Location investment, credits and incentives survey · Location investment, credits and incentives...

16

Location investment, credits and incentives survey

Transcript of Location investment, credits and incentives survey · Location investment, credits and incentives...

Location investment, credits and incentives survey

2 | Location investment, credits and incentives survey

Methodology This report provides an overview of key themes and findings from Ernst & Young LLP’s semiannual C&I survey. Its findings are based on a quantitative survey instrument augmented by the views and experiences of key members of our C&I practices. The survey, compiled in late 2015, encapsulates the strategies and practices as described by 625 primarily tax and finance executives from Fortune 1000 businesses.

3Location investment, credits and incentives survey |

There is strong evidence of economic growth, led by more than $150 billion in capital investment announced by companies in the US, according to the Ernst and Young LLP Investment Monitor for 2015. Meanwhile, by all measures, merger and acquisition (M&A) activity is on the upswing, while at the same time, many companies are moving aggressively to consolidate their existing operations. High levels of capital investment, M&A and active consolidation all lead to an increase in site-focused decision-making: where to expand, where to consolidate, where to pursue greenfield investment. Companies are also making significant advances in sustainability-focused technologies.

Yet, even active companies are not pursuing all incentive opportunities equally. Credits potentially seen as niche areas, including sustainability C&I programs, are not pursued at the same rate, even though most companies can find benefits for green investments. In addition, companies are not as likely to look outside of the US for incentives, when in reality, international locations have multiple C&I programs that could apply.

Foreword

Paul NaumoffEY Americas Location Investment, Credits and Incentives Leader

With so many international, federal, state and local programs, each with their own definitions and rules, there’s no doubt that the way forward can be complex. So what are the best practices, and what process might you consider to optimize the benefit from the multitude of tax credits and incentive programs available? Our survey also provides a look into some of the best practices of active companies that are benefiting from the available credits and incentives.

We submit the following summary of key findings from this year’s C&I survey with these thoughts in mind. Whatever your role in such opportunities, we hope you find this report to be interesting and valuable.

In today’s global economy, there continues to be an increase in factors to be considered when making location investment decisions. Taxes and incentives are not typically the sole driver of strategy in these location investment decisions. However, companies that actively1 pursue tax credits and business incentives (C&I) are twice as likely as others to find that when two or more potential locations are evenly suited on other fronts, such benefits can become the deciding factor.

Put another way, those that aren’t active — that have processes and focus that don’t make room for identification and evaluation of C&I — are twice as likely to miss out on opportunities. That’s just one of many key findings in our most recent C&I survey. The fact that less than one-half of companies are active in this area is particularly surprising, especially in an environment abundant with opportunities in C&I — both for businesses in optimizing their operations and for nations, states and municipalities seeking to preserve and build tax base, employment and overall economic health.

1. About half of companies — 46% — say they are either very active (10%) or active (36%) in the pursuit and utilization of C&I. The 10% that say they are very active are referred to as the “active” group throughout this research.

4 | Location investment, credits and incentives survey

Companies that overlook tax credits and business incentives — that have related processes that are less than optimal — are likely missing out on significant opportunities. In evidence, compare the practices and outcomes between those described in the foreword as active in C&I and the general population of businesses.

Start with economic modeling. Nearly 9 out of 10 active companies (89%) say they model the various C&I packages likely available from alternative locations either always (49%) or often (40%). Compare this with the average businesses where only 1 out of 3 (38%) use modeling always (15%) or often (23%).

Now consider how often tax credits and business incentives have a material impact on the location decision that they become the determining factor: 26% on average — but for active companies, 55%.

By no means does this imply that tax and related incentives are the core driving factors in a location decision. Rather, once companies have their options down to a short list, companies with processes that enable critical analysis of C&I opportunities are twice as likely to find such packages meaningful enough to break the tie. Whether the benefits are negotiated or legislated, active companies can create competitive advantage by building processes that enable them to identify, model, compare and ultimately make the most of available C&I opportunities.

Opportunities abound

Model: always/often? Deciding factor?

