London Sumatra Plantation - PhillipCapital

20

Page | 1 | PHILLIP SECURITIES INDONESIA MCI (P) 019/11/2014_0013 Ref. No.: INDO2014_0017 London Sumatra Plantation (LSIP ID) Planting Through Tough Period INDONESIA | AGRICULTURE | INITIATION 18 December 2014 Company Background PT. PP London Sumatra Indonesia Tbk. (Lonsum) is one of the largest Indonesian-based plantation companies. It engages in plant breeding, planting, harvesting, processing, and selling of palm products, rubber, cocoa, and tea. The company owns a sizeable land bank, having over 100,000 ha planted nucleus area in North Sumatra, South Sumatra, Java, East Kalimantan, North Sulawesi, and South Sulawesi producing approximately 195,000 tons of Certified Sustainable Palm Oil (CSPO) per year. With relatively young age profile and ISO 14001 certification across all estates, all crop sectors, and all factories, bulking stations and research stations to support its growth potential going forward. Investment Merits One of the largest CPO players in Indonesia with 90,707 hectares planted oil palm area and is expected to produce 456,000 tons of Crude Palm Oil (CPO) in 2014. Young palm trees age profile averaging at 12.8 years to support its high quality FFB production. Maintain healthy financial position with cash and cash equivalent amounting to IDR 1.3 trillion sitting on its balance sheet. These sizeable cash reserves will provide a great opportunity for Lonsum to expand and grow its business portfolio. Best palm kernel extractor with 5.5 percent kernel extraction rate while industry average only stood at 4.7 percent. High quality FFB processed also contributed to an above-average palm oil extraction rate of 22.9 percent per ton. Highly efficient plantation company generated net profit of IDR 10.27 million per hectares in 2013, higher than the industry average of only IDR 8.45 million per hectares. Zero-debt Company as an indication of its resilience during severe commodities price volatility and reduce its exposure to interest rate risk as they are insulated from any rise in borrowing costs. Furthermore, Lonsum is in a better shape as there is no cash outflow on interest payments and hence, able to keep its costs to a minimum. Key Risk Factors High volatility in CPO prices has been our main concern for plantation companies. As a pure upstream producer, Lonsum’s financial performance is highly dependent to the volatility in its commodities selling prices. Both CPO and rubber have gone through a tough year and lack of positive catalyst to the commodities prices next year will cast a shadow on the share price. Accumulate CMP IDR 1,885 TARGET IDR 2,040 (+8.2%) COMPANY DATA O/S SHARES (MN) : 6,822.9 MARKET CAP (IDR BN) : 12,861.1 MARKET CAP (USDMN) : 1,013.3 52 - WK HI/LO (IDR) : 2,480 / 1,470 LIQUIDITY 3M (USDMN) : 22 PAR VALUE (IDR) : 100 MAJOR SHAREHOLDERS, % SALIM IVOMAS PRATAMA Tbk 59.51 PUBLIC 40.49 PRICE VS. JCI 80 90 100 110 120 130 140 Nov-13 Mar-14 Jul-14 Nov-14 LSIP IJ JCI Rebased Source: Phillip Securities Indonesia Research KEY FINANCIALS IDR bn FY14 FY15 FY16F FY17F Net Sales 4,651 5,087 5,598 6,076 EBIDTA 1,468 1,647 1,966 2,174 Net Profit 842 975 1,186 1,306 EPS, IDR 123 143 174 192 PER, x 15.27 13.18 10.84 9.84 EV/EBIDTA, x 7.85 6.77 5.59 4.96 P/BV, x 1.81 1.66 1.50 1.37 ROE, % 11.8 12.6 13.9 13.9 Debt/Equity (%) 0 0 0 0 Source: Phillip Securities Indonesia Research Est. Valuation Method: Discounted Cash Flow (DCF) Analyst Phillip Research Team (+65 6531 1240) [email protected]

Transcript of London Sumatra Plantation - PhillipCapital

Page | 1 | PHILLIP SECURITIES INDONESIA MCI (P) 019/11/2014_0013 Ref. No.: INDO2014_0017

London Sumatra Plantation (LSIP ID)

Planting Through Tough Period

INDONESIA | AGRICULTURE | INITIATION

18 December 2014

Company Background

PT. PP London Sumatra Indonesia Tbk. (Lonsum) is one of the largest

Indonesian-based plantation companies. It engages in plant breeding,

planting, harvesting, processing, and selling of palm products, rubber,

cocoa, and tea. The company owns a sizeable land bank, having over

100,000 ha planted nucleus area in North Sumatra, South Sumatra,

Java, East Kalimantan, North Sulawesi, and South Sulawesi producing

approximately 195,000 tons of Certified Sustainable Palm Oil (CSPO) per

year. With relatively young age profile and ISO 14001 certification across

all estates, all crop sectors, and all factories, bulking stations and

research stations to support its growth potential going forward.

Investment Merits

One of the largest CPO players in Indonesia with 90,707 hectares

planted oil palm area and is expected to produce 456,000 tons of Crude

Palm Oil (CPO) in 2014. Young palm trees age profile averaging at 12.8

years to support its high quality FFB production.

Maintain healthy financial position with cash and cash equivalent

amounting to IDR 1.3 trillion sitting on its balance sheet. These sizeable

cash reserves will provide a great opportunity for Lonsum to expand and

grow its business portfolio.

