LEVERAGING PRIVATE CAPITAL FOR INFRASTRUCTURE...

32

LEVERAGING PRIVATE CAPITAL FOR INFRASTRUCTURE FINANCE Zoubida Allaoua Director of the Finance, Economics and Urban Development Department The World Bank 1 November 21 st , 2011

Transcript of LEVERAGING PRIVATE CAPITAL FOR INFRASTRUCTURE...

LEVERAGING PRIVATE CAPITAL FOR INFRASTRUCTURE FINANCE

Zoubida Allaoua Director of the Finance, Economics and Urban Development Department The World Bank

1

November 21st, 2011

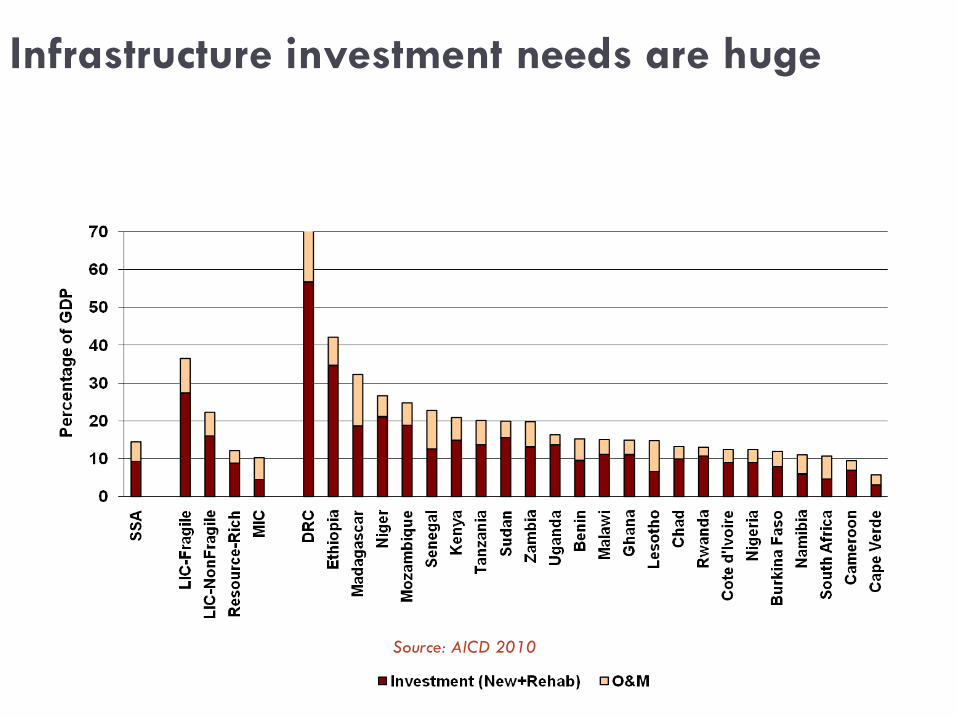

Infrastructure investment needs are huge

Source: AICD 2010

2

3

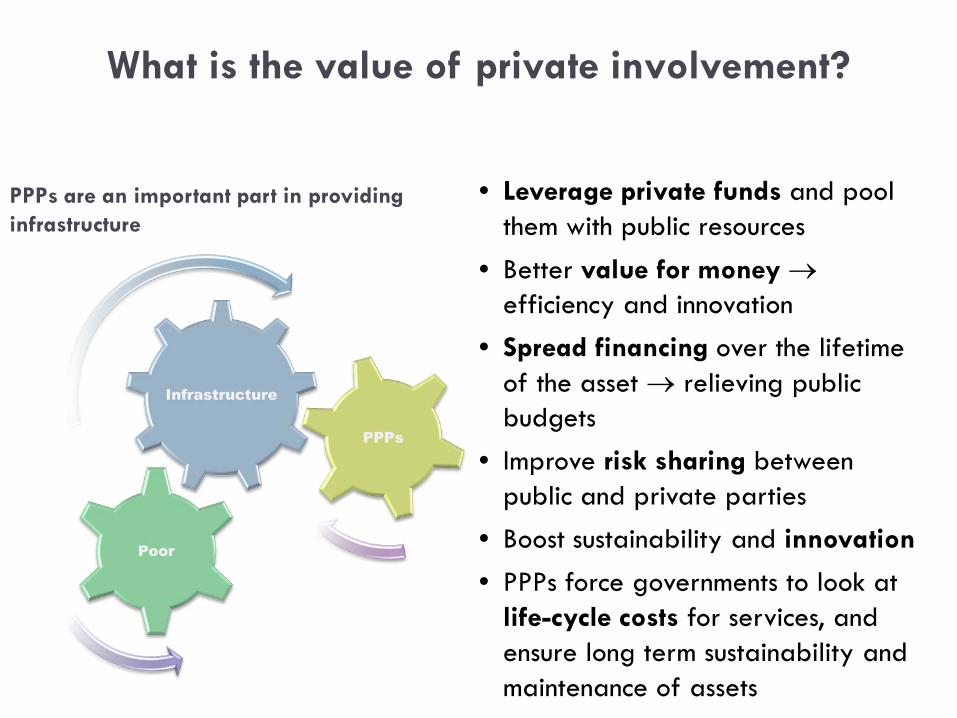

What is the value of private involvement?

• Leverage private funds and pool them with public resources

• Better value for money → efficiency and innovation

• Spread financing over the lifetime of the asset → relieving public budgets

• Improve risk sharing between public and private parties

• Boost sustainability and innovation • PPPs force governments to look at

life-cycle costs for services, and ensure long term sustainability and maintenance of assets

PPPs are an important part in providing infrastructure

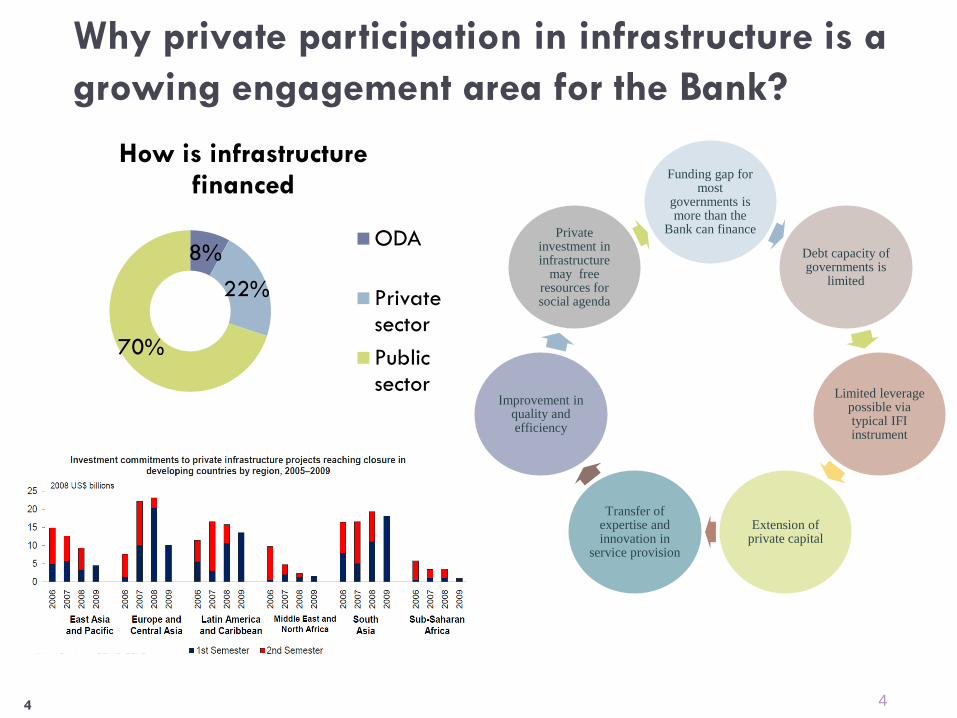

Why private participation in infrastructure is a growing engagement area for the Bank?

