Listing and De-Listing of Securities - Corporate Professionals · Listing and De-Listing of...

63

Listing and De-Listing of Securities Anjali Aggarwal Partner & Head: Capital Market and Stock Exchange Services

Transcript of Listing and De-Listing of Securities - Corporate Professionals · Listing and De-Listing of...

Listing and De-Listing

of

Securities

Anjali AggarwalPartner & Head:

Capital Market and Stock Exchange Services

Listing of Securities means admission

of securities of an issuer to trading

privileges (dealings) on a stock

exchange through a formal agreement.

Whose securities are eligible to be listed?

The securities eligible to be listed may be of any:

Public limited company,

Central or State Government,

Quasi governmental and

Other financial institutions/corporations, municipalities, etc.

Objectives of

Listing

Provide liquidity and

marketability to

securities.

Channelize & Mobilize

savings for economic

development.

To unlock the hidden value

of the business

To attain market

capitalization

No Long Term Capital Gains

Tax on transfer of shares

through the Exchange, on

payment of STT

Listing provides an opportunity to the corporates to raise capital to fund new projects expansions/diversifications and for acquisitions. It also provides an exit route to private equity investors as well as liquidity to the ESOP-holding employees.

Listing brings in liquidity and ready marketability of securities on a continuous basis adding prestige and importance to listed companies.

Fund Raising and exit route to investors

Ready Marketability of Security

Fair Price for the Securities

The prices are publicly arrived at on the basis of demand and supply; the stock exchange quotations are generally reflective of the real value of the security. Thus listing helps generate an independent valuation of the company by the market.

Collateral Value of Securities

Listed securities are acceptable to lenders as collateral for credit facilities. A listed company can also borrow from financial institutions easily as it is rated favorably by lenders of capital; the company can also raise additional funds from the public through the new issue market with a greater degree of assurance.

Better Corporate Practice

Since violations of the listing agreement entail de-listing/suspension of securities from the exchange, the listed companies are expected to follow fair practices to the advantage of investors and public.

Supervision and Control of Trading in Securities

Ability to raise further capital

All transactions in securities are monitored by the regulatory mechanisms of the stock exchange, preventing unfair trade practices. It improves the confidence of small investors and protects them.

An initial listing increases a company's ability to raise further capital through various routes like preferential issue, rights issue, Qualified Institutional Placements and ADRs/GDRs/FCCBs, and in the process attract a wide and varied body of institutional and professional investors.

Regulatory Framework forListing of Securities

WAYS TO GET LISTED

By making an Initial Public Offer (IPO):

When an unlisted company makes either a fresh issue of securities or an offer for sale of its existing securities or both for the first time to the public.

Through Direct Listing:The Company which is already listed on any Recognized Stock Exchange can apply to Stock Exchange having nation-wide terminal to get its securities listed without coming out with an IPO.

PRE- REQUISITES OF LISTING

All Listed Companies are required to maintain

minimum level of public shareholding at 25%

Where the public shareholding falls below 25% at any

time:

The Company shall bring the public shareholding to 25%

within a period of 12 months from the date of such fall, in the

manner specified by SEBI.

Listing Agreement

Till Dec 15, listing of securities was governed by way of a formal arrangement via listing agreement which was

entered into between the issuer and the stock exchanges where the securities of the issuer are listed or intended to be

listed.

It was a binding Agreement between the Company & Stock Exchange, aimed to provide transparency & timely &

accurate disclosures, with severe penal provisions for Non-Compliances.

www.company.com

SEBI (Listing Obligations & Disclosure

Requirements) Regulations, 2015

www.company.com

Listing Regulations…….An introduction

• Applicable wef 1st Dec 15

• To bring the basic framework governing the regime of listed entities in line with Companies Act, 2013.