Best palm kernel extractor with 5.5 percent kernel extraction rate

while industry average only stood at 4.7 percent. High quality FFB

processed also contributed to an above-average palm oil extraction rate

of 22.9 percent per ton.

Highly efficient plantation company generated net profit of IDR

10.27 million per hectares in 2013, higher than the industry average of

only IDR 8.45 million per hectares.

Zero-debt Company as an indication of its resilience during severe

commodities price volatility and reduce its exposure to interest rate risk

as they are insulated from any rise in borrowing costs. Furthermore,

Lonsum is in a better shape as there is no cash outflow on interest

payments and hence, able to keep its costs to a minimum.

Key Risk Factors

High volatility in CPO prices has been our main concern for plantation

companies. As a pure upstream producer, Lonsum’s financial

performance is highly dependent to the volatility in its commodities

selling prices. Both CPO and rubber have gone through a tough year and

lack of positive catalyst to the commodities prices next year will cast a

shadow on the share price.

Accumulate

CMP IDR 1,885

TARGET IDR 2,040 (+8.2%) COMPANY DATA

O/S SHARES (MN) : 6,822.9

MARKET CAP (IDR BN) : 12,861.1

MARKET CAP (USDMN) : 1,013.3

52 - WK HI/LO (IDR) : 2,480 / 1,470

LIQUIDITY 3M (USDMN) : 22

PAR VALUE (IDR) : 100

MAJOR SHAREHOLDERS, %

SALIM IVOMAS PRATAMA Tbk 59.51

PUBLIC 40.49

PRICE VS. JCI

80

90

100

110

120

130

140

Nov-13 Mar-14 Jul-14 Nov-14

LSIP IJ JCI Rebased

Source: Phillip Securities Indonesia Research

KEY FINANCIALS

IDR bn FY14 FY15 FY16F FY17F

Net Sales 4,651 5,087 5,598 6,076

EBIDTA 1,468 1,647 1,966 2,174

Net Profit 842 975 1,186 1,306

EPS, IDR 123 143 174 192

PER, x 15.27 13.18 10.84 9.84

EV/EBIDTA, x 7.85 6.77 5.59 4.96

P/BV, x 1.81 1.66 1.50 1.37

ROE, % 11.8 12.6 13.9 13.9

Debt/Equity (%) 0 0 0 0

Source: Phillip Securities Indonesia Research Est.

Valuation Method: Discounted Cash Flow (DCF)

Analyst Phillip Research Team (+65 6531 1240) [email protected]

PHILLIP SECURITIES INDONESIA | 2 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Unfavorable weather condition such as El Niño could potentially

reduce the CPO production. Such dry weather often causes palm trees to

get stress which will in turn producing lower quality of FFB. Low quality

of FFB also means a lower Oil extraction rate that, at the end, will affect

the CPO production.

Lower Palm seeds sales caused by a decelerated palm oil area growth

in Indonesia. As the slowdown in palm oil planting continues, palm

seeds sales will likely to remain sluggish. However, the sluggish seeds

sales represent no significant impact to Lonsum as seeds sales only

accounted for a small percentage of its total revenue.

