Long-Lasting Insecticide-treated Bednet Supplier ... GF Sub Sahara LLIN ... India Royal Sentry...

55

Long-Lasting Insecticide-treated Bednet Supplier Conference - Geneva - 13 May 2013 AGENDA Time Title and Objectives 8.30-9.00 Welcome Coffee and Registration 9.00-9.45 Introduction, Objectives and Agenda: Alan Court, Special Advisor, UN Special Envoy Office 9.45-10.15 Welcoming remarks: Christopher Game, Chief Procurement Officer Keynote Speech: Dr. Mark Dybul, Executive Director 10.15-10.45 Coffee break 10.45-12.30 Setting the Scene: Global Fund: Where we are today and our new approach to supplier management - Christopher Game / Mariatou Tala Jallow PMI: Approach to procurement and Challenges – Megan Fotheringham, Public Health Adviser UNICEF: Approach to procurement and challenges – Elena Trajkovska, Contracts Specialist IVCC: Barriers to innovation – Dr. Tom McLean, Chief Operating Officer RX360: Overview and Structure-Lynn Byers VP GSK RBM HWG/ALMA: LLINs in Africa – Melanie Renshaw, Chief Technical Officer (ALMA), RBM HWG Co-Chair 12.30-13.30 Lunch 13.30-14.30 The New Approach in the context of LLIN and the implications for suppliers – Christopher Game Q&A 14.30-1600 The Supplier Perspective: Group Discussion and Plenary Presentation 1. What worked well and not so well under the previous arrangements? 2. What are the key get rights for the Global Fund and partner agencies to make this work? 1600-1645 Executive Forum with Buyers Q&A 16.45-17.00 A re-cap on the day and next steps

Transcript of Long-Lasting Insecticide-treated Bednet Supplier ... GF Sub Sahara LLIN ... India Royal Sentry...

Long-Lasting Insecticide-treated Bednet Supplier Conference - Geneva - 13 May 2013

AGENDA

Time Title and Objectives

8.30-9.00 Welcome Coffee and Registration

9.00-9.45 Introduction, Objectives and Agenda: Alan Court, Special Advisor, UN Special Envoy Office

9.45-10.15 Welcoming remarks: Christopher Game, Chief Procurement Officer Keynote Speech: Dr. Mark Dybul, Executive Director

10.15-10.45 Coffee break

10.45-12.30 Setting the Scene: Global Fund: Where we are today and our new approach to supplier management - Christopher Game / Mariatou Tala Jallow PMI: Approach to procurement and Challenges – Megan Fotheringham, Public Health Adviser UNICEF: Approach to procurement and challenges – Elena Trajkovska, Contracts Specialist IVCC: Barriers to innovation – Dr. Tom McLean, Chief Operating Officer RX360: Overview and Structure-Lynn Byers VP GSK RBM HWG/ALMA: LLINs in Africa – Melanie Renshaw, Chief Technical Officer (ALMA), RBM HWG Co-Chair

12.30-13.30 Lunch

13.30-14.30 The New Approach in the context of LLIN and the implications for suppliers – Christopher Game Q&A

14.30-1600 The Supplier Perspective: Group Discussion and Plenary Presentation 1. What worked well and not so well under the previous arrangements? 2. What are the key get rights for the Global Fund and partner agencies to make this work?

1600-1645 Executive Forum with Buyers Q&A

16.45-17.00 A re-cap on the day and next steps

The Global Fund

LLIN Supplier Conference

Geneva Monday 13th May 2013

1

2

Introduction, Objectives and Agenda

Alan Court, Special Advisor, UN Special Envoy Office

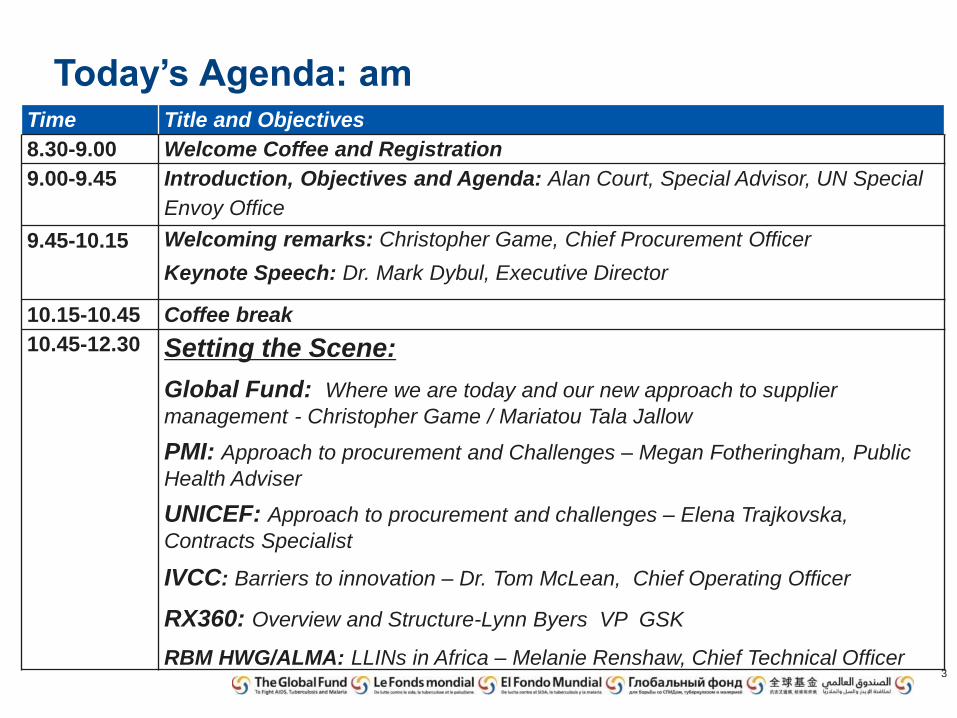

Today’s Agenda: am

3

Time Title and Objectives

8.30-9.00 Welcome Coffee and Registration

9.00-9.45 Introduction, Objectives and Agenda: Alan Court, Special Advisor, UN Special

