LOCAL CHURCH AUDIT GUIDE - NGUMC

22

LOCAL CHURCH AUDIT GUIDE Providing Solutions, Sustaining Ministries www.UMCSupport.org

Transcript of LOCAL CHURCH AUDIT GUIDE - NGUMC

LOCAL CHURCH AUDIT GUIDE

Providing Solutions, Sustaining Ministries

www.UMCSupport.org

This booklet is given to you as a service of the Committee on Audit and Review of the General Council on Finance and Administration of The United Methodist Church (GCFA). We hope you will find it useful. If you have concerns or suggestions, please contact us at:

General Council on Finance and Administration1 Music Circle NorthNashville, TN 37203

Main Phone Number: (615) 329‐3393 Toll Free Number: (866) 367‐4232 Fax: (615) 329‐3394Email: [email protected]

DISCLAIMER

The General Council on Finance and Administration and the Committee on Audit and Review are not responsible for the conduct of local church audits, nor do they provide legal or financial advice to local churches through this booklet. Local churches should seek assistance and advice from their local advisors when specific issues arise. This booklet is provided to you as a service; it should be used to increase the knowledge of auditing principles within your local church, including the understanding of why audits should be conducted and the uses to which they can be applied to local church officials.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 1 OF 20

TABLE OF CONTENTS

Introduction .................................................................................................................................................................. 3

Key Definitions ........................................................................................................................................................... 3

Selecting an Auditor .............................................................................................................................................. 5

Purpose of an Audit ................................................................................................................................................ 6

Groups to Be Included in the Audit ............................................................................................................7

Information Required ............................................................................................................................................ 8

Confidential Information ..................................................................................................................................... 8

Conducting the Audit ............................................................................................................................................ 9

Internal Controls Review .................................................................................................................................... 9

Receipts and Disbursements ....................................................................................................................... 10

Reporting and Review ....................................................................................................................................... 10

Tax Reporting Requirements ........................................................................................................................ 10

Other General Requirements .........................................................................................................................11

Auditor’s Written Report .....................................................................................................................................11

Audit Report Preparation ..................................................................................................................................12

Appendix A: Recommended Procedures............................................................................................ 13

Appendix B: Internal Control Checklist ................................................................................................. 18

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 2 OF 20

LOCAL CHURCH AUDIT GUIDEFifth Edition

INTRODUCTION

The United Methodist Book of Discipline (the “Discipline”) assigns the responsibility for the annual audit of financial records to the committee on finance. The committee “shall make provisions for an annual audit of the financial statements of the local church and all its organizations and accounts. The committee shall make a full and complete report to the annual charge conference” (¶258.4d). The purpose of this audit guide is to assist the committee in its work.

KEY DEFINITIONS

A local church audit – an independent evaluation of the financial reports and records of the internal controls of the local church by a qualified person or persons for the purpose of reasonably verifying the reliability of financial reporting, determining whether assets are being safeguarded, and whether the law, the Discipline, and policies and procedures are being complied with.

Audit – the term is used in the Discipline, is meant to be a process that provides reasonable assurance that good stewardship is being used in handling and accounting for the funds and other assets of the local church. The ultimate goals of the audit include:

• Protection for the persons the local church elects to offices of financial responsibility from unwarranted charges of careless or improper handling of funds;

• Trust and confidence of the financial supporters of the church in the way their money is being accounted for (trust and confidence lead to improved patterns of financial support);

• Fiscal responsibility to assure that through turnover in personnel there will be continuity in accountability and transparency; and

• Assurance that gifts made to the church with restrictions attached are consistently administered in accordance with the donors’ instructions and to provide checks and balances for funds received and expended.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 3 OF 20

Independent audit – The Discipline states the need for independence on the part of those conducting the annual audit. Independent means that the auditor must not be subject to control or influence by anyone who has responsibility for the financial accounts and records of the local church. There should not be even the appearance of a relationship that may dilute the perception of the independence of the auditor. An independent auditor is one who is unrelated to those with financial responsibilities in the church. If a CPA or accounting firm is chosen, the firm should be unrelated and separate from those with financial responsibilities in the church.

Internal controls – policies and procedures that are followed to help minimize financial risks by helping to deter potential fraud, detect errors or omissions and protect innocent workers.

Internal control policy – a policy prepared for a church that documents the processes and procedures to be followed to help safeguard the financial assets of the church.

Net assets without donor restrictions – net assets that are not subject to donor-imposed restrictions and may be expended for any purpose in performing the primary objectives of the church. These net assets may be used at the discretion of church leadership. Net assets with donor restrictions may be further classified with the following sub-classifications:

• Invested in Property and Equipment – represents net assets invested in property and equipment, net of accumulated depreciation.

• Designated – assets that have been voted by the local church’s governing board, such as its church, council or equivalent body, to be used for a particular purpose. Because the stipulation for its particular use was made by the church itself, that stipulation (or designation) can be changed by the action of the body that put it in place.

• Undesignated – represents the cumulative net assets without donor restrictions excluding those net assets invested in property and equipment and designated for specific activities.

Net assets with donor restrictions – net assets subject to stipulations imposed by donors and grantors. Some donor restrictions are temporary in nature; those restrictions will be met by actions of the church or by the passage of time. Other donor restrictions are perpetual in nature, whereby the donor has stipulated the funds be maintained in perpetuity.

Trust clause – The Discipline ¶2501 states that “all properties of United Methodist local churches and other United Methodist agencies and institutions are held, in trust, for the benefit of the entire denomination, and ownership and usage of church property is subject to the Discipline.” When conducting an audit, the auditor should assess any impact of ¶2501 on the information to be presented in the audited annual financial statements or in the results of other procedures

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 4 OF 20

performed. (Refer to recommended procedures for item 6. “Church Property” on pages 14 and 15.)