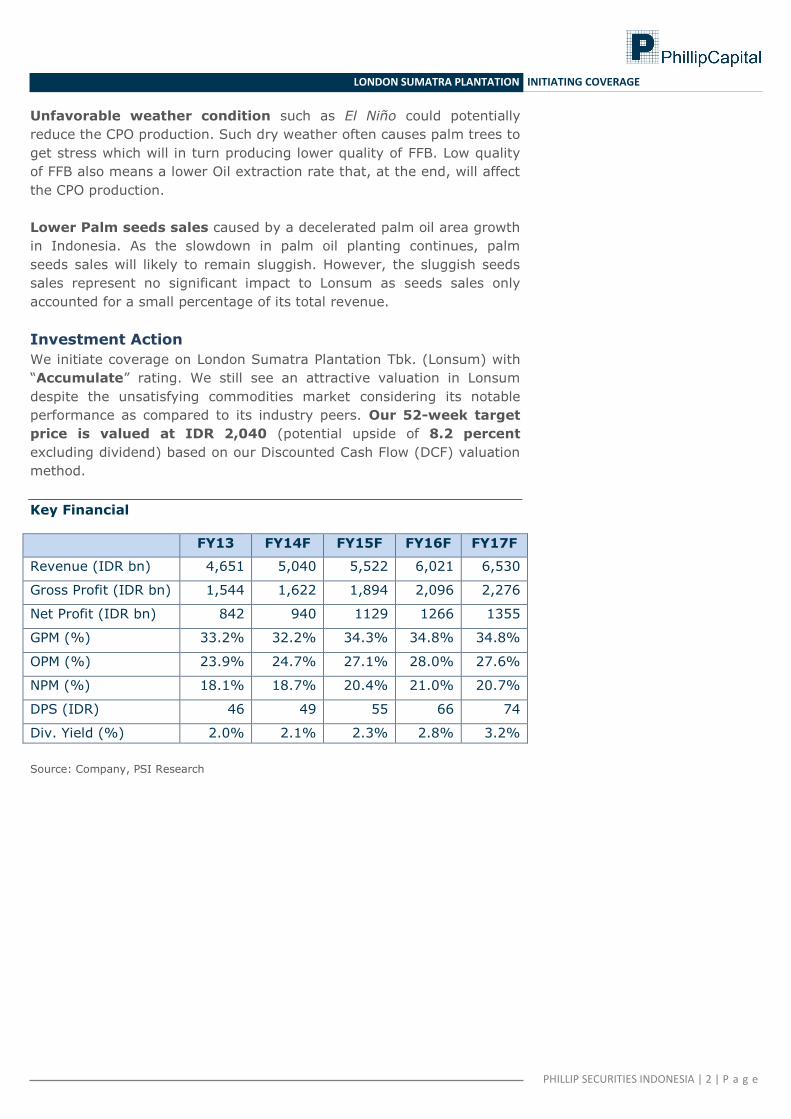

Investment Action

We initiate coverage on London Sumatra Plantation Tbk. (Lonsum) with

“Accumulate” rating. We still see an attractive valuation in Lonsum

despite the unsatisfying commodities market considering its notable

performance as compared to its industry peers. Our 52-week target

price is valued at IDR 2,040 (potential upside of 8.2 percent

excluding dividend) based on our Discounted Cash Flow (DCF) valuation

method.

Key Financial

FY13 FY14F FY15F FY16F FY17F

Revenue (IDR bn) 4,651 5,040 5,522 6,021 6,530

Gross Profit (IDR bn) 1,544 1,622 1,894 2,096 2,276

Net Profit (IDR bn) 842 940 1129 1266 1355

GPM (%) 33.2% 32.2% 34.3% 34.8% 34.8%

OPM (%) 23.9% 24.7% 27.1% 28.0% 27.6%

NPM (%) 18.1% 18.7% 20.4% 21.0% 20.7%

DPS (IDR) 46 49 55 66 74

Div. Yield (%) 2.0% 2.1% 2.3% 2.8% 3.2%

Source: Company, PSI Research

PHILLIP SECURITIES INDONESIA | 3 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Background of Company

PP London Sumatra Indonesia (Lonsum) was established back 100 years

ago in 1906 by Harrison and Crossfield, a general trading and plantation

management services firm. In 2007, PT. Indofood Sukses Makmur,

through its subsidiaries – Indofood Agri Resources Ltd (IndoAgri) and

PT. Salim Ivomas Pratama Tbk (SIMP) took over Lonsum from

Singapore-based First Durango and London-based Ashmore Funds.

Lonsum is currently one of the largest Indonesian listed plantation

companies with sizeable land bank, having over 100,000 ha planted

nucleus area with relatively young age profile for growth potential.

Location Map

In its early years, Lonsum diversified its business into rubber, cocoa,

and tea and concentrated on rubber throughout Indonesia’s formative

years as an independent nation. Lonsum then started commencing its oil

palm production in 1980s, and since then, oil palm has become the

Company’s primary commodity. Lonsum currently operates 11 palm oil

mills, four in North Sumatra, six in South Sumatra and one in East

Kalimantan with total annual processing capacity of 2,295,000 tons of

FFB per annum. Lonsum also owns 4 crumb rubber factory with 42,720

tons of Dry Rubber annual processing capacity as well as 3 sheet rubber

factory with annual processing capacity of 11,100 tons of dry rubber.

In 2012, Lonsum planted 4,522 hectares of new oil palm plantation area

in its estates in East Kalimantan. In 2013, the company continued to

expand its plantation area by adding another 4,541 hectares of new oil

palm in East Kalimantan as well as South Sumatra. As of September

2014, Lonsum owned a total of 90,707 hectares of oil palm plantation

across its nucleus estates in North Sumatra, South Sumatra, and East

Kalimantan, of which 76,658 hectares comprised of mature crops and

14,049 hectares of immature crops. In addition, Lonsum also managed

PHILLIP SECURITIES INDONESIA | 4 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

more than 36,000 hectares of planted plasma area of oil palm

plantations in South Sumatra and East Kalimantan.

Lonsum’s rubber plantation areas are located in North Sumatra, South

Sumatra, and South Sulawesi estates. As of September 2014, Lonsum

owned more than 17,100 hectares of rubber plantation, comprising

13,302 hectares of mature plantation and 3,843 hectares of immature

plantation areas.

On top of oil palm and rubber, Lonsum also operates tea and cocoa

plantations in East Java, North Sulawesi and North Sumatra. The

company’s total tea and cocoa plantation area was 2,804 hectares by

the end of September 2014.

Shareholding Structure

Industry Highlights

Palm Oil is the largest vegetable oil produced and consumed

worldwide. Palm Oil is widely-known for its stability and efficiency as a

common ingredient for food products, cosmetics, candles, detergents,

and all the way to biodiesel. The list of products that rely on the unique

properties of palm oil is long, that one estimate suggesting about half of

PHILLIP SECURITIES INDONESIA | 5 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

all packages items found in supermarkets contains palm oil. In terms of

world edible oil productions, Crude palm oil (CPO) dominates the market

with production amounting to 30 percent of global edible oils

productions followed by soya oil with 22.70 percent market shares in

terms of production volume.

Indonesia and Malaysia dominate the world’s CPO productions

with combined contribution of around 85 - 90 percent of total world CPO

output. Indonesia remains the largest CPO producer and exporter in the

world with total planted area of more than 10 million hectares, consists

of roughly 4.54 million hectares of plasma area, 4.98 million hectares of

private-owned and 690 thousand hectares of state-owned area.