Envoy Office

9.45-10.15 Welcoming remarks: Christopher Game, Chief Procurement Officer

Keynote Speech: Dr. Mark Dybul, Executive Director

10.15-10.45 Coffee break

10.45-12.30 Setting the Scene:

Global Fund: Where we are today and our new approach to supplier

management - Christopher Game / Mariatou Tala Jallow

PMI: Approach to procurement and Challenges – Megan Fotheringham, Public

Health Adviser

UNICEF: Approach to procurement and challenges – Elena Trajkovska,

Contracts Specialist

IVCC: Barriers to innovation – Dr. Tom McLean, Chief Operating Officer

RX360: Overview and Structure-Lynn Byers VP GSK

RBM HWG/ALMA: LLINs in Africa – Melanie Renshaw, Chief Technical Officer

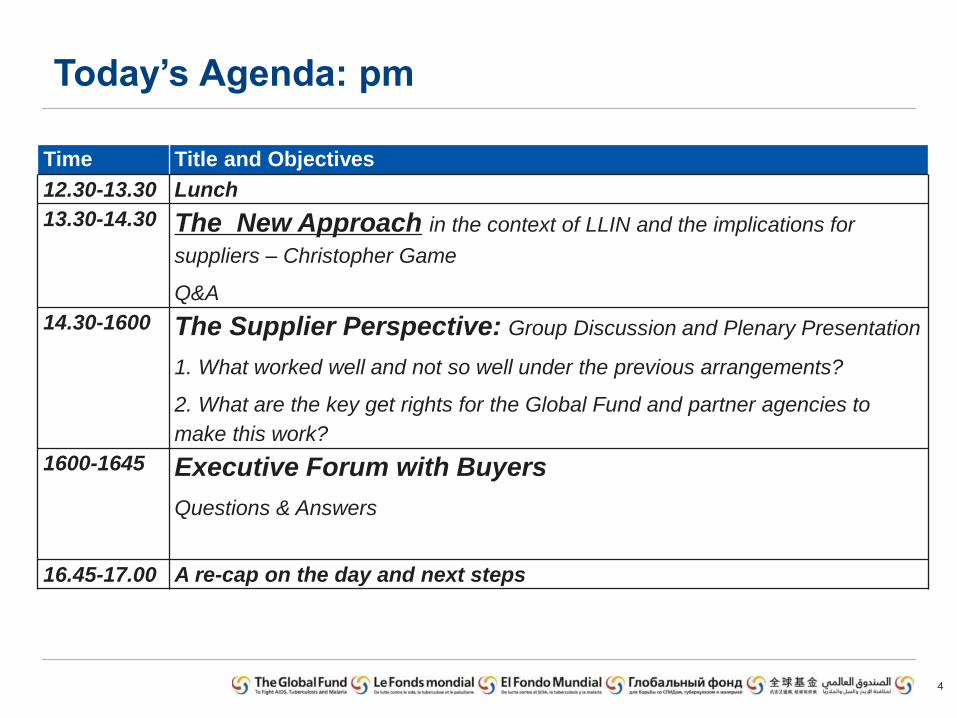

Today’s Agenda: pm

4

Time Title and Objectives

12.30-13.30 Lunch

13.30-14.30 The New Approach in the context of LLIN and the implications for

suppliers – Christopher Game

Q&A

14.30-1600 The Supplier Perspective: Group Discussion and Plenary Presentation

1. What worked well and not so well under the previous arrangements?

2. What are the key get rights for the Global Fund and partner agencies to

make this work?

1600-1645 Executive Forum with Buyers

Questions & Answers

16.45-17.00 A re-cap on the day and next steps

5

Welcome: Christopher Game, Chief Procurement Officer

Introduction

A reminder of what Malaria means

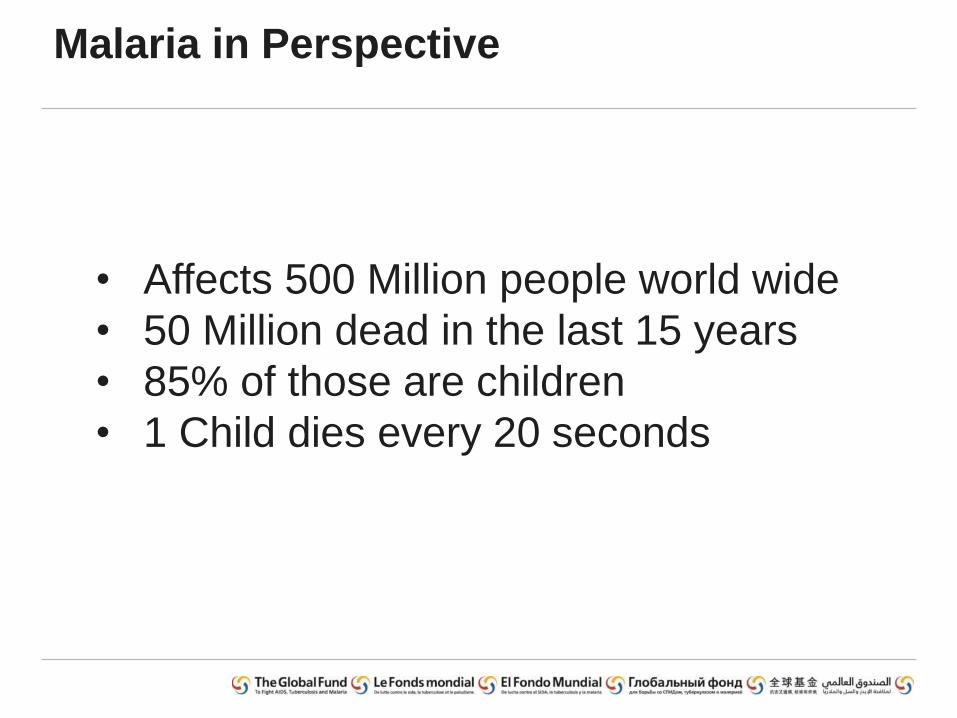

Malaria in Perspective

In Countries where Malaria is prevalent

average life span can be as low as 30

Malaria in Perspective

Malaria has shaped Africa in terms of

Colonization - Independence then shaped

Malaria

Malaria in Perspective

Five times more men have been lost to

Malaria than in any battle

Malaria in Perspective

• Affects 500 Million people world wide

• 50 Million dead in the last 15 years

• 85% of those are children

• 1 Child dies every 20 seconds

Malaria in Perspective

And now a personal

experience :

For those of you who have read Great

Expectations by Charles Dickens,

these are Pip’s graves. Dickens lived

at Shorne, near to this Church in

Cooling, Kent half an hour from

London in the United Kingdom.