Overall 38% 26%

Active 89% 55%

Location decisions: How often do you “model” C&I; how often do such incentives make the difference?

Overall

Aggressive growth (more than 20%) 8%

Strong growth (10%-20%) 22%

Moderate (5%-10%) 37%

Flat (0%-5%) 22%

Decline/not sure 10%

What are your plans for capital expenditures?2

2. Just over half of this investment will be made in the U.S. (approximately 53% ─ calculated using the midpoints of ranges).

Business conditions today mean a growing number of companies are facing significant “siting” decisions. Again, the Ernst & Young LLP US Investment Monitor for 2015 provides solid evidence of such growth. Adding further support, the survey shows that two-thirds of organizations are forecasting and pursuing significant capital expansion. This breaks down to 8% seeing aggressive growth (more than 20% increase in investment), 22% strong growth (10%-20%) and 37% moderate (5%-10%).

High levels of capital spending lead to more site-focused decisions. Choosing where to expand — where to invest additional capital in facilities and personnel — should be informed by greater insight into the relative availability of the full spectrum of C&I.

As for which parts of the world such investment will take place, 45% of firms say that 75% of investment will be in the US; 10% say one-half to three-quarters will be in the US. But extrapolating from these ranges, it is also clear that just under half of total investment will be outside the US. This highlights the importance of making strides to analyze the nature and degree of C&I available from jurisdictions outside the US. Yet only 22% of companies are active in capturing international tax credits and business incentives,

5Location investment, credits and incentives survey |

Where will capital investment take place?

Overall

Greater than 75% in the US 45%

Greater than 50% to 75% in the US 10%

Greater than 25% to 50% in the US 11%

Greater than 5% to 25% in the US 10%

0%–5% in the US 24%

Where outside of the US do you anticipate significant capital investment?

Overall

Western Europe 25%3

Eastern Europe 12%

Asia/Pacific 32%

Central/South America 24%

Canada 25%

Other regions/nations 8%

3. Forty-six percent among “aggressive growth” companies — note, however, that in terms of total non-US investment, this group is in line with the overall sample.

Here, companies should be candid about their challenges and work closely with government officials to identify opportunities of mutual interest and benefit. Many governments will offer incentives for retaining jobs in addition to the net new jobs created if it means that the consolidated operation will remain in their jurisdiction.

Finally, 20% of survey participants say they have been active in pursuing “sustainable” C&I, the sorts of tax and incentive benefits that stem from investments in materials or energy efficiency like LEED-certified facilities, solar power or co-generation. Five percent of respondents say they plan to remain very active in this regard, which raises the question: what about the remaining 95%?

4. This heading, used throughout this research, represents the 10% of firms that indicate they are very active in C&I.5. “Growth-oriented” refers to firms indicating they are in pursuit of aggressive growth.6. “Sustainability-focused” refers to firms indicating they are pursuing environmentally-friendly and related socially responsible strategies.

How active are the various subgroups?

Overall Active4 Growth-oriented5

Sustainability-focused6

Very active 10% 100% 17% 24%

Active 36% 37% 52%

Moderately active

40% 33% 24%

Not active 15% 14% 0%

*Totals may not add up to 100% due to rounding

compared with the 46% of companies that are active in overall C&I opportunities. Though this may add significant complexity, the benefits can also be significant.

In addition to capital expenditures, many EY clients are in the midst of consolidating operations and M&A activity, endeavors that often lead to questions about where to move which activities.

6 | Location investment, credits and incentives survey

Business insight: key trends in location investment

Q&A with Ernst & Young LLP Incentives professionals Brian R. Smith, Principal, National Location Investment Incentives Leader, and Leslie Hobson, Senior Manager, Location Based Investment Services — Credits and Incentives

What are the trends in site selection relating to C&I? Smith: “Rationalization and M&A activities are on the upswing. More often than not, such activity leads to consolidating facilities to optimize the overall organizational footprint. Although the US economy is performing better than most countries, uncertainty in emerging markets and a strong dollar are pressuring many companies towards enterprise reductions. For example, we are seeing consolidations of facilities and/or reduction in overall headcount. Companies are being pressured by their shareholders and market forces to enhance their operations and control costs — but with the least amount of disruption to the company.”