Indonesia is expected to produce around 31 million tons of CPO which

accounted for 57 percent of the world’s CPO production in 2014. Experts

predict that next year’s production will be around 32.5 million tons and

will grow further to 41.7 million tons in 2020 and 51 million tons in

2025.

Edible Oils Production and CPO Production in 2014

Source: Index Mundi

CPO production growth increase at the same pace as the growth in new

planted area. With Indonesia oil palm expansion area that is still

growing, CPO production is expected to increase further for years to

come. However, as the growth rate of planted area started to slow in

2012, growth rate of mature area is expected to start slowing in 2015.

The slowdown in palm oil planting is largely due to land use conflicts,

the first and second phases of Indonesia’s forest moratorium, and also a

strong push to comply with both International and national sustainability

requirements.

PHILLIP SECURITIES INDONESIA | 6 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Indonesia Oil Palm Area

Source: U.S. Department of Agriculture (USDA)

Indonesia Oil Palm Area Growth (hectares)

Source: U.S. Department of Agriculture (USDA)

Outlook for CPO

In 2013, world consumption of palm oil increased to 55.6 million tons,

up from 52.1 million tons in 2012. European Union (EU), China, India,

and Indonesia consume more than 10 percent each of world CPO supply

in 2013. This year, Indonesia is expected to produce around 31 million

tons of CPO where more than 21 million tons of the production will be

exported and the rest will be consumed domestically for industrial use

as well as in food making processes. Indonesia exports majority of its

production to China, India, and also European Union.

PHILLIP SECURITIES INDONESIA | 7 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Indonesia’s CPO Export

Source: Indonesian Palm Oil Association

As seen from the chart above, India has been the largest single importer

of Indonesia’s CPO production over the years, followed by European

Union and China. These three largest importers absorb more than 60

percent of Indonesia’s exports volume in 2013.

Stable outlook from CPO exports

In 2014, CPO export is facing a sluggish demand, especially from India

and China. The slowing economic growth in these countries is the main

factor affecting the demand. An excess supply of soy bean harvested in

US made it even worse as the price of soybean became more

competitive. However, up to third quarter of 2014, we have seen an

increasing demand from other countries like Pakistan, Bangladesh, USA,

and other parts of the world. The growing demand for CPO is expected

to continue in the long run as the increasing world population will act as

the driving force for higher CPO consumptions.

Biodiesel to fuel demand for CPO

Indonesia has to depend on its domestic demand to absorb its huge CPO

output; one of which is by imposing a higher mandate for biodiesel.

Since September 2013, Indonesia has boosted the amount of biodiesel

blending from 7.5 percent to 10 percent, also requested power plants to

use gasoil blended with 20 percent biodiesel from January this year

onwards. The government plans to increase the biodiesel blending

mandatory to 20 percent effective in 2016 and 30 percent blending

mandatory in 2020. Plans to move to B20 in 2016 has become more

promising after the B20 road test involving various car brands and

models was successfully being done 40,000 kilometers in West Java

Province. The test will be continued to 100,000 kilometers by some car

manufacturers. Stakeholders are also working closely to implement the

Bioavtur mandatory in 2016.

PHILLIP SECURITIES INDONESIA | 8 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Indonesia Biodiesel Production

Source: Pertamina, Indonesian Biodiesel Producers Association

Factors affecting CPO price

Economic Slowdown in main exporting countries especially China

and India poses a threat that would result in reduced demand for palm

oil. Up to September 2014, Indonesian export of CPO to India fell by 38

percent to 305,000 tons on month-on-month basis. On year-on-year

basis, exports to India have declined by 26 percent to 3.3 million tons in

the first month of 2014. The substantial decline in exports was caused

by India’s higher import tariffs for CPO, the depreciated rupee currency

vs. the U.S dollar, and India’s high inflation.

Meanwhile, Indonesian CPO exports to China fell 31 percent month-on-

month to 56,000 tons in September and declined by 10 percent on year-

on-year basis to 1.6 million tons in the first nine-month period. Chinese

palm oil imports slowed as buyers are struggling to obtain funding amid

Beijing’s crackdown on commodity financing that caused banks to be

more stringent in lending. A slower GDP growth in China, as a result of a

slumping real-estate market as well as a weak domestic demand and

industrial production, also acts as a contributing factor to the sluggish

CPO imports.

Good harvest of substitute seeds such as soybean and rapeseed.

With an expected record high U.S. soybean production in 2014, soybean

oil prices have responded by moving sharply lower; narrowing the price

gap of CPO discount to soybean. Historically, palm oil is known for its

big price gap to soybean oil of around US$ 150 – 200 discount per ton

range. However, with the excess supply of soybean production, the price

gap shrank to an average of US$ 84 each ton; making it more price

competitive as compared to CPO.

PHILLIP SECURITIES INDONESIA | 9 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Price gaps among major edible oils

Source: LMC International.