These graves are in fact those of the

Comport Children, none is more than a

meter long, and if memory serves me

correctly there are 11 or 12 of them.

They died of Malaria, not far from one

of the worlds great cities.

200 years ago.

13

Keynote Address: Dr Mark Dybul, Executive Director

14

Investing for Impact and The Global Fund Strategy

Procurement for Impact P4I

LLIN Procurement Facts and Figures

The Global Fund: Where

we are today and our new

approach to supplier

management

Christopher Game

Mariatou Tala Jallow

A historical perspective

15

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

Total GF Sub Sahara LLIN Deliveries by year

2004 -2010 saw a dramatic increase in the in the supply of LLIN

before a subsequent sharp decline

Looking Forward

16

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

2010 2011 2012 2013 2014

GF LLIN Actual and Forecast orders against estimated requirement

A gap existed between the number required to maintain coverage

and the planned volumes. This was leading to short lead time

orders

Estimated number to maintain coverage (UNICEF)

GF forecast volume

Currently unplanned

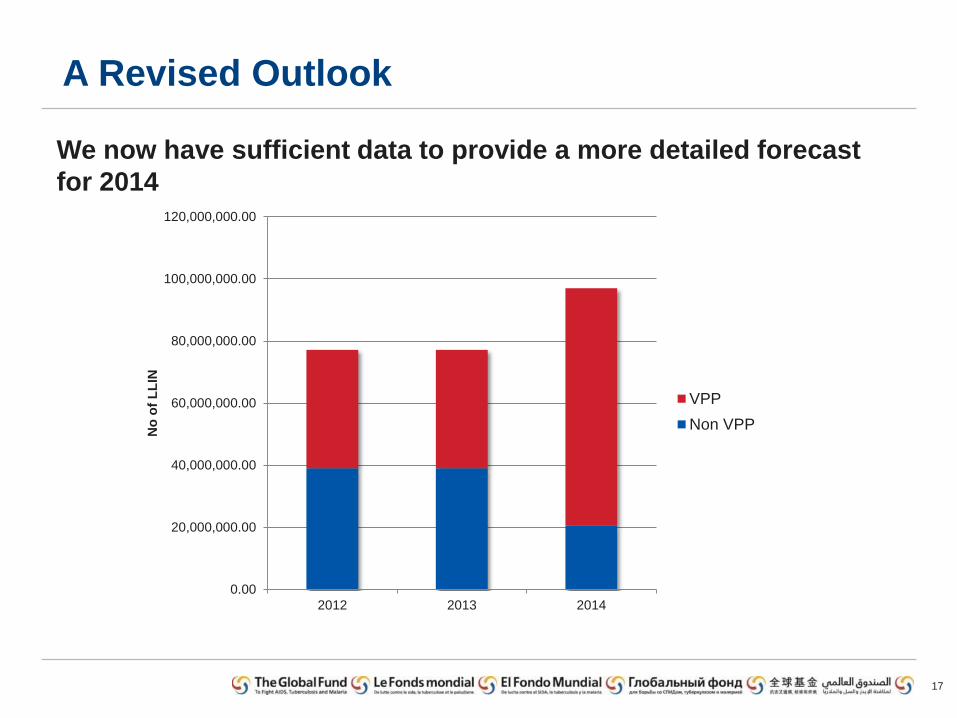

A Revised Outlook

17

We now have sufficient data to provide a more detailed forecast

for 2014

0.00

20,000,000.00

40,000,000.00

60,000,000.00

80,000,000.00

100,000,000.00

120,000,000.00

2012 2013 2014

No

of

LL

IN

VPP

Non VPP

WHOPES approved suppliers

18

Company Product Name

Material BASF, Switzerland Interceptor

Polyester Bayer (PTY) Ltd, South Africa LifeNet

Polypropylene Bestnet (Insect Intelligence ,

Denmark Netprotect

Polyethylene Disease Control Technologies,

India Royal Sentry

Polyethylene Net Health Ltd, Tanzania Olyset Plus

Polyethylene Shobikaa Impex Pvt Ltd, India Duranet

Polyethylene Sumitomo Chemical Co. Ltd,

Japan Olyset

Polyethylene Tana Netting (NRS), Dubai DawaPlus 2.0

Polyester Tinajin Yorkool International

Trading Co. Ltd, China Yorkool LN

Polyster Vestergaard Frandsen,

Switzerland PermaNet 2.0 Polyester

PermaNet 2.5 Polyester

PermaNet 3.0 Polyester

Polyester / polyethylene VKA Polymers Pvt Ltd, MAGNet

Polyethylene

Supplier Name Product

Kuse Lace Co, Japan Aka Net

A to Z Textile,

Tanzania

MiraNet

Life Ideas Textiles,

China

PandaNet 1.0

PandaNet 2.0

Fujian Yamein

Industries, China

Yahe LN

There are 11 approved suppliers and 5 more products currently

going through the approval process

Price Analysis

19

Prices have dropped 45% since Q3 2009 caused by factors

including excess capacity and the new ‘generic’ suppliers

Further pricing analysis

20

A snapshot analysis has revealed the

following key statistics:

1. In 2012 VPP LLIN agency fees were 2.4%

and freight 5% of total spend.

2. There are large variations in price driven by,

specification, order size, country of

manufacture.

3. In 2012 the largest like for like variation in

cost was 29%

4. VPP purchased nets were on average 13%

cheaper than those purchased directly by

PR during 2011.