Funding gap for most

governments is more than the

Bank can finance

Debt capacity of governments is

limited

Limited leverage possible via typical IFI instrument

Extension of private capital

Transfer of expertise and innovation in

service provision

Improvement in quality and efficiency

Private investment in infrastructure

may free resources for social agenda

8%

22%

70%

How is infrastructure financed

ODA

Private sector Public sector

4 4

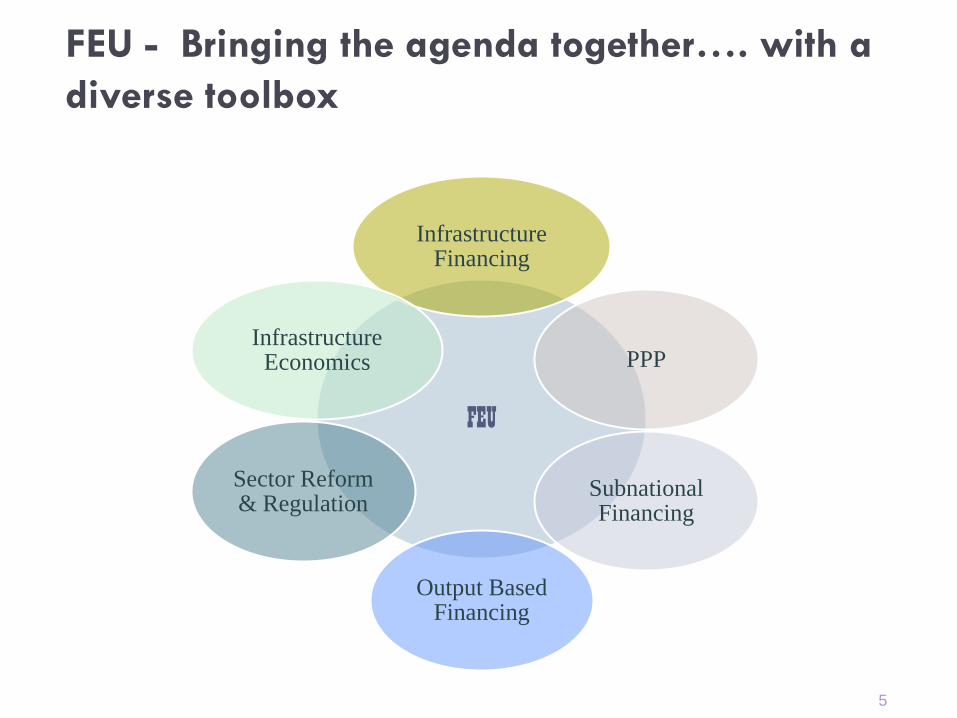

FEU - Bringing the agenda together…. with a diverse toolbox

FEU

Infrastructure Financing

PPP

Subnational Financing

Output Based Financing

Sector Reform & Regulation

Infrastructure Economics

5

5

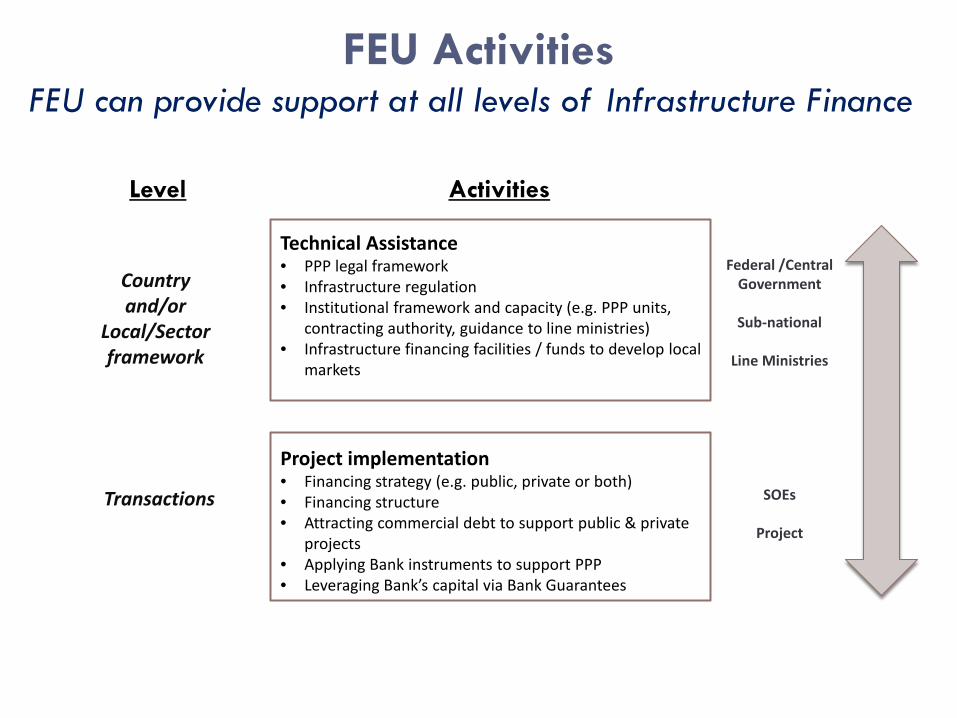

FEU Activities

Technical Assistance • PPP legal framework • Infrastructure regulation • Institutional framework and capacity (e.g. PPP units,

contracting authority, guidance to line ministries) • Infrastructure financing facilities / funds to develop local

markets

Project implementation • Financing strategy (e.g. public, private or both) • Financing structure • Attracting commercial debt to support public & private

projects • Applying Bank instruments to support PPP • Leveraging Bank’s capital via Bank Guarantees

Country and/or

Local/Sector framework

Transactions

Federal /Central

Government

Sub-national

Line Ministries

SOEs

Project

Level Activities

FEU can provide support at all levels of Infrastructure Finance 6

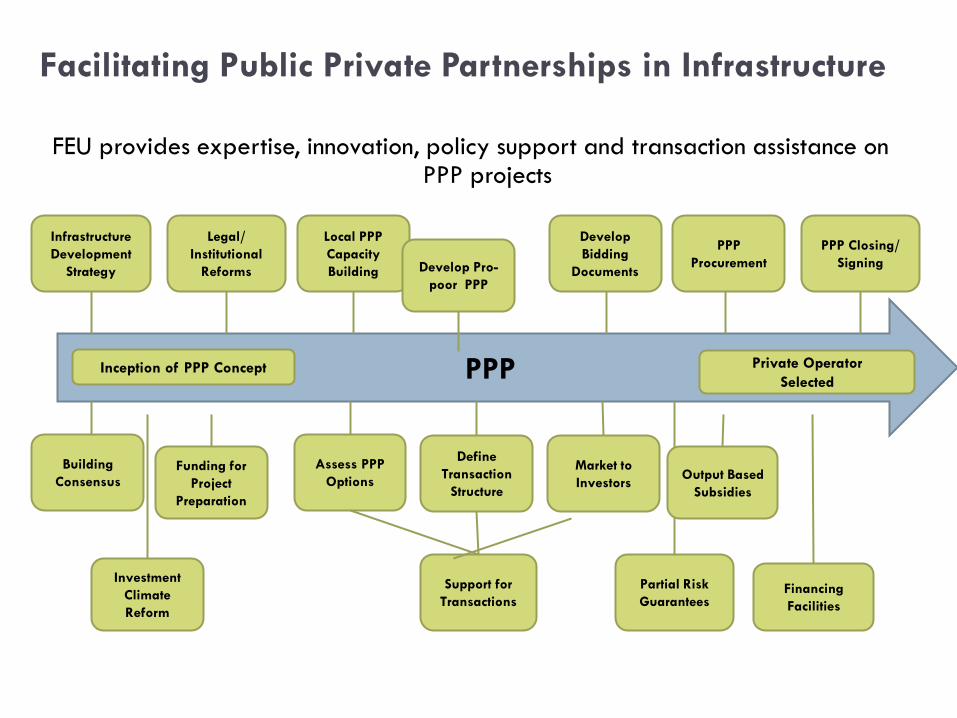

Facilitating Public Private Partnerships in Infrastructure

FEU provides expertise, innovation, policy support and transaction assistance on PPP projects

PPP Inception of PPP Concept Private Operator Selected

Infrastructure Development

Strategy

Legal/ Institutional

Reforms

Building Consensus

Local PPP Capacity Building

Support for Transactions

Assess PPP Options

Define Transaction

Structure

Market to Investors

Develop Bidding

Documents

PPP Procurement

PPP Closing/ Signing

Partial Risk Guarantees

Investment Climate Reform

Output Based Subsidies

Develop Pro-poor PPP

6

Financing Facilities

Funding for Project

Preparation

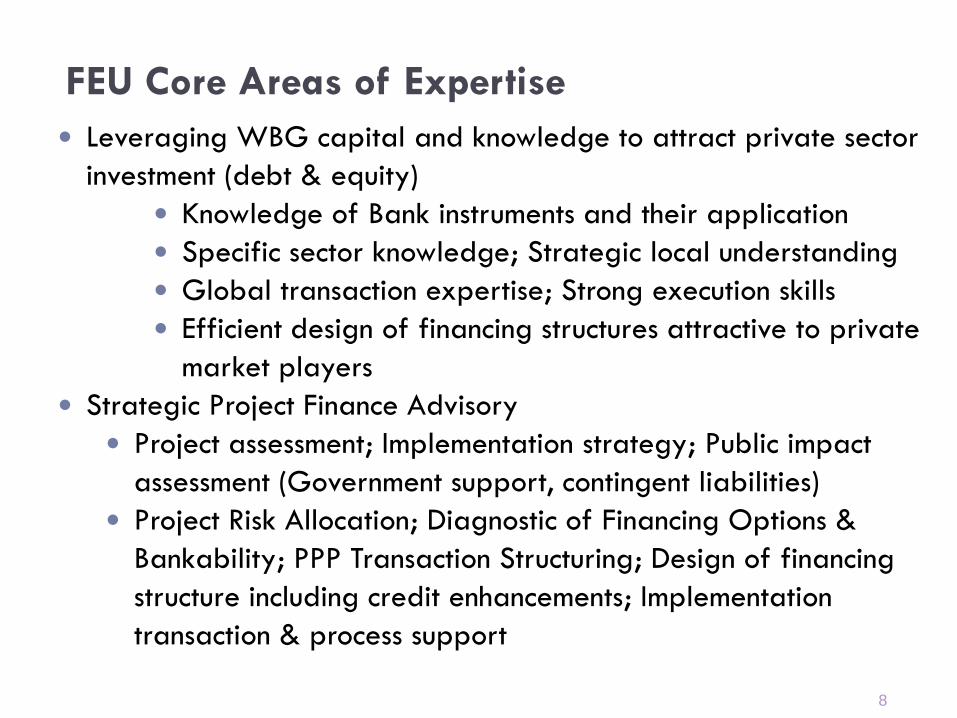

FEU Core Areas of Expertise Leveraging WBG capital and knowledge to attract private sector

investment (debt & equity) Knowledge of Bank instruments and their application Specific sector knowledge; Strategic local understanding Global transaction expertise; Strong execution skills Efficient design of financing structures attractive to private

market players Strategic Project Finance Advisory

Project assessment; Implementation strategy; Public impact assessment (Government support, contingent liabilities)