Indonesia’s “Toothless Mandate” for Biodiesel is hurting CPO

prices. Indonesia introduced a regulation last September to boost the

use of palm-based biodiesel in a move to cut its oil import bill. The

government raised its minimum blending requirement to 10 percent for

biodiesel fuel used for transportations and 20 percent blending

requirement for power plant generators with a target for biodiesel

consumption in 2014 to be 3.3 million tons. Despite the ambitious

regulations, Indonesia is predicted to use not more than 2 million tons of

biodiesel; blaming the failure to live up to their commitment for use of

palm biodiesel as transport fuels. The government is pushed to impose

rewards and punishments in order to effectively implement the biodiesel

mandate. At the time being, the mandate acts as a request rather than

a mandate itself as there has been no direct penalty for non-compliance.

Unless if the government is committed to expand its palm-based

biodiesel through strict rules, the palm oil industry is expected to face a

challenging time in the last half of 2015.

Declining crude oil prices makes palm oil less appealing for

blending into biodiesel. Crude oil prices have tumbled to five-year low

amid ample supply and came under pressure as OPEC decided not to cut

oil output. The decline in crude oil prices will have a big impact on the

use of palm oils for biodiesel. It is estimated that the world will consume

29 million tons of oils and fats as fuel this year. Palm oil will account for

a third of the total feedstock used to produce biodiesel. This means that

9.3 million tons or 16 percent of the global CPO production is for fuel.

The weak crude oil price is expected to dent palm oil demand by making

it less appealing for blending into biodiesel. With that said palm oil

prices might need to go below premium over Brent in order to increase

its comparative advantages in blending into biodiesel.

PHILLIP SECURITIES INDONESIA | 10 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

CPO Prices Premium over Brent

Source: LMC International.

Growing population acts as catalyst to boost CPO consumptions.

As we all know, CPO is used globally as an ingredient to produce almost

all kinds of food products. With the fast population growth in the

developing countries, the needs for foods are also growing at the same

rate; hence will increase the demand for CPO in the future. An increase

in income per capita is also one of the main reason driving up the CPO

consumptions. Moreover, the CPO consumptions rate is still low in

developing countries which will have a huge potential to absorb the

growing supply of CPO in years to come.

CPO Price Outlook

Considering all the factors that we discussed above, the short-term

demand for CPO is still sensitive to the economic growth in main

importing countries and CPO prices are also under pressure as the drop

in Brent oil will lessen the attractiveness of palm oil to produce biodiesel

as CPO price is currently trading above the Brent oil. In the first half of

2015, we expect CPO price to have a little gain as the low-harvesting

season hits and dry up the supply of CPO. The benchmark for CPO will

range between MYR 2,200 – 2,400 in the first half of 2015 and

the price movement towards the end of the year will strongly be tied to

the decisions made by Indonesian government on the biodiesel

mandate. If the mandate is implemented in full, prices will rise; vice

versa.

Investment Thesis

One of the largest CPO players in Indonesia with more than 90,000

hectares of planted nucleus area and also supported by 36,000 hectares

of planted plasma area, Lonsum is expected to increase its CPO

production for 2014 to be around 456,000 tons, or increased by 15

percent yoy. We expect Lonsum’s CPO production to increase steadily

for the upcoming years as the droughts that impacted some of its

plantation areas were not significant. The growing CPO production is

PHILLIP SECURITIES INDONESIA | 11 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

also supported by Lonsum’s young palm trees’ profile with average age

at 12.8 years.

Lonsum plans to increase its palm oil estates by 3,500 hectares

this year. Up to 9-month of 2014, Lonsum has increased its palm oil

area to 90,707 hectares or up by 862 hectares. The additional areas up

to the third quarter are still well below its full year target; however, the

company remains confident that they will hit the target as most of the

acquisitions and planting activities are done near the end of the year.

Lonsum’s expansion program has been quite modest, around 4,000 –

5,000 hectares per annum.

High Cash Reserves

In 3Q14, Lonsum reported a strong cash position as compared to its

peers. Lonsum cash and cash equivalent worth more than IDR 1.38 tn in

3Q14. These vast cash reserves will help to finance the company’s

expansion plan of IDR 1 tn to build their infrastructure facilities as well

as the new plantation areas as their key expansion programs in the

future.

No debt track record. Since the issuance of new shares as the

conversion of company’s debt in 2004, Lonsum’s balance sheet position

continued to be strong with vast cash reserves and no funded debt.

Gross debt to equity and net debt to equity ratio were 0.00 times and -

0.21 times in 2013. The finalized debt restructuring provides Lonsum

with a much stronger balance sheet and greater liquidity for the

company to focus on the operational improvements.

Cash Ratio Peers Comparison

Source: Company Data

PHILLIP SECURITIES INDONESIA | 12 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Gearing Ratio Peers Comparison

Source: Company Data

Best Palm Kernel Extractor. Lonsum’s Kernel Extraction Rate (KER) is

the highest among its industry peers. In its 1H14 report, Lonsum posted

the Palm Kernel Extraction Rate at 5.5 percent; where majority of the

industry players posted KER below 5 percent mark. Palm Kernel

production up to 3Q14, consequently, increased by 26.2 percent yoy to

80,921 tons. Palm kernel revenue also grew by 105.7 percent yoy in

3Q14 supported by the increase in production as well as a jump in the

average selling price.