Market Capacity and Forecast Demand

21

Market Capacity 175m-200m

(excludes potential new entrants)

Market demand 90m-160m

Current excess capacity is not dramatic if replenishment levels

are attained , this is evidenced by new entrants. It is anticipated

GF will provide half the market demand.

Some graphics courtesy of PRESENTATIONPRO

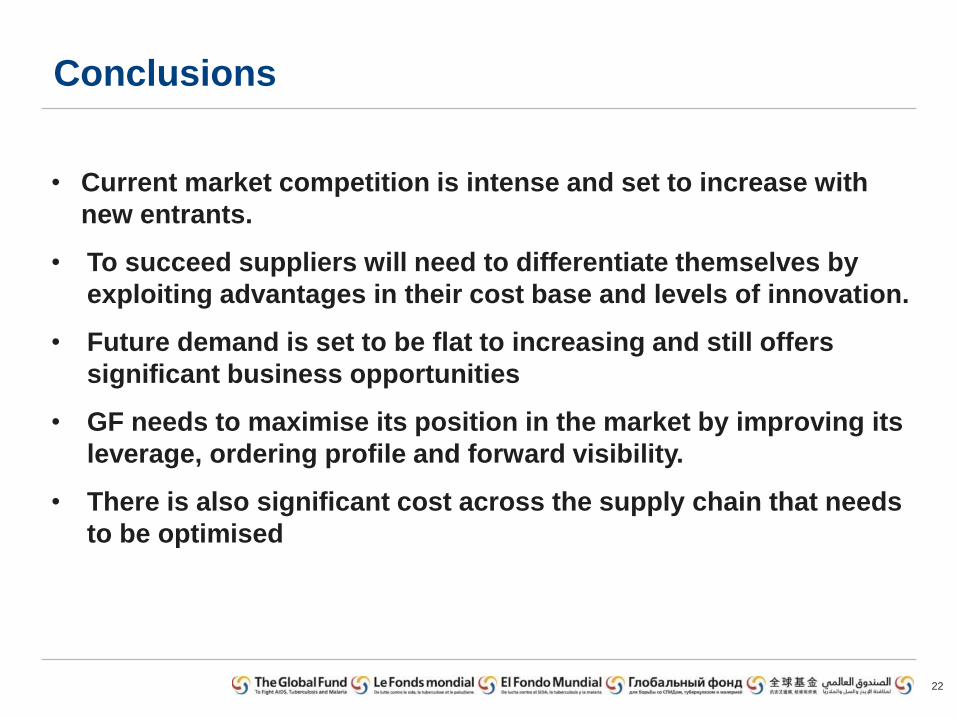

Conclusions

22

• Current market competition is intense and set to increase with

new entrants.

• To succeed suppliers will need to differentiate themselves by

exploiting advantages in their cost base and levels of innovation.

• Future demand is set to be flat to increasing and still offers

significant business opportunities

• GF needs to maximise its position in the market by improving its

leverage, ordering profile and forward visibility.

• There is also significant cost across the supply chain that needs

to be optimised

23

Investing for Impact and The Global Fund Strategy

Procurement for Impact P4I

LLIN Procurement Facts and Figures

The fight goes on

24

2000 2010-12

Metric 2000 Latest

Sub –Saharan

ARV therapy 50,000 6milion

4.5 million treatments

TB Case

Detection 43% 67%

TB Treatment

Success 67% 87%

9.7 million treatments

LLIN

Ownership 5% 53%

310m nets provided

Progress However

2012

HIV/AIDS TB Deaths

2,700,000

Malaria Deaths (2010)

600,000

2014-16

Future Funding required and targeted

in period

HIV/

AIDS

$58bn

TB

$15bn

Malaria

$14bn

Other

$61bn

TGF

$15bn

$87m $76m

Maximising the value from procurement will contribute to the

number of lives saved

Investing for Impact

25

The Global Fund Strategy 1.

26

Strategic Objectives

1. Invest more

strategically

2. Evolve the

funding model

3. Actively support

grant implementation

process

Str

ate

gic

Acti

on

s

1.1 Focus on the highest

impact countries interventions

and populations while keeping

the fund global

1.2 Fund based on quality

national strategies and

through national systems

1.3 Maximise the impact of the

Global Fund investments on

strengthening health systems

1.4 Maximise the impact of

Global Fund investments on

improving the health of

mothers and children

2.1 Replace the rounds

system with a more

flexible and effective model

• Iterative, dialogue

based system

• Early preparation of

implementation

• More flexible,

predictable funding

opportunities

2.2 Facilitate the strategic

refocusing of existing

investments

3.1 Actively manage grants

based on impact, value for

money and risk

3.2 Enhance the quality and

efficiency of grant

implementation

3.3 Make partnerships work

to improve grant

implementation.

27

Strategic Objectives

4. Promote and protect human

rights

5. Sustain the gains, mobilise

resources

4.1 Ensure that the Global Fund does not

support programs that infringe human rights

4.2 Increase investments in programs that

address human rights related barriers to

access

4.3 Integrate human rights considerations

throughout the grant cycle.

5.1 Increase the sustainability of Global

Fund supported programs

5.2 Attract additional funding from current

and new sources

Strategic

Enablers Enhance partnerships to deliver results

Transform to improve Global Fund governance, operations

and fiduciary controls

The Global Fund Strategy 2.