• Compiling all the mandates of varied SEBI Regulations/ circulars governing equity as well as debt segments of capital market under the ambit of single document.

www.company.com

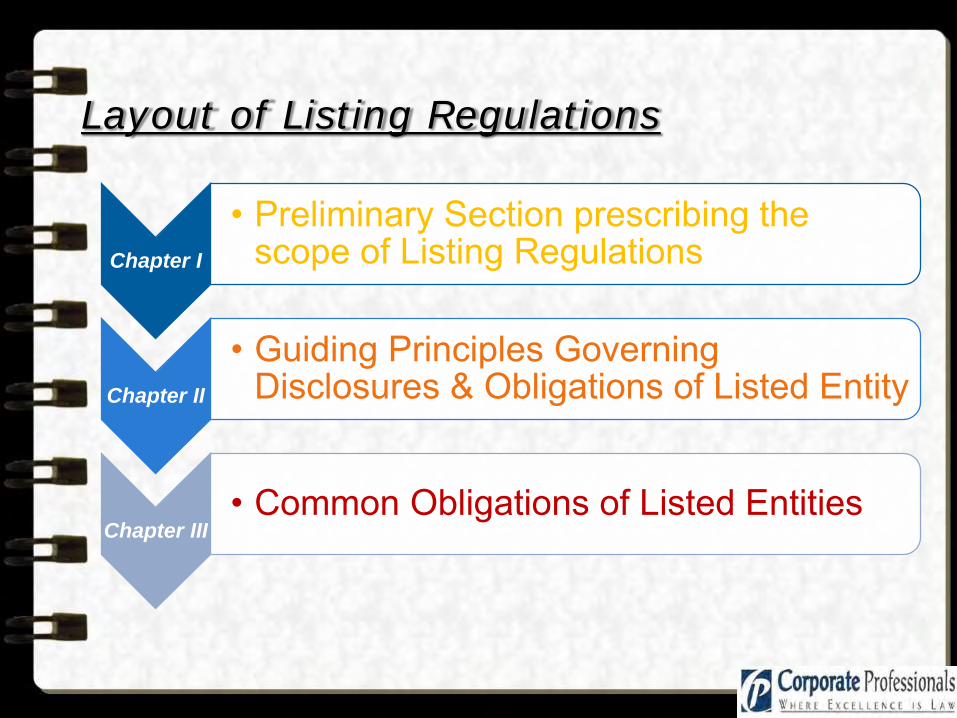

Layout of Listing Regulations

Chapter I

• Preliminary Section prescribing the scope of Listing Regulations

Chapter II

• Guiding Principles Governing Disclosures & Obligations of Listed Entity

Chapter III• Common Obligations of Listed Entities

www.company.com

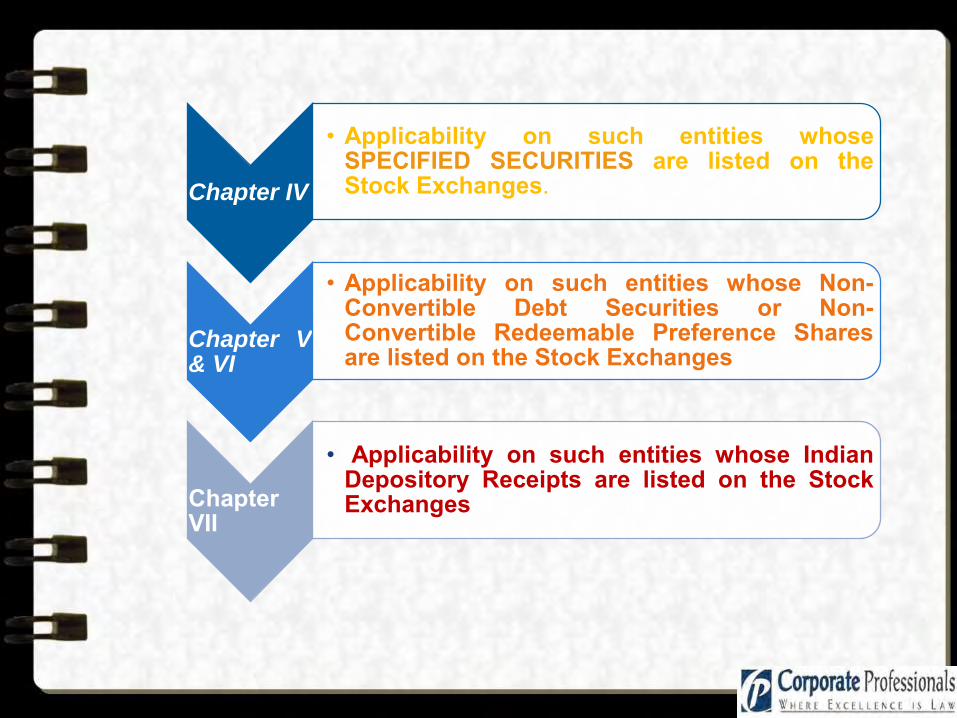

Chapter IV

• Applicability on such entities whoseSPECIFIED SECURITIES are listed on theStock Exchanges.