FFB Yield, Oil Extraction Rate (%), Kernel Extraction Rate (%)

Peers

Comparison

Source: Company Data

Lonsum is among the largest seeds producers in Indonesia. With

more than 70 years experience, Lonsum’s research arm, Sumatra

Bioscience “SumBio”, has gained reputation as top seed producer in

PHILLIP SECURITIES INDONESIA | 13 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Indonesia producing around 20,000 superior oil palm seeds which have

been commercially proven in Indonesia to be at least equal and

generally outperform the yield performance as compared to other seeds

from local and overseas suppliers. Unlike seeds from overseas suppliers,

SumBio seeds have been developed and selected in breeding trials in

both North and South Sumatra for the specific environments of

Indonesian customers.

Key risks

Risk of CPO price fluctuation

Palm Oil is a globally traded commodity where the price mechanism is

derived from the supply and demand in the market. The fluctuations of

CPO prices have direct exposure to the company’s top and bottom line

due to the sizeable amount of CPO that they produce. As a typical price

taker company, Lonsum will bear the fluctuation risk where in times of

weak CPO prices, Lonsum will likely to book lower revenue if outputs

remain the same; vice versa. For instance, Lonsum experienced an

increase in revenue up to the third quarter this year as the average

selling price of CPO went higher than last year. We still expect that

Lonsum will be able to maintain its revenue growth through the end of

the year despite the reversal signs in CPO prices from its peak.

Adverse weather conditions have traditionally been the single biggest

risk for planters. The abnormal warming of sea water temperatures in

the Pacific, or formally called El Niño phenomenon, can drench parts of

the globe and parch others, damaging crops and food supply. Although

this year’s El Niño failed to materialize, fears of its appearance have not

entirely subsided. An El Niño weather phenomenon, which is typically

associated with dryness, could cause tree stress in some of plantation

estates and hence, reducing Fresh Fruit Bunch (FFB) harvesting yield.

Planters with lower FFB will in turn produce lower CPO outputs and

damaging their financial performance. Although the El Niño phenomenon

has usually been compensated by higher CPO selling prices, the question

remains on how severe the droughts impacts to the palm trees.

Investment Correlation

The correlation between Lonsum’s stock price and CPO price has been

44.55 percent over the past 12 months. Among the big plantation

companies, Lonsum has the highest correlation rate with CPO price

movement. Hence, it is very crucial that we pay a close attention to CPO

price developments.

Correlation – r

London Sumatra Plantation 44.55 %

Sampoerna Agro 31.39 %

Astra Agro Lestari 30.82 %

Salim Ivomas Pratama 25.11 %

Sawit Sumbermas Sarana 8.52 %

Source: Bloomberg, PSI Research

PHILLIP SECURITIES INDONESIA | 14 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Share Price Correlation with CPO

Source: Bloomberg, PSI Research

Valuation and Sensitivity Analysis

We value London Sumatra based on our Discounted Cash Flow (DCF)

valuation method for the next 52 weeks at IDR 2,040 per share with

WACC at 9.39 percent and terminal growth rate at 1 percent per annum.

Our price target implies P/E 14.27x. Plantation is a longer dated

business with a long harvesting period before the crops are fructified

and processed into commodities. Commodities prices can be extremely

volatile in those periods hence we believe DCF is a better valuation

method to value the business throughout the cycle.

Valuation Summary

(IDR bn) FY13 FY14F FY15F FY16F FY17F

Operating Cashflow 1,284 1,456 1,694 1,914 2,104

Less: Capex (1,036) (1,030) (1,133) (1,206) (1,317)

Add: Investment in associates 54 295 - - -

Free Cash Flow (FCF) 302 720 561 707 786

WACC Components

PV of FCFF (growth + terminal) 13,914 Risk Free Rate 7.69%

Beta 0.48

Fair Value per share (IDR) 2,040 Required Return 11.23%

2015 EPS (IDR) 143 Equity Risk Premium3.54%

Target PER (X) 14.27 WACC 9.39%

Source: Company, PSI Research

PHILLIP SECURITIES INDONESIA | 15 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

DCF Fair Value Sensitivity

7.89% 8.39% 8.89% 9.39% 9.89% 10.39% 10.89%

-0.5% 2,229 2,091 1,969 1,859 1,761 1,671 1,590

0.0% 2,313 2,163 2,031 1,913 1,808 1,712 1,626

0.5% 2,409 2,245 2,101 1,973 1,859 1,758 1,666

1.0% 2,518 2,337 2,179 2,040 1,917 1,808 1,710

1.5% 2,645 2,442 2,268 2,115 1,982 1,863 1,758

2.0% 2,793 2,565 2,369 2,201 2,054 1,926 1,811

2.5% 2,969 2,707 2,487 2,299 2,137 1,996 1,871

IDRWACC

Terminal

Growth

Source: PSI Research

Sensitivity Analysis

We have identified the following 3 variables that are vital to the earnings

performance and price target: (1) Fresh Fruit Bunch (FFB) yield, (2) CPO

Production, and (3) CPO price assumption. In the analysis below, we will

vary the FFB yield, CPO production, and CPO price assumption by 10

percent. Other variables are kept constant.