28

Investing for Impact and The Global Fund Strategy

Procurement for Impact P4I

LLIN Background and Challenge

The P4i Vision

29

The Global Fund will become the benchmark organisation in the sector for Sourcing and Procurement

Minimising waste and eliminating non value adding

activities

Using simple, clear leading edge processes and tools

designed by and for the organisation

Ensuring effective governance and watertight compliance

With measurable performance

in value and lives saved

Building collaborative relationships with partner agencies suppliers and donors

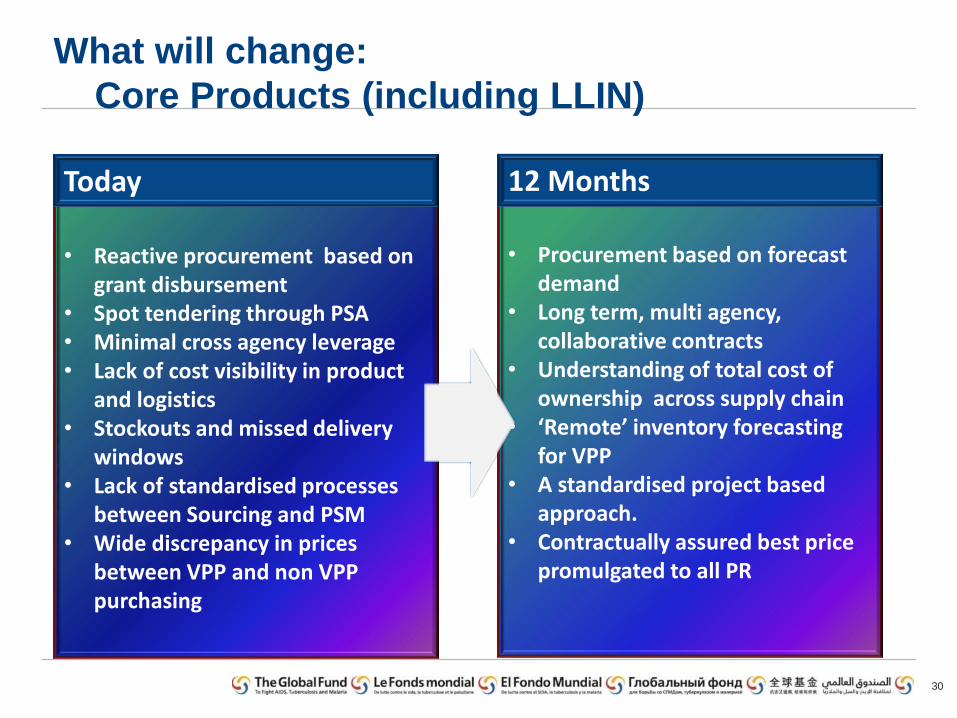

Is directly aligned to the Global Funds objectives

• Procurement based on forecast

demand • Long term, multi agency,

collaborative contracts • Understanding of total cost of

ownership across supply chain • ‘Remote’ inventory forecasting

for VPP • A standardised project based

approach. • Contractually assured best price

promulgated to all PR

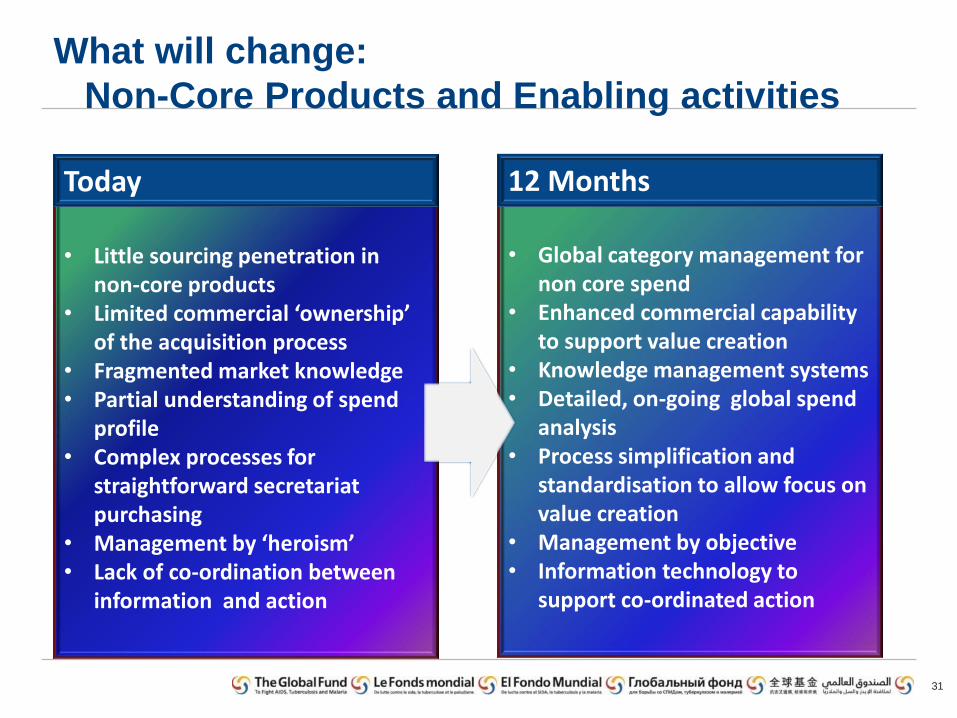

What will change:

Core Products (including LLIN)

30

• Reactive procurement based on

grant disbursement • Spot tendering through PSA • Minimal cross agency leverage • Lack of cost visibility in product

and logistics • Stockouts and missed delivery

windows • Lack of standardised processes

between Sourcing and PSM • Wide discrepancy in prices

between VPP and non VPP purchasing

Today 12 Months

• Global category management for

non core spend • Enhanced commercial capability

to support value creation • Knowledge management systems • Detailed, on-going global spend

analysis • Process simplification and

standardisation to allow focus on value creation

• Management by objective • Information technology to

support co-ordinated action

What will change:

Non-Core Products and Enabling activities

31

• Little sourcing penetration in

non-core products • Limited commercial ‘ownership’

of the acquisition process • Fragmented market knowledge • Partial understanding of spend

profile • Complex processes for

straightforward secretariat purchasing

• Management by ‘heroism’ • Lack of co-ordination between

information and action

•

Today 12 Months

Achieving the Vision

32

Our objective: To Increase Access to Products

By fundamentally changing the way we work across the supply chain

Earlier involvement and closer

collaboration with

manufacturers

Improving our purchasing

capability and changing our contracting

models

Optimising the international supply chain

to reduce cost

Better planning and

scheduling to support

continuity of supply

Delivering more products at the right time and place to more

people

The Impact on the Ground

33

Multi agency demand

is combined to develop

long term forecasts

supported by the new

funding model

GF will negotiate direct

with manufacturers

offering longer term

contracts in return for

open book best pricing

GF wants open

collaborative supplier

relationships to drive

innovation and reduce

cost.