Chapter V& VI

• Applicability on such entities whose Non-Convertible Debt Securities or Non-Convertible Redeemable Preference Sharesare listed on the Stock Exchanges

ChapterVII

• Applicability on such entities whose IndianDepository Receipts are listed on the StockExchanges

www.company.com

ChapterVIII

• Applicability on such entities whoseSecuritised Debt Instruments are listed onthe Stock Exchanges

Chapter IX

• Applicability on such entities whose MutualFund Units are listed on the StockExchanges

Chapter X& XI

• Duties & Obligations of the RecognizedStock Exchange(s) and provisions for actionin case of default.

Chapter XII• Miscellaneous Provisions

www.company.com

ApplicabilityOf

Listing Regulations

Listed Entities Whose Securities are

Listed On any Recognised

Stock Exchange

Specified Securities Listed on Main Board or SME Exchange or ITP.

any other securities as may be specified by the Board

Non-convertible debt securities (NCDs)

Non- Convertible Redeemable preference Shares (NCRPS)

Perpetual Debt securities

Securitized Debt instruments

Indian Depository Receipts;

Mutual fund Units

www.company.com

MAIN HIGHLIGHTS OF

CHAPTER III

Common Obligations Of

Listed Entities

www.company.com

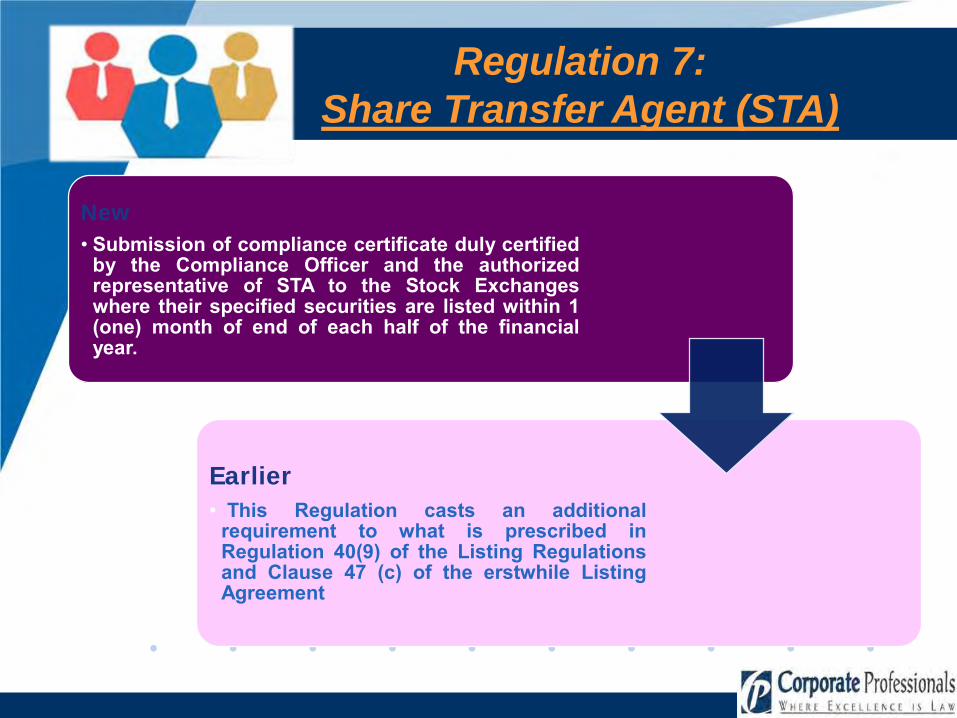

Regulation 7:

Share Transfer Agent (STA)

New

• Submission of compliance certificate duly certifiedby the Compliance Officer and the authorizedrepresentative of STA to the Stock Exchangeswhere their specified securities are listed within 1(one) month of end of each half of the financialyear.