How does this impact C&I planning?Hobson: “Business formation changes such as rationalizations, M&A and investment activities create opportunities to proactively identify and secure incentives. Governments and economic development officials recognize the necessity of working with companies to encourage them to maintain and/or grow their footprint in their jurisdiction(s). As such, incentives offered by a given jurisdiction can play a pivotal role in the overall financial and operational decision-making process of company executives.”

What sorts of programs are clients accessing? Smith: “There’s no question governments are seeking to attract or retain key businesses, and that can lead to significant incentives opportunities. Certainly, active companies are looking closely at state and local programs — but also federal — to see what might be available. But it’s very important to understand a shift taking place, which is away from ‘as of’ or strictly legislated programs to more discretionary incentives. To act more boldly and swiftly, governors and economic development leaders increasingly have access to more closing funds, which can not only speed the process but also lead to some flexible or creative opportunities.

“In general, companies need to work with state and local officials and to proactively identify those incentives or policy changes that are of the most interest and value to the company. Oftentimes, working with an economic development team, a business plan can be tweaked in ways to improve eligibility and benefits, creating a win-win outcome.

“One key issue to bear in mind: in the case of downsizing, companies need to evaluate whether or not there could be clawback relating to existing incentives. This is an area that, for many, is too easy to overlook.”

This suggests that three groups warrant closer attention in regard to their approach to and use of C&I:

• Active companies: About half of companies — 46% — say they are either very active (10%) or active (36%) in the pursuit and utilization of C&I. Only 22% say they are active (3%) or very active in the pursuit of overseas C&I. The 10% that say they are very active are referred to as the “active” group throughout this research.

• Growth-oriented companies: This category includes the 30% of companies that say they expect annual growth in capital expenditures and expansion of 10% or more. About half of these

companies are also active companies as described. Note that 10% of growth-oriented companies say that while they are not active or very active today, they recognize that their companies are missing out on significant opportunities.

• Sustainability-focused companies: This group comprises those companies indicating that they are active in investments in sustainable assets. Note: these companies are even more likely than the growth-oriented group to say they are very active in C&I.

7Location investment, credits and incentives survey |

Business insight: key trends in tax creditsQ&A with Ernst & Young LLP Incentives professionals Leigh G. Messina, Partner, National Director of Tax Credits, and Phil S. Hurak, Senior Manager, Indirect Tax

What are the key trends in tax credits?Hurak: “There are four primary areas that trigger tax credits: employment, investment, R&D and training. The big tax credits today at the federal level are the work opportunity tax credit (WOTC), federal empowerment zones, and various R&D and sustainability credits/deductions. As for state and local, each jurisdiction has its own specific focus of activities it wants to incentivize through tax credits. Jurisdictions are using tax credits to attract and retain the types of businesses that are best suited for the local economies. Because of this extreme geographic and business diversity — varying objectives, eligibility, calculations and flexibility — companies need to do their homework to make certain they understand and are accessing all that can be made available.”

How can companies improve their performance in tax credits? Messina: “It starts with executive leadership — tax leadership should be aware of how tax credits can impact the company. But whatever team takes the lead on C&I — usually tax but it

might also be a group like real estate or government affairs — that group needs to be engaged early on when business decisions are still under consideration. The tax team or that group with responsibility for C&I can then provide input and analysis of the potential business activity and opine on potential tax credit benefits. But doing this effectively requires the tax team to communicate and coordinate with a range of other functions within the business. Often we see a coordinated effort between HR, payroll, R&D, logistics, finance, legal, operations and others to understand what’s happening. From there, it’s a matter of digging in to identify and evaluate potential opportunities. Given so many programs at the federal, state and local level, it can be complicated, but the opportunities are everywhere.”

Any other suggestions to improve tax credit performance? Hurak: “Two suggestions. First, companies that have not been active in reviewing potential tax credit opportunities based on business activities should and can often review retroactively for potential refund opportunities as many tax credit programs are refundable in nature. Second, companies should take an active role in compliance and tracking of tax credits — both to ensure the benefit is received but also to provide management with reporting that shows the value provided through research and diligent oversight.”