Project Risk Allocation; Diagnostic of Financing Options & Bankability; PPP Transaction Structuring; Design of financing structure including credit enhancements; Implementation transaction & process support

8

8

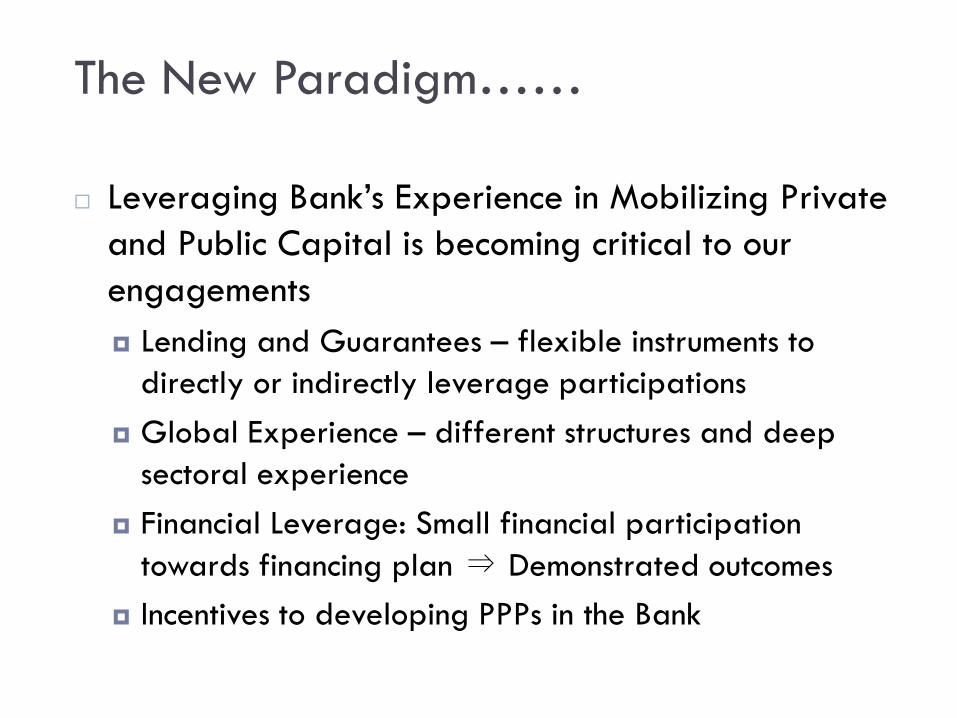

The New Paradigm…… 9

Leveraging Bank’s Experience in Mobilizing Private and Public Capital is becoming critical to our engagements Lending and Guarantees – flexible instruments to

directly or indirectly leverage participations Global Experience – different structures and deep

sectoral experience Financial Leverage: Small financial participation

towards financing plan ⇒ Demonstrated outcomes Incentives to developing PPPs in the Bank

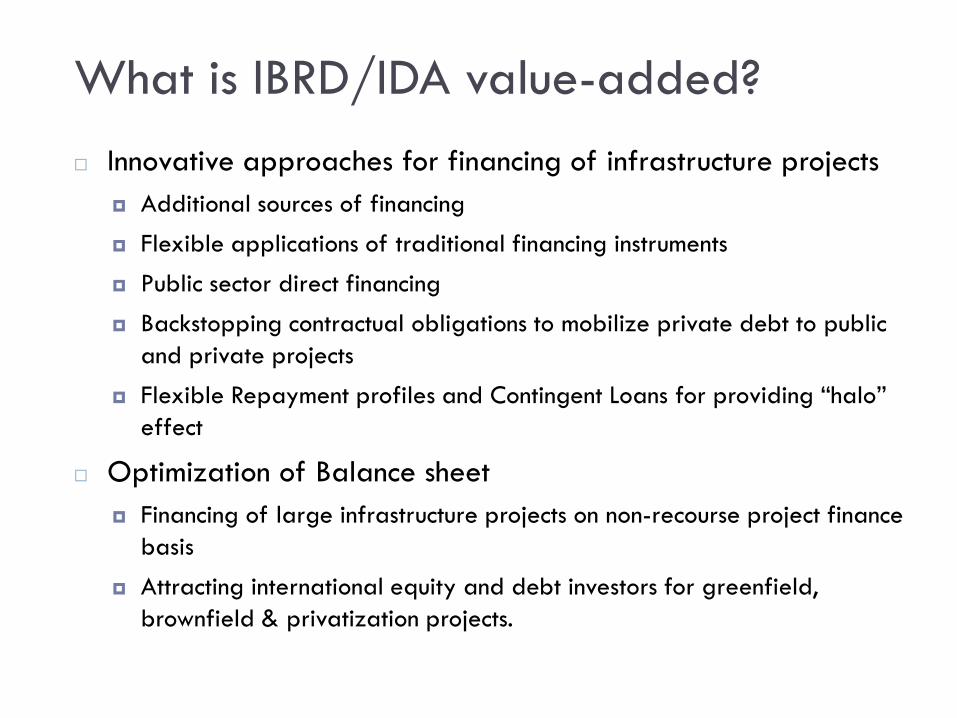

What is IBRD/IDA value-added? 10

Innovative approaches for financing of infrastructure projects Additional sources of financing

Flexible applications of traditional financing instruments

Public sector direct financing

Backstopping contractual obligations to mobilize private debt to public and private projects

Flexible Repayment profiles and Contingent Loans for providing “halo” effect

Optimization of Balance sheet Financing of large infrastructure projects on non-recourse project finance

basis

Attracting international equity and debt investors for greenfield, brownfield & privatization projects.

What are Client Government’s main concerns related to infrastructure development?

Issues Possible solutions

How can I minimize the counting of Bank resources against my designated allocation?

How can I finance this project without taking on more debt?

How can I match the maturity of my debt liability to the life of underlying asset?

How can I mitigate the risks so that the market is willing to provide loans and equity investment in my country?

How can I minimize the contingent liability on my balance sheet from PPPs?

Introduce PPPs to mobilize public sector money

Use guarantees to leverage Bank and public resources

Use PCGs/PBGs for leverage impact and stretch maturity of commercial debt

Use PRGs to reduce risk levels of private sector

Use results-based financing to incentivize service providers

Introduce optimal PPP structure to minimize public financing

11

11

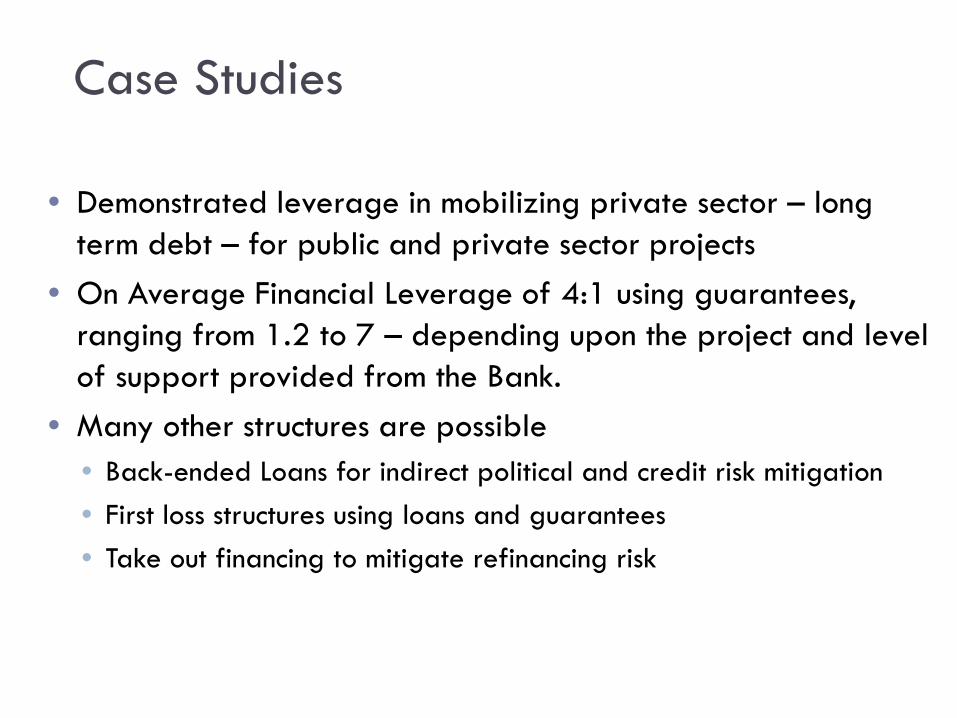

Case Studies 12

• Demonstrated leverage in mobilizing private sector – long term debt – for public and private sector projects

• On Average Financial Leverage of 4:1 using guarantees, ranging from 1.2 to 7 – depending upon the project and level of support provided from the Bank.