Earlier

• This Regulation casts an additionalrequirement to what is prescribed inRegulation 40(9) of the Listing Regulationsand Clause 47 (c) of the erstwhile ListingAgreement

www.company.com

Regulation 9:

Preservation of Documents

Formulation of Preservation Policy for Documents

documents whose preservation shall be permanent in nature;

documents with preservation period of not less than eight years

after completion of the relevant transactions.

(Maintenance of documents in electronic mode will be deemed to be complying with the aforesaid regulation.)

www.company.com

Regulation 12: Payment of Dividend,

Interest, Redemption or Repayment.

Mandatory use of E-payment facility, as approved by RBI, for the purpose of making the following

payments:

DIVIDENDS REDEMPTION OR REPAYMENT

AMOUNTS

INTEREST

where it is not possible to use e-payment facility then ‘payable-at-par warrants’ or cheques may be issued.

If the amount of Dividend> Rs 1,500/-, the ‘payable-at-par warrants’ or cheques shall be sent by speed post

www.company.com

Regulation 13:

Grievance Redressal Mechanism

New

• Registered on the SCORES platform or any other similar platform to electronically handle the investor complaints.

• Filing of Statement of Investor Grievance to the stock exchange, within 21 days from the end of the relevant quarter .

Earlier

• In the erstwhile ListingAgreement, the informationpertaining to pending investorscomplaints were submitted on aquarterly basis only along withthe Financial Results.

www.company.com

Main Highlights of

CHAPTER IV

Obligations in case of

Listing of

Specified Securities

www.company.com

www.company.com

www.company.com

Regulation 23: Related Party Transaction

Meaning of RPT: Transfer of resources,

services or obligations between a listed entity

and a related party, regardless of whether a

price is charged and a "transaction" with a

related party shall be construed to include a

single transaction or a group of transactions in

a contract

Seek approval from shareholders in General Meeting by passing an ordinary resolution for approving material related party transactions subject to the stipulation that such related parties shall be abstained from voting on such resolution.

Policies: 1. Materiality of

RPTs.2. Dealings with

RPTs

Role of Audit Committee

1. All RPTs are required to be approved by the Audit Committee.2. Audit committee may grant omnibus approval, which shall be valid for not more than one year, for the RPT proposed to be entered by the company for which it shall lay down the criteria.3. It is required to quarterly review the details of RPTs entered into by the company for which such omnibus approval is granted.

Important Provisions relating to Related Party Transaction (RPT)

www.company.com

Regulation 28: Prior In Principle Approval

New

• The Listed company, prior toissuance of securities is neededto obtain an In Principle approvalfrom SEs.

www.company.com

Regulation 29: Prior Intimations

For Financial Results

For alteration in the date of payment of interest or nomenclature of the specified securities

For Corporate Actions

At least 5 days advance notice(excluding the date of intimation and date of meeting) before consideration of Financial Results of the company.

At least 2 working days advance notice (excluding the date of intimation and date of meeting) for considering the said proposal.

At least 11 working days 'advance notice for considering the proposals pertaining to:

Prior Intimation to Stock Exchange about the Board Meeting held, from time to time in the following manner:

www.company.com

• The responsibility is casted on the Board of listed entities, to authorize one or more KMPs

for the purpose of determining materiality of an event or information and making

disclosures to the stock exchange.

• The Listed Entity is required to frame a Policy For Determination Of Materiality Of

Events, duly approved by the Board of Directors of such entity.

The term material events is used in a wider sense in the said regulations.

On one hand certain events are prescribed in the schedules and on the other hand onus is on the

companies to frame a policy on materiality of events and disclose the same to the stock exchanges

in addition to the events specified in the schedules.

Regulation 28: Disclosure of Events or Information

Every Listed Entity is needed to ensure timely and accurate disclosures of such Events or Information which in the opinion of Board is material.

Regulation 31: Holding of Specified Securities

and Shareholding pattern

Filing of Statement showing holding of securities and Shareholding Pattern to Stock

Exchange

For the entity listed on other than SME

Exchange

within 21 days from the end of

respective quarter.

For the entity listed on SME Exchange

within 21 days from the end of each half year.