SELECTING AN AUDITOR

The type of auditor selected and the type of audit performed at each church each year will be dependent on the amount of funds received by the church. In general, the following guidelines should be used to determine the type of audit that should be performed each year as well as the type of auditor who should perform the audit (i.e. if a certified public accountant firm should be hired to perform the audit or if an independent volunteer will be adequate):

1. For churches that are considered very small (e.g., those with 10 to 20 members and with minimal funding and asset balances), the processes and internal controls in place may vary greatly. For those churches, an independent qualified member of the church or other volunteer from another church can perform audit procedures and evaluate internal controls and report the results directly to the church’s finance committee. The recommended procedures included in Appendix A of this guide should serve as example procedures that may be performed. Depending on the nature of the church activities and assets, many of these procedures may not be relevant and as such, may not need to be performed. In addition, other procedures may be considered necessary based on the nature and activities of each specific church. In addition to the financial transaction procedures, the auditor should assess the design of the church’s internal controls (see Appendix B for an internal control checklist to be completed). While smaller churches may not have ideal internal controls in place, church leadership should work to implement internal controls in key risk areas to help ensure assets are not misappropriated or misused and errors are detected quickly.

2. For churches with less than $500K in receipts, an independent qualified member of the church or other volunteer can perform audit procedures and evaluate internal controls and report the results directly to the church’s finance committee. The recommended procedures included in Appendix A of this guide should serve as the minimum expected financial transaction procedures. Other procedures may be considered necessary based on the nature and activities of each specific church. In addition to the financial transaction procedures, the auditor should assess the design of the church’s internal controls (see Appendix B for an internal control checklist to be completed).

3. For churches with between $500K and $1M in receipts, the recommended procedures outlined in Appendix A or a financial statement audit conducted in accordance with generally accepted auditing standards (GAAS) should be completed and reported on by an external Certified Public Accountant (CPA)every three years. If the recommended procedures are performed by the CPA, the

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 5 OF 20

procedures would be performed as part of an Agreed Upon Procedures (AUP) engagement. As part of either type of engagement, the auditor would be expected to communicate any internal control deficiencies that are identified during the audit procedures.

In the alternate years, a review similar to number one in this list should be conducted. A volunteer or member of the church could perform and report on the procedures and perform the internal control evaluation.

4. For churches between $1M and $2M in receipts, a financial statement audit conducted in accordance with GAAS should be completed and reported on by an external CPA at least every two years. An agreed upon procedures engagement is not permitted in the place of the GAAS audit.

Similar to #2 above, in the alternate years when the GAAS audit is not performed, a volunteer or member of the church could perform and report on the recommended procedures and perform the internal control evaluation.

5. For churches with receipts greater than $2M, an external financial statement audit conducted by an independent CPA in accordance with GAAS should be performed every year. Any identified internal control deficiencies should be reported by the independent CPA. An agreed upon procedures engagement is not permitted in the place of the GAAS audit.

Each of the scope amounts included above should be calculated as the average for each of the last three fiscal years for the church. Further, the applicable procedure or audit reports should be presented within six months of the fiscal year end.

THE PURPOSE OF AN AUDIT

The purpose of an audit is the summation of the items presented below:

• Independently verify the reports of the treasurer(s) and financial secretary.• Follow the money and test how it is treated at different steps.• Document that donated and earned funds of the congregation have been

used as stipulated by the donors.• Reviews accounting controls (systems that reduce the possibility of

loss, embezzlement or errors).• Segregation of duties (assurances that more than one person is involved in critical

steps in handling money so that there can be checks and balances).• Reasonableness of systems and procedures in the light of all factors, including

the size of the church and its budget.• Records that show donors’ stipulations for the use of gifts made to the local church.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 6 OF 20

It should be noted that a “review” or “compilation” performed by an independent CPA is not considered an acceptable form of an “audit.” Both of these types of engagements are significantly less in scope than an audit performed in accordance with professional standards. A “review” only requires the auditor to perform inquiry and analytical procedures. Confirmation of balances and detailed testing are not performed. A “compilation” is simply the compilation of data provided by the church. No actual testing is performed. Both a “review” and “compilation” offer very limited assurance on the accuracy of the underlying financial statements. For these reasons, neither should be performed in the place of an actual audit (or the recommended procedures outlined in this guide).

In addition, the following information should be presented to the audit or finance committee of the church for their consideration:1

• Adequacy of insurance coverage.• Systems for retaining and accessing meeting minutes that have financial

implications (i.e. Finance Committee, Trustees, Charge Conferences).

A local church’s unique circumstances may suggest that additional steps should be taken. It is important to document the financial processes of your particular local church.

1For larger churches only being subjected to a GAAS audit, these items may not be reviewed by the external financial statement auditor. If not, church leadership should review this information internally and provide it to the finance or audit committee.

GROUPS TO BE INCLUDED IN THE AUDIT

We Methodists are instructed by the Discipline to audit not only the financial offices of the local church, but “all its organizations….” That means that the treasuries that are to be audited include:

• Trustees, if their funds are held separately• Memorial Funds (if any)• Local Church Foundation or Endowment funds• All other separate treasuries or bank accounts maintained by a group using the

same employer’s tax identification number as the church, including, for example:o United Methodist Meno Pastor’s discretionary fundo United Methodist Youth fundo Church schoolo Others

In addition, the accounts held by the United Methodist Women (UMW) at each church should be audited each year. UMW funds are different from other church offices

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 7 OF 20

in that, according to the Discipline, they are owned by the UMW local unit and are not owned by the local church. Consequently, the funds should not be consolidated with all other funds. The financial reporting, procedures performed, and results of procedures performed should be presented separately.

INFORMATION REQUIRED FOR THE AUDIT

For audits performed by a qualified member of the church or other volunteer, the person(s) must obtain access to the following information and materials (at a minimum) during the audit:

1. Copies of all church policies and procedures related to finance and treasury functions and copies of minutes approving those policies.

2. Copies of all minutes from the finance committee, the trustees, the administrative board, the previous charge conference(s), and any other entity listed on the prior page.

3. Listing of all bank and investment accounts, including the person authorized to sign on each, and including any special use accounts under the control of the pastor(s) and in the name of the church.