8 | Location investment, credits and incentives survey

Emulating best practices

Overall ActiveGrowth-oriented

Sustainability-focused

Very aware 22%7,8 61% 38% 30%

More aware than two years ago

19% 19% 22% 27%

Only somewhat aware

43% 17% 21% 42%

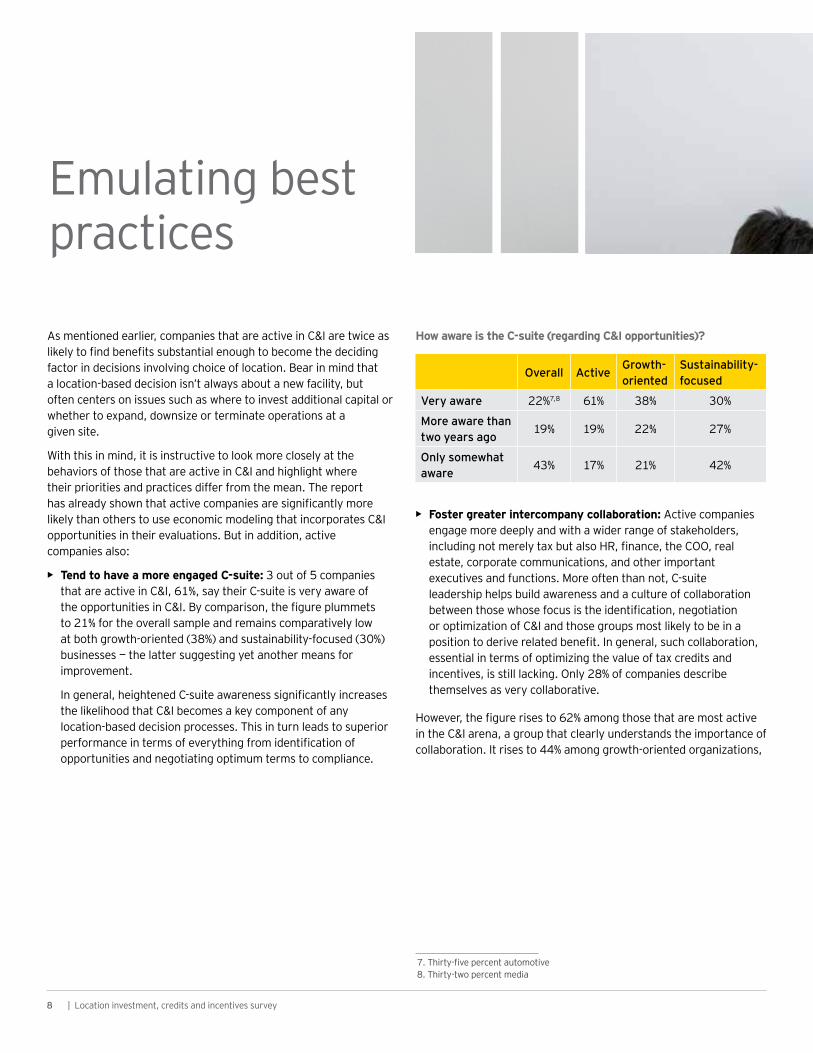

How aware is the C-suite (regarding C&I opportunities)?As mentioned earlier, companies that are active in C&I are twice as likely to find benefits substantial enough to become the deciding factor in decisions involving choice of location. Bear in mind that a location-based decision isn’t always about a new facility, but often centers on issues such as where to invest additional capital or whether to expand, downsize or terminate operations at a given site.

With this in mind, it is instructive to look more closely at the behaviors of those that are active in C&I and highlight where their priorities and practices differ from the mean. The report has already shown that active companies are significantly more likely than others to use economic modeling that incorporates C&I opportunities in their evaluations. But in addition, active companies also:

• Tend to have a more engaged C-suite: 3 out of 5 companies that are active in C&I, 61%, say their C-suite is very aware of the opportunities in C&I. By comparison, the figure plummets to 21% for the overall sample and remains comparatively low at both growth-oriented (38%) and sustainability-focused (30%) businesses — the latter suggesting yet another means for improvement.