This provision is in line with Cl 35 of erstwhileListing Agreement.

www.company.com

Regulation 31(A): Disclosures of Class of

Shareholders and Conditions For

ReclassificationThe Stock Exchange may allow for reclassification upon receipt of a request from the

listed company or the concerned shareholder, along with requisite evidence. The reclassification will be allowed subject to compliance of specified conditions.

I. Reclassification of Promoter as Public Shareholder

• When a new promoter replaces the previous promoter subsequent to an open offer or in any other manner, re-classification shall be permitted subject to approval of shareholders in the general meeting.

• Shareholders need to specifically approve whether the outgoing promoter can hold any KMP position in the company. In any case, the outgoing promoter cannot act as KMP for a period of more than 3 years from the date of shareholders’ approval.

A. In case of change in Promoter

www.company.com

• The outgoing promoter along with the promoter group and PAC cannot hold more than 10% of the paid-up equity share capital of the company and shall not have any special rights through any formal or informal arrangements.

In case of transmission/succession/inheritance, the inheritor shall be classified as promoter.

Existing promoters may be re-classified as public in case the company becomes professionally managed and does not have any identifiable promoter subject to the approval of shareholders in a general meeting. A company will be considered as professionally managed for this purpose, if:

• No person or group along with PAC taken together holds more than 1% of the paid-up equity share capital of the company.

B. In case of Inheritance:

C. In case of Company not having any identifiable promoter:

www.company.com

• SEBI may relax any condition for reclassification in specific cases, if it is satisfied about non-exercise of control by the outgoing promoter or its person acting in concert.

II. Reclassification of Public Shareholder as a Promoter:• Then Public shareholder is required to make an open offer in accordance with

the provisions of SEBI (SAST) Regulations, 2011.

E Power to relax the provisions on a case to case basis

www.company.com

Regulation 32: Statement of

deviation(s) or variation(s)

The listed entity shall submit to the stock exchange the following statement(s) on a quarterly basis for public issue, rights issue, preferential issue etc. ,-

• indicating deviations, if any, in the• use of proceeds from the objects stated;• indicating category wise variation between projected utilization of funds and the

actual utilization of funds. The above statement is required to be reviewed by the Audit Committee prior to

its submission and to be given till the issue proceeds have been fully utilized or the purpose for which these proceeds were raised, has been achieved;

The variation is required to be furnished in the Directors Report as well on an annual basis;

If the listed company has appointed any monitory agency then the report/comments of such agency is required to be submitted

• In case of SME listed entities, the same is required to be furnished on semi-annual

basis.

www.company.com

Regulation 33: Financial Results

• The listed company shall submit to the stock exchange the following:•• Audited or unaudited quarterly and year-to-date standalone financial results to

the stock exchange within 45 days from the end of relevant quarter.

• In case the listed company has subsidiaries, then it may submit also quarterly/ year-to-date consolidated financial results of its subsidiary.

• Audited standalone financial results along with the audit report for the financial year, within 60 days from the relevant financial year.

• In respect of companies listed on SME Exchange, the quarterly results needed to be submitted on a half yearly basis and ‘year-to-date’ financial results are not required to be filed to the stock exchanges.

Regulation 33 has duly replaced Clause 41 of the erstwhileListing Agreement.

www.company.com

Regulation 34: Annual Report

• The listed company is required to submit the Annual Report to the Stock Exchange within 21 working days of it being

approved and adopted in the Annual General Meeting.

The disclosures as sought in the Regulation are needed to be incorporated in the Annual Report.

www.company.com

Regulation 36: Documents &

Information to Shareholders

The listed company is required to submit its Annual Report to the shareholders in the following manner:For shareholders, who have their Ids registered with the Company, soft copy of the full Annual Report;For the ones who don’t have their Ids registered, hard copy of the statement containing salient features, in terms of Sec 136 of Companies Act 2013;Hard copies of full Annual reports, to the shareholders who request for the same.

www.company.com

Regulation 37: Draft Scheme of

Arrangement

• Any listed company desirous of undertaking a Scheme of Arrangement shallprior to filing it with High Court/ Tribunal, file the same with the StockExchanges and obtain a NOC/ Observation Letter from theExchange(s).

• The Observation Letter or No-objection Letter granted by the stockexchange prior to presenting scheme before the Court or the Tribunal will bevalid for the period of 6 months from the date of its issuance.

