

Ó 23

Country codes

AL Albania KZ Kazakhstan RS Serbia

BY Belarus LT Lithuania RU Russia

BA Bosnia and Herzegovina LV Latvia SI Slovenia

BG Bulgaria MD Moldova SK Slovakia

CZ Czech Republic ME Montenegro TR Turkey

EE Estonia MK North Macedonia UA Ukraine

HR Croatia PL Poland XK Kosovo

HU Hungary RO Romania

CESEE23 Central, East and Southeast Europe

CIS4+UA Commonwealth of Independent States-4 and Ukraine

EA19 Euro area

EU-CEE11 European Union – Central and Eastern Europe

WB6 Western Balkans

Ó 24

Wiener Institut für Internationale Wirtschaftsvergleiche

The Vienna Institute forInternational EconomicStudies

www.wiiw.ac.at

Extra slides

Ó 25Source: IMF April WEO.

• Second/third wave

• Delayed vaccine

• Limits on US response after election

• Greater international tensions

• Bad policy decisions in major economies

• Social unrest in systemically important country/countries

• Food shortages and sharp increase in prices

• New euro area crisis centred on Italy

Negative scenario