In general, heightened C-suite awareness significantly increases the likelihood that C&I becomes a key component of any location-based decision processes. This in turn leads to superior performance in terms of everything from identification of opportunities and negotiating optimum terms to compliance.

7. Thirty-five percent automotive8. Thirty-two percent media

• Foster greater intercompany collaboration: Active companies engage more deeply and with a wider range of stakeholders, including not merely tax but also HR, finance, the COO, real estate, corporate communications, and other important executives and functions. More often than not, C-suite leadership helps build awareness and a culture of collaboration between those whose focus is the identification, negotiation or optimization of C&I and those groups most likely to be in a position to derive related benefit. In general, such collaboration, essential in terms of optimizing the value of tax credits and incentives, is still lacking. Only 28% of companies describe themselves as very collaborative.

However, the figure rises to 62% among those that are most active in the C&I arena, a group that clearly understands the importance of collaboration. It rises to 44% among growth-oriented organizations,

9Location investment, credits and incentives survey |

and to 48% of sustainability-focused companies. Of companies describing themselves as not very collaborative/coordinated, half say they have plans in place to improve matters.

No matter which groups form the core team leading collaboration within C&I, companies must be certain to use both tax savings and cash incentives in the ROI analysis. Teams that are driven solely or primarily by the tax department may have a tendency to overlook or undervalue cash incentives and grants (since tax is often evaluated based on the overall tax rate).

• Engage significantly earlier in the process: Enormous benefits are associated with beginning C&I analysis early on. For starters, early insight provided to decision-makers can often lead to significantly better decisions and outcomes. Sometimes, simply being made aware of potential benefits like job training credits or tax abatements can have a dramatically positive impact on planning. Also, as those on the ground gain more time to investigate, negotiate and evaluate competing options and offers from various state, local and even federal programs.

Again, active companies demonstrate best practices, with 60% indicating that C&I issues enter discussions right at the beginning of planning processes — more than twice the rate of the overall sample. Growth-oriented companies are slightly more likely than average to do so; sustainability-focused companies are significantly more likely. As the active group demonstrates, though, all leave room for significant improvement.

Overall ActiveGrowth-oriented

Sustainability-focused

Very collaborative/coordinated

28% 62% 44% 48%

Collaborative 48% 36% 42% 39%

Not collaborative/plan to improve

11% 2% 4% 12%

Not at all collaborative/don’t know

14% 0% 10% 0%

How collaborative/coordinated is your company in pursuing C&I opportunities?

At what point in the decision process do C&I issues enter the equation?

Overall Active Growth Sustainability-focused

Beginning of the process

27% 60% 34% 45%

Later in the process

30% 24% 16% 23%

Not engaged or after the fact

42% 16% 50% 32%

10 | Location investment, credits and incentives survey

Business insight: key trends in sustainabilityQ&A with Ernst & Young LLP Incentives professionals Dominick Brook, US Leader of Sustainability Tax Services, and Andrew Soulier, Senior Manager, Sustainability Tax Services

What is happening in energy, environment and related sustainability-focused investments? Brook: “We’re seeing increasing interest and in general, very strong growth across the board — driven by a range of factors. One driver, of course, is the continuing push for corporate social responsibility and the desire to be a good corporate citizen. Another driver, though energy costs are down at the moment, businesses know this can’t last and see investments in energy efficiency as a way to reduce future costs. With the remarkable progress in sustainable technologies, the return on investment of such projects make them attractive all by themselves. Moreover, there are significant regulatory actions, such as current environmental taxes and proposed carbon regimes, that are driving companies to think more in terms of sustainability.”