4. All financial statements for each month of the year, plus December of the prior year and January of the subsequent year (a fourteen month period).

5. Bank and investment account statements for the same period.6. Bank reconciliations for that same period.7. Original books of entry, which will be the general and subsidiary journals; for

those books that are computerized, a print‐out of all transactions by account for the entire year.

8. All paid invoices, payroll data and files (including 941’s, year‐end W‐2’s, 1099’s and transmittal forms), income transmittals and deposit records for the 14-month period.

9. The Financial Secretary’s records and other income records for the same period.10. Access to the deeds and other related supporting documentation for all real property

owned by the church.

For audits performed by an independent external auditor, similar information will be requested.

CONFIDENTIAL INFORMATION

The person(s) conducting the audit may obtain access to confidential information and must treat that information accordingly. The auditor’s work papers may contain confidential information. These work papers as well as all financial records should be retained for at least seven years in a secure, limited access, storage area.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 8 OF 20

CONDUCTING THE AUDIT

As discussed above, the audit may be performed via the following based on the amounts of the funds received (averaged over the prior three years):

Procedures conducted by an independent member of the church or volunteer.Procedures conducted by an independent accountant hired by the church.Financial Statement Audit performed by an independent CPA hired by the church.

For recommended procedure evaluations, the auditor (either a volunteer or CPA) should meet with church leadership (including the finance or audit committee) and determine the procedures to be performed to ensure all necessary financial information is included in the scope of the procedures. It is worth noting that church leadership will be responsible for identifying all financial information and processes to be included in the scope of the procedures. As part of an AUP engagement, the auditor should work to understand the church’s internal controls within the processes being audited and then communicate any deficiencies identified during the performance of the procedures.

For financial statement audit engagements, the CPA will conduct the audit in accordance with generally accepted auditing standards to obtain reasonable assurance that the financial statements are not materially misstated. As part of the audit, the CPA will communicate any significant internal control deficiencies identified during the audit.

INTERNAL CONTROLS REVIEW

As part of the audit, it is essential that the internal control structure for receipts and disbursements procedures be reviewed regardless of the size of the church. The internal control structure is the process that assures the local church’s operational efficiency and effectiveness, that its financial reporting is reliable, that it is complying with the Discipline and with laws, and that its assets are safeguarded. The internal control process should be in place on paper as well as in practice. Internal control systems that are only policy and are not enforced are no better than having no system at all.

The following guidelines are intended to assist those with financial responsibilities in local churches to identify and implement basic internal control procedures. These minimum standards should be increased for churches with higher volumes of transactions and should be considered for lower volumes of transactions. Ideally, all local churches will meet these minimum standards and these procedures should be reviewed to ensure practice of each of these during the annual evaluation.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 9 OF 20

RECEIPTS AND DISBURSEMENTS

Treasurer and Financial Secretary should not be the same person and should not be in the same immediate family residing in the same household.

Counting team (at least two unrelated persons) should count offerings and document totals – not treasurer and not financial secretary.

Offerings should be deposited the same or next business day.Offering count details should be given to financial secretary for recording.Offering totals should be given to the treasurer or financial secretary to record deposit.The Financial Secretary’s deposit log should be compared to the bank

statement to verify deposits (by bank reconciliation reviewer).At least two persons should be listed as authorized signatures on all accounts.

This should also be the case for setting up electronic payments (or EFTs). For EFTs, one of those individuals should be a Trustee or a member of the Finance Committee (other than the Secretary or Treasurer).

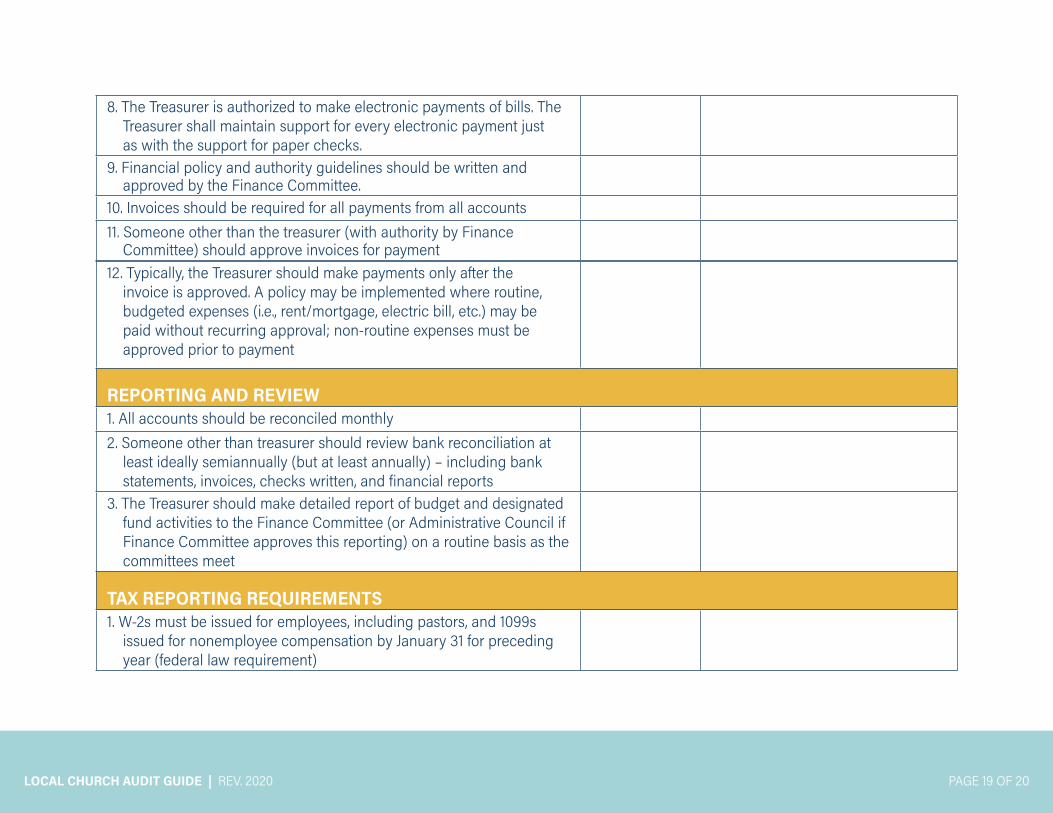

The Treasurer is authorized to make electronic payments of bills. The Treasurer shall maintain support for every electronic payment just as with the support for paper checks.