FY14F FY15F FY16F FY14F FY15F FY16F FY14F FY15F FY16F

FFB Yield (tons / ha) 15.8 15.9 16.2 17.5 17.7 18.0 19.3 19.5 19.8

Sales 4,347 4,740 5,220 4,651 5,087 5,598 4,972 5,434 5,976

Gross Profit 1,240 1,321 1,592 1,544 1,669 1,970 1,865 2,016 2,348

Net Profit 614 715 903 842 975 1,186 1,083 1,236 1,469

EPS 90 105 132 123 143 174 159 181 215

Price Target

CPO Production ('000 tons) 385.2 417.6 450.9 428.4 463.6 501.0 470.8 510.4 551.1

Sales 4,276 4,685 5,152 4,651 5,087 5,598 5,019 5,496 6,043

Gross Profit 1,169 1,267 1,524 1,544 1,669 1,970 1,912 2,078 2,415

Net Profit 561 674 852 842 975 1,186 1,118 1,282 1,519

EPS 82 99 125 123 143 174 164 188 223

Price Target

CPO Price (IDR / ton) 7,740 7,785 7,920 8,600 8,650 8,800 9,460 9,515 9,680

Sales 4,279 4,682 5,153 4,651 5,087 5,598 5,023 5,492 6,044

Gross Profit 1,172 1,264 1,525 1,544 1,669 1,970 1,916 2,074 2,415

Net Profit 563 671 852 842 975 1,186 1,121 1,279 1,520

EPS 83 98 125 123 143 174 164 188 223

Price Target

2,040

2,040

2,040

1,963 2,117

2,131

2,131

1,950

1,950

IDR bn -10% vs. base Base estimates +10% vs. base

Source: PSI Research

PHILLIP SECURITIES INDONESIA | 16 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

SWOT Analysis

Strength

One of the largest palm oil plantation company in Indonesia

having over 100,000 hectares of planted area

Cash-rich Plantation Company with more than IDR 1.3 trillion

sitting on its balance sheet to support its long-term expansion

program

Financially healthy with no debt burden

Strong earnings power, measured by revenue and net income

per hectare

Young trees age profile producing high extraction rate FFB

Well-known for its strong research and development division

High-quality palm seeds producer

Weakness

High concentration on upstream production line

Exposed to CPO price volatility

Sells majority of CPO production to one company; Lonsum

business nature is to supply CPO to parent company, PT Salim

Ivomas Pratama Tbk

Opportunities

Upcoming palm-based Biodiesel mandate in several countries,

Malaysia and Indonesia

Growing number of population to serve as a backbone for higher

CPO consumptions

Growing demand from developing countries, such as Pakistan

and Bangladesh

Threats

Slowing economic growth in importing countries like China and

India

Falling crude oil prices that have close association with CPO will

suppress CPO prices

European Union’s anti-palm oil campaign where “Without Palm

Oil” labels are placed on food products

Adverse weather conditions to affect output

Competition from other edible oils

Land ownership issues

PHILLIP SECURITIES INDONESIA | 17 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Financial Statement

Key Ratios

FY13 FY14F FY15F FY16F FY17F FY18F FY19F

P/E (X) 20.36 15.27 13.18 10.84 9.84 9.05 8.14

P/B (X) 2.43 1.81 1.66 1.50 1.37 1.25 1.14

EV/EBITDA (X) 11.52 7.85 6.77 5.59 4.96 4.42 3.85

Div. Yield (%) 2.4% 2.5% 2.6% 3.0% 3.7% 4.1% 4.4%

EPS 116 123 143 174 192 208 232

ROE (%) 11.6% 11.8% 12.6% 13.9% 13.9% 13.8% 14.0%

ROA (%) 9.6% 9.7% 10.3% 11.3% 11.3% 11.1% 11.2%

DER - - - - - - -

Income Statement

FY13 FY14F FY15F FY16F FY17F FY18F FY19F

Revenue 4,134 4,651 5,087 5,598 6,076 6,618 7,179

Cost of Goods Sold (2,880) (3,107) (3,418) (3,628) (3,926) (4,255) (4,605)

Gross Profit 1,253 1,544 1,669 1,970 2,150 2,363 2,574

Operating expense (228) (431) (375) (396) (408) (475) (473)

Finance income (29) 10 6 7 (0) 5 5

Profit Before Tax 997 1,123 1,300 1,581 1,742 1,893 2,106

Taxation (228) (281) (325) (395) (435) (473) (527)

Profit After Tax 769 842 975 1,186 1,306 1,420 1,580

Cash Flow Statement

FY13 FY14F FY15F FY16F FY17F FY18F FY19F

CFO

Net Income 769 842 975 1,186 1,306 1,420 1,580

WC Changes 1,195 1,125 1,472 1,640 1,834 2,064 2,412

Others (649) (682) (992) (1,132) (1,227) (1,381) (1,658)

Cashflow from operation 1,314 1,285 1,456 1,694 1,914 2,104 2,334

CFI

Capex, net (1,071) (1,036) (1,030) (1,133) (1,206) (1,317) (1,399)

Others (207) 20 280 (14) (17) (23) (25)

Cashflow from investment (1,277) (1,016) (750) (1,148) (1,223) (1,340) (1,424)

CFF

Dividends (450) (315) (337) (390) (474) (523) (568)

Others 21 (21) - - - - -

Cashflow from financing (429) (337) (337) (390) (474) (523) (568)

Net changes in cash (392) (67) 369 156 216 241 342

Ending CCE 1,401 1,334 1,703 1,859 2,075 2,316 2,658

PHILLIP SECURITIES INDONESIA | 18 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Balance Sheet