Regulation 38: Minimum Public Shareholding

All listed companies have to comply withMinimum Public Shareholding norms, aslaid down in Rule 19(2) and 19A of SCRR,in the manner specified by SEBI from timeto time.

www.company.com

Regulation 39Issuance of Certificates or

Receipts/Letters/Advices for securities and dealing with unclaimed securities

Company to issue certificates or receipts or advices pursuant to subdivision, split,consolidation, renewal, exchanges, endorsements, issuance of duplicates or newcertificates or receipts or advices, as applicable, in cases of loss or old decrepit orworn out certificates or receipts or advices, as applicable within a period of thirtydays from the date of such lodgment.

The listed company is required to submit the information regarding loss of sharecertificate and issue of the duplicate certificate, to the stock exchange within twodays of its getting information.

The listed entity is required to intimate the record date/ bookclosure date to all the concerned Stock Exchanges at least 7

working days (excluding the date of intimation and the recorddate) before the record date/ closure of transfer books.

The listed entity is required to declare dividend/ cash bonusesat least 5 working days (excluding the date of intimation andthe record date) before the record date fixed for that purpose.

There must be gap of minimum 30 days between two recorddates or two transfer book closure dates.

Regulation 42: Record Date or Date of Closure of

Transfer Books

Regulation 46: Website

The listed company is required to update any change in the content of its website within 2 working days from the date of such change in the content.

This regulation provides clarity as the erstwhile listing agreement was silent regarding updation of contents on the

website of the company.

www.company.com

Regulation 47: Advertisements in

NewspapersCo. to publish the following in at least 1 English newspaper, circulating in whole or substantially whole of India and in 1 daily newspaper in the

vernacular language, where the registered office of the company is situated: • Notice of meeting of the Board of Directors where financial results would be

considered;• Financial results along with the opinion(s) or reservation(s), if any, expressed

by the Auditor within 48 hours of conclusion of the meeting of Board of Directors;

• Statements of deviations/ variations• Notices given to shareholders by advertisement

The above provisions are not applicable on the entities listed on SME Exchange.

Policies

Reg. 9

Policy onPreservation of Documents

Reg. 30

Policy on Materiality of

Events

Reg. 30

Archival Policy

Additional Policies required to be framed

under Chapter IV

Audit Committee

Reg. 8

Nomination & Remuneration

CommitteeReg. 19

Stakeholders Relationship Committee

Reg. 20

Risk Management Committee

Reg. 21

• “Delisting” is totally the reverse of listing. To delist meanspermanent removal of securities of a listed company from a stockexchange. As a consequence of delisting, the securities of that companywould no longer be tradeable at that stock exchange.

• "Delisting" i.e. the said removal from a Stock Exchange, may be Voluntary(i.e. at the will of the Company) or Compulsory (i.e. out of a penal actionby the Stock Exchanges, for the reason of any violations/ lapses).

DELISTINGSTOCK

EXCHANGESCOMPANY

Reasons for Delisting

Smaller & Other Companies

undervalued Companies

Maintaining a listing status entails various costs which may no longer be justifiable.

Maintaining a listing statusinvolves various ongoingcosts relating to financialreporting requirements, ad-hoc disclosures, investorrelations and the increaseddemands on management todevelop a goodrelationship with analysts andinvestors.

Conditions Precedent to Delisting

No company shall apply for delisting of equity shares of a company,(a) pursuant to a buy back of equity shares by the company;(b) pursuant to a preferential allotment made by the company;(c) unless a period of three years has elapsed since the listingof that class of equity shares on any recognized stock exchange; or(d) if any instrument is convertible into the same class of equity shares

that are ought to be delisted, are outstanding. No person belonging to the Promoter Group have sold shares during

six months preceding the date of Board Meeting where Delisting Proposal is approved.

How to Delist??

A recognized stock exchange may, by order, delist any equity shares of a company on any ground prescribed in the rules made under Section 21A of the Securities Contracts (Regulation) Act, 1956.

Reasons

- unfair trade practices

- non payment of listing fees

- violation of listing agreement

- non redressal of grievances.

Decision by panel of experts after considering the various parameters given in the regulations.

Public notice by the exchange for inviting the representation by the aggrieved persons.