• Many other structures are possible • Back-ended Loans for indirect political and credit risk mitigation • First loss structures using loans and guarantees • Take out financing to mitigate refinancing risk

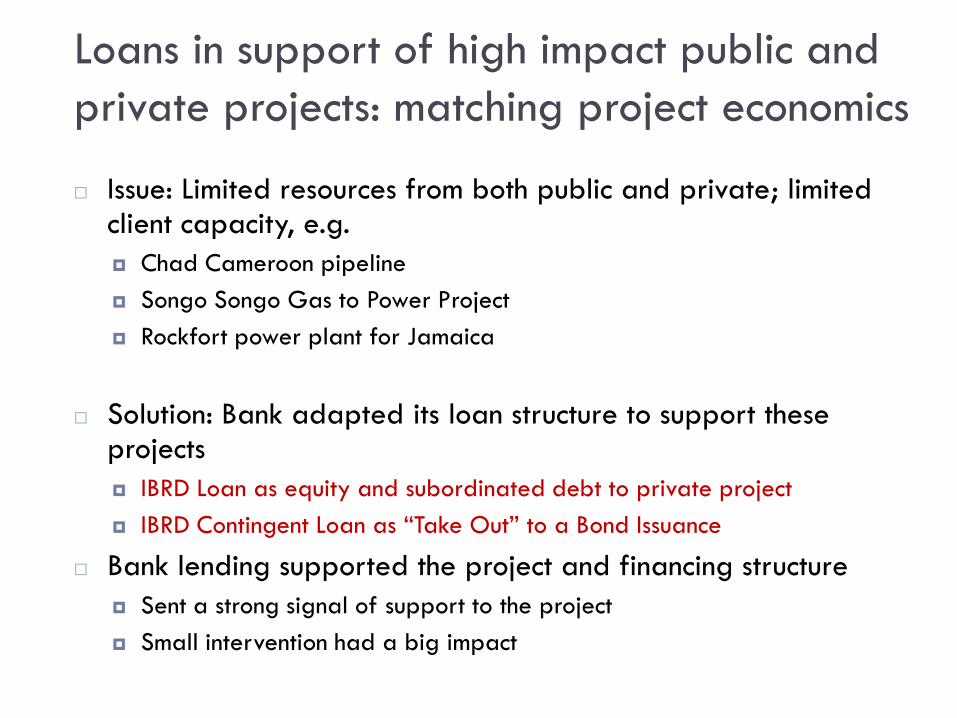

Loans in support of high impact public and private projects: matching project economics

13

Issue: Limited resources from both public and private; limited client capacity, e.g. Chad Cameroon pipeline Songo Songo Gas to Power Project Rockfort power plant for Jamaica

Solution: Bank adapted its loan structure to support these projects IBRD Loan as equity and subordinated debt to private project IBRD Contingent Loan as “Take Out” to a Bond Issuance

Bank lending supported the project and financing structure Sent a strong signal of support to the project Small intervention had a big impact

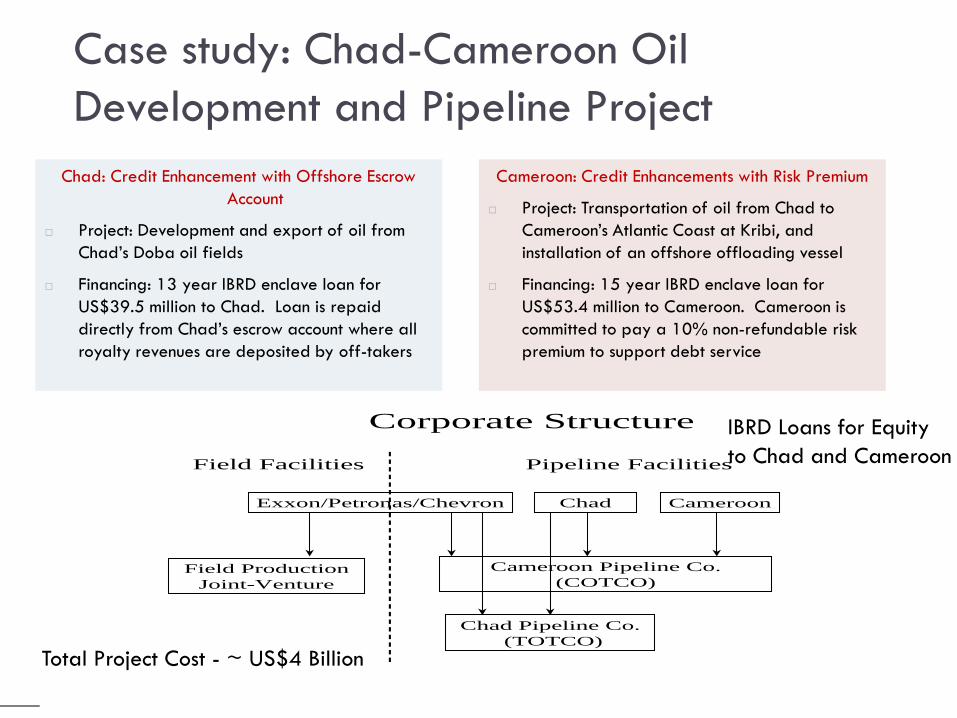

Case study: Chad-Cameroon Oil Development and Pipeline Project

Chad: Credit Enhancement with Offshore Escrow Account

Project: Development and export of oil from Chad’s Doba oil fields

Financing: 13 year IBRD enclave loan for US$39.5 million to Chad. Loan is repaid directly from Chad’s escrow account where all royalty revenues are deposited by off-takers

Cameroon: Credit Enhancements with Risk Premium

Project: Transportation of oil from Chad to Cameroon’s Atlantic Coast at Kribi, and installation of an offshore offloading vessel

Financing: 15 year IBRD enclave loan for US$53.4 million to Cameroon. Cameroon is committed to pay a 10% non-refundable risk premium to support debt service

14

Chad Pipeline Co. (TOTCO)

Corporate Structure

Field Facilities Pipeline Facilities

Field ProductionJoint-Venture

Cameroon Pipeline Co.(COTCO)

Exxon/Petronas/Chevron CameroonChad

IBRD Loans for Equity to Chad and Cameroon

Total Project Cost - ~ US$4 Billion

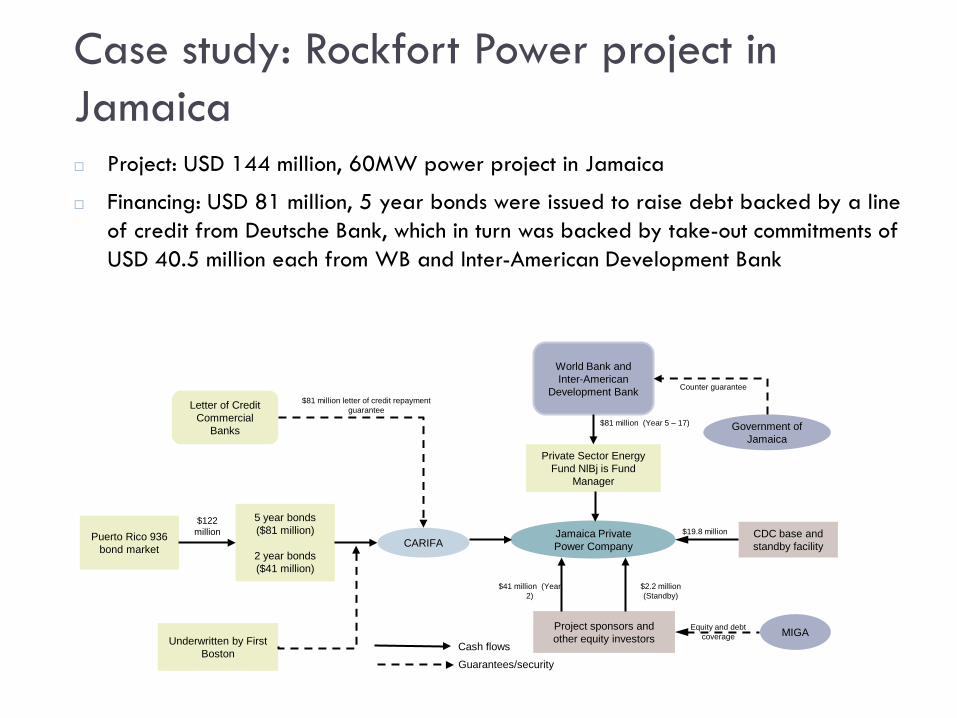

Case study: Rockfort Power project in Jamaica

15 Project: USD 144 million, 60MW power project in Jamaica

Financing: USD 81 million, 5 year bonds were issued to raise debt backed by a line of credit from Deutsche Bank, which in turn was backed by take-out commitments of USD 40.5 million each from WB and Inter-American Development Bank

5 year bonds ($81 million)

2 year bonds ($41 million)

Puerto Rico 936 bond market

Underwritten by First Boston

World Bank and Inter-American

Development Bank Letter of Credit

Commercial Banks

Private Sector Energy Fund NlBj is Fund

Manager

CDC base and standby facility

Project sponsors and other equity investors MIGA

Jamaica Private Power Company CARIFA

Cash flows

Government of Jamaica

Guarantees/security

$122 million

$81 million letter of credit repayment guarantee

Counter guarantee

$81 million (Year 5 – 17)

$19.8 million

$2.2 million (Standby)

$41 million (Year 2)