What sorts of sustainability investments are proving most attractive? Soulier: “Traditionally the lowest-cost, highest-visibility investments were favored to support brand strategy, but companies are now going beyond simple lighting retrofits and

power purchase agreements, digging deeper for long-term cost savings and risk reduction. Different options will look better or worse based on geographic location, and there are currently hundreds of active incentives covering the vast majority of energy efficiency and energy generation technologies. Unfortunately, many projects are deemed unattractive when teams fail to identify all available federal, state, local and utility incentives. In all cases, tax and incentive impacts will influence the ranking of investment options and the regions in which to prioritize. Further, companies that track energy and water across their portfolios are better positioned to target their most attractive projects, as opposed to approving capital requests on a site-by-site basis. Note that many sustainability incentive programs will pay out higher amounts for early application — yet another reason to include incentives in the earliest stages of decision-making.“

How should companies approach such opportunities? Brook: “Building, renovating, improving operations, innovating — technologies have evolved and there are so many incentive programs that any sustainability-related projects absolutely need to include a fresh look at the economics and overall opportunities. And absolutely — tax needs to be at the table right alongside the real estate, sustainability or operations teams. Moreover, companies need to make sure their tax teams have adequate resources to investigate, scrutinize and access the various grants, credits and other programs that can be accessed.”

11Location investment, credits and incentives survey |

“How often do you pursue9 ... ?”

Frequently Occasionally Total

Active 51% 23% 74%

Overall 20% 26% 46%

Frequently Occasionally Total

Active 25% 27% 52%

Overall 13% 11% 24%

Frequently Occasionally Total

Active 51% 21% 72%

Overall 27% 15% 42%

Frequently Occasionally Total

Active 52% 19% 71%

Overall 21% 21% 42%

Frequently Occasionally Total

Active 40% 23% 63%

Overall 17% 18% 35%

Frequently Occasionally Total

Active 19% 25% 44%

Overall 6% 14% 20%

Property tax abatements

International R&D incentives

WOTC

Investment tax credits

Enterprise zone credits

Enterprise zone credits

9. The findings are similar for all forms of grants and tax credits across the spectrum of investing, hiring, low-income or historic housing, new markets, R&D, training and related C&I categories.

• Devote greater staffing: Without experienced people focused on the right issues, C&I opportunities can fall by the wayside. Here, 4 out of 5 companies, 81%, devote fewer than one full-time equivalent (FTE) to the pursuit of C&I (see Chart 1).

By contrast, the number having one FTE or less falls to 47% among active companies. From there, 32% of active companies have one to three FTEs engaged in C&I activity, and 21% have three or more. Note that even growth-oriented and sustainability-focused organizations appear to have lighter staffing than the most active in the survey, possibly pointing to a deficiency in these organizations.

Similarly, as opposed to relying solely on internal or solely on external sources of C&I insight, active companies are significantly more likely than the rest to rely on a combination of outside vendors and in-house resources. For example, overall, almost 1 in 5 companies, 18%, rely exclusively on outside vendors — compared with only 7% of active companies.

• Create access to a wider and more valuable range of C&I opportunities: Not only are active firms more than twice as likely to model C&I opportunities within their investment decision-making (noted earlier), they are similarly much more likely to benefit from such programs. From tax abatements and work opportunity tax credits (WOTC) to federal sustainability initiatives and international research and development (R&D) grants and credits, companies that are active in C&I access such programs far more often than companies at large. The result: significant savings and related advantages for their companies.

Chart 1: How much staff is devoted to C&I?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Overall Active Growth-oriented Sustainability-focused

Less than one FTE One to three FTEs More than three

Q&A with Andrew D. Phillips, Principal, Quantitative Economics & Statistics (QUEST), Ernst & Young LLP

What is the general financial health of national, provincial and state, and city government C&I programs around the world?

“The answer depends on the geography in question. The US economy and tax collections remain fairly strong by many measures, while a good number of economies in the Americas have been impacted by falling commodity prices and slowing growth in China. Outside the US, revenue has slowed with some countries moving into recession.” What is the state of competition among these nations, states and cities in terms of attracting and retaining businesses?

“Competition seems to continue, especially for the largest and most strategic projects. That said, there has been an increasing awareness that winning a competition for a new project often comes at a significant up-front cost to taxpayers, and an increasing number of states have mandated more comprehensive benefit and cost reporting and analysis. Some states, like California, have restructured their incentive programs to increase their discretion in awarding incentives. Many others have reexamined their use of special industry credits, such as film production tax credits.”