Operational

procurement will be

shared between direct

relationships with

logistics providers and

PSA.

PR will have access to

best pricing and able to

order core and non-

core items to fulfil

their requirements

The process will be

supported by improved

knowledge

management,

benchmarking and

technology to provide

improved purchasing

support for PRs.

Internal processes will

be improved to support

capability development

and maintain continuity

of supply

Improved Access to Products

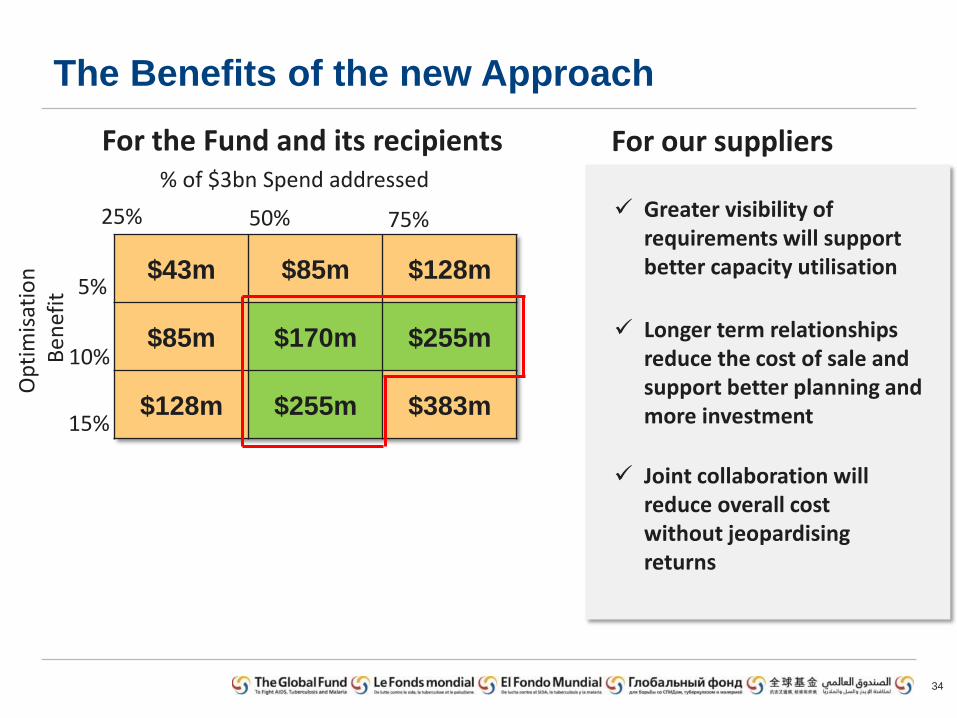

The Benefits of the new Approach

34

$43m $85m $128m

$85m $170m $255m

$128m $255m $383m

25% 50% 75%

5%

10%

15%

% of $3bn Spend addressed

Op

tim

isat

ion

B

en

efit

For the Fund and its recipients For our suppliers

Greater visibility of requirements will support better capacity utilisation

Longer term relationships reduce the cost of sale and support better planning and more investment

Joint collaboration will reduce overall cost without jeopardising returns

What does this mean for our Suppliers?

35

We want a new style of relationship that moves away from

price centric spot tendering

We are prepared to enter into longer term contracts with

forecast volumes that will allow you to run your

businesses more effectively.

In return we will require a more open and collaborative

style which means working with us in a straightforward,

honest fashion.

We will adjust our level of business with you dependent

on your performance with us and our buying partners.

This afternoon we will share with you how we intend to

achieve these aims in our LLIN procurement

Zero tolerance of non compliance with Global Fund

policies

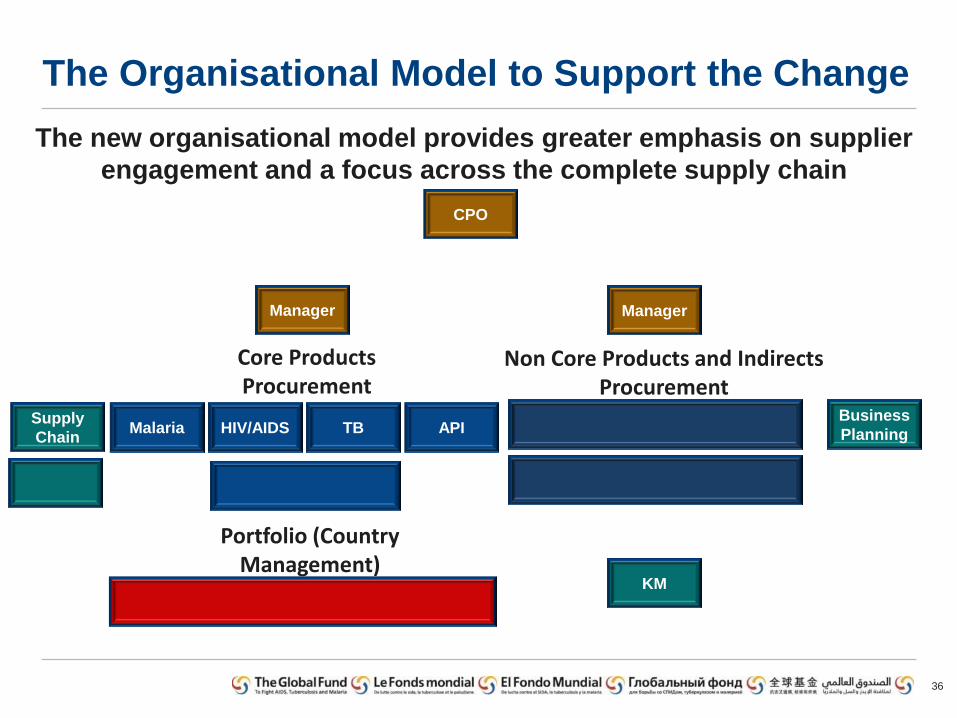

The Organisational Model to Support the Change

36

Malaria HIV/AIDS TB API

KM

Business

Planning Supply

Chain

Manager Manager

Core Products Procurement

Non Core Products and Indirects Procurement

Portfolio (Country Management)

