LEADERSHIP Winston Churchill Members: Leong Qi Dong Samuel Ng Gao Yan Sha Yicheng.

date post

21-Dec-2015Category

view

215download

0

LOGO

How Could Bank of China, BOC Tower Sub-Branch

Reduce the Prepayment of Mortgage Loan

How Could Bank of China, BOC Tower Sub-Branch

Reduce the Prepayment of Mortgage Loan

Name: Yu Yamin (俞雅敏 ) 2003175214 Shen Yicheng (沈一成 ) 2003175232

Major: International Finance

Name: Yu Yamin (俞雅敏 ) 2003175214 Shen Yicheng (沈一成 ) 2003175232

Major: International Finance

CONTENTS

INTRODUCTION 1

ISSUE 2

DEFINITION OF THE PREPAYMENT 3

METHODOLOGIS 4

5 DEMARCATIONS

FOUR MARJOR ASPECTS6

1 INTRODUCTION

1.1 Introduction of Bank of China, BOC Tower Sub-Branch

Founded in 2001

Located at Lu Jia Zui

The mortgage loan is the most important part of Bank of China, BOC Tower Sub-Branch since it occupies almost 70% profit of the entire sub-branch

1 INTRODUCTION

1.2 Introduction of the mortgage market in Shanghai

The Total Amount of Personal Consumption Loans (2001-2004)Unit: billion Yuan

The Total Amount of Personal Consumption Loans (2001-2004)Unit: billion Yuan

20012002

20032004

65

26.62.262

108.671

31.7984.145

170.913

34.639

8.468

244.553

34.642

7.928

0

50

100

150

200

250

300

Mortgage loans Housing-fund loans Auto loans

Shanghai real estate market developed quickly in recent years. The residential market in 2006 will be more diversified. The overall transaction volume will see an escalation and the average price of overall residential property decline.

2 ISSUE

The Mortgage Condition of the First Quarter,2006The Mortgage Condition of the First Quarter,2006Unit: Thousand Yuan

Total amount of mortgage loan 152,252.00

Total prepayment 215,602.00

The new increasing amount of mortgage loan

-63,350.00

The new increasing amount of mortgage loan= the total amount of mortgage loan – the total prepayment.

The new increasing amount of mortgage loan= the total amount of mortgage loan – the total prepayment.

Add YourTitle Text

•Text 1•Text 2•Text 3•Text 4•Text 5

METHODOLOGIESMETHODOLOGIES DEMARCATIONSDEMARCATIONS

44

1. Commercial banking management

2. Market research

3. Sales promotion

55

1. Time zone: 1998~2006

2. Geography: Shanghai

6 FOUR MARJOR ASPECTS

SALES PROMOTION STRATEGY REFORM

INVESTMENT CONSULTANT SERVICE PROVIDING

INTEREST RATE SYSTEM REFORM

COMMITMENT FEE REFORM

REDUCE THE REDUCE THE PREPAYMENTPREPAYMENT

INTEREST RATE SYSTEM REFORM

COMMITMENT FEE REFORM

SALES PROMOTION STRATEGY REFORM

INVESTMENT INVESTMENT CONSULTANT CONSULTANT SERVICE SERVICE PROVIDINGPROVIDING

INVESTMENT CONSULTANT SERVICE PROVIDING

INTEREST RATE SYSTEM REFORM

Benchmark interest rate

Loan interest rate

Monthly repayment

High prepayment risk

To bank

To borrowers

To bank

The Adjustable-Rate Mortgage (ARM)

The Fixed-Rate Mortgage

The comparison between Adjustable-Rate Mortgage and The comparison between Adjustable-Rate Mortgage and Fixed-Rate Mortgage Fixed-Rate Mortgage

Item Adjustable-Rate Mortgage Fixed-Rate Mortgage

Interest rate Variable Fixed

Interest payment Variable Fixed

Prepayment Risk Higher Lower

INTEREST RATE SYSTEM REFORM

The advantage of Fixed-Rate MortgageThe advantage of Fixed-Rate Mortgagea) Locking the mortgage loan interest rate risk b) Reducing borrowers’ early repaymentsc) Minimizing the prepayment risk of the bank d) Preparing for the development of mortgage securitization

Suggestion: Using a Fixed-Rate Mortgage

Target marketing screeningTarget marketing screening Term to maturity and the Fixed-RateTerm to maturity and the Fixed-Rate

settingsetting

Schedules of RepaymentsSchedules of Repayments(1)Same principal and same interest repayment(1)Same principal and same interest repayment

(2)Same principal repayment(2)Same principal repayment

INTEREST RATE SYSTEM REFORM

Term to maturity Fixed-Rate

Less than 3years(inclusive) 5.95%

3-5years(inclusive) 6.04%

5-10years(inclusive) 6.28%

SALES PROMOTION STRATEGY REFORM

COMMITMENT FEE REFORM

INVESTMENT CONSULTANT

SERVICE PROVIDING

INVESTMENT CONSULTANT

SERVICE PROVIDING

SALES SALES PROMOTION PROMOTION STRATEGY STRATEGY REFORMREFORM

A Discount Interest Rate

Unit: Yuan The repayment per month

The total interest

The discount interest rates of 5.751%

p.a.2,917.23 550,545.5

The discount interest rates of 5.508%

p.a.2,841.46 522,923.85

SALES PROMOTION STRATEGY REFORM

The effect of interest rates adjustment(the benchmark interest rate )

The effect of interest rates adjustment( the discount interest)

Unit: Yuan The repayment per month

The total interest

The benchmark interest rate of

6.39% p.a.3,126.22 624,732.3

The benchmark interest rate of

6.12% p.a.3,036.44 593,117.03

Difference of total interest=31,615.27 Difference of total interest=27,621.65

The influence on the total interest payments is less when implement a discount interest rate

as interest rate adjusted.

