LIBOR TRANSITION: NO TIME TO LOSE

5

LIBOR TRANSITION: NO TIME TO LOSE Despite the disruption caused by the COVID-19 pandemic, 2020 continues to be a key year for the transition from LIBOR to alternative risk-free rates. Markets and Securities Services In fact the increased market volatility as a result of the pandemic highlighted the weaknesses of LIBOR benchmarks, with the Bank of England Financial Stability Committee noting, in its Interim Financial Stability Report (FSR) published 7 May 2020, that in March 2020 both GBP and USD three-month LIBOR rates diverged from the alternative bank risk-free rates (RFRs), SONIA and SOFR, due to the lack of transaction-based submissions, reinforcing the Bank of England’s view of the importance of completing the transition to alternative rates. 1 So what should Asset Managers be doing and when do they need to do it by? Regulators have made it clear that the pandemic will not delay the transition away from LIBOR and that firms should still plan for the end of LIBOR post 2021. Asset Management Firms (AMs) broadly have two exposures to LIBOR: • Funds holding investments that reference LIBOR; and • Funds that reference LIBOR as a target or comparison benchmark, including for performance fees. Regulators have stated that AMs should work towards LIBOR ceasing after December 2021 and that they have a responsibility to facilitate and contribute to its orderly end. On 27 February 2020, in a letter to CEOs of AMs, the UK Financial Conduct Authority (FCA) stated that it expects asset managers to “take proactive steps now where appropriate and not wait for instructions from clients”. 2

Transcript of LIBOR TRANSITION: NO TIME TO LOSE

1

LIBOR TRANSITION: NO TIME TO LOSE Despite the disruption caused by the COVID-19 pandemic, 2020 continues to be a key year for the transition from LIBOR to alternative risk-free rates.

Markets and Securities Services

In fact the increased market volatility as a result of the pandemic highlighted the weaknesses of LIBOR benchmarks, with the Bank of England Financial Stability Committee noting, in its Interim Financial Stability Report (FSR) published 7 May 2020, that in March 2020 both GBP and USD three-month LIBOR rates diverged from the alternative bank risk-free rates (RFRs), SONIA and SOFR, due to the lack of transaction-based submissions, reinforcing the Bank of England’s view of the importance of completing the transition to alternative rates.1

So what should Asset Managers be doing and when do they need to do it by?Regulators have made it clear that the pandemic will not delay the transition away from LIBOR and that firms should still plan for the end of LIBOR post 2021.

Asset Management Firms (AMs) broadly have two exposures to LIBOR:

• Funds holding investments that reference LIBOR; and

• Funds that reference LIBOR as a target or comparison benchmark, including for performance fees.

Regulators have stated that AMs should work towards LIBOR ceasing after December 2021 and that they have a responsibility to facilitate and contribute to its orderly end.

On 27 February 2020, in a letter to CEOs of AMs, the UK Financial Conduct Authority (FCA) stated that it expects asset managers to “take proactive steps now where appropriate and not wait for instructions from clients”.2

2

AMs are users of swaps on behalf of clients, and so this target [2 March 2020 – the date market makers are encouraged to change the market convention for sterling interest rate swaps from LIBOR to SONIA] implies asset management fi rms should now consider switching from LIBOR swaps to SONIA swaps for new positions where possible.

AMs are signifi cant investors on behalf of clients in cash products (such as bonds, securitisations, structured products, loans). Therefore, [the Q3 2020 target for ceasing issuance of GBP LIBOR-based cash products maturing beyond 2021] suggests asset management fi rms should consider not making any new investments in GBP LIBOR-based cash products maturing beyond 2021 by end Q3 2020.

AMs also often operate funds and other products which have benchmarks or performance fees linked to LIBOR. So we think this target of end Q3 2020 is sensible for fi rms to consider when planning to cease launching new products with benchmarks or performance fees linked to LIBOR.

[The transition of legacy LIBOR products to signifi cantly reduce the stock of LIBOR referencing contracts by Q1 2021] is directly applicable to AMs that have LIBOR exposures or dependencies in the funds they operate, or the instruments they hold on behalf of clients. If your fi rm has LIBOR exposures or dependencies, but does not have a plan in place, you must act now.

In addition fi rms should not expect or base their transition plans on future regulatory relief or guidance or on legislative solutions.

The letter further makes reference to 2020 targets published by the FCA, Bank of England and the Working Group on

Sterling Risk-Free Reference Rates (RFRWG), on 16th January 2020, which identifi ed where they see AMs need to act on LIBOR exposure, setting targets for when these actions should commence or be completed:

3

Although the RFRWG subsequently amended the target dates for lenders, the FCA has not indicated that it will amend its expectations of AMs.