CPO

The new organisational model provides greater emphasis on supplier

engagement and a focus across the complete supply chain

37

The New Approach

in The Context of

LLIN

Christopher Game

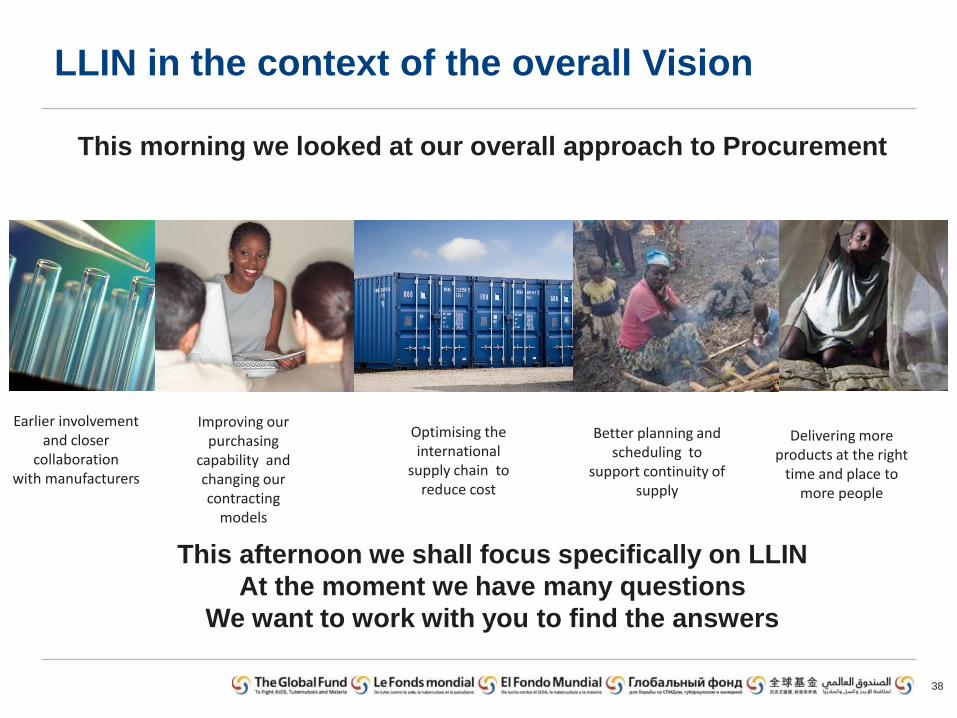

LLIN in the context of the overall Vision

38

Earlier involvement and closer

collaboration with manufacturers

Improving our purchasing

capability and changing our contracting

models

Optimising the international

supply chain to reduce cost

Better planning and scheduling to

support continuity of supply

Delivering more products at the right

time and place to more people

This morning we looked at our overall approach to Procurement

This afternoon we shall focus specifically on LLIN

At the moment we have many questions

We want to work with you to find the answers

Our Focus

39

This is about increasing access to products through a direct

relationship, reduced cost and supply chain optimisation.

We acknowledge businesses need to make a return

• Maintain business continuity

• Re-investment

If your return is reasonable we will be prepared to protect it and even

incentivise you based on performance against our key objectives

Production

Inbound Freight

Raw Materials

Distribution

Margin

• Total cost of • Ownership • Continuity of supply • Quality

Market dynamics (Commodity

prices)

Market sustainability

Labour arbitrage

Specification and product life

Order profiling

Payment mechanisms

Supply chain structure Quality and Lead times

Our focus

40

1. To create value for the Global Fund in LLIN through improved sourcing and

greater understanding of the market.

2. To develop a new supply chain model incorporating direct vendor management, an

updated approach to pooled procurement and improved delivery to recipients.

3. To develop new processes including forecasting to improve net availability in line

with country programmes

4. To move towards standardisation of specifications to simplify procurement

5. To reduce the risk associated with the LLIN supply chain

6. To engage with other agencies and suppliers to drive innovation and

collaboration

7. Where appropriate to encourage local manufacturing to WHO standards without de-

stabilising the market.

Objectives of LLIN Project

41

Project Structure

LLIN forms a pilot for our new ways of working and we have put

together a project team who will work with you to deliver our

objectives.

We are aligning with partners

Planning and Forecasting

42

TGF provides a 12 month master schedule for overall capacity required. Updated quarterly

Master schedule is turned into detailed forecast by product type. Blanket orders are placed by TGF for core products

Call off orders are placed 2014 VPP, thereafter all.

Fixed

Call off orders (M) M-3

months M-6

months

+/-

10%

Master Schedule Detailed Plan

Manufacturing starts earlier

with volumes underwritten by TGF.

Payment structures adjusted

We propose a new scheduling and ordering process to optimise

capacities combined with an earlier payment mechanism. (All figures and dates illustrative)

We want your input to help design the solution

Plans will be mapped to the rainy

seasons

+/-

30%

Improving our forecasting accuracy

43

To support our new planning process we will change the way we

interact with our primary recipients. This approach will also be

facilitated by the new funding proposals

Today The Future

Demands are triggered by

PSM plans which are

presented in an

inconsistent format.

Overall demand is

calculated reactively by

hand

Orders are placed on PSA

for onward transmission to

manufacturers

Overall demand will be

calculated from available

funding

This demand will be placed

on manufacturers as an

underwritten volume

Detailed PR requirements

will be presented in a

consistent format

We will use a planning tool

to convert our forecast in

to specific orders by type

44

Element Approach Typical Questions

Managing the Physical Supply Chain

We want to work with you to examine each element of the supply

chain to see how we can make improvements.

Wh

at is

the m

ost e

ffectiv

e w

ay to

dep

loy P

SA

in V

PP

to s

up

po

rt t ou

r ob

jectiv

es

Specifications and Quality

45

• Specification

Work has started on the standardising specifications and this will

continue. we want your input and ideas and engagement with

WHOPES to maintain the momentum.