Suggestion

SALES PROMOTION STRATEGY REFORM

Provide the discount interest rate of Provide the discount interest rate of mortgage loansmortgage loans

Prize systemPrize system

Year 5-10 11-15 16-20 21-25 26-30

The proportion between the value of prize and the amount of mortgage loan (%)

0.1 0.2 0.3 0.4 0.5

COMMITMENT FEE REFORM

SALES PROMOTION STRATEGY REFORM

INVESTMENT CONSULTANT

SERVICE PROVIDING

INVESTMENT CONSULTANT

SERVICE PROVIDING

COMMITMENT COMMITMENT FEE REFORMFEE REFORM

The Commitment fee Amount =early repayment of the loan amount X monthly

interest rate

The Commitment fee Amount=Zero

For loans less than one year

Current Commitment Fee of The Sub-Branch

COMMITMENT FEE REFORM

For loans more than one year

The current commitment fee policy could not be

efficient to reduce the phenomenon of borrowers’

repayments before maturities and the prepayment risk

of the bank as well.

Efficiency of The Current Commitment Fee

COMMITMENT FEE REFORM

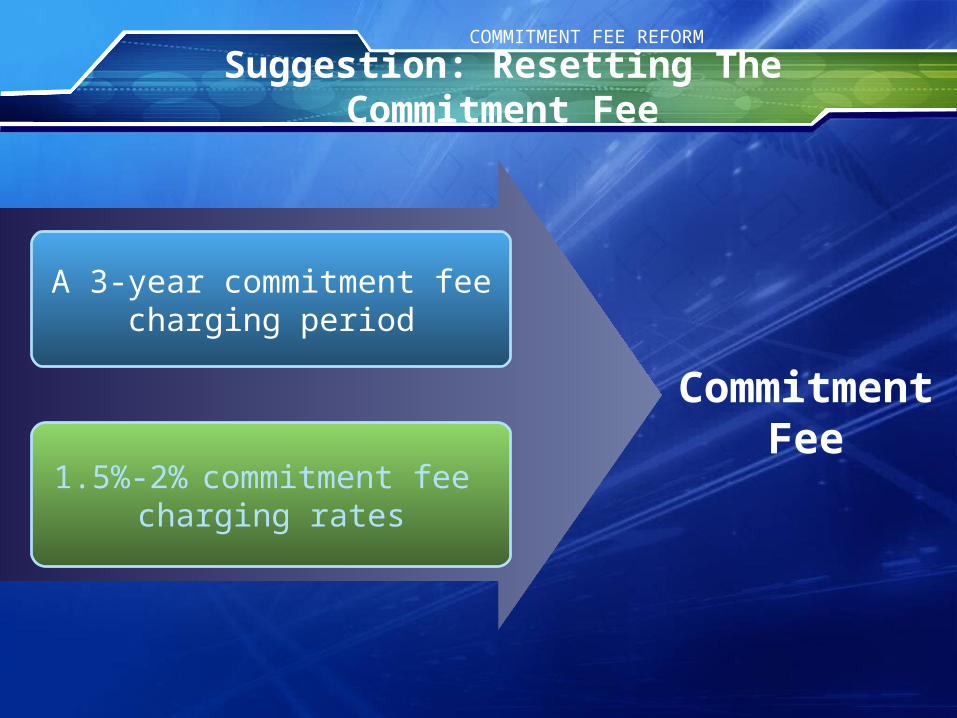

Suggestion: Resetting The Commitment Fee

COMMITMENT FEE REFORM

A 3-year commitment feecharging period

1.5%-2% commitment fee charging rates

Commitment Fee

INVESTMENT CONSULTANT SERVICE PROVIDING

COMMITMENT FEE REFORM

SALES PROMOTION STRATEGY REFORM

INVESTMENT CONSULTANT

SERVICE PROVIDING

INVESTMENT INVESTMENT CONSULTANT CONSULTANT

SERVICE SERVICE PROVIDINGPROVIDING

Borrowers’ Excess Money

Salary payment

Living Standards

Mortgage Prepayments

Investments

Life Enjoying

INVESTMENT CONSULTANT SERVICE PROVIDING

Borrowers’ Borrowers’ Excess MoneyExcess Money

Suggestion: Attract Borrowers’ Investment

INVESTMENT CONSULTANT SERVICE PROVIDING

Providing investment information for the borrowers

Holding investment seminars for the borrowers text

Opening a new investment account Which linking with

the mortgage loan account

Investments Investments instead of instead of

PrepaymentsPrepayments

Investments Investments instead of instead of

PrepaymentsPrepayments

10 CONCLUSION

With the development of the mortgage market, the amount of Bank of China, BOC Tower Sub-Branch mortgage loans increases quickly in recent years. But the condition that borrowers’ prepayment become serious, that lead to Bank of China, BOC Tower Sub-Branch which mortgage loan business occupies almost 70% of the whole business into a worse situation.

LOGO