Equity and debt coverage

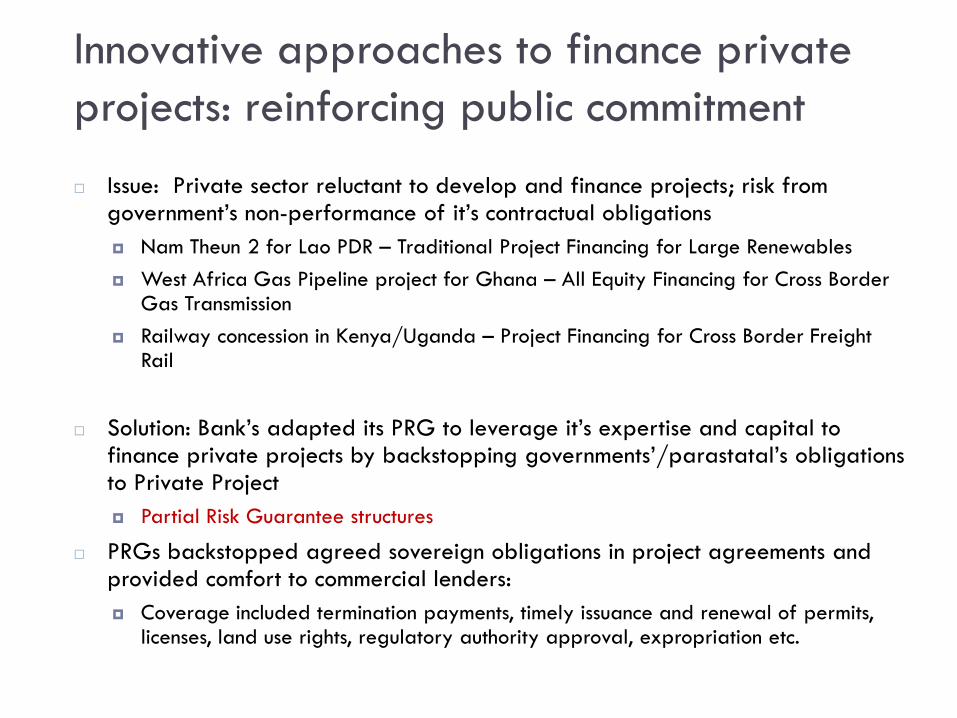

Innovative approaches to finance private projects: reinforcing public commitment

16

Issue: Private sector reluctant to develop and finance projects; risk from government’s non-performance of it’s contractual obligations Nam Theun 2 for Lao PDR – Traditional Project Financing for Large Renewables West Africa Gas Pipeline project for Ghana – All Equity Financing for Cross Border

Gas Transmission Railway concession in Kenya/Uganda – Project Financing for Cross Border Freight

Rail

Solution: Bank’s adapted its PRG to leverage it’s expertise and capital to finance private projects by backstopping governments’/parastatal’s obligations to Private Project Partial Risk Guarantee structures

PRGs backstopped agreed sovereign obligations in project agreements and provided comfort to commercial lenders: Coverage included termination payments, timely issuance and renewal of permits,

licenses, land use rights, regulatory authority approval, expropriation etc.

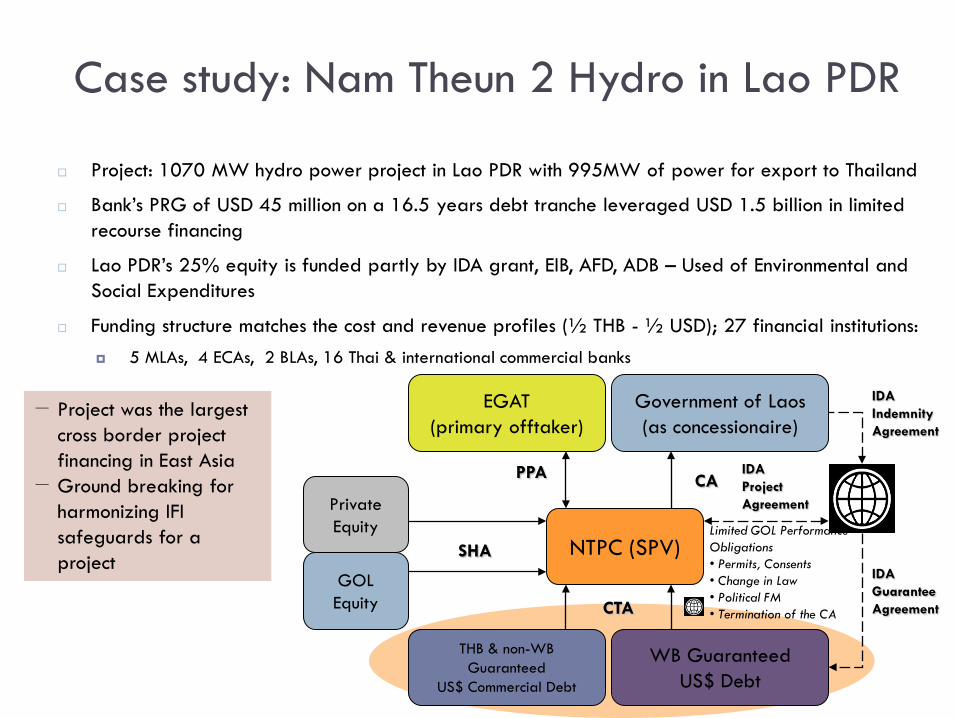

Case study: Nam Theun 2 Hydro in Lao PDR 17

Project: 1070 MW hydro power project in Lao PDR with 995MW of power for export to Thailand

Bank’s PRG of USD 45 million on a 16.5 years debt tranche leveraged USD 1.5 billion in limited recourse financing

Lao PDR’s 25% equity is funded partly by IDA grant, EIB, AFD, ADB – Used of Environmental and Social Expenditures

Funding structure matches the cost and revenue profiles (½ THB - ½ USD); 27 financial institutions: 5 MLAs, 4 ECAs, 2 BLAs, 16 Thai & international commercial banks

NTPC (SPV) GOL Equity

Private Equity

EGAT (primary offtaker)

Government of Laos (as concessionaire)

THB & non-WB Guaranteed

US$ Commercial Debt

WB Guaranteed US$ Debt

Limited GOL Performance Obligations • Permits, Consents • Change in Law • Political FM • Termination of the CA

PPA CA

CTA

IDA Guarantee Agreement

SHA

IDA Indemnity Agreement

IDA Project Agreement

− Project was the largest cross border project financing in East Asia

− Ground breaking for harmonizing IFI safeguards for a project

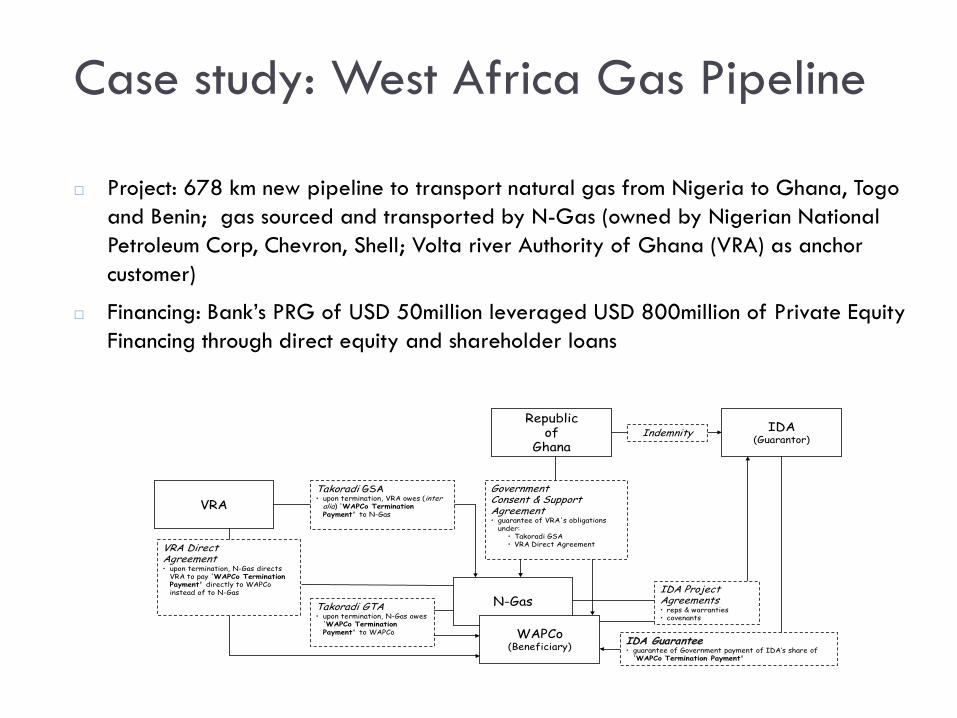

N-Gas

WAPCo(Beneficiary)

Republicof

Ghana

VRA

IDA(Guarantor)

Takoradi GSA• upon termination, VRA owes (inter

alia) 'WAPCo Termination Payment' to N-Gas

Indemnity

IDA Guarantee• guarantee of Government payment of IDA’s share of

'WAPCo Termination Payment'

IDA ProjectAgreements• reps & warranties• covenants

Takoradi GTA• upon termination, N-Gas owes

'WAPCo Termination Payment' to WAPCo

GovernmentConsent & SupportAgreement• guarantee of VRA's obligations

under:• Takoradi GSA• VRA Direct AgreementVRA Direct

Agreement• upon termination, N-Gas directs

VRA to pay 'WAPCo Termination Payment' directly to WAPCo instead of to N-Gas

Case study: West Africa Gas Pipeline

Project: 678 km new pipeline to transport natural gas from Nigeria to Ghana, Togo and Benin; gas sourced and transported by N-Gas (owned by Nigerian National Petroleum Corp, Chevron, Shell; Volta river Authority of Ghana (VRA) as anchor customer)