Financial policy and authority guidelines should be written and approved by the Finance Committee.

Invoices should be required for all payments from all accounts.Someone other than the treasurer (with authority by Finance Committee)

should approve invoices for payment.Typically, the Treasurer should make payments only after the invoice is

approved. A policy may be implemented where routine, budgeted expenses (i.e., rent/mortgage, electric bill, etc.) may be paid without recurring approval; non‐routine expenses must be approved prior to payment.

REPORTING AND REVIEW

All accounts should be reconciled monthly.Someone other than treasurer should review bank reconciliation at least

semiannually – including bank statements, invoices, checks written, and financial reports.

The Treasurer should make detailed report of budget and designated fund activities to the Finance Committee at least quarterly.

TAX REPORTING REQUIREMENTS

W‐2s must be issued for employees, including pastors, and 1099s issued for nonemployee compensation by January 31 for preceding year (federal law requirement).

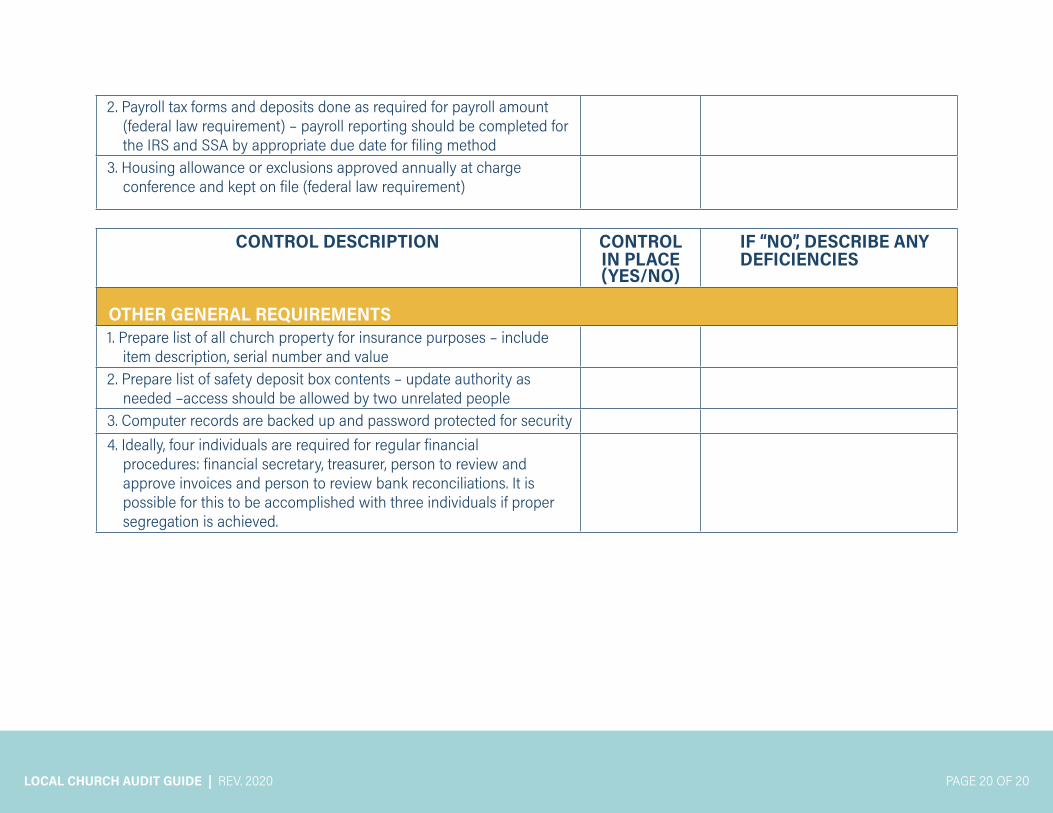

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 10 OF 20

Payroll tax forms and deposits done as required for payroll amount (federal law requirement) – payroll reporting should be completed for the IRS and SSA by appropriate due date for filing method.

Housing allowance or exclusions approved annually at charge conference and kept on file (federal law requirement).

OTHER GENERAL REQUIREMENTS

Prepare list of all church property for insurance purposes – include item description, serial number and value.

Prepare list of safety deposit box contents – update authority as needed – access should be allowed by two unrelated people.

Computer records are backed up and password protected for security.Ideally, four individuals are required for regular financial procedures: financial

secretary, treasurer, person to review and approve invoices and person to review bank reconciliations. It is possible for this to be accomplished with 3 individuals if proper segregation is achieved.

The steps outlined in this section have been compiled into a checklist for easier use during an audit. This checklist is included as Appendix B. When all the audit review steps have been completed, the auditor should review the work done with the church treasurer and financial secretary, endeavor to answer any lingering questions, then consider preparation of the report of the audit.

AUDITOR’S WRITTEN REPORT

The type of report provided at the conclusion of the audit will be dependent on the type of audit performed. For agreed upon procedure and financial statement audits performed by an independent CPA, professional audit standards will dictate the reporting provided by the auditor.

For audits performed by church member, the reporting ideally will provide the following, at a minimum:

1. Listing of Procedures Performed and Related Results.2. Statement of Financial Position (balance sheet or listing of all assets and liabilities

if full financial statements are not prepared for the church).3. Statement of changes in net assets (statement of activities or listing of all income

and expenses if full financial statements are not prepared for the church).4. Comments, if any, on internal control deficiencies or issues with church

procedures noted during the evaluation.

The reporting should be provided in written format to the audit committee (or finance

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 11 OF 20

committee if there is no audit committee) to disclose the results of testing and any findings or observations during the audit. The Discipline requires that the report ultimately be delivered to the Charge Conference.