Determination of exit price by an independent valuerappointed by the concerned stock exchange.

No requirement of going through the reverse book building process.

Acquisition of shares by the promoters at fair value

VOLUNTARY DELISTING FROM ALL

NATINWIDE STOCK EXCHANGES

VOLUNTARY DELISTING FROM FEW

EXCHANGES BUT REMAINS LISTED

ON AT LEAST ONE STOCK EXCHANGE

HAVING NATION WIDE TERMINALS

VOLUNTARY DELISTING THROUGH

SMALL COMPANIES ROUTE

VOLUNTARY DELISTING FROM ALL THEEXCHANGES

Under this Route, the Acquirer/Promoter isrequired to give an Exit Opportunity to all thepublic shareholders through Reverse BookBuilding System (RBBS) in lieu of providingproposed non-marketability of the Shares.

Shareholders Approval: The special resolution to be passed by postal ballot

shall be acted upon if the votes cast by public shareholders in favour of the

proposal constitutes at least two times the number of votes cast by public

shareholders against it.

Stock Exchange Approval: Application for seeking In-principle approval from the Stock Exchange

where its securities are listed.

Board Approval: Approving the proposal of Voluntary Delisting after taking

on record the Due-diligence Report of the Merchant Banker in respect of

trading in the shares during last 2 Financial Years.

Procedural Aspects prior to initiation of the process of Voluntary Delisting

DETERMINATION OF EXIT PRICE THROUGH

REVERSE BOOK BUILDING MECHANISM

Exit price determined through Reverse Book Building(RBB) is the highest price at which the promoter touchesthe threshold of 90%

Final Price= Price at which shareholding of the Promoter

plus shares tendered by the public shareholders reaches the

threshold limit of 90%

Bid price (Rs.) No. of investors

Demand (no. of shares)

Cumulative Demand (no. of shares)

550 5 2,50,000 2,50,000

565 8 4,00,000 6,50,000

575 10 2,00,000 8,50,000

585 4 4,00,000 12,50,000

595 6 1,20,000 13,70,000

600 5 1,30,000 15,00,000

605 3 2,10,000 17,10,000

620 1 5,00,000 25,00,000

Exit price

Promoter shareholding = 75,00,000 sharesPublic shareholding = 25,00,000 sharesMin Tendering = 15,00,000 shares 90% threshold limit for successful Delisting

An illustration for arriving at the final offer price is given as follows:

VOLUNTARY DELISTING FROM FEW EXCHANGES BUT REMAIN LISTED AT ONE STOCK EXCHANGE HAVING

NATION WIDE TRADING TERMINAL

If after the proposed delisting from any one or more recognized stock

exchanges, the equity shares would remain listed on any recognized stock

exchange which has nationwide trading terminals,

No Exit Opportunity needs to be given to the public shareholders. (Section 6

(a))

No need to pass Special resolution by members.

The company has to give a public notice of the proposed delisting.

The company shall disclose the fact of the delisting in the first annual report

after delisting.

Small Company means:

Company having:

paid up capital not exceeding Rs. 10 Cr. And

Net worth not exceeding Rs. 25 Cr. as on the

last day of previous financial year.

Trading in shares of the company in last 1 year < 10% of total no. of shares

Securities are not suspended from Stock

Exchange

• Board Approval: Approving the proposal of Voluntary Delisting after taking on record the Due-diligence Report of the Merchant Banker in respect of trading in the shares during last 2 Financial Years.

• Shareholders Approval: The special resolution to be passed by postal ballot shall be acted upon if the votes cast by public shareholders in favour of the proposal constitutes at least two times the number of votes cast by public shareholders against it.

• Stock Exchange Approval: Application for seeking In-principle approval from the Stock Exchange where its securities are listed.

Procedural Aspects under Small Company Voluntary Delisting Route

• 90% public shareholders should give their consent for delisting of the equity shares by not following the reverse book building process.

• The shareholders should be given a option to remain the shareholders even if the company gets delisted.

• The promoter makes payment of consideration in cash within the stipulated time period

• The promoter writes individually to all public shareholders in the company informing them of his intention to get the equity shares delisted, and seeking their consent for the proposal for delisting

Anjali Aggarwal

Partner & Head: Capital Market and Stock Exchange Services