Financing: Bank’s PRG of USD 50million leveraged USD 800million of Private Equity Financing through direct equity and shareholder loans

18

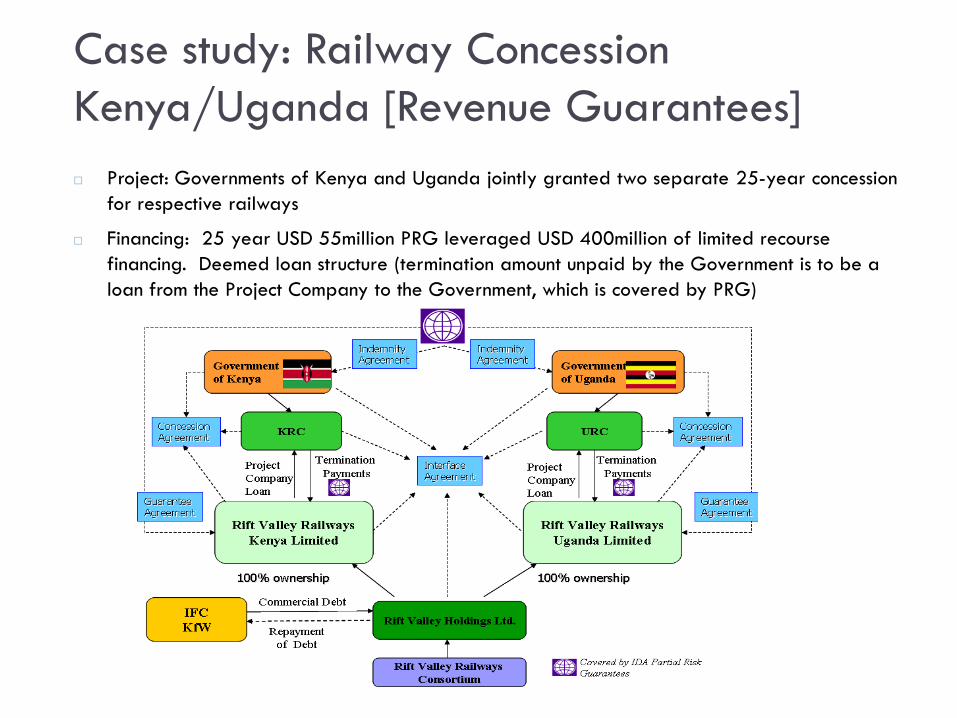

Case study: Railway Concession Kenya/Uganda [Revenue Guarantees]

19

Project: Governments of Kenya and Uganda jointly granted two separate 25-year concession for respective railways

Financing: 25 year USD 55million PRG leveraged USD 400million of limited recourse financing. Deemed loan structure (termination amount unpaid by the Government is to be a loan from the Project Company to the Government, which is covered by PRG)

Mobilizing commercial money for public sector projects: optimizing balance sheets

Issue: Public sector wants to match it’s liabilities with the life of assets by borrowing longer term Investors are hesitant in buying public securities for longer term, primarily due to lack of

established track record of payment which goes beyond the medium term, e.g. Public utility’s investment program in Thailand

Public financing of 3 power plants in China

Solution: Bank adapted its Partial Credit Guarantee to backstop debt repayment obligations of public sector agencies to tap international markets International (US144a, private placements and Eurobond) bond issuances

Tapping $-based syndicated loans for public sector investment projects

Potentially, IBRD structures can also help raise money to finance operating deficits

Under PCG, the Bank covered 100% credit risk of the issuing authority for a portion of financing Providing minimum coverage which gave enough comfort to the market in taking Public

Entity’s credit risk

By doing so, public entity established a track record in the market for future issuances

20

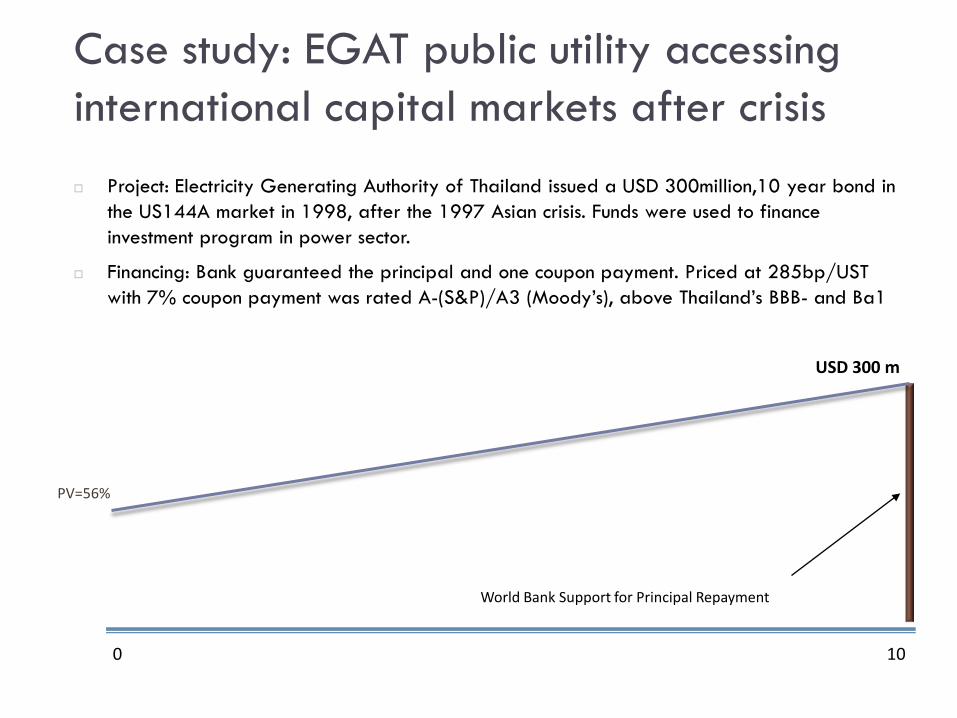

Case study: EGAT public utility accessing international capital markets after crisis

21

Project: Electricity Generating Authority of Thailand issued a USD 300million,10 year bond in the US144A market in 1998, after the 1997 Asian crisis. Funds were used to finance investment program in power sector.

Financing: Bank guaranteed the principal and one coupon payment. Priced at 285bp/UST with 7% coupon payment was rated A-(S&P)/A3 (Moody’s), above Thailand’s BBB- and Ba1

World Bank Support for Principal Repayment

PV=56%

USD 300 m

10 0

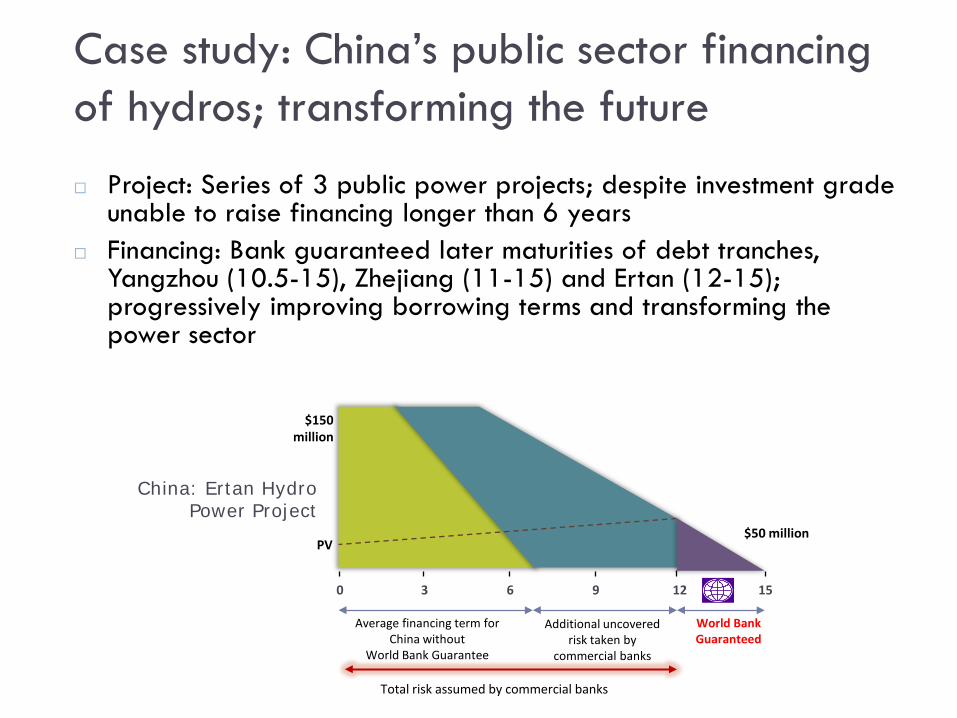

Case study: China’s public sector financing of hydros; transforming the future

22

Project: Series of 3 public power projects; despite investment grade unable to raise financing longer than 6 years

Financing: Bank guaranteed later maturities of debt tranches, Yangzhou (10.5-15), Zhejiang (11-15) and Ertan (12-15); progressively improving borrowing terms and transforming the power sector