AUDIT REPORT PREPARATION

While the audit report is in draft format, the auditor should meet with the audit or finance committee to discuss the audit report. The final audit report, along with any responses the finance committee may choose to add, should then be delivered to the charge conference.

If the auditor meets with either the finance committee or the charge conference, the committee should be made aware of restrictions on closed meetings in the Discipline. Although church meetings generally must be open to all, discussions with accountants and matters involving personnel issues may be held in closed meetings if confidential information is likely to be disclosed. Examples of discussions that should happen in closed session include, but are not limited to, suspicion of inappropriate use of church funds or embezzlement. Suspicions should not be discussed in open meetings. Closed meetings will include only the members of the committee that is meeting, plus any invited guests, such as the auditor or the church’s legal advisor. The committee should be aware of the manner in which closed meetings must be reported, as set out in the Discipline. The appropriate paragraph of the Discipline should be provided to the legal advisor prior to the meeting.

When the auditor has delivered the audit to the charge conference with responses of the finance committee, the audit process is finished for that fiscal year. The auditor’s findings and Report of the Annual Audit should be kept by the church permanently. The reports should be provided to the subsequent year’s audit team for review in preparation for the next audit.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 12 OF 20

Appendix ALocal Church Audit Guide

Recommended Procedures

1. Obtain a copy of (1) the previous year end’s balance sheet (statement of financial position) and “statement of income and expenses” (statement of activities) for the year then ended and (2) the balance sheet and year‐to‐date statement of income and expenses available as of the end of the current year (the “Test Period”). For both sets of statements, agree each amount on such financial statements to the corresponding amounts in the church’s general ledger. (Note: The statements used should be the same ones provided to and used by the church’s Finance Committee.)

2. Using the balance sheet as of the end of the Test Period, identify any “credit” account balances included in the “Assets” section of the church’s balance sheet or “debit” balances included in the “Liabilities” or “Equity” or “Net Assets” sections of the balance sheet. For all such balances identified, obtain an explanation from the church’s accountant of the nature of the account and why it has a “credit” (for asset accounts) or “debit” (for” liability” or “net assets” accounts) balance. Summarize such explanation(s) in your report to the finance committee.

3. If the balance sheet at the end of the Test Period reflects an accumulated deficit, ask the church’s accountant to explain the source or sources of the funding for that deficit, and provide the explanation in the final report to the Finance Committee. (Note: sources of funding for the deficit might include one or more of the following: bank borrowings, negative working capital (e.g., accounts payable and other short‐term liabilities exceed cash balances), restricted assets used to support ongoing church operations).

4. Cash balances ‐ Obtain copies of the monthly bank statements and corresponding bank reconciliations for each church bank account for the end of the Test Period and for one other month end during the Test Period, and perform the following:

a. Agree the “balance per bank” from the reconciliation to the corresponding ending balance of the bank statement, and the “balance per books” (or general ledger) to the corresponding amount in the church’s general ledger.

b. Obtain written confirmation of such balances directly from the bank or banks.c. If there are deposits in transit included in the bank reconciliations, agree such amounts

to the following month’s bank statements. If such deposits are not recorded by the bank in the church’s bank statements in the following month within three business days following the preceding month end, obtain an explanation for the delay from the church’s accountant, and include that explanation in the final report to church’s Finance Committee.

d. If there are outstanding checks included in the reconciliations, select fifteen checks from the following month’s bank statement(s) that have dates on or before the date of the end of the bank reconciliation tested. Agree the amounts of selected checks to the corresponding outstanding check amounts included in the list of outstanding checks included in the bank reconciliation being tested. (For example, to test the completeness of the list of outstanding check list used in the bank reconciliation for December 2019, select checks from the January 2020 bank statement with dates on or before December

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 13 OF 20

31, 2019) and agree them to the corresponding amounts included on the December 2019 bank reconciliation.)

e. Prove the mathematical accuracy of the total dollar amount of outstanding checks included in the bank reconciliation(s) by adding the list(s) of outstanding checks and agreeing that amount to the total amount used in the bank reconciliation(s).

f. Include a listing of outstanding checks that have been outstanding more than six months in your final report to the Finance Committee.

g. Obtain an explanation of any other reconciling items used in the bank reconciliation(s), and include the explanation of any significant reconciling items in the final report to the Finance Committee.

h. Agree each General Ledger cash balance as of December 31 of the prior year (for example, if these procedures are performed in 2020, use balances as of December 31, 2019) to the corresponding year‐end cash amount included in a copy of the church’s signed “cash” report filed with the Conference office.

5. Investments – Obtain a listing of individual investments comprising the balance or balances of any investments included in the church’s balance sheet as of the end of December of the previous year and as of the end of the Test Period, and perform the following procedures as of the end of the Test Period (It would be unusual if the church has no “investment” account(s)). At least a small number of members in larger churches sometimes give stocks or bonds to their churches in lieu of or in addition to cash gifts due to the tax advantages associated with such gifts. However, if the Church does not have such account or accounts, skip this step.):

a. Add the individual investment amounts comprising each investment account included on the Church’s balance sheet, and agree each such amount to the corresponding amount in church’s balance sheet.

b. Agree the amount of each individual investment on the listing to the corresponding amount on the appropriate reports received from the investment custodian(s) or trustee(s) used by the Church.

c. Obtain written confirmation of all investment balances from the investment custodian(s) or trustee(s), including the number of shares or bonds held for each security, the cost basis for each security, and the market value for each security as of the end of the testing period.

d. Select five “withdrawal” transactions at random from the monthly or quarterly investment reports received from the investment trustee(s) or custodian(s) for the Test Period. Agree the proceeds from such withdrawals to corresponding deposits recorded in the church’s cash account(s).

e. Understand where invested funds are held (i.e., the custodian) and ensure that a Service Organization Control report is received from the custodian, or some other assurance is provided that the funds are accounted for accurately and the custodian has adequate and effective internal controls.