With reference to the two exposures AMs have to LIBOR, they need to consider the following:

Investments that reference LIBORAs stated in the 2020 targets, AMs should be in the process of replacing investments that reference LIBOR where possible. New investments should not be based on LIBOR if they mature beyond 2021 and existing investments that extend beyond Q4 2021 should be reviewed to see if the reference rate can be replaced or the investment closed-out and replaced with non-LIBOR equivalents.

For derivatives that extend beyond the end of 2021 and reference LIBOR, International Swaps and Derivatives Association (ISDA) is actively looking at fall-back provisions to ensure continuity in the market in the event that LIBOR rates cease to be produced while products are still referencing them. At the time of writing it is anticipated that the Supplement and Protocol will be published during July 2020.

Funds that reference LIBORAs stated in the 2020 targets, AMs that operate funds that reference LIBOR should be looking at replacements. Where

a benchmark is included in a fund’s’ investment objectives, the firm should consider whether the replacement requires investor agreement, for example if the new benchmark differs significantly from the existing one, or whether a notification period will suffice. Firms will also need to consider whether local requirements mean that the home state regulator of the fund needs to approve the change of benchmark prior to implementation.

However, the structure of RFRs is different from LIBOR in that they are overnight rates and do not, as proposed, have term structures. This difference will generally mean that longer-term products, such as UCITS and AIFs, need the applicable overnight rate for each day to be aggregated, i.e. as a compounded or simple average to provide the right data to calculate performance fees or show whether a fund has met its objective. A feature of averaging an RFR rate is that any idiosyncratic, day-to-day fluctuations in market rates are smoothed out, so that the rate reflects movements in interest rates over a given period. Therefore, in general, compounded and averaged RFRs can be less volatile than forward looking LIBOR benchmarks.

Whereas LIBOR term rates are forward looking, average or compounded RFRs look back over the relevant period and are calculated using actual overnight rates. As a result, AMs could adopt backward looking average or compounded RFRs that better reflect the recommended holding period of a fund.

4

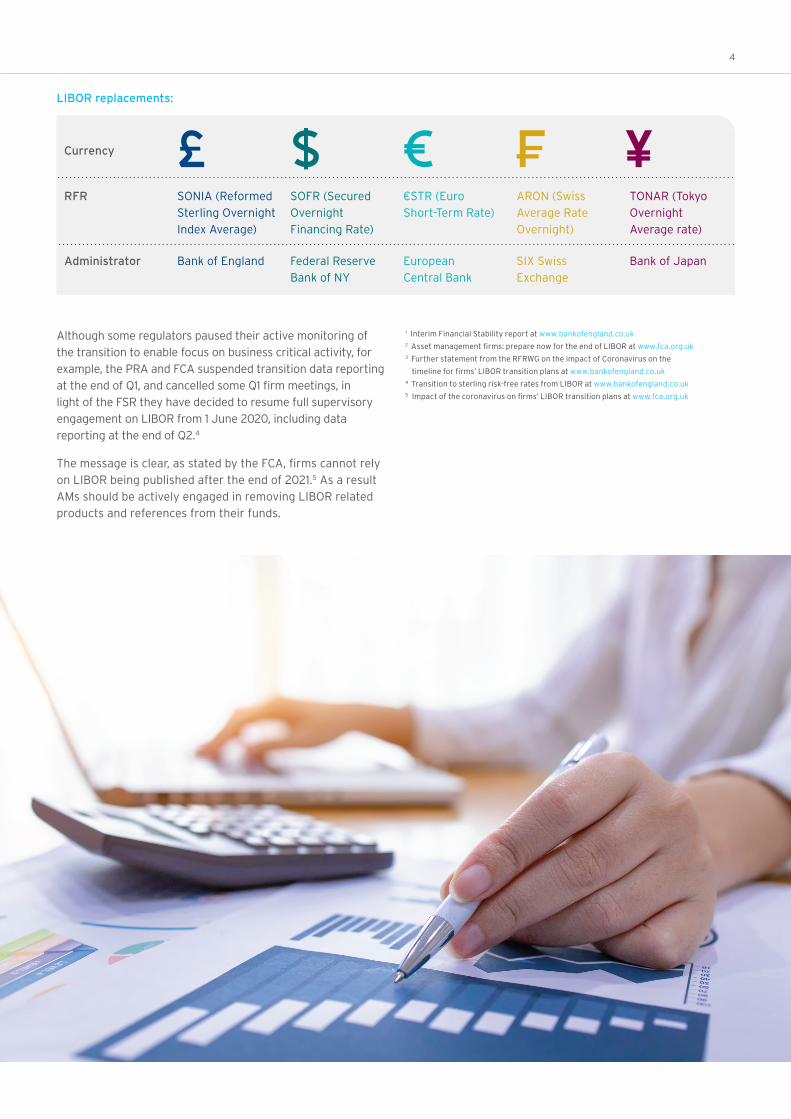

LIBOR replacements:

1 Interim Financial Stability report at www.bankofengland.co.uk2 Asset management firms: prepare now for the end of LIBOR at www.fca.org.uk3 Further statement from the RFRWG on the impact of Coronavirus on the

timeline for firms’ LIBOR transition plans at www.bankofengland.co.uk4 Transition to sterling risk-free rates from LIBOR at www.bankofengland.co.uk5 Impact of the coronavirus on firms’ LIBOR transition plans at www.fca.org.uk

Although some regulators paused their active monitoring of the transition to enable focus on business critical activity, for example, the PRA and FCA suspended transition data reporting at the end of Q1, and cancelled some Q1 firm meetings, in light of the FSR they have decided to resume full supervisory engagement on LIBOR from 1 June 2020, including data reporting at the end of Q2.4

The message is clear, as stated by the FCA, firms cannot rely on LIBOR being published after the end of 2021.5 As a result AMs should be actively engaged in removing LIBOR related products and references from their funds.

Currency

RFR SONIA (Reformed Sterling Overnight Index Average)

SOFR (Secured Overnight Financing Rate)

€STR (Euro Short-Term Rate)

ARON (Swiss Average Rate Overnight)

TONAR (Tokyo Overnight Average rate)

Administrator Bank of England Federal Reserve Bank of NY

European Central Bank

SIX Swiss Exchange

Bank of Japan

5

www.citibank.com/mss

The market, service, or other information is provided in this communication solely for your information and “AS IS” and “AS AVAILABLE”, without any representation or warranty as to accuracy, adequacy, completeness, timeliness or fitness for particular purpose. The user bears full responsibility for all use of such information. Citi may provide updates as further information becomes publicly available but will not be responsible for doing so. The terms, conditions and descriptions that appear are subject to change; provided, however, Citi has no responsibility for updating or correcting any information provided in this communication. No member of the Citi organization shall have any liability to any person receiving this communication for the quality, accuracy, timeliness or availability of any information contained in this communication or for any person’s use of or reliance on any of the information, including any loss to such person.

This communication is not intended to constitute legal, regulatory, tax, investment, accounting, financial or other advice by any member of the Citi organization. This communication should not be used or relied upon by any person for the purpose of making any legal, regulatory, tax, investment, accounting, financial or other decision or to provide advice on such matters to any other person. Recipients of this communication should obtain guidance and/or advice, based on their own particular circumstances, from their own legal, tax or other appropriate advisor.

Not all products and services that may be described in this communication are available in all geographic areas or to all persons. Your eligibility for particular products and services is subject to final determination by Citigroup and/or its affiliates.

The entitled recipient of this communication may make the provided information available to its employees or employees of its affiliates for internal use only but may not reproduce, modify, disclose, or distribute such information to any third parties (including any customers, prospective customers or vendors) or commercially exploit it without Citi’s express written consent. Unauthorized use of the provided information or misuse of any information is strictly prohibited.

Among Citi’s affiliates, (i) Citibank, N.A., London Branch, is regulated by Office of the Comptroller of the Currency (USA), authorised by the Prudential Regulation Authority and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority (together, the “UK Regulator”) and has its registered office at Citigroup Centre, Canada Square, London E14 5LB and (ii) Citibank Europe plc, is regulated by the Central Bank of Ireland, the European Central Bank and has its registered office at 1 North Wall Quay, Dublin 1, Ireland. This communication is directed at persons (i) who have been or can be classified by Citi as eligible counterparties or professional clients in line with the rules of the UK Regulator, (ii) who have professional experience in matters relating to investments falling within Article 19(1) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 and (iii) other persons to whom it may otherwise lawfully be communicated. No other person should act on the contents or access the products or transactions discussed in this communication. In particular, this communication is not intended for retail clients and Citi will not make such products or transactions available to retail clients. The information provided in this communication may relate to matters that are (i) not regulated by the UK Regulator and/or (ii) not subject to the protections of the United Kingdom’s Financial Services and Markets Act 2000 and/or the United Kingdom’s Financial Services Compensation Scheme.

© 2020 Citibank, N.A. and/or each applicable affiliate. All rights reserved by Citibank, N.A. and/or each applicable affiliate. Citi and Arc Design is a trademark and service mark of Citigroup Inc., used and registered throughout the world.

GRA31656 07/20

Please contact for further details:

Amanda Hale Head of Regulatory Services [email protected] +44 (0)20 7508 0178

David Morrison Global Head of Trustee and Fiduciary Services [email protected] +44 (0) 20 7500 8021

Caroline Chan APAC Head of Fiduciary Business [email protected] +852 5181 2602

Shane Baily EMEA Head of Trustee and Fiduciary Services UK, Ireland and Luxembourg [email protected] +353 (1) 622 6297

Jan-Olov Nord EMEA Head of Fiduciary Services Netherlands and Sweden [email protected] +31 20 651 4313

Ann-Marie Roddie Head of Product Development Fiduciary Services [email protected] +44 (1534) 60-8201