$150 million

Average financing term for China without

World Bank Guarantee

Additional uncovered risk taken by

commercial banks

World Bank Guaranteed

Total risk assumed by commercial banks

$50 million

0 3 6 9 12 15

PV

China: Ertan Hydro Power Project

Bringing international investors to invest in public assets: Privatization Issue: Early stages of sector reform; international investors are hesitant in

buying public distribution assets, primarily due to tariffs not being adjusted towards cost-recovery in a timely manner, e.g. Power distribution in Albania - PRG Power distribution in Romania - PRG Power distribution in Uganda – IDA credit structured to provide risk mitigation

Solution: Bank adapted the PRG and/or the Bank Loan to specifically to

support privatization by backstopping regulatory risk Letter of Credit structure

Limited risks covered under PRG include: Non compliance by the Regulator and change or repeal by governments of

pre-agreed framework, e.g. regarding distribution tariff formula, Retail Public Supply tariff formula and Compensation Mechanisms

Timely approval of tariffs

23

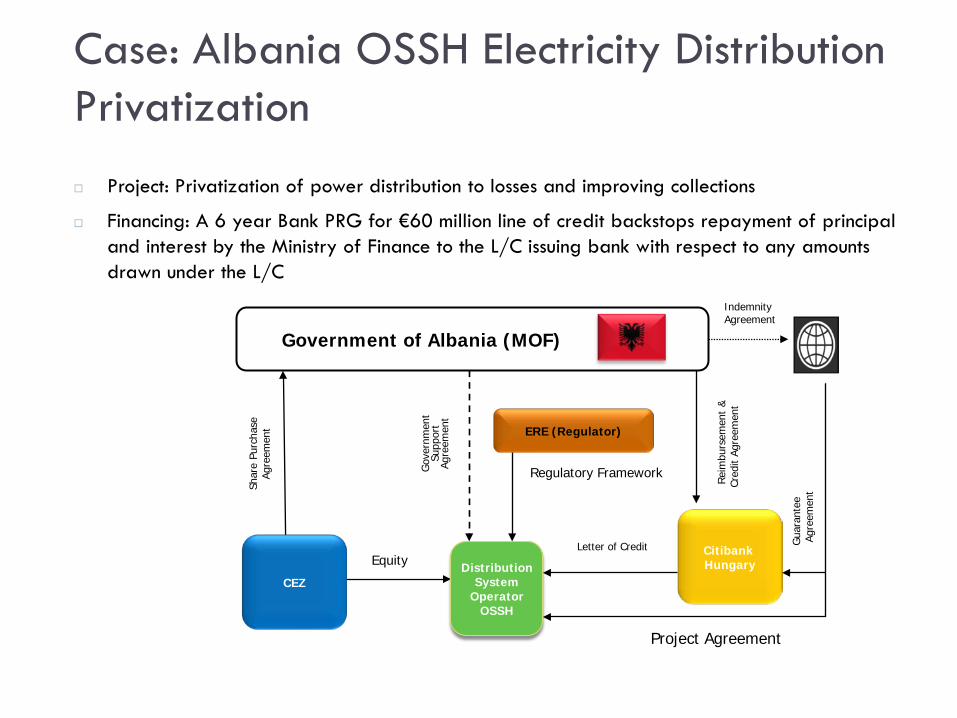

Case: Albania OSSH Electricity Distribution Privatization Project: Privatization of power distribution to losses and improving collections

Financing: A 6 year Bank PRG for €60 million line of credit backstops repayment of principal and interest by the Ministry of Finance to the L/C issuing bank with respect to any amounts drawn under the L/C

Equity

Indemnity Agreement

Regulatory Framework Gov

ernm

ent

Supp

ort

Agre

emen

t

Project Agreement

Gua

rant

ee

Agr

eem

ent

Letter of Credit

Shar

e Pu

rcha

se

Agre

emen

t

Rei

mbu

rsem

ent

&

Cred

it Ag

reem

ent

Government of Albania (MOF)

CEZ Distribution

System Operator

OSSH

Citibank Hungary

ERE (Regulator)

24

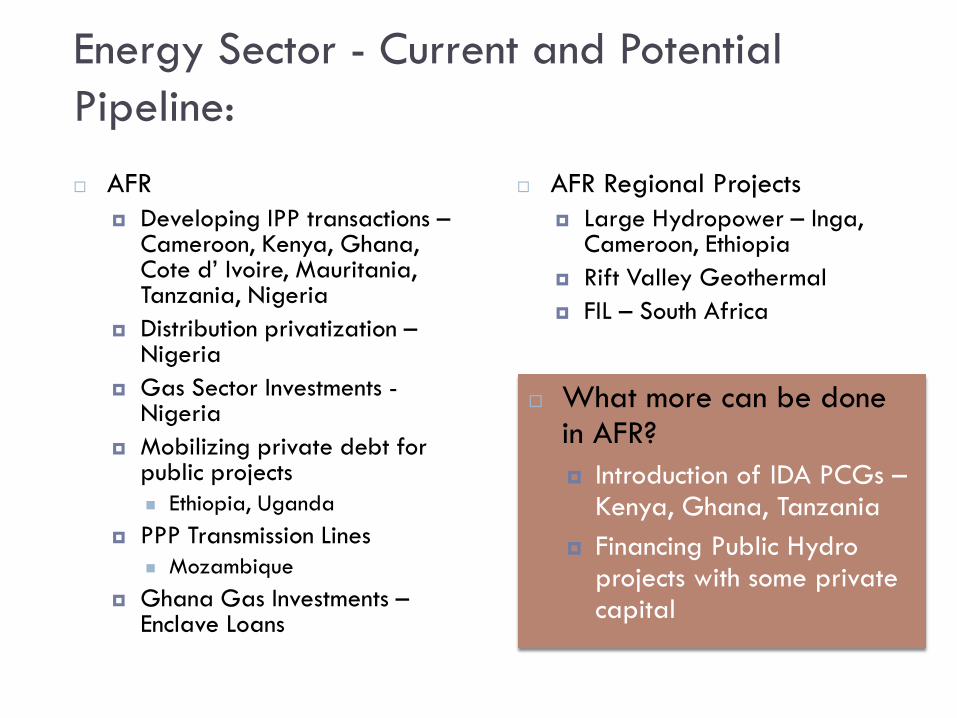

Energy Sector - Current and Potential Pipeline: AFR

Developing IPP transactions – Cameroon, Kenya, Ghana, Cote d’ Ivoire, Mauritania, Tanzania, Nigeria

Distribution privatization – Nigeria

Gas Sector Investments - Nigeria

Mobilizing private debt for public projects Ethiopia, Uganda

PPP Transmission Lines Mozambique

Ghana Gas Investments – Enclave Loans

AFR Regional Projects Large Hydropower – Inga,

Cameroon, Ethiopia Rift Valley Geothermal FIL – South Africa

25

What more can be done in AFR? Introduction of IDA PCGs –

Kenya, Ghana, Tanzania Financing Public Hydro

projects with some private capital

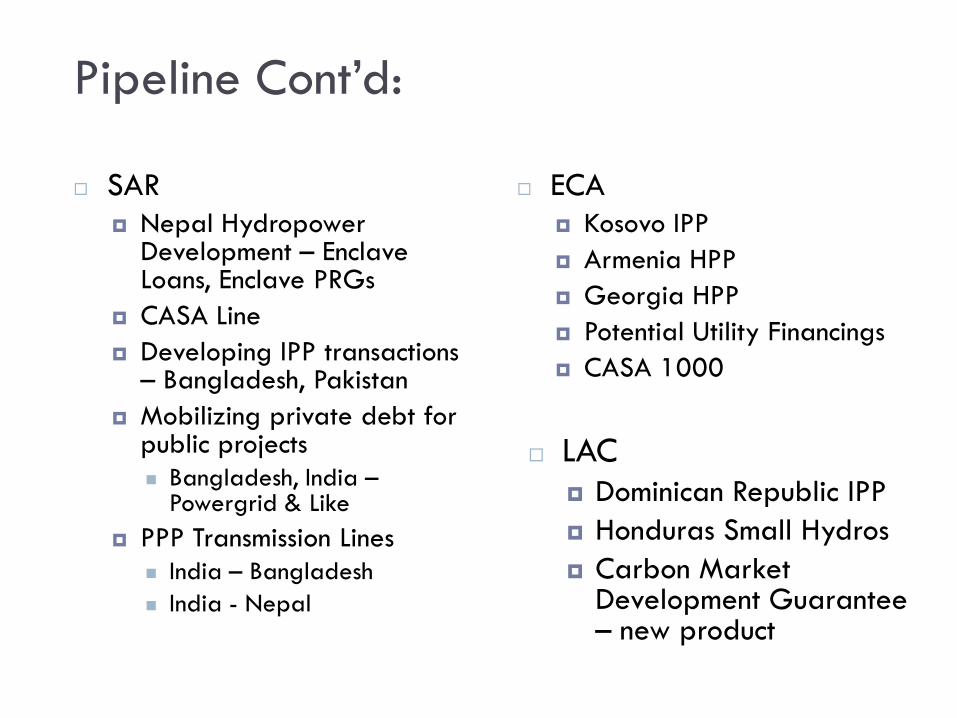

Pipeline Cont’d:

SAR Nepal Hydropower

Development – Enclave Loans, Enclave PRGs

CASA Line Developing IPP transactions

– Bangladesh, Pakistan Mobilizing private debt for

public projects Bangladesh, India –

Powergrid & Like PPP Transmission Lines

India – Bangladesh India - Nepal

ECA Kosovo IPP Armenia HPP Georgia HPP Potential Utility Financings CASA 1000

26

LAC Dominican Republic IPP Honduras Small Hydros Carbon Market

Development Guarantee – new product

Pipeline Cont’d (2):

EAP Laos Hydropower

Development – Enclave Loans, Enclave PRGs

PNG – HPP (domestic) PNG – HPP (export) Solomon Islands (Tina

Hydro) Indonesia – debt fund &

guarantee fund

MNA Egypt – gas and wind IPPs Jordan – Gas IPPs x 2 Jordan – Wind Egypt – Wind Morocco – Solar IPP

27

What more can be done by Debt Mkts? Financing Sector Deficits Financing Public Sector

Project through private loans

GUARANTEE STRUCTURES SDN Anchor, World Bank

28

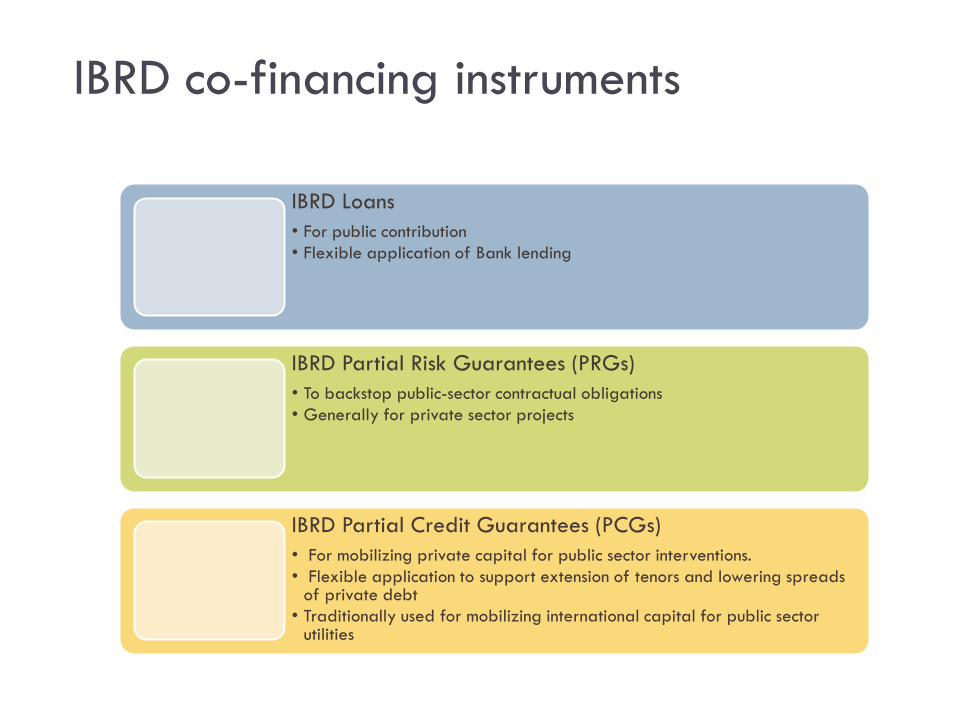

IBRD co-financing instruments 29

IBRD Loans • For public contribution • Flexible application of Bank lending

IBRD Partial Risk Guarantees (PRGs) • To backstop public-sector contractual obligations • Generally for private sector projects

IBRD Partial Credit Guarantees (PCGs) • For mobilizing private capital for public sector interventions. • Flexible application to support extension of tenors and lowering spreads

of private debt • Traditionally used for mobilizing international capital for public sector

utilities

Partial Risk Guarantee Structures

Lenders’ Guarantees

Government

Project Company (SPV)

Commercial Bank

Indemnity

Guarantee Project

Contract/ Obligation

Project Loan

Government World Bank

Project Company

(SPV) Commercial

Bank Private

Investors

Guarantee Government Obligations

Indemnity

Concession/BOT / Support Agreement etc.

Equity Project Loan

World Bank

30

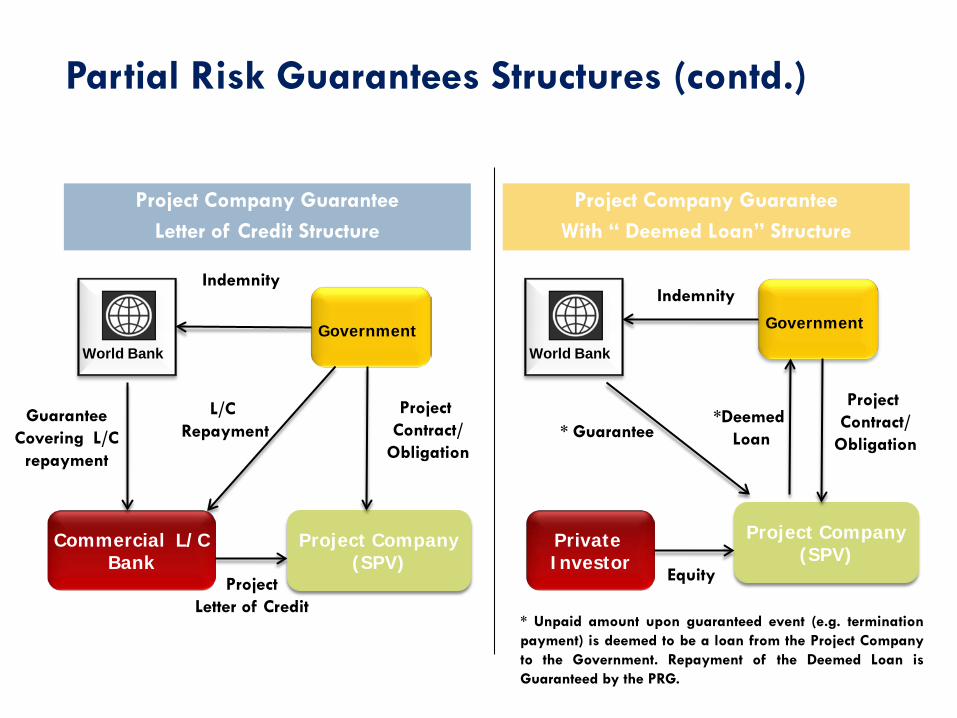

Partial Risk Guarantees Structures (contd.)

Project Company Guarantee Letter of Credit Structure

Project Company Guarantee With “ Deemed Loan” Structure

World Bank Government

Project Company (SPV)

Commercial L/C Bank

Project Letter of Credit

Indemnity

Guarantee Covering L/C

repayment

Project Contract/

Obligation

L/C Repayment

Government

Project Company (SPV)

* Guarantee

Indemnity

Project Contract/

Obligation

World Bank

* Unpaid amount upon guaranteed event (e.g. termination payment) is deemed to be a loan from the Project Company to the Government. Repayment of the Deemed Loan is Guaranteed by the PRG.

Private Investor

Equity

*Deemed Loan

31

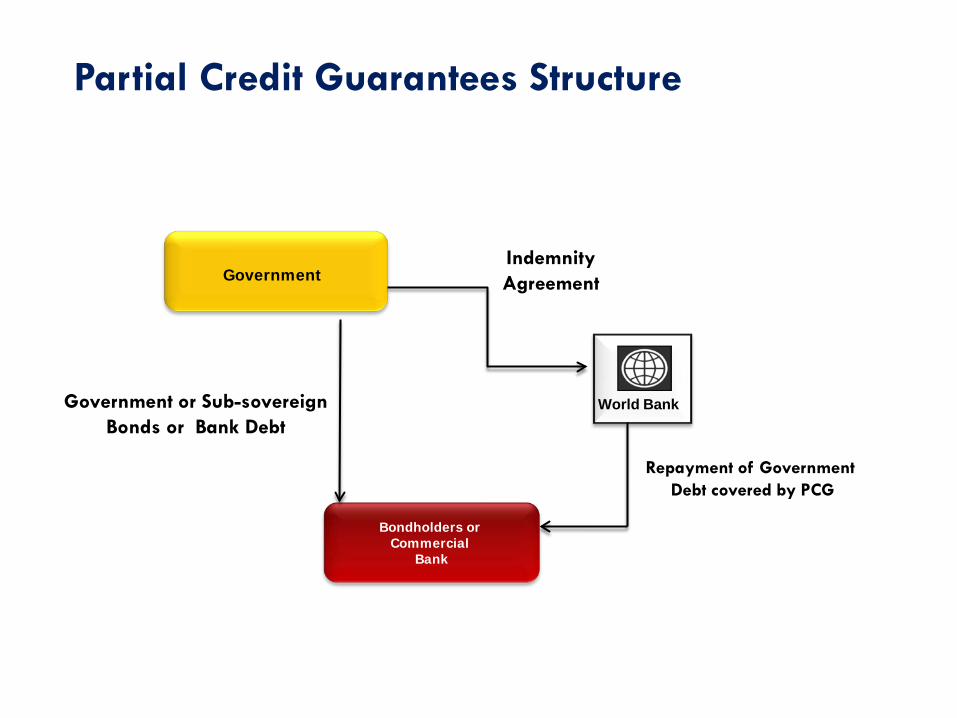

Partial Credit Guarantees Structure

Government

World Bank

Bondholders or Commercial

Bank

Repayment of Government Debt covered by PCG

Indemnity Agreement

Government or Sub-sovereign Bonds or Bank Debt

32