6. Church Property – Obtain a listing of all property owned or occupied by the church and perform the following:

a. Request the title and/or deed to the land, building and vehicles.b. Determine and report where the title and deeds are maintained.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 14 OF 20

c. Determine through discussions with management whether insurance is in place for all of the identified assets. Report the amount of coverage and the type of insurance.

d. Assess any impact of ¶2501 and ¶2503 of the Discipline on the information to be presented in the audited annual financial statements or in the results of other procedures performed. According to ¶2501, “all properties of United Methodist local churches and other United Methodist agencies and institutions are held, in trust, for the benefit of the entire denomination, and ownership and usage of church property is subject to the Discipline.” Consider these sections of the Discipline when documenting the listing of properties owned by the church as well as when documenting the ownership structure in the notes to the annual financial statements and the results of the audit procedures. An example of a footnote in audited financial statements might be as follows: Note X -- Restrictions on Church Property As indicated by ¶2501 of The Book of Discipline (“Discipline”) of The United Methodist Church (“UMC”), titles to all real and personal property held by a local church are held “in trust” for the benefit of the UMC, and subject to the provisions of its Discipline. In addition, ¶2503 of the Discipline requires the inclusion of a “trust clause” in deeds for real property, which generally indicates the premises shall be kept, maintained, and disposed of for the benefit of the UMC, and subject to the Discipline. (Refer to the Discipline for its provisions.)

7. Church Credit/Purchasing Cards – Some churches provide credit cards to staff and certain committee chairpersons or members to use to purchase products and services for the church. If the church uses such credit cards, perform the following:

a. Obtain a copy of the credit card statement(s) as of the end of the Test Period and for one other month‐end during the period. Using the statements provided by the card issuer, confirm the any card balance(s) from the previous month(s) were paid in the statement months. For example, if the end of the Test Period is April 2019 and the other month selected at random for testing is September 2018, confirm that any beginning of the month card balances due (i.e., card balances as of the end of March 2019 and August 2018)were paid in the months of April 2019 and September 2018. If not, confirm that the unpaid balances were reflected in the appropriate church balance sheet, and include any such unpaid balances in your report to the Finance Committee.

b. Additional credit and procurement card transaction testing should be performed as part of 11.c. below.

8. Tithes and offerings received:

a. Select six Sundays from the Test Period. For each Sunday selected, obtain a copy of the summary counting sheet prepared by the counters for that Sunday. Agree the amounts received as shown on the counting sheet to the corresponding amounts recorded in the church’s general ledger for that Sunday.

b. Select twelve “credit” entries from the church’s various “revenue” accounts recorded in the General Ledger or Cash Receipts Journal (or similar accounting record) during the Test Period. Agree the amounts selected into the corresponding bank deposit recorded in the church’s bank statements and to giving records of the church. (Note: the amount

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 15 OF 20

selected will likely be one of several entries that together add to the total deposit reflected in the bank statement. If that is the case, agree the specific general ledger entry from the general ledger to the list of entries that comprise the total deposit, and prove the arithmetic accuracy of the listing to ensure the total of the list of entries agrees with the total deposit reflected in the bank statement.)

c. Verify with the church’s accountant (i.e., the staff person responsible for maintaining the general ledger and other accounting records for the church) that he or she has no ability to record entries in or otherwise alter the individual giving records of the church or distribute annual or interim individual giving statements provided to members or others who contribute money or other gifts to the church. Also, confirm such individual does not participate in counting the Sunday offerings.

d. Verify that the church’s financial secretary (the person responsible for maintaining the individual giving records of the church used to provide church members with annual giving statements at year‐end) that he or she has no ability to record entries in the accounting records (general ledger, payroll ledger, and other subsidiary accounting records other than the individual records of the church) or otherwise alter such records. Also, confirm such individual does not participate in counting the Sunday offerings.

e. Select five (5) journal entries in the general ledger recorded to revenue accounts during the Test Period from sources other than cash receipts or cash disbursements. Agree the amounts of such journal entries to supporting documentation, and determine the propriety of such journal based on the supporting documents reviewed. Include in your report a description of any journal entries for which supporting documentation was not available, or where you could not conclude entries were appropriate and necessary.

9. Other income – If the church has other sources of income (e.g., childcare or preschool tuition and fees, property rentals, and such amounts exceed ten (10) percent of the church’s total revenues for any of the preceding three years, develop limited procedures to test the completeness and accuracy of such amounts, and describe the procedures performed and the results of such procedures in the final report to the Finance Committee. (Note: Any such procedures should be reviewed with and approved by the Finance Committee or its designee prior to any such procedures being performed.)

10. Donations – For significant donations to the church (to be determined based on the size of each church), confirm with the donor the amount and intended purpose of the donation. Review to ensure the donation is being used in accordance with its intended purpose and has been accounted for completely and accurately.

11. Church expenses/expenditures and cash disbursements – Judgmentally select twenty‐four (24) expenditures recorded during the Test Period from the general ledger (if individual cash disbursements are recorded directly in the general ledger) or from the cash disbursements journal or register and payroll register or records (if the church posts a summary of expenses from such journals or registers.) In addition, judgmentally select 18 cash disbursements selected from bank statements covering the Test Period. (Note: Care should be taken to select a wide variety of expenditures for testing, and at least one entry for each month of the Testing Period.) For each individual expenditure or cash disbursement selected, perform the following:

a. For salary or wage payments selected, agree the pay rate used to determine the payment to the applicable schedule of salaries and pay rates approved by the Staff Parish Relations

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 16 OF 20

Committee. Recalculate the salary or wages paid based on such approved salary and wage rates and if applicable, the approved timecard or sheet (or similar record) approved by the employee’s supervisor.

b. For payroll tax or benefit payments, recalculate the amount of expense recorded and payment made or remitted based on approved tax or benefit rates in effect at the time of the payment.

c. For expenditures paid for using a church credit or procurement card, agree the charge to a copy of the supplier receipts submitted as support for the charge, and determine the appropriateness of the specific expense account to which the charge was recorded. Confirm the credit card charge was approved for payment in accordance with the established practices of the church. Also, agree the charge for the month to inclusion in the monthly credit card statement received by the church and used as a basis to pay the monthly credit or procurement card charge.

d. For expenditures paid using church‐issued checks, agree the amount of the expenditure selected to the supporting documentation (typically, this will be an invoice issued by the supplier of the products or services purchased or a supplier contract). Recalculate the charges on the invoice based on the quantities and unit costs listed on the invoice. Confirm the purchase was approved for payment in accordance with the established practices of the church. Agree the appropriate details (dollar amount of the purchase and the supplier’s name) to the cancelled check or appropriate details provided in the bank statement received from the bank.

e. For all expenditures, determine the account in which the expenditure was recorded was appropriate given the nature of the expenditure and consistent with the established practices of the church.