What advice would you give to nations, states and cities in terms of improving their long-term attractiveness to companies?

“In the current fiscal year, many US state budgets have focused on increasing funding to education, which is a reasonable long-term investment to increase a jurisdiction’s competitiveness. For most companies and types of facilities,

labor cost and quality is the most important factor in the location decision, and increasing the supply of qualified labor will increase the long-run attractiveness of a jurisdiction.

“Another effective approach is the provision of a competitive tax system. Many jurisdictions, including Canada and several US states, have reduced general corporate tax rates to increase competitiveness, rather than relying on a more complex system of targeted tax incentives.” What advice do you have for improving effectiveness of incentive programs?

“Jurisdictions should be focused on maximizing the economic impact of projects receiving incentives and the benefits to taxpayers of their economic development programs by incentivizing marginal investments that would not occur in the absence of an incentive. While satisfying the ‘but-for’ test is often cited as evidence that a project provides a marginal benefit, the marginal benefit of providing a financial incentive compared with an alternative use of the funds is not always clearly understood. Highly mobile, export-focused projects are the most likely to generate significant economic benefits for a jurisdiction — as compared with population-serving projects like retail or personal services. Similarly, projects that require deep, local supply chains and pay high wages will create the greatest economic benefits.

“Another basic question that remains unresolved in many debates about the role of incentives in economic development policy is the definition of ‘effective.’ Some would argue that the most effective credits are those which generate the highest return to the public sector in the form of higher tax revenues. Others view the goal of incentive programs as providing benefits to the private sector, including job creation, income creation and investment attraction. Although each of these objectives could be considered worthy, policymakers should clearly understand the objectives of the programs to achieve the desired result.”

Business insight: the evolution of global C&I programs

12 | Location investment, credits and incentives survey

13Location investment, credits and incentives survey |

14 | Location investment, credits and incentives survey

Should your company ratchet up its C&I efforts? The research shows that active companies are using a more focused and coordinated approach to capturing value from C&I. Their efforts are resulting in many millions of dollars in both one-off and recurring savings, translating into stronger group performance and earnings per share. Key questions for reflection include:

• Where is our footprint likely to grow and where is it likely to contract?

• What are our current capabilities and processes for identifying and evaluating C&I opportunities?

• What group or groups take the lead in the analysis of C&I opportunities? At what point in related processes are they engaged — and is this early enough to drive informed decision-making?

• What C&I benefits are currently being obtained — are we aware of agreements already in place throughout the company? What C&I opportunities are being overlooked? (Evaluate existing footprints, future expansion/consolidation.)

• If C&I agreements are already in place in certain locations, how well are they optimized on an after-tax basis? What is our mix of tax credits and cash grants? How well are we meeting milestones as well as managing compliance?

• What resources should be added to our C&I process? Could job descriptions be expanded to include C&I? Which executives in which parts of the organization (e.g., tax, real estate, government affairs) are best suited for which C&I roles?

Conclusion: time for reflection

• What other tools, technology or external resources might be needed to improve returns from C&I?

• What level of executive sponsorship might be needed to create a more informed, collaborative and successful set of C&I processes?

• What can be done to create a more collaborative, transparent and mutually beneficial partnership with government officials?

Note that the inability to readily answer one or more of the above questions could point to significant opportunity. Bottom line:

• Companies in general need to take a closer look at C&I opportunities.

• Greater C-suite awareness can spur activity leading to greater optimization.

• To obtain a clearer picture of potential benefits — and to better coordinate group-wide efforts — initiatives need to involve functions beyond tax or finance (including operations, real estate, government affairs and HR).

• Companies should examine resources — both internal and, as needed, external — to ensure adequate C&I knowledge and coverage.

15Location investment, credits and incentives survey |

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 EYGM Limited. All Rights Reserved.

EYG no. 02477-161GblBMC AgencyGA 0000_02660

ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

EY | Assurance | Tax | Transactions | Advisory