FY13 FY14F FY15F FY16F FY17F FY18F FY19F

PPE 5,270 5,960 6,643 7,391 8,165 8,993 9,850

Investments 348 295 - - - - -

Others 358 392 411 430 452 480 511

Total non-current assets 5,976 6,647 7,054 7,821 8,617 9,473 10,361

CCE 1,401 1,334 1,703 1,859 2,075 2,316 2,658

Inventories 374 421 461 507 550 600 650

Receivables 117 135 153 173 194 218 245

Others 106 130 138 148 163 179 193

Total current assets 1,999 2,021 2,455 2,688 2,983 3,314 3,747

Total Assets 7,975 8,668 9,509 10,509 11,600 12,787 14,107

Payables 427 505 559 583 632 681 722

Short-term employee benefit 224 247 271 299 329 361 397

Others 153 144 152 166 189 206 215

Total current liabilities 804 896 982 1,048 1,149 1,249 1,334

Long-term employee benefit 547 643 759 897 1,056 1,244 1,468

Others 10 10 10 10 10 10 10

Total non-current assets 556 653 769 907 1,066 1,254 1,478

Shareholders Equity 6,614 7,119 7,758 8,554 9,386 10,283 11,295

Total Liabilities and Equity 7,975 8,668 9,509 10,509 11,600 12,787 14,107 Source: PSI Research

PHILLIP SECURITIES INDONESIA | 19 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Contact Information (Singapore Research Team) Management Chan Wai Chee (CEO, Research - Special Opportunities)

+65 6531 1231 Research Operations Officer Jaelyn Chin +65 6531 1240

Joshua Tan (Head, Research - Equities & Macro)

+65 6531 1249

Macro | Equities Market Analyst | Equities US Equities Soh Lin Sin +65 6531 1516 Kenneth Koh +65 6531 1791 Wong Yong Kai +65 6531 1685 Bakhteyar Osama +65 6531 1793 Finance | Offshore Marine Real Estate Benjamin Ong +65 6531 1535 Caroline Tay +65 6531 1792 Telecoms | Technology Transport & Logistics Colin Tan +65 6531 1221 Richard Leow, CFTe +65 6531 1735

Contact Information (Regional Member Companies) SINGAPORE

Phillip Securities Pte Ltd Raffles City Tower

250, North Bridge Road #06-00 Singapore 179101 Tel +65 6533 6001 Fax +65 6535 6631

Website: www.poems.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd

B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450

Kuala Lumpur Tel +603 2162 8841 Fax +603 2166 5099

Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong

Tel +852 2277 6600 Fax +852 2868 5307

Websites: www.phillip.com.hk

JAPAN

Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku,

Tokyo 103-0026 Tel +81-3 3666 2101 Fax +81-3 3666 6090

Website: www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia

ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia

Tel +62-21 5790 0800 Fax +62-21 5790 0809

Website: www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co Ltd

No 550 Yan An East Road, Ocean Tower Unit 2318,

Postal code 200001 Tel +86-21 5169 9200 Fax +86-21 6351 2940

Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak,

Bangkok 10500 Thailand Tel +66-2 6351700 / 22680999

Fax +66-2 22680921 Website www.phillip.co.th

FRANCE King & Shaxson Capital Limited

3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France

Tel +33-1 45633100 Fax +33-1 45636017

Website: www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Capital Limited

6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS

Tel +44-20 7426 5950 Fax +44-20 7626 1757

Website: www.kingandshaxson.com

UNITED STATES Phillip Futures Inc

141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building

Chicago, IL 60604 USA Tel +1-312 356 9000 Fax +1-312 356 9005

Website: www.phillipusa.com

AUSTRALIA Phillip Capital Limited

Level 12, 15 William Street, Melbourne, Victoria 3000, Australia

Tel +61-03 9629 8288 Fax +61-03 9629 8882

Website: www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited

No-10 Prince Alfred Tower, Alfred House Gardens, Colombo 03, Sri Lanka Tel: (94) 11 2429 100 Fax: (94) 11 2429 199

Website: www.ashaphillip.net

INDIA PhillipCapital (India) Private Limited

No.1, 18th Floor Urmi Estate

95, Ganpatrao Kadam Marg Lower Parel West, Mumbai 400-013

Maharashtra, India Tel: +91-22-2300 2999 / Fax: +91-22-2300 2969

Website: www.phillipcapital.in

TURKEY PhillipCapital Menkul Degerler

Dr. Cemil Bengü Cad. Hak Is Merkezi No. 2 Kat. 6A Caglayan 34403 Istanbul, Turkey

Tel: 0212 296 84 84 Fax: 0212 233 69 29

Website: www.phillipcapital.com.tr

DUBAI Phillip Futures DMCC

Member of the Dubai Gold and Commodities Exchange (DGCX)

Unit No 601, Plot No 58, White Crown Bldg, Sheikh Zayed Road, P.O.Box 212291

Dubai-UAE Tel: +971-4-3325052 / Fax: + 971-4-3328895

Website: www.phillipcapital.in

PHILLIP SECURITIES INDONESIA | 20 | P a g e

LONDON SUMATRA PLANTATION INITIATING COVERAGE

Important Information

This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore (“Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication.

The information contained in this publication has been obtained from public sources, which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision, including, but not limited to your reliance on the information, data and/or other materials presented in this publication.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this publication.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction. Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication.

This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document. This report is only for the purpose of distribution in Singapore.