• Quality

To date the focus has been on third party quality control (checking

the products are of the required quality). We now want to include other

elements of quality assurance.

The Commercial Relationship

46

To ensure we maintain a competitive price in a longer term

contractual framework we will need to change our commercial

model.

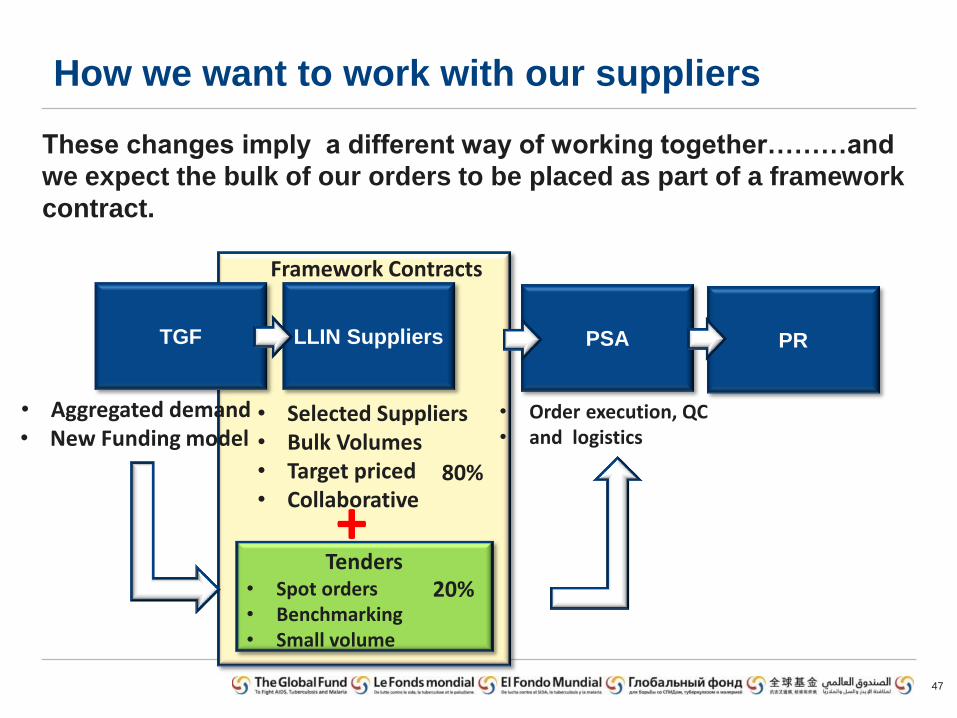

How we want to work with our suppliers

47

These changes imply a different way of working together………and

we expect the bulk of our orders to be placed as part of a framework

contract.

TGF LLIN Suppliers PSA PR

Framework Contracts

• Selected Suppliers • Bulk Volumes • Target priced • Collaborative

• Order execution, QC • and logistics

• Aggregated demand • New Funding model

Tenders • Spot orders • Benchmarking • Small volume

+ 80%

20%

The Implications for our Suppliers

48

1

2

3

4

5

A Closer, more strategic relationship

With appropriate governance and regular reviews. 1

Longer term contracts

supported by increased focus on planning and

scheduling

Collaboration to drive continuous improvement

Joint teams working together to achieve specific

objectives

Our Commitment

We are committed to this way forward and will

ensure our people have the right skills and

attitude to make it work.

A fair return

Based on market norms and with the opportunity for

incentivisation.

Apr May Jun Jul Aug Sep Oct Nov Dec

The Proposed Timeline

49

Initial

Concept

Co-plan

with

UNICEF

PSA

Alignment

Supplier Conference

Supplier

Feedback

Supplier Engagement and selection

Finalise design and then build

Contracting

Potential joint RFP

Design finalisation Go live

Note 1

Note 1: the joint RFP will represent a move in our direction of travel but may not incorporate all the end state requirements

Next Steps

50

We have shared our thoughts with you

Now we would like your feedback

This afternoon we would request your thoughts in open

forum

Tomorrow we will meet individually to decide the way

forward.

51

Supplier Feedback

Session

Looking Back: What went well

52

• Competition…but the equivalence process made the competition not level

• Transparency in the tendering process

• Circulation of the bid opening report gave opportunity to become more

competitive. Supplier had opportunity to correct mistake and change price

on any new or unused capacity

• Fair and relatively transparent process through VPP

• Reducing timeframe and ensuring shorter procurement order process

• VPP reduces risk exposure in comparison to local tenders

• Establishing the volume created the market and brought down prices

• A pool of suppliers brought down the price but no innovation followed

• Created market and opportunities

• Visibility of orders and money from VPP

• Created need for harmonisation

• VPP reduces corruption

• Some kind of centralised and harmonised system

• Price reductions through economies of scale

Looking Back: What went not so well…

53

• Speed of disbursement , lack of demand pooling and forecast

• VPP not voluntary

• Non commodity cost gaps not covered through funding

• VPP not smooth payments

• Lots of short lead time orders

• Unclear and undefined objectives for innovation, no incentive for innovation

• Non standard processes

• VPP not exactly voluntary

• Delays in funding owing to risk averse environment

• Disconnect with country expectation for lead times

• No pool effect

• Too long a lead time from grant signature to contract

• No technical evaluation of proposals

• Lack of visibility of production capacity

• Product quality and poor technical specification

• Poor issue resolution

• Violation of the normative space

• Time wastage through cancellations, changes of specs etc

• Payment terms

Key “get rights” going forward

54

• Better planning and forecasting

• Set up quality assurance mechanisms building national capacity

• Set up mechanism to review country generated procurement decisions

• Need to involve end users

• Work with existing solutions, don’t invent all the solutions

• Criteria for selection for LTA

• Value not cost

• Be transparent about processes

• Identify best possible proxies for GF in country presence

• Resolve PSM bottlenecks

• Have adequate in house procurement capability

• Categorise products based on quality and durability

• Respect normative space and IP

• Guidance on non-value of post shipment inspection

• Make sure PRs understand implications of new model

• Steady money flow

• Commitment

• Responsiveness to PRs and manufacturers

• Do not lose sight of country preferences