12. Review all insurance policies in effect (according to church leadership) and ensure adequate types and levels of coverage are in place for local church needs. If minimum requirements for coverage are set by the annual conference, ensure policy levels comply with these minimum levels.

13. In accordance with the Discipline ¶258.4.b, review to ensure bonding is in place for the church treasurer. Further, review the bond amount with church leadership to ensure the bonding is appropriate for the assets held by the church. Review the current policy and payment information to ensure the bonding policy is current.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 17 OF 20

Appendix BLocal Church Audit

Guide Internal Control Checklist

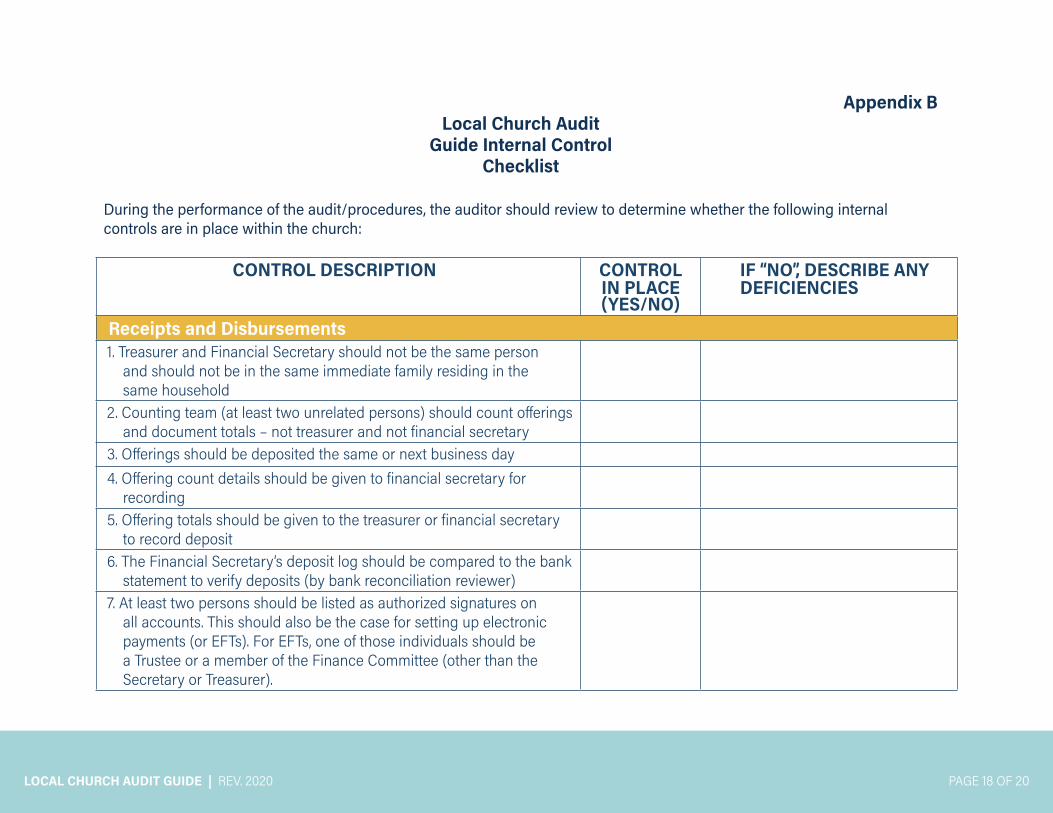

During the performance of the audit/procedures, the auditor should review to determine whether the following internal controls are in place within the church:

CONTROL DESCRIPTION CONTROL IN PLACE(YES/NO)

IF “NO”, DESCRIBE ANY DEFICIENCIES

Receipts and Disbursements1. Treasurer and Financial Secretary should not be the same person

and should not be in the same immediate family residing in the same household

2. Counting team (at least two unrelated persons) should count offerings and document totals – not treasurer and not financial secretary

3. Offerings should be deposited the same or next business day4. Offering count details should be given to financial secretary for

recording5. Offering totals should be given to the treasurer or financial secretary

to record deposit6. The Financial Secretary’s deposit log should be compared to the bank

statement to verify deposits (by bank reconciliation reviewer)7. At least two persons should be listed as authorized signatures on

all accounts. This should also be the case for setting up electronic payments (or EFTs). For EFTs, one of those individuals should be a Trustee or a member of the Finance Committee (other than the Secretary or Treasurer).

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 18 OF 20

8. The Treasurer is authorized to make electronic payments of bills. The Treasurer shall maintain support for every electronic payment just as with the support for paper checks.

9. Financial policy and authority guidelines should be written and approved by the Finance Committee.

10. Invoices should be required for all payments from all accounts11. Someone other than the treasurer (with authority by Finance

Committee) should approve invoices for payment12. Typically, the Treasurer should make payments only after the

invoice is approved. A policy may be implemented where routine, budgeted expenses (i.e., rent/mortgage, electric bill, etc.) may be paid without recurring approval; non‐routine expenses must be approved prior to payment

REPORTING AND REVIEW1. All accounts should be reconciled monthly2. Someone other than treasurer should review bank reconciliation at

least ideally semiannually (but at least annually) – including bank statements, invoices, checks written, and financial reports

3. The Treasurer should make detailed report of budget and designated fund activities to the Finance Committee (or Administrative Council if Finance Committee approves this reporting) on a routine basis as the committees meet

TAX REPORTING REQUIREMENTS1. W‐2s must be issued for employees, including pastors, and 1099s

issued for nonemployee compensation by January 31 for preceding year (federal law requirement)

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 19 OF 20

2. Payroll tax forms and deposits done as required for payroll amount (federal law requirement) – payroll reporting should be completed for the IRS and SSA by appropriate due date for filing method

3. Housing allowance or exclusions approved annually at charge conference and kept on file (federal law requirement)

CONTROL DESCRIPTION CONTROL IN PLACE(YES/NO)

IF “NO”, DESCRIBE ANY DEFICIENCIES

OTHER GENERAL REQUIREMENTS1. Prepare list of all church property for insurance purposes – include

item description, serial number and value2. Prepare list of safety deposit box contents – update authority as

needed –access should be allowed by two unrelated people3. Computer records are backed up and password protected for security4. Ideally, four individuals are required for regular financial

procedures: financial secretary, treasurer, person to review and approve invoices and person to review bank reconciliations. It is possible for this to be accomplished with three individuals if proper segregation is achieved.

LOCAL CHURCH AUDIT GUIDE | REV. 2020 PAGE 20 OF 20

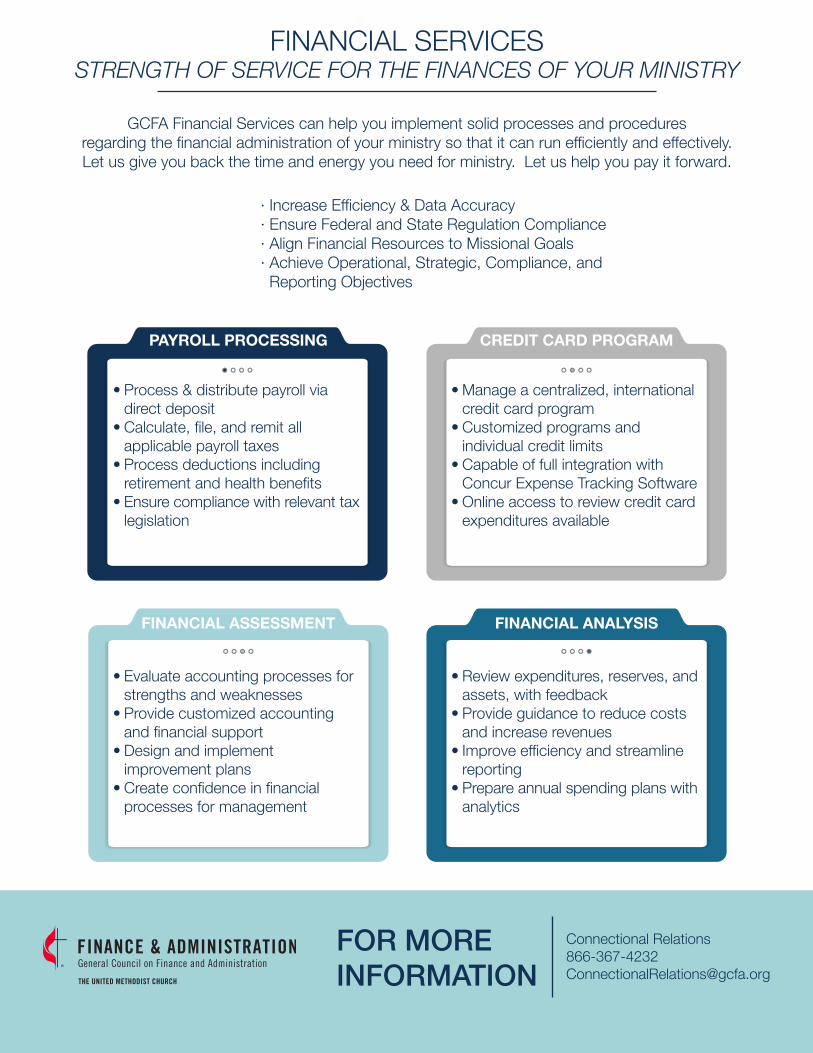

FINANCIAL SERVICESSTRENGTH OF SERVICE FOR THE FINANCES OF YOUR MINISTRY

GCFA Financial Services can help you implement solid processes and procedures regarding the financial administration of your ministry so that it can run efficiently and effectively.Let us give you back the time and energy you need for ministry. Let us help you pay it forward.

· Increase Efficiency & Data Accuracy· Ensure Federal and State Regulation Compliance· Align Financial Resources to Missional Goals· Achieve Operational, Strategic, Compliance, and Reporting Objectives

FOR MOREINFORMATION

Connectional [email protected]

• Process & distribute payroll via direct deposit• Calculate, file, and remit all applicable payroll taxes• Process deductions including retirement and health benefits• Ensure compliance with relevant tax legislation

PAYROLL PROCESSING CREDIT CARD PROGRAM

• Manage a centralized, international credit card program• Customized programs and individual credit limits• Capable of full integration with Concur Expense Tracking Software• Online access to review credit card expenditures available

FINANCIAL ASSESSMENT

• Evaluate accounting processes for strengths and weaknesses• Provide customized accounting and financial support• Design and implement improvement plans• Create confidence in financial processes for management

FINANCIAL ANALYSIS

• Review expenditures, reserves, and assets, with feedback• Provide guidance to reduce costs and increase revenues• Improve efficiency and streamline reporting• Prepare annual spending plans with analytics

![Small Group Presentation2 - NGUMC...Microsoft PowerPoint - Small Group Presentation2 [Compatibility Mode] Author: keehawk Created Date: 6/2/2017 3:27:52 PM ...](https://static.fdocuments.net/doc/165x107/60332c9cb794df0e4976476e/small-group-presentation2-ngumc-microsoft-powerpoint-small-group-presentation2.jpg)